XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

FROM MY no 4 SON STEPHEN //THROUGH AI: ENJOY

099 H DEUTSCHE BANK AG 219

118 H MACQUARIE FUTURES US 23

323 C HSBC 13

332 H STANDARD CHARTERED B 1

363 H WELLS FARGO SECURITI 35

661 C JP MORGAN SECURITIES 15 171

905 C ADM 9

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 243 CONTRACTs NOTICES FOR 24300 OZ or 0.7558 TONNES

total notices so far: 4600 contracts for 460,000 OR 14.308 tonnes)

SILVER NOTICES: 499 NOTICE(S) FILED FOR 2.495 MILLION OZ/

total number of notices filed so far this month : 12,303 CONTRACTS (NOTICES) for 61.515 million oz

A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD

INVENTORY RESTS AT 977.95 TONNES

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 24.675 MILLION OZ.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 62.785 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING) PLUS 3.0 MILLION OZ EX FOR RISK = 65.785 MILLION OZ. THIS IS THE FIRST ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.7216 TONNES PLUS 6.277 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 16.364//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 30.830 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 47.583 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE 2756 CONTRACTS OI TO 159,829 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 535 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 535 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 630 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2756 CONTRACTS AND ADD TO THE 535 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 3474 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.46 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 16.455 MILLION PAPER OZ

OCCURRED WITH OUR $0.46 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 4.71 PTS OR 0.12%

//Hang Seng CLOSED UP 301.84 PTS OR 1.16%

// Nikkei CLOSED UP 395.62 PTS OR 0.89% //Australia’s all ordinaries CLOSED UP .63%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1240 OFFSHORE CLOSED DOWN AT 7.1235/ Oil DOWN TO 62.26 dollars per barrel for WTI and BRENT DOWN TO 66.36 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1240 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1235 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A TINY SIZED 307 CONTRACTS TO 510,353 OI DESPITE OUR LOSS IN PRICE OF $7.50 WITH RESPECT TO THURSDAY’S // TRADING.. WE OF COURSE, LOST NO NET LONGS, DESPITE THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1661). WE HAD ZERO T.A.S. LIQUIDATION AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1968 CONTRACTS (OR 6.121 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD FOR THE 4TH TIME WITH MONTH A HUGE 2179 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 217,900 OZ (6.2777 TONNES) AND ALL OF THIS OCCURRED WITH A PRICE LOSS?????

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 3 MONTHS;

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW WEDNESDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

AND NOW:

SEPT:

SEPTEMBER: FOUR ISSUANCES SO FAR TOTALLING 5261 CONTRACTS OR 526,100 OZ OR 16.364 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW YESTERDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: FOUR ISSUANCES FOR 5261 CONTRACTS SO FAR FOR 526,100 OZ OR 16.364 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS AND :

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH SEPT//ONLY MISSING JUNE.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//FINAL

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1968 CONTRACTS DESPITE OUR STRONG LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1347 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DESPERATELY TRYING TO STOP GOLD’S ADVANCE AND THIS ENDS IN FAILURE. FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!!

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH PREVIOUS AUGUST MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.7216 TONNES QUEUE JUMP TO GO ALONG WITH THE 6.277 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 16.364 TONNES//NEW TOTALS STANDING ADVANCES TO 30.830 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 240 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

AND NOW SEPTEMBER:

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.7216 TONNES QUEUE JUMP AND 6.277 TONNES EXCHANGE FOR RISK TODAY// NEW TOTALS OF 16.364 TONNES OF EXCHANGE FOR RISK ISSUANCE/:

THAT IS;

A) 6.277 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY + 9.586 TONNES EX FOR RISK PRIOR =//TOTAL FOR MONTH: 16.364 TONNES EX FOR RISK!!

B) 0.7216 TONNES TODAY QUEUE JUMP

TOTALS: 30.364 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1661 EFP CONTRACT WAS ISSUED: : /DEC 1661 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1661 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY

- MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A FAIR SIZED SIZED 1677 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S STRONG GAIN IN PRICE IN GOLD AND A CORRESPONDING HUGE GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

2) AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

3) TO BE FOLLOWED BY SEPTEMBER’S 4 ISSUANCES FOR EXCHANGE FOR RISK FOR 16.364 TONNES.

STANDING AT THE COMEX FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

AND NOW SEPT:

SEPT: 14.466 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) + 6.277 TONNES EX FOR RISK TODAY+ 9.586 TONNES EX FOR RISK PRIOR =_//TOTAL EX FOR RISK// FOR MONTH = 16.364//NEW TOTALS FOR GOLD STANDING SEPT = 30.830 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A STRONG $7.50./ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE LONGS PILING IT ON TRYING TO OBTAIN BADLY NEEDED GOLD///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS) WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH LAST WEEK AND THIS WEEKS’S TRADING!! THIS IS THE FIRST TIME THAT THE CROOKS COULD NOT MUSTER A RAID ON OPTIONS EXPIRY LONDON/OTC AUGUST TRADING. THEIR RAID ON OUR PRECIOUS METALS CAUSED NO DAMAGE TO OUR PRICE.

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

DETAIL SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH SEPTEMBER TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FEBRUARY IS THE SECOND HIGHEST ISSUANCE OF EXCHANGE FOR RISK AS AUGUST BECOMES THE HIGHEST EVER RECORDED AS YOU WILL SEE BELOW!

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH 3 ISSUANCES

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRIL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAD 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE: 3

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WAS ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK ISSUED JULY 25 = 41.106 TONNES OF GOLD STANDING

AUGUST: 7 ISSUED,

TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 44.696 TONNES, THE HIGHEST MONTHLY EVER COMEX ISSUANCE!!!!!!

THUS 107.5117 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS/EX FOR PHYS TRANSFERS) + 44.696 TONNES EX FOR RISK = 152.208 TONNES.

SEPTEMBER: 4 ISSUED:

THE CME NOTIFIED US THAT OUR FOUR ISSUANCES OF EXCHANGE FOR RISK WITH TODAY’S ISSUANCE EQUATING TO 2179 CONTRACTS FOR 217,900 OZ FOR A TOTAL MONTH OF 16.364 TONNES. WE WILL PROBABLY HAVE A DOOZY FOR SEPT DELIVERIES AS THE BANK OF ENGLAND WANTS ITS GOLD BACK+ THE MASSIVE QUEUE JUMPING BY OTHER CENTRAL BANKS IS CERTAINLY ON DISPLAY TODAY’S 0.7216 TONNES QUEUE JUMP.

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 49.023 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 0.7216 TONNES OF GOLD ALONG WITH 6.277 TOTAL TONNES OF EXCHANGE FOR RISK TODAY/// TOTAL FOR MONTH TOTALS EX FOR RISK// MONTH = 16.364//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 30.830 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $7.50

WE HAD A MAMMOTH 13,793 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 307 CONTRACTS OR 30700 0Z (6.123 TONNES)

confirmed volume THURSDAY 236,381 contracts// fair//

speculators have left the gold arena

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

SEPT 12 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1.entries i) into Brinks 32.151 Brinks (1 kilobars) . |

| Deposit to the Dealer Inventory in oz | 0- |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 243 notice(s) 24,300 OZ 0.7538 TONNES |

| No of oz to be served (notices) | 51 contracts 5100 OZ 0.1586 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4600 notices 460,000 oz 14.308 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER 0

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entries

1.entries

i) into Brinks 32.151 Brinks

(1 kilobars)

ADJUSTMENTs 1

Brinks; added 2218.419 oz (69 kilobars) into eligible account

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 294 CONTRACTS FOR A LOSS OF 85 CONTRACTS. WE HAD 317 CONTRACTS FILED ON THURSDAY SO WE GAINED 232 CONTRACTS OR 23,200 OZ ENTERTAINED A QUEUE JUMP OF 0.7216 TONNES. WE NOW MUST ADD TO OUR INITIAL 2.333 TONNES OF GOLD STANDING TO TODAY’S QUEUE JUMP OF 0.7216 TONNES AND THEN ADD MONTH SEPT// EX FOR RISK = 16.364//THUS NEW TOTAL OF GOLD STANDING ADVANCES TO 30.830 TONNES

OCTOBER LOST 994 CONTRACTS DOWN TO 59,490

NOVEMBER GAINED 10 CONTRACTS UP TO 2943 CONTRACTS.

We had 243 contracts filed for today representing 24,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 15 notices issued from their client or customer account. The total of all issuance by all participants equate to 243 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 171 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (4600 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 294 CONTRACTS) minus the number of notices served upon today (243 x 100 oz per contract) equals 465,100 OZ OR 14.466 TONNES OF GOLD TO WHICH WE ADD OUR TOTAL EX FOR RISK/SEPT MONTH OF 16.369 TONNES//NEW TOTAL STANDING ADVANCES TO 30.830 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (4600 x 100 oz +we add the difference for front month of SEPT. (294 OI} minus the number of notices served upon today (243 x 100 oz) which equals 465,100 OZ OR 14.466 TONNES PLUS 16.364 TONNES EXCHANGE FOR RISK = 30.830 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 30.830 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,024,054.573 oz 62.956 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,914,490.822 oz

TOTAL REGISTERED GOLD 21,289,381.227 or 662.19 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,625,109.695 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,264,8458oz ((REG GOLD- PLEDGED GOLD)= 599.20 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 12 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries: i) Out of Stonex: 9952.980 oz total withdrawal 9952,980 oz |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Stonex: 545,022.650 oz total deposit 545,022.650 oz |

| Deposits to the Customer Inventory | 5 DEPOSIT ENTRIES/CUSTOMER ACCOUNT i)Into Asahi 1,255,203.880 oz ii) Into CNT 14,914.500 oz iii) into HSBC: 600,001.400oz iv) Into Loomis: 205,798.200 oz v) Into Stonex: 2045.800 o total deposit 2,374,755.800 oz |

| No of oz served today (contracts) | 499 CONTRACT(S) (2.495 million OZ |

| No of oz to be served (notices) | 254 contracts (1.270 MILLION oz) |

| Total monthly oz silver served (contracts) | 12,303 Contracts (61.515 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 ENTRY

i) Into Stonex: 545,022.650 oz

total deposit 545,022.650 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

5 DEPOSIT ENTRIES/CUSTOMER ACCOUNT

i)Into Asahi 1,255,203.880 oz

ii) Into CNT 14,914.500 oz

iii) into HSBC: 600,001.400oz

iv) Into Loomis: 205,798.200 oz

v) Into Stonex: 2045.800 o

total deposit 2,374,755.800 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 entries:

i) Out of Stonex: 9952.980 oz

total withdrawal 9952.980 oz

ADJUSTMENTs 2

a) Customer to dealer

Delawarfe: 15,225.660 oz

b) Dealer to customer Stonex: 655,516.271 oz

TOTAL REGISTERED SILVER: 196.654 MILLION OZ//.TOTAL REG + ELIGIBLE. 527.473 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 753 OPEN INTEREST CONTRACTS FOR A GAIN OF 204 CONTRACTS. WE HAD 153 CONTRACTS SERVED ON THURSDAY SO WE GAINED A STRONG 357 CONTRACTS OR 1.785 MILLION OZ ENTERTAINED A QUEUE JUMP//NEW STANDING FOR SILVER COMEX INCREASES TO 61.785 MILLION OZ. THEN WE MUST ADD OUR INITIAL ISSUANCE OF 600 CONTRACTS FOR EXCHANGE FOR RISK OR 3.0 MILLION OZ//NEW STANDING ADVANCES TO 65.785 MILLION OZ

STANDING FOR SILVER: 65.785 MILLION OZ

OCTOBER GAINED 91 CONTRACTS TO 2471

NOVEMBER GAINED 32 CONTRACTS UP TO 1432.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 499 or 2.495 MILLION oz

CONFIRMED volume; ON THURSDAY 65,945 fair//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 12,303 X5,000 oz = 61.515 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (753) AND the number of notices served upon today (499 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (12,303) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(753) minus number of notices served upon today (499)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 62.785 MILLION OZ TO WHICH WE ADD OUR INITIAL EXCHANGE FOR RISK SEPT TOTALLING 3.0 MILLION OZ//NEW STANDING ADVANCES TO 65.785 MILLION OZ

New total standing: 65.785 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 196.654 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/527.5880 million. 39.84%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

GLD INVENTORY: 977.95 TONNES, TONIGHTS TOTAL

SILVER

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

CLOSING INVENTORY 485.677 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

Silver soars, gold follows

Bull markets in gold and silver, or more accurately the dollar’s disaster, resume as demand mounts ahead of the Fed’s FOMC meeting next week when a cut in rates is expected.

| Alasdair MacleodSep 12∙Paid |

This morning, gold and silver ventured into new high ground after a week of minor consolidation. In early morning European trade, gold was $3650, up $64 from last Friday’s close and 39% since 1 January. Silver was $42.15, up $1.17, and 46% higher over the same respective timescales.

In their particulars, the factors driving gold and silver differ. In gold’s case, speculator demand is beginning to build, evidenced in open interest (the black line) in the chart of the Comex contract below:

This chart is instructive: since March, open interest began to fall sharply while the price continued to rise peaking at $3445 in early-April, since when the price consolidated sideways, despite speculator liquidation taking open interest to its lowest level since February 2024. After a period of normalisation based around 450,000 contracts, at the end of August speculators finally began to buy, driving the price above and out of its consolidation pattern into new high ground.

The normal relationship between buying and a rising price has been restored, with some way to go before this contract becomes technically overbought. Context is important, which I will address below after looking at silver.

Silver exhibits not so much speculator buying as a systemic bear squeeze, illustrated by this chart from Bloomberg (posted by Ronnie Stoeferle of Incrementum on X):

The spike in lease rates to the highest level for many years is the clearest evidence of a panic for physical silver. It sets the scene for the dynamics behind our next chart, of open interest on Comex and its relationship with the price:

Open interest has declined while silver has soared, clear evidence of the price being driven by a systemic squeeze while speculators stand aside. Meanwhile, stand-for-deliveries are substantial, with 58,255,000 ounces (1,812 tonnes) since just 29 August for a total of 10,550 tonnes so far this year. This represents physical liquidity vanishing, so it’s little wonder that the systemic squeeze is on.

Shortly, we can expect speculators to spot this and chase silver prices higher still. Furthermore, growing public participation from those who feel that they have missed out in gold’s upward momentum are likely to view silver as the affordable alternative. This demand will almost certainly be through ETF buying against a background of diminishing physical liquidity with a disproportionate effect on the price. Therefore, a rerating to a gold/silver ratio below 50 and even lower still (currently 87 and falling) is not impossible.

Next week will see the Fed’s FOMC decide on a likely cut to the Feds funds rate, widely expected to be 0.25% with some going for 0.5%. This suggests that gold could see some short-term profit taking on a 0.25% cut, or would rise on 0.5% reduction. But in a more general context, it’s all about weakening the dollar. It’s trade weighted index appears due to slide significantly lower, which is our last chart:

A lower dollar is the ambition of President Trump and Stephen Miran, his new FOMC rate-setting acolyte and author of the Mar-a-Largo accord. It is surprising that the foreign exchanges are yet to reflect the importance of these developments.

Of course, they will — probably suddenly. This likelihood is being front run by gold. But when the dollar’s TWI declines convincingly below its current 97.5, gold will almost certainly go far higher, reflecting declining dollars.

We finish with gold’s updated technical chart:

Strong gold, without doubt. But really, it’s the dollar’s disaster.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 240

a must view

5. COMMODITY REPORT IRON ORE

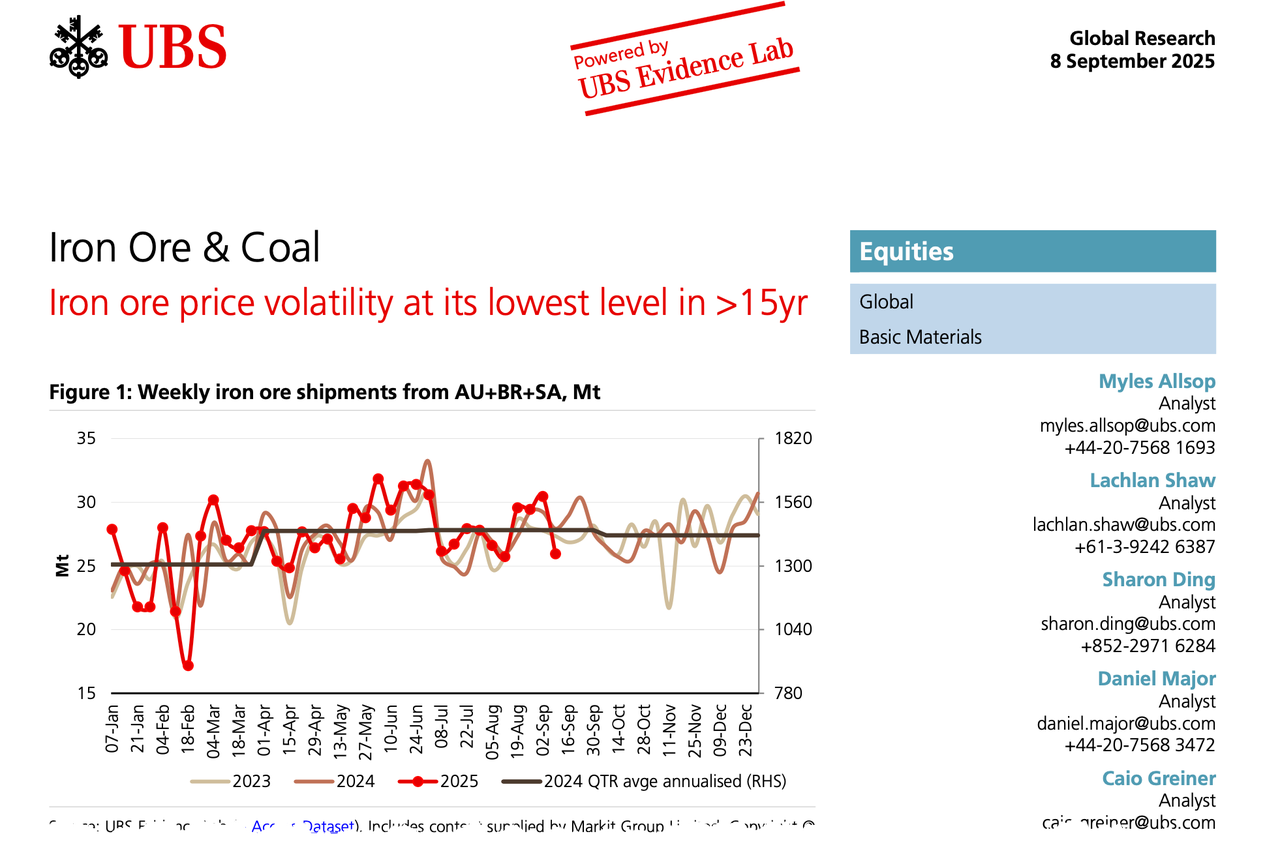

Iron Ore Price Volatility Now At 2008 Low

Friday, Sep 12, 2025 – 11:40 AM

Singapore iron ore futures closed the week near six-month highs, supported by signs of revived Chinese demand driving peak-season restocking, alongside other factors such as steel mills curbing supply and expectations for a 25-bps interest rate cut in the U.S. next week.

Earlier in the week, UBS analyst Catherine Gordon told clients, “I would flag that the team has seen strong demand for the UBS Gold Miners Basket {UBXXGOLD} amid the frenzy. Iron Ore remains the least discussed with investors on the sidelines.”

Has the iron ore market been long lost and forgotten by Wall Street desks, with prices stuck around $100 a ton for more than a year?

Possibly. UBS analyst Myles Allsop noted that iron ore volatility has collapsed to its lowest level in 15 years. With no trend to follow and prices compressed around the $100 handle, iron ore has become one of the least discussed commodities among UBS clients – well, for now.

Allsop provided more color about this collapse in volatility:

Iron ore prices: why is volatility at the lowest level in >15yrs?

The volatility in the iron ore price is at its lowest level since the industry moved to spot pricing in 2008/09, with prices trading in a tight range since mid-2024 (average ~$100/t with a low of $90/t & a high of $110/t). In our opinion, one of the key drivers of this stability is a change in buying behaviour in China, supported by widespread uncertainty & balanced market fundamentals. The Chinese govt established China Minerals Resources Group (CMRG) in Jul-22 with an aim to stabilise the iron ore market through centralised demand, price negotiations, and strategic inventory mgmt. CMRG now represents >50% of China’s steelmakers in negotiations with global suppliers, fundamentally changing the negotiating leverage from miners to Chinese steel mills and altering the iron ore market dynamics; it has also dampened speculative activity in the market by building substantial strategic inventory holdings. Looking forward, we expect lower price volatility to become the new normal, which helps steelmakers through improved cost forecasting but reduces trading opportunities for financial participants; we expect supply-demand fundamentals to continue to drive broader market price trends though the concentrated buying power of CMRG is likely to compress margins.

Iron ore prices holding up with supply/ demand balanced & inventories stable

Iron ore prices have shuffled up to ~$105/t last week with activity rebounding after the military parade and on improving sentiment (due to the China Work Plan & Fed rate cut expectations). On the key signals we note: 1) Iron ore inventories at ports (Fig24) and at mills (Fig26) in China are broadly stable w/w; 2) Iron ore shipments from traditional markets (Fig2) continue to recover with Brazil +3% YTD (> Access Dataset); 3) Steel production in China accelerated in early-Aug in the CISA data (Fig10), though MySteel utilisation rate data remains broadly flat (Fig14); 4) Steel exports from China remain strong at ~106Mtpa in Aug despite increasing trade restrictions (Fig19) – Baosteel expects China steel exports to remain >100Mt in 2025, albeit softer in 4Q; 5) Positioning on the Dalian has turned incrementally more negative and is now at -2Mt of net contracts (Fig37). We have Neutral ratings on Vale, RIO & BHP, and Sell on FMG & KIO; we est. spot 2026 FCF yield of BHP at 4%, RIO at 8%, Vale at 15% (interactive model).

Separately, Goldman analyst James McGeoch added more color about why prices of the steelmaking ingredient have soared in recent weeks to six-month highs:

“Your coming into the pre-golden week restock (Golden week October 1), the onshore feedback is positive, August imports at 105mt is impressive. The range $100-105 is still where the traders see it, consumer buying at $100, and producer hedging at $105. Of note the story Friday on the CMRG (China group) selling to calm prices down, they are not going away… “

Chart

The longer the compression, the larger the eventual move in iron ore markets. The big question is what could trigger a breakout to the upside: China stimulus, U.S. rate cuts, or Beijing pressuring mills to curb production?

Full chart pack available exclusively for ZeroHedge Pro Subs here.

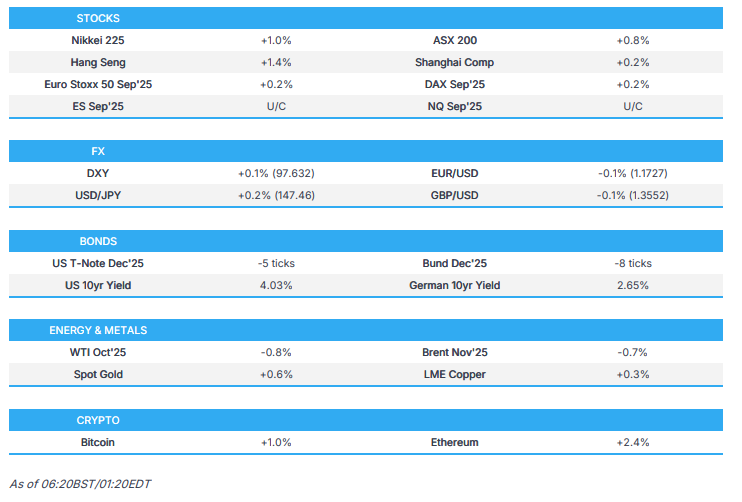

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 4.71 PTS OR 0.12%

//Hang Seng CLOSED UP 301.84 PTS OR 1.16%

// Nikkei CLOSED UP 395.62 PTS OR 0.89% //Australia’s all ordinaries CLOSED UP .63%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1240 OFFSHORE CLOSED DOWN AT 7.1235/ Oil DOWN TO 62.26 dollars per barrel for WTI and BRENT DOWN TO 66.36 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1240 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1235 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1240

OFFSHORE YUAN: DOWN TO 7.1235

HANG SENG CLOSED UP 301.84 PTS OR 1.16%

2. Nikkei closed UP 395.62 PTS OR 0.89%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 97.76 EURO FALLS TO 1.1719 DOWN 14 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.595//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.50…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.204 DOWN 2 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6887 Italian 10 Yr bond yield UP to 3.510 SPAIN 10 YR BOND YIELD UP TO 3.258

3i Greek 10 year bond yield UP TO 3.380

3j Gold at $3639.00 Silver at: 42.26 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 4 /100 roubles/dollar; ROUBLE AT 84.61

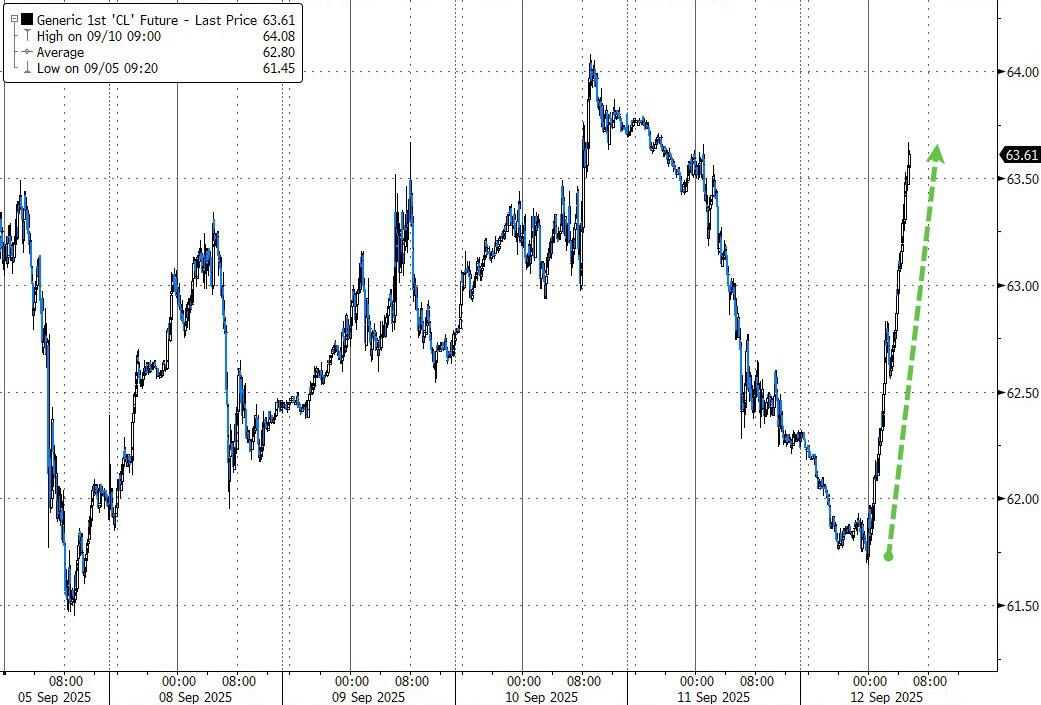

3m oil (WTI) into the 62 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.50/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.595% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.204 DOWN 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7973 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9342 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.040 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.698 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.560 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.37

10 YR UK BOND YIELD: 4.6210 DOWN 1 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.446 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.170 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.748 DOWN 1 BASIS PTS.

2a New York OPENING REPORT

Futures Dip As Record-Breaking Rally Runs Out Of Steam

Friday, Sep 12, 2025 – 08:37 AM

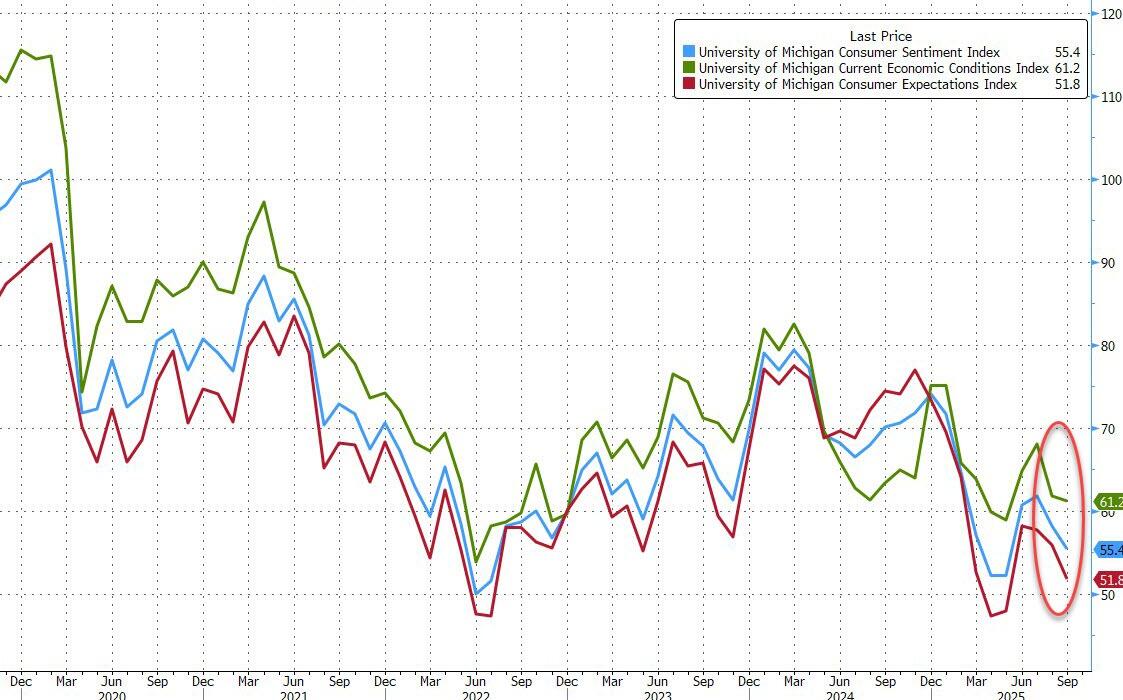

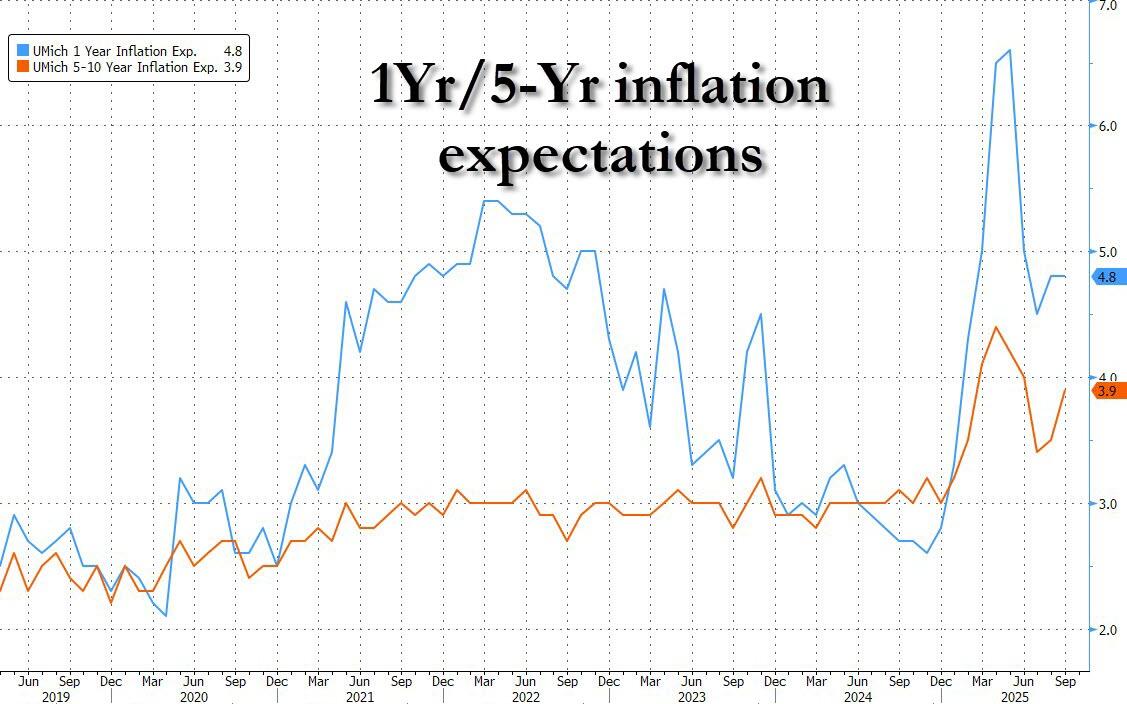

US equity futures are fractionally lower with small caps lagging as the record-breaking rally in stocks appeared to be running out of steam. At 8:15am ET, S&P 500 futures slid 0.1% after all major US indexes hit all-time highs on Thursday, however Nasdaq 100 futures are still in the green amid an relentless tech bid: Microsoft rose in premarket trading, leading the Mag 7 after it avoided a hefty antitrust penalty from the European Union. Europe’s Stoxx 600 eased as well. Incremental headlines after yesterday’s close were limited as Fed policy and AI development continue to support bulls over job market concerns or geopolitics. On trade, Bessent and Chinese VP will meet in Madrid next week. Yields are 1-2bp higher and USD is higher. Commodities are mixed, with oil and base metals higher, while precious metals are lower. Today’s econ data slate is just the September prelim University of Michigan sentiment at 10am New York time.

In premarket trading, Mag 7 stocks are mostly higher with AMZN and AAPL lagging (Microsoft +1%, Nvidia +0.1%, Amazon -0.07%, Meta +0.01%, Tesla +0.1%, Apple -0.3%, Alphabet +0.2%)

- Adobe (ADBE) rises about 3% after giving a strong quarterly revenue outlook, suggesting that the software maker is seeing a payoff from its investment in AI features.

- Alaska Air (ALK) gains 2% as an upgrade from UBS gives the stock a clean sweep of buy ratings among analysts.

- Array Technologies (ARRY) declines 5% as BofA assigns the solar tracking technology firm its only negative analyst rating, downgrading to underperform based on tariff drag.

- RH (RH) falls 8% after the luxury furniture company cut its sales outlook for the full year, citing mounting impacts from new US tariffs that resulted in delays to a seasonal catalog.

- Stellantis’ US shares (STLA) fall 3%, giving back some of the gains booked on Thursday following comments from CEO Antonio Filosa on dealer inventory levels and the company’s tariff talks with Washington. UBS tempered the optimism this morning, claiming the risk-reward profile looks “unattractive” in the near-term.

- Super Micro Computer (SMCI) gains 5% after the server company announced the availability of its Nvidia Blackwell Ultra solutions

- Warner Bros. Discovery (WBD) is up 6%, set to extend Thursday’s 29% rally as Paramount Skydance, the Hollywood studio taken over by independent filmmaker David Ellison, is said to be preparing a bid for the company.

Stocks repeatedly scaled all-time highs after a raft of data this week pointed to a strained labor market and relatively contained inflation, sealing a Fed cut when policymakers meet next week. Some now question whether the rally has further room to run as seasonal weakness and geopolitical uncertainty linger. Meanwhile swaps pricing indicates traders anticipate the equivalent of between two or three quarter point cuts through year-end, with some wagering on a jumbo half-point cut next week (odds about 10%).

Claudia Panseri, chief investment officer for France at UBS Wealth Management, cautioned that markets were reaching the limit of pricing in Fed support: “I would say that the market is overestimating the scale of rate cuts across the 12 coming months,” she said. “As for next week, some investors will be disappointed if there’s not a 50 basis-point cut, and I don’t think there will be.”

While the slowdown in the labor market has raised concerns that the Federal Reserve may have stayed on pause for too long, Bank BofA strategist Michael Hartnett said markets are betting that policymakers would still be ahead of the curve once they begin cutting rates. A rally in banks and other rate-sensitive stocks, along with a decline in investment-grade credit spreads, signal that investors are “saying the Fed can cut with credibility and is cutting into US growth re-acceleration,” he said.

Analysts expect small caps to outperform over the next twelve months, with the potential for a 20% advance in the Russell 2000, compared with calls for an 11% jump in the S&P 500, as highlighted in today’s Taking Stock column. BI strategist Gillian Wolff notes the Russell 2000 broke above the key psychological level of 2,400 this week and at 68, the 14-day RSI remains far from overbought levels — prior highs were marked by RSI above a 73-handle.

In European markets, European stocks are subdued on Friday as investors await the Federal Reserve meeting next week. Automobile and retail shares are biggest laggards, while mining and utilities equities are the best-performers.

The Stoxx Europe 600 Index was little changed at 554.86. Here are the biggest movers Friday:

- European miners are outperforming on Friday thanks to a broad rise in metal prices, with gold, copper, aluminum and nickel all gaining ground

- Hannover Rueck SE shares rise as much as 3.4%, the most since April, after UBS raised the recommendation on the German reinsurance company to buy from neutral on earnings resilience

- Inwido rises as much as 6%, reaching the highest in two months, as Berenberg initiates on the Swedish windows and door manufacturer with a buy rating

- Vallourec shares rise as much as 6.3%, the most in over two months, after the tubular product maker said it has won a major contract from Petrobras that could generate up to $1 billion in revenue

- European energy firms are lagging the wider market on Friday as oil extends a decline after the International Energy Agency projected an even bigger surplus next year

- Novartis drops as much as 2.9% after the stock was downgraded to sell from neutral at Goldman Sachs. The analysts say the Swiss drugmaker’s valuation looks “stretched” given the increasing impact of generic competition following drug patent expiries in the coming years

- Ocado shares plunge as much as 12% extending losses booked in late trading on Thursday. Morgan Stanley analysts noted “negative readacross” from comments made on US grocer Kroger’s conference call yesterday

French bonds lagged most regional peers ahead of a Fitch Ratings update on the country, due after the close. French assets have been unsettled after former Prime Minister Francois Bayrou lost a confidence vote, failing to muster enough support to rein in the budget deficit. “The market is already incorporating at least one or two or even three downgrades,” Vincent Mortier, chief investment officer at Amundi SA, told Bloomberg TV. “We’re still far away from a sub-investment-grade rating. The market has been quicker than the rating agencies to adjust the levels.”

Earlier in the session, Asian equities advanced, as technology shares extended their rally on rising expectations that the Federal Reserve will cut interest rates next week. The MSCI Asia Pacific Index rose as much as 1.1%, poised for a seventh day of rise in its longest winning streak since May 2024. South Korea’s Kospi notched another all-time high, after SK Hynix announced it had completed development of its next-generation AI memory chip. Shares in Hong Kong also rose, with Alibaba surging amid optimism over its AI infrastructure plans. Risk appetite has been improving in Asia as tariff worries ease on progress in US trade talks. The return of optimism on the AI trade, a liquidity-driven rally in Chinese stocks and expectations that Fed cuts will allow Asian central banks room to ease further have helped power the advance. Tech got a boost this week from Oracle Corp.’s upbeat cloud-business outlook. Stocks also climbed Friday in Taiwan, Japan and Australia. Indonesia’s key equity gauge jumped more than 1% on optimism over plans from the nation’s new finance minister. Here Are the Most Notable Movers

- Ain Holdings Inc. shares jumped after the Japanese pharmacy operator raised its full-year operating profit guidance. Meanwhile, Fuji Oil Co. shares surged following a takeover offer from Idemitsu Kosan Co.

- Infosys shares rise as much as 2.3% to their highest in seven weeks after the software firm said it will buy back shares worth 180 billion rupees ($2 billion).

- Aristocrat Leisure shares fall as much as 4.5%, the most since May 14, after the Australian game machine operator said Dylan Slaney will replace Moti Malul as CEO of the interactive division.

- Star Plus Legend shares rise as much as 22% in Hong Kong, the most since July 30, after a media report saying that a robot dog created by the company and Hangzhou Unitree Technology will make its first appearance soon.

- Malaysian car distributor Bermaz Auto Bhd. fell to a record low after its first-quarter net income slumped 88%, weighed by strong competition from Chinese automakers.

- Ascletis Pharma shares rise as much as 6.6% in Hong Kong after the company said Chairman Jason Wu and Executive Director Judy Wu are demonstrating “strong faith” in its long-term value and future prospects.

- Verisilicon Microelectronics shares surge as much as 20% to a record high, resuming trading following a halt, after the company announced plans to buy a Shanghai chip tech firm.

- Alibaba Group Holding Ltd.’s stock gained the most in about two weeks after the company initiated a series of moves intended to shore up its place in China’s AI development boom.

- Anritsu shares jump as much as 13% to the highest intraday level since Nov 2021 after Goldman Sachs initiates a buy rating on the Japanese measurement instruments company on expectations of profit growth driven by AI and data center businesses.

- Timee shares plunged as much as 18%, the most in a year, after the part-time job app developer’s quarterly sales missed estimates, spurring concern about weakness in its food industry operations.

In FX, the dollar rebounded from back-to-back losses. The yen lags G-10 currency peers, down by 0.5%, and set for a third consecutive weekly decline. The pound trimmed a weekly gain after the economy showed a sluggish start to the third quarter, with gross domestic product flat and slowing from the previous month.

In rates, treasuries pulled back from Thursday’s advance alongside weakness in Europe, with the US 10-year yield rising two basis points to 4.05%. Yields are biased slightly higher amid bigger losses for bunds during European morning following German and French CPI data. US front-end to 10-year yields are cheaper by as much as 1.5bp with 2s10s curve barely 1bp steeper on the day. Long-end yields are little changed, flattening 5s30s by about 1bp. German and UK counterparts lag US 10-year by 2bp and 1bp. Gilt yields are higher and the pound is weaker after UK economy flat-lined in July.

In commodities, gold pares gains after testing another record, but is still up by $6 to $3,639/oz as money pours into bullion-backed ETFs. Copper and nickel also rise to buoy miners in Europe. Oil prices reverse an earlier decline, with Brent trading up 1% and shy of $67/barrel.

Looking ahead, today’s calendar includes the US September University of Michigan Survey, UK July monthly GDP, Italy’s Q2 unemployment rate, and Canada’s July building permits. Central bank speakers include the ECB’s Rehn, Kocher, and Nagel, as well as the BoE’s inflation attitudes survey.

Market Snapshot

- S&P 500 mini -0.1%

- Nasdaq 100 mini little changed

- Russell 2000 mini -0.5%

- Stoxx Europe 600 -0.1%

- DAX -0.3%

- CAC 40 -0.4%

- 10-year Treasury yield +2 basis points at 4.04%

- VIX little changed at 14.68

- Bloomberg Dollar Index +0.2% at 1199.62

- euro -0.1% at $1.172

- WTI crude +0.6% at $62.74/barrel

Top Overnight News

- Trump says Charlie Kirk’s murder suspect has been captured and is in police custody

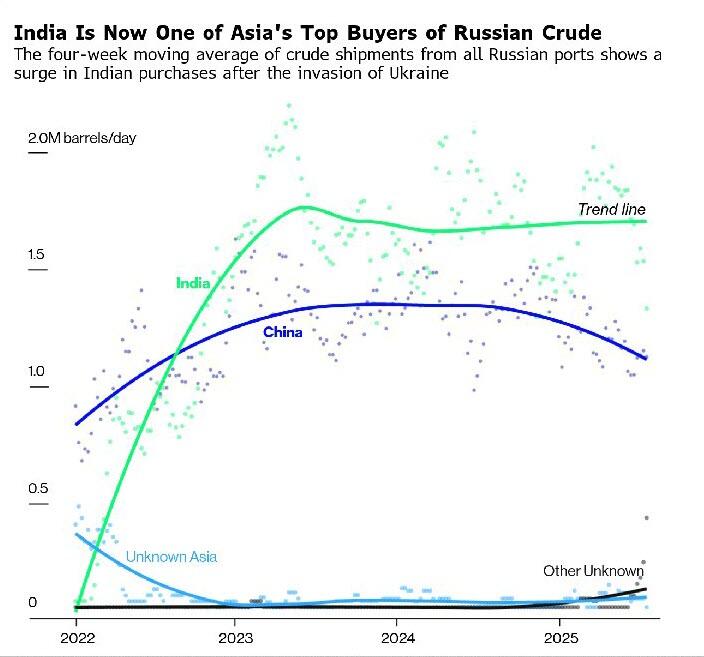

- The US will pressure G7 countries to hit India and China with sharply higher tariffs for buying Russian oil in an attempt to force Moscow into peace talks with Ukraine, according to four people briefed on the plans. FT

- China on Thursday warned Mexico that raising tariffs on Chinese goods will be considered “appeasement” to US “bullying,” after Mexico mulled plans to impose import duties of up to 50%. Nikkei

- Allianz and AllianceBernstein are among global firms boosting holdings of Chinese government bonds after a selloff driven by a rotation into stocks sent yields to multi-month highs. Analysts also expect the PBOC to resume purchases. BBG

- US Treasury Secretary Scott Bessent plans to meet with Chinese Vice Premier He Lifeng and other senior officials next week in Madrid to continue their discussions on trade, economic and national security issues, the Treasury said on Thursday. RTRS

- Brazil’s Supreme Court sentenced former president Jair Bolsonaro to 27 years in prison for plotting a coup after his 2022 election defeat. Marco Rubio said the US will respond “accordingly.” BBG

- OpenAI is moving closer to a for-profit structure under a new deal with Microsoft, giving its nonprofit parent an equity stake of more than $100 billion. The plan faces resistance from Elon Musk and regulatory scrutiny. BBG

- Sam Altman and Nvidia’s Jensen Huang will announce investments worth billions of dollars in UK data centers next week, people familiar said. BBG

- Adobe (+3.8% premkt) shares rose on a strong revenue forecast, suggesting investments in AI features are paying off. Reported solid quarterly results, and upped its Revenue, net new ARR, and EPS guidance which should help push back on bear thesis.

- Gold ETF holdings jumped about 25 tons this week — the sixth-highest weekly gain this year — on the back of Fed rate-cut bets, weaker yields and central-bank demand. Still, Phillip Nova warned long-term holding is riskier amid volatile momentum-driven trading. BBG

Trade/Tariffs

- US Treasury Secretary Bessent will travel to Spain and the UK on September 12th-18th on a trip that includes government and private sector meetings in London. Bessent will meet with Chinese Vice Premier He and other senior Chinese officials next week in Madrid, while Bessent and He are to discuss key US-China national security, economic and trade issues, including TikTok and anti-money-laundering cooperation. Furthermore, Bessent will also meet with Spanish government counterparts to discuss the US-Spain relationship and is to join US President Trump in the UK for an official state visit with King Charles.

- China’s Commerce Ministry said planned Mexican tariffs on China are too seriously affect Mexico’s business environment and confidence of enterprises in investing in Mexico, while it added that China will take necessary measures to safeguard legitimate rights and interests.

- Taiwan said it will continue advanced talks with the US and seeks more equitable reciprocal trade terms with the US, while Taiwan and the US affirmed that some progress was made in trade talks

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher following the gains on Wall St, where the major indices climbed to record highs after a jump in Initial Jobless claims further boosted Fed rate cut pricing. ASX 200 edged higher with outperformance in Real Estate, Miners, Materials & Financials spearheading the advances as Fed rate hike expectations boost global risk sentiment. Nikkei 225 extended on record highs and approached closer towards the 45,000 level despite little fresh pertinent drivers. Hang Seng and Shanghai Comp traded mixed with tech leading the gains in Hong Kong after it was reported that Alibaba (9988 HK) and Baidu (9888 HK) are using internally designed chips for training AI models are to adopt their own AI chips in a major shift for Chinese tech, while the mainland lagged amid frictions, with the US reportedly to urge G7 to impose high tariffs on China and India over Russian oil purchases.

Top Asian News

- Japanese and US finance ministers’ joint statement noted as trusted partners, the United States Department of the Treasury and the Japanese Ministry of Finance agreed to continue their close consultations on macroeconomic and foreign exchange matters, while they reaffirmed that exchange rates should be market-determined and that excess volatility can have adverse implications for economic and financial stability.

- Japanese Member of the House of Representatives Takaichi leads in a Kyodo poll to be next head of Japan ruling party.

- Chinese finance minister says local debt swap programme is achieving results. China’s finance minister vows to resolutely curb new local hidden debt.