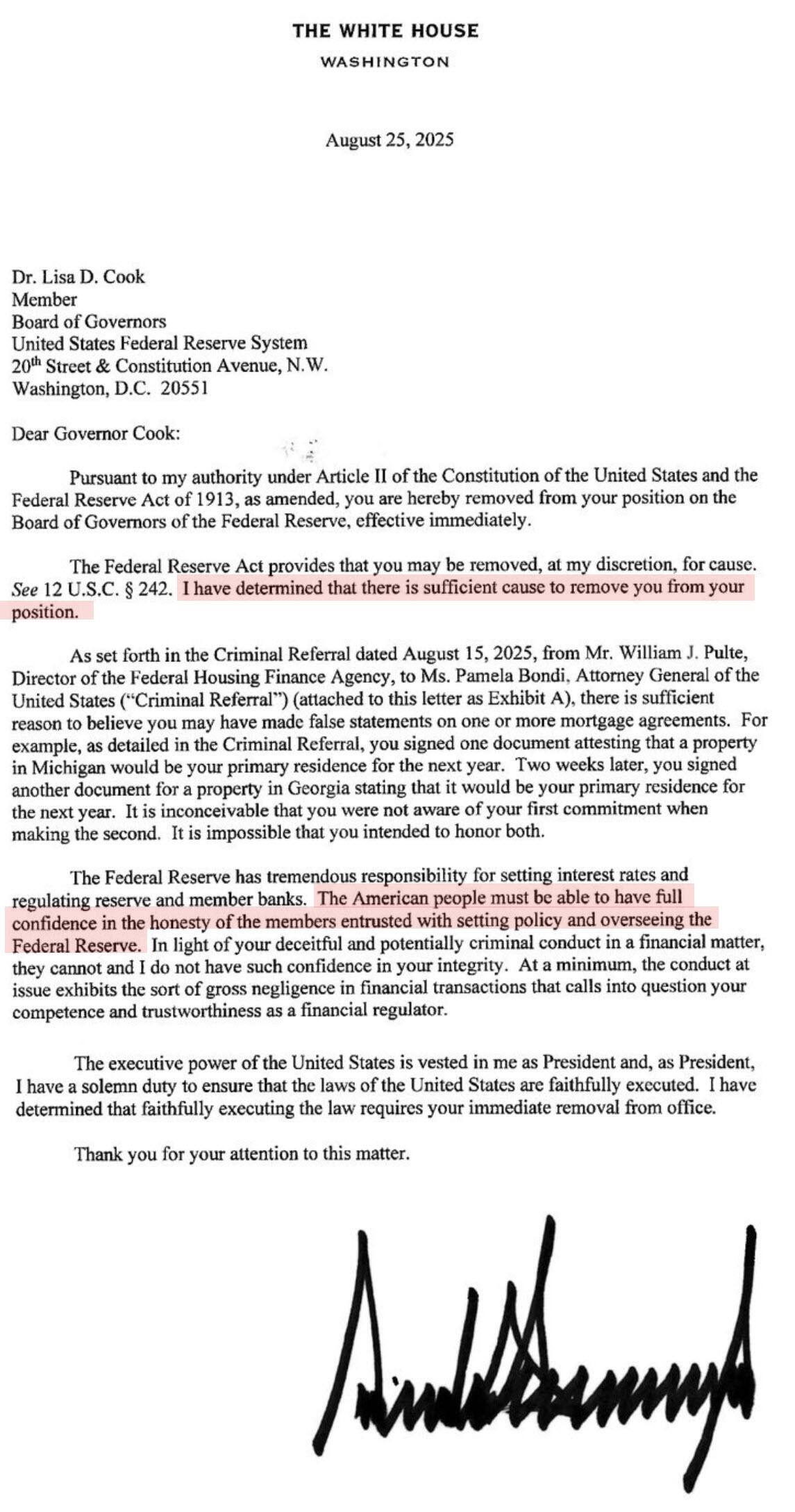

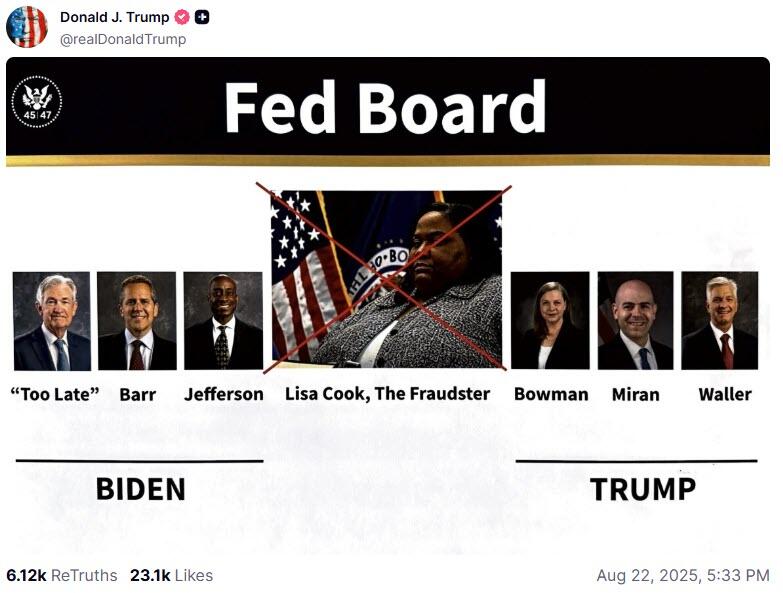

AUGUST 26/COMEX EXPIRY ON GOLD/SILVER CONTRACTS ENDS TODAY//GOLD CLOSED UP $12.15 TO $3384.20 WHILE SILVER WAS DOWN $0.19 TO $38.55//PLATINUM WAS UP $0.90 TO $1346.40 WHILE PALLADIUM WAS FLAT AT $1101.50//GOLD COMMENTARY TONIGHT FROM ALASDAIR MACLEOD/GREG HUNTER INTERVIEWS JOHN RUBINO AND ANOTHER MUST VIEW//ZERO HEDGE COMMENTARY ON THE PLIGHT OF JAPANESE BONDS//EXCELLENT COMMENTARY ON THE HUGE PROBLEMS INSIDE THE FINANCES OF FRANCE//ISRAEL UPDATES TBN ISRAEL//ISRAEL VS HAMAS: ISRAEL HITS NASSAR HOSPITAL WITH 20 DEAD: HOWEVER 6 WERE HAMAS TERRORISTS//RUSSIA VS UKRAINE UPDATES/COVID UPDATES/DR PAUL ALEXANDER/NEWS ADDICTS/EVOL NEWS/RABOBANK COMMENTARY TONIGHT AS WELL AS DR DANIEL LACALLE//USA DATA RELEASES//TRUMP FIRES LISA COOK SETTING UP A SHOWDOWN WITH POWELL: MANY UPDATES ON THIS//SWAMP STORIES FOR YOU TONIGHT//

099 H DEUTSCHE BANK AG 226 118 H MACQUARIE FUTURES US 1 332 H STANDARD CHARTERED B 154 363 H WELLS FARGO SECURITI 303 657 C MORGAN STANLEY 40 657 H MORGAN STANLEY 32 661 C JP MORGAN SECURITIES 9 39 732 C RBC CAP MARKETS 6 905 C ADM 28

TOTAL: 419 419 MONTH TO DATE: 33,538

JPMORGAN stopped 39/419

AUGUST

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2025: 419 CONTRACTs NOTICES FOR 41,900 OZ or 1.303 TONNES

total notices so far: 33,538 contracts for 3,353,800 OR 104.317 tonnes)

FOR AUGUST

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 334 NOTICE(S) FILED FOR 1,670,000 OZ/

total number of notices filed so far this month : 2113 CONTRACTS (NOTICES) for 10.565 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $12.15 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 958.49 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.19 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV:

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 491.546 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE 522 CONTRACTS TO 161,952 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0,28 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE FINALLY ARE MOVING MUCH HIGHER THAN THE BASE $34.40 SILVER PRICE BARRIER. WE HAD A HUGE SIZED GAIN OF 859 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A STRONG 337 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD LITTLE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO MONDAY’S TRADING COUPLED WITH SOME OF OUR MONTHLY SPREADER LIQUIDATION AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $36.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED A BIT ON MONDAY WITH SILVER’S LOSS IN PRICE. THE PRICE HOWEVER FINISHED MILES ABOVE THE MAGIC NUMBER OF $36.00 SILVER SPOT PRICE CLOSING AT $38.74 . WE FINALLY STOPPED HAVING THOSE MEGA MEGA HUGE T.A.S. ISSUANCE BUT STILL WITNESSING LARGE ISSUANCE: AS TODAY’S TOTAL ISSUANCE WAS RECORDED AT A STRONG 391 CONTRACTS. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 38.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A HUGE 337 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG SIZED 391 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THIS WEEK’S TRADING OR BEYOND/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 859 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.28.

EXCHANGE FOR RISK ISSUANCE FOR SILVER/MAY

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS WERE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A HUGE SIZED 391 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.28) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE GAIN OF 859 CONTRACTS ON OUR TWO EXCHANGES WE HAD LITTLE IF ANY T.A.S. SPREADER LIQUIDATION ON MONDAY BUT WE DID HAVE CONSIDERABLE MONTHLY SPREADER LIQUIDATION!

WE HAD A 337 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.70 MILLION OZ FOLLOWED BY TODAY’S 339 CONTRACT QUEUE JUMP OR AN ADDITIONAL 1.695 MILLION OZ WILL STAND FOR PHYSICAL ON THIS SIDE OF THE POND //NEW STANDING ADVANCES AT 10.570 MILLION OZ.

THUS:

INITIAL STANDING FOR AUGUST: 4.90 MILLION OZ FOLLOWED BY TODAY’S 1.695 MILLION OZ QUEUE JUMP//NEW STANDING ADVANCES TO 10.570 MILLION OZ

WE HAD:

/ HUGE COMEX OI GAIN+// A HUGE SIZED EFP ISSUANCE 337 CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 391 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: 128 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 17 DAY(S), total 7446 contracts: OR 37.320 MILLION OZ (438 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 37.320 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 37,320 MILLION OZ (QUITE SMALL)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 522 CONTRACTS DESPITE OUR LOSS IN PRICE OF $0.28 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE 337 CONTRACT EFP ISSUANCE CONTRACTS: 337 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 5 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 1.695 MILLION OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.570 MILLION OZ

THE NEW TAS ISSUANCE MONDAY NIGHT (391) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE IN THIS WEEK’S TRADING.

WE HAD 334 NOTICE(S) FILED TODAY FOR 1.670 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 3572 OI CONTRACTS TO 442,378 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 330 CONTRACTS //.

WE HAD A INCREASE IN COMEX OI (3672 CONTRACTS) . THIS OCCURRED DESPITE OUR LOSS OF $1.05 IN PRICE// MONDAY///.

LAST FOUR MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE MONTH’S QUEUE JUMP OF 46.83 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES AND NOW AUGUST 26: 9.1010 TONNES //NEW STANDING ADVANCES TO 107.377 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS) +23.702 TONNES EX.FOR RISK = 136.079 TONNES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A TINY SIZED 100 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 442,378 /STILL EXTREMELY LOW AND WE NOW WITNESS A LOW COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A LOW COMEX OI OF 160,952 CONTRACTS

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3672 CONTRACTS WITH 3572 CONTRACTS INCREASED AT THE COMEX// AND A TINY SIZED 100 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3672 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 352 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID LIKE LAST THURSDAY WHEN CALLED UPON. GOLD PRICE ON FRIDAY FELL BY $1.05.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A TINY SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(100) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 3572 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3672 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR AUGUST AT 60.547 TONNES FOLLOWED BY THE MONTH’;S 46.83TONNES OF QUEUE JUMPS + OUR INITIAL 5.4432 TONNES EX FOR RISK AUGUST 7 AND SATURDAY’;S AUG 9 2.413 TONNES EX FOR RISK ISSUANCE + WEDNESDAY’S AUGUST 12: 2.637 TONNES AND THEN AUG 25: 9.107 TONNES//AUGUST 26: 9.1010//NEW STANDING ADVANCES TO 136.079 TONNES

NEW STANDING FOR GOLD, AUGUST CONTRACT AT 136.079 TONNES OF GOLD

.

/ 3) ZERO OR LITTLE T.A.S. LIQUIDATION (AND SOME MONTHLY SPREADER LIQUIDATION) AS WE HAD 1)A $1.05 COMEX PRICE LOSS. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG SIZED GAIN OF 3672 CONTRACTS ON OUR TWO EXCHANGES WE HAD ZERO LIQUIDATION OF OUR TAS SPREADERS BUT SOME MONTHLY SPREADER LIQUIDATION/ /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND YOU CAN VISUALIZE THIS BY THE HUGE AMOUNTS OF QUEUE JUMPING WE HAVE BEEN HAVING LATELY ESPECIALLY TODAY’S JUMP OF 1.216 TONNES !!

4) STRONG SIZED COMEX OI GAIN// 5) TINY SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (100 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 352 T.A.S.CONTRACTS/

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST :

TOTAL EFP CONTRACTS ISSUED: 46,513 CONTRACTS OR 4,651,300 OZ OR 144.67 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 2736 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN17 TRADING DAY(S) IN TONNES: 144.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 144.67 TONNES DIVIDED BY 3550 x 100% TONNES = 4.08% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

UNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 144.67 TONNES GETTING A LITTLE LARGER THIS MONTH.

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE 522 CONTRACTS OI TO 160,952 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 337 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 337 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 950 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 522 CONTRACTS AND ADD TO THE 337 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 859 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.28 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.295 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 15.18 PTS OR 0.39%

//Hang Seng CLOSED DOWN 304.99 PTS OR 1.18%

// Nikkei CLOSED DOWN 413.47 PTS OR 0.97% //Australia’s all ordinaries CLOSED DOWN 0.41%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1598 OFFSHORE CLOSED DOWN AT 7.1620/ Oil DOWN TO 64.01 dollars per barrel for WTI and BRENT DOWN TO 68.00 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1598 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1620 AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 3,572 CONTRACTS TO 442,378 OI WITH OUR LOSS IN PRICE OF $1.05 WITH RESPECT TO MONDAY’S // TRADING.. WE OF COURSE, LOST NO NET LONGS, WITH THAT SMALL PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A TINY NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (100). WE HAD LITTLE IF ANY T.A.S. LIQUIDATION //MONDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3672 CONTRACTS (OR 11.421 TONNES).THEN WITH MUCH SHOCK TO ME WE HAD ANOTHER MASSIVE 2,926 CONTRACTS ISSUED FOR EXCHANGE FOR RISK MONDAY FOR 292,600 OZ OR 9.1010 TONNES OF GOLD. EITHER THE FRBNY OR THE BANK OF ENGLAND WERE VERY BUSY THIS MORNING AS THEY NEEDED TO REPLACE THE GOLD THEY LOANED OUT TO BULLION BANKS. THE HIGH NUMBER OF CONTRACTS ISSUED ON EXCHANGE FOR RISK MEANS TIME IS RUNNING OUT FOR ONE OR BOTH OF THEM!@!!!!!

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY:

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST;

EARLY THURSDAY MORNING, AUGUST 7 THE CME ANNOUNCED MUCH TO MY HORROR ITS FIRST EXCHANGE FOR RISK ISSUANCE FOR AUGUST OF A MONSTER 1750 CONTRACTS FOR 175,000 OZ OR (5.4432 TONNES OF GOLD, THIRD HIGHEST ON RECORD!!. WITH ALL THE CHAOS AT THE COMEX IT WAS NO SURPRISE THAT THEY ISSUED THEIR SECOND EXCHANGE FOR RISK, AUG 10 TOTALLING 776 CONTRACTS OR 77,600 OZ (2.418 TONNES).MUCH TO MY ANGER LAST WEEK, THE CME ANNOUNCED ITS 3RD EXCHANGE FOR RISK OF 848 CONTRACTS TOTALLING 84,800 OZ OR 2.637 TONNES.

NOW WE REACH TODAY WERE THE CME ISSUED ITS 4TH EXCHANGE FOR RISK FOR A MASSIVE 2928 CONTRACTS TOTALLING 292800 OZ OR 9.107 TONNES.

THUS THE TOTAL FOR AUGUST IS 6302 CONTRACTS OR 630,200OZ OR 19.6019 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS. THE RECEPIENT OF THIS LARGESS IS PROBABLY NOW THE BANK OF ENGLAND AS WE HAVE JUST LEARNED THAT THE FRBNY HAS RETURNED ONLY 14,000 OZ AS THEIR LOANS TO THE BIS REMAIN AT 34+ TONNES.(JULY 31 FIGURES). BUT IT COULD ALSO BE THE FRBNY AS URGENCY TO RETURN THAT GOLD MAY HAVE BEEN ISSUED BY THE BIS. IT SEEMS NOW THAT EITHER THE BANK OF ENGLAND OR THE FRBY ARE IN QUITE A HURRY TO GET ITS GOLD BACK!! (AND THEY ARE THE PROBABLE OWNERS OF THOSE EXCHANGE FOR RISK CONTRACTS). THIS IS THE HIGHEST EVER MONTHLY RECORDED ISSUANCE OF EXCHANGE FOR RISK!!

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 5 ISSUANCES FOR A MONSTER 9,228 CONTRACTS OR 922,800 OZ ( 28.702 TONNES). YESTERDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY TODAY’S ISSUANCE OF 2926 CONTRACTS THUS BECOMING THE HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BEATING YESTERDAY’S ISSUANCE OF 2924 CONTRACTS.

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//INITIAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 3672 CONTRACTS WITH OUR SMALL LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE , JULY AND NOW AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 352 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST WEEK’S RAID DURING COMEX OPTION EXPIRY WEEK. THE TAS SPREADER LIQUIDATIONS COMBINE AT MONTH END WITH OUR MONTHLY SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED THREE WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH AUGUST MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 46.83 TONNES +28.702 TONNES EX FOR RISK (5 ISSUANCES) //NEW STANDING 136.079 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 237 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE 46.83 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE AND FINALLY TODAY’S MASSIVE 9.1016 TONNES ISSUANCE/NEW STANDING ADVANCES TO 136.079 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A TINY SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A TINY SIZED 100 EFP CONTRACT WAS ISSUED: : /DEC 100 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 100 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

ZERO OR TINY LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY

MONTH END SPREADERS HAVE NOW APPEARED ON THE SCENE DISTORTING OI NUMBERS.

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A SMALL SIZED SIZED 352 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST WEEK ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S SMALL LOSS IN PRICE IN GOLD AND A CORRESPONDING FAIR GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S 5 ISSUANCES OF EXCHANGE FOR RISK FOR 28.702 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 1.216TONNES TO WHICH WE ADD OUR 5 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK

28.702 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.377 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

EQUALS

136.079 TONNES TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/AUGUST CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A SMALL $1.05/ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD LITTLE IF ANY T.A.S. SPREADER LIQUIDATION (SAVING IT TODAY, TUESDAY) AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE LONGS PILING IT ON TRYING TO OBTAIN BADLY NEEDED GOLD///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH THIS WEEK’S TRADING!! GENERALLY WE WITNESS GOLD HAVING A STRONG DAY WHEN WE WITNESS THESE EXCHANGE FOR RISK ISSUANCES.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FEBRUARY IS THE SECOND HIGHEST ISSUANCE OF EXCHANGE FOR RISK AS AUGUST BECOMES THE HIGHEST EVER RECORDED AS YOU WILL SEE BELOW!

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRIL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE:

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: FIVE SO FAR,

TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 29.702 TONNES, THE HIGHEST EVER COMEX ISSUANCE!

THUS 107.377 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS) + 28.702 TONNES = 136.079 TONNES.

ANALYSIS AUGUST DELIVERY MONTH GOING FROM FIRST DAY NOTICE// AUGUST COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 39.56 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST FIRST RECORDED AT 60.547 TONNES ON FIRST DAY NOTICETO WHICH WE TODAY;S QUEUE JUMP OF 1.216 TO OUR MONTHLY QUEUE JUMPS OF 46.83// TOTAL MONTH OF AUGUST QUEUE JUMPS: 46.83 TONNES

TO WHICH WE THEN ADD OUR 5 EXCHANGE FOR RISK FOR 28.702 TONNES FOR RISK//NEW STANDING ADVANCES TO 136.079 TONNES

ALL OF THIS HUGE STANDING FOR AUGUST WAS ACCOMPLISHED WITH OUR SMALL LOSS IN PRICE TO THE TUNE OF $1.05

WE HAD 330 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 2672 CONTRACTS OR 267200 0Z (11.421 TONNES)

confirmed volume MONDAY 107,537 contracts// very weak//everybody vacating the comex???

i) out of Asahi 3954.573 oz (123 kilobars) ii) out of Brinks 385.82 oz (12 kilobares)

total withdrawal 4340.393 oz

.

Deposit to the Dealer Inventory in oz

0 ENTRY

Deposits to the Customer Inventory, in oz

DEPOSITS/CUSTOMER

1 ENTRY

i) Into International Delaware: 19,290.600 oz (6000 kilobars)

total weight: 19,290.600 oz

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

419 notice(s) 41,900 OZ 1.303 TONNES

No of oz to be served (notices)

984 contracts 98400 OZ 3.060 TONNES

Total monthly oz gold served (contracts) so far this month

33,538 notices 3,353,800 oz 104.317 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits:

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRY

i) Into International Delaware: 19,290.600 oz (6000 kilobars)

total weight: 19,290.600 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

2 entries

i) out of Asahi 3954.573 oz (123 kilobars) ii) out of Brinks 385.82 oz (12 kilobares)

total withdrawal 4340.393 o

adjustments:

i) Brinks 3086.390 oz

96 kilobars

AMOUNT OF GOLD STANDING FOR AUGUST

THE FRONT MONTH OF AUGUST STANDS AT 1318 CONTRACTS FOR A GAIN OF 385 CONTRACTS

WE HAD 6 CONTRACTS SERVED ON MONDAY SO WE GAINED A STRONG SIZED 391 CONTRACTS OR 39,100 OZ OF GOLD (1.216 TONNES) EXERCISED A QUEUE JUMP AS THEY WERE WILLING TO STAND FOR PHYSICAL METAL ON THIS SIDE OF THE POND.. THIS ALSO REPRESENTS CENTRAL BANKS STANDING FOR PHYSICAL GOLD AND THEIR APPETITE FOR THIS GOLD IS UNABATED!

SEPT LOST 328 CONTRACTS TO 3580. SEPTEMBER BECOMES THE FRONT MONTH STANDING FOR GOLD

OCTOBER GAINED 399 CONTRACTS UP TO 60,177

We had 419 contracts filed for today representing 41900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 9 notices issued from their client or customer account. The total of all issuance by all participants equate to 419 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 39 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2025. contract month, we take the total number of notices filed so far for the month (33,538 X 100 oz ) to which we add the difference between the open interest for the front month of AUGUST ( 1318 CONTRACTS) minus the number of notices served upon today (419 x 100 oz per contract) equals 3,452,200 OZ OR 107.377 TONNES TO WHICH WE ADD OUR FIVE ISSUANCES OF 28.702 TONNES OF EXCHANGE FOR RISK/AUG 7 , 11 12TH 25TH AND 26TH AUG// = 136.079 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (33,538 x 100 oz +we add the difference for front month of AUGUST (1318 OI} minus the number of notices served upon today (419 x 100 oz) which equals 3,452,200 OZ OR 107.377 TONNES + 28.702 TONNES EX FOR RISK = 136.079 TONNES

TOTAL COMEX GOLD STANDING FOR AUGUST.: 125.499TONNES WHICH IS A MONSTER FOR THIS NORMALLY ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. AND THIS RUNS COUNTER INTUATIVE TO OUR CONSTANT RAIDING THIS WEEK

TOTAL REGISTERED SILVER: 191.098 MILLION OZ//.TOTAL REG + ELIGIBLE. 508.778 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF AUGUST /2025 OI: 337 OPEN INTEREST CONTRACTS FOR A GAIN OF 337 CONTRACTS. WE HAD 2 CONTRACTS SERVED ON MONDAY SO WE GAINED 339 CONTRACTS OR AN ADDITIONAL 1.695 MILLION OZ WILL STAND AT THE COMEX HAVING UNDERGONE A MASSIVE QUEUE JUMP AS THESE GUYS ARE STANDING FOR DELIVERY OVER ON THIS SIDE OF THE POND.

SEPTEMBER LOST 7783 CONTRACTS DOWN TO 37,000 CONTRACTS. SEPT BECOMES THE FRONT MONTH FOR DELIVERY IN SILVER AND WE HAVE 3 MORE READING DAYS BEFORE FIRST DAY NOTICE!

OCTOBER GAINED 190 CONTRACTS TO 1630

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 334 or 1.670 MILLION oz

CONFIRMED volume; ON TUESDAY 69,587 good//

AND NOW AUGUST DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 2113 X5,000 oz = 10.565 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST (337) AND the number of notices served upon today (334 )x (5000 oz)

Thus the standings for silver for the AUGUST 2025 contract month: (2113) Notices served so far) x 5000 oz + OI for the front month of AUGUST(337) minus number of notices served upon today (334)x 5000 oz equals silver standing for the AUGUST contract month equating to 10.570 MILLION OZ .

New total standing: 10.570 million oz which is pretty good for this NON active delivery month of AUGUST. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 191.098 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/508.778 million. 41.27%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

GLD INVENTORY: 958.49 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 25 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

In recent decades, China which ranks fifth in global silver reserves has not only mined 3,500—4,000 tonnes annually but imported large quantities of silver doré for refining as well. Less well known is the Peoples Bank’s role in managing silver reserves, which many people in China still regard as a monetary metal. China was on a silver standard only ninety years ago.

Today, gold is the principal monetary metal, and silver is widely regarded as industrial only. But since 1983, along with gold the PBOC has been responsible for overseeing the accumulation of the nation’s silver bullion reserves. The key to this policy has been price management. This article shows how this was achieved.

Introduction

About twelve ago, I was speaking in New York at a conference attended by about a dozen silver mining and exploration companies. At that time, conspiracy theories about JPMorgan’s dealings in the silver market were rife. But when Blythe Masters, then Head of Global Commodities at JPMorgan went on CNBC, she made JPMorgan’s position clear:

“Speculation is [rife] particularly in the blogosphere about this topic and I think the challenge is that speculation represents a misunderstanding as the nature of our business. As I mentioned earlier our business is a client driven business where we execute on behalf of clients to achieve their financial and risk management objectives. The challenge is that commentators don’t see all of that activity simultaneously. So just to give you a simple example we store significant amounts of commodities, for example silver on behalf of customers. We operate vaults in New York City, in Singapore, and in London. And often when customers have that metal stored in our facilities, they hedge it on a forward basis through JPMorgan who in turn hedges itself in the commodity markets. If you see only the hedges and our activity in the futures market, but you aren’t aware of the underlying client position then hedging it would suggest inaccurately that we’re running a large directional position. In fact, that’s not the case at all. We have offsetting positions. We have no stake in whether prices rise or decline. Rather, we’re running a flat or a relatively neutral… [interviewer interrupts]”[i]

Silver bulls rushed to condemn her, calling her a liar and worse. But I was convinced that a senior executive of her undoubted ability and in her position would be telling the truth. Furthermore, I suspected that Masters did the CNBC interview specifically to quash the wild rumours about JPMorgan’s silver dealing rather than ignore them.

So, what was JPMorgan’s true role in the market? Clearly, it was intermediating for clients and not taking one-sided positions on its own book. As Masters revealed, the bank only took out derivative positions to hedge their dealings with clients.

The conference in New York gave me a chance to dig a little deeper. I asked the dozen or so silver companies present the process of how they turned their silver at the mine into cash to pay their costs. They all said that the process started with an assessment of the silver doré’s value by a specialist assessor, usually from Glencore, who then arranged for payment and shipment to a refiner. None of the miners admitted they knew where the doré was shipped to for refining — it was no longer their concern. But the common assumption was probably China.

Glencore is a huge commodity trader acting for large mining corporations as well as the smaller miners I interviewed. They obviously worked with a major bank on the payments side, which is where JPMorgan would come into the picture. As soon as the doré was shipped, the cashflow-hungry miner would be paid on the assessor’s valuation by JPMorgan. Likely, it would be shipped FOB Origin, which means the doré enters Chinese possession at the point of shipment.

Presumably, China (which would have been the PBOC) instructed JPMorgan to hedge the silver price on Comex or London, timed to suppress the price. Note that this is not JPMorgan acting as principal but acting for the Chinese as a client.

As well as being a large miner herself, China was refining considerable amounts of imported doré when some western refineries were closing down on environmental and cost grounds. So, the hedging book through JPMorgan would have been significant enough to manage the price. We can take this even further, in the context of a normal dealer/client relationship. As dealer and client work together, an element of dealing discretion can be given to the dealer along with dealing objectives.

So what might those objectives be?

As a major buyer of doré, it would have been in China’s interests to keep the price as low as possible. And shorting derivatives would have been the means for China to accumulate substantial silver reserves for monetary purposes, which she had already done with gold.

In this context, the original 1983 Regulations on the Control of Gold and Silver appointing the Peoples Bank of China states:

Article 4. The People’s Bank of China shall be the State organ responsible for the control of gold and silver in the People’s Republic of China.

The People’s Bank of China shall be responsible for the control of the State’s gold and silver reserves; responsible for the purchase and sale of gold and silver; work in conjunction with the authority responsible for commodity prices to formulate and administer a purchase and sales price for gold and silver [my emphasis]

Note the PBOC’s responsibility for controlling the price of silver.

We know or should know that in the period 1983—2002 when the Shanghai Gold Exchange finally came into existence under the control of the PBOC, that the PBOC was able to secretly accumulate vast quantities of gold which was in a substantial bear market fuelled by American and European financial communities liquidating their bullion holdings in favour of dollars. I believe that during this period China secretly acquired as much as 20,000 tonnes, hidden by being spread round various state bodies.

These easy conditions for accumulating gold were not generally true for stockpiling silver in the far larger quantities required, reflected in the price relationship between the two monetary metals. The PBOC had to use different tactics. The practical way to accumulate massive quantities of silver was to become the world’s refiner and manage the price — in other words keep it suppressed principally by selling as a covered bear in paper markets.

Blythe Masters had no need to lie about JPMorgan’s role in this. Between Glencore and China as its customers, JPMorgan would be central to achieving the outcome China desired.

There is another aspect to this puzzle rarely mentioned. Note, that under Article 4 of the Regulations appointing the PBOC that no distinction is made between gold and silver. For the purposes of the regulations, silver is as much money as gold, a reserve to be controlled by the central bank as general backing for the currency.

It should be remembered that China was on a silver standard as recently as 1935. Ordinary people accumulated silver as wealth and banks kept reserves in silver. For the Chinese population, silver was their money as much as gold was in the west. There is every reason why silver should be singled out in the Regulations to have the same status as gold.

Will China continue to suppress prices? Those days are probably over. Almost certainly, China has accumulated substantial silver reserves, more than enough for a supporting monetary role to gold. The state’s monetary silver reserves are likely to be segregated from industrial production, which has become an uncontrollable source of demand.

Clearly, the PBOC understands the role of monetary metals, which is ultimately to secure the value of credit. They know that gold and silver values are generally stable, and that it is credit which declines. Their very public disposal of dollars for gold tells us that they are no longer suppressing prices of gold. What goes for gold must also apply to their policy regarding silver.

END

THIS IS VERY IMPORTANT!!

The Mar-a-Lago Accord Confirmed: Miran Brings Trump’s Reset To The Fed

[ZH: This was written before Trump fired Fed Governor Cook, potentially further entrenching his appointees on the Fed Board]

Stephen Miran’s appointment to the Federal Reserve isn’t just another personnel move—it’s the placement of Trump’s Reset architect inside the very institution that will help carry out America’s most ambitious economic overhaul in generations.

If you’re still unfamiliar with what Trump’s Reset entails, I strongly recommend checking out Matt Smith’s comprehensive analysis. He’s done the heavy lifting of connecting dots that were only hinted at in Miran’s original white paper.

Without getting into the weeds, Miran, the mastermind behind what’s been dubbed the “Mar-a-Lago Accord,” outlined a comprehensive plan to flip the U.S. dollar’s reserve status from a burden into a bargaining chip. To turn America’s towering debt from an embarrassment into leverage. And to reorient the entire global economic structure in Washington’s favor.

And of course, what makes this especially relevant right now—particularly for anyone with gold exposure—is the timing.

The yellow metal has been on a relentless march higher throughout 2025, setting multiple all-time highs and blasting past $3,400 an ounce just last month. Now, with Miran’s appointment to the Fed, we’re seeing exactly why smart money has been quietly accumulating the yellow metal all year.

But anyone thinking Miran’s appointment is simply about giving Trump another dovish vote for rate cuts is missing the much bigger picture. Gold isn’t just rising because of anticipated rate cuts. It’s been rising because informed investors recognized what Trump’s Reset strategy would eventually require: the systematic weakening of dollar dominance and a potential gold revaluation.

Again, I urge you to check out Matt’s report if you’re unclear on the specifics—he’s laid out the relationships and implications more clearly than anyone I’ve seen attempt it.

The upshot is that Miran’s appointment is simply the latest confirmation that this plan is moving from theory into practice. (And once you see what that implies for both the dollar and gold, it’s easier to understand why $3,400 gold may be only the beginning.)

Miran’s Fed Position Is a Game-Changer

I don’t want to sound like a broken record, but I can’t stress this enough.

This isn’t just about securing another dovish vote for rate cuts—Trump could have picked any yes-man for that. It’s about placing the architect of America’s monetary reset directly inside the Federal Reserve.

You see, the Fed doesn’t set tariffs, negotiate trade deals, or sign defense pacts—but it does control the single most important lever in Trump’s Reset: the cost and flow of money.

From his position as Fed governor, Miran will have a permanent vote on the Federal Open Market Committee (FOMC), giving him direct influence over interest rates, money supply, and crucially, the Fed’s balance sheet operations. But more importantly, he’ll be positioned to coordinate monetary policy with the broader Reset strategy he designed.

Think about what this means in practical terms—and from Trump’s perspective. The Reset strategy involves coordinated dollar devaluation—but that requires the Fed to be on board. You can’t orchestrate a Plaza Accord (more on it below)-style currency adjustment if your central bank is fighting you every step of the way. With Miran inside the Fed, Trump gets someone who understands both the macroeconomic theory behind dollar devaluation and the practical mechanics of how to execute it through monetary policy.

Note: The U.S. dollar has already weakened more than 10% over the past six months. To put it in perspective, the last time the dollar fell this much early in the year was 1973—right after the U.S. finalized its break from gold and the fiat era fully took hold.

Miran’s appointment also signals something even more significant: the institutional capture of monetary policy. When Jerome Powell’s term expires in May 2026, Fed chairs are typically chosen from among existing governors. By installing Miran now, Trump is positioning his Reset architect to potentially lead the entire Federal Reserve system.

In short, it’s Trump making sure the Fed itself becomes a primary tool for carrying out his Reset. And there’s a very deliberate reason for that.

Trump’s Reset Needs the Fed on Side

Now, I brought up the Plaza Accord above because it’s the closest historical precedent to what we’re calling Trump’s Monetary Reset (or the Mar-a-Lago Accord).

You’ve probably heard of it.

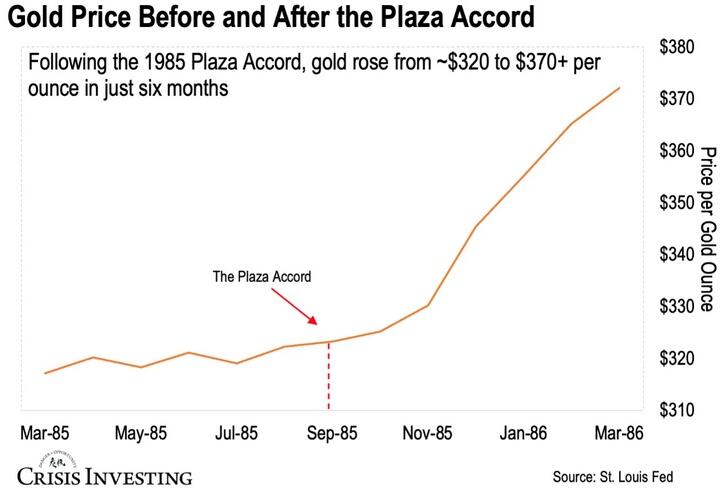

On September 22, 1985, finance ministers from the world’s largest economies gathered at New York’s Plaza Hotel to coordinate a devaluation of the unnaturally strong U.S. dollar.

Naturally, outside the U.S., no one wanted a weaker dollar—it would make their exports pricier for American buyers. But, just like today, Washington applied pressure with tariffs, import surcharges, quotas, and pointed accusations of “unfair trade.”

And guess what? It worked. West Germany and Japan—the economic powerhouses of the day—caved.

But here’s what made the Plaza Accord actually work: the Federal Reserve was fully on board. Fed Chairman Paul Volcker coordinated closely with Treasury Secretary James Baker to ensure monetary policy backed the dollar devaluation strategy. He cut interest rates from roughly 12% to 6% between late 1984 and late 1986, creating the conditions for the dollar to fall. Without that cooperation, the Plaza Accord probably would have been just another piece of paper.

This is exactly why Miran’s appointment is so crucial. Trump learned from Reagan’s playbook—to execute coordinated currency devaluation, you better make sure your central bank is pulling in the same direction. By installing the Reset architect inside the Fed, Trump ensures that monetary policy will align with, rather than undermine, his broader economic strategy.

And what happened to gold in the wake of the Plaza Accord?

It surged. Take a look at the chart below.

After the Plaza Accord in 1985, gold jumped from about $320 per ounce to over $370 between September 1985 and March 1986. That’s in just six months.

Adjusted for today’s prices, that would be like seeing gold leap to roughly $4,000 an ounce.

But here’s the thing… If Trump’s Reset unfolds the way Matt and I believe it will, it won’t just be a repeat of the Plaza Accord—it’ll be that on steroids.

In today’s globalized and overleveraged economy, the ripple effects could be enormous. I wouldn’t be surprised to see gold surge to $5,000–$8,000 per ounce as markets scramble to adapt.

* * *

Stephen Miran’s arrival at the Fed isn’t just a policy shift—it’s confirmation that Trump’s Reset strategy is already moving from blueprint to reality. The implications for the dollar, gold, and your personal wealth are enormous. We’ve been tracking the signs of this coming shift for months—the hidden gold run out of London, the quiet buildup of reserves, and now the placement of Trump’s Reset architect inside the Federal Reserve itself. If you’ve been wondering what all this means for your money—and how to prepare before the Reset accelerates—I strongly urge you to read our latest deep-dive: Get Ready for Trump’s Monetary Reset. Inside, you’ll see why central banks are scrambling for gold, how Trump’s team plans to “monetize America’s balance sheet,” and why we believe this could unleash the biggest wealth revaluation in half a century. Most importantly, you’ll learn the practical steps you can take right now to protect your savings—and position yourself to potentially profit. Click here to get the full story before the Reset leaves you behind.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 237

5. COMMODITY REPORT.LUMBER

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 15.18 PTS OR 0.39%

//Hang Seng CLOSED DOWN 304.99 PTS OR 1.18%

// Nikkei CLOSED DOWN 413.47 PTS OR 0.97% //Australia’s all ordinaries CLOSED DOWN 0.41%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1598 OFFSHORE CLOSED DOWN AT 7.1620/ Oil DOWN TO 64.01 dollars per barrel for WTI and BRENT DOWN TO 68.00 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1598 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1620 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1596

OFFSHORE YUAN: DOWN TO 7.1620

HANG SENG CLOSED DOWN 304.99 PTS OR 0.48%

2. Nikkei closed DOWN 413.47 PTS OR 0.97%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 98.25 EURO RISES TO 1.1626 UP 12 BASIS PTS