099 H DEUTSCHE BANK AG 34

323 C HSBC 22

661 C JP MORGAN SECURITIES 20 6

709 C BARCLAYS 1

737 C ADVANTAGE FUTURES 16

905 C ADM 27

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 63 CONTRACTs NOTICES FOR 6300 OZ or 0.1959 TONNES

total notices so far: 33,113 contracts for 3,311,300 OR 102.995 tonnes)

SILVER NOTICES: 57 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 1777 CONTRACTS (NOTICES) for 8.885 million oz

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 30.795 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 120,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 8.900 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE MONTH’S QUEUE JUMP OF 43.7665 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK //NEW STANDING ADVANCES TO 104.186 TONNES OF GOLD (INCLUDES ALL MONTHLY QUEUE JUMPS) +10.4932 TONNES EX.FOR RISK = 114.7445 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 136.152 TONNES QUITE SMALL

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE 1119 CONTRACTS OI TO 160,144 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 350 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 320 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1119 CONTRACTS AND ADD TO THE 350 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1469 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.29 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 7.345 MILLION PAPER OZ

OCCURRED WITH OUR $0.29 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 54.66 PTS OR 1.45%

//Hang Seng CLOSED UP 214.70 PTS OR 0.86%

// Nikkei CLOSED UP 23.12 PTS OR 0.05% //Australia’s all ordinaries CLOSED DOWN 0.57%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1812 OFFSHORE CLOSED DOWN AT 7.1845/ Oil UP TO 63.70 dollars per barrel for WTI and BRENT UP TO 67.70 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1812 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1845 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3597 CONTRACTS TO 434,098 OI WITH OUR LOSS IN PRICE OF $6.80 WITH RESPECT TO THURSDAY’S // TRADING.. WE LOST NO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1677). WE HAD ZERO T.A.S. LIQUIDATION //THURSDAY TRADING AS WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1920 CONTRACTS (OR 5.972 TONNES). WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FRIDAY. THE CROOKS COULD NOT FLEECE ANY OF OUR NET LONGS AS THE COMEX LEVEL OI WAS EXTREMELY LOW AND THUS VERY VERY STICKY: AND AS SUCH THE OI ROSE QUITE BIT DESPITE OUR LOSS IN PRICE.

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AS MENTIONED ABOVE: TONIGHT WE HAD 0 CONTRACTS ISSUED FOR EXCHANGE FOR RISK FOR AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER TONIGHT, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

THUS THE TOTAL FOR AUGUST IS 3374 CONTRACTS OR 337,400OZ OR 10.4932 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES) IT SEEMS NOW THAT THE BANK OF ENGLAND IS IN QUITE A HURRY TO GET ITS GOLD BACK!! (AND PROBABLE OWNER OF THOSE EXCHANGE FOR RISK CONTRACTS)

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 3 ISSUANCES FOR A MONSTER 3374 CONTRACTS OR 337,400 OZ ( 10.4932 TONNES)

AS I EXPLAINED ABOVE,:THE RECPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 1920 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 808 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED THREE WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 43.7445 TONNES +10.4932 TONNES EX FOR RISK (3 ISSUANCES) //NEW STANDING 114.7445 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 236 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE 43.7665 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES AND THEN AUGUST 12: 2.637 TONNES:/NEW STANDING ADVANCES TO 114.7445 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1677 EFP CONTRACT WAS ISSUED: : /DEC 1677 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1677 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY

- MONTH END SPREADERS WILL APPEAR FOR SURE ON THE LAST WEEK OF AUGUST AND MAYBE IT BEGAN STARTING TODAY AUGUST 21

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A SMALL SIZED SIZED 808 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING;

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S SMALL LOSS IN PRICE IN GOLD AND A CORRESPONDING FAIR GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S FIRST THREE ISSUANCES OF EXCHANGE FOR RISK FOR 10.4932 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.1275TONNES TO WHICH WE ADD THURSDAY’S AUG 7 HUGE 5.4432 EXCHANGE FOR RISK, SATURDAY’S//MONDAY AUG 10 STRONG 776 CONTRACT ISSUANCE (77600 OZ) FOR 2.413 TONNES AND THEN WEDNESDAY.S AUGUST 12 FOR 2.637 TONNES/// TOTAL EX FOR RISK AUGUST = 10.4932 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

104.2513 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

EQUALS

114.7445 TONNES TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $6.80/ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION (SAVING IT TODAY, FRIDAY AND THAT LOSS IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE SPREADERS///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES, IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH TUESDAY’S/RAID!.

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: THREE SO FAR, AUGUST 7 THROUGH AUG 12 AT 3374 CONTRACTS FOR 337,400 OZ (10.4932 TONNES OF GOLD) TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 10.4932 TONNES

THUS 114.2513 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 10.4932 TONNES = 114.7445 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE A FAIR SIZED LOSS TOTAL OF 5.972 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICE TO WHICH WE ADD LAST AUG 8 RECORD BREAKING QUEUE JUMP OF 10.8775 TONNES OF GOLD ON TOP OF AUG 12: 1.7604 TONNES QUEUE JUMP AND THEN WEDNESDAY;S AUG 13 MASSIVE QUEUE JUMP OF 3.527 TONNES AND THEN THURSDAY AUG 14 A HUGE 2.463 TONNES QUEUE JUMP AND FRIDAY;S AUG 15 QUEUE JUMP OF .7030 TONNES AND THEN SATURDAY’S 1.617 TONNE QUEUE JUMP AND THEN AUG 19: 1.058 QUEUE JUMP THEN YESTERDAY’S MASSIVE QUEUE JUMP OF 3.263 TONNES , AND THEN TODAY;S 0.1275 QUEUE JUMP TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK/PRIOR FOR 10.4932 TONNES FOR RISK//NEW STANDING ADVANCES TO 114.7445 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $6.80

WE HAD A MASSIVE 6594 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 1920 CONTRACTS OR 192000 0Z (5.972 TONNES)

confirmed volume THURSDAY 135,619 contracts// extremely poor//everybody vacating the comex???

speculators have left the gold arena

END

INITIAL GOLD COMEX

END

INITIAL GOLD COMEX

AUGUST CONTRACT MONTH

AUGUST 21 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entries i) out of Asahi: 9952.03 oz total withdrawal 9952.03 oz . |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 63 notice(s) 6300 OZ .1959 TONNES |

| No of oz to be served (notices) | 344 contracts 34400 OZ 1.0699 TONNES |

| Total monthly oz gold served (contracts) so far this month | 33,113 notices 3,311,300 oz 102.995 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits:

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entries:

i) Out of HSBC 12,262.960 oz

total withdrawal 12,262.960 oz

adjustments: 1

a) dealer to customer Asahi: 3954.73 oz (123 kilobars)

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 407 CONTRACTS FOR A LOSS OF 2581 CONTRACTS

WE HAD 2622 CONTRACTS SERVED ON THURSDAY SO WE GAINED A GOOD SIZED 41 CONTRACTS OR 4100 OZ OF GOLD (0.1275 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT LOST 214 CONTRACTS TO 4232

OCTOBER GAINED 378 CONTRACTS UP TO 60,409

We had 411 contracts filed for today representing 41,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 20 notices issued from their client or customer account. The total of all issuance by all participants equate to 63 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 6 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (33,113 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 407 CONTRACTS) minus the number of notices served upon today (63 x 100 oz per contract) equals 3,351,700 OZ OR 104.2513 TONNES TO WHICH WE ADD OUR THREE ISSUANCES OF 10.4932 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 AND 12TH = 114.7445 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (33,113 x 100 oz +we add the difference for front month of AUGUST (407 OI} minus the number of notices served upon today (63 x 100 oz) which equals 3,351,7000 OZ OR 104.186 TONNES + 10.4932 TONNES EX FOR RISK = 114.7445 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 114.7445TONNES WHICH IS A MONSTER FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. AND THIS RUNS COUNTER INTUATIVE TO OUR CONSTANT RAIDS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,031,308.902 oz 63.18 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,563,812.006 oz

TOTAL REGISTERED GOLD 21,295,507.280 or 662.37 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,268,304.726 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,264,199 oz ((REG GOLD- PLEDGED GOLD)= 599.19 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE AUGUST 2025 SILVER CONTRACTS

AUGUST 22 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries: i) Out of HSBC 12,262.960 oz total withdrawal 12,262.960 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 0 DEPOSIT ENTRY/CUSTOMER ACCOUNT |

| No of oz served today (contracts) | 57 CONTRACT(S) (285,000 OZ |

| No of oz to be served (notices) | 3 contracts (0.015 MILLION oz) |

| Total monthly oz silver served (contracts) | 1777 Contracts (8.885 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

0 DEPOSIT ENTRY/CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 entry:

1 entries:

i) Out of HSBC 12,262.960 oz

total withdrawal 12,262.960 o

ADJUSTMENTs 1

i) Out of Brinks; customer to dealer: 270,140.900 oz

TOTAL REGISTERED SILVER: 190.670 MILLION OZ//.TOTAL REG + ELIGIBLE. 508.486 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 60 OPEN INTEREST CONTRACTS FOR A GAIN OF 24 CONTRACTS. WE HAD 0 CONTRACTS SERVED ON THURSDAY SO WE GAINED 24 CONTRACTS OR AN ADDITIONAL 120,000 OZ WILL STAND AT THE COMEX HAVING UNDERGONE A QUEUE JUMP AS THESE GUYS ARE STANDING FOR DELIVERY OVER ON THAT SIDE OF THE POND.

SEPTEMBER LOST 6216 CONTRACTS UP TO 53,171 CONTRACTS.

OCTOBER GAINED 183 CONTRACTS TO 1400

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 57 or 285,000 oz

CONFIRMED volume; ON THURSDAY 70,113 good//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 1777 X5,000 oz = 8.885 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (60) AND the number of notices served upon today (57 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (1777) Notices served so far) x 5000 oz + OI for the front month of AUGUST(60) minus number of notices served upon today (57)x 5000 oz equals silver standing for the AUGUST contract month equating to 8.900 MILLION OZ .

New total standing: 8.900 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 190.670 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/508.486 million. 41.33%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

J

GLD INVENTORY: 956.77 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

CLOSING INVENTORY 491.183 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/S

PETER SCHIFF

2. MATHEW PIEPENBERG/VON GREYERZ/RON STOEFERLE

GOLD INTERVIEW: RANDY SMALLWOOD OF WHEATON PRECIOUS METALS:

SPECIAL THANKS TO KEVIN W FOR SENDING:

END

ALASDAIR MACLEOD…

PMs ready for next move

Quiet conditions in precious metals belie explosive upside potential, given a government bond market crisis developing in all major currencies.

| Alasdair MacleodAug 22∙Paid |

In quiet trading, the current consolidation phase in precious metals extended this week. This morning in Europe, gold at $3,330 was down $6 from last Friday’s close, and silver at $38.00 was barely changed. Gold has now been trending sideways for four months, half of 2025 to date while silver has outperformed with the gold/silver ratio falling from 105 to 87.

A notable feature in these otherwise unremarkable conditions has been stand for deliveries on Comex. Since the end of July, a whopping 102.8 tonnes of gold have been stood for delivery, taking the total so far this year to 873.6 tonnes. In silver, over the same periods, 267.5 tonnes and 8,665 tonnes have stood for delivery respectively.

Those in the know are hoarding physical at the expense of paper. But in the very short-term, so far as prices are concerned, the last trade for September options is next Tuesday with calls expiring, providing a strong incentive for market makers to mark gold and silver lower.

This short-term stuff will prove to be irrelevant. We are in the eye of a financial hurricane, and this is set to change.

With trading in gold and silver quiet, we turn our attention to a developing bond market crisis, and how it impacts gold and silver. Long maturity yields are rising as evidence mounts of a buyers’ strike on a global scale. The only reasons that yields have not gone even higher is because governments have restricted supply by funding in short maturities, and markets are still in a summer torpor with investment managers away from their desks.

When they return in the coming weeks, they will find that CPI inflation is rising, economies are stagnating, and the government deficits which require funding are turning out to be larger than expected.

Japan’s 10-year bond yield is higher than it has been since 2008 and appears to be going higher still:

The 30-year JGB yield is double that. Germany’s 30-year bund tells a similar story:

Uk’s long gilt yield is similarly bearish, while the US long bond yield is left slightly behind but look set to break out at any moment:

It is a global phenomenon common to the largest four currencies. Rising yields at the long end of the curve are now dragging benchmark 10-year yields higher. And when the long bond yield rises above 5.1%, it is likely to trigger a crisis not just back down the yield curve, but for equity valuations and those of other financial assets as well.

So where would that leave gold and silver? Clearly, a debt crisis popping the equity bubble has major implications for fiat currencies.

Until recently, traders believed that higher interest rates and bond yields were bad for gold, but that myth ignored the experience of the 1970s and has been blown out of the water by gold correlating with higher bond yields. The reason is simple: higher bond yields reflect a decline in confidence in the issuer and/or an expectation of a fall in the currency’s purchasing power and the value of associated credit. It is the fundamental reason why central banks are selling fiat for gold.

The risk to government bond values is tied to a rapid deterioration in government finances. Stagnating economies combined with high debt to GDP metrics are leading them into debt traps, which can only be negated by massive cuts in government spending. There is no evidence that the necessary cuts are forthcoming. Keynesians believing in credit stimulation completely wrong-footed.

Therefore, gold whose purchasing power is relatively consistent over the centuries appears to rise as currencies decline. But after its 4-month consolidation, gold is now close to breaking out on the upside as credit risk in currencies increases, as the technical chart below illustrates.

And silver leads the way. If silver was a stock, we would say it is undergoing a radical rerating.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 237

5. COMMODITY REPORT.LUMBER

Tariff-Driven Rally Reverses In Lumber Market

Thursday, Aug 21, 2025 – 05:20 PM

There is some good news in the lumber market: contracts have plunged more than 14% in recent weeks, reversing highs last seen during the pandemic shortages. The sharp reversal comes as bets on tariff-driven cost pressures and lower interest rates failed to lift demand. At the same time, disappointing housing data and weak earnings across the housing industry underscored the trouble festering.

Traders ramped up bets that U.S. tariffs on Canadian imports and lower interest rates would lift costs and demand, but housing activity has failed to deliver any demand tailwinds.

There has been weak builder confidence (hitting 13-year lows), disappointing housing permits, and earnings misses at Home Depot, James Hardie Industries, Builders FirstSource, and UFP Industries.

Earlier today…

Canadian mills are operating at a loss, which will likely mean lumber supply cuts are just ahead. Even as tariffs doubled this summer, traders remained in “wait-and-see” mode on interest rates. Now the FOMC is preparing for an interest rate decision next month.

On Thursday, lumber futures for September delivery traded around $604 per thousand board feet, down about 14% from the settlement of $695.50 per thousand board feet on Aug. 1.

Greg Kuta, president and CEO of lumber broker Westline Capital Strategies, told MarketWatch that lumber demand is sagging, with possible stabilization next year after Canadian mills dial back production.

Prices “got ahead of themselves with some overbuying on the way up, and a very large and unsustainable futures premium” developed, according to Steve Loebner, vice president of forest products and risk management at Sherwood Lumber, adding that upward pressure in price was driven by tariffs and future supply levels.

END

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 54.66 PTS OR 1.45%

//Hang Seng CLOSED UP 214.70 PTS OR 0.86%

// Nikkei CLOSED UP 23.12 PTS OR 0.05% //Australia’s all ordinaries CLOSED DOWN 0.57%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1812 OFFSHORE CLOSED DOWN AT 7.1845/ Oil UP TO 63.70 dollars per barrel for WTI and BRENT UP TO 67.70 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1812 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1845 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1812 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.1845

HANG SENG CLOSED UP 214.70 PTS OR 0.86%

2. Nikkei closed UP 23.12 PTS OR 0.05%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 98.64 EURO FALLS TO 1.1594 DOWN 18 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.625//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.60…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7525Italian 10 Yr bond yield UP to 3.604 SPAIN 10 YR BOND YIELD UP TO 3.340

3i Greek 10 year bond yield UP TO 3.455

3j Gold at $3327.60 Silver at: 38.06 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 16 /100 roubles/dollar; ROUBLE AT 80.41

3m oil (WTI) into the 63 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.60/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.625% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8096 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.93.86 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.338 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.929 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.760 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 40.94

10 YR UK BOND YIELD: 4.7510 UP 4 PTS

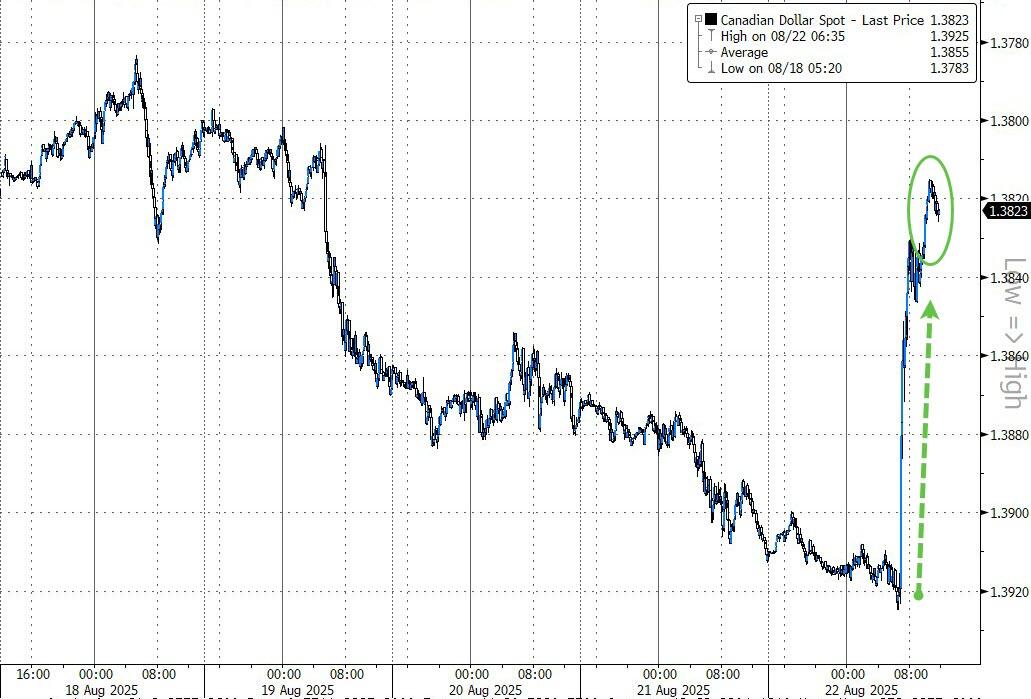

10 YR CANADA BOND YIELD: 3.487UP 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.996 UP 2 PTS

2a New York OPENING REPORT

Futures Rebound Ahead Of Powell’s Speech

Friday, Aug 22, 2025 – 08:35 AM

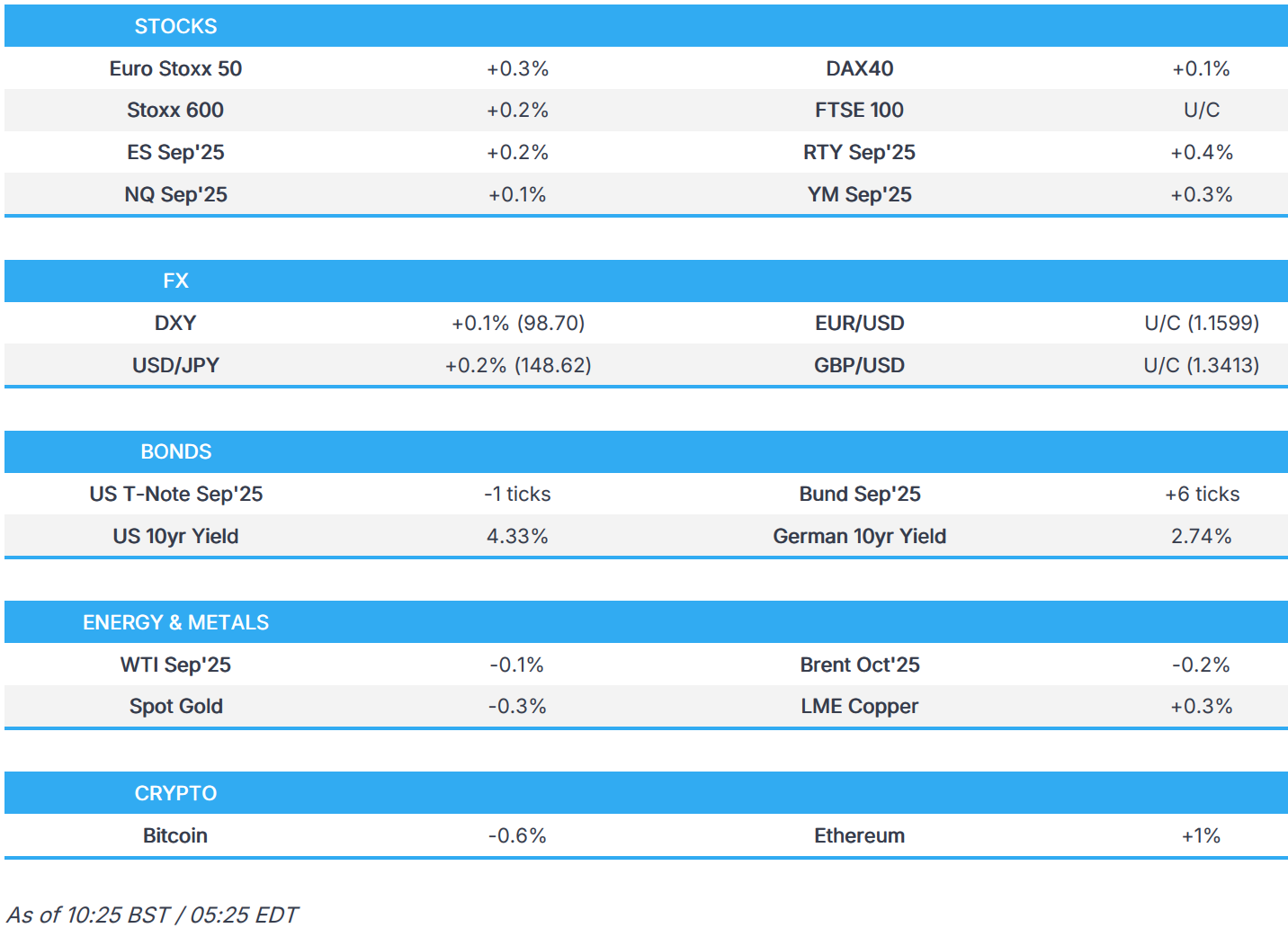

After five days of selling – the longest stretch since Jan 2 – US stock futures halted this week’s run of losses in muted trading ahead of Jerome Powell’s Jackson Hole speech, even as markets scaled back bets on imminent interest rate cuts following very strong economic data on Thursday. As of 8:00am ET, S&P 500 rose 0.2% erasing an earlier decline, while Nasdaq futures rose 0.1% as Nvidia shares fall 1% in premarket after the Information reported the chipmaker had instructed component suppliers to stop production related to the H20 AI chip. European stocks advanced 0.2%, nudging toward an all-time high. US Treasuries held steady after Thursday’s pullback, with the 10-year rate at 4.33%. The dollar was little changed. there are no scheduled events on the US economic data calendar; Fed Chair Powell is set to speak at 10am ET at Jackson Hole with a slew of other central bank comments expected from the event. The Fed speaker slate also includes Boston Fed President Collins at 9am and Cleveland Fed President Hammack at 11:30am; hawkish comments by Hammack on Thursday pushed yields to session highs. Swap contracts linked to future Fed rate decisions fully price in one quarter-point rate cut this year in October and a second one by year-end.

In premarket trading, Nvidia shares fell 1.1% after the chip giant instructed component suppliers including Samsung Electronics and Amkor to stop production related to the H20 AI chip. Other Magnificent Seven stocks were all higher (Alphabet +1.1%, Tesla +0.5%, Apple +0.5%, Microsoft +0.09%, Amazon +0.4%, Meta +0.2%). Here are the other notable premarket movers:

- Biohaven shares (BHVN) gain 13% after the company said the FDA communicated to the company on Aug. 21 that an expected decision regarding the NDA for Troriluzole will still be the fourth quarter.

- Cameco (CCJ) shares rise 1.9% in premarket trading after National Bank Financial raised its price target on the uranium company to C$115 from C$110 as it sees the company’s Westinghouse stake adding value.

- Gap shares (GAP) fall 2.1% in premarket trading on Friday as Barclays downgrades to equal-weight from overweight saying the previous bullish scenario for double-digit operating margins by FY26 is off the table.

- Intuit shares (INTU) decline 6.1% ahead of the bell after the tax software company’s tepid forecast overshadowed an otherwise strong fourth quarter report.

- Ross Stores shares (ROST) rise 2.7% after the retailer posted earnings per share for the second quarter that beat the average analyst estimate after better-than-expected tariff-related costs.

- Workday shares (WDAY) drop 5.1% after the human-resources software company reported second-quarter professional services adjusted gross profit that missed estimates. The company also announced it has agreed to acquire Paradox.

- Zoom Communications shares (ZM) rise 5.0% in premarket trading on Friday after the video conferencing company raised its revenue guidance for the full year, beating the average analyst estimate.

- Trucking stocks might be active on Friday after Secretary of State Marco Rubio said that US will halt issuance of worker visas for commercial truck drivers. Watch: Saia, Old Dominion Freight Line, Knight-Swift Transportation and JB Hunt.

A selloff in big tech this week halted the record-breaking rally in US stocks, ahead of Powell’s latest policy blueprint, which will signal whether the Fed will stay cautious on inflation, which is showing signs of stickiness, or tilt toward supporting a softer labor market. A Bloomberg equal-weighted index of the Mag 7 has dropped 3.4% since Monday, putting it on track for its steepest weekly decline since April’s market rout.

The stakes are heightened by pressure from the Trump administration to cut rates and growing divisions within the Fed’s rate-setting committee. To keep his options open, Powell may emphasize that the Fed’s September move will be guided by employment and inflation figures set for release early next month. Swaps have reduced the odds of aggressive near-term easing, now pricing about a 65% chance of a cut next month and fewer than two moves this year. Little more than a week ago, markets were betting on a full quarter-point cut in September, with some traders even positioning for a half-point move.

Powell is due to speak at 10 a.m. New York time (full preview here). A hawkish speech is expected to weigh on shorter-maturity government bond yields. It could also add pressure to the recent series of large options market trades, which are positioned for an outsized rate cut next month and a total of 75 basis points in reductions by year-end.

“If the Fed doesn’t cut in September, markets will drop because they’re expecting the Fed to do something. If they cut too much, markets may take it as a sign that the Fed is losing its independence, which may trigger much higher inflation,” said Joachim Klement, a strategist at Panmure Liberum. “It’s like Goldilocks with two bears and a bull.”

In Europe, the Stoxx 600 rises 0.2%, led by gains in chemical, health care and auto names. Paper and forestry stocks rise after a report that Suzano will increase pulp prices, while Akzo Nobel gained after activist investor Cevian Capital built a stake in the company. Polish banks plunge after the country’s government announced plans to raise corporate taxes on lenders. Here are the biggest movers Friday:

- Akzo Nobel gains as much 5.4% after activist investor Cevian Capital acquired a 3% stake in the company, putting its weight behind a strategy overhaul at the struggling Dulux paintmaker

- Hensoldt and RENK gain as much as 4.5% and 1.1% after being upgraded to neutral from sell at Citi, with the broker expecting the companies to benefit from Germany’s increased defense spending

- European forestry stocks are rising on Friday after a report that Suzano will increase pulp prices starting in September; Metsa Board shares rise as much as 4.7% and Stora Enso as much as 3.6%

- Standard Chartered gains as much as 3.5% after the US Department of Justice rejected claims by two whistleblowers that it failed to properly investigate allegations of sanctions violations by the bank, the lender said

- Morgan Advanced Materials shares rise as much as 5.1%, the most in more than a month, after the materials and components firm agreed to sell its MMS business unit, including 75% shareholding in MCIL

- Polish banks are among the worst performers in Europe on Friday morning after the country’s Finance Ministry announced plans to raise corporate taxes on lenders to help ease pressure on a strained budget

- Dino Polska shares drop as much as 8.4%, briefly hitting their lowest level in over four months, after the Polish supermarket chain reported results below expectations for the second quarter, according to analysts

- Aspen shares slide as much as 16% in Johannesburg, to its lowest intraday level since April 2020, after the pharmaceutical company said it expects its full-year normalized headline EPS to come in below analyst expectations

- Deutsche Post shares fall as much as 1.5% after Kepler Cheuvreux lowered its recommendation to hold from buy saying the firm will struggle to achieve its Ebit guidance of more than €6 billion

Earlier in the session, Asian stocks crept higher, as a rally in Chinese and South Korean shares helped offset losses in Taiwan and India. The MSCI Asia Pacific Index gained 0.1%, with TSMC among the biggest drags while Tencent supported the regional benchmark. Equities in South Korea gained ahead of President Lee Jae Myung’s visit to Japan. Vietnam’s main equity gauge dropped 2.5%, and Australian shares also fell. A measure of onshore Chinese stocks recorded its biggest weekly rise since November. Gains in local chipmakers provided an added tailwind Friday after a report that US rival Nvidia has instructed component makers to stop production related to its H20 AI chips. Shares also advanced in Hong Kong. Next week will see central bank policy decisions in South Korea and the Philippines.

In FX, the Dollar extended yesterday’s gains overnight and is marginally outperforming across most of the G10 complex as NY sits down. The Norwegian krone is the weakest of the G-10 currencies, falling 0.3% against the greenback. The yen also weakens 0.2%. The Dollar index continued to rally overnight, now at its highest point in two weeks. USDJPY is up 21bps to ~148.75 after Japan’s national CPI data for Jul came in cooler than expectations at +3.1% on headline. And the EUR is mostly unchanged on the day, with mixed signals overnight from data (German Q2 GDP contracted but eurozone wages are up 4% YoY). No major data releases in the US today; all eyes are on Fed Chair Powell at 10AM as well as other speakers at the Jackson Hole Economic Symposium.

In rates, treasuries inch lower, with US 10-year yields rising 1 bp to 4.34%. The 2-year yield is now at the highest level since the beginning of the month at 3.80%, as inflation and price data curbed cuts priced into the next few meetings. There is little price action in USTs overnight after yesterday’s sell-off as the market awaits Powell’s speech later this morning. Yesterday, we saw 3bps of cuts priced out of the September meeting, down to a 70% chance of a 25bps cut at the meeting. Gilts underperform, pushing UK 10-year borrowing costs up 3 bps to 4.76% despite today’s UK Retails Sales print being delayed until September 5th. JGBs are higher across the curve after inflation data continues to sustain the markets expectations for a rate hike by the BOJ. In terms of flows, we saw two way interest in September FOMC, and flattening of the nominal curve.

In credit, macro credit is opening the final session of the week just a touch firmer in sympathy with equity futures in the green and European CDS index spreads largely flat. Risk continued to trade soft yesterday for the fourth session in a row. CDX HY came a touch under pressure with risk generically offered, while there was further negative gamma buying of CDX IG protection into the spread widening. FM was the most active community in vol yesterday, leaning generally better buyers of IG vol, while HY vol was offered by both FM and RM. All eyes and ears will be on Powell this morning (10am ET) with any hawkish tone expected to put pressure on the front end of the curve and synthetic credit spreads.

In commodities, oil prices are steady, with WTI crude futures near $63.50 a barrel. Spot gold falls $10.

Looking at today’s US calendar, there are no scheduled events. The Fed speaker slate also includes Boston Fed President Collins at 9am and Cleveland Fed President Hammack at 11:30am; hawkish comments by Hammack on Thursday pushed yields to session highs

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.1%

- Russell 2000 mini +0.5%

- Stoxx Europe 600 +0.2%

- DAX little changed, CAC 40 +0.2%

- 10-year Treasury yield +1 basis point at 4.34%

- VIX -0.1 points at 16.53

- Bloomberg Dollar Index little changed at 1211.1

- euro little changed at $1.1598

- WTI crude little changed at $63.48/barrel

Top Overnight News

- Fed officials are reportedly readying to quietly pull back from the signature Flexible Average Inflation Targeting (FAIT) policy innovation announced five years ago in which they focused on the risks brought on by near-zero interest rates and low prices, with officials to abandon that approach as it is now seen as no longer relevant given the backdrop of high and more volatile inflation. According to Nick “Nikileaks” Timiraos noted that Powell is expected to unveil the shift at Jackson Hole on Friday, although changes won’t impact near-term policy decisions and are instead part of the framework the Fed uses to interpret its mandate inflation and employment mandates: WSJ

- Nvidia asked suppliers Samsung and Amkor to stop production related to its H20 AI chip after Beijing urged local firms to avoid using it, The Information reported. CEO Jensen Huang reiterated the processor has no security backdoors. Nvidia shares fell premarket (NVDA -110bps). BBG

- The Trump-Putin Alaska summit followed by the visit of European leaders at the White House were supposed to jump-start momentum to end the Russia-Ukraine war. A week later we are back at the same old stand, as Vladimir Putin is playing familiar tricks and showing no serious interest in a deal. The question is what President Trump will do about it. WSJ

- Elon Musk unsuccessfully tried to enlist Mark Zuckerberg in his unsolicited bid for OpenAI this year. BBG

- Trump said the US is leading the AI race and that AI is the hottest thing in decades.

- Trump’s administration reportedly considers a plan to reallocate USD 2bln in CHIPS Act funding for critical minerals and aims to give Commerce Secretary Lutnick greater oversight of minerals financing decisions, according to Reuters citing sources.

- Rubio said the US is pausing all issuances of worker visas for commercial truck drivers with immediate effect. It was separately reported that President Trump’s administration said it is reviewing all 55mln people with US visas for potential deportable violations, according to AP.

- Austan Goolsbee called the recent spike in services inflation “dangerous,” but hopes it proves a blip. He also said the September meeting will be “live.” Susan Collins told the WSJ a rate cut may be appropriate if labor market weakness outweighs inflation risks. BBG

- The US won’t demand equity stakes from chipmakers including TSMC and Micron, which are expanding in the US, a person familiar said. BBG

- Euro-zone negotiated wages jumped 4% from a year ago, the ECB said, supporting its caution on further reducing interest rates. BBG

- Japan’s national CPI for Jul came in at +3.1% headline (down from +3.3% in June and inline w/the Street) while the core number (ex-food and energy) was flat at +3.4% (also inline w/the Street) BBG

- Germany’s economic output shrank by more than initially estimated in the second quarter, with industry faring worse than expected as U.S. tariffs hurt exports. Germany’s final Q2 GDP report is revised lower from the preliminary reading (now -0.3% vs. the prior -0.1%). WSJ

- Fed’s Collins (2025 voter) signalled an openness for a rate cut as soon as next month amid labor market concerns and flagged that higher tariffs might squeeze consumers’ purchasing power, which could weaken spending. Furthermore, Collins said she expects inflation to continue rising through the end of the year before resuming a decline in 2026, according to a Wall Street Journal article that noted divisions grow inside the Fed ahead of the September rate cut decision and cited Fed’s Hammack (2026 voter) opposing cuts due to rising inflation.

- Fed’s Goolsbee (2025 voter) said the September FOMC meeting is a live meeting and the Fed has been getting mixed messages on the economy, while he added that the most recent inflation data wasn’t great and the Fed still has time to take in more data. Goolsbee responded he doesn’t want to get his hands tied, when asked about a September rate cut, as well as commented that a rise in services inflation is a dangerous data point and reacting to a stagflation shock is very difficult. Furthermore, he said central bank independence is critically important, and that tariff increases don’t seem close to being done and risk persistent inflation.

Trade/Tariffs

- Chinese President Xi is unlikely to attend ASEAN Leaders’ Summit in October, “dashing hopes of a meeting with US President Trump at the summit”; while Premier Li is set to represent China, according to two regional sources cited by Reuters.

- South Korea’s Foreign Minister Cho is expected to meet with US Secretary of State Rubio as early as today before the Trump summit with South Korea President Lee, according to Yonhap. South Korean top security adviser confirms discussions with US on increasing defence spending, citing NATO framework as reference; said US investment and weapons purchases are under review. In talks about nuclear power cooperation with the US.

- South Korean top security adviser confirms discussions with US on increasing defence spending, citing NATO framework as reference; said US investment and weapons purchases are under review.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed amid cautiousness heading into Fed Chair Powell’s remarks at Jackson Hole and following the subdued handover from Wall St, where participants digested a slew of data and mostly hawkish Fed comments. ASX 200 marginally declined with price action choppy around the 9,000 focal point as participants continue to mull over the latest earnings releases. Nikkei 225 swung between gains and losses with participants indecisive after recent yen weakness and somewhat mixed Japanese inflation data, which mostly matched estimates, aside from the slightly hotter-than-expected Core CPI reading. Hang Seng and Shanghai Comp were kept afloat with strength seen following recent earnings releases and with chipmakers supported after Beijing summoned Chinese tech companies to discuss their use of NVIDIA (NVDA) chips and encourage them to use more homegrown options, while NVIDIA ordered a halt to H20 production following China’s directive against purchases.

Top Asian News

- Japan 2026 budget requests to total around JPY 120tln, according to Kyodo.

- China’s Industry Ministry said it has issued interim measures for controlling and managing rare earth mining, smelting, and separation.

- PBoC seeks feedback on draft regulations for interbank FX market.

European stocks (STOXX 600 +0.1%) are little changed, albeit with a positive bias amid a lack of newsflow into Fed Chair Powell’s speech in the European afternoon. A bout of risk aversion, with no specific fundamental driver, was seen pre-cash open. Nonetheless, this did little to inflict sustained pressure on European bourses, which have been edging higher since the lacklustre open. European sectors opened mostly in the red after a quiet open. However, positivity has since dominated across the board as sentiment improved. Chemicals sits at the top, led by Akzo Nobel (+5%), after the FT reported that Activist Cevian acquired a more than 3% (EUR 300ln) stake in the company. Banks also underperform, though they are off their worst levels; this comes after Bloomberg reported that Poland is planning to increase corporate income tax for banks, proposing to increase the tax to 30% from 19%.

Top European News

- German Economy Minister said Q2 GDP figures show “urgent need for action”; Further and courageous reforms are unavoidable to make the German economy competitive.

FX

- DXY is firmer on Friday in the run-up to Fed Chair Powell’s speech at 15:00BST /10:00 EDT, which is expected to see a text release. Attention will focus on whether Chair Powell’s Jackson Hole remarks indicate any shift in views since recent US data and if he signals a September rate cut, which markets price at ~70% probability. DXY trades in a 98.58-98.83 intraday range after finding support at the 50 DMA (at 98.09 today) earlier in the week. Powell aside, there will be commentary from Collins and Hammack.

- Softer in tandem with the firmer Dollar. EUR remains subdued by the diminishing optimism surrounding Russia-Ukraine, in which US President Trump said, “we will know in about two weeks regarding Russia-Ukraine”. Meanwhile, Ukrainian President Zelensky said Russia’s overnight attacks show that Moscow is trying to avoid the need for meetings aimed at ending the war. On the data front, German GDP for Q2 was revised lower across the board, albeit this prompted little EUR move at the time, with eyes turning to Fed Chair Powell’s speech at 15:00 BST for a dollar-induced impulse. EUR/USD currently sits in a 1.1583-1.1668 range.

- Choppy trade overall in which USD/JPY initially extended on Thursday’s advances overnight after returning to the 148.00 territory and was unfazed by the Japanese inflation data, in which Core CPI printed firmer-than-expected. Inflows into the JPY were seen around 15 minutes before the European equity cash open, in tandem with some broader risk aversion despite a lack of fresh catalysts at the time, though it was short-lived. USD/JPY trades in a 148.27-148.77 parameter.

- Not much in the way of Sterling-specific catalysts nor newsflow, with Cable moving in tandem with the Dollar ahead of a long weekend (UK bank holiday on Monday).

- PBoC set USD/CNY mid-point at 7.1321 vs exp. 7.1871 (Prev. 7.1287).

Fixed Income

- USTs are flat and have been trading in a very narrow 111-16 to 111-20 range, as traders await an appearance from Fed Chair Powell at 15:00 BST / 10:00 EDT. On that, focus will be on whether Chair Powell’s Jackson Hole remarks indicate any shift in views since recent US data and if he signals a September rate cut, which markets price at ~70% probability. In terms of price action, currently contained in a minuscule 4 tick range, and within the confines made in the prior session.

- Bunds are also flat/incrementally firmer and trade in a very narrow 128.94 to 129.12 range; the trough today was made in the moments after the release of German GDP revisions, which were lower than the prelim; Q/Q revised down to 0.2% (prev. 0.4%) whilst the Y/Y metric declined 0.3% (prev. no growth).

- Gilts are on the back foot today and underperforming vs peers, albeit within narrow ranges. Nothing really fresh driving things at the moment for UK paper, but perhaps as fiscal-related fears resurge into the Autumn Budget. From a yield perspective, the 10yr has been knocking on the door of the 4.75% mark; traders tout levels above 4.80% as the “danger zone” for Chancellor Reeve’s and her “black hole”.

Commodities

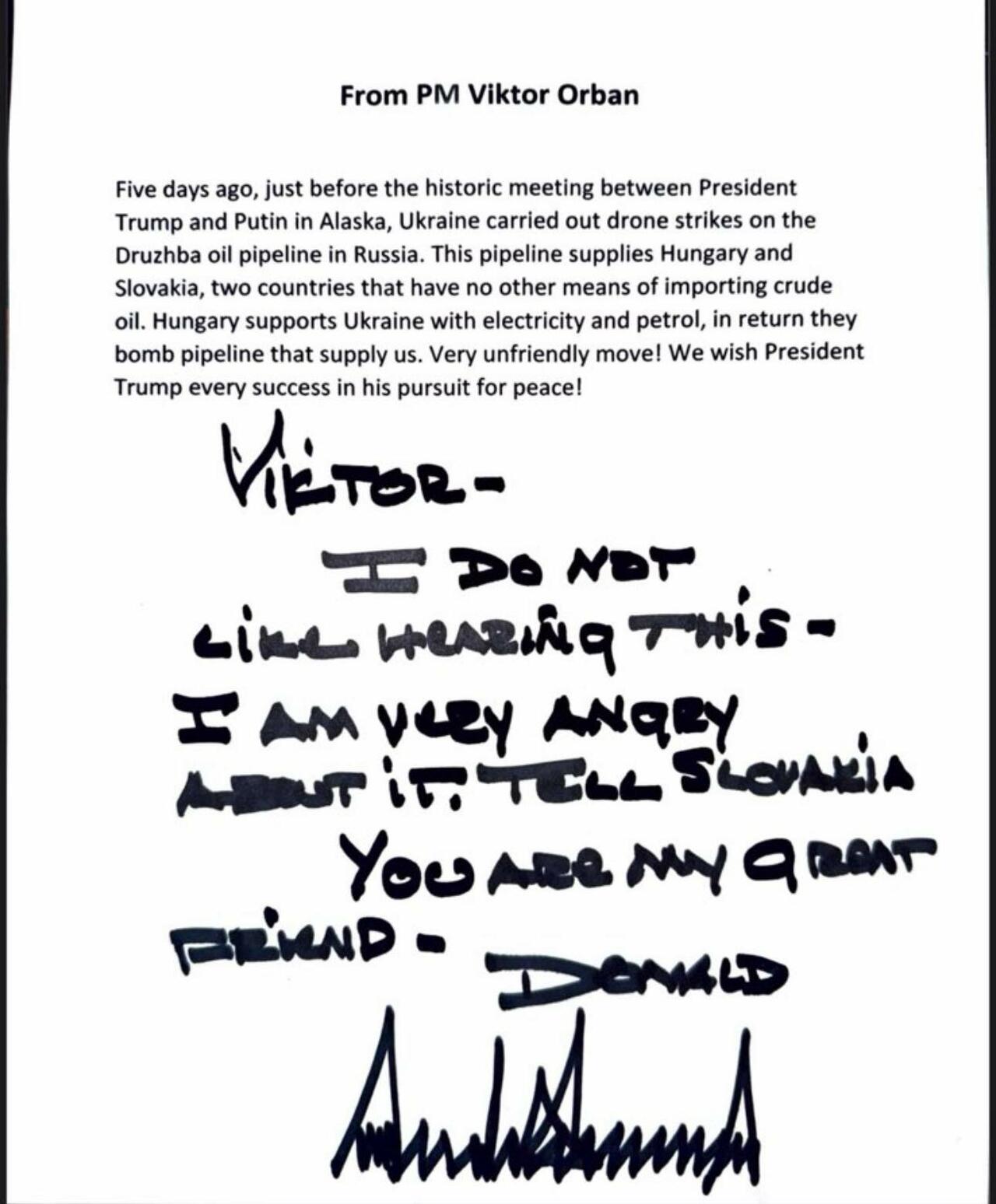

- Modest gains across the crude complex despite the firmer Dollar and alongside the choppy mood across the stock market, with equity bourses swinging from modest losses to mild gains. Upside in the crude complex comes amid diminishing optimism surrounding Russia-Ukraine, in which US President Trump said, “We will know in about two weeks regarding Russia-Ukraine”. Meanwhile, Ukrainian President Zelensky said Russia’s overnight attacks show that Moscow is trying to avoid the need for meetings aimed at ending the war. On that note, the Hungarian Foreign Minister said oil deliveries to Hungary via the Druzhba pipeline have been halted due to attacks near the Russia-Belarus border. Deliveries seem to be suspended for at least five days, according to reports. WTI currently resides in a 62.05-62.68/bbl range while Brent sits in a USD 67.44-67.95/bbl range.