XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

FROM MY no 4 SON STEPHEN //THROUGH AI: ENJOY

118 C MACQUARIE FUTURES US 4

118 H MACQUARIE FUTURES US 2

363 H WELLS FARGO SECURITI 6

435 H SCOTIA CAPITAL (USA) 2

661 C JP MORGAN SECURITIES 6 2

726 C PLUS500US FINANCIAL 1

880 C CITIGROUP 3

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 13 CONTRACTs NOTICES FOR 1300 OZ or 0.0404 TONNES

total notices so far: 2597 contracts for 259,700 OR 8.0777 tonnes)

SILVER NOTICES: 723 NOTICE(S) FILED FOR 3.615 OZ/

total number of notices filed so far this month : 9993 CONTRACTS (NOTICES) for 49.915 million oz

WHAT A BUNCH OF CRAP!!

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 11.550 MILLION OZ.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 55.200 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S EX. FOR PHYSICAL TRANSFER TO LONDON OF 0.00933 TONNES PLUS 0. TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 8.6314//NEW TOTAL STANDING FOR GOLD SEPT REDUCES TO = 18.5536 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 14.7455 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A TINY 91 CONTRACTS OI TO 158,277 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 395 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 395 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1075 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 91 CONTRACTS AND ADD TO THE 395 E.FP. ISSUED

WE OBTAIN A FAIR SIZED GAIN OF 304 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.53 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 1.520 MILLION PAPER OZ

OCCURRED WITH OUR $0.53 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED DOWN 47.68 PTS OR 1.25%

//Hang Seng CLOSED DOWN 277.11 PTS OR 1.09%

// Nikkei CLOSED UP 644.38 PTS OR 1.53% //Australia’s all ordinaries CLOSED UP 0.90%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1398 OFFSHORE CLOSED UP AT 7.1385/ Oil DOWN TO 63.13 dollars per barrel for WTI and BRENT DOWN TO 66.91 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1398 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1385 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1808 CONTRACTS TO 494,776 OI DESPITE OUR HUGE GAIN IN PRICE OF $43.20 WITH RESPECT TO WEDNESDAY’S // TRADING.. WE OF COURSE, LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2000). WE HAD ZERO T.A.S. LIQUIDATION AND OUR MONTH END SPREADER LIQUIDATION FINALIZED WITH //FRIDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3808 CONTRACTS (OR 11.844 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD A ZERO EXCHANGE FOR RISK ISSUANCE FOR 0 CONTRACTS OR 0 OZ (0 TONNES).

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES THESE PAST 3 MONTHS;

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW WEDNESDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: TWO ISSUANCES SO FAR TOTALLING 2775 CONTRACTS OR 277,500 OZ OR 8.6314 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW YESTERDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: TWO ISSUANCES FOR 2725 CONTRACTS SO FAR FOR 272,500 OZ OR 8.6314 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH SEPT//ONLY MISSING JUNE.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//FINAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 5477 CONTRACTS WITH OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1420 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST MONTH’S RAID DURING COMEX OPTION EXPIRY WEEK FOR JULY. THE TAS SPREADER LIQUIDATIONS COMBINE WITH MONTH END AUGUST SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED 5 WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY FOR AUGUST AND THEY FOR THE FIRST TIME FAILED WITH RAIDS FINALIZATION ON AUGUST OPTIONS EXPIRY WEEK.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH AUGUST MONTH- END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.00933 TONNES EX.FOR RISK TRANSFER TO GO ALONG WITH THE 0 TONNES OF EXCHANGE FOR RISK ISSUANCE // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 8.6314 TONNES//NEW TOTALS STANDING REDUCES TO 18.5536 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 238 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.00933 TONNES OF EXCHANGE FOR PHYSICAL TRANSFER TO LONDON AND 8.6314 TONNES OF EXCHANGE FOR RISK ISSUANCE:

THAT IS;

A) 0 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY//TOTAL FOR MONTH: 8.6314 TONNES

B) 0.00933 TONNES TODAY EXCHANGE FOR PHYSICAL TRANSFER TO LONDON

TOTALS: 18.5536 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2000 EFP CONTRACT WAS ISSUED: : /DEC 2000 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2000 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY

- MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A FAIR SIZED SIZED 1420 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S STRONG GAIN IN PRICE IN GOLD AND A CORRESPONDING HUGE GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

2) AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES30

3) TO BE FOLLOWED BY SEPTEMBER 2 ISSUANCES FOR EXCHANGE FOR RISK FOR 8.6314 TONNES.

STANDING FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT: 9.9222 TONNES OF GOLD (INCLUDES TODAY’S EXCHANGE FOR PHYSICAL TRANSFER) + 0 TONNES EX FOR RISK TODAY_//TOTAL FOR MONTH = 8.6314//NEW TOTALS FOR GOLD STANDING SEPT = 18.5536 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $43.20./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE LONGS PILING IT ON TRYING TO OBTAIN BADLY NEEDED GOLD///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH LAST WEEK’S TRADING!! THIS IS THE FIRST TIME THAT THE CROOKS COULD NOT MUSTER A RAID ON OPTIONS EXPIRY LONDON/OTC AUGUST TRADING. THEY ARE ATTEMPTING A RAID TODAY ON OUR PRECIOUS METALS.

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

DETAIL SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH SEPTEMBER TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FEBRUARY IS THE SECOND HIGHEST ISSUANCE OF EXCHANGE FOR RISK AS AUGUST BECOMES THE HIGHEST EVER RECORDED AS YOU WILL SEE BELOW!

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH 3 ISSUANCES

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRIL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE: 3

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: 7 ISSUED,

TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 44.696 TONNES, THE HIGHEST MONTHLY EVER COMEX ISSUANCE!!!!!!

THUS 107.5117 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS/EX FOR PHYS TRANSFERS) + 44.696 TONNES EX FOR RISK = 152.208 TONNES.

SEPTEMBER: 2 ISSUED:

THE CME NOTIFIED US THAT OUR TWO ISSUANCE OF EXCHANGE FOR RISK EQUATES TO 2725 CONTRACTS FOR 272,500 OZ OR 8.6314 TONNES. WE WILL PROBABLY HAVE A DOOZY FOR SEPT DELIVERIES AS EITHER THE BANK OF ENGLAND OR THE BIS (LOANED TO THE FRBNY) WANTS ITS GOLD BACK+ THE MASSIVE QUEUE JUMPING BY OTHER CENTRAL BANKS

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 11.844 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OF 0.00933 TONNES OF GOLD ALONG WITH 8.6314 TOTAL TONNES OF EXCHANGE FOR RISK TOTAL FOR MONTH (TODAY’S EX FOR RISK ISSUANCE = 0 TONNES EXCHANGE FOR RISK) AND THUS NEW TOTALS EX FOR RISK MONTH = 8.6310//NEW TOTAL STANDING FOR GOLD IN SEPT REDUCES TO: 18.5536 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED WITH OUR HUGE GAIN IN PRICE TO THE TUNE OF $43.20

WE HAD 1669 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 3808 CONTRACTS OR 380,800 0Z (11.844 TONNES)

confirmed volume WEDNESDAY 243,321 contracts// fair//

speculators have left the gold arena

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

SEPT 4 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entries . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 13 notice(s) 1300 OZ 0.0404 TONNES |

| No of oz to be served (notices) | 593 contracts 59300 OZ 1.8444 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2597 notices 259,700 oz 8.0777 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entries

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

ADJUSTMENTs 2

both dealer to customer accts:

a) Brinks dealer account to customer; 3,086.496 oz

b) JPMorgan: dealer to customer account; 8,061.491 oz

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 606 CONTRACTS FOR A LOSS OF 46 CONTRACTS. WE HAD 43 CONTRACTS FILED ON WEDNESDAY SO WE LOST 3 CONTRACTS OR 300 OZ ENTERTAINED A EXCHANGE FOR PHYSICAL TRANSFER OF 0.00933 TONNES. WE NOW MUST ADD OUR INITIAL 2.333 TONNES OF GOLD ISSUED UNDER EXCHANGE FOR RISK/PRIOR TO YESTERDAY’S 6.299 TONNES/NEW EX FOR RISK = 8.63147//THUS NEW TOTAL OF GOLD STANDING REDUCES TO 18.5536 TONNES

OCTOBER LOST 115 CONTRACTS DOWN TO 61,763

NOVEMBER LOST 29 CONTRACTS UP TO 2663 CONTRACTS.

We had 13 contracts filed for today representing 1300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 8 notices issued from their client or customer account. The total of all issuance by all participants equate to 13 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 2 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (2597 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 606 CONTRACTS) minus the number of notices served upon today (13 x 100 oz per contract) equals 319,000 OZ OR 9.9222 TONNES OF GOLD TO WHICH WE ADD OUR INITIAL EX FOR RISK OF 8.632 TONNES//NEW TOTAL STANDING REDUCES TO 18.5536 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (2597 x 100 oz +we add the difference for front month of SEPT. (606 OI} minus the number of notices served upon today (13 x 100 oz) which equals 319,000 OZ OR 9.9222 TONNES PLUS 8.632 TONNES EXCHANGE FOR RISK = 18.5536 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 18.5536 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,049,534.159 oz 63.756 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,957,797.857 oz

TOTAL REGISTERED GOLD 21,304,588.071 or 662.662 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,653,209.786 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,255,054 oz ((REG GOLD- PLEDGED GOLD)= 598.91 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 4 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries: i) Out of Delaware: 3898.140 oz ii) Out of HSBC 80,325.460 oz total withdrawal 84,223.600 oz |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Stonex 1135,107.020 oz total deposit1135,107.02 oz |

| Deposits to the Customer Inventory | 1 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into CNT 294,847.600 oz total deposit 294,877.600 oz |

| No of oz served today (contracts) | 723 CONTRACT(S) (3.615 million OZ |

| No of oz to be served (notices) | 1057 contracts (5.285 MILLION oz) |

| Total monthly oz silver served (contracts) | 9983 Contracts (49.915 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

i) Into Stonex 1135,107.020 oz

total deposit1135,107.02 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into CNT 294,847.600 oz

total deposit 294,877.600 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

2 entries:

i) Out of Delaware: 3898.140 oz

ii) Out of HSBC 80,325.460 oz

total withdrawal 84,223.600 oz

ADJUSTMENTs 3

1dealer to customer accts:

a) Brinks dealer account to customer; 112,000.620 oz

next two: customer to dealer

b) CNT: customer account to dealer;; 1,400,717.730 oz

c) Manfra: 183,891.480 oz//customer to dealer.

TOTAL REGISTERED SILVER: 195.234 MILLION OZ//.TOTAL REG + ELIGIBLE. 517.413 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 1780 OPEN INTEREST CONTRACTS FOR A LOSS OF 847 CONTRACTS. WE HAD 975 CONTRACTS SERVED YESTERDAY SO WE GAINED A HUGE 128 CONTRACT OR 1.024 MILLION OZ ENTERTAINED A QUEUE JUMP//NEW STANDING FOR SILVER COMEX ADVANCES TO 55.200 MILLION OZ.

STANDING FOR SILVER: 55.200 MILLION OZ

OCTOBER GAINED 33 CONTRACTS TO 2501

NOVEMBER GAINED 195 CONTRACTS UP TO 1231.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:723 or 3.615 MILLION oz

CONFIRMED volume; ON WEDNESDAY 69,090 strong//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 9983 X5,000 oz = 49.915 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (1780) AND the number of notices served upon today (723 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (9983) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(1780) minus number of notices served upon today (723)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 55.200 MILLION OZ .

New total standing: 55.200 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 195.234 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/517.413 million. 40.61%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

GLD INVENTORY: 984.26 TONNES, TONIGHTS TOTAL

SILVER

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

CLOSING INVENTORY 491.308 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

Which Housing Domino Will Fall First?

Boomers, Airbnb, or private equity…or all three?

| John RubinoSep 4 |

At least three big groups of homeowners have the potential to crash the US housing market. And with home prices at unaffordable levels and mortgage rates above 6%, it’s now a question of when, not if, this market tanks. But it’s still fun to speculate about which domino will be first to fall?

Here are three likely suspects:

Aging Boomers

I live in a neighborhood that’s mostly retirees in pricy houses. And a couple of things are happening:

- Many of our neighbors are sick, some seriously, which makes statistical sense. If a married couple is in their 70s, the odds that one of them is dealing with health issues are pretty high. In just the past year, several of them have died, and in every case, the surviving spouse — in no shape to manage a big house on a high-maintenance lot — has immediately put it on the market.

- Other neighbors are moving to be closer to their grandchildren. One couple, who have become good friends and will be sorely missed, just made an offer on a Florida house for that reason. If the offer is accepted, they’ll immediately list their current house for sale.

Basic math says that as Boomers age, the above trends will intensify. Who will buy the Boomers’ 30 or so million houses? Well, at today’s prices, no one, obviously. The average Millennial or Gen Z buyer can’t come close to affording the required mortgage.

Meanwhile, the kids and grandkids who inherit Boomer McMansions frequently can’t keep them. Another personal aside: A friend just died, leaving her house in Washington state to her daughter, who lives in Alaska. The daughter and her husband have just remodeled their existing home, leaving them with no money for upkeep on an inherited house in another state. Faced with this new cash drain, they’re considering listing the house immediately.

Conclusion: Boomers are becoming a source of massive new housing inventory, and will continue thus for at least another decade.

Failed Airbnb entrepreneurs

Once upon a time, Airbnb was about making housing part of the “sharing economy” by allowing regular people to monetize spare rooms or RVs or even backyard tents by renting them to strangers. (Yes, that sounds even creepier than ride sharing.)

It worked, at first. Tenants got cheap, quirky, and convenient rentals while owners got small but welcome bits of extra cash.

One more personal aside: My first Airbnb experience was maybe a decade ago, when I rented an RV in Arizona for a couple of nights. The owners lived in a neighboring RV and invited me over for dinner. We had a good time, and I left a 5-star review. Smooth and easy.

But now, the typical Airbnb rental is an upscale, expensive, and highly complicated proposition, with requirements that the tenant clean up before leaving and multiple fees that frequently raise the cost to as much or more than nearby hotels.

Adding to the creepy vibe, it has recently been discovered that some Airbnb hosts have wired cameras into their units to spy on tenants. Here’s a video explaining how to detect those cameras:

Last but not least, a typical Airbnb entrepreneur now owns multiple properties and only interacts with tenants when there’s a problem. The algorithm handles everything else.

The result: A growing number of travelers are asking Why bother with the complexities and uncertainties of an Airbnb when a hotel costs the same and doesn’t require you to clean up after yourself?

So…an inferior — or at least unpredictable — product peddled by amateurs who are leveraged to the hilt and have never weathered a serious downturn. A bust sounds pretty much guaranteed. But is it imminent? Let’s see what’s happening now:

Soaring inventory. Short-term rentals became a get-rich-quick scheme for inexperienced people who had access to cheap financing in the early 2020s. And now these folks have over 2 million units, many of which are not generating positive cash flow:

One of the biggest challenges currently facing the short-term rental market is market saturation. As the Airbnb platform gained popularity, an influx of new property owners and investors rushed to list their homes and apartments. Cities like Dallas saw more than 6,000 new Airbnb listings added since 2020, far outpacing local demand. This oversupply has created intense competition among property managers, driving down nightly rates and occupancy in many areas. What once looked like easy profit has become a struggle for visibility and pricing power in an increasingly crowded STR market.

The following video predicts massive forced selling by Airbnb landlords:

Private Equity “Landlords”

After the 2008 housing bust, the only people with access to cheap credit were hedge funds and private equity firms. They used some of this capital to buy up houses — sometimes entire neighborhoods — and converted them to rentals, raising rents and scrimping on upkeep in the face of strong demand from people who had no choice but to rent.

What more needs to be said? Obviously, Wall Street sharks are terrible landlords, and — given their propensity to pile into and then back out of bubble assets — they’re setting the housing market up for a crash.

But, you might ask, aren’t these guys the world’s most intelligent people? Well…high IQs, yes, but judgement, no. Look at the chart for the 1990s tech stock bubble for a view of housing’s future. Remember that in 1999, Wall Street’s geniuses were all-in on the dot-com stocks:

Which Goes First?

This is a tough one, because all three of these potential dominoes are teetering as this is written. Boomers are aging, Airbnb landlords are hemorrhaging cash, and private equity “landlords” are in waaayyy over their heads. So relying on personal experience, I’m going to rank them in this order: Airbnb landlords first, Boomers second, and private equity as the crescendo that blows up the banks along with housing. Have fun, and keep stacking.

MARKET EAR…………………

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

US destroys her hegemony

The Shanghai Cooperation Organisation gathering in Tianjin hosting 23 world leaders and more at the military parade in Beijing shows that the world is ignoring autarkic America.

| Alasdair MacleodSep 4∙Paid |

Ever since the US decided that China was a threat to its role as the world’s policeman and financier, it has been on the back foot. Provocation failed in its objective every time, as the Chinese leadership always took the long view and failed to react. It had analysed US tactics of dollar debt pump-and-dump, concluding rightly or wrongly that it could be extended to China. Sensibly, China refused to borrow dollars, accumulating them instead, implying it could be China doing the pump-and-dump by selling US treasuries and driving up bond yields.

Then there is the history of US attempts at regime change, usually successful. The crude overthrow of leaders by covert CIA actions was not possible in China’s case. Instead, China was cast out as a pariah state because of its maltreatment of Uigurs. The attempts to curtail Chinese technology by casting back door spying aspersions followed, along with the detention of Meng Wanzhou, Huawei’s CFO in Canada on US instructions. The list of provocations which failed in their intent is extensive.

Every time, China’s view of American interference was why interrupt an enemy when it defeats its own objectives by making all the mistakes?

Of course, US anti-Chinese propaganda has been imprinted on western minds, which are pigheadedly unaware of China’s role in assembling a global trade force wholly independent from the US and its dollar. Mainstream media reporting of the major gathering in Tianjin is dismissive, which is an egregious error.

Emerging nations, mostly sick of the Americans and Europeans and less fearful of the consequences are flocking to join the joint Chinese and Russian sphere of influence. The combination of the Shanghai Cooperation Organisation, which is predominantly Asian mainland, and BRICS which is the rest of the world is growing rapidly. President Trump’s MAGA autarkicism and tariff policies have triggered a flood of nations looking to join what is rapidly becoming the most powerful economic force on earth.

Trump’s abusive threat against India for processing Russian oil backfired badly. In the past India would have rushed to mollify the US. Instead, it is said that when Trump tried to climb down, Modi refused to take his ‘phone calls and travelled to Tianjin where he has been seen in close conversation with Putin and Xi despite the territorial dispute with China, and China’s supply of weapons to Pakistan.

At the centre of it all is these three nations, members of both SCO and BRICS. India, China, and Russia combined represents 3 billion souls or 37% of the world’s population. That they will work closely together was one of the messages from Tianjin.

It will surprise readers to learn that Wednesday’s military parade in Beijing was also attended by some key western allies. These included Kim Min-seok, South Korea’s prime minister, Prabowo Subianto, Indonesian president, Shebaz Sharif, Pakistan’s prime minister, Robert Fico, Slovak prime minister, Daniel Andrews former premier of Victoria Australia, John Key, New Zealand former prime minister, and Helen Clark also a former New Zealand prime minister.

Trading without the dollar

The primary objective of the SCO and BRICS is for member nations to do away with the dollar in trade finance, commodity pricing, and capital investment. It is likely that the SCO’s proposed development bank will have a central role in replacing national debts denominated in dollars with Chinese yuan, allowing them to escape dollar hegemony. It will supplement the BRICS development bank in Shanghai.

National members of the SCO and BRICS amount to over 70% of the world’s population. As these plans mature, the dollar’s reserve status will be replaced by the yuan, leading to a winding down of foreign dollar balances, currently estimated by the US Treasury to total about $40 trillion, about one-third more than the US’s entire GDP.

This estimate doesn’t include offshore dollar balances estimated some time ago by the Bank for International Settlements to be close to a further $90 trillion principally facilitating foreign exchange transactions between other currencies and to a lesser extent the eurodollar market.

The negative implications for the dollar will not be lost on China’s leadership. It is a process which will be sped up by BRICS members and potential members replacing their dollar obligations with yuan. They also see the dollar heading towards a crisis on US economic policy alone. The irony is that the US pump-and-dump operation used against other nations is now playing out against America itself, with treasury yields rising and inevitably leading to a financial and credit crisis, with or without a push from China.

For a long time, China has taken the view that the entire fiat currency system has a limited life: use it while you can but protect yourself against its ultimate failure. We know that China and its citizens have used a significant portion of their post-Mao wealth to accumulate gold bullion following legislation introduced specifically towards that end in 1983. In the 42 years since, unwanted bullion in the west has migrated into China and almost none has been allowed out.

China understands the difference between fiat credit and monetary gold, and that currencies are merely a promise of final settlement which no issuer today is prepared to honour. She knows that in a post-dollar world that promise must return, and China can provide that assurance by backing the yuan with some guarantee of convertibility. To this end, the Shanghai Gold Exchange has said it will open vaults in Hong Kong and Saudi Arabia, presumably to be followed by others, which will accept gold exchangeable for yuan.

A post-fiat world is emerging. It will be central to trade and finance for a generally underdeveloped world, rapidly embracing communications and Chinese commercial technology which is now superior to anything in America and in her spheres of influence.

Conclusion

It appears that the SCO and BRICS are on the verge of a further leap forward, facilitated by the continuing failures of US containment strategies and the unintended consequences of President Trump’s MAGA policies and tariff disruptions. The following has emerged:

· The establishment of an SCO bank alongside the BRICS bank in Shanghai will assist members to replace capital commitments in dollars with yuan.

· We know that other nations are looking to join BRICS, and the SCO itself will expand as associates and dialog partners move towards full status. The surprise is that while Australia and New Zealand are not officially interested, they have sent unofficial representatives to the Beijing military parade. Fico from Slovakia alerts us that some of the East Europeans are potentially interested.

· Plans to ensure that gold is central to the entire SCO/BRICS payments system as and when it will be necessary are materialising before our eyes.

· The dollar faces an unwinding of its central position to the world economy which is likely to be more rapid that generally expected.

None of this is reflected in foreign exchange markets yet. But as the US debt trap is sprung, it will be an additional factor accelerating the fiat dollar’s demise.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

Central banks are urged to pool dollar reserves as Fed help is doubted

Submitted by admin on Wed, 2025-09-03 17:07 Section: Daily Dispatches

By Francesco Canepa and Balazs Koranyi

Reuters

Wednesday, September 3, 2025

FRANKFURT, Germany — The European Central Bank and its peers around the world should pool their reserves for U.S. dollar liquidity as Federal Reserve help cannot be guaranteed given President Donald Trump’s attacks, the head of an influential think tank said.

Adam Posen of the Peterson Institute for International Economics told an ECB conference today it should not be taken for granted that a politicised Fed would lend dollars to foreign central banks in a crisis, as it did a few times since the 2007-2008 financial meltdown.

He recommended that the ECB and its peers outside the United States pool their reserves in dollars to provide emergency liquidity to domestic banks if needed. This option has been raised by European central bankers behind closed doors. …

… For the remainder of the report:

end

World Gold Council concocting another form of disembodied gold

Submitted by admin on Wed, 2025-09-03 09:33 Section: Daily Dispatches

London’s Bullion Market to Trial Digital Gold

By Leslie Hook

Financial Times, London

Wednesday, September 3, 2025

The World Gold Council is seeking to launch a digital form of gold, a move that could revolutionise London’s $900 billion physical market for the precious metal by creating a new way to trade, settle, and collateralise bullion.

This new format would create the ability to “pass gold digitally around the gold ecosystem, as collateral, for the first time,” said David Tait, chief executive of the World Gold Council, an industry body representing gold miners, in an interview with the Financial Times.

While many investors value gold precisely because of its physical nature and its lack of counterparty risk, seeing it as a haven asset, Tait argues that bullion must be digitised to broaden its market reach.

“We are trying to standardise that digital layer of gold, such that the various financial products used in other markets can be used in the gold market going forward,” said Tait, a former banker. “My goal is that many asset managers around the world will suddenly look at it differently,” he added. …

… For the remainder of the report:

end

Jesse Colombo: Gold and silver officially confirm their breakouts

Submitted by admin on Tue, 2025-09-02 19:51 Section: Daily Dispatches

By Jesse Colombo

The Bubble Bubble Report

Tuesday, September 2, 2025

Today is a very exciting day because gold and silver have both officially broken out, giving the green light for powerful rallies into year-end. This is the scenario I’ve been long anticipating as summer wrapped up and Wall Street returned from vacation mode.

In my last update on Sunday, I explained that gold and silver were beginning to break out, but I was waiting for additional confirmation such as strong Comex futures volume and breakouts across all major currencies.

That had not happened yet because Friday was right before the three-day Labor Day weekend, when trading volume was subdued, so I wanted to be cautious and wait for follow-through this week. And today, that follow-through arrived in a big way. In this update, I will show you where gold, silver, and the miners stand now, along with my outlook going forward. …

… For the remainder of the analysis:

end

China advances development bank to help 10 Eurasian countries curb U.S. dollar risks

Submitted by admin on Tue, 2025-09-02 07:05 Section: Daily Dispatches

By Ralph Jennings

South China Morning Post, Hong Kong

Tuesday, September 2, 2025

A strong push on Monday to create a development bank serving 10 Eurasian countries, including China, would help insulate the group from increasingly risky U.S. dollar-dominated trade while accelerating key infrastructure work, according to analysts.

Such a concessional lender — part of an idea that has long been put on hold — would serve China, Russia, India, and seven other nations that have worked together since 2001 as the Shanghai Cooperation Organisation (SCO).

President Xi Jinping said at a summit of the organisation’s leaders in Tianjin on Monday that the bank “should be established as soon as possible to provide stronger support for the security and economic cooperation of member states,” Xinhua reported.

And an official statement later released by Xinhua in the evening said the SCO had “decided to establish a development bank and accelerate consultations on a series of issues related to the financial institution’s operation.” …

… For the remainder of the report:

end

India’s central bank edges away from U.S. Treasuries toward gold

Submitted by admin on Tue, 2025-09-02 06:58 Section: Daily Dispatches

From the Times of India, Mumbai

Monday, September 1, 2025

U.S. Treasury bills seem to be losing favour, with the Reserve Bank of India stepping up gold holdings to increase India’s foreign exchange reserves.

India’s central bank has shown a preference for increasing gold reserves instead of U.S. Treasury bills to strengthen its foreign exchange holdings, according to recent data from the U.S. Department of Treasury and RBI. This is part of a broader global shift towards diversifying national reserves beyond dollar-based assets.

The quantity of gold within foreign exchange reserves reached 879.98 metric tonnes as of June 27, 2025, rising from 840.76 metric tonnes recorded on June 28, 2024.

According to an Economic Times report, data reveals a decline in India’s U.S. T-bill investments in June compared to the previous year, whilst the country’s gold reserves increased during this

period. …

… For the remainder of the report:

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 238

5. COMMODITY REPORT GOLD

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED DOWN 47.68 PTS OR 1.25%

//Hang Seng CLOSED DOWN 277.11 PTS OR 1.09%

// Nikkei CLOSED UP 644.38 PTS OR 1.53% //Australia’s all ordinaries CLOSED UP 0.90%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1398 OFFSHORE CLOSED UP AT 7.1385/ Oil DOWN TO 63.13 dollars per barrel for WTI and BRENT DOWN TO 66.91 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1398 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1385 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1398

OFFSHORE YUAN: UP TO 7.1386

HANG SENG CLOSED DOWN 277.11 PTS OR 1.09%

2. Nikkei closed UP 644.38 PTS OR 1.53%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 98.21 EURO FALLS TO 1.1651 DOWN 9 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.602//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.37…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.262 DOWN 3 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7198 Italian 10 Yr bond yield DOWN to 3.614 SPAIN 10 YR BOND YIELD DOWN TO 3.321

3i Greek 10 year bond yield DOWN TO 3.452

3j Gold at $3540.15 Silver at: 40.89 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 36 /100 roubles/dollar; ROUBLE AT 81.61

3m oil (WTI) into the 63 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.37/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.602% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.262 DOWN 3 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8050 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9351 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.204 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.890 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.608 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.17

10 YR UK BOND YIELD: 4.7330 DOWN 2 PTS ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.582 DOWN 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.394 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.871 DOWN 1 BASIS PTS.

2a New York OPENING REPORT

US Futures Rise As Global Bond Rout Fizzles

Thursday, Sep 04, 2025 – 08:21 AM

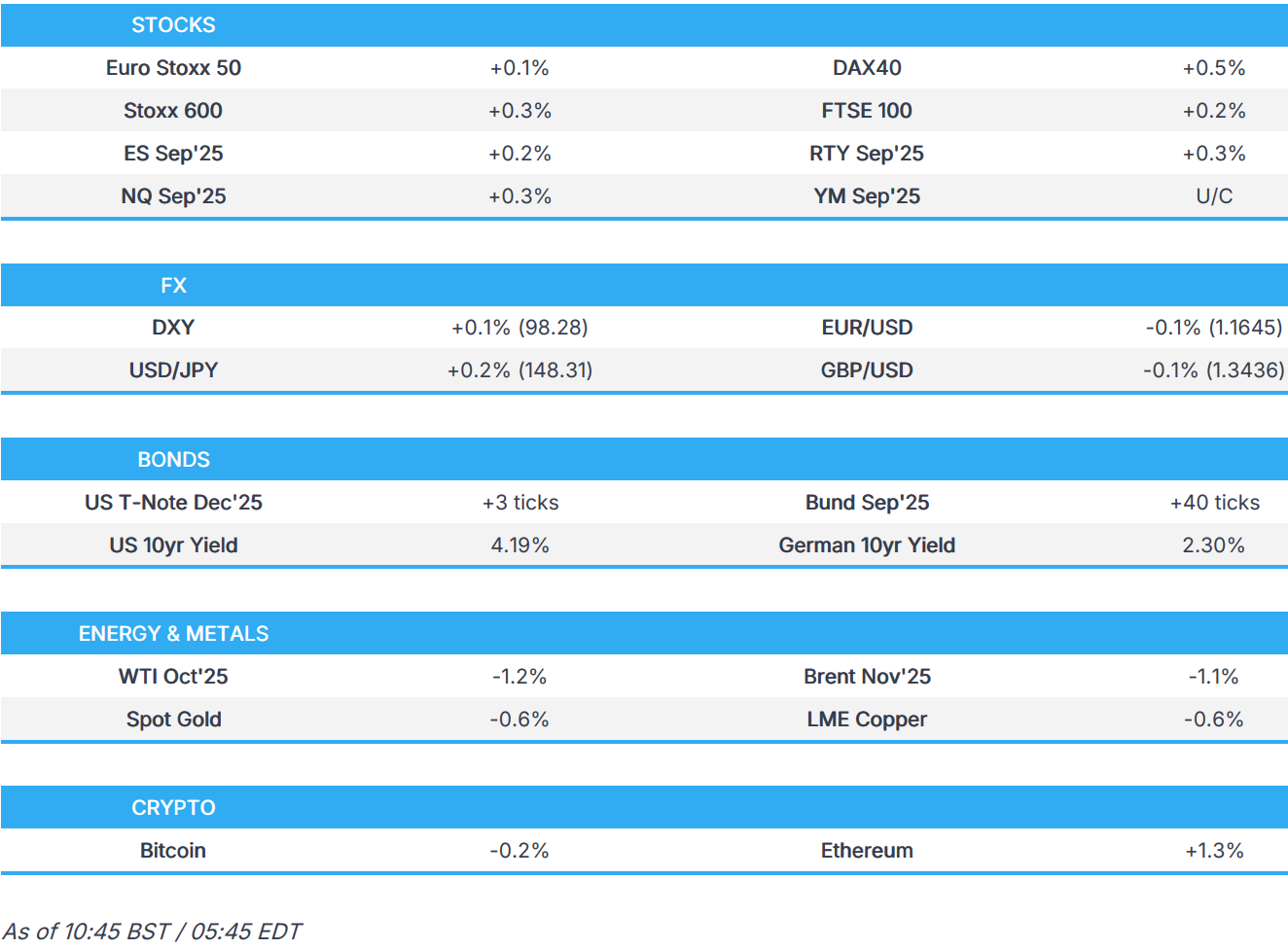

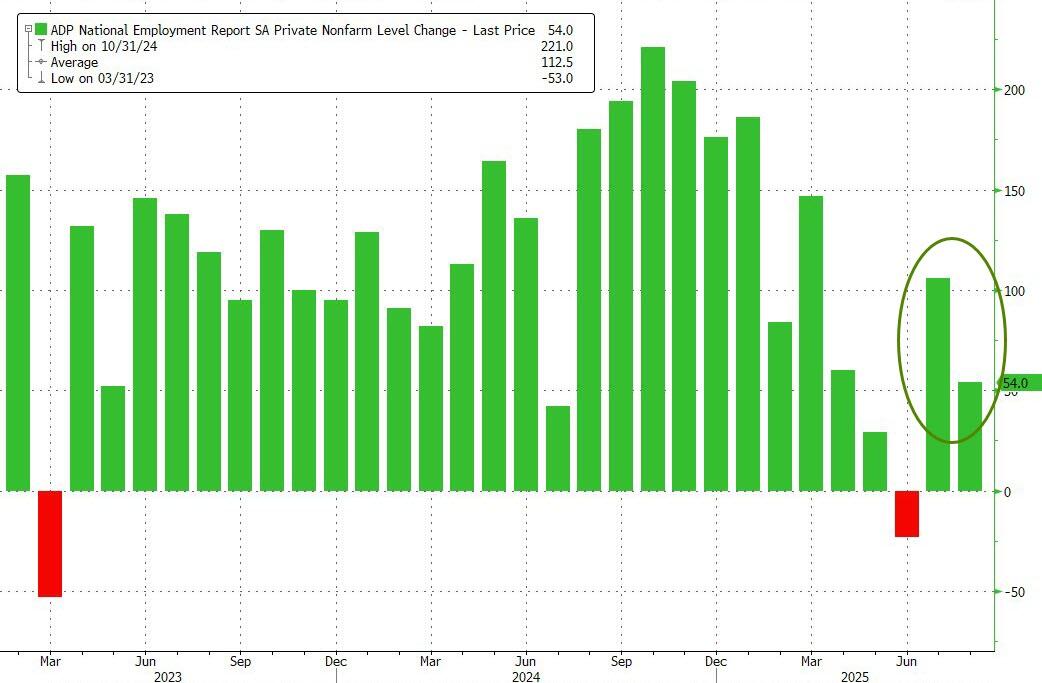

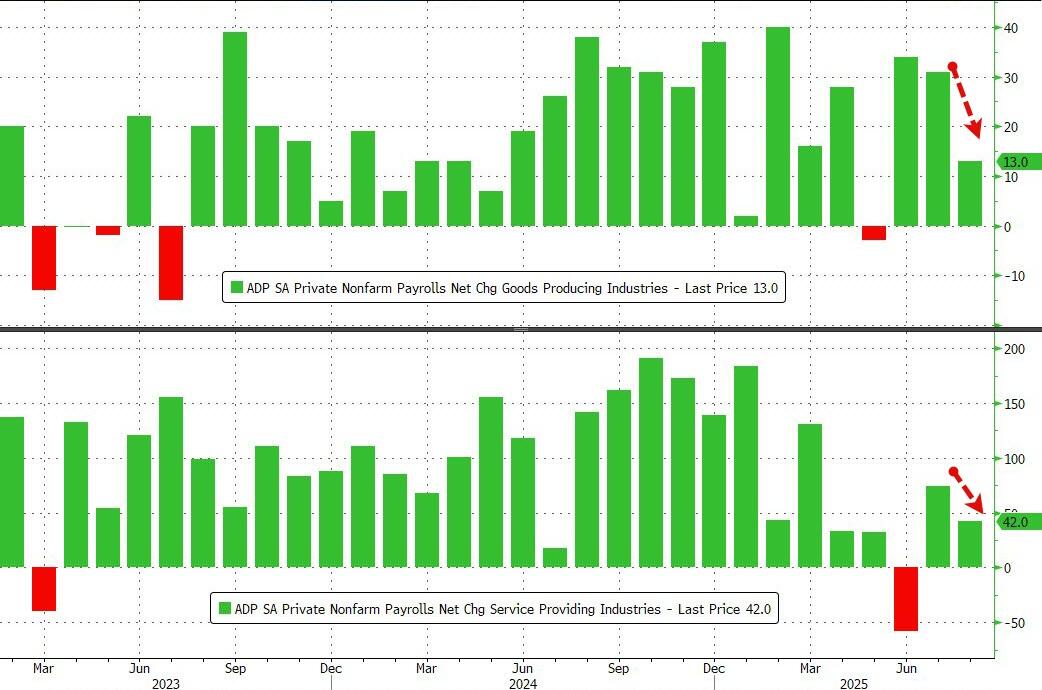

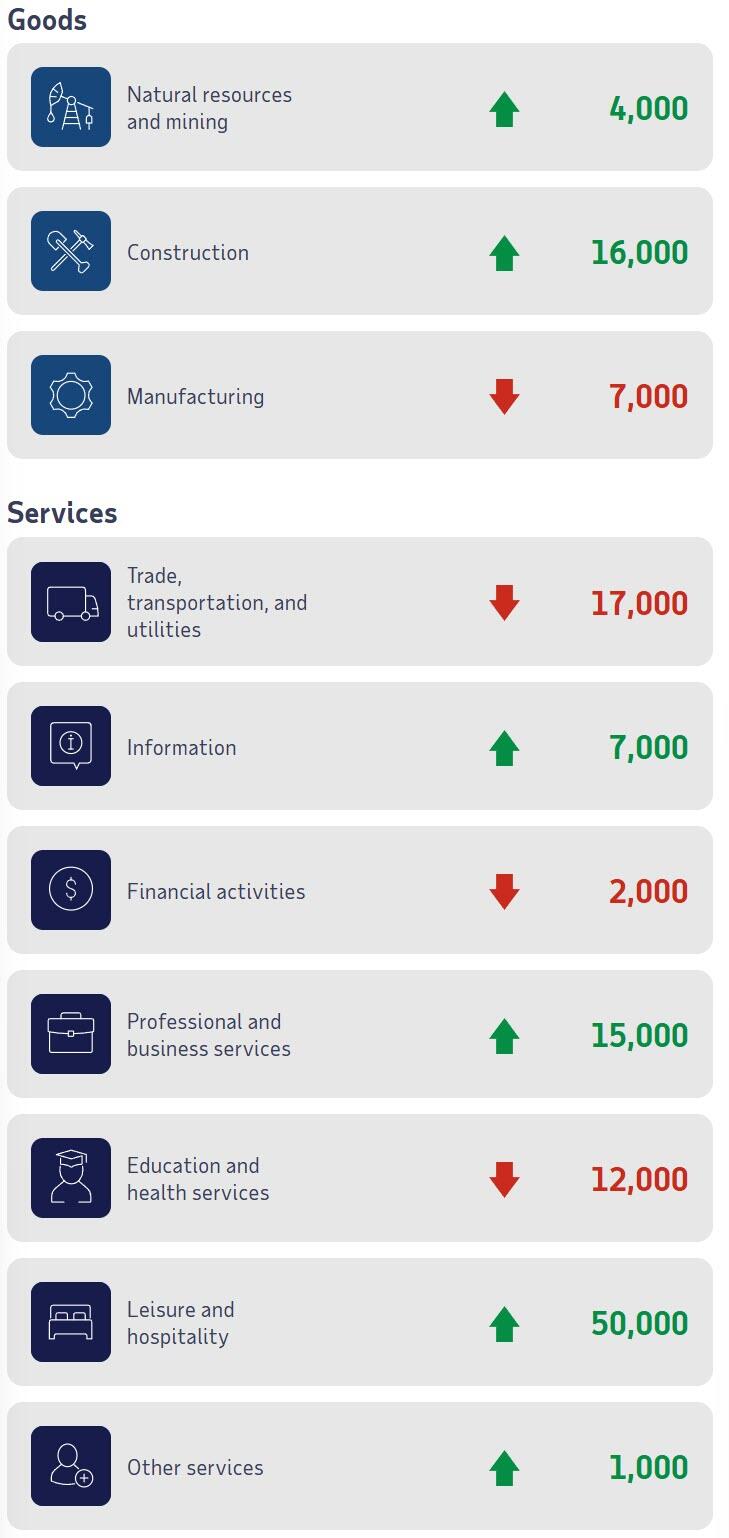

US equity futures are higher, extending yesterday’s gains, while the global bond rout is put on hold for the time being as traders boost wagers on a faster pace of US interest-rate cuts ahead of Friday’s pivotal jobs report. As of 8:00am ET, S&P futures are 0.1% higher, pointing to a back-to-back advance, and Nasdaq futures gain 0.25%, with Mag 7s mostly higher premarket as AMZN and TSLA add 1.3% and 1.4%, respectively. Advances were stronger in Europe, where the Stoxx 600 strengthened 0.6% and French bonds led gains across the board. Treasuries extended gains, with the yield on 10-year notes falling two basis points to 4.19% while the USD is higher. Commodities are mostly lower; oil -1.2%; gold -0.6%. Overnight, not a lot of major headlines in the US as investors are waiting for the 2x major catalysts this week (Broadcom earnings today after the close, and NFP tomorrow). Today we get the ADP Employment report at 8:15am ET (68k survey vs 104k prevsious) and ISM Services at 10am ET today (50.9 survey vs. 50.1 prior).

In premarket trading, Mag 7 stocks are mostly higher (Amazon +1.6%, Tesla +1.1%, Nvidia -0.7%, Meta +1.8%, Apple -0.3%, Microsoft -0.1%, Alphabet -0.7%).

- American Eagle (AEO) gains 26% after the clothing retailer reported better-than-expected 2Q revenue, boosted by demand following its Sydney Sweeney ad campaign.

- C3.ai (AI) slumps 13% after the software company forecast revenue for the second quarter that missed the average analyst estimate. It also named Stephen Ehikian as its new CEO, replacing founder Tom Siebel, who will remain executive chairman.

- Caleres (CAL) falls 7% after the footwear retailer reported adjusted earnings per share for the second quarter that missed the average analyst estimate.

- Ciena (CIEN) climbs 11% after the maker of equipment used by telecom companies reported adjusted earnings per share for the third quarter that beat the average analyst estimate.

- Credo Technology (CRDO) is up 11% after reporting adjusted earnings per share for the first quarter that beat the average analyst estimate.

- Figma (FIG) falls 15% after the software design company forecast annual sales that failed to impress Wall Street’s lofty expectations. This was the company’s first report since it went public in late July.

- GitLab (GTLB) is down 7% after the software company gave an outlook for third-quarter revenue that was weaker than expected. It also said that Brian Robins will step down as chief financial officer.

- HP Enterprise (HPE) is up 3% even as the company expects narrower profit margins as it enters the next leg of AI-driven demand. Bloomberg Intelligence says that with server execution issues behind it, the company should get free cash flow back on track in fiscal 2026.

- PagerDuty (PD) falls 3.6% after the cloud computing company trimmed the top end of its 2026 revenue guidance range. The company’s third quarter adjusted EPS view came in slightly lower than the consensus estimate.

- Salesforce (CRM) is down 7% after the software company gave an outlook that was seen as underwhelming.

- T. Rowe Price Group Inc. (TROW) rises 8% as Goldman Sachs Group Inc. will invest as much as $1 billion in the company and team up with the asset manager to sell private-market products to retail investors.