GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 411 CONTRACTs NOTICES FOR 41,100 OZ or 1.278 TONNES

total notices so far: 30,122 contracts for 3,012,200 OR 93.692 tonnes)

SILVER NOTICES:0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1720 CONTRACTS (NOTICES) for 8.600 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 27.445 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 50,000 OZ QUEUE JUMP//NEW STANDING ADVANCES AT 8.790 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE MONTH’S QUEUE JUMP OF 40.376 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK //NEW STANDING ADVANCES TO 97.90 TONNES OF GOLD (INCLUDES ALL MONTHLY QUEUE JUMPS) +10.4932 TONNES EX.FOR RISK = 111.4142 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 118.363 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A FAIR 245 CONTRACTS OI TO 158,528 AND FURTHER FROMTHE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 220 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 220 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 245 CONTRACTS AND ADD TO THE 220 E.FP. ISSUED

WE OBTAIN A TINY SIZED LOSS OF 25 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.64 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 0.125 MILLION PAPER OZ

OCCURRED DESPITE OUR $0.64 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 38.92 PTS OR 1.02%

//Hang Seng CLOSED UP 68.29 PTS OR 0.27%

// Nikkei CLOSED DOWN 657.74 PTS OR 1.51% //Australia’s all ordinaries CLOSED UP 0.04%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1793OFFSHORE CLOSED UP AT 7.1828/ Oil DOWN TO 62.80 dollars per barrel for WTI and BRENT UP TO 66.41 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1793 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1928 AGAINST US DOLLAR/ AND THUS STRONGER

SHANGHAI CLOSED DOWN 0.74 PTS OR 0.02%

//Hang Seng CLOSED DOWN 53.95 PTS OR 0.21%

// Nikkei CLOSED DOWN 168.02 PTS OR 0.38% //Australia’s all ordinaries CLOSED DOWN 0.76%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1821 OFFSHORE CLOSED DOWN AT 7.1855/ Oil DOWN TO 62.90 dollars per barrel for WTI and BRENT DOWN TO 65.90 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1821 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1855 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1352 CONTRACTS TO 438,541 OI WITH OUR LOSS IN PRICE OF $16.90 WITH RESPECT TO TUESDAY’S // TRADING.. WE LOST NO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2978). WE HAD CONSIDERABLE T.A.S. LIQUIDATION //TUESDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1626 CONTRACTS (OR 5.057 TONNES). WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FRIDAY. THE CROOKS COULD NOT FLEECE ANY OF OUR NET LONGS AS THE COMEX LEVEL OI WAS EXTREMELY LOW AND THUS VERY VERY STICKY: AND AS SUCH THE OI ROSE A BIT DESPITE OUR LOSS IN PRICE.

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AS MENTIONED ABOVE: TONIGHT WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FOR AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER TONIGHT, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

THUS THE TOTAL FOR AUGUST IS 3374 CONTRACTS OR 337,400OZ OR 10.4932 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES) IT SEEMS NOW THAT THE BANK OF ENGLAND IS IN QUITE A HURRY TO GET ITS GOLD BACK!! (AND PROBABLE OWNER OF THOSE EXCHANGE FOR RISK CONTRACTS)

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 3 ISSUANCES FOR A MONSTER 3374 CONTRACTS OR 337,400 OZ ( 10.4932 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1626 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 860 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED THREE WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 40.376 TONNES +10.4932 TONNES EX FOR RISK (3 ISSUANCES) //NEW STANDING 111.4142 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 236 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE 40.376 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES AND THEN AUGUST 12: 2.637 TONNES:/NEW STANDING ADVANCES TO 111.4192 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2978 EFP CONTRACT WAS ISSUED: : /DEC 1447 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2978 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- HUGE LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY

- MONTH END SPREADERS WILL APPEAR ON THE LAST WEEK OF AUGUST.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A SMALL SIZED SIZED 697 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING SMALL LOSS OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S FIRST THREE ISSUANCES OF EXCHANGE FOR RISK FOR 10.4932 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 3.023TONNES TO WHICH WE ADD THURSDAY’S AUG 7 HUGE 5.4432 EXCHANGE FOR RISK, SATURDAY’S//MONDAY AUG 10 STRONG 776 CONTRACT ISSUANCE (77600 OZ) FOR 2.413 TONNES AND THEN WEDNESDAY.S AUGUST 12 FOR 2.637 TONNES/// TOTAL EX FOR RISK AUGUST = 10.4932 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

100.923 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

EQUALS

111.4142 TONNES TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A $16.90/ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH YESTERDAY;S TRADING/RAID!.

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: THREE SO FAR, AUGUST 7 THROUGH AUG 12 AT 3374 CONTRACTS FOR 337,400 OZ (10.4932 TONNES OF GOLD) TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 10.4932 TONNES

THUS 100.923 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 10.4932 TONNES = 111.4142 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE A FAIR SIZED GAIN TOTAL OF 5.057 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD LAST AUG 8 RECORD BREAKING QUEUE JUMP OF 10.8775 TONNES OF GOLD ON TOP OF AUG 12 1.7604 TONNES QUEUE JUMP AND THEN WEDNESDAY;S AUG 13 MASSIVE QUEUE JUMP OF 3.527 TONNES AND THEN THURSDAY AUG 14 HUGE 2.463 TONNES QUEUE JUMP AND FRIDAY;S AUG 15 QUEUE JUMP OF .7030 TONNES AND THEN SATURDAY’S 1.617 TONNE QUEUE JUMP AND THEN YESTERAY’S AUG 19: 1.058 QUEUE JUMP TO WHICH WE ADD TODAY’S MASSIVE QUEUE JUMP OF 3.023 TONNES TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK/PRIOR FOR 10.4932 TONNES FOR RISK//NEW STANDING ADVANCES TO 111.4142 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.05

WE HAD XXX CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 1626 CONTRACTS OR 162,600 0Z (5.057 TONNES)

confirmed volume TUESDAY 148,394 contracts// extremely poor//everybody vacating the comex???

speculators have left the gold arena

END

INITIAL GOLD COMEX

END

INITIAL GOLD COMEX

AUGUST CONTRACT MONTH

AUGUST 20 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entries i) Out of Asahi: 65,318.611 oZ total withdrawal: 65,318.611 oz . |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 411 notice(s) 41100 OZ 1.278 TONNES |

| No of oz to be served (notices) | 2019 contracts 2019 OZ 6.279 TONNES |

| Total monthly oz gold served (contracts) so far this month | 30,122 notices 2,971,100 oz 93.692 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entries

i) Out of Asahi: 65,318.611 oZ

total withdrawal: 65,318.611 oz

adjustments: 2

a) out of Brinks 385.812 oz/ dealer account to customer account

b) Asahia: 9352.03 oz//dealer to customer acocunt

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 2325 CONTRACTS FOR A GAIN OF 561CONTRACTS

WE HAD 411 CONTRACTS SERVED ON TUESDAY SO WE GAINED A HUGE SIZED 972 CONTRACTS OR 97200 OZ OF GOLD (3.023 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT GAINED 84 CONTRACTS TO 4794

OCTOBER LOST 438 CONTRACTS UP TO 61,101

We had 411 contracts filed for today representing 41,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 411 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 148 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (30,122 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 2325 CONTRACTS) minus the number of notices served upon today (411 x 100 oz per contract) equals 3,247,700 OZ OR 100.923 TONNES TO WHICH WE ADD OUR THREE ISSUANCES OF 10.4932 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 AND 12TH = 111.4142 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (30,122 x 100 oz +we add the difference for front month of AUGUST (2325 OI} minus the number of notices served upon today (411 x 100 oz) which equals 3,247,700 OZ OR 100.923 TONNES + 10.4932 TONNES EX FOR RISK = 111.4142 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 111.412TONNES WHICH IS HUGE FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. AND THIS RNS COUNTER INTUATIVE TO OUR CONSTANT RAIDS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,030,244.382 oz 63.14 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,563,812.006 oz

TOTAL REGISTERED GOLD 21,289,509.823 or 662.19 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,274,302.183 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,259,256 oz ((REG GOLD- PLEDGED GOLD)= 599.04 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACT//INITIAL

AUGUST 20 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries: |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 DEPOSIT ENTRY/CUSTOMER ACCOUNT i)Into CNT: 347,707.050 oz total deposit: 347,707.050 oz |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ |

| No of oz to be served (notices) | 38 contracts (0.190 MILLION oz) |

| Total monthly oz silver served (contracts) | 1720 Contracts (8.60 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

0 DEPOSIT ENTRY/CUSTOMER ACCOUNT

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i)Into CNT: 347,707.050 oz

total deposit: 347,707.050 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

0 entry:

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.400 MILLION OZ//.TOTAL REG + ELIGIBLE. 508.519 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 38 OPEN INTEREST CONTRACTS FOR A GAIN OF 10 CONTRACTS. WE HAD 0 CONTRACTS SERVED ON TUESDAY SO WE GAINED 10 CONTRACTS OR AN ADDITIONAL 50,000 OZ WILL STAND AT THE COMEX HAVING UNDERGONE A HUGE QUEUE JUMP

SEPTEMBER LOST 2217 CONTRACTS DOWN TO 62,636 CONTRACTS.

OCTOBER LOST 186 CONTRACTS TO 1015

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or NIL oz

CONFIRMED volume; ON TUESDAY 66,142 good//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1720 X5,000 oz = 8.600 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (38) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1720) Notices served so far) x 5000 oz + OI for the front month of AUGUST(38) minus number of notices served upon today (0)x 5000 oz equals silver standing for the AUGUST contract month equating to 8.790 MILLION OZ .

New total standing: 8.790 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.400 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/508.151 million. 41.33%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES37

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 962.21 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 493.181 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

3,000,000 million oz = 93 3 tonnes. It is now higher by 8 tonnes to 101 tonnes.

3M Gold Ounces Drained as U.S. Gold Imports Surge

![]()

by ITM Trading

Tuesday, Aug 19, 2025 – 14:17

It’s happening quietly, but the numbers don’t lie. August is on track to break records with over 3 million ounces of gold requested for delivery—on a market that was never designed for physical settlement. Meanwhile, U.S. gold imports have surged 17x.

This isn’t panic buying. It’s calculated. Coordinated. Institutional. And possibly sovereign.

The Fed’s recent whisper of a gold revaluation to manage U.S. debt only adds fuel to the speculation. Something big is shifting in the monetary landscape—and those with the most to lose are moving first.

The rest of us? We’d better be paying attention.

Follow Taylor Kenney on X

Free Report: How physical gold and silver outlasted the world’s worst currency collapses—proof that real money endures when fiat fails. Download it FREE

About ITM Trading: ITM Trading has spent nearly 30 years helping clients prepare for monetary resets, inflation, and systemic risk using physical gold and silver. We focus on education, historical context, and strategies designed to protect wealth when trust in the system breaks down.

END

GOLD TRADING!@!

Gold Ready to Explode? Fear Says Yes, Cheap Volatility Is the Trade

Wednesday, Aug 20, 2025 – 16:21

Ever time for gold?

Gold continues to trade inside the boring range that has been in place for months. Note we are down to the 100 day moving average. Last time we bounced off the 100 day, things took off…

Source: LSEG Workspace

Dirt cheap

Gold volatility is starting to screen as a bargain. Playing direction via options is very attractive given where volatility trades… and don’t forget that gold trades with an upside volatility skew, i.e gold up sharply usually means volatility picks up.

Source: LSEG Workspace

The fear factor

Gold likes fear… and tech fear has exploded higher over the past 2 sessions.

Source: LSEG Workspace

Lagging

Gold continues to lag little brother, silver. Chart 2 shows 3 months chart in %.

Source: LSEG Workspace

Source: LSEG Workspace

Far from big longs

Gold net non commercials have room to buy much more gold…

Source: LSEG Workspace

The dollar connection

Gold vs. DXY connection stays very strong.

Source: LSEG Workspace

Miners showing the way?

GDX momentum going to spill over to gold?

Source: LSEG Workspace

1/ PETER SCHIFF/S

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 236

5. COMMODITY REPORT.

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 38.92 PTS OR 1.02%

//Hang Seng CLOSED UP 68.29 PTS OR 0.27%

// Nikkei CLOSED DOWN 657.74 PTS OR 1.51% //Australia’s all ordinaries CLOSED UP 0.04%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1793OFFSHORE CLOSED UP AT 7.1828/ Oil DOWN TO 62.80 dollars per barrel for WTI and BRENT UP TO 66.41 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1793 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1928 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1793 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1828

HANG SENG CLOSED UP 68.29 PTS OR 0.27%

2. Nikkei closed DOWN 657.24PTS OR 1.51%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 98.14 EURO RISES TO 1.1645 UP 4 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.611//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.44…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7424Italian 10 Yr bond yield DOWN to 3.580 SPAIN 10 YR BOND YIELD DOWN TO 3.316

3i Greek 10 year bond yield DOWNTO 3.424

3j Gold at $325.00 Silver at: 37.16 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 51 /100 roubles/dollar; ROUBLE AT 80.26

3m oil (WTI) into the 62 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.44/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.611% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8026 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9408 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.362UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.910 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.758 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.91

10 YR UK BOND YIELD: 4.7330 DOWN 1 PTS

10 YR CANADA BOND YIELD: 3.455UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.973 UP 1 PTS

2a New York OPENING REPORT

Futures Drop For 4th Day As Momentum Unwind Continues

Wednesday, Aug 20, 2025 – 08:30 AM

US equity futures are down and headed for a 4th day of losses, but trade well off session lows as markets assess if the sharp momentum selloff we have discussed for the past week will extend into today’s session: the JPM Momentum Basket (JPMPURE Index) is down more than 7% since the CPI print while Goldman said it’s time to resume buying momentum factor. As of 8:00am S&P futures are down 0.2%, after dipping 0.5% earlier in the session; Nasdaq futures are also down 0.2% after the index logged its second-biggest decline since April on Tuesday, with Mag7 names lower premarket ex-NVDA/MSFT; Defensives are outperforming Cyclicals. According to JPM “today feels like a test for the dip-buyers, as Flash PMIs tomorrow and Powell at Jackson Hole on Friday may prove to be market movers/narrative changers.” The yield curve is twisting flatter with the USD not flat. Commodities are seeing a bid across all 3 complexes highlighted by WTI. The macro data today is mortgage applications and Fed Minutes with tomorrow delivering Flash PMIs, jobless data, leading index, and existing home sales.

In premarket trading, Mag 7 stocks are mostly lower (Nvidia +0.05%, Microsoft +0.1%, Tesla -0.3%, Alphabet -0.5%, Meta -0.4%, Amazon -0.4%, Apple -0.5%). Target plunged 10% after saying management still sees a sales decline of low-single digit percentage. The company also named veteran Michael Fiddelke as its next chief executive officer, betting that the insider will rejuvenate sales and help the storied retailer regain its footing. Here are the other notable premarket movers>

- Analog Devices (ADI) rises 3% after the semiconductor-device company reported adjusted earnings per share for the third quarter that beat the average analyst estimate.

- Celldex Therapeutics (CLDX) falls 18% after the drug developer said it was discontinuing development of barzolvolimab in eosinophilic esophagitis after a Phase 2 study.

- Custom Truck One Source (CTOS) declines 4% after being downgraded at JPMorgan to underweight from neutral, on expectations that vocational truck sales will soften over the coming quarters due to weak orders data.

- Dayforce (DAY) rises 2% after the software firm said it’s in advanced discussions with Thoma Bravo regarding a potential acquisition for $70 per share.

- Estee Lauder (EL) falls 7% after issuing an annual adjusted EPS forecast that trails expectations. The organic sales decline for 4Q was slightly worse than expected, driven by Skin Care and Makeup segments.

- Hertz (HTZ) rises 10% after CNBC reported that the car-rental company will start selling pre-owned cars on Amazon Autos. Shares of Carvana (CVNA) decline 5%, while CarMax (KMX) drops 4%.

- La-Z-Boy (LZB) falls 22% after the home furniture retailer posted weaker-than-expected first-quarter adjusted earnings per share.

- Lowe’s Cos. (LOW) rises 3% after agreeing to buy Foundation Building Materials for about $8.8 billion in cash as it expands further beyond home-improvement supplies to serve more professional customers.

- Novavax (NVAX) drops 7% after BofA Global Research downgraded the vaccine maker to underperform from neutral, citing a “bumpy road” ahead.

- Nubank (NU) rises 2% as Citi double upgrades to buy from sell, with analysts saying the bank is now able to accelerate in key portfolios while maintaining good asset quality.

- Rocket Pharmaceuticals (RCKT) falls 18% after announcing that the FDA lifted the clinical hold on the Phase 2 trial of RP-A501 for the treatment of Danon disease.

- Toll Brothers (TOL) is down 2% after the luxury builder’s quarterly orders missed estimates as affordability challenges and economic uncertainty held back buyers.

Investors pared back positions in tech amid growing concern that the S&P 500’s recent record-breaking rally has run too far, too fast and has leaned heavily on a few growth leaders. That momentum will get a further test this week as focus turns to Jackson Hole, Wyoming, where Fed Chair Jerome Powell is set to speak on Friday with traders betting on a September cut in interest rates.

“This was a textbook case of profit-taking after a powerful tech rally,” wrote Bjarne Breinholt Thomsen, head of cross-asset strategy at Danske Bank A/S. “Yesterday’s move does not alter our tactical stance. On fundamentals alone, we would likely overweight tech. But when factoring in stretched positioning and valuations, we remain neutral.”

Investors are also waiting to hear whether Powell will validate current market expectations or counter them by stressing that fresh economic data arriving before the next policy meeting could alter the outlook. They’re also scanning for hints about how the Fed foresees the pace of rate cuts extending into next year.

“If we get an indication that they are more inclined to cutting interest rates, that will be more supportive again,” HSBC Head of APAC Equity Strategy Herald van der Linde said in a Bloomberg TV interview.

Europe’s Stoxx 600 is slightly higher after erasing an earlier drop, and edges closer toward a new high after erasing losses. Personal care stocks outperform, while industrials and construction shares are the biggest laggards. European tech stocks also decline. In the UK, money markets kept wagers on Bank of England interest-rate cuts broadly steady, seeing around a 40% chance of another reduction by year-end after inflation climbed for a second month in July. A full quarter-point cut had been expected earlier this month. Gilts rose, with the two-year yield falling four basis points at 3.93%. The pound fluctuated. Here are the biggest movers Wednesday:

- Emmi gains 6.4%, the most since 2024, after the Swiss dairy producer published solid results in a challenging environment, with a beat on organic growth driven entirely by the Americas segment, according to Vontobel

- Convatec shares rise as much as 6%, the most in two months, after the medical equipment manufacturer announced the start of a buyback program, with Morgan Stanley saying the announcement signals confidence

- Sensirion rises as much as 11%, the most since April, after the semiconductor device manufacturer posted results that beat analysts’ estimates, with higher sales volumes attributed to US demand for a refrigerant sensor product

- Ithaca Energy shares jumped as much as 8.6% to the highest level since February 2023 after the UK oil and gas company boosted its production forecast for the full year

- ASR Nederland climbs as much as 2.5% to a record high after the Dutch insurance company released first-half results. Morgan Stanley said it was another strong print, while KBC highlighted the good performance in the Life unit

- NEPI Rockcastle rallied as much as 3% in Johannesburg to its highest intraday level since Feb. 24 after the property investor posted Ebit for the first half that increased 10% year-on-year

- Paradox Interactive gains as much as 4.7% after the Swedish video game company announced release dates for two highly anticipated game releases, Europa Universalis V and Vampire: The Masquerade – Bloodlines 2

- Alcon drops as much as 11% in Zurich, the most since March 2020, after delivering sales growth below expectations in the second quarter and announcing downward revisions to its full-year net sales guidance

- K+S falls as much as 3.3% as Berenberg double-downgrades to sell, with previous buy thesis no longer standing up due to expectations of “broadly lower” prices for agricultural commodities from 2026

- Geberit falls as much as 4.3%, the most in more than four months, after the Swiss building materials firm reported a lower-than-expected Ebitda in the second quarter

- European defense stocks remain under pressure this morning after Russian President Vladimir Putin “agreed to begin the next phase of the peace process,” according to White House Press Secretary Karoline Leavitt

- UK housebuilder shares drop after inflation climbed for a second month in July, adding pressure on the Bank of England to reconsider its pace of interest-rate cuts

- LINK Mobility falls as much as 9.4%, the most since November last year and trimming large YTD gains, after the Norwegian communications technology group reported its latest earnings. DNB Carnegie sees a “minor miss”

- EVS Broadcast Equipment drops as much as 13%, the most since March 2020, as ING Bank describes the company’s first-half results as “very weak”

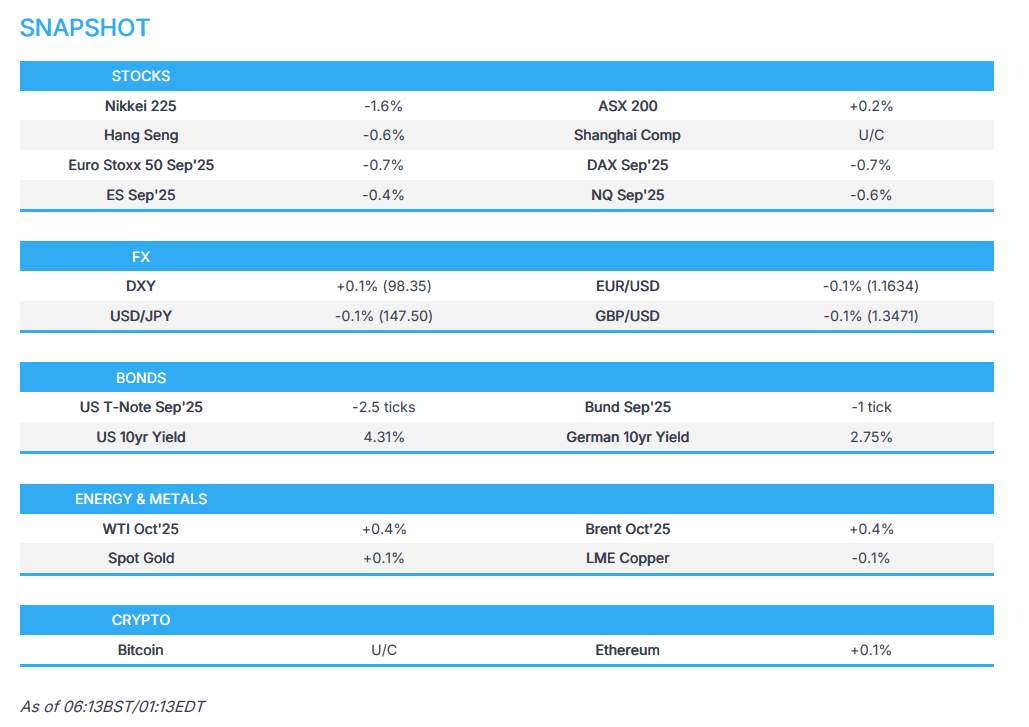

Earlier in the session, Asian stocks fell, as technology shares tracked declines in US peers amid valuation concerns ahead of upcoming key events. The MSCI Asia Pacific Index dropped 0.7%, falling for the third consecutive session, with TSMC and Softbank among the biggest drags. Taiwan led declines, with South Korea and Japan also notably in the red. Risk-off mood has gripped markets ahead of the Jackson Hole symposium, with Federal Reserve Chair Jerome Powell expected to speak on Friday. Investors also await Nvidia’s earnings next week for indications on the health of the artificial intelligence boom that has driven gains in global tech shares. Meanwhile, New Zealand stocks climbed after the nation’s central bank lowered its benchmark interest rate by 25 basis points. Indonesian stocks gained as the central bank surprised markets by cutting its benchmark rate for a second straight month and signaling more easing was on the table. Shares in India, Australia and China rose.

In FX, the Bloomberg dollar index is flat; the pound adds 0.1% on modest CPI support. The kiwi lags, down more than 1% after the RBNZ cut rates and flagged further easing. The krona is little changed after the Riksbank held policy as expected.

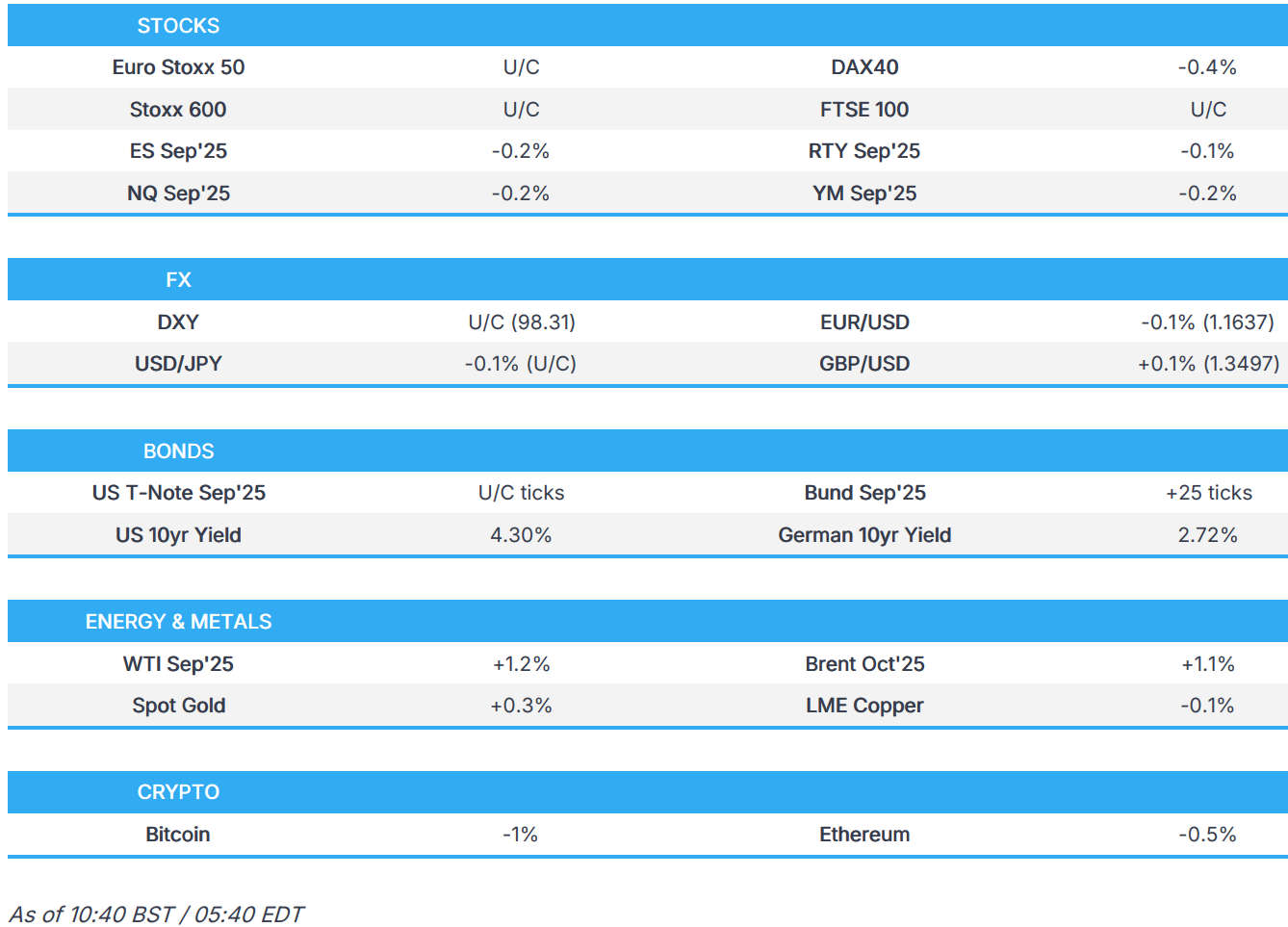

In rates, treasuries are steady, with 10-year yields flat at 4.30%. Gilts lead a rally in European bonds even as UK inflation topped forecasts, sending 10-year yields 4 bps lower to 4.70%.

In commodities, Brent crude rose more than 1% to around $66.60 a barrel while spot gold climbs $10.

Today’s US economic data calendar features FOMC minutes; the Fed speaker slate includes Governor Waller on payments at blockchain symposium at 11am and Atlanta Fed President Bostic at 3pm.

Market Snapshot

- S&P 500 mini -0.1%

- Nasdaq 100 mini -0.2%

- Russell 2000 mini little changed

- Stoxx Europe 600 little changed

- DAX -0.3%

- CAC 40 little changed

- 10-year Treasury yield little changed at 4.3%

- VIX +0.4 points at 15.94

- Bloomberg Dollar Index little changed at 1207.67

- euro little changed at $1.1637

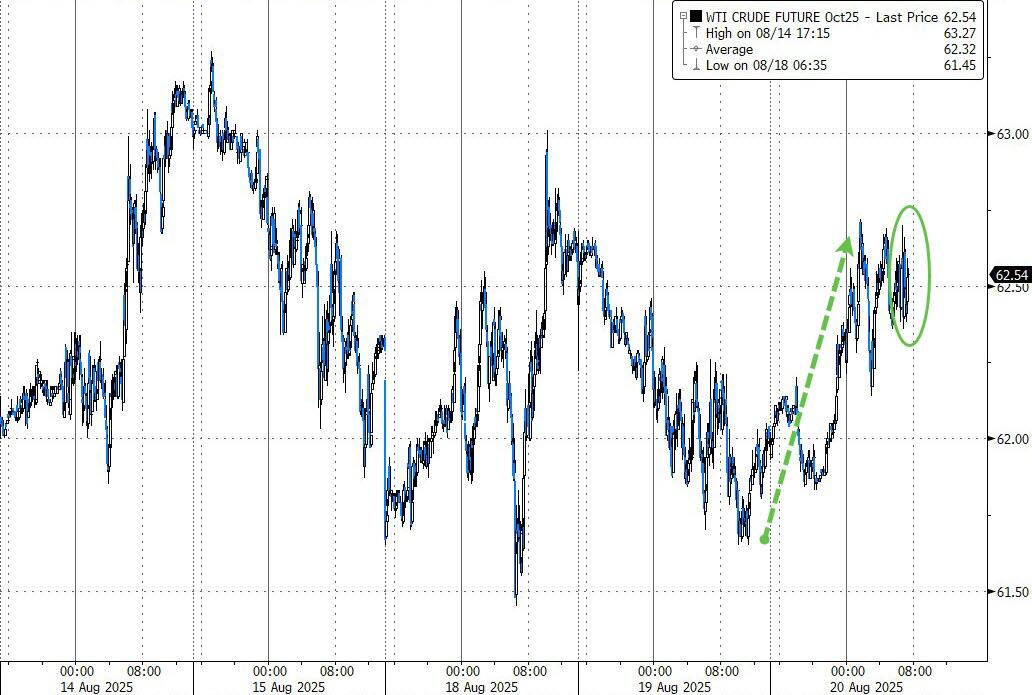

- WTI crude +1% at $63/barrel

Top Overnight News

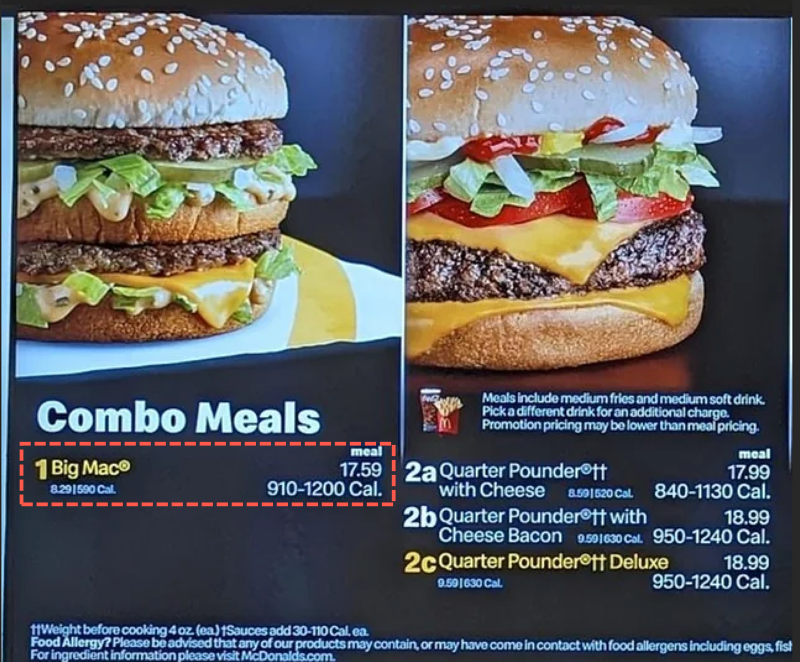

- McDonald’s is lowering the cost of its combo meals, after consumers were left sticker-shocked by Big Mac meals that climbed to $18 in some places: WSJ

- Trump posted “Could somebody please inform Jerome “Too Late” Powell that he is hurting the Housing Industry, very badly? People can’t get a Mortgage because of him. There is no Inflation, and every sign is pointing to a major Rate Cut. “Too Late” is a disaster!”

- Secretary Bessent is reportedly betting the crypto industry will become a crucial buyer of Treasuries in the coming years as Washington seeks to shore up demand for a deluge of new US government debt: FT.

- US is looking into taking equity stakes in chip makers in exchange for CHIPS Act funding, similar to the Intel plan: RTRS

- Estée Lauder Cos. issued a weak profit outlook for its fiscal year, dragged down in part by tariff costs.

- Xiaomi Corp. intends to sell its first electric vehicle in Europe by 2027, declaring plans to take on Tesla Inc. and BYD Co. globally after gaining traction with its year-old Chinese EV business.

- Novo Nordisk A/S implemented a global hiring freeze as the Danish drugmaker seeks to cut costs and regain its footing in the competitive market for weight-loss treatments.

- Baidu Inc.’s revenue fell, hurt by an economic downturn that’s capping its ability to fight bigger rivals in AI and make inroads in new growth areas.

- Temasek Holdings Pte is mulling one of its biggest overhauls in years, potentially reorganizing the firm into three investment vehicles in a bid to boost returns and efficiencies, according to people familiar with the matter.

- Shares of Chinese pop toy maker Pop Mart International Group Ltd. rose to a record after founder and Chief Executive Officer Wang Ning said the company could easily surpass its annual sales projection and announced plans to launch a new mini Labubu.

Shipments of phones within China -9.3% Y/Y at 22.6mln handsets in June (prev. -21.8% Y/Y at 23.72mln in May), via CAICT; shipments of foreign phones incl. Apple (AAPL) iPhones within China -31.3% at 1.97mln (prev. 9.7% at 4.54mln in May).

Trade/Tariffs

- US Treasury Secretary Bessent said the US has had very good talks with China and that China is the biggest revenue line in terms of tariff income, while he added that the status quo on China is working very well.

- Mexico will propose reinstating a North American Steel Committee to improve trade ties with the US, according to Bloomberg.

- Russian Embassy in India said INR payments being accepted by all Russian businesses; open to doing all oil trade INR too.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed after a lacklustre performance stateside, where mega-cap tech led the declines amid AI-related concerns, while the region digested earnings and central bank updates including the RBNZ’s dovish rate cut. ASX 200 was led higher by outperformance in the top-weighted financials sector and with strength also seen in defensives, while participants also reflected on a slew of earnings updates. Nikkei 225 retreated beneath the 43,000 level amid continued profit taking from recent record highs and after mixed data in which Machinery Tools topped forecasts but trade data mostly disappointed and showed Japanese Exports suffered the largest decline in four years. Hang Seng and Shanghai Comp were varied as participants digested earnings releases including from Xiaomi and XPeng, while there was a lack of surprises from China’s benchmark Loan Prime Rates which were maintained at the current levels, although the PBoC continued with its firm liquidity efforts via 7-day reverse repo operations.

Top Asian News

- Chinese Foreign Minister Wang Yi said regarding a meeting with Indian PM Modi that after comprehensive and in-depth communication, China and India reached an agreement to restart dialogue mechanisms in various fields.

- India’s Foreign Ministry said India and China agreed to resume direct flight connectivity between the Chinese mainland and India at the earliest, while they agreed to the re-opening of border trade through the three designated trading points. Furthermore, they agreed to facilitate trade and investment flows between the two countries through concrete measures.

- RBNZ cut the OCR by 25bps to 3.00%, as expected, while it lowered OCR projections and stated if medium-term inflation pressures continue to ease as expected, there is scope to lower the OCR further. RBNZ stated that with spare capacity in the economy and declining domestic inflation pressure, headline inflation is expected to return to around the 2% target midpoint by mid-2026, and further data on the speed of New Zealand’s economic recovery will influence the future path of the OCR. RBNZ lowered the Official Cash Rate projection for December 2025 to 2.71% (prev. 2.92%) and to 2.59% in September 2026 (prev. 2.90%). The RBNZ Minutes revealed that the rate decision was made by a majority of 4 votes to 2 and the committee discussed three policy options: keeping the OCR on hold at 3.25%, cutting the OCR by 25bps to 3% or cutting by 50bps to 2.75%, but voted on the options of either reducing the OCR by 25bps or reducing the OCR by 50bps, while the case for lowering the OCR by 25bps was based on the upside and downside risks around the central projection being broadly balanced. Furthermore, RBNZ Governor Hawkesby said during the Q&A that the next two meetings are live but no decisions have been made, as well as stated that the OCR projection troughs at 2.5% and is consistent with further cuts, while whether they go faster or slower on cuts is up to the data.

- Baidu (9888 HK) Q2 (USD): EPS 1.90 (exp. 1.74), Revenue 4.57bln (exp. 4.60bln); AI cloud business continued to deliver robust growth.

European bourses (STOXX 600 -0.2%) are trading on the backfoot in a reversal of some of Tuesday’s upside and following on from the tech-led selling pressure seen Stateside. Stocks have been attempting to clamber higher as the morning progressed, with a few indices now holding around the unchanged mark. European sectors are overall mixed with a slightly defensive tilt given the current risk environment. Food, Beverage and Tobacco sits at the top of the leaderboard with Nestle (+1.2%) leading some of the upside, other sectors outperforming include Utilities, Telecoms and Insurance. To the downside, Basic Resource names lag.

Top European News

- ECB’s Lagarde said recent trade deals have alleviated but not eliminated uncertainty; EZ economy has proven resilient in the face of challenging global environment. Notes that projections show growth is expected to slow in Q3. ECB will factor the implications of the EU-US trade deal for the Euro area economy into the September projections, will guide decisions over the coming months. Europe should aim to deepen its trade ties with other jurisdictions outside of the US, leveraging the strengths of its export-oriented economy.

- UK Chancellor Reeves is drawing up plans to hit owners of high-value properties with capital gains tax when they sell their homes as she seeks to fill a GBP 40bln hole in the public finances, according to The Times.

- UK ONS said average UK House Prices increased 3.7% in the 12 months to June 2025 (vs 3.3% Y/Y).

- Riksbank maintains its rate at 2.00% as expected; still some probability of a further interest rate cut this year, in line with the June forecast. COMMENTARY: Developments in inflation and economic activity during the summer have deviated somewhat from the forecast in June, the Executive Board assesses that the outlook remains largely the same. Economic activity is weak. New information indicates that growth is still low. Households are still cautious with regard to their spending, and the labour market is not yet showing any clear sign of improving. Uncertainty regarding international developments also remains high, not least given US economic policy, the war in Ukraine and developments in the Middle East.

- Riksbank Governor Thedeen said it is far from certain that central bank will cut going forward, but there is a certain likelihood.

FX

- After two sessions of gains, the USD rally has paused for breath. There hasn’t been a clear driver for the upside seen at the start of the week with the macro narrative relatively unaltered heading into Powell’s Jackson Hole speech on Friday. FOMC minutes are due later today. However, they will likely be deemed as stale in some quarters given the aforementioned August jobs report hit just a few days after the meeting. Fed’s Bostic and Waller are due on today’s speaker slate. Note, the subject matter for the latter is on Blockchain payments. DXY has ventured as high as 98.44 with the next upside target coming via the 12th August peak at 98.62.

- EUR is marginally softer vs. the USD with it remaining the case that there has not been a great deal of incremental macro newsflow from the Eurozone. Remarks from ECB President Lagarde failed to engineer a move in the EUR today with the policy chief noting that recent trade deals have alleviated but not eliminated uncertainty. EUR/USD sits in close proximity to its 50DMA at 1.1644 and towards the bottom end of Tuesday’s 1.1639-93 range.

- JPY is flat vs. the USD with no material follow-through from mixed data in which Machinery Tools topped forecasts but trade data mostly disappointed and showed Japanese Exports suffered the largest decline in four years. That being said, the drop-off in exports could prompt some concern from those on the BoJ who expect a negative growth hit from the trade conflict with the US. USD/JPY currently sits towards the mid-point of yesterday’s 147.44-148.11 range.

- GBP is mildly firmer vs. the USD in the wake of hotter-than-expected UK inflation metrics, which saw headline Y/Y CPI advance to 3.8% from 3.6% (Exp. 3.7%) and services jump to 5.0% from 4.7% (Exp. 4.7%). The ONS has attributed some of this to the timing of school holidays, which has triggered a surge in airfares. However, given the outcome of the most recent BoE rate decision, which saw a higher-than-expected level of hawkish dissent, markets will likely further cement expectations that the BoE will slow down the current quarterly cadence of rate cuts. Cable has hit a 1.3509 peak but is still some way off Tuesday’s best at 1.3519.

- NZD is the standout laggard across the majors following the RBNZ rate decision, which saw the Bank cut the OCR by 25bps to 3.00%, as widely expected, while it also lowered its OCR forecasts across the projection horizon and revealed it had voted on the options of either a 25bps or 50bps cut at the meeting; 2 members backed a 50bps move.

- SEK is a touch softer vs. the EUR in the wake of the Riksbank rate decision, which saw policymakers stand pat on policy as expected. The decision to do so was predicated on the board’s balancing act in managing weak growth vs. above target inflation. That being said, the Bank still judges that there is still some probability of a further interest rate cut this year, in line with the June forecast. EUR/SEK is currently above its 200DMA at 11.1771 with upside capped by the 11.20 mark.

Fixed Income

- USTs are flat and underperforming vs peers, after trading with a slight downward bias overnight. Nothing specifically driving the underperformance, but perhaps some cooling from the upside seen in the prior session, where stocks took a beating. Some of the pressure could also be in part due to some positioning heading into a 20yr supply later. In terms of price action today, USTs were initially on the backfoot but global fixed income has caught a slight bid to trade in a 111-20 to 111-24 range. Auction aside, focus will be on commentary from the Fed’s Waller, Bostic and the reported Fed Chair candidate Zervos, who is to speak on CNBC.