099 H DEUTSCHE BANK AG 1608

118 C MACQUARIE FUTURES US 1

118 H MACQUARIE FUTURES US 11

285 C NANHUA USA-HK 19

323 C HSBC 409

363 H WELLS FARGO SECURITI 104

435 H SCOTIA CAPITAL (USA) 27

624 H BOFA SECURITIES 2400

657 H MORGAN STANLEY 200

661 C JP MORGAN SECURITIES 6 360

709 C BARCLAYS 78

737 C ADVANTAGE FUTURES 16

905 C ADM 5

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 2622 CONTRACTs NOTICES FOR 262,200 OZ or 8.1555 TONNES

total notices so far: 33,050 contracts for 3,305,000 OR 102.799 tonnes)

SILVER NOTICES:0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1720 CONTRACTS (NOTICES) for 8.600 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 29.045 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 10,000 OZ EFP JUMP TO LONDON//NEW STANDING REDUCES AT 8.780 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE MONTH’S QUEUE JUMP OF 43.639 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK //NEW STANDING ADVANCES TO 104.186 TONNES OF GOLD (INCLUDES ALL MONTHLY QUEUE JUMPS) +10.4932 TONNES EX.FOR RISK = 114.6792 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 130.963 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG 453 CONTRACTS OI TO 158,930 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 320 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 320 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 453 CONTRACTS AND ADD TO THE 350 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 803 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.41 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.45 MILLION PAPER OZ

OCCURRED WITH OUR $0.41 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

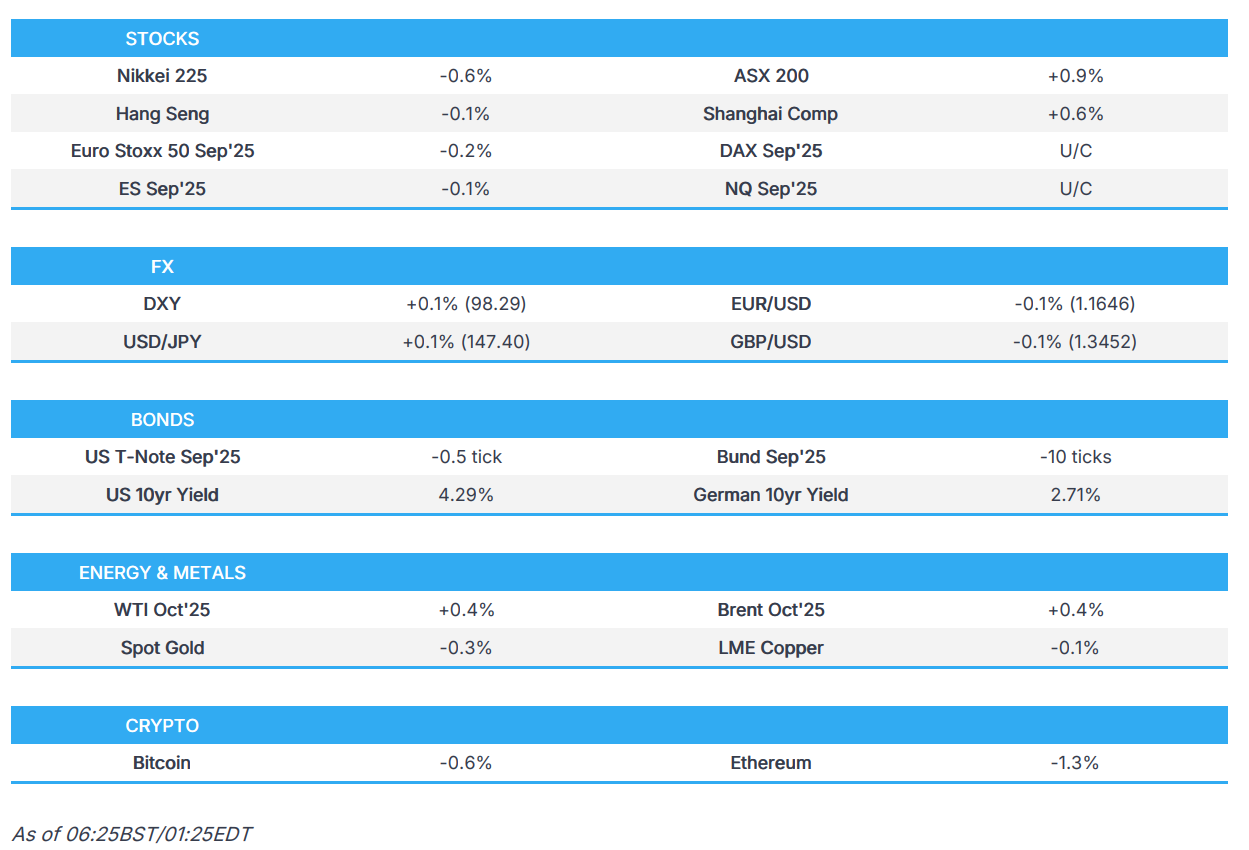

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED UP 4.89 PTS OR 0.13%

//Hang Seng CLOSED DOWN 61.33 PTS OR 0.24%

// Nikkei CLOSED DOWN 278.38 PTS OR 0.65% //Australia’s all ordinaries CLOSED UP 1.16%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1776 OFFSHORE CLOSED UP AT 7.1811/ Oil UP TO 63.26 dollars per barrel for WTI and BRENT UP TO 67.40 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1776 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1811 AGAINST US DOLLAR/ AND THUS STRONGER

SHANGHAI CLOSED DOWN 0.74 PTS OR 0.02%

//Hang Seng CLOSED DOWN 53.95 PTS OR 0.21%

// Nikkei CLOSED DOWN 168.02 PTS OR 0.38% //Australia’s all ordinaries CLOSED DOWN 0.76%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1821 OFFSHORE CLOSED DOWN AT 7.1855/ Oil DOWN TO 62.90 dollars per barrel for WTI and BRENT DOWN TO 65.90 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1821 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1855 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 846 CONTRACTS TO 437,695 OI DESPITE OUR STRONG GAIN IN PRICE OF $29.95 WITH RESPECT TO WEDNESDAY’S // TRADING.. WE LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3954). WE HAD ZERO T.A.S. LIQUIDATION //WEDNESDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 4294 CONTRACTS (OR 13.35 TONNES). WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FRIDAY. THE CROOKS COULD NOT FLEECE ANY OF OUR NET LONGS AS THE COMEX LEVEL OI WAS EXTREMELY LOW AND THUS VERY VERY STICKY: AND AS SUCH THE OI ROSE A BIT DESPITE OUR LOSS IN PRICE.

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AS MENTIONED ABOVE: TONIGHT WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FOR AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER TONIGHT, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

THUS THE TOTAL FOR AUGUST IS 3374 CONTRACTS OR 337,400OZ OR 10.4932 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES) IT SEEMS NOW THAT THE BANK OF ENGLAND IS IN QUITE A HURRY TO GET ITS GOLD BACK!! (AND PROBABLE OWNER OF THOSE EXCHANGE FOR RISK CONTRACTS)

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 3 ISSUANCES FOR A MONSTER 3374 CONTRACTS OR 337,400 OZ ( 10.4932 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 3108 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED A 710 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED THREE WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 43.639 TONNES +10.4932 TONNES EX FOR RISK (3 ISSUANCES) //NEW STANDING 114.6792 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 236 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE 43.639 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES AND THEN AUGUST 12: 2.637 TONNES:/NEW STANDING ADVANCES TO 114.6792 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3954 EFP CONTRACT WAS ISSUED: : /DEC 3954 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3954 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//WEDNESDAY

- MONTH END SPREADERS WILL APPEAR FOR SURE ON THE LAST WEEK OF AUGUST AND MAYBE IT BEGAN STARTING TODAY AUGUST 21

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A SMALL SIZED SIZED 710 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S STRONG GAIN IN PRICE IN GOLD AND A CORRESPONDING SMALL GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S FIRST THREE ISSUANCES OF EXCHANGE FOR RISK FOR 10.4932 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 3.263TONNES TO WHICH WE ADD THURSDAY’S AUG 7 HUGE 5.4432 EXCHANGE FOR RISK, SATURDAY’S//MONDAY AUG 10 STRONG 776 CONTRACT ISSUANCE (77600 OZ) FOR 2.413 TONNES AND THEN WEDNESDAY.S AUGUST 12 FOR 2.637 TONNES/// TOTAL EX FOR RISK AUGUST = 10.4932 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

104.186 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

EQUALS

114.6792 TONNES TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $29.95/ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION (SAVING IT TODAY, THURSDAY ///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH TUESDAY’S/RAID!.

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: THREE SO FAR, AUGUST 7 THROUGH AUG 12 AT 3374 CONTRACTS FOR 337,400 OZ (10.4932 TONNES OF GOLD) TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 10.4932 TONNES

THUS 14.186 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 10.4932 TONNES = 114.6792 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 9.667 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD LAST AUG 8 RECORD BREAKING QUEUE JUMP OF 10.8775 TONNES OF GOLD ON TOP OF AUG 12 1.7604 TONNES QUEUE JUMP AND THEN WEDNESDAY;S AUG 13 MASSIVE QUEUE JUMP OF 3.527 TONNES AND THEN THURSDAY AUG 14 A HUGE 2.463 TONNES QUEUE JUMP AND FRIDAY;S AUG 15 QUEUE JUMP OF .7030 TONNES AND THEN SATURDAY’S 1.617 TONNE QUEUE JUMP AND THEN AUG 19: 1.058 QUEUE JUMP AND FINALLY TODAY’S MASSIVE QUEUE JUMP OF 3.263 TONNES TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK/PRIOR FOR 10.4932 TONNES FOR RISK//NEW STANDING ADVANCES TO 114.6792 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $29.95

WE HAD 1186 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 3108 CONTRACTS OR 310,800 0Z (9.667 TONNES)

confirmed volumeTHURSDAY 149,905 contracts// extremely poor//everybody vacating the comex???

speculators have left the gold arena

END

INITIAL GOLD COMEX

END

INITIAL GOLD COMEX

AUGUST CONTRACT MONTH

AUGUST 21 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entries . |

| Deposit to the Dealer Inventory in oz | 1 ENTRY i) Into Asahi dealer: 9,352.03 oz total deposit 9352.03 oz |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 2622 notice(s) 262,200 OZ 8.1555 TONNES |

| No of oz to be served (notices) | 446 contracts 44600 OZ 1.3574 TONNES |

| Total monthly oz gold served (contracts) so far this month | 33,050 notices 3,305,000 oz 102.799 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

1 ENTRY

i) Into Asahi dealer: 9,352.03 oz

total deposit 9352.03 oz

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

adjustments: 0

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 3068 CONTRACTS FOR A GAIN OF 743CONTRACTS

WE HAD 306 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED A HUGE SIZED 1049 CONTRACTS OR 104,900 OZ OF GOLD (3.263 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT LOST 348 CONTRACTS TO 4446

OCTOBER LOST 1070 CONTRACTS DOWN TO 60,031

We had 411 contracts filed for today representing 41,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 6 notices issued from their client or customer account. The total of all issuance by all participants equate to 2622 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 360 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (33,050 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 3068 CONTRACTS) minus the number of notices served upon today (2622 x 100 oz per contract) equals 3,349,600 OZ OR 104.186 TONNES TO WHICH WE ADD OUR THREE ISSUANCES OF 10.4932 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 AND 12TH = 114.6792 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (33,050 x 100 oz +we add the difference for front month of AUGUST (3068 OI} minus the number of notices served upon today (2622 x 100 oz) which equals 3,349,600 OZ OR 104.186 TONNES + 10.4932 TONNES EX FOR RISK = 114.6792 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 114.6792TONNES WHICH IS A MONSTER FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. AND THIS RUNS COUNTER INTUATIVE TO OUR CONSTANT RAIDS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,030,244.382 oz 63.14 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,573,264.036 oz

TOTAL REGISTERED GOLD 21,299,461.853 or 662.50 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,274,302.183 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,259,256 oz ((REG GOLD- PLEDGED GOLD)= 599.04 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACT//INITIAL

AUGUST 21 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries: |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 0 DEPOSIT ENTRY/CUSTOMER ACCOUNT |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ |

| No of oz to be served (notices) | 36 contracts (0.180 MILLION oz) |

| Total monthly oz silver served (contracts) | 1720 Contracts (8.60 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

0 DEPOSIT ENTRY/CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

0 entry:

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 190.400 MILLION OZ//.TOTAL REG + ELIGIBLE. 508.519 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 36 OPEN INTEREST CONTRACTS FOR A LOSS OF 2 CONTRACTS. WE HAD 0 CONTRACTS SERVED ON WEDNESDAY SO WE LOST 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL NOT STAND AT THE COMEX HAVING UNDERGONE AN EFP TRANSFER TO LONDON AS THESE GUYS COULD NOT WAIT ANY LONGER AS THEY ARE STANDING FOR DELIVERY OVER ON THAT SIDE OF THE POND.

SEPTEMBER LOST 3249 CONTRACTS DOWN TO 59,387 CONTRACTS.

OCTOBER GAINED 202 CONTRACTS TO 1217

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or NIL oz

CONFIRMED volume; ON WEDNESDAY 75,190 good//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1720 X5,000 oz = 8.600 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (36) AND the number of notices served upon today (0 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1720) Notices served so far) x 5000 oz + OI for the front month of AUGUST(36) minus number of notices served upon today (0)x 5000 oz equals silver standing for the AUGUST contract month equating to 8.780 MILLION OZ .

New total standing: 8.780 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.400 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/508.151 million. 41.33%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 10 WITH GOLD UP $4.75 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.860 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.37 TONNES/

JULY 9 WITH GOLD UP $4.05 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 946.51 TONNES/

JULY 8 WITH GOLD $24.65 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 7 WITH GOLD UP $0.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 3 WITH GOLD DOWN $15.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.57 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 947.66 TONNES/

JULY 2 WITH GOLD UP $8.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.30 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 948.23 TONNES/

JULY 1 WITH GOLD UP $43.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD //: /// ///INVENTORY RESTS AT 952.53 TONNES/

JUNE 30 WITH GOLD UP $20.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.43 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 954.82 TONNES/

JUNE 27 WITH GOLD DOWN $58.50 TODAY// NO CHANGES IN GOLD AT THE GLD //: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 26 WITH GOLD UP $4.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 953.39 TONNES/

JUNE 25 WITH GOLD UP $8.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD//: /// ///INVENTORY RESTS AT 955.68 TONNES/

JUNE 24 WITH GOLD DOWN $58.05 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 7.16 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 957.40 TONNES/SINCE JUNE 13 ADDED 24.49 TONNES

JUNE 23 WITH GOLD UP $9.25 TODAY// HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.599 TONNES OF GOLD INTO THE GLD//: /// ///INVENTORY RESTS AT 950.241 TONNES

GLD INVENTORY: 958.21 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 10 WITH SILVER UP $0.47/ NO CHANGES AT THE SLV// A DEPOST OF 0.999 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 9 WITH SILVER DOWN $0.18/ NO CHANGES AT THE SLV// A DEPOST OF 2.136 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 480.176 MILLION OZ.//

JULY 8 WITH SILVER DOWN $0.16/ NO CHANGES AT THE SLV A DEPOST OF 0.000 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 7 WITH SILVER DOWN $0.14/ HUGE CHANGES AT THE SLV A DEPOST OF 0.727 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.040 MILLION OZ.//

JULY 3 WITH SILVER UP $0.34/ HUGE CHANGES AT THE SLV A WITHDRAWAL OF 0.917 MILLION OZ IOUT OF THE SLV//:.////INVENTORY RESTS AT 477.313 MILLION OZ.//

JULY 2 WITH SILVER UP $0.36/ HUGE CHANGES AT THE SLV A DEPOSIT OF 1.363 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 478.049 MILLION OZ.//

JULY 1 WITH SILVER UP $0.21/ HUGE CHANGES AT THE SLVA WITHDRAWAL OF 1.272 MILLION OZ FROM THE SLV//:.////INVENTORY RESTS AT 476,686 MILLION OZ.//

JUNE 30 WITH SILVER DOWN $0.20/ NO CHANGES AT THE SLV:.////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 27 WITH SILVER DOWN $0.53/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.636 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 477.958 MILLION OZ.//

JUNE 26 WITH SILVER UP $0.48/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 1.091 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 479.594 MILLION OZ.//

JUNE 25 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV:. A WITHDRAWAL OF 2.363 MILLION OZ IOUT OF THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//

JUNE 24 WITH SILVER DOWN $0.37/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 3.453 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 480.685 MILLION OZ.//FROM JUNE 2 A HUGE 19.264 MILLION OZ ADDED

JUNE 23 WITH SILVER UP $0.18/ HUGE CHANGES AT THE SLV:. A DEPOSIT OF 2.591 MILLION OZ INTO THE SLV..////INVENTORY RESTS AT 477.232 MILLION OZ.

CLOSING INVENTORY 492.091 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

MARKET EAR:

The $4,000 Gold Dream: One Peace Deal Away from a Putin Punch

Thursday, Aug 21, 2025 – 8:55

Gold on our minds

Gold continues to trade inside the boring range that has been in place for months. Note we are down to the 100 day moving average. Last time we bounced off the 100 day, things took off… Let’s examine the 4000 dream and if a “Putin Punch” can derail it.

Source: LSEG Workspace

Keeping the 4000 dream alive

GS: “We maintain our $4,000/toz forecast for mid-2026.“

Source: Goldman

How to get to 4000

Goldman’s 4000 price is driven by structurally strong central bank demand and ETF-inflows supported by Fed easing and a 30% US recession risk that could amplify inflows.

Source: Goldman

Another 4000

Yardeni: “We are still targeting a gold price of $4,000 per ounce by the end of this year.”

Source: Yardeni

Just a seasonal Central Bank lull

“Our June nowcast of central bank and institutional gold demand on the London OTC market came in at 16 tonnes, below our 2025 average forecast of 80 tonnes/month. This is consistent with the recent seasonal pattern: central bank purchases tend to slow in the summer and re-accelerate from September.”

Source: Goldman

The Putin connection

The price of gold has been rising ever since the US froze the foreign exchange reserves of Russia after the country invaded Ukraine in February 2022. The central banks of countries that don’t share America’s values and interests have been buying more gold and selling dollars.

Source: Yardeni

No need for a Putin Put

Goldman is not afraid of the potential “Putin Punch”: “While speculative clearing since April reduces near-term downside price risk, a Russia-Ukraine peace deal agreement could – in our view – still trigger a short-lived sell-off that we estimate at around 3% as speculators sell. Yet, we see little lasting impact on fundamentals.”

Re-routing reflation

“On the supply side, sanctioned Russian-produced gold is already reaching global markets through rerouting via the CIS (Armenia, Kazakhstan, Uzbekistan), the UAE, and Hong Kong. In fact, export volumes are now above pre-pandemic averages once rerouting is accounted for.” (Goldman)

Source: Global Trade Tracker

Far from big longs

Gold net non commercials have room to buy much more gold…

Source: LSEG Workspace

Lagging

Gold continues to lag little brother, silver. Chart 2 shows 3 months chart in %.

Source: LSEG Workspace

Source: LSEG Workspace

Dirt cheap

Gold volatility starting to screen as a bargain. Playing direction via options is very attractive given where volatility trades… and don’t forget that gold trades with an upside volatility skew, i.e gold up sharply usually means volatility picks up.

Source: LSEG Workspace

1/ PETER SCHIFF/S

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

ALASDAIR MACLEOD…

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

GoldCore’s Jan Skoyles sees far bigger threats to wealth than gold confiscation

Submitted by admin on Tue, 2025-08-19 20:56 Section: Daily Dispatches

8:54p ET Tuesday, August 19, 2025

Dear Friend of GATA and Gold:

In her commentary for GoldCore today, Jan Skoyles explains why gold confiscation is far less a threat to investors and savers than financial repression, tax increases, and inflation, and why investors and savers can take good precautions against all those threats.

Her commentary is 16 minutes long and can be viewed at the GoldCore channel at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Gold gains traction in Islamic investing as rally spurs interest

Submitted by admin on Tue, 2025-08-19 10:27 Section: Daily Dispatches

By Yihui Xie

Bloomberg News

via News24, Cape Town, South Africa

Monday, August 18, 2025

In a small town an hour’s drive from Malaysia’s capital, a new, high-security vault illustrates the growing popularity of gold products and services designed to cater to Islamic principles.

Run by a subsidiary of Loomis AB, the Swedish cash- and bullion-handling company, together with local security firm E2S Group, the 20-ton facility in Nilai represents a push to tap into the nation’s burgeoning Islamic bullion sector.

“There’s a desire among local bullion dealers to have proper storage facilities,” Jeremy Beh, Loomis International’s country head in Singapore, said in an interview, before the site was inaugurated to an audience of traders, refiners and bankers last week. Several local banks have recently rolled out so-called halal gold investment products as demand has surged, he said. …

… For the remainder of the report:

end

OK I get it: gold from mines travels to London where it is then converted via Switzerland to gold bars and then this goes to China

(globe and mail)

Gold, not canola or coal, is China’s top import from Canada, at least according to China

Submitted by admin on Mon, 2025-08-18 19:52 Section: Daily Dispatches

China is the world’s leading gold-producing country, so why does it need to import gold from Canada? Is it because China sees gold as the world’s once and future money?

* * *

By Steven Chase

The Globe and Mail, Toronto

Monday, August 18, 2025

Gold bullion from Canada makes up a far greater portion of Chinese gold imports than is generally understood outside of China, according to data from the Asian country’s customs agency that has drawn little notice outside of professional circles here.

The total value of these imports, according to figures from China Customs, is more than 10 times higher than Canadian export statistics suggest — a discrepancy that hints at the full extent of the role trade between the two countries plays in the global gold market. In China’s eyes, gold is its No. 1 import from Canada by value, rather than the canola and coal shipments Canada records as its top exports.

The difference is not a result of an accounting lapse on either country’s part. Instead, it arises from a difference in perspective. Canada is unable to track where its exports end up if they change hands multiple times on their way to their ultimate buyer. But China Customs can and does require importers to track where their products originate.

This means that when Canada sells gold to bullion markets in London and New York, those exports are counted here as sales to Britain and the United States. But when China buys that same Canadian gold from those same markets, it considers the imports to be from Canada.

As a result, Statistics Canada says direct exports of unwrought gold — such as bars or bullion — to China and Hong Kong in 2024 amounted to $1.9 billion.

But the figures from China Customs say that China imported dramatically more from Canada: $25 billion in that same category of goods.

Although the Chinese figures are public, they are not routinely scrutinized in Canada. The Royal Canadian Mint and the Mining Association of Canada were both unable to offer insight into China’s gold import statistics.

Unlike canola or petroleum or coal, gold isn’t generally consumed or destroyed. Aside from some industrial applications, the world’s mined gold supply simply increases over time. According to the World Gold Council, a global industry association, the “above ground” stock of gold was 216,265 tonnes at the end of 2024.

China, however, has started amassing significant gold holdings, and gold investors appear to be unloading their supplies of Canadian bullion in response. The country’s central bank holdings of gold hit 2,292 tonnes in the first quarter of 2025, up substantially from 1,800 tonnes in the same period in 2016. …

… For the remainder of the report:

end

The $1-billion gold mine bringing death to desperate villagers in Tanzania

Submitted by admin on Sun, 2025-08-17 16:34 Section: Daily Dispatches

By Jack Denton

The Sunday Times, London

Sunday, August 17, 2025

NYAMONGO, Tanzania — It was the middle of the night and Chacha was bound hand and foot, hanging upside down from a bridge spanning the crocodile-infested Mara River.

He was there because of the gold.

Masked men had abducted Chacha from Nyamongo, a village near the North Mara gold mine, one of Tanzania’s largest. He was transferred between police stations and tortured so badly he blacked out.

The men had two questions. Who was buying gold from him and other independent miners, and what did he know about the latest police killings at North Mara?

Gold has been coveted since ancient times but demand has rarely been as potent as it is now. The price has almost doubled since 2022, driven up by geopolitical uncertainty, inflation concerns and, latterly, President Trump’s tariffs. …

… For the remainder of the report:

end

Uganda targets higher exports with first big gold mine (owned by China)

Submitted by admin on Sun, 2025-08-17 16:17 Section: Daily Dispatches

By Elias Biryabarema

Reuters

Sunday, August 17, 2025

KAMPALA, Uganda — Uganda has inaugurated its first large-scale gold mine, a $250 million Chinese-owned project in the country’s east that will also refine the bullion to 99.9% purity, according to a statement from the president’s office.

The landlocked east African country, which has a variety of minerals including copper, cobalt, and iron ore, wants to expand its mining industry and position itself as a major gold producer and exporteR

Last year Uganda raised $3.4 billion from gold exports, according to central bank data, about 37% of the country’s total export revenue. The figure includes the re-export of gold brought into the country, with nearly all its domestic production from small-scale artisanal miners. …

… For the remainder of the report:

*END

Another gold rush could bring open pit mines to South Dakota’s Black Hills

Submitted by admin on Sun, 2025-08-17 09:37 Section: Daily Dispatches

By Sarah Raza

Associated Press

Saturday, August 16, 2025

SIOUX FALLS, South Dakota — A gold rush brought settlers to South Dakota’s Black Hills roughly 150 years ago, chasing the dream of wealth and displacing Native Americans in the process.

Now a new crop of miners driven by gold prices at more than $3,000 an ounce are seeking to return to the treasured landscape, promising an economic boost while raising fears of how modern gold extraction could forever change the region.

“These impacts can be long-term and make it so that tourism and outdoor recreation are negatively impacted,” said Lilias Jarding, executive director of the Black Hills Clean Water Alliance. “Our enjoyment of the Black Hills as a peaceful place, a sacred place, is disturbed.” …

… For the remainder of the report:

* * *

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 236

5. COMMODITY REPORT.

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED UP 4.89 PTS OR 0.13%

//Hang Seng CLOSED DOWN 61.33 PTS OR 0.24%

// Nikkei CLOSED DOWN 278.38 PTS OR 0.65% //Australia’s all ordinaries CLOSED UP 1.16%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1776 OFFSHORE CLOSED UP AT 7.1811/ Oil UP TO 63.26 dollars per barrel for WTI and BRENT UP TO 67.40 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1776 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1811 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1776 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1811

HANG SENG CLOSED DOWN 61.33 PTS OR 0.24%

2. Nikkei closed DOWN 278.38PTS OR 0.65%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 98.13 EURO RISES TO 1.1655 UP 4 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.606//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.59…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7325Italian 10 Yr bond yield DOWN to 3.570 SPAIN 10 YR BOND YIELD DOWN TO 3.314

3i Greek 10 year bond yield DOWNTO 3.420

3j Gold at $3339.10 Silver at: 37.77 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 32 /100 roubles/dollar; ROUBLE AT 80.82

3m oil (WTI) into the 63 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.59/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.606% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8052 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.93.85 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.3079 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.913 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.760 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.94

10 YR UK BOND YIELD: 4.7150 UP 4 PTS

10 YR CANADA BOND YIELD: 3.456UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.962 DOWN 0 PTS

2a New York OPENING REPORT

Futures Slide For Fifth Day As Jackson Hole Jitters Rise

Thursday, Aug 21, 2025 – 08:07 AM

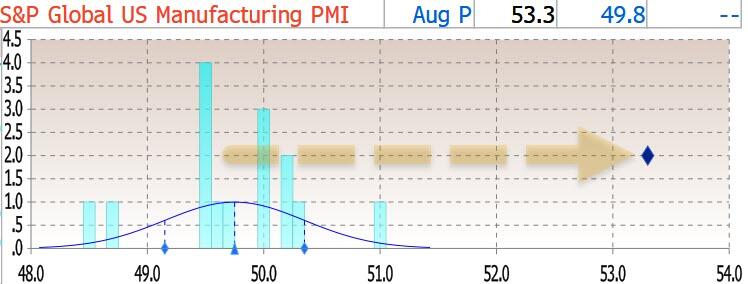

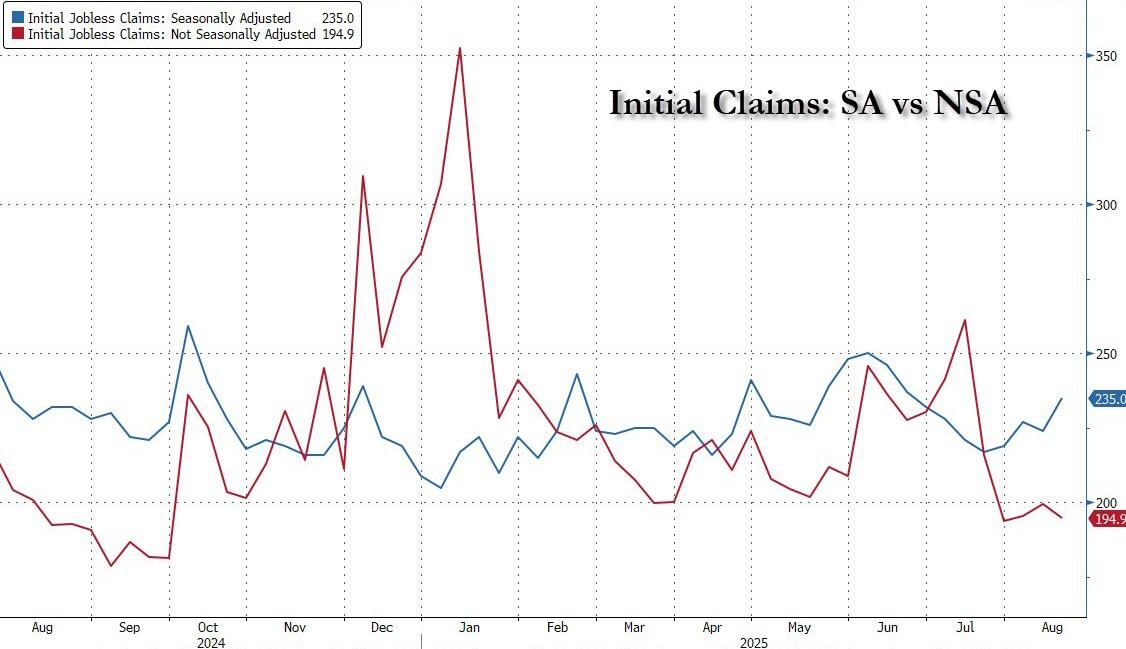

US equity futures dropped, extending the recent selloff into its fifth day, as traders stayed guarded ahead of the Federal Reserve’s gathering at Jackson Hole. As of 8:00am, S&P 500 futures fell 0.2%, while Nasdaq 100 futures were flat after a two-day selloff that erased 2% off the index. In premarket trading, Nvidia rose 0.8% while most Magnificent Seven peers posted losses. Retail giant Walmart brought Q2 earnings season to an unofficial close after reporting an EPS miss (68c vs exp. 74c) and even though it lifted guidance (now expects net sales to rise 3.75% to 4.75% this year, versus previous forecast of a 3% to 4%) that wasn’t enough for the market, however, and the stock dropped in premarket trading. European stocks dropped 0.3%, erasing an earlier gain, and snapping a three-day winning streak. US treasuries fell, pushing the yield on the 10-year higher to 4.31%. The dollar strengthened and reversed all of yesterday’s losses while Brent crude rose to the highest in two weeks even as the rest of the commodity complex was mixed. It’s a busy economic calendar: we get weekly jobless claims and August Philadelphia Fed business outlook (8:30am), S&P Global US PMIs (9:45am) and July leading index and existing home sales (10am). The Fed speaker slate includes Atlanta Fed President Bostic at 7:30am, the last central bank official slated to speak before Chair Powell’s discourse at Jackson Hole Friday

In premarket trading, Mag 7 stocks are mostly lower (Nvidia +0.8%, Tesla unchanged, Microsoft -0.1%, Alphabet -0.2%, Amazon -0.3%, Meta -0.3%, Apple -0.5%). Here are some other notable premarket movers:

- Aegon ADRs (AEG) are up 5% after the Dutch insurance company posted better-than-expected results and said it planned to increase its share buyback. Management said the company may redomicile to the US, a move that Morgan Stanley said would “make sense.”

- Boeing Co. (BA) gains 1.5% as the company is heading closer toward finalizing a deal with China to sell as many as 500 aircraft, according to people familiar with the matter.

- Canadian Solar (CSIQ) falls 11% after forecasting third-quarter revenue below analyst expectations.

- Coty (COTY) falls 20% after the personal care products company forecast steep sales declines and reported a wider-than-expected loss for the fourth quarter.

- Dayforce (DAY) rises 1.4% after entering into a definitive agreement with Thoma Bravo to become a privately held company in an all-cash transaction with an enterprise value of $12.3 billion.

- Hewlett Packard Enterprise (HPE) gains 3.1% after being raised to overweight from equal-weight at Morgan Stanley as analysts note that recently-closed Juniper deal will be an earnings upside.

- SharkNinja (SN) trades lower by 2% as holders affiliated with Chairperson CJ Xuning Wang offer 5 million shares in the household-appliance maker via JPMorgan, BofA Securities.

- Two Harbors Investment (TWO) falls 3% after the mortgage REIT resolved litigation with Pine River via a one-time $375m cash settlement and cut its quarterly dividend to 34c a share.

- Walmart (WMT) slips 2.4% after the world’s largest retailer posted second quarter profit that disappointed.

In corporate news, FanDuel, the online gambling division of Flutter Entertainment, is teaming up with CME Group, the largest US derivatives exchange, to offer bets on stocks, commodity prices and even inflation. Google introduced a new slate of consumer gadgets, including several smartphones, a watch and new wireless earbuds, all meant to show off the company’s latest advances in artificial intelligence. Musk‘s Starlink service is said to be in conversation with Emirates and other Middle Eastern airlines, with winning business in the region potentially marking a watershed moment in Starlink’s global competition.

This week has seen pressure on momentum names (read tech stocks) particularly the largest names, amid worries that their sharp rally since April has moved too far, too fast. Traders are also cautious as the Jackson Hole symposium kicks off later today, with investors awaiting Fed Chair Jerome Powell’s speech at 10am ET Friday for guidance on the path for interest rates. Despite the pullback in stocks this week, the VIX hasn’t really budged, and Goldman said it’s time to buy the dip in momentum stocks (and the overall market according to JPMorgan).

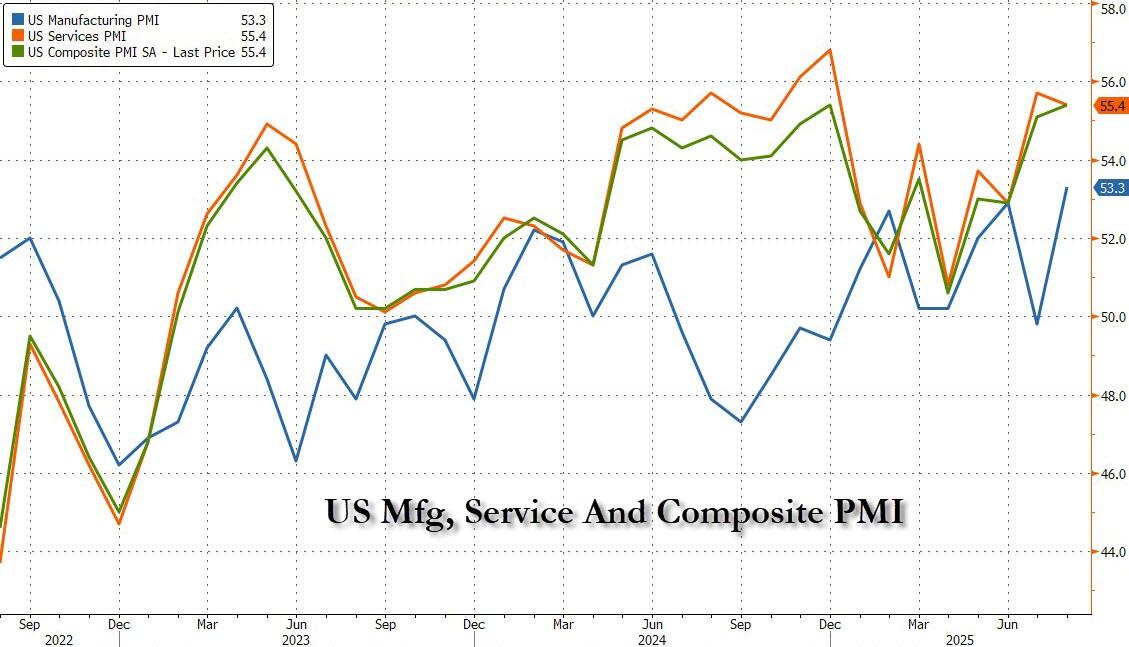

The market’s direction today will also be shaped by PMIs, home sales data and Walmart earnings (which missed but boosted its revenue forecast). For the euro area, the Composite Purchasing Managers’ Index compiled by S&P Global grew at the quickest pace in 15 months as manufacturing exited a three-year downturn.

“What we are currently seeing is profit-taking and a natural flight to quality ahead of Jerome Powell’s speech in Jackson Hole,” said John Plassard, head of investment strategy at Cité Gestion. But “let’s not beat around the bush: this is not the end of tech, and even less so for stocks linked to artificial intelligence.”

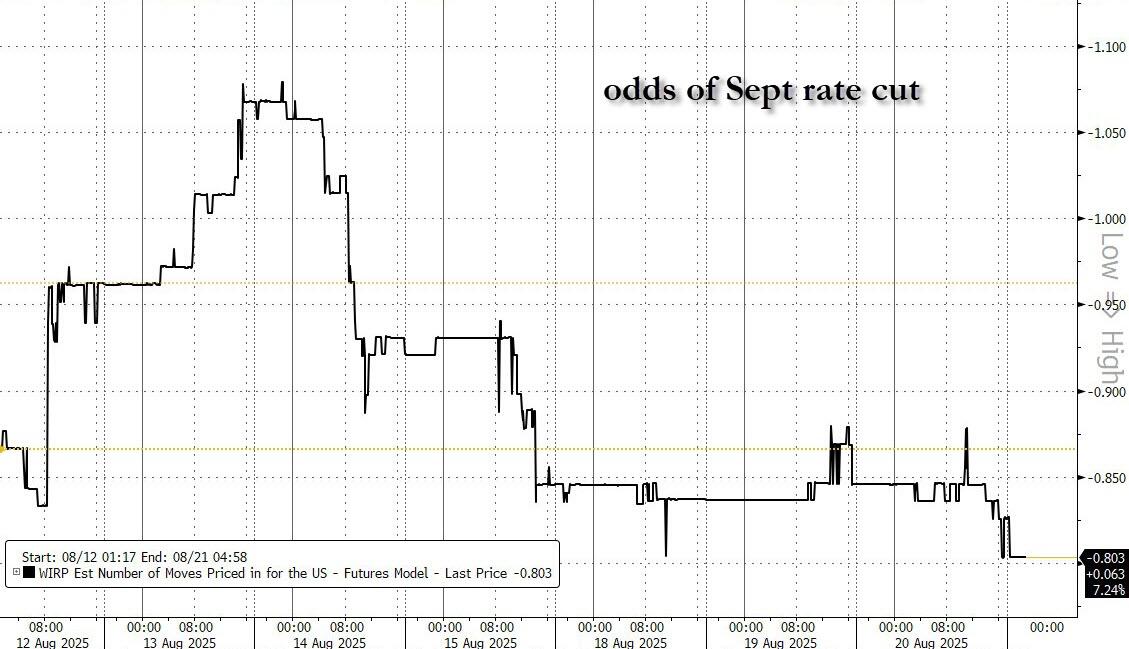

Swaps are currently pricing in 80% chance of a Fed quarter-point cut in September, and at least three more over the next year, some strategists warned that the market may be too optimistic about the pace and depth of easing.

“All it’s going to take is a bit of stickiness in inflation and actually a labor market print which shows it’s not falling off a cliff for the market to say, ‘hang on,’” Karen Ward, chief market strategist for EMEA at JPMorgan Asset Management, told Bloomberg TV.

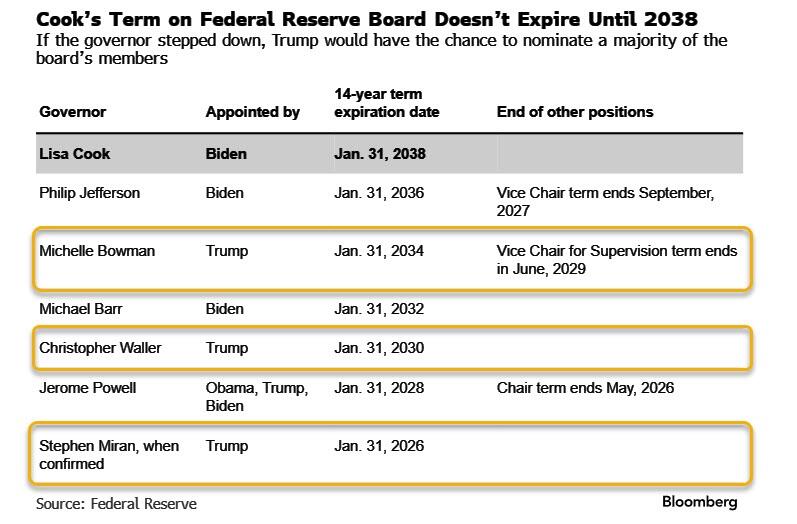

In his latest effort to stack the Fed board, Trump and his allies are demanding Fed Governor Lisa Cook resign over alleged owner-occupancy fraud. For her part, Cook signaled her intention to remain at the central bank.

Yesterday, the latest FOMC Minutes for the July 29-30 meeting showed most officials viewed inflation risks as outweighing labor-market concerns, with tariffs fueling a growing divide within the rate-setting committee, though the discussions came before subsequent dramatic dire revisions to jobs data.

On the geopolitical front, US Vice President JD Vance said negotiations over ending Russia’s war in Ukraine are focused on security guarantees for Ukraine and territory Russia wants to control — including Ukrainian territory that Russia isn’t occupying — as the US tries to broker a peace deal between the two nations. Brent crude rose 0.8%.

The Stoxx 600 falls 0.2% with media, consumer product and chemical shares leading declines. Nordics represented several of the region’s biggest movers, with hearing-aid maker GN Store Nord surging 19% after reporting earnings, while Norwegian oil firm Aker BP jumped after a large oil find in the North Sea. UK retailer WH Smith plunged after signaling North American profit will be much weaker than previously hoped. Here are the biggest movers Thursday:

- Aegon shares jump as much as 7.4%, reaching a 10-year high, after the Dutch insurance company posted better-than-expected results and said it planned to increase its share buyback

- GN Store Nord gains as much as 19% after the Danish hearing aid and audio equipment firm’s 2Q earnings beat estimates across the board. Analysts see a strong showing following weaker reports from European peers

- Aker BP shares rise as much as 4.6% after the Norwegian industrial investment company announced a “significant oil discovery” as it completed the Omega Alfa exploration campaign in the Norwegian North Sea

- ALK-Abello gains as much as 5.9%, the most since May, after the Danish allergy drugmaker reported 2Q earnings. Analysts say that while the report holds few surprises after the company pre-released figures, they reassured

- Salmar gains as much as 6.1%, the most since April, after the Norwegian salmon firm reported its latest earnings, which DNB Carnegie described as in line, with “positive” cost and volume guidance for the rest of the year

- DNO gains as much as 11%, the most since 2023, after the Norwegian oil company reported its latest earnings and hiked its dividend per share by around 20%. DNB Carnegie expects the raised payouts to support the shares

- Renishaw shares rise as much as 8.9% to the highest since February after the precision measuring equipment maker indicated its adjusted pretax profit for the full year will be at the high end of the guidance range

- WH Smith shares plummet as much as 38%, the biggest drop on record, after the retailer warned headline trading profit from North America will be significantly lower than previously hoped

- CTS Eventim shares slide as much as 20%, the most since 2007, after the events firm reported 2Q Ebitda well below estimates. The firm cited “intense and persistent cost pressures” for live events and headwinds in other divisions

- Novonesis falls as much as 7.8% after the Danish biotechnology group reported earnings. Analysts say a profitability miss and merely reiterated margin guidance disappointed, and will lead to slight consensus cuts

- European stocks in the beauty and personal care sector fell after US company Coty reported a wider adjusted loss per share in 4Q than analysts expected, while forecasting steep sales declines will continue

- Sensirion falls as much as 8.2% after both Berenberg and Research Partners downgraded the semiconductor device manufacturer to hold from buy following its first-half earnings

- UK housebuilders are under pressure on Thursday as London builders are taking longer to start home constructions after receiving permits, with a slump in demand threatening to derail the government’s plan to build 1.5m homes

- Kojamo declines as much as 5.9% following its second-quarter results, with JPMorgan retaining its underweight rating and a cautious stance on the real estate company

Earlier in the session, Asian stocks traded in a tight range, as a rebound in some tech stocks was offset by declines in Japan. The MSCI Asia Pacific Index fell 0.2%, with Japan’s Daiichi Sankyo among the top drags after a series of block trades at a discount. Hon Hai and TSMC were among the biggest boosts for the gauge. Shares hit a record high in Australia, while those in South Korea and Taiwan also advanced. Investors are awaiting cues from the Jackson Hole symposium, where Federal Reserve Chair Jerome Powell is expected to speak on Friday. Nvidia’s results next week will be another key test, with expectations for improving global tech earnings having bolstered sentiment. Equities also traded higher in mainland China, Vietnam and New Zealand on Thursday. MSCI equity gauges for every nation in the region are trading above their 200-day moving averages for the first time since 2021, according to Sentimentrader.com.

In FX, the euro and pound both edge higher against the greenback after the better-than-expected PMI data. The Norwegian krone is the best-performing G-10 currency, rising 0.5% after Norway’s GDP grew more than forecast in the second quarter.

In rates, treasuries are under pressure in early US trading amid steeper losses for most European bond markets sparked by stronger-than-anticipated August preliminary PMI gauges. US yields are higher by 1bp-2bp, the 10-year by about 1.8bp at 4.31%, vs increases of 3bp-4bp for UK and most euro-zone counterparts. US session features 30-year TIPS reopening auction at 1pm New York time. Week’s major focal point is Fed Chair Powell’s Jackson Hole speech on Friday. UK gilts are leading declines in European government bonds after the UK private sector expanded at the strongest pace in 12 months. UK 10-year yields rise 3 bps to 4.70%. German 10-year borrowing costs add 2 bps to 2.73% after the euro area’s private sector grew at the quickest pace in 15 months.

Looking at today’s calendar, US economic data calendar includes weekly jobless claims and August Philadelphia Fed business outlook (8:30am), August preliminary S&P Global US PMIs (9:45am) and July leading index and existing home sales (10am). Fed speaker slate includes Atlanta Fed President Bostic at 7:30am, the last central bank official slated to speak before Chair Powell’s discourse at Jackson Hole Friday

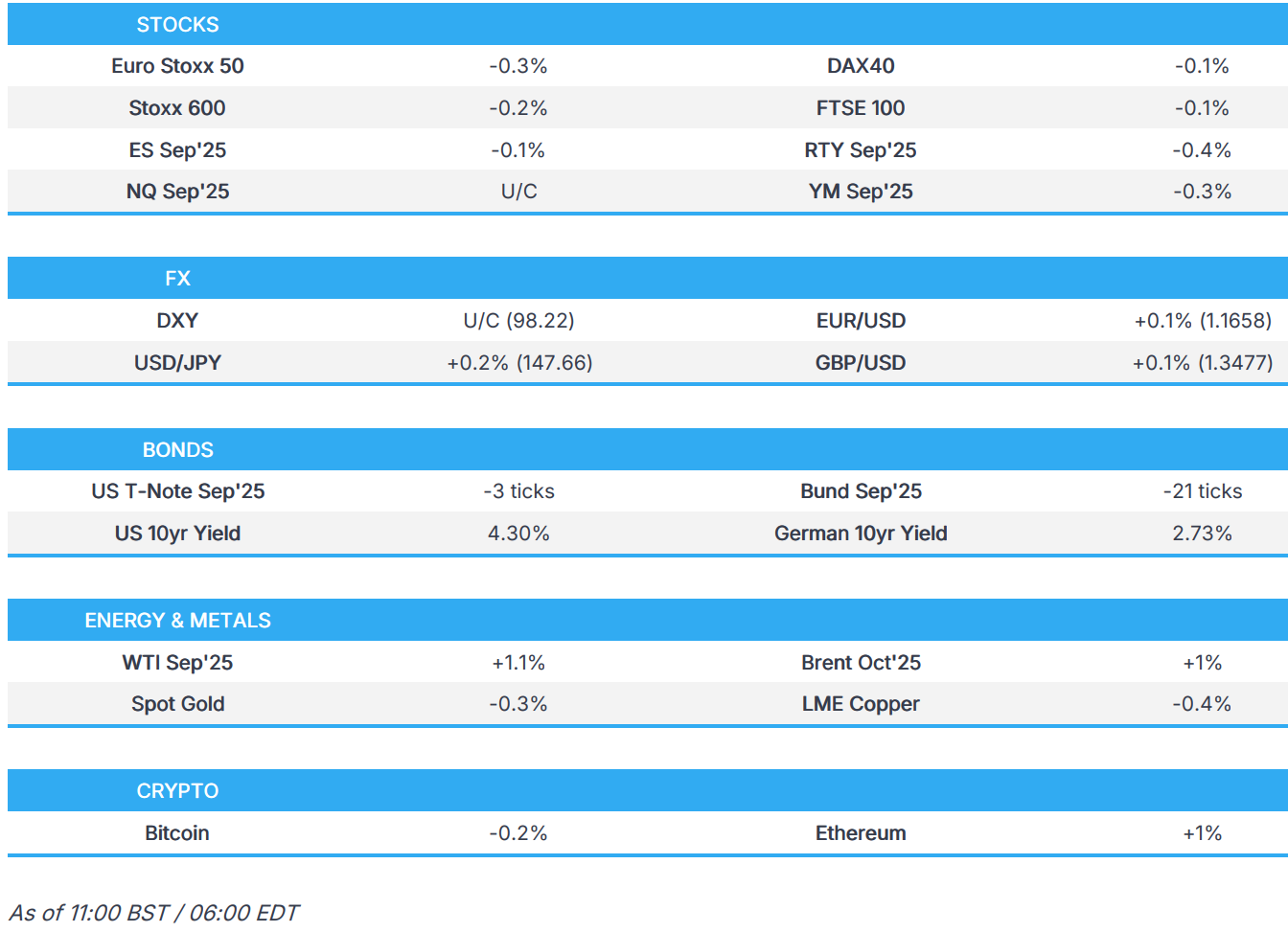

Market Snapshot

- S&P 500 mini -0.1%

- Nasdaq 100 mini little changed

- Russell 2000 mini -0.3%

- Stoxx Europe 600 -0.2%

- DAX -0.1%

- CAC 40 -0.5%

- 10-year Treasury yield +1 basis point at 4.3%

- VIX +0.2 points at 15.93

- Bloomberg Dollar Index little changed at 1207.17

- euro little changed at $1.1658

- WTI crude +1% at $63.35/barrel

Top Overnight News

- Fed reserve governor Lisa Cook has defied calls from Trump to resign, saying she has “no intention of being bullied to step down” after FHFA Director Bill Pulte posted he was making a criminal referral based on a mortgage application from four years ago: FT

- The Texas House approved a new congressional map that may add up to five GOP seats in the 2026 midterms. In California, the state’s top court declined to halt Governor Gavin Newsom’s own redistricting plan, which he’s pursuing to offset the moves in Texas and elsewhere. BBG

- Meta Platforms has frozen hiring in its artificial-intelligence division after spending months scooping up 50-plus AI researchers and engineers. WSJ

- South Korea will unveil an additional $150 billion in US investment from private firms during Lee Jae Myung’s summit with Trump, local media said. BBG

- The euro area’s private sector expanded at the quickest pace in 15 months, PMI data showed, adding to evidence of the region’s resilience. Manufacturing ended a three-year downturn despite higher US levies. UK composite PMI also rose more than expected. BBG

- China is aggressively trying to persuade domestic tech firms to avoid buying Nvidia chips following “insulting” remarks from Commerce Sec Lutnick. FT