XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

FROM MY no 4 SON STEPHEN //THROUGH AI: ENJOY

118 C MACQUARIE FUTURES US 135

118 H MACQUARIE FUTURES US 122

323 C HSBC 520

332 H STANDARD CHARTERED B 25

435 H SCOTIA CAPITAL (USA) 70

624 H BOFA SECURITIES 6

661 C JP MORGAN SECURITIES 9 35

732 C RBC CAP MARKETS 16

737 C ADVANTAGE FUTURES 6

880 C CITIGROUP 101

905 C ADM 13

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 529 CONTRACTs NOTICES FOR 52,900 OZ or 1.6454 TONNES

total notices so far: 3126 contracts for 312,600 OR 9.723 tonnes)

SILVER NOTICES: 32 NOTICE(S) FILED FOR 0.160 OZ/

total number of notices filed so far this month : 10,015 CONTRACTS (NOTICES) for 50.075 million oz

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 13.050 MILLION OZ.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 55.500 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.3017 TONNES PLUS 0. TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 8.6314//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 18.8544 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 15.7729 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE 1185 CONTRACTS OI TO 157,092 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 300 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 300 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1075 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1185 CONTRACTS AND ADD TO THE 300 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 882 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.68 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.425 MILLION PAPER OZ

OCCURRED WITH OUR $0.68 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 46.24 PTS OR 1.24%

//Hang Seng CLOSED UP 357.25 PTS OR 1.43%

// Nikkei CLOSED UP 438.48 PTS OR 1.03% //Australia’s all ordinaries CLOSED UP 0.90%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1377 OFFSHORE CLOSED UP AT 7.1343/ Oil DOWN TO 63.23 dollars per barrel for WTI and BRENT DOWN TO 66.74 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1377 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1343 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 592 CONTRACTS TO 495,368 OI DESPITE OUR LOSS IN PRICE OF $22.70 WITH RESPECT TO THURSDAY’S // TRADING.. WE OF COURSE, LOST NO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (330). WE HAD ZERO T.A.S. LIQUIDATION AND OUR MONTH END SPREADER LIQUIDATION FINALIZED WITH LAST FRIDAY TRADING AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 922 CONTRACTS (OR 2.867 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD A ZERO EXCHANGE FOR RISK ISSUANCE FOR 0 CONTRACTS OR 0 OZ (0 TONNES). THE RAID ACCOMPLISHED NOTHING FOR OUR CROOKS

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES THESE PAST 3 MONTHS;

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW WEDNESDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: TWO ISSUANCES SO FAR TOTALLING 2775 CONTRACTS OR 277,500 OZ OR 8.6314 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW YESTERDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: TWO ISSUANCES FOR 2725 CONTRACTS SO FAR FOR 272,500 OZ OR 8.6314 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH SEPT//ONLY MISSING JUNE.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//FINAL

IN TOTAL WE HAD A SMALL SIZED GAIN ON OUR TWO EXCHANGES OF 922 CONTRACTS DESPITE OUR STRONG LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 882 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE WITH LAST MONTH’S RAID DURING COMEX OPTION EXPIRY WEEK FOR JULY. THE TAS SPREADER LIQUIDATIONS COMBINE WITH MONTH END AUGUST SPREADERS AS THEY JOIN FORCES IN AN ATTEMPT TO TEMPER THE GOLD/SILVER PRICE GAINS. THE RAIDS ON OUR PRECIOUS METALS CONTINUED 5 WEEKS AGO WITH HUGE FURY AS WE FINALIZED THE LONDON/OTC OPTION EXPIRY FOR AUGUST AND THEY FOR THE FIRST TIME FAILED WITH RAIDS FINALIZATION ON AUGUST OPTIONS EXPIRY WEEK.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH AUGUST MONTH- END SPREADERS) IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD

NEW FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.3017 TONNES QUEUE JUMP TO GO ALONG WITH THE 0 TONNES OF EXCHANGE FOR RISK ISSUANCE // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 8.6314 TONNES//NEW TOTALS STANDING ADVANCES TO 18.8544 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 239 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.3017TONNES QUEUE JUMP AND 8.6314 TONNES OF EXCHANGE FOR RISK ISSUANCE//PRIOR:

THAT IS;

A) 0 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY//TOTAL FOR MONTH: 8.6314 TONNES

B) 0.3017 TONNES TODAY QUEUE JUMP

TOTALS: 18.8544 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 330 EFP CONTRACT WAS ISSUED: : /DEC 330 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 330 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY

- MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A SMALL SIZED SIZED 882 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S STRONG GAIN IN PRICE IN GOLD AND A CORRESPONDING HUGE GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

2) AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES30

3) TO BE FOLLOWED BY SEPTEMBER’S 2 ISSUANCES FOR EXCHANGE FOR RISK FOR 8.6314 TONNES.

STANDING FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT: 10.223 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) + 0 TONNES EX FOR RISK TODAY_//TOTAL FOR MONTH = 8.6314//NEW TOTALS FOR GOLD STANDING SEPT = 18.8544 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $22.70./ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A SMALL SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE LONGS PILING IT ON TRYING TO OBTAIN BADLY NEEDED GOLD DESPITE THE RAID///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH LAST WEEK’S TRADING!! THIS IS THE FIRST TIME THAT THE CROOKS COULD NOT MUSTER A RAID ON OPTIONS EXPIRY LONDON/OTC AUGUST TRADING. THEIR RAID ON OUR PRECIOUS METALS CAUSED NO DAMAGE TO OUR PRICE.

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

DETAIL SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH SEPTEMBER TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FEBRUARY IS THE SECOND HIGHEST ISSUANCE OF EXCHANGE FOR RISK AS AUGUST BECOMES THE HIGHEST EVER RECORDED AS YOU WILL SEE BELOW!

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH 3 ISSUANCES

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRIL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE: 3

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: 7 ISSUED,

TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 44.696 TONNES, THE HIGHEST MONTHLY EVER COMEX ISSUANCE!!!!!!

THUS 107.5117 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS/EX FOR PHYS TRANSFERS) + 44.696 TONNES EX FOR RISK = 152.208 TONNES.

SEPTEMBER: 2 ISSUED:

THE CME NOTIFIED US THAT OUR TWO ISSUANCE OF EXCHANGE FOR RISK EQUATES TO 2725 CONTRACTS FOR 272,500 OZ OR 8.6314 TONNES. WE WILL PROBABLY HAVE A DOOZY FOR SEPT DELIVERIES AS EITHER THE BANK OF ENGLAND OR THE BIS (LOANED TO THE FRBNY) WANTS ITS GOLD BACK+ THE MASSIVE QUEUE JUMPING BY OTHER CENTRAL BANKS

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A SMALL SIZED GAIN TOTAL OF 2.867 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 0.3017 TONNES OF GOLD ALONG WITH 8.6314 TOTAL TONNES OF EXCHANGE FOR RISK TOTAL FOR MONTH (TODAY’S EX FOR RISK ISSUANCE = 0 TONNES EXCHANGE FOR RISK) AND THUS NEW TOTALS EX FOR RISK MONTH = 8.6310//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 18.8544 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $22.70

WE HAD 8157 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 922 CONTRACTS OR 92200 0Z (2.867 TONNES)

confirmed volume THURSDAY 254,684 contracts// fair//

speculators have left the gold arena

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

SEPT 5 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2 entries I) Out of Brinks 79,781.925 oz II) Out of JPMorgan 45,286.300 oz total withdrawal: 120,568.725 oz . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRIES i) Into Loomis: 1075,315.020 oz total deposit 1,075,315.020 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 529 notice(s) 52,900 OZ 1.6454 TONNES |

| No of oz to be served (notices) | 161 contracts 16,100 OZ 0.5007 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3126 notices 312,600 oz 9.723 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0 entries

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRIES

i) Into Loomis: 1075,315.020 oz

total deposit 1,075,315.020 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

2 entries

I) Out of Brinks 79,781.925 oz

II) Out of JPMorgan 45,286.300 oz

total withdrawal: 120,568.725 oz

ADJUSTMENTs 0

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 690 CONTRACTS FOR A GAIN OF 84 CONTRACTS. WE HAD 13 CONTRACTS FILED ON THURSDAY SO WE GAINED 97 CONTRACTS OR 97000 OZ ENTERTAINED A QUEUE JUMP OF 0.3017 TONNES. WE NOW MUST ADD OUR INITIAL 2.333 TONNES OF GOLD ISSUED UNDER EXCHANGE FOR RISK/PRIOR TO YESTERDAY’S 6.299 TONNES/NEW EX FOR RISK = 8.63147//THUS NEW TOTAL OF GOLD STANDING REDUCES TO 18.8544 TONNES

OCTOBER LOST 826 CONTRACTS DOWN TO 60,937

NOVEMBER GAINED 80 CONTRACTS UP TO 2743 CONTRACTS.

We had 529 contracts filed for today representing 52,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 8 notices issued from their client or customer account. The total of all issuance by all participants equate to 529 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 35 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (3126 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 690 CONTRACTS) minus the number of notices served upon today (529 x 100 oz per contract) equals 328,700 OZ OR 10.223 TONNES OF GOLD TO WHICH WE ADD OUR INITIAL EX FOR RISK OF 8.632 TONNES//NEW TOTAL STANDING REDUCES TO 18.8549 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (3126 x 100 oz +we add the difference for front month of SEPT. (690 OI} minus the number of notices served upon today (529 x 100 oz) which equals 328,700 OZ OR 10.223 TONNES PLUS 8.632 TONNES EXCHANGE FOR RISK = 18.8544 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 18.8544 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,049,534.159 oz 63.756 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,957,797.857 oz

TOTAL REGISTERED GOLD 21,304,588.071 or 662.662 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,653,209.786 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,255,054 oz ((REG GOLD- PLEDGED GOLD)= 598.91 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 5 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries: i) Out of Delaware: 3898.140 oz ii) Out of HSBC 80,325.460 oz total withdrawal 84,223.600 oz |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Stonex 1135,107.020 oz total deposit1135,107.02 oz |

| Deposits to the Customer Inventory | 1 DEPOSIT ENTRY/CUSTOMER ACCOUNT i) Into CNT 294,847.600 oz total deposit 294,877.600 oz |

| No of oz served today (contracts) | 32 CONTRACT(S) (0.160 million OZ |

| No of oz to be served (notices) | 1085 contracts (5.465 MILLION oz) |

| Total monthly oz silver served (contracts) | 10,015 Contracts (50.075 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

i) Into Stonex 1135,107.020 oz

total deposit1135,107.02 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

1 DEPOSIT ENTRY/CUSTOMER ACCOUNT

i) Into CNT 294,847.600 oz

total deposit 294,877.600 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

2 entries:

i) Out of Delaware: 3898.140 oz

ii) Out of HSBC 80,325.460 oz

total withdrawal 84,223.600 oz

ADJUSTMENTs 1

i) Customer to dealer; Manfra 49,720.860 oz

TOTAL REGISTERED SILVER: 195.284 MILLION OZ//.TOTAL REG + ELIGIBLE. 518.368 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 1117 OPEN INTEREST CONTRACTS FOR A LOSS OF 663 CONTRACTS. WE HAD 723 CONTRACTS SERVED YESTERDAY SO WE GAINED A STRONG 60 CONTRACTS OR 0.3000 MILLION OZ ENTERTAINED A QUEUE JUMP//NEW STANDING FOR SILVER COMEX ADVANCES TO 55.500 MILLION OZ.

STANDING FOR SILVER: 55.500 MILLION OZ

OCTOBER LOST 9 CONTRACTS TO 2492

NOVEMBER GAINED 137 CONTRACTS UP TO 1368.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:32 or 0.160 MILLION oz

CONFIRMED volume; ON THURSDAY 71,062 strong//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 10,015 X5,000 oz = 50.075 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (1117) AND the number of notices served upon today (32 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (10,015) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(1117) minus number of notices served upon today (32)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 55.500 MILLION OZ .

New total standing: 55.500 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 195.284 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/518.368 million. 40.59%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 30 WITH GOLD DOWN $27.50 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 29 WITH GOLD UP $16.45 TODAY//SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.86 TONNES OF GOLD FROM THE GLD/ //// ///INVENTORY RESTS AT 956.23 TONNES/

JULY 28 WITH GOLD DOWN $24.00 TODAY//NO CHANGES IN GOLD AT THE GLD: //// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 25 WITH GOLD DOWN $37.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: A HUGE DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 957.09 TONNES/

JULY 24 WITH GOLD DOWN $17.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD: NO CHANGES AT THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 23 WITH GOLD DOWN $40.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 7.74 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 954.80 TONNES/

JULY 22 WITH GOLD UP $36.60 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 947.06 TONNES/

JULY 21 WITH GOLD UP $40.30 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A FRAUDULENT WITHDRAWAL OF 4.87 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 943.63 TONNES/

JULY 18 WITH GOLD UP $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.29 TONNES OF GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 948.50 TONNES/

JULY 17 WITH GOLD DOWN $11.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 950.79 TONNES/

JULY 16 WITH GOLD UP $22.70 TODAY//NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 947.64 TONNES/

JULY 15 WITH GOLD DOWN $20.80 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 947.64 TONNES/

JULY 14 WITH GOLD UP $0.90 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

JULY 11 WITH GOLD UP $32.35 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.44 TONNES OF GOLD INOT THE GLD //: /// ///INVENTORY RESTS AT 948.81 TONNES/

GLD INVENTORY: 984.26 TONNES, TONIGHTS TOTAL

SILVER

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

JULY 30 WITH SILVER DOWN $0.54/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487.852 MILLION OZ.//

JULY 29 WITH SILVER UP $0.11/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.211 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 487.398 MILLION OZ.//

JULY 25 WITH SILVER DOWN $0.84/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 24 WITH SILVER DOWN $0.11/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 488.942 MILLION OZ.//

JULY 23 WITH SILVER DOWN $0.04/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 4.906 MILLION OZ INTO THE SLV//:.////INVENTORY RESTS AT 487.353 MILLION OZ.//

JULY 22 WITH SILVER UP $0.20/ HUGE CHANGES AT THE SLV// A FRAUDLENT DEPOSIT OF 11.175 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 482.447 MILLION OZ.//

JULY 21 WITH SILVER UP $0.78/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 471.272 MILLION OZ.//

JULY 18 WITH SILVER UP $0.13/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.998 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 472.453 MILLION OZ.//

JULY 17 WITH SILVER UP $0.22/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 476.451 MILLION OZ.//

JULY 16 WITH SILVER UP $0.09/ HUGE CHANGES AT THE SLV// A FRAUDLENT WITHDRAWAL OF 3.543 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 477.632 MILLION OZ.//

JULY 15 WITH SILVER DOWN $0.65/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 481.175 MILLION OZ.//

JULY 14 WITH SILVER UP $0.14/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

JULY 11 WITH SILVER UP $1.42/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 2.453 MILLION OZ OUT OF THE SLV//:.////INVENTORY RESTS AT 478.722 MILLION OZ.//

CLOSING INVENTORY 491.308 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

Schiff: Trump’s Wrong; “We Screw Over The World” On Trade

Friday, Sep 05, 2025 – 12:05 PM

Donald Trump’s tariffs split opinion—champions said they were leverage to rebuild U.S. industry, while critics argued they were hidden taxes that raised costs and invited retaliation. At last night’s ZH Debate, Cornell chemistry professor Dave Collum — fresh off his Tucker Carlson controversy — moderated as Peter Schiff and Brent Johnson squared off on trade, tariffs, and the future of the dollar.

Brent is no fan of tariffs but thinks there is some wisdom to Trump’s long-term plan and that the U.S. dollar still reigns supreme. Peter… well all ZH readers know where Peter stands.

Below were the key moments for those short on time:

Trump Has Trade Deficits Wrong

Peter Schiff argued that America’s trade deficits are misunderstood. “It’s actually the other way around,” he said, pushing back on Donald Trump’s claim that the U.S. is being taken advantage of. “We take advantage of the world. They give us goods produced at significant cost in resources, land, labor, capital… and all we do is run off dollars on a printing press, cost us nothing, and we give it to them.”

Brent Johnson responded that this imbalance is exactly what comes with America’s position. “That’s the privilege of being the hegemon as you get global.”

Schiff countered that such privilege is temporary. “It’s the privilege that we are about to lose. That’s what $3,500 gold tells you. Dollar is on the way out as the reserve currency.”

“I expect Powell to lose”

Brent went on record with a bold call that included something rarely seen in market commentary: timing.

He predicts — as soon as October — a 10 or 20% market downturn… perhaps welcomed by the Trump admin so they can blame the Fed and lower rates.

“To get the cover to do that, they need some pain. I don’t think they can do that right now with things the way they already are.”

“Some kind of a crisis that they blame on the Fed, and then they go back to even easier monetary policy than maybe they had last time. And that is what then gives the fuel to go much higher.”

With markets at record highs and inflation still sticky, “it’s really hard to do it now.”

Brent’s prediction: “I think Powell is pushing back a little bit. But this is the thing—I expect Powell to lose. I think Trump and Bessent are going to get control.”

Watch the full debate below or listen on Spotify for more fun moments like this one…

Schiff on the world’s attitude towards the U.S. dollar once rates drop: “Shove it up your ass.”

Full Debate (X, YT, and Spotify):

Secure your wealth against inflation with JM Bullion.

JOHN RUBINO

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

Gold and silver bullish

There’s growing appreciation that the gold and silver bull has returned, though the reasons justifying it may not be apparent. But this week’s price action is an important turning point.

| Alasdair MacleodSep 5∙Paid |

There are important factors in the background driving the relationship between monetary metals, the dollar, and the other major G7 currencies. These include geopolitics: this week saw plans advancing for a non-dollar (and G7) currency area incorporating the Shanghai Cooperation Organisation, BRICS, and those nations in the queue to join, representing 70% of the world’s population. Additionally, there is a developing G7 bond crisis as the debt bubble hits the buffers. And technical analysis tells us that gold and silver prices are going potentially far higher.

Gold and silver appear to be front-running major changes in the relationship between G7 currencies and the consequences of these tectonic shifts. It is in this context that this week’s performance should be read.

Gold and silver chose a four-day week in the US (Monday was Labor Day) to break out of holding patterns, putting a dramatic squeeze on Comex futures. In European trade this morning, gold was $3550, up $102 from last Friday’s close, and silver was $40.77, up $1.02 over the same timescale.

Having been subdued since early-April, Comex open interest in the gold contract increased by about 50,000 contracts as momentum traders in the managed money category began to buy. With the relationship to price, this is shown in our next chart.

This is a return to normal bull market conditions, with buying rather than short covering driving the price.

However, the swaps will be careful not to be squeezed, raising prices to discourage buyers. We can only assume that their short positions on Comex are roughly covered by long positions in London’s forward market. Less commented on are the shorts in the speculator categories. The latest COT report (26 August) showed 33,577 managed money shorts, 27,879 other reported shorts, and 20,058 non-reported shorts for a total of 81,514. Some of these are bound to have been closed since that date, but what remains will be suffering pain.

To summarise, the set up remains bullish with plenty of shorts yet to be squeezed into covering. Furthermore, the fiasco earlier this year at the Bank of England’s vault will have convinced central banks to desist in leasing activities, so physical liquidity will remain extremely tight, as the declining trend of vault data from the bank illustrates:

The technical position is bound to encourage more speculative buying, and this chart is next:

The chart pattern is unequivocally bullish, with a minimum projection to $4,300. As to why this is justified on fundamentals, momentum traders are unlikely to care. But political pressure on the Fed to reduce rates coupled with a stalling economy plus increasing price inflation is probably enough reason for most.

Additionally, stubbornly high long bond yields in the US and elsewhere forces central banks to fund government debt at short maturities. While lower interest rates will reduce funding costs in treasury bills, it means that increasing quantities of debt need to be rolled over in addition to new funding. Long term, this is bound to be a problem. Short term, it encourages the Fed and other central banks to cut rates as much as they dare, which undermines the currency and increases gold and silver prices.

Silver’s chart is equally bullish with the breakout obvious:

Furthermore, there is the prospect of the gold/silver ratio declining. The g/s chart tells us very little, but as gold rises, on average silver rises almost twice as fast. Furthermore, the decline of the fiat dollar as the world’s reserve currency should draw increasing attention to silver’s monetary qualities, pushing the gold/silver ratio considerably lower. With gold at $4000 and a ratio of 50, that makes silver $80. This is not a forecast, only an illustration of silver’s potential.

Finally, the dollar’s trade weighted chart shows the dollar poised for its next move down against other currencies, principally the euro and yen, hardly paragons of virtue themselves:

A move lower with lower interest rates is Trump’s stated objective and that of the so-called Mar-o-Largo accord devised by Stephen Miran, whose appointment to the Fed’s board is before Congress.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 239

a must view:

5. COMMODITY REPORT GOLD

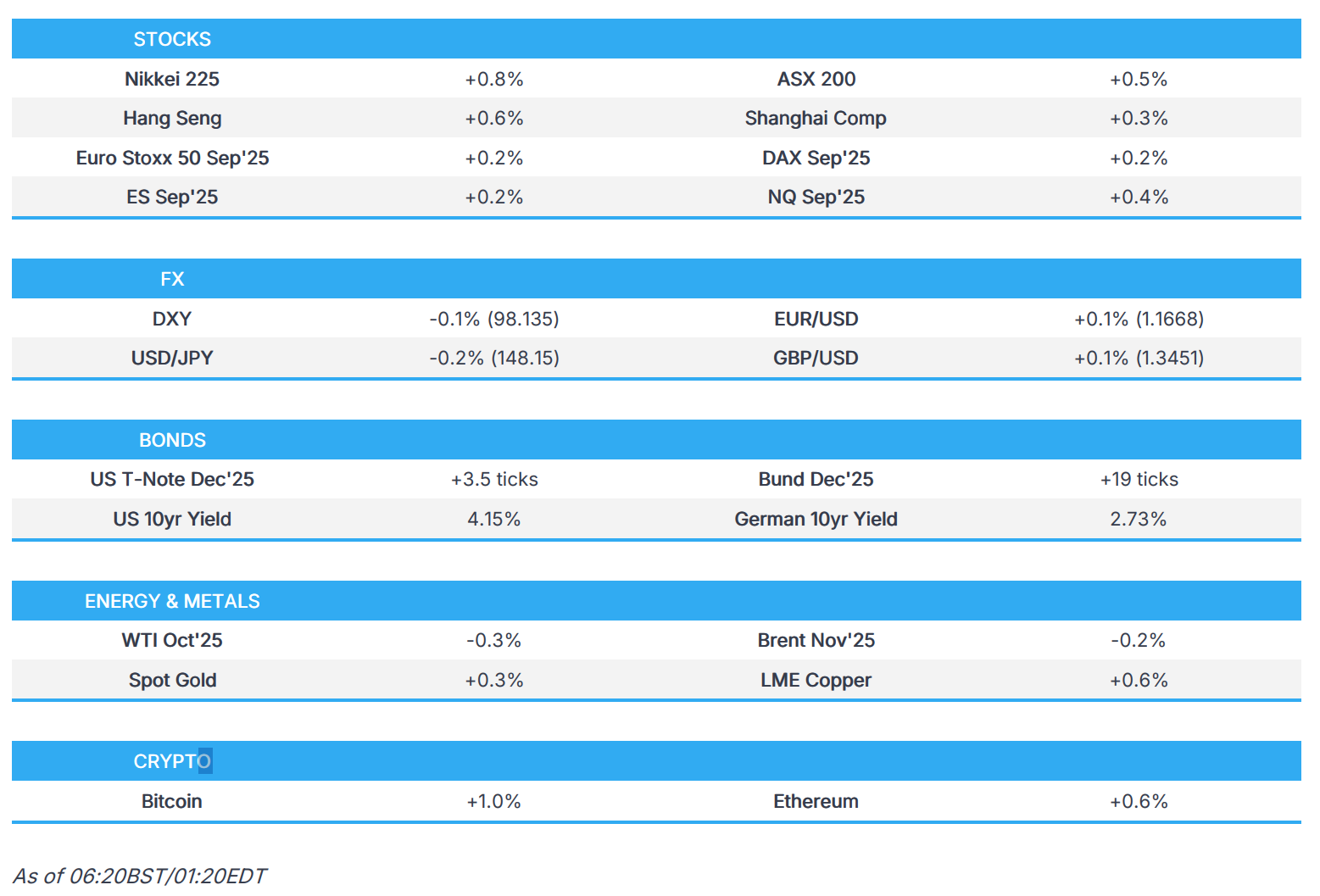

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED UP 46.24 PTS OR 1.24%

//Hang Seng CLOSED UP 357.25 PTS OR 1.43%

// Nikkei CLOSED UP 438.48 PTS OR 1.03% //Australia’s all ordinaries CLOSED UP 0.90%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1377 OFFSHORE CLOSED UP AT 7.1343/ Oil DOWN TO 63.23 dollars per barrel for WTI and BRENT DOWN TO 66.74 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1377 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1343 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1377

OFFSHORE YUAN: UP TO 7.1343

HANG SENG CLOSED UP 357.25 PTS OR 1.43%

2. Nikkei closed UP 438.48 PTS OR 1.03%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 98.05 EURO RISES TO 1.1674 UP 17 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.575//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.21…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.237 DOWN 2 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7120 Italian 10 Yr bond yield DOWN to 3.582 SPAIN 10 YR BOND YIELD DOWN TO 3.290

3i Greek 10 year bond yield DOWN TO 3.415

3j Gold at $3548.15 Silver at: 40.76 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 12 /100 roubles/dollar; ROUBLE AT 81.41

3m oil (WTI) into the 63 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.21/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.575% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.237 DOWN 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8038 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9383 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.165 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.857 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.590 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.26

10 YR UK BOND YIELD: 4.7220 DOWN 1 PTS ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.567 DOWN 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.347 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.903 UP 0 BASIS PTS.

2a New York OPENING REPORT

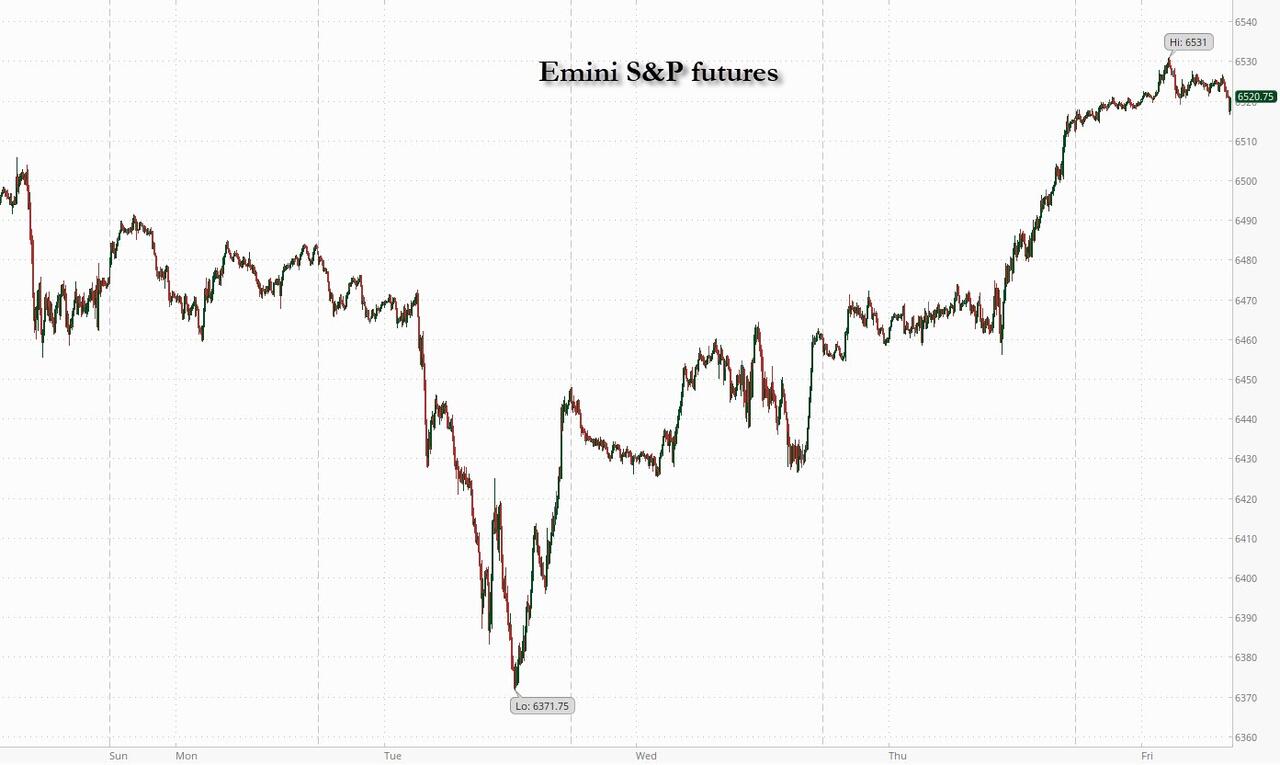

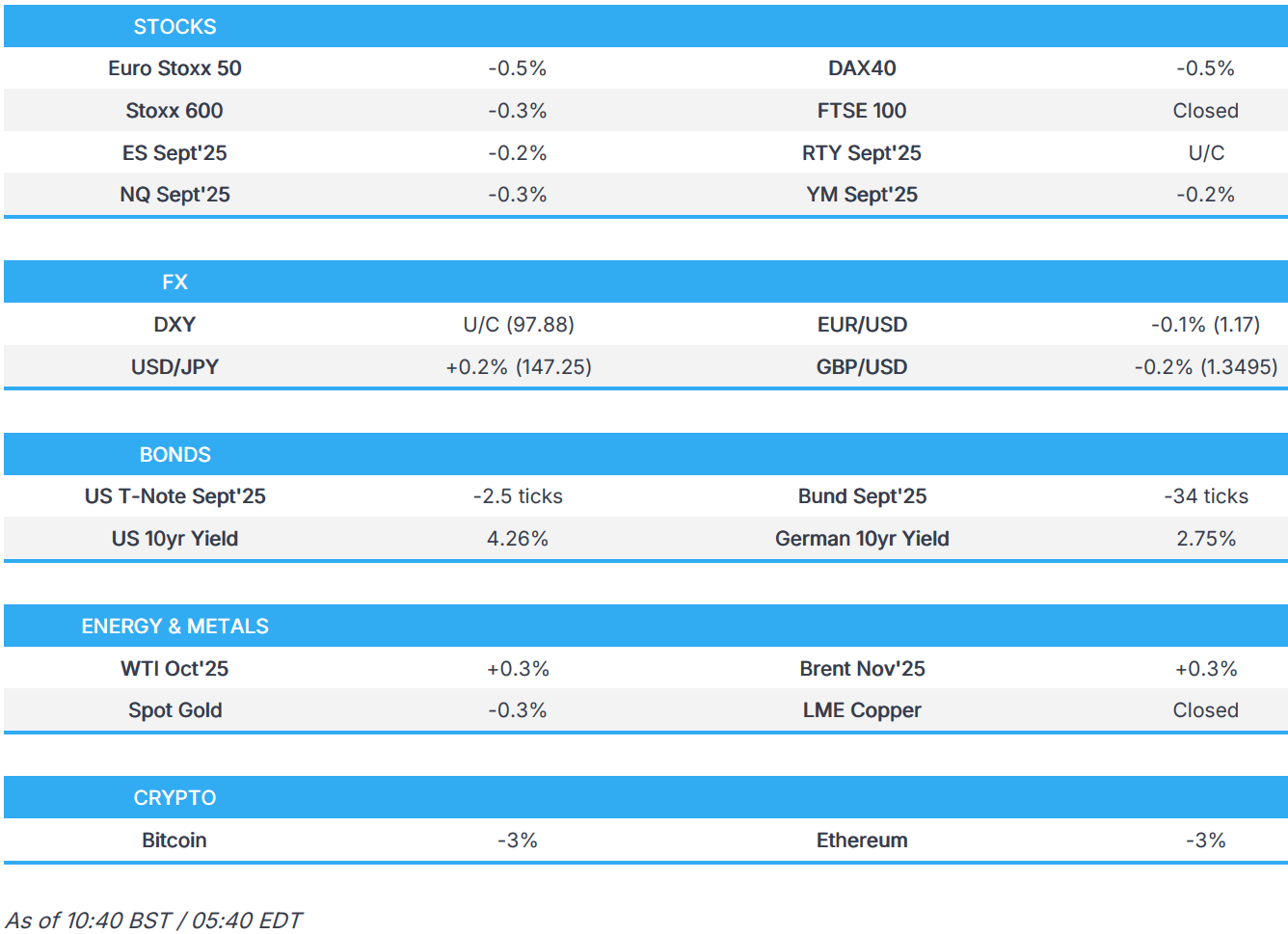

Futures Rise Further Into Record Territory Ahead Of Jobs Report

Friday, Sep 05, 2025 – 08:23 AM

US equity futures are higher into NFP, rising after strong results from Broadmcom and on optimism that Friday’s jobs report will set the stage for the Fed to resume cutting interest rates this month. At 8:00am, futures for the S&P 500 ticked 0.1% higher – reaching a new record high – but eased off the best levels of the session. Nasdaq contracts advanced 0.5%. In premarket trading, Broadcom rallied more than 9% following its pact with OpenAI to create an artificial-intelligence chip. Tesla rose 2% after the board proposed a potentially $1 trillion pay package for Elon Musk. US Treasuries were little changed, with the two-year yield near the lowest in almost a year. The dollar headed for its weakest showing this week. Commodities are mixed: oil and base metals are lower, while gold and ags are mostly higher.

In premarket trading, Mag 7 stocks are mixed (Tesla +2%, Meta Platforms +0.3%, Microsoft +0.2%, Apple -0.1%, Amazon -0.3%, Alphabet -0.1%, Nvidia -0.8%) as Broadcom (AVGO) soars 11% after the chipmaker is said to be helping OpenAI design and produce an artificial intelligence accelerator from 2026. It also said that its artificial intelligence outlook will improve “significantly” in fiscal 2026.

- Crypto-linked stocks rose with Bitcoin and Ether prices up as broader markets gain on hopes that US jobs data on Friday will increase the chances of a Federal Reserve interest rate cut later this month. Coinbase (COIN) +1.2%, Riot Platforms (RIOT) +1.8%, Bitdeer Technologies (BTDR) +2.7%

- BioNTech ADRs (BNTX) gains 10% after the drugmaker said a late-stage trial of an experimental therapy for breast cancer met its primary endpoint.

- Braze (BRZE) climbs 18% as the cloud software company beat its second-quarter revenue and third-quarter revenue forecast estimates. An analyst at Needham notes that AI is seen to be a growth driver. .

- DocuSign (DOCU) rises 6.6% after the e-signature company reported second-quarter results that beat expectations and raised its full-year forecast.

- Guidewire (GWRE) is up 14% after forecasting revenue for the first quarter above the average analyst estimate.

- Lululemon (LULU) falls 18% after slashing its outlook, disappointing investors for a third straight quarter as the company struggles to meet high expectations and balance tariff expenses in a difficult consumer environment.

- Samsara (IOT) is up 12% as the US hardware-software platform company boosted its adjusted earnings guidance for the full year.

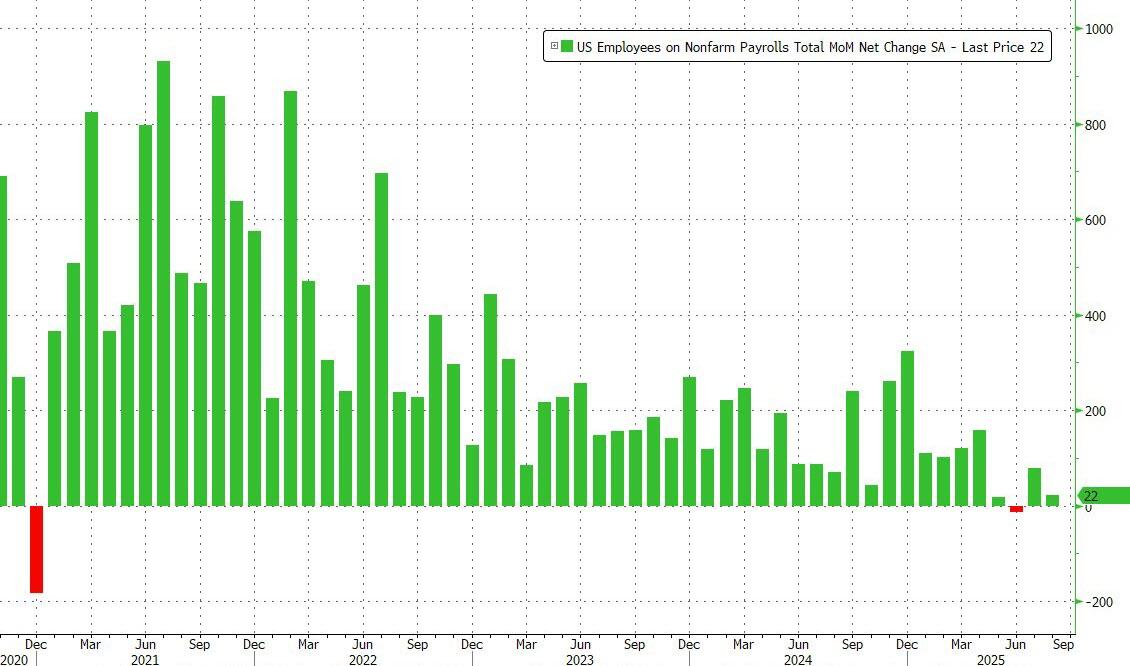

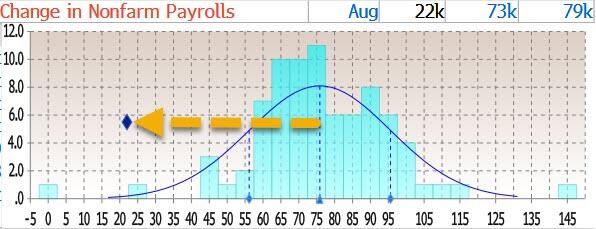

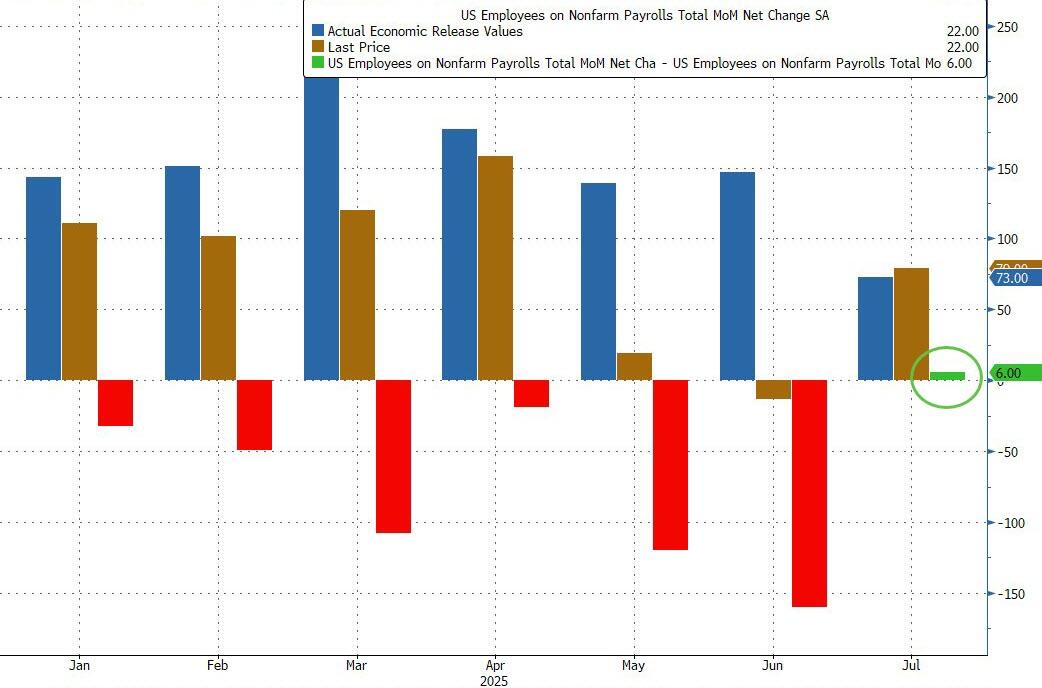

Investors are riding high ahead of today’s nonfarm payrolls report, with hopes it will strike the balance of a softer labor market that clears the way for policy easing without undercutting confidence in the economy. A bigger surprise in either direction could unsettle markets.

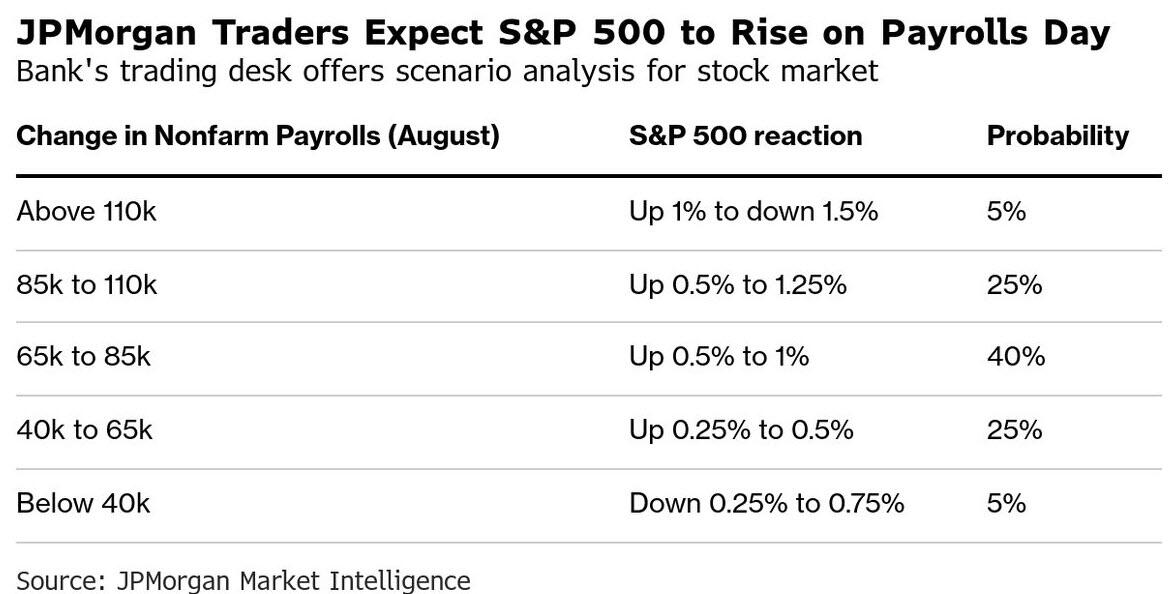

August payrolls are projected to rise by roughly 75,000, extending a four-month streak of job growth below 100,000. The unemployment rate is seen climbing to 4.3%, the highest since 2021 (our full preview is here). JPMorgan Market Intel estimates a better than 90% chance that the S&P 500 will advance following the payrolls report. Although the data is unlikely to sway the September decision, a weaker-than-expected print could amplify calls for a 50 basis-point cut, the team led by Andrew Tyler noted earlier this week. While softer numbers may briefly stoke recession fears, the bank notes that the real risk lies in a substantially stronger-than-expected report.

“Today’s release is unlikely to show the kind of pronounced weakness that would force the Fed to accelerate its easing plans,” wrote Max McKechnie, global market strategist at JPMorgan Asset Management. “Instead, investors should focus on the unemployment rate and wage growth for a clearer sense of the Fed’s next steps.”

The run-up to today’s payrolls report has brought a raft of data signaling a slowdown in the labor market. Fed Chair Jerome Powell cautiously opened the door to a first rate cut for 2025 in his Jackson Hole speech, citing risks to the jobs backdrop even as inflation concerns persist.

Some investors are approaching the release cautiously after recent revisions showed significantly weaker growth than previously reported. The downward adjustments, published with the July report, also led US President Donald Trump to dismiss the head of the Bureau of Labor Statistics, raising concerns about the integrity of data going forward. Stretched valuations also argue for restraint.

“We’re at a pivotal moment not only on growth and the labor market but also on inflation,” said Patrick Brenner, chief investment officer of multi-asset at Schroders Plc. “The market is priced for perfection and so we’re taking a wait-and-see approach by taking profits on our equity position.”

European stocks rise for a third straight session as investors await key US payrolls data later in the day. The Stoxx 600 rose 0.3% to 551.97 with the FTSE 100 outperforming European peers. The CAC 40 lagged, flat on the day. Miners, industrials and tech led sector moves. Dutch chip equipment maker ASML gains after an upgrade at UBS. Here are some of the biggest movers on Friday:

- ASML shares rise as much as 2.9% after UBS upgraded the firm to buy from neutral, noting that the factors that have seen the Dutch semiconductor equipment maker underperform over the past year are now priced in.

- Hexagon gains as much as 7.7% after the Swedish industrial design and measurement firm announced it would sell its design and engineering (D&E) unit to Cadence Design Systems for €2.7 billion ($3.2 billion).

- Berkeley Group rises as much as 2.5% as the housebuilder reassures that trading has been stable over the first four months of the year. Peers Persimmon, Taylor Wimpey, Bellway, Vistry, Barratt Redrow and Crest Nicholson also rise.

- Sixt gains as much as 6.9% after being initiated with a buy recommendation at UBS, with the bank saying the market underestimates tailwinds from better fleet management as well as US market-share gains.

- Ashmore shares fall as much as 15% after full-year results from the UK asset manager missed analyst estimates.

- Temenos shares drop as much as 14% after the Swiss banking software provider dismissed CEO Jean-Pierre Brulard, naming CFO Takis Spiliopoulos as his successor and interim CEO.

- Orsted falls as much as 2.2% after the wind farm developer cut its Ebitda excluding items forecast for the full year.

- BioArctic shares drop as much as 13% after Nordea analysts cut their recommendation on the Swedish biopharma company to sell from hold, setting their price target at a Street-low.

Earlier in the session, Asian stocks rose, on track for a weekly advance, supported by a rebound in Chinese equities as well as bullish sentiment around a US-Japan trade deal. The MSCI Asia Pacific Index gained as much as 1.2% in Friday’s session, set to finish higher on the week. China’s benchmark CSI 300 Index rose more than 2% after a three-day selloff. Stocks in Hong Kong, Japan, South Korea and Taiwan also advanced. Chinese stocks are bouncing back as investors mull the week’s events, including President Xi Jinping’s strengthening ties with India and North Korea as well as market policy proposals. Regulators are considering measures to curb the speed of the rally in its stock market, which may introduce more stable structural growth. Elsewhere in the region, Thailand got a new prime minister, with parliament electing Anutin Charnvirakul on Friday. Thailand’s stock index gained to its highest since mid-August. Shares in India traded lower, dragged by information technology firms.

In FX, the Bloomberg Dollar Spot Index edged down 0.3%, trimming its weekly gain. Markets have almost fully priced a Fed rate cut in September, with a follow-up reduction cemented by year-end, according to swaps data compiled by Bloomberg

In rates, Treasuries are steady with yields close to Thursday’s closing levels as investors wait for the August payrolls data and the potential impact on expectations for the September FOMC decision. Treasury yields marginally richer on the day, underpinned by gilts, where a broader bull-flattening move has been seen over the early London session. US 10-year yields trade around 4.15%, with gilts outperforming by 1bp in the sector and bunds trading broadly in line. Ahead of the jobs report, Fed-dated OIS is pricing in around 23bp of easing for the September policy meeting. For nonfarm payrolls change, which was 73k in July, the Bloomberg survey median estimate is 75k, matching the crowd-sourced whisper number. French and UK bonds advanced, while bunds were little changed.

In commodities, WTI held near $63.44 and gold added about $3 to $3,548/oz. Bitcoin gained another 2%.

Today’s US economic data slate includes only the August jobs report at 8:30am. The Fed speaker slate is empty for the session, and external communications blackout ahead of Sept. 17 rate decision begins Saturday

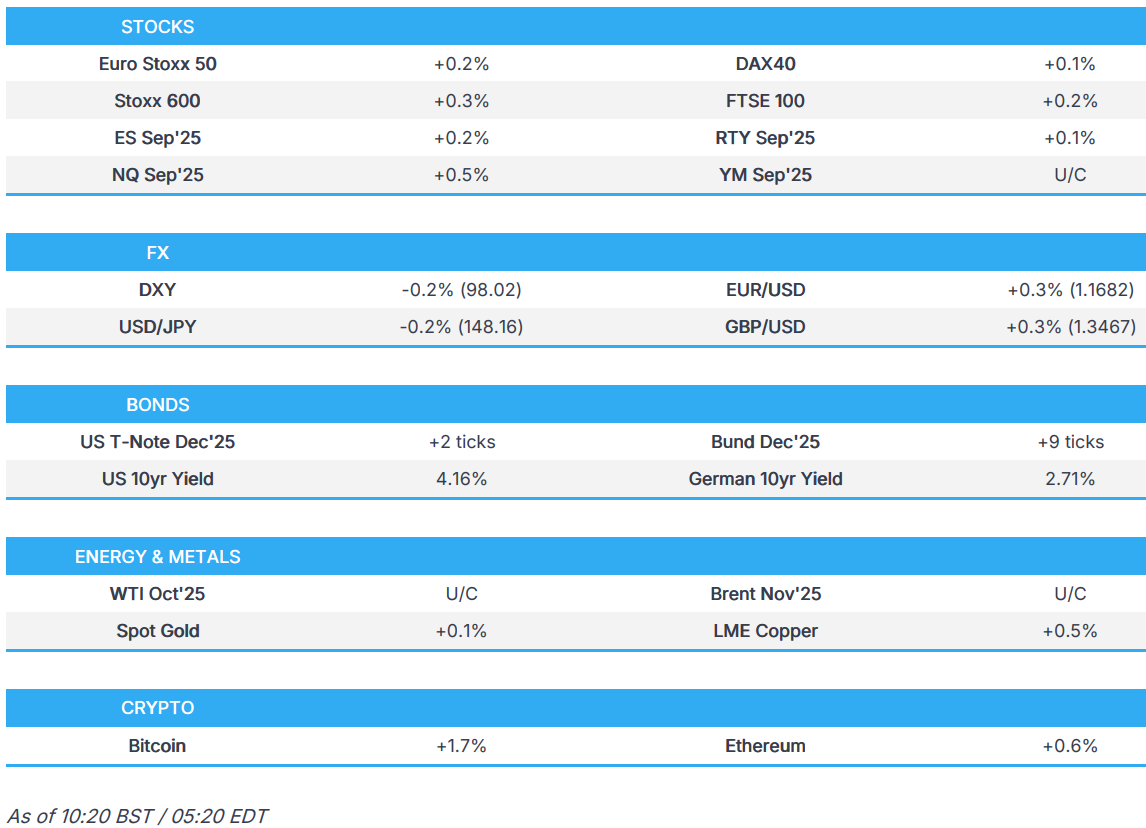

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.5%

- Russell 2000 mini +0.1%

- Stoxx Europe 600 +0.2%

- DAX +0.1%

- CAC 40 little changed

- 10-year Treasury yield little changed at 4.16%

- VIX -0.1 points at 15.24

- Bloomberg Dollar Index -0.3% at 1203.5

- euro +0.4% at $1.1692

- WTI crude -0.3% at $63.32/barrel

Top Overnight News

- Trump signed an order implementing the US-Japan trade deal, imposing a 15% tariff on most imports. The pact requires Japan to set up a $550 billion US investment fund or risk higher levies. BBG

- At a White House dinner, Silicon Valley leaders including Mark Zuckerberg pledged to increase AI spending. Trump said he would soon impose tariffs on chip imports but exempt goods from companies such as Apple that are expanding their US investments. BBG

- Lisa Cook argued that Donald Trump’s attempt to fire her is a cover for his real motive — taking control of the Fed. She pointed to a court ruling that Trump’s purported concerns about antisemitism at Harvard were a “smokescreen” to target the university. BBG

- Congressional leaders begin formulating a short-term deal to avoid a gov’t shutdown on 10/1, but the two sides still have a lot to work through in the coming weeks. NYT

- China’s investors borrowed a record $322 billion to buy stocks this year, but sharp corrections this week and heightened regulatory scrutiny to cool overheated markets are now making them jittery about the leveraged bets. While risks for China’s broader financial system have been elevated for months due to deflation in the economy and a persistent property debt crisis, the stock investors’ recent actions could add more pressure. RTRS

- Japan’s nominal wages rose by a more-than-expected 4.1% in July from a year earlier, the fastest clip in seven months. Separately, prefectures nationwide will raise the minimum hourly wage by a record 6.3%. BBG

- U.K. retail sales increased at the start of the third quarter, a boost as the country looks to get some momentum into its sluggish economy. Retail sales came in at +0.5% M/M (vs. the Street +0.3%). WSJ

- German factory orders unexpectedly slumped in July, as weaker foreign orders reflected a fragile export market amid increased trade barriers. Factory orders came in at coming in -2.9% M/M (vs. the Street +0.5%). WSJ

- Trump is to sign an order on Friday to rename the Department of Defense to the Department of War, according to a White House official. However, a CBS News reporter noted regarding President Trump signing an executive order to rename the Department of Defense to the Department of War, that it will be a secondary title as an official name change requires an Act of Congress.

- US House Speaker Johnson has, in an interview with Punchbowl, opened the door somewhat to extending Obamacare subsidies that are scheduled to expire at end-2025.

- Fed’s Goolsbee (2025 voter) said the labor market might be deteriorating and inflation might be picking back up, while he added there is a bit of wait and see because of uncertainty and that rates are better indicators for the labour market than raw job growth. Goolsbee also commented that the impact of tariffs on price increases is dependent on sector and noted the September Fed meeting is a live meeting, but he hasn’t made up his mind.

Trade/Tariffs

- US President Trump said he would be placing chip tariffs “very shortly,” which will be “fairly substantial”, but signalled Apple (AAPL) and others will be safe during his dinner with tech CEOs at the White House on Thursday, according to CNBC.

- US President Trump is reportedly preparing to start North American trade deal renegotiations and public consultations on the key US trade deal with Mexico and Canada, which will be the first acts of a likely lengthy and contentious review, according to WSJ.

- White House said US President Trump signed an Executive Order officially implementing the US-Japan trade agreement, while it added that Japan is working towards an expedited implementation of a 75% increase of US rice procurements and the US will apply a baseline 15% tariff on nearly all Japanese imports. It was later reported that Japan and the US issued a memorandum of understanding on the USD 550bln plans with investments to be made up to January 19th, 2029.

- Japanese PM Ishiba reiterated they will work to minimise the impacts on the economy and employment, while he added the US and Japan tariff agreement is very meaningful and it is important to implement the agreement sincerely and promptly.

- Japan’s top trade negotiator Akazawa said Japan agreed to issue joint statements on the US request and they signed an MOU on Japan’s investment package. Akazawa said nothing had changed from the July 22nd agreement with regards to the USD 550bln investment package and the amended executive order does not mention most-favoured-nation treatment for pharma and chips, and will continue to push for the treatment. Furthermore, he said their stance that additional tariffs themselves are regrettable remains unchanged, as well as stated that lower auto tariffs will take effect within up to two weeks.

- Anthropic is to stop selling AI services to majority Chinese-owned groups and is trying to limit the ability of Beijing to use its technology to benefit China’s military and intelligence services, while Anthropic’s policy will also apply to US adversaries including Russia, Iran and North Korea, according to FT.

- Indian oil skips US crude and buys Nigerian and Middle Eastern oil via tender, according to Reuters sources.

- Swiss Economy Minister set to visit the US this weekend, according to EconomieSuisse.

A more detailed look at global markets courtesy of Newsquawk