FROM MY no 4 SON STEPHEN //THROUGH AI: ENJOY

I made a different version on X:

118 C MACQUARIE FUTURES US 13

118 H MACQUARIE FUTURES US 141

190 H BMO CAPITAL MARKETS 97

323 C HSBC 1409

332 H STANDARD CHARTERED B 140

363 H WELLS FARGO SECURITI 307

435 H SCOTIA CAPITAL (USA) 147

624 H BOFA SECURITIES 203

657 H MORGAN STANLEY 193

661 C JP MORGAN SECURITIES 563 1362

690 C ABN AMRO CLR USA LLC 8

709 C BARCLAYS 2

732 C RBC CAP MARKETS 371

905 C ADM 14 2

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 2456 CONTRACTs NOTICES FOR 245,600 OZ or 7.702 TONNES

total notices so far: 2486 contracts for 248,600 OR 7 tonnes)

SILVER NOTICES: 7702 NOTICE(S) FILED FOR 38.510 OZ/

total number of notices filed so far this month : 7702 CONTRACTS (NOTICES) for 38.510 million oz

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 54.080 MILLION OZ (QUITE SMALL)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 49.825 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 166.34 TONNES GETTING A LOT LARGER THIS MONTH.

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE 1844 CONTRACTS OI TO 156,057 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1025 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1025 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 950 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1844 CONTRACTS AND ADD TO THE 1025 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 2869 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.48 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 14.345 MILLION PAPER OZ

OCCURRED WITH OUR $0.48 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

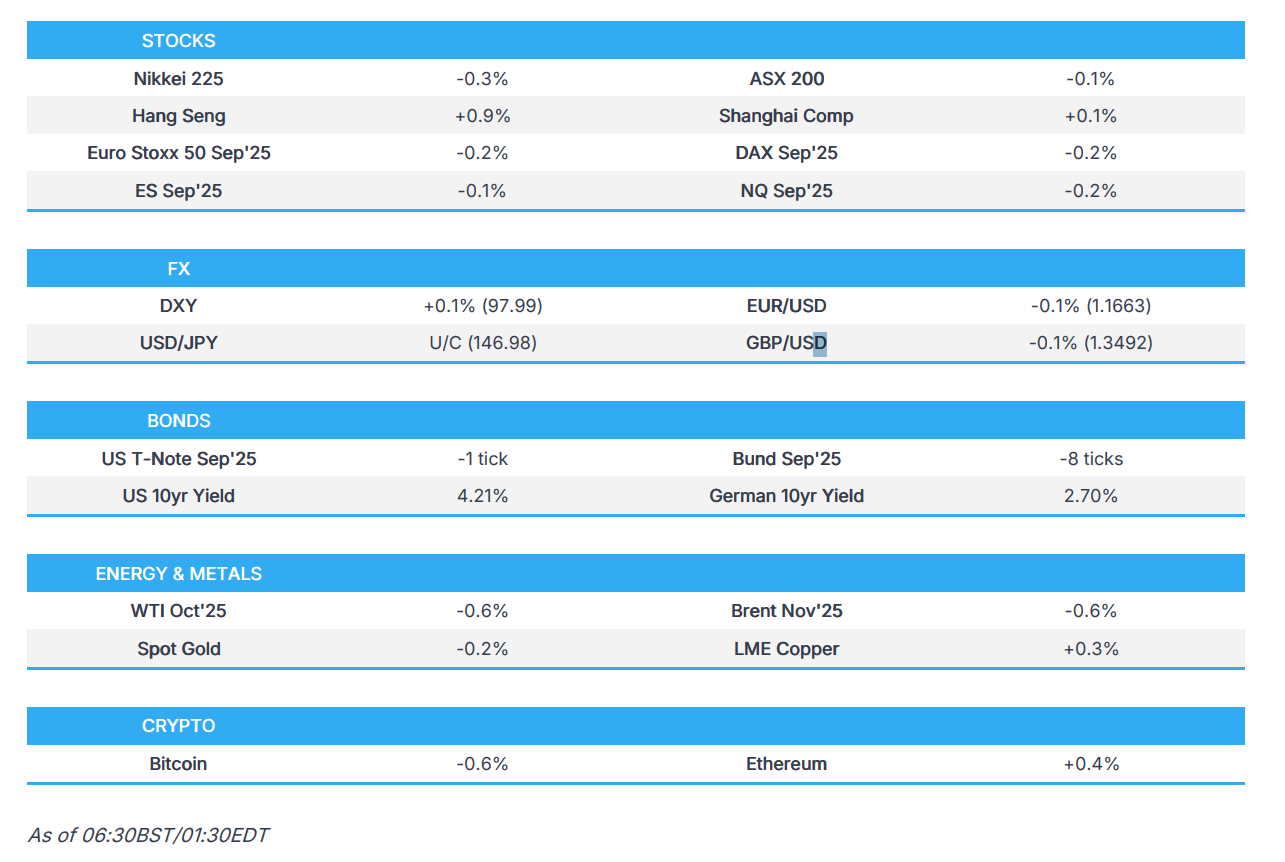

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 14.23 PTS OR 0.37%

//Hang Seng CLOSED UP 222.58 PTS OR 0.89%

// Nikkei CLOSED DOWN 110.32 PTS OR 0.20% //Australia’s all ordinaries CLOSED UP 0.02%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1339 OFFSHORE CLOSED UP AT 7.1297/ Oil UP TO 64.14 dollars per barrel for WTI and BRENT UP TO 67.52 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1339 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1297 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7310 CONTRACTS TO 456,226 OI WITH OUR STRONG GAIN IN PRICE OF $18.20 WITH RESPECT TO THURSDAY’S // TRADING.. WE OF COURSE, LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1382). WE HAD ZERO T.A.S. LIQUIDATION BUT CONSIDERABLE MONTH END SPREADER LIQUIDATION //THURSDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 8692 CONTRACTS (OR 27.035 TONNES).THEN WE NOTIFIED THAT WE HAD 0 EXCHANGE FOR RISK ENDING THE STREAK OF 4 CONSECUTIVE ISSUANCES

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES THESE PAST THREE MONTHS;

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW WEDNESDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: NONE FOR FAR

HISTORY: LAST SEVEN MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW YESTERDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: 0 ISSUED SO FAR!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 7TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH AUGUST.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//FINAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 7,310 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH AUGUST CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 2102 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST MONTH’S RAID DURING COMEX OPTION EXPIRY WEEK FOR JULY. THE TAS SPREADER LIQUIDATIONS COMBINE WITH MONTH END AUGUST SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED 4 WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY AND THEY WILL TRY AGAIN WITH RAIDS FINALIZATION OF AUGUST OPTIONS EXPIRY WEEK ENDS TODAY.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH AUGUST MONTH END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES. HOWEVER JUNE WHICH IS NORMALLY A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

AND NOW FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; 2602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 237 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAVE A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1382 EFP CONTRACT WAS ISSUED: : /DEC 1382 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1382 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO OR TINY LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY

- MONTH END SPREADERS HAVE NOW APPEARED ON THE SCENE DISTORTING OI NUMBERS. HOWEVER STILL NOT IN FULL FORCE YET

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A FAIR SIZED SIZED 1382 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S STRONG GAIN IN PRICE IN GOLD AND A CORRESPONDING STRONG GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY) AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

STANDING FOR GOLD LAST 7 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT: 8.093 TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2025:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING/ENDING AUGUST CONTRACT MONTH AND NOW BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A STRONG $18.20/ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION (PROBABLY SAVING FOR TODAY, FRIDAY) AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE LONGS PILING IT ON TRYING TO OBTAIN BADLY NEEDED GOLD///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH THIS WEEK’S TRADING!!

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

DETAIL SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH AUGUST TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FEBRUARY IS THE SECOND HIGHEST ISSUANCE OF EXCHANGE FOR RISK AS AUGUST BECOMES THE HIGHEST EVER RECORDED AS YOU WILL SEE BELOW!

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRIL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE: 3

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: 7 ISSUED,

TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 44.696 TONNES, THE HIGHEST MONTHLY EVER COMEX ISSUANCE!!!!!!

THUS 107.5117 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS/EX FOR PHYS TRANSFERS) + 44.696 TONNES EX FOR RISK = 152.208 TONNES.

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 27.035 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNESS

SEPT; 0 ISSUED SO FAR!

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED WITH OUR STRONG GAIN IN PRICE TO THE TUNE OF $18.20

WE HAD 9790 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 8692 CONTRACTS OR 869,200 0Z (27.035 TONNES)

confirmed volume THURSDAY 173,462 contracts// weak//everybody vacating the comex???

speculators have left the gold arena

END

INITIAL GOLD COMEX

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

AUGUST 29 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entries . |

| Deposit to the Dealer Inventory in oz | 1 ENTRIES i) Into Asahi dealer 17,843.805 505 KILOBARS total deposit dealer 17,843.805 oz .505 tonnes |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRIES i) Into manfra: 143,372.456 oz (4.45 tonnes of real gold) total deposit: 143,372.456 oz 4.45 tonnes total weight dealer and customer acct 5.000 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 2486 notice(s) 248600 OZ 7.732 TONNES |

| No of oz to be served (notices) | 116 contracts 11,600 OZ 0.360 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2486 notices 248,600 oz 7.732 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1 entries

1 ENTRIES

i) Into Asahi dealer 17,843.805

505 KILOBARS

total deposit dealer 17,843.805 oz

.505 tonnes

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRIES

i) Into manfra: 143,372.456 oz

(4.45 tonnes of real gold)

total deposit: 143,372.456 oz

4.45 tonnes

total weight dealer and customer acct

5.000 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

adjustments: 1

i) Brinks dealer to customer acct: 31,415.272 0z

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 2602 CONTRACTS FOR A LOSS OF 140 CONTRACTS

THUS BY DEFINITION, THE INITIAL AMOUNT OF GOLD STANDING FOR THIS NON ACTIVE DELIVERY MONTH OF SEPTEMBER IS AS FOLLOWS;

2602 NOTICES X 100 OZ PER NOTICE

EQUALS

260,200 OZ OR 8.093 TONNES OF GOLD. I THOUGHT WE WOULD HAVE 7 TONNES STANDING SO WE HAD A LITTLE BETTER SHOWING!

OCTOBER GAINED 1256 CONTRACTS UP TO 57,465

We had 2486 contracts filed for today representing 248,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 593 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 2486 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (2486 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 2602 CONTRACTS) minus the number of notices served upon today (2486 x 100 oz per contract) equals 248,600 OZ OR 8.093 TONNES OF GOLD

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (2486 x 100 oz +we add the difference for front month of SEPT. 2602 OI} minus the number of notices served upon today (2486 x 100 oz) which equals 248,600 OZ OR 8.093 TONNES

TOTAL COMEX GOLD STANDING FOR SEPT..: 8.093 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,068,470.784 oz 64.34 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,925,852.749 oz

TOTAL REGISTERED GOLD 21,426,967.559 or 666.46 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,498,885.190 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,365,161 oz ((REG GOLD- PLEDGED GOLD)= 602.33 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

AUGUST 29 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries: i) Out of Delaware 2121.150 oz ii) Out of HSBC 150,054.400 oz iii) Out of Loomis 50,604.250 oz total withdrawal: 202,779.800 oz |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into the dealer Asahi; 39,426.800 oz total deposit 39,426.800 oz |

| Deposits to the Customer Inventory | 2 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into CNT 601,503.060 oz ii) Into Loomis 599,434.440 oz total deposit 1,200,937.500 oz |

| No of oz served today (contracts) | 7702 CONTRACT(S) (38.510 million OZ |

| No of oz to be served (notices) | 2263 contracts (11.315 MILLION oz) |

| Total monthly oz silver served (contracts) | 7002 Contracts (38.510 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

1 deposit into dealer accounts

i) Into the dealer Asahi; 39,426.800 oz

total deposit 39,426.800 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into CNT 601,503.060 oz

ii) Into Loomis 599,434.440 oz

total deposit 1,200,937.500 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 entries:

i) Out of Delaware 2121.150 oz

ii) Out of HSBC 150,054.400 oz

iii) Out of Loomis 50,604.250 oz

total withdrawal: 202,779.800 oz

ADJUSTMENTs 2

a) CNT customer to dealer account of CNT 2,934,838.68 oz

b) Manfra: dealer to customer account; 56,366.570 oz

TOTAL REGISTERED SILVER: 199.957 MILLION OZ//.TOTAL REG + ELIGIBLE. 518.232 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 9965 OPEN INTEREST CONTRACTS FOR A LOSS OF 3266 CONTRACTS. THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING IN THIS VERY ACTIVE DELIVERY MONTH OF SEPTEMBER IS AS FOLLOWS:

9965 NOTICES XX 5000 OZ PER NOTICE

EQUALS

49.825 MILLION OZ OF SILVER STANDING. I EXPECTED AROUND 40 MILLLION OZ TO STAND SO AGAIN WE HAD A PRETTY GOOD SHOWING FOR SEPTEMBER.

OCTOBER GAINED 151 CONTRACTS TO 2016

NOVEMBER GAINED 25 CONTRACTS UP TO 914.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:7702 or 38.50 MILLION oz

CONFIRMED volume; ON THURSDAY 65,453 fair//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 7702 X5,000 oz = 38.510 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (9965) AND the number of notices served upon today (7702 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (7702) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(9965) minus number of notices served upon today (7702)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 49.825 MILLION OZ .

New total standing: 49.825 million oz which is pretty good for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 199.937 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/518.232 million. 40.61%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 967.94 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

GLD INVENTORY: 967.94 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

CLOSING INVENTORY 492.954 MILLION OZ//

PHYSICAL GOLD/SILVE

1/ PETER SCHIFF/S

PETER SCHIFF

JOHN RUBINO

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

Preparing for liftoff!

Gold and silver are ready to break into new highs as investors increasing lose faith in the dollar. Bear squeezes in gold and silver are now driving prices, which look set to move higher.

| Alasdair MacleodAug 29∙Paid |

For decades, the expansion of artificial supply in the form of paper derivatives has been used to keep gold and silver prices subdued. Could it be that it is beginning to be reversed, as gold leasing declines, and the shortage of physical supply particularly of silver begin to bite? And could this be compounded as evidence mounts of debt traps being sprung on G7 governments in the major currencies, leading to an escalating loss of faith in their values?

Gold and silver were both firm over the week, with gold in European trade this morning at $3410, up $40 on the week, and silver at $38.95 was barely changed. Prices this week peaked yesterday, but opening levels this morning were only marginally lower. Comex volumes in gold were subdued, but higher in silver.

Perversely, open interest in silver has declined, while the price rose. This is illustrated next:

Clearly, the shorts are being squeezed and are being forced to reduce their exposure to a market which the financial consensus is beginning to suspect is underpriced. For example, through its central bank a Saudi wealth fund invested $40m in silver and silver mining ETFs recently. And only this week the US Department of the Interior has included silver in its latest draft list of critical minerals, which is likely to confirm buying by financial institutions.

These developments are indicative of changing institutional sentiment towards silver, realising the greater danger is to be short instead of long.

Silver’s multiyear high of $39.30 only a month ago should not prove to be an obstacle to higher prices. The problem for the paper shorts is that in the face of rising physical demand there is little chance of them closing their positions. Liquidity is drying up at a time when momentum traders are likely to start buying futures and forwards. While the shorts will be reluctant to do so, the only solution open to them is to bite the bullet and let prices rise to a point where liquidity returns. This is confirmed by the bullishness of silver’s technical chart:

Adding to the silver shorts’ misery is the position in gold. As with silver, there is a developing squeeze on Comex futures:

In this case open interest collapsed as gold began to make new highs back in April, falling to oversold levels and barely recovering since. At the same time, gold has stubbornly refused to correct lower, indicating strong and persistent support in a pattern best illustrated in the technical chart which is repeated here:

This flat-topped pennant is a very bullish pattern, indicating rising support taking out profit-takers and leaving the market short of sellers. When it breaks above its supply line at $3440, experience of pennant patterns tells us that that the price will rise quickly to mirror the move in as a minimum objective — in this case $900+, possibly by the year end.

Again, we can see the difficulties this is already causing Comex and London. Recent up-days have been during their trading sessions, while prices have tended to pause in Asia overnight. Quietly, as well as central banks and sovereign wealth funds some big funds are beginning to accumulate bullion. Gold stand for deliveries on Comex so far this year are 878.3 tonnes, and net investment in physical ETFs is becoming consistent, albeit still at subdued levels. But when momentum traders get hold of this contract there can be no doubt about prices moving far higher.

The economic conditions driving gold, silver, and also other commodities have become obvious to an increasingly wide audience this week. The persistent increases in term debt yields are drawing attention to the political impossibility in all G7 nations of reducing budget deficits, while their economies stall. These are the conditions when debt traps lead to far higher interest rates and bond yields, destabilising the entire fiat currency system.

With respect to the dollar, Trump is applying enormous political pressure on the Fed to reduce interest rates and is on record demanding a lower dollar. So far, the foreign holders of some $40 trillion do not appear to have taken these threats seriously. As they return from their summer breaks, that is likely to change.

In conclusion, my last chart is of the dollar’s TWI. Which is leading the other major currencies lower:

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 238

5. COMMODITY REPORT GOLD

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 14.23 PTS OR 0.37%

//Hang Seng CLOSED UP 222.58 PTS OR 0.89%

// Nikkei CLOSED DOWN 110.32 PTS OR 0.20% //Australia’s all ordinaries CLOSED UP 0.02%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1339 OFFSHORE CLOSED UP AT 7.1297/ Oil UP TO 64.14 dollars per barrel for WTI and BRENT UP TO 67.52 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1339 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1297 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1339

OFFSHORE YUAN: UP TO 7.1296

HANG SENG CLOSED UP 222.58 PTS OR 0.89%

2. Nikkei closed DOWN 110.32 PTS OR 0.20%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 98.10 EURO FALLS TO 1.1665 DOWN 13 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.608//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.15…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7080 Italian 10 Yr bond yield UP to 3.586 SPAIN 10 YR BOND YIELD UP TO 3.307

3i Greek 10 year bond yield DOWN TO 3.413

3j Gold at $3408.75 Silver at: 38.85 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND33 /100 roubles/dollar; ROUBLE AT 80.63

3m oil (WTI) into the 63 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.15/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.608% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8017 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9353 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.216 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.892 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.623 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.15

10 YR UK BOND YIELD: 4.7170 DOWN 1 PTS

10 YR CANADA BOND YIELD: 3.428 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.943 DOWN 2 PTS

2a New York OPENING REPORT

Futures Drop Led By Tech Ahead Of PCE Data

Friday, Aug 29, 2025 – 08:29 AM

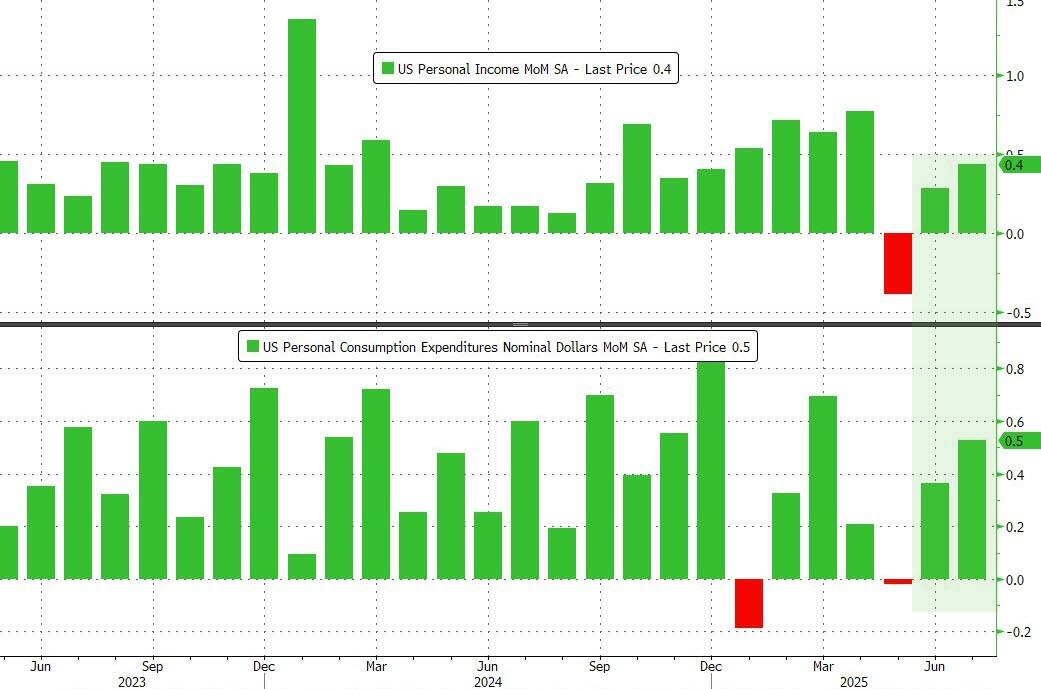

US equity futures are lower after closing at a new all time high, dragged by tech stocks as traders cut risk ahead of today’s core PCE data that may test expectations for the pace of Fed rate cuts. As of 8:00am ET, S&P futures are down 0.3% and Nasdaq futures fell 0.5%: in premarket trading, Alphabet dropped 1.2% leading losses among the Magnificent Seven giants; Nvidia shares extended their premarket decline to over 1%, after the Wall Street Journal reported Alibaba had created a new AI chip. Dell slumped more than 6% after reporting slower sales of artificial intelligence servers. Europe’s Stoxx 600 also dropped 0.4% while bond markets weakened across the board amid ongoing political turmoil in France. US Treasuries fell, with the yield on 30-year notes rising three basis points to 4.90% while the dollar gained 0.2%, putting it on track to snap a run of three weekly losses. Attention today will be on the July personal income/spending which includes the Fed’s favorite core PCE data; we also get the advance goods trade balance and wholesale inventories (8:30am), August MNI Chicago PMI (9:45am, several minutes earlier to subscribers), August final University of Michigan sentiment (10am) and Kansas City Fed services activity (11am).

In premarket trading, Mag 7 stocks: are all lower (Microsoft -0.1%, Alphabet -1%, Apple -0.2%, Amazon -0.3%, Meta Platforms -0.6%, Tesla -0.4%, Nvidia -0.9%).

- Affirm Holdings (AFRM) climbs 15% after the financial technology company reported fourth-quarter results that beat expectations and gave an outlook that is seen as strong.

- Alibaba Group ADRs (BABA) rise 3% after the company reported a surge in revenue from China’s AI boom, helping offset a surprise drop in profit tied to a worsening battle with Meituan and JD.com Inc. in internet commerce.

- Ambarella (AMBA) jumps 18% after the US semiconductor device maker beat revenue and EPS estimates and increased its fiscal 2026 revenue growth estimate. Analysts note strong AI momentum.

- Caterpillar (CAT) falls 3% after the industrial giant warned that it faces a larger-than-anticipated tariff headwind of as much as $1.8 billion this year.

- Celsius Holdings Inc. (CELH) rises 9% after PepsiCo Inc. increased its stake in the energy-drink maker.

- Dell Technologies Inc. (DELL) falls 6% after the company booked fewer sales of artificial intelligence servers than in the previous three months and reported profit margins that fell short of analysts’ estimates.

- Elastic (ESTC) rises 16% after the software company reported first-quarter results that beat expectations and raised its full-year forecast.

- Marvell Technology (MRVL) falls 13% after reporting data center revenue for the second quarter that missed the average analyst estimate.

- NeoGenomics (NEO) rises 4% after saying a US district court ruled in its favor, invalidating all of Natera’s asserted patent claims and clearing the way for broader commercialization of its RaDaR ST assay.

- Petco (WOOF) jumps 22% after the US pet food maker gave 3Q guidance that topped expectations and nudged up its outlook for 2026.

- SentinelOne (S) gains 8% after the software company raised its revenue forecast for the year. Analysts note that results were boosted by strong annual recurring revenues.

- Ulta Beauty (ULTA) climbs 3% after the cosmetics retailer boosted its comparable sales forecast for the full year.

Friday’s stock market weakness casts a shadow heading into what is historically the toughest month for US equities. The S&P 500 has declined in September 56% of the time, with an average drop of 1.17%, according to Bank of America’s Paul Ciana, citing data back to 1927.

“Some profit-taking is healthy as the AI theme has been playing out for some time,” said François Rimeu, senior strategist at Credit Mutuel Asset Management in Paris. As for economic data, “if the labor market is really heating up, then that could lead to some repricing.”

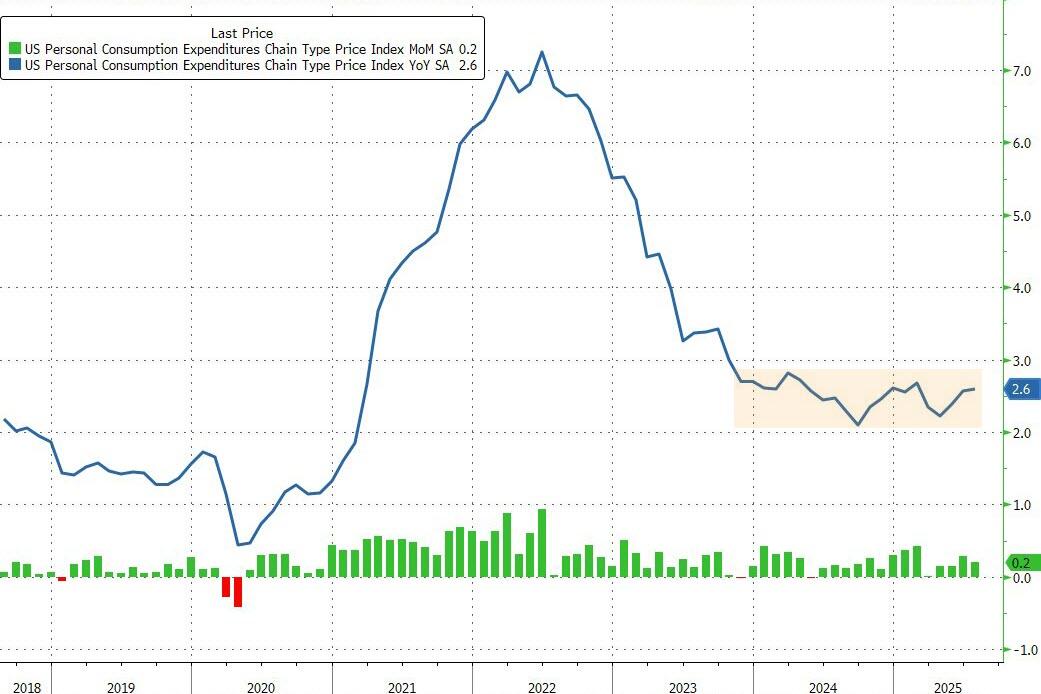

Friday’s personal consumption expenditures report comes a week after Fed Chair Jerome Powell’s dovish tilt at Jackson Hole bolstered bets on the first rate cut of the year next month. Still, doubts linger over what follows that move, with inflation stuck above target. Swaps are pricing two quarter-point cuts this year and another two by June. The report is expected to show core PCE, the Fed’s preferred gauge for tracking inflation, rising 2.9% in July from the year before, the fastest pace in five months. Policymakers will have to balance higher price pressures with data next week that’s expected to show a rise in unemployment.

European stocks extend losses, as the Stoxx 600 drops 0.4% hitting its lowest level in over two weeks with financial stocks leading losses. All 20 sectors are in the red. UK banks dropped after a think tank said Chancellor of the Exchequer Rachel Reeves could raise billions of pounds of revenue through a windfall tax on commercial banks. Defense stocks advanced after German Chancellor Friedrich Merz said a meeting between the Russian and Ukrainian presidents is unlikely to happen. Here are the biggest movers Friday:

- European defense stocks are rising on Friday after German Chancellor Friedrich Merz said a meeting between the Russian and Ukrainian presidents is unlikely to happen

- Lotus Bakeries shares rise as much as 6.5% as BofA upgrades its rating on the maker of Biscoff cookies to buy from neutral with a €10,500 target price, and adds the stock to its SMID cap Europe Best Ideas list

- Brunello Cucinelli shares rise to the highest in about a month after the luxury fashion company reported strong operating income for the first half-year. Analysts foresee limited tariff risk

- Schaeffler gains as much as 4.5%, climbing to the highest since June 2024, as Citi upgrades to buy from neutral ahead of the automotive supplier’s forthcoming capital markets day

- UK bank stocks slide after a think tank says Chancellor of the Exchequer Rachel Reeves could raise billions of pounds of revenue by imposing a windfall tax on commercial lenders

- Ayvens drops as much as 3.7% on a downgrade to neutral at Citi, which now sees a fairly balanced risk-reward for the car leasing company following a strong rally in the shares over the past year

- CD Projekt drop as much as 3.4% as mounting development costs and uncertainty on timeline of forthcoming productions cast shadow on 2Q earnings beat

- Pernod Ricard shares drop as much as 4.3% after analysts poured cold water on the optimism stemming from the spirit maker’s earnings beat on Thursday

- Elekta shares drop as much as 6.2%, reversing earlier gains, after the firm reported first-quarter results. Citigroup analysts flagged the lack of order growth acceleration, while Barclays noted revenue will be under pressure in the second quarter

Earlier in the session, Asian stocks traded little changed, with a rally in Chinese equities offset by losses in Japan amid profit taking. The MSCI Asia Pacific Index edged 0.1% lower, with Contemporary Amperex Technology and Suzhou TFC Optical Communication among the biggest gainers. China Taiping Insurance Holdings was among the laggards after its lackluster earnings. Chinese stocks continued to march higher, partly as investor sentiment stayed high ahead of a military parade on Sept. 3 to mark the 80th anniversary of the end of World War II. Meantime, optimism around solid state batteries also supported gains in the broad market. Shares of CATL, a Chinese battery maker, soared on revenue hopes following an earnings report from a supplier. China’s onshore benchmark CSI 300 Index rose 0.7% to its highest level since 2022. The Hang Seng China Enterprises Index advanced as much as 1.3%. Elsewhere, Japanese stocks fell on profit-taking before the release of personal-consumption-expenditure data in the US. Selling spread across a broad range of sectors, hitting exporters such as makers of electronics and cars, as well as banks and insurers.

In FX, the Bloomberg Dollar Spot Index rises 0.1%. The pound is the weakest of the G-10 currencies, falling 0.4% against the greenback. Currency traders are also pointing to the potential for further dollar weakness next month, particularly as Trump escalates his attacks on the Fed into uncharted territory. The greenback is poised to resume its streak of monthly losses after posting a gain in July, its first of the year.

“There are long-term implications from the US administration’s recent actions,” wrote Jayati Bharadwaj, head of FX strategy at TD Securities. “This chips away at the USD’s safe haven status.”

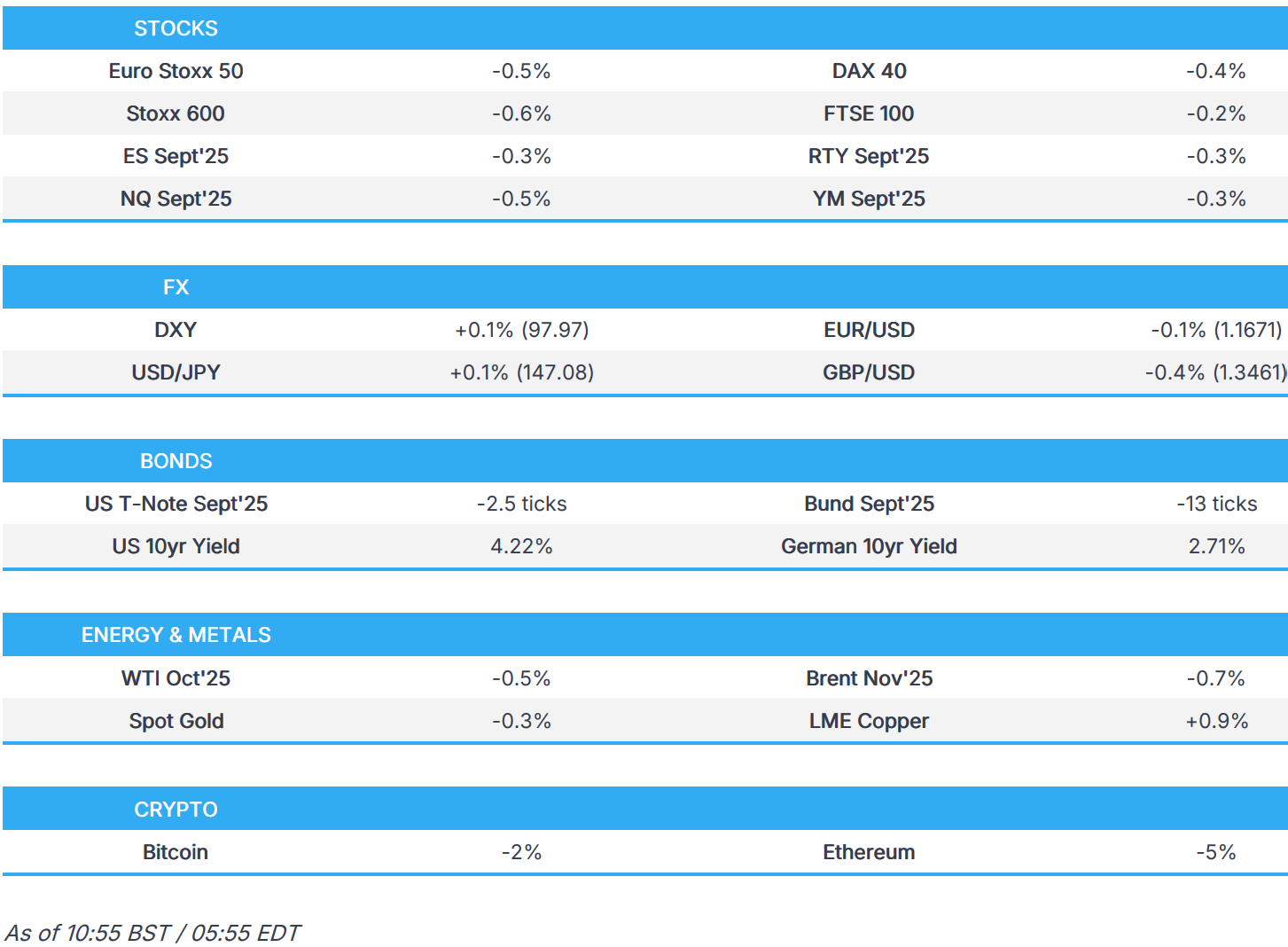

In rates, treasuries slip, with longer-dated maturities leading the slide, and 10-year yields rising 2 bps to 4.22%. European government bonds also fall, though Bunds didn’t show much immediate reaction to mixed regional euro-area inflation data.

In commodities, spot gold is down $10. WTI crude futures drop 0.5% to near $64.30 a barrel. Bitcoin falls 2% and below $110,000.

Today’s economic data slate includes July personal income/spending (including PCE price indexes), advance goods trade balance and wholesale inventories (8:30am), August MNI Chicago PMI (9:45am, several minutes earlier to subscribers), August final University of Michigan sentiment (10am) and Kansas City Fed services activity (11am). Fed speaker slate empty for the session. The first hearing in Lisa Cook’s lawsuit against Trump is set for 10am ET.

Market Snapshot

- S&P 500 mini -0.3%

- Nasdaq 100 mini -0.5%

- Russell 2000 mini -0.3%

- Stoxx Europe 600 -0.6%

- DAX -0.6%, CAC 40 -0.6%

- 10-year Treasury yield +2 basis points at 4.23%

- VIX +0.2 points at 14.61

- Bloomberg Dollar Index +0.1% at 1202.63

- euro little changed at $1.1679

- WTI crude -0.8% at $64.1/barrel

Top Overnight News

- FHFA Director Pulte sent a new criminal referral against Fed’s Cook

- The Trump administration plans to expand national-security tariffs on steel, aluminum and a variety of other industries in coming months in hopes of redirecting production in these sectors to the U.S. and thwarting potential legal threats in the trade war. WSJ

- The EU must be prepared to walk away from a trade deal with the US if Trump acts on his threats to target the bloc unless it waters down its digital legislation, Brussels’ competition tsar Teres Ribera said. FT

- The Fed’s Christopher Waller again said he would support a quarter-point rate cut next month and signaled more easing over the next three to six months. Waller said he does not believe a bigger September cut is needed unless the August jobs report shows substantial weakening and inflation stays well contained, while Waller added that he wanted a rate cut in July and feels more strongly about it now. BBG

- US VP Vance said interest rates are too high and the Fed is not doing its job: Fox News

- Russian oil exports to India are set to rise further in Sept as New Delhi defies the White House. RTRS

- Alibaba posted a 3% drop in operating profit after an escalating price-based battle with Meituan and JD.com hurt margins. Separately, Alibaba developed a new chip compatible with the Nvidia platform, meaning engineers can repurpose programs they wrote for Nvidia chips. BBG

- Tokyo’s inflation rate excluding fresh food slowed to 2.5% in August as expected, but remained above the BOJ’s target. The unemployment rate unexpectedly fell. BBG

- Vladimir Putin will meet Xi Jinping and Narendra Modi at a summit in Tianjin, China, this weekend to discuss energy ties. BBG

- CPIs from France, Italy, and Spain come in a bit cooler than anticipated in Aug at +0.8% Y/Y, +1.7%, and +2.7% Y/Y, respectively, although German regional CPIs accelerated in Aug vs. Jul. WSJ

- U.S. companies have an unwelcome message for inflation-weary consumers: Prices are going up. Companies from Hormel to Ace Hardware forecast prices rising as the costs of Trump’s tariffs are passed on to consumers. Inflation has eased in recent months, but job growth has also slowed, and there are signs shoppers worry that tariffs could further increase prices. WSJ

- HFs have aggressively net bought EM stocks so far in August, led by Chinese equities, EM EMEA, and to a lesser extent Taiwan, while EM Latin America has seen little net activity. Despite this month’s large net buying, Net allocation in Chinese equities does not look extended and is inline with 5-year average. Goldman Prime

Trade/Tariffs

- Canada does not expect US President Trump to drop all his tariffs on the country, according to officials cited by FT.

- Brazil’s Vice President Alckmin said they plan to end negotiations for a complementary trade agreement with Mexico next June and plan to sign a complementary trade agreement with Mexico in August 2026.

- Japanese trade negotiator Akazawa said he will visit the US as soon as necessary arrangements have been made, while he added that he may need to visit the US at least one more time before a presidential executive order is issued.

- Indian Trade Minister says India is to look to new markets, including Australia; India is considering steps to boost domestic demand and support exporters hit by unilateral action by a country; India is taking steps to diversify exports.

- China increases soybean purchases from Argentina and Uruguay due to ongoing US trade tensions, according to Reuters sources; says China has yet to book US soybean imports for Q4

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were ultimately mixed heading into month-end and as participants digested a slew of data and earnings. ASX 200 traded rangebound as strength in tech and energy was offset by losses in real estate, healthcare, industrials and financials, while stock headlines in Australia continued to be dominated by a busy earnings slate. Nikkei 225 weakened after a slew of data releases, which were ultimately mixed, although Industrial Production and Retail Sales disappointed. Hang Seng and Shanghai Comp gained following another substantial liquidity injection by the PBoC of around CNY 783bln and with Beijing authorities recently vowing support measures, while the spotlight is also on incoming earnings, including from Alibaba and Chinese banks.

Top Asian News

- China state planner spokesperson said they are aware that household consumption capability and confidence need to be improved, and aware that company competition has intensified. The spokesperson added that China will study further increasing support from the central government to reduce funding pressure for local governments for people’s livelihood projects and will investigate dumping cases, misleading promotions, and improve governance of disorderly competition. Furthermore, China is to push for reducing R&D costs for AI innovation and will innovate methods to subsidise AI product purchases.

- Chinese Foreign Minister Wang Yi held a phone call with Brazil’s Foreign Minister and said China is willing to strengthen strategic mutual trust with Brazil and strengthen mutual support, while he added that China is willing to strengthen coordination with Brazil and work with BRICS countries to resist unilateralism and bullying.

- Industrial and Commercial Bank (1398 HK) H1 (CNY): Net Income 168.1bln (prev. 171.1bln Y/Y), NII 313.6bln (prev. 314bln Y/Y).

- Agricultural Bank of China (601288 CN) H1 (CNY): net 139.94bln (+2.7% Y/Y), net fee income 51.44bln.

- Bank of Communications (3328 HK) H1 (CNY): Net Income 46bln, NII 85.3bln.

- Bank of China (601988 CH) H1 (CNY): Net Income 117.59bln, -0.9% Y/Y, NIM 214.81bln.

- TSMC (TSM) reportedly plans major supply chain overhaul, targeting high-margin and China-exposed suppliers, according to DigiTimes Asia.

- Alibaba (BABA) Q1 2025 (USD): Revenue 34.6bln (exp. 34.3bln), EPS 2.06 (exp. 2.13); notes new highs in monthly active customers and daily order volume; to increase cloud adoption for AI. Alibaba (BABA) has developed a new AI chip to help fill China’s void, according to WSJ sources.

European bourses began the session on the back foot despite stateside gains on Thursday. A slew of European data points had little impact on price action, which held a negative bias throughout the day. European sectors began the session mixed, though sectors have since slipped nearly entirely in the red as the risk tone deteriorated. Energy and Industrials prove resilient to the downbeat tone, with German Chancellor’s remarks on Thursday helping defence stocks. Merz said there would be no meeting between Russian President Putin and Ukrainian President Zelensky. Banks are the clear underperformers after the think-tank IPPR, recommended the Treasury should hit commercial banks with a new windfall tax on profits to raise up to GBP 8bln.

US equity futures are trading lower but faring better than stocks across the Atlantic. NQ underperforms following outperformance on Thursday, while ES and RTY are a little more resilient into PCE, the latter outperforms.

Top European News

- ECB SCE: Consumers keep inflation expectations stable 1yr: 2.6% (prev. 2.6%). 3yr: 2.5% (prev. 2.4%). 5yr: 2.1% (prev. 2.1%).

- ECB’s de Guindos says “The US-EU trade agreement was the best outcome achievable among a series of difficult negotiations for Europe. In other words, it can be seen as the lesser evil.”, via Econostream X

- German Job Agency Head says the nation has reached a bottoming out of the Labour market.

FX

- DXY is choppy after softening on Thursday alongside a lower yield environment and despite the several encouraging data releases stateside, including the upward revisions to headline US GDP and GDP Sales for Q2, while Core PCE Prices were revised lower and jobless claims fell. DXY currently resides in a narrow 97.85-98.04 parameter at the time of writing, with the 50 DMA seen at 95.58.

- EUR/USD gradually eased back from Thursday’s peak, with the single currency thwarted by resistance near the 1.1700 level. In terms of data this morning, German retail sales fell by -1.5% M/M in July (exp. -0.4%), which saw a tick higher in Bund futures, while German import prices fell by -0.4% M/M in July (exp. -0.3%). French prelim HICP printed 0.8% Y/Y in August (exp. 0.9%, prev. 0.9%), resulting in fleeting EUR downside; Spain’s HICP printed 2.7% Y/Y (exp. 2.7%, prev. 2.7%), but notable that the Core Spanish CPI saw an uptick to 2.4% from 2.3% – little EUR movement. Back to Germany, state CPIs printed in line with what is expected from the mainland metric at 13:00 BST – an uptick in the Y/Y and a downtick in the M/M. Furthermore, ECB SCE saw consumers keep inflation expectations stable. EUR/USD resides in the 1.1657-1.1682 range at the time of writing after briefly dipping under its 50 DMA 1.1661.

- JPY lacks direction as participants digested several data releases from Japan, which were ultimately mixed, whilst macro newsflow remained light in the European morning. The mixed bag of data releases included Tokyo CPI, which mostly matched estimates, and the Unemployment Rate surprisingly declined, although Industrial Production and Retail Sales disappointed. USD/JPY trades on either side of its 50 DMA (146.99) in a current 146.77-147.19 range.

- GBP/USD fell further below the 1.3500 focal point, with Sterling lagging despite light pertinent catalysts for the UK, although there were reports yesterday that PM Starmer plans a cabinet shake-up and is expected to appoint a new economic advisor ahead of the Autumn Budget. Some focus also on the UK think tank IPPR (widely described as left-wing), which recommended that Chancellor Rachel Reeves impose a windfall tax on commercial banks to reclaim profits earned from taxpayer-backed deposits at the Bank of England. A senior banker, speaking with the FT, said, “Politically it is an easy target… No one likes banks, they are seen as a whipping boy for the government”.

- Antipodeans remained afloat after recent advances, and as the PBoC continued to strengthen the yuan reference rate setting.

Fixed Income

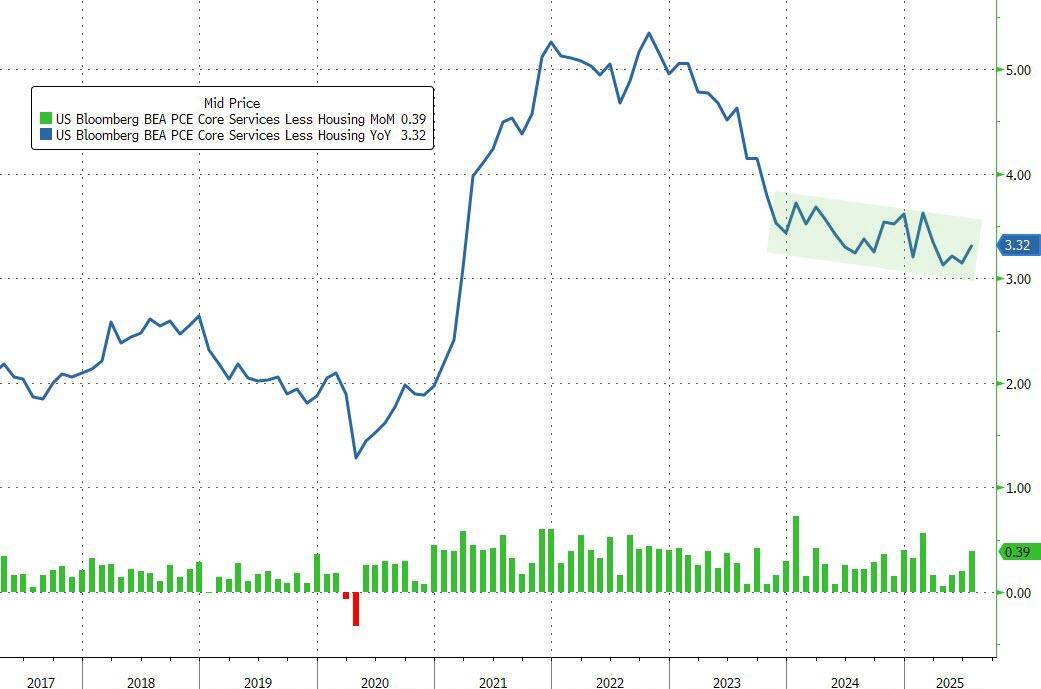

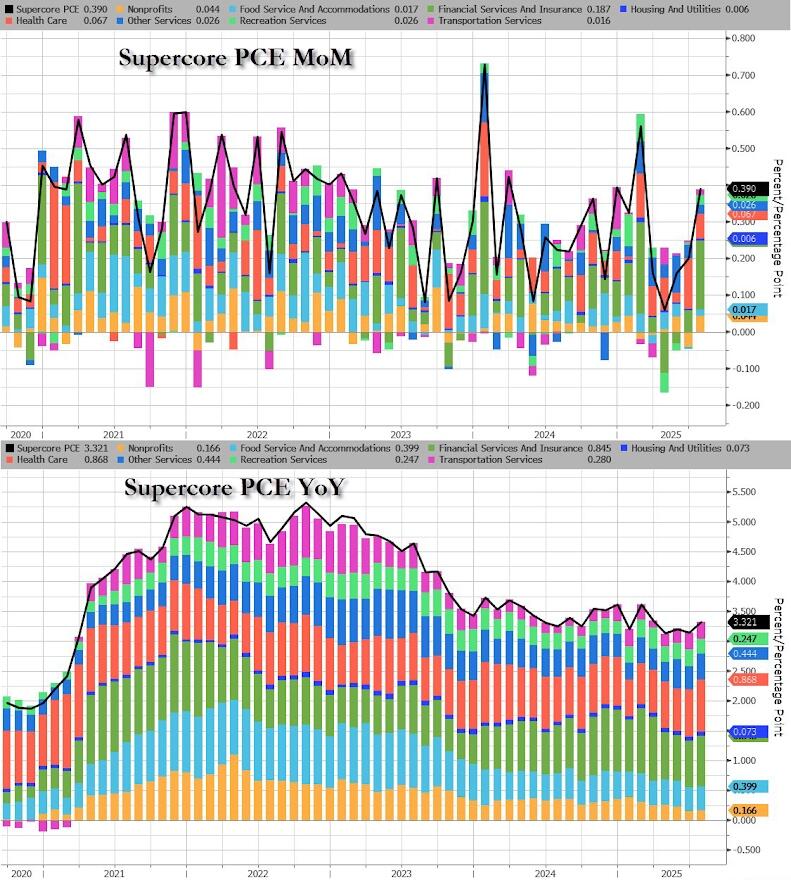

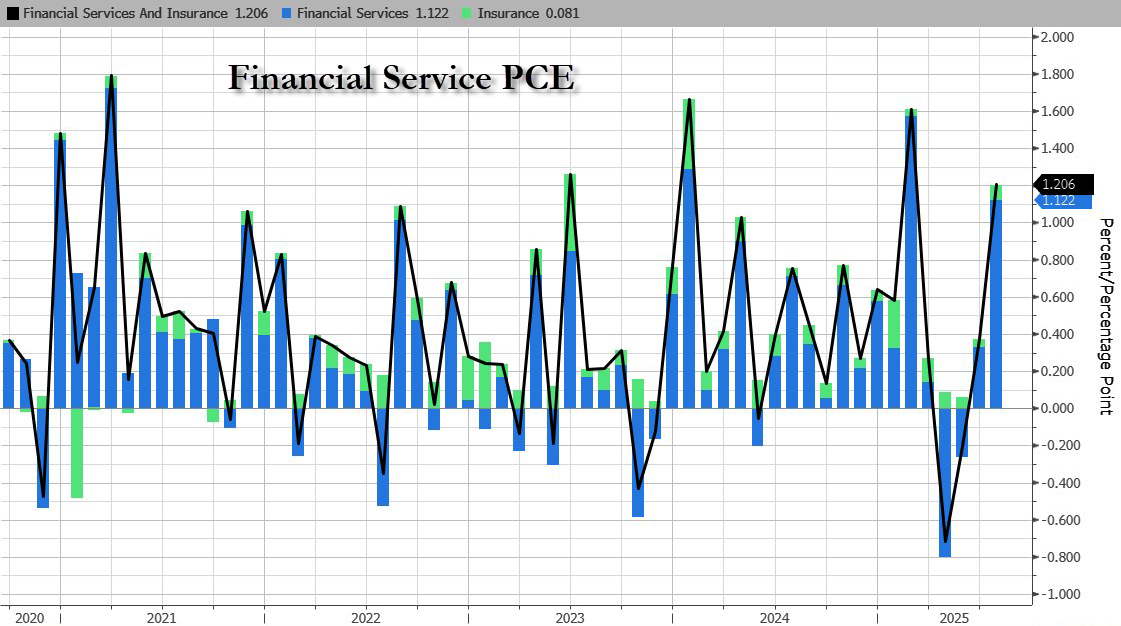

- USTs are lower by a handful of ticks in what has been a quiet and rangebound trade overnight. Currently trading in a 112-13+ to 112-18+ range, as traders now turn their attention to the US PCE later today at 13:30 BST/08:30 EDT. Headline PCE is expected to rise by +0.2% M/M (prev. +0.3%), with the annual rate unchanged at 2.6% Y/Y; the core PCE rate is seen rising +0.3% M/M (prev. 0.3%).

- Bunds are ever so slightly on the back foot, as European traders finally have some key data to digest, by way of Retail Sales/inflation metrics. Nonetheless, moves have been relatively contained so far. German Retail Sales sparked some modest upticks in Bunds and then took another leg higher on the softer-than-expected French inflation metrics – high for the day at 129.77. No real move on German Unemployment or Spanish/Italian/German State CPIs.