XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

FROM MY no 4 SON STEPHEN //THROUGH AI: ENJOY

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 3,682.200000000 USD

INTENT DATE: 09/15/2025 DELIVERY DATE: 09/17/2025

FIRM ORG FIRM NAME ISSUED STOPPED

118 H MACQUARIE FUTURES US 9

323 C HSBC 13

363 H WELLS FARGO SECURITI 31

435 H SCOTIA CAPITAL (USA) 18

624 H BOFA SECURITIES 1

661 C JP MORGAN SECURITIES 94 11

686 C STONEX FINANCIAL INC 2

732 C RBC CAP MARKETS 13

880 C CITIGROUP 7

905 C ADM 15

TOTAL: 107 107

MONTH TO DATE: 5,647

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 107 CONTRACTs NOTICES FOR 10700 OZ or 0.3328 TONNES

total notices so far: 5647 contracts for 564,700 OR 17.6578 tonnes)

SILVER NOTICES: 42 NOTICE(S) FILED FOR 0.210 MILLION OZ/

total number of notices filed so far this month : 12,409 CONTRACTS (NOTICES) for 62.045 million oz

A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 976.81 TONNES

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 26.675 MILLION OZ.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 63.000 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING) PLUS 3.0 MILLION OZ EX FOR RISK = 66.000 MILLION OZ. THIS IS THE FIRST ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.3110 TONNES PLUS 0 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 16.364//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 34.202 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 62.07 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE 1128 CONTRACTS OI TO 162,383 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 250 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 150 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1129 CONTRACTS AND ADD TO THE 250 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 1378 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.28 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 6.890 MILLION PAPER OZ

OCCURRED WITH OUR $0.28 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 1.36 PTS OR 0.04%

//Hang Seng CLOSED UP 41.39 PTS OR 0.16%

// Nikkei CLOSED UP 134.15 OR 0.30% //Australia’s all ordinaries CLOSED UP .33%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1147 OFFSHORE CLOSED UP AT 7.1110/ Oil UP TO 63.16 dollars per barrel for WTI and BRENT UP TO 67.12 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1149 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1110 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7,430 CONTRACTS TO 519,611 OI WITH OUR GAIN IN PRICE OF $45.30 WITH RESPECT TO MONDAY’S // TRADING.. WE OF COURSE, LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2615). WE HAD ZERO T.A.S. LIQUIDATION AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 10,045 CONTRACTS (OR 31.244 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD 0 CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 3 MONTHS;

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW WEDNESDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

AND NOW:

SEPT:

SEPTEMBER: FOUR ISSUANCES SO FAR TOTALLING 5,261 CONTRACTS OR 526,100 OZ OR 16.364 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW YESTERDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: FOUR ISSUANCES FOR 5261 CONTRACTS SO FAR FOR 526,100 OZ OR 16.364 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS AND :

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH SEPT//ONLY MISSING JUNE.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON SEPTEMBER COMEX MONTH//

IN TOTAL WE HAD A HUGE SIZED GAIN ON OUR TWO EXCHANGES OF 10,045 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1165 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DESPERATELY TRYING TO STOP GOLD’S ADVANCE AND THIS ENDS IN FAILURE. FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!!

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH PREVIOUS AUGUST MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.3110 TONNES QUEUE JUMP TO GO ALONG WITH THE 0. TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 16.364 TONNES//NEW TOTALS STANDING ADVANCES TO 34.202 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 240 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

AND NOW SEPTEMBER:

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.3110 TONNES QUEUE JUMP AND 0.000 TONNES EXCHANGE FOR RISK TODAY// NEW TOTALS OF 16.364 TONNES OF EXCHANGE FOR RISK ISSUANCE/:

THAT IS;

A) 0.00 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY // =//TOTAL FOR MONTH EX FOPR RISK: 16.364 TONNES EX FOR RISK!!

B) 0.3110 TONNES TODAY QUEUE JUMP

TOTALS: 34.202 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2615 EFP CONTRACT WAS ISSUED: : /DEC 2615 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2615 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY

- MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED SIZED 2615 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S HUGE GAIN IN PRICE IN GOLD AND A CORRESPONDING HUGE GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

2) AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

3) TO BE FOLLOWED BY SEPTEMBER’S 4 ISSUANCES FOR EXCHANGE FOR RISK FOR 16.364 TONNES.

GOLD STANDING AT THE COMEX FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

AND NOW SEPT:

SEPT: 17.527 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) +0 EX FOR RISK TODAY//

TOTAL EX FOR RISK// FOR MONTH = 16.364//NEW TOTALS FOR GOLD STANDING SEPT = 34.202 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A STRONG $45.30./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE LONGS PILING IT ON TRYING TO OBTAIN BADLY NEEDED GOLD///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS) WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH LAST WEEK AND THIS WEEKS’S TRADING!! THIS IS THE FIRST TIME THAT THE CROOKS COULD NOT MUSTER A RAID ON OPTIONS EXPIRY LONDON/OTC AUGUST TRADING. THEIR RAID ON OUR PRECIOUS METALS CAUSED NO DAMAGE TO OUR PRICE.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 31.244 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 0.3110 TONNES OF GOLD ALONG WITH 0 TOTAL TONNES OF EXCHANGE FOR RISK TODAY/// TOTAL FOR MONTH TOTALS EX FOR RISK// MONTH = 16.364//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 34.202 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $45.30

WE HAD A SMALL247 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 10,045 CONTRACTS OR 1,004,500 0Z (31.244 TONNES)

confirmed volume MONDAY 208,695 contracts// poor//

speculators have left the gold arena

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

SEPT 16 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1.entries i) out of Manfra: 14,098.380 oz total withdrawal 14,0989.380 oz . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 107 notice(s) 10,700 OZ 0.3328 TONNES |

| No of oz to be served (notices) | 88 contracts 8,800 OZ 0.2737 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5647 notices 564,700 oz 17.6578 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER 0

total deposit

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1.entries

i) out of Manfra: 14,098.380 oz

total withdrawal 14,0989.380 oz

ADJUSTMENTs 2

a) Brinks: customer to dealer account 78,040.434 oz

b) JPMorgan dealer to customer 289.359 oz

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 195 CONTRACTS FOR A LOSS OF 840 CONTRACTS. WE HAD 940 CONTRACTS FILED ON MONDAY SO WE GAINED 100 CONTRACTS OR 10,000 OZ ENTERTAINED A QUEUE JUMP OF 0.3110 TONNES. WE NOW MUST ADD TO OUR INITIAL 8.093 TONNES OF GOLD STANDING TO TODAY’S QUEUE JUMP OF 0.3110 TONNES AND THEN ADD MONTH SEPT// EX FOR RISK = 16.364//THUS NEW TOTAL OF GOLD STANDING ADVANCES TO 34.202 TONNES

OCTOBER GAINED 171 CONTRACTS UP TO 60,163

NOVEMBER GAINED 41 CONTRACTS UP TO 3098 CONTRACTS.

We had 107 contracts filed for today representing 10,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 94 notices issued from their client or customer account. The total of all issuance by all participants equate to 107 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 11 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (5647 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 195 CONTRACTS) minus the number of notices served upon today (107 x 100 oz per contract) equals 573,500 OZ OR 17.838 TONNES OF GOLD TO WHICH WE ADD OUR TOTAL EX FOR RISK/SEPT MONTH OF 16.369 TONNES//NEW TOTAL STANDING ADVANCES TO 34.202 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (5647 x 100 oz +we add the difference for front month of SEPT. (195 OI} minus the number of notices served upon today (107 x 100 oz) which equals 573,500 OZ OR 17,838 TONNES PLUS 16.364 TONNES EXCHANGE FOR RISK = 34.202 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 34.202 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,024,054.573 oz 62.956 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,166,532.740 oz

TOTAL REGISTERED GOLD 21,399,458.758 or 665.613 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,7677,373.982 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,375,404oz ((REG GOLD- PLEDGED GOLD)= 602.65 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 16 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries: i) Out of Asahi 2,413,243.800 oz ii) Delaware 5179.480 oz iii) Manfra: 596,806.682 oz total withdrawal 3,015,229.962 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 0 entries |

| No of oz served today (contracts) | 42 CONTRACT(S) (0.210 million OZ |

| No of oz to be served (notices) | 191 contracts (0.955 MILLION oz) |

| Total monthly oz silver served (contracts) | 12,407 Contracts (62.045 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

0 DEPOSIT ENTRIES/CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 entries:

3 entries:

i) Out of Asahi 2,413,243.800 oz

ii) Delaware 5179.480 oz

iii) Manfra: 596,806.682 oz

total withdrawal 3,015,229.962 oz

ADJUSTMENTs 2 dealer to customer

a)Asahia: 2044,066.610 oz

b) Delaware 579,595.175 oz

TOTAL REGISTERED SILVER: 194.327 MILLION OZ//.TOTAL REG + ELIGIBLE. 524,632 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 233 OPEN INTEREST CONTRACTS FOR A LOSS OF 25 CONTRACTS. WE HAD 64 CONTRACTS SERVED ON MONDAY SO WE GAINED A FAIR SIZED 39 CONTRACTS OR 195,000 OZ ENTERTAINED A QUEUE JUMP//NEW STANDING FOR SILVER COMEX INCREASES TO 63.000 MILLION OZ. THEN WE MUST ADD OUR INITIAL ISSUANCE OF 600 CONTRACTS FOR EXCHANGE FOR RISK OR 3.0 MILLION OZ//NEW STANDING ADVANCES TO 66.000 MILLION OZ

STANDING FOR SILVER: 66.000 MILLION OZ

OCTOBER LOST 103 CONTRACTS TO 2388

NOVEMBER GAINED 195 CONTRACTS UP TO 1658.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 42 or 0.210 MILLION oz

CONFIRMED volume; ON MONDAY 52,249 fair//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 12,409 X5,000 oz = 62.045 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (233) AND the number of notices served upon today (42 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (12,409) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(233) minus number of notices served upon today (42)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 63.000 MILLION OZ TO WHICH WE ADD OUR INITIAL EXCHANGE FOR RISK SEPT TOTALLING 3.0 MILLION OZ//NEW STANDING ADVANCES TO 66.000 MILLION OZ

New total standing: 66.000 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 194.327 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/524.632 million. 40.08%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 976.81 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

GLD INVENTORY: 976.81 TONNES, TONIGHTS TOTAL

SILVER

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

CLOSING INVENTORY 487.177 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

JAMES RICKARDS

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 240

a must view

5. COMMODITY REPORT BEEF AND EGGS

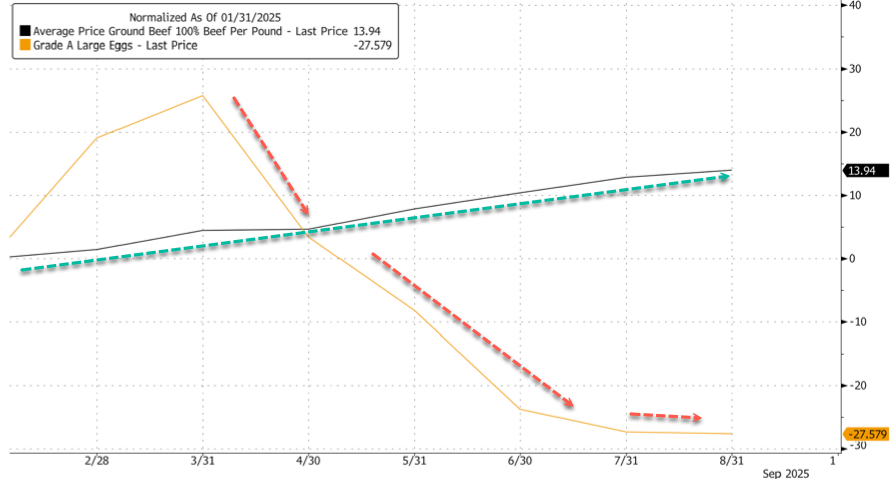

Ground Beef Inflation Sizzles, Egg Prices Cool Off

Tuesday, Sep 16, 2025 – 06:55 AM

The best bang for the buck in the grocery store protein aisle this year hasn’t been beef, it’s been eggs. Prices have plummeted thanks to President Trump’s swift action to fix the Biden-Harris regime’s botched bird flu culling disaster. By contrast, ground beef has surged to a record $6.32 per pound, squeezed by the smallest US cattle herd in decades, with a bleak outlook despite some signs of a rebuilding phase nearing.

Here’s more from Bloomberg:

For more than a year, egg prices have served as the poster child for the higher cost of living in the US. That distinction may soon move over to the beef market, said Darin Parker, president of global meat trader Parker-Migliorini International Llc. Parker warns that Americans will keep paying more for burgers as restrictions on Brazilian imports further squeeze already tight domestic supplies. Indeed, one measure of US retail prices shows that ground beef has climbed more than 10% since January, while eggs dropped nearly 30%.

Beef inflation is sticky, while egg prices have cooled.

Egg prices are back to pre-crisis levels.

Meanwhile.

Related:

- 12-Year Cattle Cycle Bottoms: Tyson CEO Predicts Rebuild Phase Beginning Next Year

- Tyson Foods Confirms Protein Switching Underway Amid Record High Beef Prices

- Got Beef? 12-Year Cycle Signals “Cyclical Low”

- Cattle Herd Rebuild Begins Just As Consumers Get Slaughtered By Record Beef Prices

The next cattle herd rebuild cycle must bring small, family-run ranchers back into the fold if America wants a resilient domestic beef supply.

Supporting independent journalism goes hand in hand with supporting independent ranchers – both make this nation stronger.

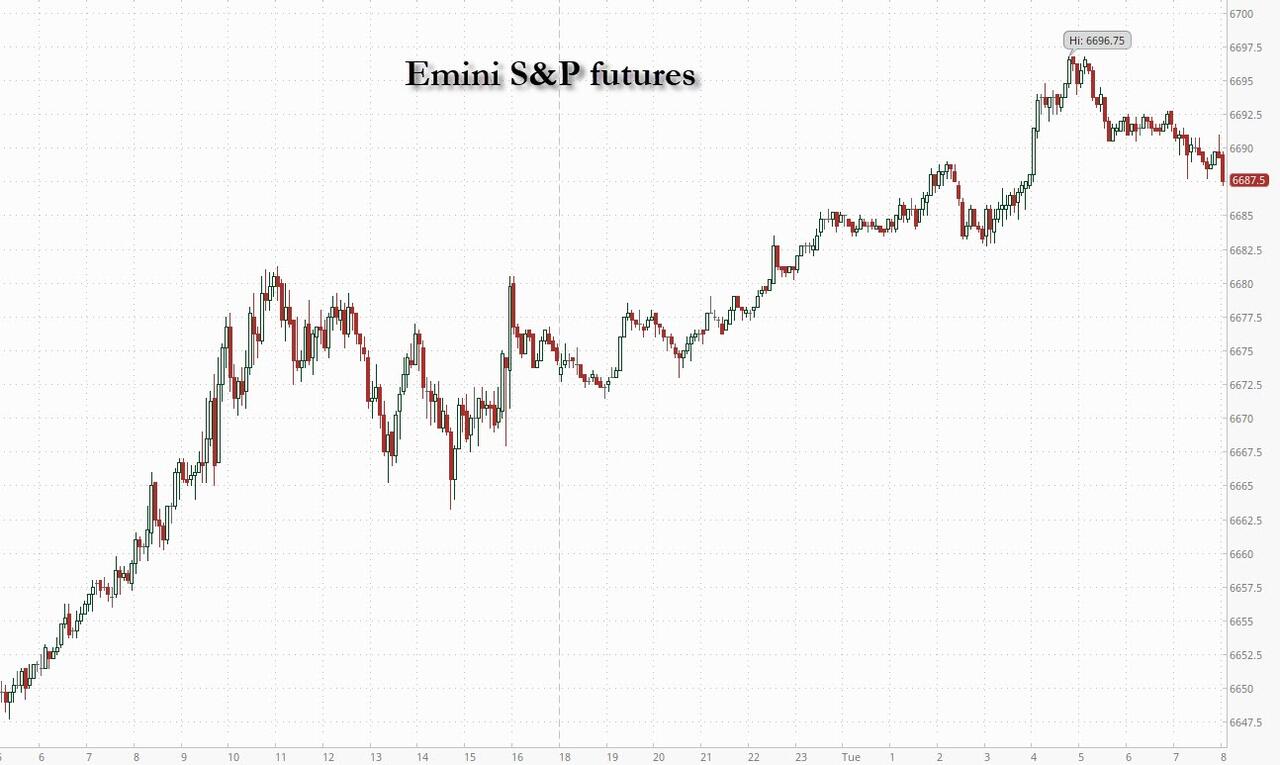

US Futures Set For Another Record, Nasdaq On Pace For 10th Straight Gain

Tuesday, Sep 16, 2025 – 08:29 AM

US equity futures are higher (duh) outperforming global counterparts, while the Nasdaq is on pace for a historic 10th day of gains. As of 8:00am ET, S&P and Nasdaq 100 futures were higher by 0.2% with Oracle rising more than 5% in premarket trading on news it may soon be handed control of TikTok. S&P 500 contracts edged higher after the US benchmark powered through the 6,600 mark on Monday. Pre-mkt, Mag7 is displaying strength across multiple members with add’l TMT support from AVGO (+1.4%) and ORCL (+3.7%). Cyclicals and Semis are poised to lead but with pockets of strength in Defensives (HC, Staples) also seen. Europe’s Stoxx 600 fell 0.2%. Bond yields are flat to down 1bps with the US Dollar broadly weaker ahead of a widely expected 25bp cut and the resumption of the Fed’s easing cycle which paused in Dec 2024 (right after Trump was elected). US Treasuries have been racing past peers, the euro is nearing four-year highs and Goldman strategists caution that the next pain point for bond traders may come in the five-year part of the curve. Both Cook and Miran will be a part of the vote. Today’s macro data focus is on Retail Sales where Feroli is below the Street seeing a 0.1% MoM print and 0.3% for the Control Group.

In premarket trading, Mag 7 stocks are mostly higher: Tesla rises 1.3%, paring earlier gains after the National Highway Traffic Safety Administration opened a probe over issues with door handles on certain Model Y vehicles. Alphabet gains 1.3% a day after the Google-parent on Monday joined an elite group of companies valued at more than $3 trillion (Nvidia -0.2%, Microsoft +0.1%, Apple -0.01%, Amazon +0.5%, Meta Platforms +0.6%)

- Bloom Energy (BE) jumps 7% after Morgan Stanley boosted its price target on the fuel-cell manufacturer to a Street-high, saying the company is much more favorably positioned for success in powering AI data centers.

- Dave & Buster’s (PLAY) tumbles 15% after the restaurant operator reported adjusted earnings per share and revenue for the second quarter that came in well below the average analyst estimate.

- Hershey’s (HSY) gains 2% after Goldman Sachs double upgraded the shares. Analysts said market-share trends are improving, and there are incremental tailwinds ahead for the chocolate and confectionery company.

- New York Times (NYT) shares slip 1.9% after President Donald Trump filed a $15 billion defamation and libel lawsuit against the news organization.

- Oracle (ORCL) rises 5% after CBS News reported that the software giant is among a consortium of firms that would enable TikTok to continue operations in the US if a framework deal is finalized.

- Warner Bros Discovery (WBD) shares fall 1.5% as TD Cowen downgraded to hold from buy after the stock rallied even as Paramount is still to make an official offer.

- Webtoon Entertainment (WBTN) soars 47% after Walt Disney said it plans to acquire a 2% equity interest in the online comics company.

Stock bulls are riding high ahead of a widely expected 25-basis-point Fed cut on Wednesday (potentially as high as 50), the first move in a policy easing round projected to run into 2026. Rate-sensitive tech shares have led the charge in the post-Liberation Day rebound, fueled by enthusiasm over artificial intelligence. Asset managers are growing even more bullish according to the latest BofA survey. But stretched positioning in pockets of the market, with some funds already “maximum long”, is leaving it vulnerable to a shock.

“Capex and profit forecasts linked to AI are overwhelming,” said Thomas Brenier, head of equities at Lazard Freres Gestion. “Look at Oracle, it seems that the sky is the limit.”

Expectations of aggressive Fed rate cuts drove the dollar toward its weakest level since July. The euro climbed 0.4%, nearing its highest mark since 2021. The divergence reflects the Fed’s shift toward easing, in sharp contrast with the European Central Bank, where policymakers have signaled an end to their own loosening cycle.

As the Nasdaq prints a nine-day winning streak, hedge funds net bought IT stocks at the fastest pace in seven months across all regions, according to Goldman’s prime desk. With CTAs max long, corporates increasingly moving into buyout blackouts, and hedge funds likely only able to add at the margin, retail and discretionary investors are left to support equities.

Meanwhile, the tensions between the Fed and Trump administration escalated Monday. An appeals court temporarily halted the effort to oust Governor Lisa Cook, while the Senate separately approved Trump’s economic adviser Stephen Miran for a seat on the board.

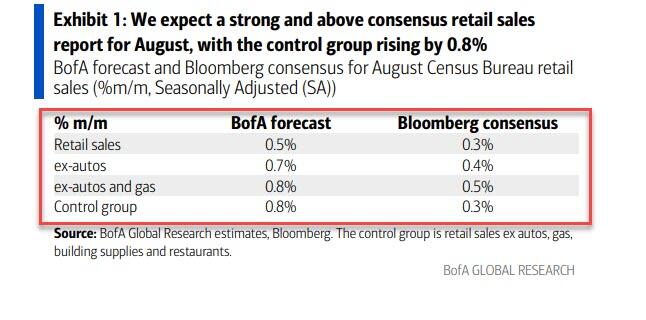

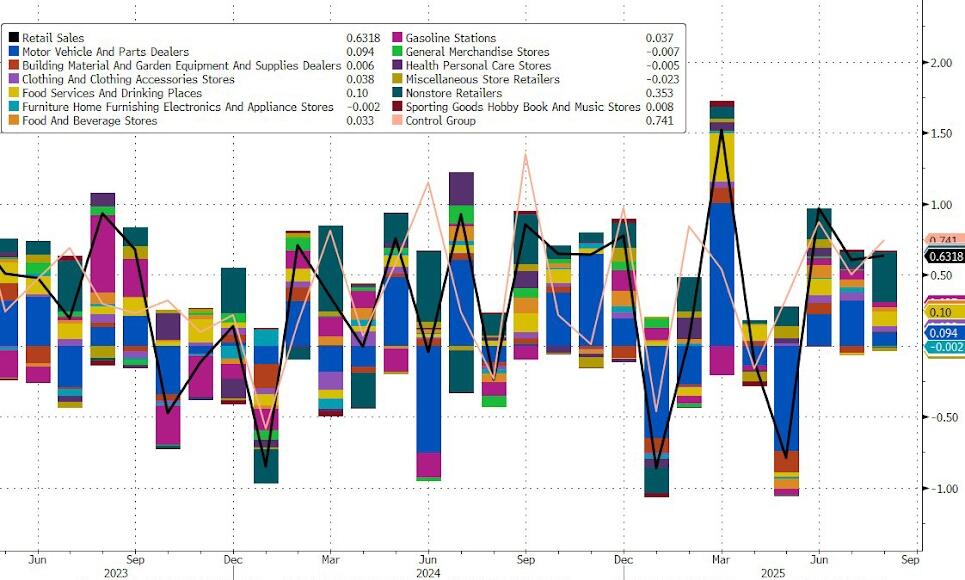

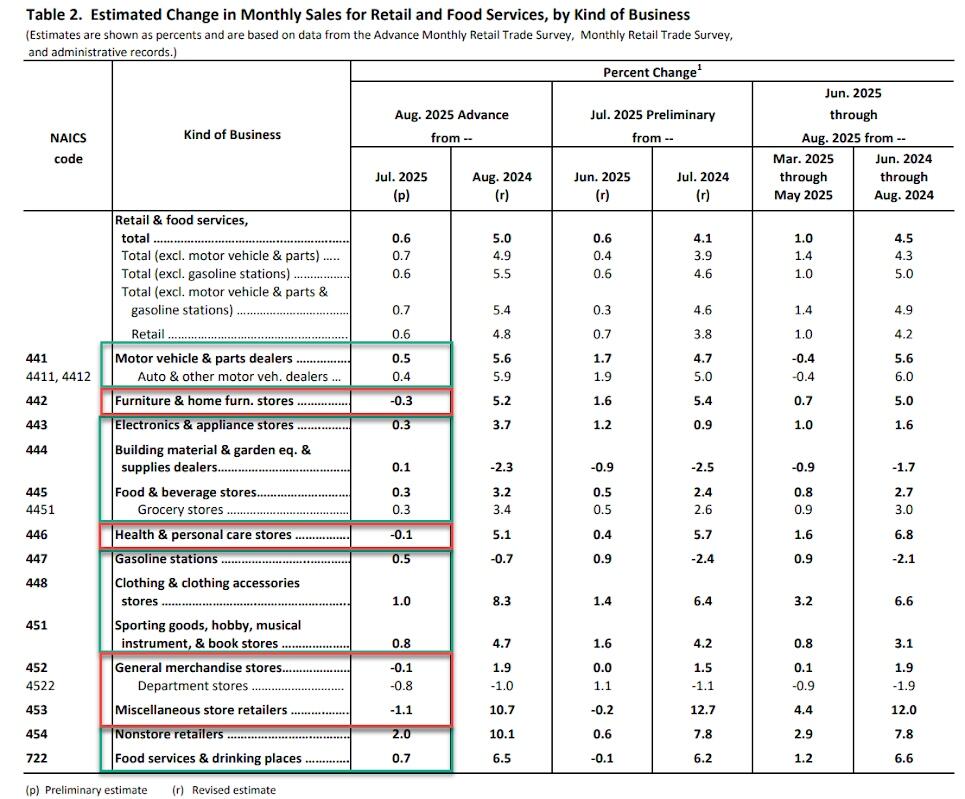

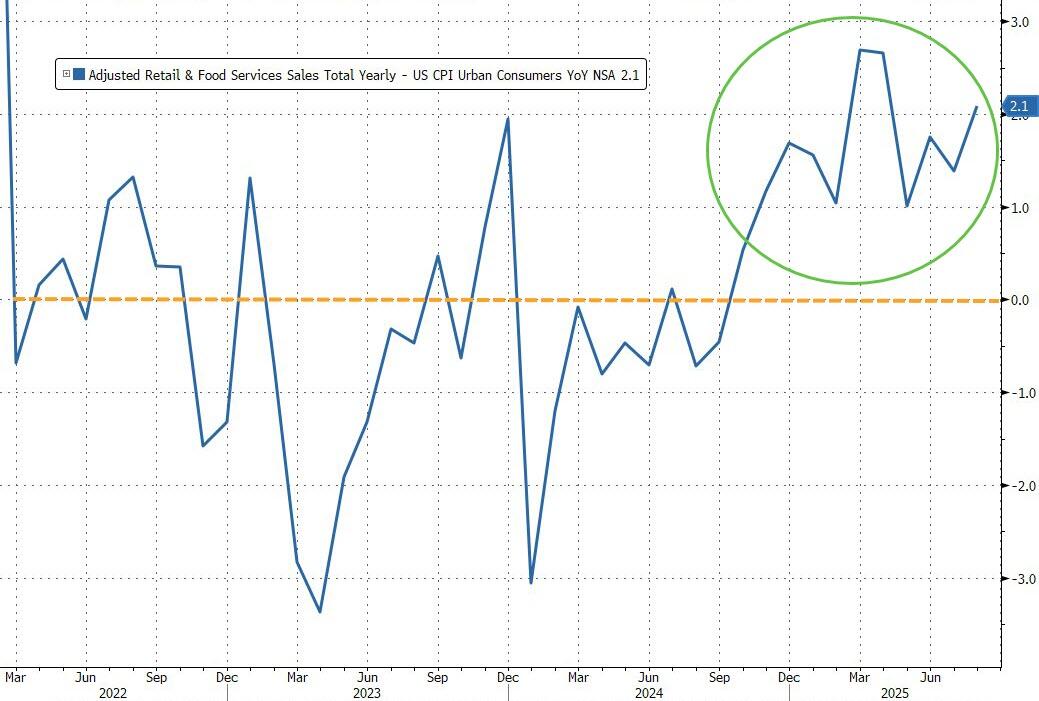

Later on Tuesday, traders are set for a final read on the American consumer. Retail sales data for August are forecast to show a 0.2% increase, following stronger advances in the previous two months, although real -time card spending data hints at an even higher print. Bloomberg economists Eliza Winger and Estelle Ou expect headline retail sales likely grew 0.2% in August, down from 0.5% in July, as auto sales slowed, noting spending remains modest overall with consumers concerned about tariffs and the economy. With the jobs market softening and prices rising, questions remain over how long consumers will keep spending freely.

“In the session ahead, we navigate US retail sales and that poses a degree of risk to markets,” wrote Chris Weston, head of research at Pepperstone Group. “However, with the Fed meeting looming large in the following session, it will likely take an outsized surprise in retail sales to really move the dial on risk.”

Stocks may have further upside as rising expectations for economic growth continue to buoy bullish sentiment, according to Bank of America’s Michael Hartnett. His latest fund manager survey found that a net 28% of global investors are overweight equities, the strongest reading in seven months. Views on growth also showed the biggest positive shift in nearly a year, with only a net 16% of respondents still anticipating an economic slowdown, Hartnett said.

Europe’s Stoxx 600 falls 0.1% as the rally that sent US and Asian stocks to fresh highs sputters in Europe. Italian banks dip on news that the government was drafting plans to raise another €1.5 billion ($1.8 billion) from lenders, while miners gained on the back of rising iron ore prices. Here are the biggest movers Tuesday:

- European mining shares are the best performers in the Stoxx 600 benchmark on Tuesday after iron ore advanced, with China’s daily steel output showing signs of improvement

- Embracer gains as much as 5.5%, the biggest contributor to the Stoxx 600 Index, after Kepler Cheuvreux reiterated its buy rating and boosted its price target for the Swedish gaming group ahead of a spinoff of its Coffee Stain subsidiary

- ASML shares continue to rally Tuesday after JPMorgan said that the worst of newsflow is likely behind the chip-gear firm as better trends in both memory and logic end-markets bode well for the 2027 sales outlook

- Kering shares gain as much as 2.4% after CIC upgraded the French luxury firm to buy from hold on improved outlook following the new CEO’s plans, a creative revamp at Gucci, and its delayed Valentino purchase agreement

- Fresnillo rises as much as 4.6% in London after JPMorgan upgraded the precious metals firm’s price target to 2,500 pence from 2,100 pence and reiterated its overweight rating, as the bank sees further upside for the miner

- Kier Group rises as much as 9.4% as the infrastructure services and construction company reported full-year results that beat estimates on better-than-expected current trading and solid order book

- VusionGroup rises as much as 20%, the most since February, after the French tech group’s full-year sales forecast beat expectations and broker Gilbert Dupont upgraded its rating for the stock

- Yellow Cake shares rise as much as 8.4% in London, hitting their highest level since December, tracking a rise in global peers after the US Energy Secretary said the US should boost its strategic uranium reserve

- Shelf Drilling jumps as much as 34%, the most since August, after Ades increased its cash consideration for the offshore drilling contractor to NOK18.5 per share, from the Aug. 5 offer of NOK14 per share

- Haleon drops as much as 6.1% as Barclays downgrades its rating on the consumer-health company to equal-weight from overweight, based on a tough backdrop in the US

- Granges falls as much as 6.9% after Nordea cut its recommendation on the Swedish aluminum group to hold from buy, saying that while the company is set to gain market share, Nordea struggles to find an inflection point

- Schindler shares slide as much as 2.8% after one of its investors offloaded shares at a discount to Monday’s close. The stock is sliding for a second consecutive session after ending last week at an all-time high

- SThree shares plummet by as much as 28%, their biggest drop this year, after the recruitment company warned it is expecting subdued activity to persist into FY26, hitting its guidance for the year

- Italian banks underperformed on Tuesday after Bloomberg reported that the country’s government is working on a preliminary plan to raise an extra €1.5 billion from lenders in 2027 by postponing their tax deductions

Earlier in the session, Asian stocks surged to a fresh intra-day record, propelled by a rally in chip stocks after Beijing’s anti-monopoly ruling on Nvidia. The MSCI Asia Pacific Index rose as much as 0.8% to reach its highest level on record, as chip stocks such as TSMC and Samsung Electronics led gains. Investor sentiment remained upbeat also on expectations of a Federal Reserve rate cut this week. Chip stocks jumped on Tuesday after a Chinese regulator ruled that Nvidia violated anti-monopoly laws in its 2020 acquisition of networking gear maker Mellanox Technologies Ltd. The decision was interpreted by some investors as a signal of Beijing’s push to promote localization and self-sufficiency in chip technology, sparking gains in Chinese home-grown semiconductor firms. Asian equities have been on a tear recently, repeatedly testing a previous high set in 2021. Investor sentiment has gradually improved since April, boosted by easing trade tensions with the US and a resurgence in Chinese stocks due to AI developments and government efforts to cut overcapacity. Here Are the Most Notable Movers

- The unlisted shares of India’s National Commodity & Derivatives Exchange Ltd. have surged after investors including global high-speed trading firms bought stakes in the company ahead of its foray into equities.

- Nintendo lost 3.3% after fans were left disappointed by the lack of a new Mario game announcement. Disco shares gained 8.2% after Morgan Stanley said it was its top pick in Japan’s chip sector.

- GCL Technology Holdings Ltd.’s stock rose after the Chinese company announced a share sale to help fund efforts to reduce overcapacity in the solar polysilicon sector.

- Disco shares rose as much as 7.6%, their biggest intraday gain since June 27.

- Nintendo shares lost as much as 4%, the most since June 20, after the firm’s Nintendo Direct event ended without an announcement of a major new Mario game for its Switch 2 console.

- LG Display shares surge as much as 14% on expectations that Apple’s new iPhones will help the Korean display panel supplier report stronger earnings.

- Yunfeng Financial shares slide as much as 15% in Hong Kong after the financial services company and a shareholder offer 191 million shares at HK$6.10 each in a top-up placement.

- Genda shares jump as much as 20% to the daily limit after the Japanese arcade operator reported half-year earnings, with operating profit rising 0.9% from a year earlier.

- Nitto Denko shares fall as much as 3.4%, the most since Aug. 4, after the Japanese specialty chemicals company conducted its annual investor’s meeting on Friday that saw an outlook decline in its new circuit products from the year before.

In FX, the dollar weakens for a second day, boosting G-10 peers. The euro touches highest since July, closing in on its strongest level in four years. Sterling hits a two-month high too after UK jobs data backed a slower pace of cuts by the Bank of England.

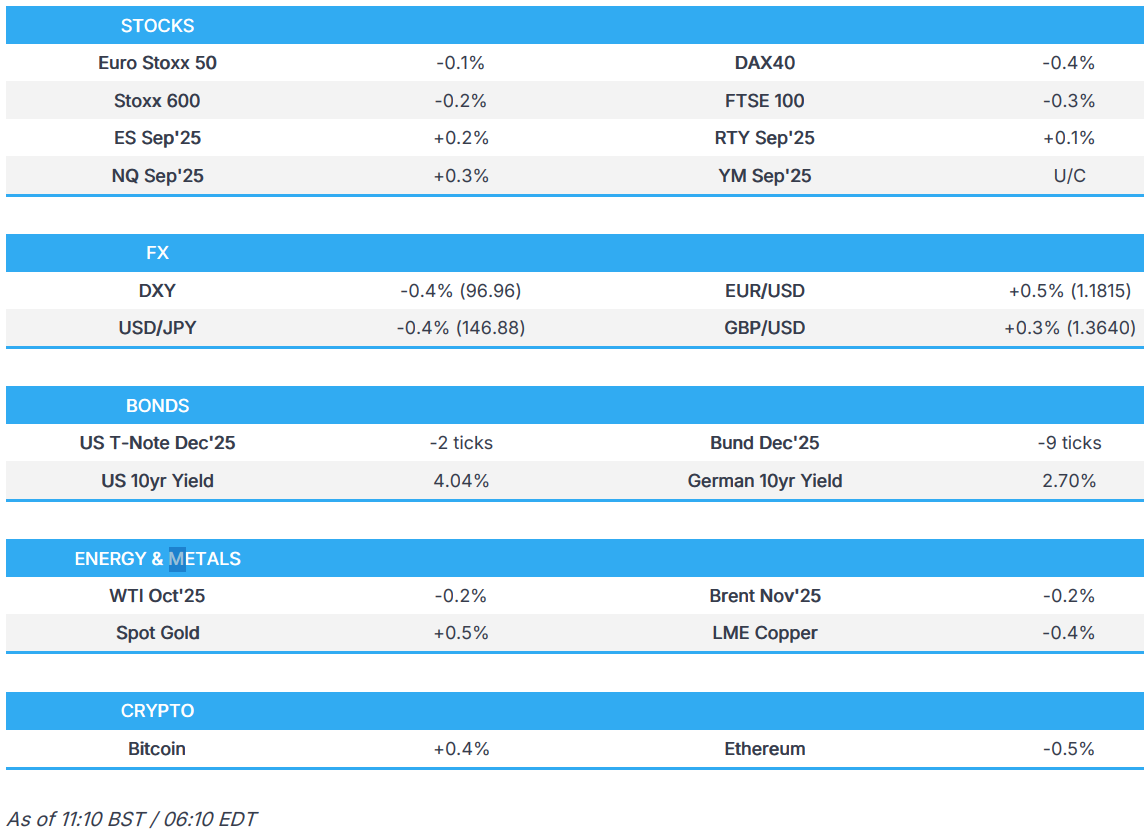

In rates, US Treasuries were little changed, with the 10-year yield at 4.04% and European bond markets, mixed for gilts. US government bonds have outpaced global peers this year, delivering a 5.8% return as expectations for policy easing reversed widely held bearish views.

In commodities, gold hits another record high, trading about $19 higher on the session to around $3,697/oz. Oil prices dip, with Brent slipping closer to $67/barrel.

Today’s economic data slate includes August retail sales and import/export prices and September New York Fed services business activity (8:30am), August industrial production (9:15am), and July business inventories and September NAHB housing market index (10am).

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.3%

- Russell 2000 mini +0.2%

- Stoxx Europe 600 -0.1%

- DAX -0.3%

- CAC 40 little changed

- 10-year Treasury yield -1 basis point at 4.03%

- VIX -0.2 points at 15.48

- Bloomberg Dollar Index -0.2% at 1191.97

- euro +0.4% at $1.1808

- WTI crude -0.4% at $63.03/barrel

Top Overnight News

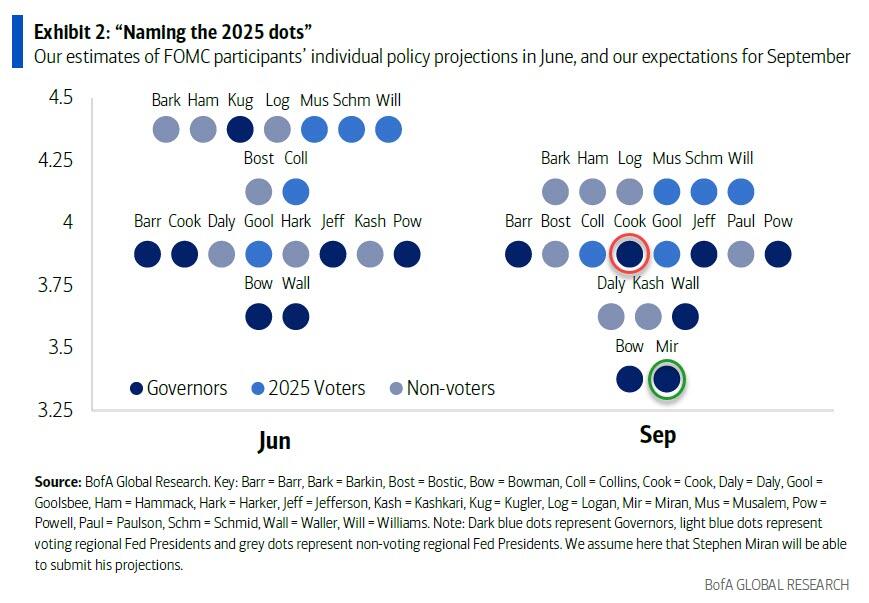

- Lisa Cook is set to take part in the FOMC meeting today and tomorrow after an appeals court blocked Donald Trump from firing the Fed governor. So is Stephen Miran, who was confirmed in a 48-47 Senate vote. BBG

- The SEC said it’s prioritizing Trump’s proposal to reduce the frequency of earnings reports after the president called for an end to quarterly disclosures. BBG

- Trump said Congressional Republicans are working on a short-term clean extension of government funding to stop Senate Minority Leader Schumer from shutting down the government.

- Trump signed a Presidential Memorandum to establish the Memphis Safe Task Force which was said to be a replica of efforts in Washington DC and will include the National Guard. Furthermore, Trump stated they are probably going to go in Chicago next and want to get to New Orleans, while he also commented that they need to save St. Louis.

- A group of GOP senators are working on legislation to extend Affordable Care Act subsidies with policy changes designed to win over conservatives, according to four people granted anonymity to disclose private discussions. Politico

- US reportedly looks to boost national strategic uranium stockpile: BBG

- Trump has filed a defamation lawsuit against the NYT seeking $15bn in damages from the media organization he accused of being a “mouthpiece” for the Democratic party. FT

- China has significant leverage when it comes to trade negotiations with Washington, including rare earth supplies and agricultural product purchases (China has halted US soybean purchases, delivering a punishing blow to American farmers). NYT

- The world must invest $540 billion annually in oil and gas exploration through 2050 to sustain output, the IEA said. Without new discoveries or demand shifts, supply may shrink by more than 5 million b/d each year — around 40% higher than it was in 2010. BBG

- The US will start formally implementing a lower 15% tariff on imports of Japanese autos and parts starting today. BBG

- Switzerland’s conservative central bank has quietly become one of the world’s biggest tech investors, amassing a stock portfolio that is equivalent in value to nearly a fifth of the national economy’s annual output. The Swiss National Bank has US equity holdings amounting $16bn, with more than $42bn invested in megacap tech. FT

- The UK labor market showed stabilizing signs after a slump triggered by higher taxes. Payrolls dropped by 8,000 in August and vacancies increased for the first time since early 2024, leaving the BOE on track to hold rates later this week. The pound gained. BBG

Trade/Tariffs

- US President Trump said he is undecided regarding a TikTok stake, and he will speak with Chinese President Xi about a significant agreement, while he believes discussions with Xi will confirm key matters.

- US opened an inclusions window for the section 232 on steel and aluminium in which the Bureau of Industry and Security established a process for including additional derivative steel and aluminium articles within the scope of the duties authorised by the President under section 232 of the Trade Expansion Act of 1962.

- Playbook citing officials reports that the forum for any UK-US talks on steel/aluminium would be a bilateral meeting, however as of Monday night there was reportedly no sign of a sit-down between UK Chancellor Reeves and US Treasury Secretary Bessent.

A more detailed look at global markets courtesy of Newsquawk

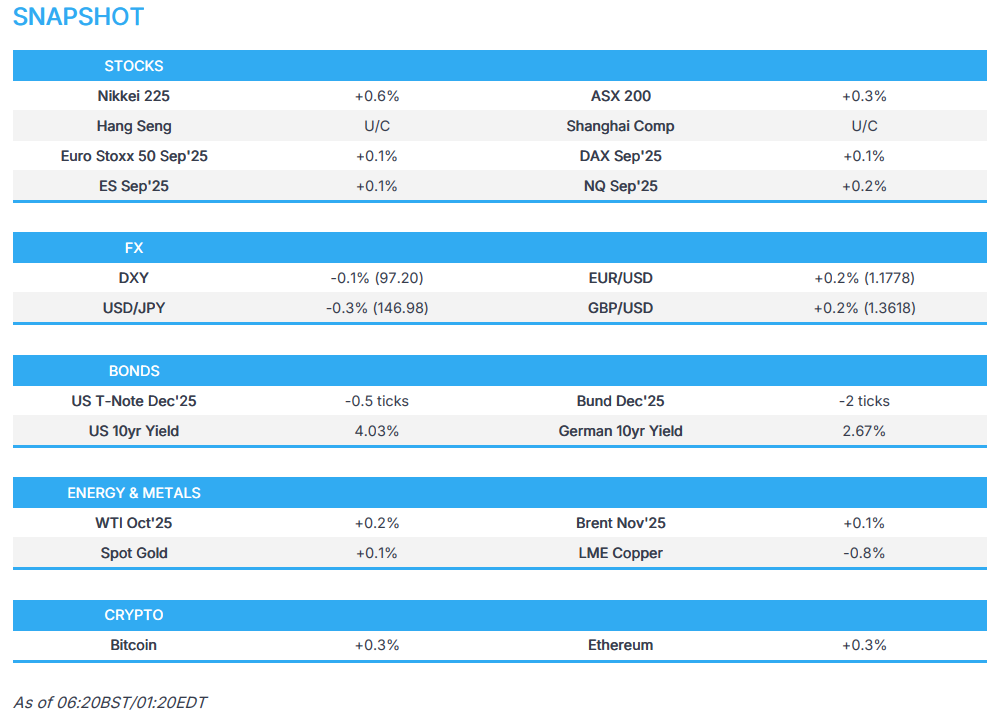

APAC stocks traded mixed amid some cautiousness ahead of upcoming risk events and despite the fresh record levels on Wall St, where the mega-caps did most of the lifting as Alphabet joined the USD 3tln market cap club. ASX 200 marginally gained with the index led by strength in mining, resources and materials, but with gains capped by weakness in defensives. Nikkei 225 swung between gains and losses following an early unprecedented climb to above the 45,000 milestone on return from the extended weekend, while the calendar was quiet, although lower US tariffs on Japan took effect. Hang Seng and Shanghai Comp were subdued despite the recent talks in Madrid where the US and China reached a framework agreement on TikTok although the details were scarce, while US President Trump and Chinese President Xi are scheduled to talk on Friday.

Top Asian News

- Japan’s Finance Minister Kato reiterated it is not appropriate to lower the consumption tax and he has decided to support Agricultural Minister Koizumi in the LDP leadership race.

- China is issuing measures on increasing consumption, according to Xinhua. Will launch a series of consumption promotion activities. Will enhance supply of quality services. Will promote an orderly opening up of sectors including the internet and cultures. Will expand pilots in telecoms, medicine and education sectors. Will extend business hours for tourist sites and museums. Will increase consumption credit support. Will coordinate funding channels, including local government special bonds, for new cultural and tourism facilities.

European bourses (STOXX 600 -0.1%) opened around the unchanged mark, but sentiment then slipped as markets turned risk-off across the board in the continent. That pressure has since slowed down a little and are off worst levels – but indices are still broadly lower. European sectors are broadly on the backfoot, in-fitting with the risk tone. IT is towards the top of the pile, boosted by strength across Dutch semiconductor names; nothing really driving the upside today, but it does come after ASML (+3%) once again overtook SAP, to become Europe’s largest company. Consumer Staples is found towards the bottom of the pile; Unilever (-1%) moves lower after it appointed a new CFO.

Top European News

- ECB’s Villeroy says French growth is not strong enough, but remains positive.

FX

- DXY is on the backfoot; currently trading towards lows of 96.96 Another weak start of the session for the index which remained subdued in APAC hours after weakening yesterday alongside softer US yields and with the greenback not helped by a drop in the NY Fed Manufacturing Survey. Participants now await Industrial Production and Retail Sales data scheduled later today, while the FOMC will also begin its 2-day policy meeting which will be attended by Fed’s Cook and Miran, after a US Appeals Court denied the Justice Department’s request to put on hold a judge’s ruling temporarily blocking Trump from removing Cook, and the US Senate confirmed Miran to join the Fed board.

- EUR/USD mildly benefits from recent dollar weakness and after ECB officials reiterated that interest rates are in a good place. In data, EUR held onto gains following mixed German ZEW survey (Economic Sentiment beat and surprisingly improved but Current Conditions missed and deteriorated), whilst the EZ metrics improved. EUR/USD eventually eclipsed 1.1800 to a current high at 1.1817.

- USD/JPY is softer amid USD weakness and broader JPY strength, with analysts at ING attributing some of the JPY upside to “the more moderate Shinjiro Koizumi is entering the LDP leadership race against Sanae Takaichi, who is seen as yen bearish for her views on loose monetary and fiscal policy.” USD/JPY found resistance near its 21 DMA (147.65) to trade in a current range between 146.69-147.54.

- GBP is benefitting from broader dollar weakness and ahead of US President Trump’s state visit to the UK, with a presser (likely joint) due on Thursday before the US leader’s departure. UK jobs data this morning were largely in line, but a slightly above-forecast employment change prompted a couple of pips of upside in cable, but nothing to write home about. Pricing remains unchanged with markets firmly expecting no change at the BoE this Thursday, with some 97% chance of a hold. Cable trades in a 1.3598-1.3642 range.

- Antipodeans trade rangebound with a slightly softer bias and following an uneventful APAC session. Comments from RBA’s Hunter and Hauser provided little to shift the dial – the former noted they are close to getting inflation to the target and that risks around the outlook are balanced.

Fixed Income

- USTs are flat, awaiting the FOMC on Wednesday, but before that, we have a Tier 1 release in the form of retail sales. Expected at +0.2% M/M in August (prev. 0.5%), while the ex-autos measure is seen rising +0.4% M/M, matching the July reading, and the Retail Control group is seen +0.4% M/M (prev. +0.5%). Thereafter, issuance in focus with a 20yr Bond auction scheduled. No concession seen in trade this morning, but that could change in the hours ahead. Elsewhere, the composition of the Fed remains in focus as Cook will remain on the board for at least the September meeting following a court update. Additionally, White House official Miran has been formally approved and will be partaking in the September meeting. Currently, USTs reside in a very thin 113-11 to 113-16 band.

- Bunds are in-fitting with peers throughout the European morning. Gapped higher around the cash equity open, seemingly as a function of the pressure seen in the equity space around this point. German ZEW for September was mixed. Economic sentiment came in above consensus and seemingly spurred some modest pressure in Bunds with financial market experts cautiously optimistic. However, the current situation has deteriorated amid ongoing US tariff concern and into the German fiscal reform window. As such, Bunds quickly retraced that pressure and are back to pre-release levels. Thereafter, a weaker-than-prior German 2030 auction spurred another bout of pressure in Bunds, back towards earlier lows of 128.54.

- Gilts are modestly lower. No significant follow-through from the morning’s jobs data. Overall, the release was broadly in-line with consensus with the labour market continuing to cool though the pace of this is seemingly beginning to slow. While the continued slowing is arguably a dovish sign, it is counteracted by the (as expected) uptick in wages, which remain at levels likely inconsistent with inflation sustainably settling at target over the medium term. Note, the next CPI release is Wednesday, where the headline Y/Y is expected at 3.8% (prev. 3.8%). Elsewhere, supply was soft. A sub-3x cover and a chunky tail, reminiscent of the auction before last. Results of this sent Gilts lower by just under 10 ticks, but comfortably within existing parameters. Gilts opened the morning unchanged from Monday’s close at 91.47, before briefly dipping to a 91.31 low and then retracing to a 91.57 peak.

- UK sells GBP 3bln 4.375% 2040 Gilt: b/c 2.95x (prev. 3.69x), average yield 5.048% (prev. 5.066%) & tail 0.9bps (prev. 0.1bps)

- Germany sells EUR 3.491bln vs exp. EUR 4.5bln 2.20% 2030 Bobl: b/c 1.70x (prev. 1.90x), average yield 2.29% (prev. 2.32%) & retention 22.42% (prev. 23.19%)

Commodities

- Subdued trade in the crude complex with aggressive losses seen around the time of the European cash equity open which also came despite USD weakness. One of the bearish factors could be reports that the 19th EU sanctions package against Russia is no longer expected to be presented on Wednesday, via Politico citing an EU diplomat (since corroborated by other reports); no detail on when the sanctions would be unveiled. WTI currently resides in a USD 62.89-63.55/bbl range while Brent sits in a USD 67.01-67.68/bbl range.

- Spot gold holds an upward bias as it continues printing fresh records on its way to USD 3,700/oz against the backdrop of a softer dollar and heightened geopolitics. Spot gold currently resides in a USD 3,674.70-3,697.40/oz range with the top end of the band the latest all-time high.

- Base metals are mostly softer despite the softer dollar and gains in US futures, albeit the mood in Europe is slightly more mixed. 3M LME copper holds above USD 10k/t and resides in a USD 10,087.90-10,177.70/t range at the time of writing.

- Commerzbank revises its gold price forecast upward to USD 3,600/oz for end-year; raises silver year-end forecast for 2025 to USD 41/oz and 2026-end forecast to USD 43/oz.

- Thai Central Bank says they have discussed tax on gold trades; to support gold trades in Dollars; other measures on gold trades were discussed.

- Ukraine’s military says it struck Russia’s Saratov oil refinery (140k BPD) in overnight attack.

Geopolitics: Middle East

- Israel has launched its ground incursion into Gaza City, two Israeli officials told CNN early Tuesday; One of the officials said the ground incursion is going to be “phased and gradual” at the beginning.

- Israel military official says will be increasing the amount of troops into Gaza city as the days go by.

- US President Trump said Israel won’t be attacking Qatar.

- US President Trump posted about Hamas moving hostages above ground to use them as human shields and stated “I hope the Leaders of Hamas know what they’re getting into if they do such a thing. This is a human atrocity, the likes of which few people have ever seen before. Don’t let this happen or, ALL “BETS” ARE OFF. RELEASE ALL HOSTAGES NOW!”

- US Secretary of State Rubio said before heading to Qatar, that they hope Qatar will re-engage on Gaza talks despite everything that’s happened, while he added that they have a very short window in which a deal on Gaza can happen and that they are on the verge of finalising an enhanced defence cooperation agreement with Qatar.

Geopolitics: Ukraine

- Polish government is boosting its cyber security budget to a record EUR 1bn this year, after Russian sabotage attempts targeted hospitals and urban water supplies, according to FT.

- Japanese Finance Minister Kato said Japan pledged to comply with WTO rules, but will consider measures to raise pressure on Russia and coordinate with G7 countries, when asked about US requests to G7 for higher sanctions on India and China for buying Russian oil.

- The 19th EU sanctions package against Russia is now off the agenda for Wednesday’s EU ambassadors meeting, no new date has been set, via an EU official. Confirmation of earlier reporting via Politico

- Russia says its drones have struck a Ukrainian gas distribution station reportedly used by the military.

US Event Calendar

- 8:30 am: Aug Retail Sales Advance MoM, est. 0.2%, prior 0.5%

- 8:30 am: Aug Retail Sales Ex Auto MoM, est. 0.4%, prior 0.3%

- 8:30 am: Aug Retail Sales Ex Auto and Gas, est. 0.4%, prior 0.2%

- 8:30 am: Aug Import Price Index MoM, est. -0.2%, prior 0.4%

- 8:30 am: Aug Import Price Index YoY, est. 0%, prior -0.2%

- 9:15 am: Aug Industrial Production MoM, est. -0.1%, prior -0.1%

- 9:15 am: Aug Capacity Utilization, est. 77.4%, prior 77.5%

- 10:00 am: Jul Business Inventories, est. 0.2%, prior 0.2%

- 10:00 am: Sep NAHB Housing Market Index, est. 33, prior 32

DB’s Jim Reid concludes the overnight wrap

I woke up this morning the father of a 10-year-old daughter. Where did the time go? Don’t tell my family as it’s a surprise for tonight, but I spent part of the summer writing and recording a new song and creating a video celebrating Maisie’s first decade. The world premiere at home will be after a night out at an escape room tonight… if we escape.

As we await tomorrow’s FOMC decision, markets have continued to power forward over the last 24 hours, with risk appetite supported by positive noises out of the US-China trade talks. That newsflow led to growing optimism that some kind of longer-term truce would eventually be reached between the two, and those hopes of a cooling in the trade war meant both the S&P 500 (+0.47%) and the NASDAQ (+0.94%) closed at another record high. Moreover, it was a decent session for sovereign bonds as well, thanks to mounting anticipation that the Fed would deliver another rate cut at tomorrow’s meeting. So, it was a strong day all round, and US Treasuries also rallied across the curve, with the 10yr yield (-2.8bps) falling back to 4.04%.

Ahead of today’s start to the FOMC, an appeals court last night blocked Mr Trump from firing Lisa Cook from the Fed board before her appeal against her dismissal is heard. So, she will likely be at the meeting barring any additional legal action. Stephen Miran could also sit as he was confirmed in his new post by the Senate last night. So, it’s shaping up to be an interesting 2-day meeting.