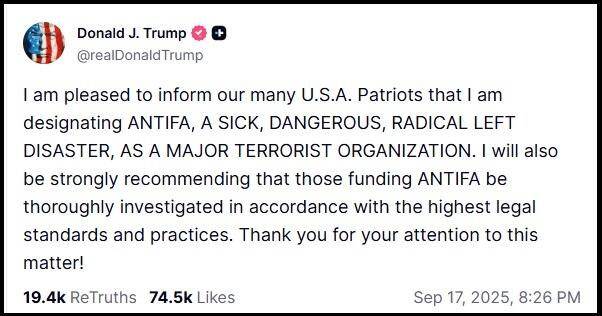

SEPT 18/HUGE RAID ON GOLD AND SILVER: GOLD CLOSED DOWN $37.50 TO $3645.50/SILVER CLOSED DOWN ONLY 3 CENTS TO $41.82//PLATINUM HAD A GOOD DAY UP $16.55 TO $1392.95 WITH PALLADIUM ALSO UP BY $13.20 TO $1167.50//GOLD COMMENTARY TONIGHT COURTESY OF ALASDAIR MACLEOD//TRUMP IS NOW SET TO GO AFTER SOROS AND HIS OSF “CHARITY” ON RICO CHARGES, AS WELL AS ANTIFA//BANK OF ENGLAND HOLDS RATES STEADY TODAY//ISRAEL VS HAMAS UPDATES: LAST 24 HRS PODCAST COURTESY OF ISRAEL TBN/WEST BANK UPDATES//RUSSIA VS UKRAINE UPDATS/COVID HEALTH ISSUES/DR PAUL ALEXANDER/NEWS ADDICTS/EVOL NEWS/MIKE EVERY COMMENTARY//ECONOMIC PROBLEMS FOR CANADA REPORTED/USA DATA RELEASES//JIMMY KIMMEL THROWN OUT BY DISNEY AND OTHER STATIONS//SWAMP STORIES FOR YOU TONIGHT//

118 H MACQUARIE FUTURES US 109 323 C HSBC 160 363 H WELLS FARGO SECURITI 139 435 H SCOTIA CAPITAL (USA) 6 661 C JP MORGAN SECURITIES 104 686 C STONEX FINANCIAL INC 9 16 732 C RBC CAP MARKETS 5 737 C ADVANTAGE FUTURES 2 8 880 C CITIGROUP 2

TOTAL: 280 280 MONTH TO DATE: 6,050

MONTH TO DATE: 5,770

JPMORGAN STOPPED 109/280

SEPT

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 280 CONTRACTs NOTICES FOR 28,000 OZ or 0.8709 TONNES

total notices so far: 6050 contracts for 605000 OR 18.818 tonnes)

FOR SEPT

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 117 NOTICE(S) FILED FOR 0.585 MILLION OZ/

total number of notices filed so far this month : 13,138 CONTRACTS (NOTICES) for 65.640 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $37.50 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 975.66 TONNES

INVENTORY RESTS AT 979.95. TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.03 AT THE SLV:

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:/ A WITHDRAWAL OF 0.908 MILLION OZ PUT OF THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 488.357 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUGE 2065 CONTRACTS TO 160,889 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS MEGA HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE LOSS OF $0,69 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE FINALLY ARE MOVING TO A MUCH HIGHER BASE SURPASSING THE $34.40 SILVER PRICE BARRIER TO A HIGH DEGREE CLOSING IN ON THE MAGIC ALL TIME HIGH OF $50.00. WE HAD A HUGE SIZED LOSS OF 1425 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE 640 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD SOME LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $42.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON WEDNESDAY WITH SILVER’S LOSS IN PRICE. THE PRICE FINISHED STILL MILES ABOVE THE MAGIC NUMBER OF $40.00 SILVER SPOT PRICE CLOSING AT $41.85 LOSING 69 CENTS. . WE FINALLY STOPPED HAVING THOSE MEGA MEGA HUGE T.A.S. ISSUANCE BUT STILL WITNESSING SOMETIMES LARGE ISSUANCE: HOWEVER TODAY’S TOTAL ISSUANCE WAS RECORDED AT A HUGE SIZED 848 CONTRACTS. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 40.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A HUGE 640 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 848 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S RAID//// TRADING / AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUGE SIZED 1425 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $0.69.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE SIZED 848 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.69) AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE SIZED LOSS OF 1425 CONTRACTS ON OUR TWO EXCHANGES,

WE HAD A 640 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 49.825 MILLION OZ COUPLED WITH TODAY’S 0.560 MILLION OZ QUEUE JUMP TO WHICH WE ADD OUR INITIAL 3.0 MILLION OZ OF EXCHANGE FOR RISK SEPT. ISSUANCE//NEW STANDING ADVANCES TO 69.730 MILLION OZ///

THUS:

INITIAL STANDING FOR SEPT: 69.730 MILLION OZ

WE HAD:

/ HUGE COMEX OI LOSS+// A HUGE SIZED EFP ISSUANCE 640 CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 848 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: XXXX CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 12 DAY(S), total 6490 contracts: OR 32.450 MILLION OZ (540 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 32.450 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 32.450 MILLION OZ.(QUITE SMALL)

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2065 CONTRACTS WITH OUR LOSS IN PRICE OF $0.69 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE 640 CONTRACT EFP ISSUANCE CONTRACTS: 640 ISSUED FOR SEPT., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 6 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 66.730 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING) PLUS 3.0 MILLION OZ EX FOR RISK = 69.730 MILLION OZ. THIS IS THE FIRST ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (848) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH TODAY’S TRADING!!

WE HAD 117 NOTICE(S) FILED TODAY FOR 0.585 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1357 OI CONTRACTS TO 517,578 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A RELATIVELY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL 383 CONTRACTS //.

WE HAD AN INCREASE IN COMEX OI (1357 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $8.30 IN PRICE// WEDNESDAY///.

LAST 5 MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.5163 TONNES PLUS 2.954 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 19.319//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 38.252 TONNES!!

E.F.P. ISSUANCE/FOR OPENING SEPT GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1215 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 517,758 / GETTING HIGHER AND WE NOW WITNESS A FAIR COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A LOW COMEX OI OF 160,889 CONTRACTS

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3252 CONTRACTS WITH 1357 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1895 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3252 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED AND CRIMINAL 821 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON LIKE THIS MORNING. GOLD PRICE ON WEDNESDAY ROSE BY $8.30

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(1895) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 1357 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3252 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR SEPT AT 8.093 TONNES PLUS 0.5163 TONNES QUEUE JUMP PLUS 2.954 TONNES EXCHANGE FOR RISK TODAY AND FOR THE MONTH 19.319 TONNES//NEW STANDING ADVANCES TO = 38.252 TONNES.@!!!

NEW STANDING FOR GOLD, SEPT CONTRACT AT 38.252 TONNES OF GOLD

.

/ 3) ZERO T.A.S. LIQUIDATION AS WE HAD 1)A $8.30 COMEX PRICE GAIN. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A FAIR SIZED GAIN OF 3252 CONTRACTS ON OUR TWO EXCHANGES /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND YOU CAN VISUALIZE THIS BY THE HUGE AMOUNTS OF QUEUE JUMPING WE HAVE BEEN HAVING LATELY (TODAY = 0.163 TONNES)

4) FAIR SIZED COMEX OI GAIN// 5) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (1895 CONTRACTS)/// SMALL T.A.S. ISSUANCE: 821 T.A.S.CONTRACTS/

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

TOTAL EFP CONTRACTS ISSUED: 23,068 CONTRACTS OR 2,306,800 OZ OR 71.751 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 1922 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN12 TRADING DAY(S) IN TONNES: 71.751 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 71.751 TONNES DIVIDED BY 3550 x 100% TONNES = 2.02% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

UNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 71.751 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE 2065 CONTRACTS OI TO 160,889 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 640 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 640 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 640 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2065 CONTRACTS AND ADD TO THE 640 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF 1425 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE LOSS IN PRICE OF $0.69 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 7.125 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED DOWN 44.69 PTS OR 1.15%

//Hang Seng CLOSED DOWN 363.54 PTS OR 1.35%

// Nikkei CLOSED UP 513.05 OR 1.15% //Australia’s all ordinaries CLOSED DOWN .70%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1075 OFFSHORE CLOSED DOWN AT 7.1047/ Oil DOWN TO 63.98 dollars per barrel for WTI and BRENT DOWN TO 67.89 Stocks in Europe OPENED ALL GREEN EXCEPT ITALY

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1075 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1047 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1,357 CONTRACTS TO 517,578 OI WITH OUR GAIN IN PRICE OF $8.30 WITH RESPECT TO WEDNESDAY’S // TRADING COMEX CLOSING TIME: 1:30 PM RIGHT BEFORE THE INTEREST RATE ANNNOUNCEMENT… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1895). WE HAD ZERO T.A.S. LIQUIDATION AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3252 CONTRACTS (OR 10.11 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD A HUGE 950 CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 95,000 OZ OR 2.954 TONNES OF GOLD

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 3 MONTHS;

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW WEDNESDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

AND NOW:

SEPT:

SEPTEMBER: FIVE ISSUANCES SO FAR TOTALLING 6,211 CONTRACTS OR 621,100 OZ OR 19.319 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW YESTERDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: FIVE ISSUANCES FOR 6211 CONTRACTS SO FAR FOR 621,100 OZ OR 19.319 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS AND :

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH SEPT//ONLY MISSING JUNE.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON SEPTEMBER COMEX MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 3635 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A SMALL T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 821 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT LAST NIGHT SEPT 17-SEPT 18.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH PREVIOUS AUGUST MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.5163 TONNES QUEUE JUMP TO GO ALONG WITH THE 2.954. TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 19.319 TONNES//NEW TOTALS STANDING ADVANCES TO 38.252 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 240 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

AND NOW SEPTEMBER:

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.5163 TONNES QUEUE JUMP AND 2.954 TONNES EXCHANGE FOR RISK TODAY// NEW TOTALS OF 19.319 TONNES OF EXCHANGE FOR RISK ISSUANCE/:

THAT IS;

A) 2.954 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY // =//TOTAL FOR MONTH EX FOPR RISK: 19.319 TONNES EX FOR RISK!!

B) 0.5163 TONNES TODAY QUEUE JUMP

TOTALS: 38.252 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1895 EFP CONTRACT WAS ISSUED: : /DEC 1895 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1895 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//WEDNESDAY

MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE. IT IS QUITE POSSIBLE THAT THEY USED MONTHLY SEPT SPREADERS IN THEIR RAID TODAY.

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A FAIR SIZED SIZED 1895 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

2) AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

3) TO BE FOLLOWED BY SEPTEMBER’S 5 ISSUANCES FOR EXCHANGE FOR RISK FOR 19.319 TONNES.

GOLD STANDING AT THE COMEX FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

AND NOW SEPT:

SEPT: 18.933 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) +2.954 TONNES EX FOR RISK TODAY//

TOTAL EX FOR RISK// FOR MONTH = 19.319//NEW TOTALS FOR GOLD STANDING SEPT = 38.252 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A STRONG $8.30./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION YESTERDAY AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE GOVERNMENT TRADING AND SPECULATIVE LONGS PILING INTO COMEX TRADING /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS LIKE TODAY ON OUR PRECIOUS METALS).

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A FAIR SIZED GAIN TOTAL OF 10.11 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 0.578 TONNES OF GOLD ALONG WITH 2.954 TOTAL TONNES OF EXCHANGE FOR RISK TODAY/// TOTAL FOR MONTH TOTALS EX FOR RISK// MONTH = 19.319//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 38.252 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $45.30

WE HAD A SMALL 383 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 3252 CONTRACTS OR 325200 0Z (10.11 TONNES)

i) Out of Brinks 31,057.866 oz (966 kilobars) total withdrawal 31,057.866 oz

.966 tonnes

.

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

DEPOSITS/CUSTOMER

1 ENTRIES

i) Into Asahi 80,505.267/ (2504 KILOBARS)

2.504 TONNES

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

280 notice(s) 28,000 OZ 0.8709 TONNES

No of oz to be served (notices)

37 contracts 3700 OZ 0.1151 TONNES

Total monthly oz gold served (contracts) so far this month

6050 notices 605,000 oz 18.818 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER 1

i) Into Asahi: 80,505.267 oz

(2504 kilobarss)

total deposit 80,505.267 oz

2.504 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1.entries

1entries

i) Out of Brinks 31,057.866 oz (966 kilobars) total withdrawal 31,057.866 oz

.966 tonnes

ADJUSTMENTs 2

a) Customer to dealer Brinks 96,453.000 oz (3000 kilobars)

b) customer to dealer Asahi 46,008.993 oz

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 317 CONTRACTS FOR A GAIN OF 43 CONTRACTS. WE HAD 123 CONTRACTS FILED ON WEDNESDAY SO WE GAINED 166 CONTRACTS OR 16,600 OZ ENTERTAINED A QUEUE JUMP OF 0.5163 TONNES. WE NOW MUST ADD TO OUR INITIAL 8.093 TONNES OF GOLD STANDING TO TODAY’S QUEUE JUMP OF 0.5163 TONNES AND THEN ADD MONTH SEPT// EX FOR RISK = 19.319//(WHICH INCLUDES TODAY’S 2.934 TONNES EX. FOR RISK) THUS NEW TOTAL OF GOLD STANDING ADVANCES TO 38.252 TONNES

OCTOBER GAINED 24 CONTRACTS UP TO 59,578

NOVEMBER GAINED 106 CONTRACTS UP TO 3371 CONTRACTS.

We had 280 contracts filed for today representing 28000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 280 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 104 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (6050 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 317 CONTRACTS) minus the number of notices served upon today (280 x 100 oz per contract) equals 608,700 OZ OR 18.933 TONNES OF GOLD TO WHICH WE ADD OUR TOTAL EX FOR RISK/SEPT MONTH OF 19.319 TONNES//NEW TOTAL STANDING ADVANCES TO 38.252 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (6050 x 100 oz +we add the difference for front month of SEPT. (317 OI} minus the number of notices served upon today (280 x 100 oz) which equals 608,700 OZ OR 18.933 TONNES PLUS 19.319 TONNES EXCHANGE FOR RISK = 38.252 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 38.252 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,030,684.621 oz 63.162 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,280,533,848 oz

TOTAL REGISTERED GOLD 21,511,920.651 or 669.11 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,768,613.197 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,481,236oz ((REG GOLD- PLEDGED GOLD)= 605.95 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 17 2025

INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

3entries

1) Out of Delaware: 6173.324 oz ii) Out of Loomis 548,951.620 oz iii) Out of Stonex 685,516.270 ooz

total withdrawal 1,240,641.214 oz

Deposits to the Dealer Inventory

0 ENTRY

Deposits to the Customer Inventory

0

No of oz served today (contracts)

117 CONTRACT(S) (0.585 million OZ

No of oz to be served (notices)

218 contracts (1.090 MILLION oz)

Total monthly oz silver served (contracts)

13,128 Contracts (65.640 million oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

1) Out of Delaware: 6173.324 oz ii) Out of Loomis 548,951.620 oz iii) Out of Stonex 685,516.270 ooz

total withdrawal 1,240,641.214 oz

ADJUSTMENTs 0

TOTAL REGISTERED SILVER: 194.327 MILLION OZ//.TOTAL REG + ELIGIBLE. 524 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPT.

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 335 OPEN INTEREST CONTRACTS FOR A LOSS OF 490 CONTRACTS. WE HAD 602 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED A HUGE SIZED 112 CONTRACTS OR 560,000 OZ ENTERTAINED A STRONG QUEUE JUMP//NEW STANDING FOR SILVER COMEX INCREASES TO 66.730 MILLION OZ. THEN WE MUST ADD OUR INITIAL ISSUANCE OF 600 CONTRACTS FOR EXCHANGE FOR RISK OR 3.0 MILLION OZ//NEW STANDING ADVANCES TO 69.730 MILLION OZ

STANDING FOR SILVER: 69.730 MILLION OZ

OCTOBER GAINED 262 CONTRACTS TO 2822

NOVEMBER GAINED 126 CONTRACTS UP TO 1869.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 117 or 0.585 MILLION oz

CONFIRMED volume; ON WEDNESDAY 97,120 strong//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 13,128 X5,000 oz = 65.640 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (335) AND the number of notices served upon today (117 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (13,128) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(335) minus number of notices served upon today (117)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 66.170 MILLION OZ TO WHICH WE ADD OUR INITIAL EXCHANGE FOR RISK SEPT TOTALLING 3.0 MILLION OZ//NEW STANDING ADVANCES TO 69.730 MILLION OZ

New total standing: 69.730 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 194.327 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/524.086 million. 40.00%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

GLD INVENTORY: 979/95 TONNES, TONIGHTS TOTAL

SILVER

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

The Fed’s interest rate cut yesterday and the prospect of more to come confirms its changing priorities. Consequently, the dollar will weaken against both gold and other currencies.

Anticipating and following the Fed’s rate cut gold and silver are seeing a healthy shakeout, which could continue in the short-term. My guess is that both will go higher when the dollar’s TWI breaks down below current 96.75 (currently 97.00). It could be the key to timing:

Given confirmation that the Fed is giving in to political pressure (targeting unemployment is a handy excuse), it shouldn’t be long before the dollar breaks down into lower ground. For non-technical analysts, take my word for it: the chart above is bearish.

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Complacency is the order of the day with bond yields having declined, leading foreigners and US investors to think everything is normal. But the Fed is cutting interest rates just as inflationary pressures begin to mount, illustrated in the chart below:

Combine this bullish commodity setup with the dollar’s bearish outlook, for the Fed to de-emphasise inflation is a big mistake which will drive the dollar lower against not just other currencies but principally gold and other commodities..

Doubtless, traders will wait a little more for things to play out, seeing a possibility of further consolidation in gold and silver. Sensible stackers should not try to double guess the consolidation and do what the world’s central banks are doing: buy gold into the dips.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 240

a must view

5. COMMODITY REPORT COFFEE

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED DOWN 44.69 PTS OR 1.15%

//Hang Seng CLOSED DOWN 363.54 PTS OR 1.35%

// Nikkei CLOSED UP 513.05 OR 1.15% //Australia’s all ordinaries CLOSED DOWN .70%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1075 OFFSHORE CLOSED DOWN AT 7.1047/ Oil DOWN TO 63.98 dollars per barrel for WTI and BRENT DOWN TO 67.89 Stocks in Europe OPENED ALL GREEN EXCEPT ITALY

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1075 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1047 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1075

OFFSHORE YUAN: UP TO 7.1047

HANG SENG CLOSED DOWN 363.54 PTS OR 1.35%

2. Nikkei closed UP 513.05 PTS OR 1.15%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 96.62 EURO RISES TO 1.1826 UP 6 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.597//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.37…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.193 DOWN 1 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6942 Italian 10 Yr bond yield UP to 3.509 SPAIN 10 YR BOND YIELD UP TO 3.249

3i Greek 10 year bond yield UP TO 3.371

3j Gold at $3665.80 Silver at: 41.81 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 20 /100 roubles/dollar; ROUBLE AT 82.78

3m oil (WTI) into the 63 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.37/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.597% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.193 DOWN 1 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7890 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9332 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.054 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.653 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.530 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.33

10 YR UK BOND YIELD: 4.6410 UP 1 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.440 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.191 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.757 UP 4 BASIS PTS.

2a New York OPENING REPORT

Futures Jump To Fresh Record High After Fed Restarts Rate Cuts

Thursday, Sep 18, 2025 – 08:32 AM

Futures are higher and back into record territory as investors shrug off some contradictions in the Fed’s policy statement and Powell’s hawkish news conference and refocus on the most dovish Fed statement since 2021, per JPM. “For whatever reason, it appears the Fed’s reaction function has shifted in a more dovish direction,” according to Bloomberg Econ head Anna Wong. S&P 500 futures were 0.8% higher at 8:05 am ET while Nasdaq 100 futures were +1.1%. Pre-mkt, Mag7 / Semis are bid up with NVDA +2.3%, AVGO +1.9%, TSLA +1.6%, GOOG +1.3%; tech was boosted by news that NVDA would buy a $5BN stake in rival chipmaker Intel. Nikkei +1.15%, Hang Seng -1.35%, Shanghai -1.15%, FTSE +15bps, CAC +1.1%, DAX +1.2%. “Last night the market was taking the view that this wasn’t so much of a dovish cut but, after sleeping on it, it decided that it was enough to keep the market going,” said Karen Georges, an equity fund manager at Ecofi in Paris. “Fed cuts are good for tech and long duration stocks.” Sure enough, both tech and small caps are outperforming as the US is poised for an “Everything Rally” alongside a global risk-on tone. The yield curve is bull flattening and USD is flat. Large-Caps across all the super-sectors are higher pre-mkt. Today’s macro data focus is on jobless claims where investors will look to confirm last week’s spike was a one-off.

In premarket trading, Mag 7 stocks are green across the board (Tesla +1.1%, Nvidia +3%, Alphabet +1.2%, Microsoft +0.3%, Apple +0.4%, Amazon +0.5%, Meta Platforms +0.6%). Some other notable movers:

89bio (ETNB) surges 83% after Roche said it will acquire the biopharmaceutical company for up to $3.5 billion.

Cracker Barrel (CBRL) falls 8% after its sales guidance missed expectations, showing the brand is still dealing with the fallout from its controversial and short-lived logo change.

CrowdStrike (CRWD) rises 4% in the wake of an investor briefing where the software company discussed its AI strategy and gave a preliminary FY27 outlook for net new annual recurring revenue that analysts see as strong.

Darden Restaurants (DRI) falls 6% after adjusted earnings per share missed expectations. Same-store sales growth for Olive Garden also came in below consensus estimates.

FactSet (FDS) slips 3% after the the financial data provider forecast adjusted earnings per share for 2026, guidance that missed the average analyst estimate.

GE Healthcare Technologies (GEHC) ticks 1.7% higher as the company is exploring options including the sale of a stake in its China unit, people familiar with the matter said.

Intel (INTC) climbs 28% after Nvidia agreed to invest $5 billion in the company and said the two will codevelop chips for PCs and data centers.

IonQ (IONQ) gains 4% after the company signed a MOU with the US Department of Energy to advance the development and deployment of quantum technologies in space.

Red Cat Holdings (RCAT) falls 10% after the drone technology company launched a secondary offering of shares via Northland Capital Markets.

In tech news, Huawei unveiled new technology from memory chips to AI accelerators, outlining a multiyear plan to challenge Nvidia’s dominance. Elsewhere, the FT reported that China has decided to end an antitrust investigation into the dominance of Google’s Android. And Meta unveiled its first smart glasses with a built-in screen, the $799 Meta Ray-Ban Display.

In other corporate news, Disney’s ABC is taking Jimmy Kimmel Live! off the air indefinitely amid a backlash to remarks the late-night host made about the killing of Charlie Kirk. And Eli Lilly said that Mounjaro helped kids as young as 10 control their blood sugar and lose weight.

While stocks initially fluctuated in the hours after the Fed’s decision, on Thursday investors turned their focus to projections showing two more rate cuts for 2025, one more cut than they saw in June. That said, there is no smoking guy for the overnight strength with as news flow is light. Strategists said the Fed’s focus on recent labor-market weakness suggests it’s ready to support the economy, even at a time when growth remains robust and corporate profits advance. According to Goldman, the “FOMC statement leaned dovish while Powell was more balanced and framed the cut as “risk management” in response to downside risks in the labor mkt.”

“The ‘front-loading’ is probably the most important part of all this,” said Michael Brown, research strategist at Pepperstone Group Ltd. “If labor market weakness persists, then the Fed will continue to cut. The monetary backdrop is set to become much easier, much sooner.”

Also overnight, Norway’s Norges Bank cut 25bps (as expected) and the the BoE kept rates unchanged at 4.00% also as expected.

Meanwhile, the AI narrative remains a key thematic driver for many, while small-caps — typically more sensitive to rate cuts — are quietly breaking out of a long-term downtrend. Citigroup strategists note that Fed cuts have historically been a tailwind for global equities and a catalyst for broadening market performance. And investors who have driven stocks to record highs do expect a rather positive growth backdrop. Bank of America’s fund manager survey published this week showed that 67% anticipate a soft landing and 18% no landing, with only 10% braced for a downturn.

Europe’s Stoxx 600 is up by 0.6% with tech firms leading the way. Here are some of the biggest European movers today:

Kone shares rise as much as 5%, hitting their highest level since early 2022, as the Finnish company is exploring a potential bid for rival TK Elevator

Wolters Kluwer shares rise as much as 5.6% on Thursday after the professional publisher said it’s speeding up the pace of share buybacks

Renishaw advances as much as 9.2%, hitting the highest since mid February, after the precision measuring equipment maker reported its full-year results

Nanobiotix shares rise as much as 20% to the highest since October 2021 after the French biotechnology company announced positive new results from an early-stage clinical study

Inchcape shares climb as much as 5% after analysts at UBS initiated coverage on the automotive distributor with a buy rating

Spire Healthcare shares rise as much as 7.7% as certain investors push the private hospital operator to explore a sale, according to a report from Sky News

OVS shares rise as much as 8.1% in Milan, the most since April 10, after the Italian fashion retailer reported an increase in adjusted Ebitda and net sales for the first half of the year.

Lime Technologies gains as much as 7.6%, the most since May, after DNB Carnegie raised its view on the Swedish enterprise software group to buy from hold

SIG shares fall as much as 24%, the most on record, triggering a temporary trading halt after the Swiss packaging maker cut its revenue growth guidance for 2025

Next shares drop as much as 6.6% after the UK fashion retailer said it expects UK sales growth to be lower in the second half compared with the first

Barry Callebaut falls as much as 5.1%, the most in a month, after Deutsche Bank cut its recommendation on the Swiss chocolate firm to hold from buy

Pets at Home shares plummet as much as 23%, marking the biggest drop on record, after the pet supply retailer warned the market remained subdued

Earlier in the session, Asian stocks fell, weighed by late losses in Chinese shares as a tech-led rally showed signs of cooling. The MSCI Asia Pacific Index dropped as much as 0.7%, on course to snap a 10-day winning streak. Chinese tech giants Tencent and Alibaba were among the main drags on the gauge. Australian energy firm Santos also posted steep losses after a third attempted sale faltered. The decline on Thursday puts a pause on the Asian benchmark’s climb after hitting a record high in the previous session. Sentiment in the region was downbeat even as the Federal Reserve cut interest rates. Trading in Chinese equities turned volatile late in the day, with analysts pointing to profit taking after the recent rally. Mainland China’s benchmark CSI 300 Index fell 1.2%, while a gauge of Hong Kong-listed Chinese shares dropped 1.5%. Equities also fell in New Zealand after the country’s economy shrank more than expected in the second quarter. Elsewhere, South Korea outperformed as chipmakers got a boost from expectations for earnings to beat estimates amid an environment of lower borrowing cost. Tech stocks also rose in Japan on continued interest in artificial intelligence.

In FX, the dollar swoons against G-10 currencies, with the Bloomberg Dollar Spot Index erasing most of its earlier gain. New Zealand dollar is the worst performer following a weak GDP reading. Sterling and gilts are steady ahead of an expected hold from the Bank of England. Norwegian krone pares its decline against the euro after Norges Bank cuts rates but gives a hawkish outlook.

In rates, US Treasuries outperform peers as European bonds decline; Treasuries held gains accumulated during Asia session and European morning, erasing Wednesday’s losses that followed Fed Chair Powell’s post-FOMC comments advocating a cautious approach to further easing. Treasury yields are 3bp-4bp richer across the curve with intermediates leading, flattening 2s10s and 2s5s spreads by about 1bp; 2s5s30s fly is about 1.5bp richer after widening sharply Wednesday. US 10-year yield is back down to around 4.05%, richer by 4bp on the day, with bunds and gilts in the sector lagging by 5bp. Following Wednesday’s FOMC rate cut, OIS contracts price in around 45bp of additional easing over this year’s two remaining meetings and a terminal rate of around 2.9% by mid-2026. Treasury auctions resume at 1pm New York time with $19 billion 10-year TIPS reopening. Focal points of US session include weekly jobless claims data and a 10-year TIPS reopening. UK gilts have had muted initial reaction to Bank of England voted 7-2 to keep policy rate at 4% as expected.

In commodities, gold reverses an earlier decline to gain about $9 to around $3,668/oz and oil prices fluctuate in a narrow range, with Brent below $68/barrel.

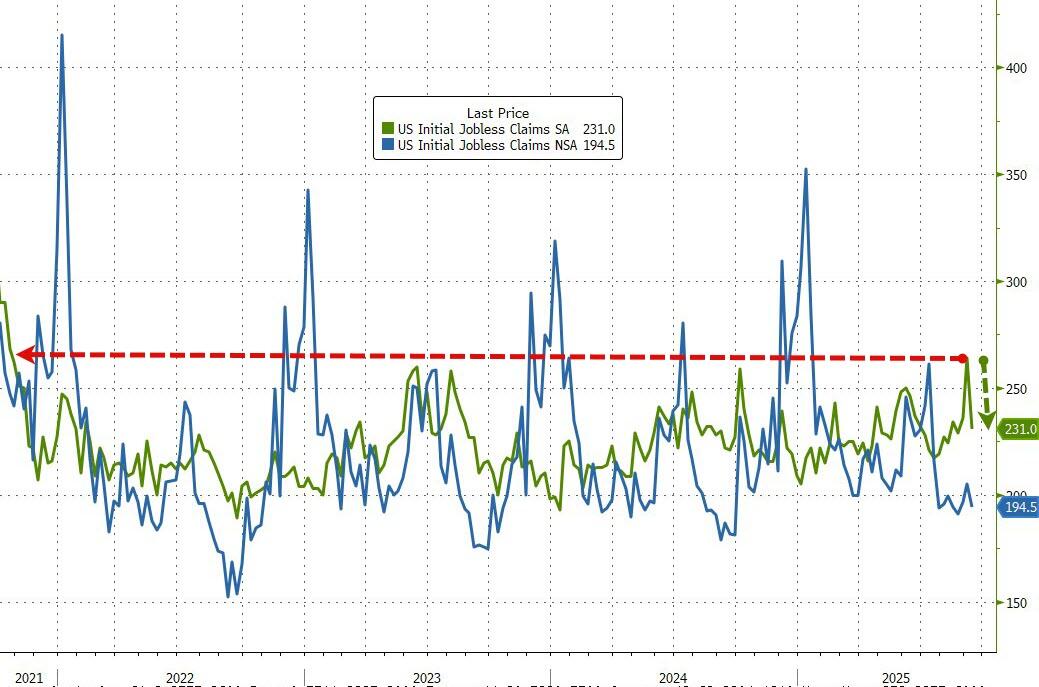

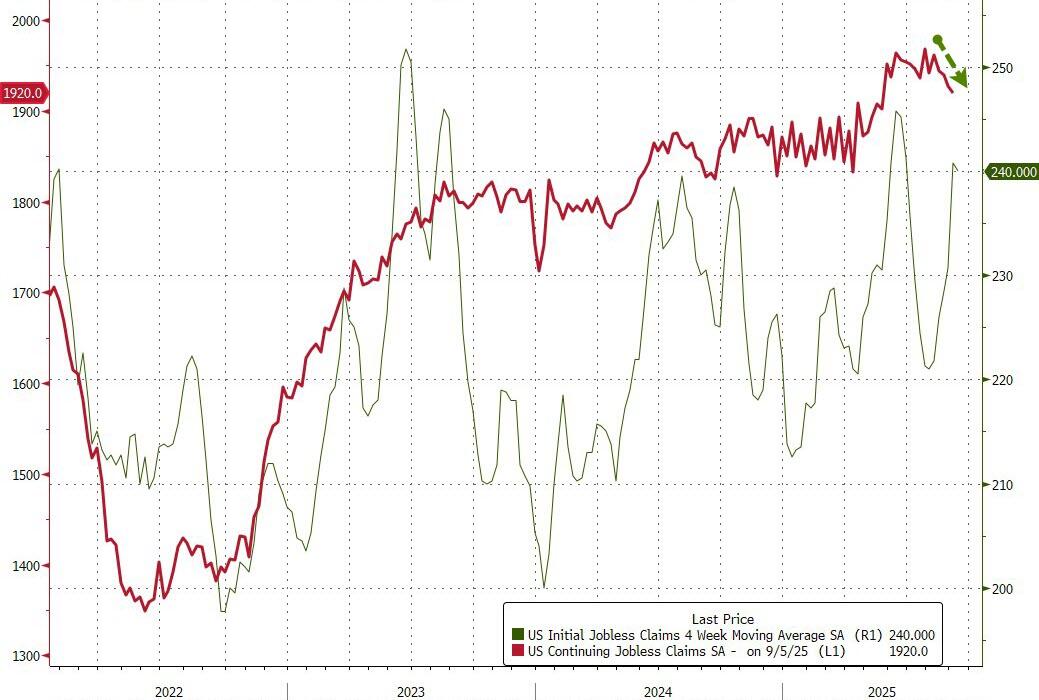

US economic data slate includes weekly jobless claims and September Philadelphia Fed business outlook (8:30am), August Leading index (10am) and July TIC flows (4pm)

Market Snapshot

S&P 500 mini +0.9%

Nasdaq 100 mini +1.1%

Russell 2000 mini +1.5%

Stoxx Europe 600 +0.8%

DAX +1.3%

CAC 40 +1.2%

10-year Treasury yield -4 basis points at 4.05%

VIX -0.9 points at 14.83

Bloomberg Dollar Index little changed at 1191.67

euro +0.1% at $1.183

WTI crude -0.3% at $63.88/barrel

Top Overnight News

US government shutdown risks are rising, with Democrats demanding health care policy changes that House Speaker Mike Johnson has said have “zero” chance of becoming law. The US House cleared the procedural hurdle for a floor vote this week on the stopgap funding measure to avert a government shutdown. BBG

Punchbowl, on the possibility of a US shutdown, surmises “Republican and Democratic leaders are growing further apart rather than closer.”

Donald Trump’s UK visit turns to diplomatic talks with PM Keir Starmer, which are expected to focus on trade and the war in Ukraine. There will be a joint press conference, at which some tech investments may be announced. BBG

The Trump administration is drawing up plans to use tariff revenue to fund a program to support US farmers as they head into harvest facing falling export sales and rising input costs. FT

China is dropping an antitrust probe into Google, as Beijing and Washington step up negotiations over TikTok, Nvidia and trade at a time of heightened tensions between the superpowers. FT

China rare earth exports jumped to a record level in Aug as Beijing permits expanded shipments following an easing of tensions with Washington. BBG

Huawei outlined its long-term chip plans for the first time on Thursday and said it would launch some of the world’s most powerful computing systems – underscoring China’s drive to wean itself off foreign semiconductor suppliers like Nvidia. RTRS

Norway’s central bank lowered rates by 25bp to 4%, as expected, and while it forecast additional cuts over the coming year, it also noted that “a somewhat higher policy rate will likely be needed ahead compared with the outlook in June. Norges Bank

Germany will borrow about a fifth more than planned in the fourth quarter to help fund a surge in spending on infrastructure and the armed forces. They aim to raise €90.5 billion ($107 billion) in the October-December period, excluding green bonds, according to an updated plan published Thursday. That’s €15 billion more than December’s original program and follows an increase of €19 billion in the third quarter. BBG

The BOE will probably announce a slowing of gilt sales at its decision today amid concern about worsening bond market volatility. No rate change is expected. BBG

Trade/Tariffs

China is reportedly dropping the Google (GOOG) antitrust probe during US trade talks, according to FT.

US House China Panel Chair said he’s concerned regarding the TikTok deal.

Brazilian President Lula said he has no relationship with US President Trump, while he described US tariffs as ’eminently political’ and said US consumers would be facing higher prices for Brazilian goods as a result, according to a BBC interview. It was also reported that Lula signed an executive order that exempts some data centre equipment from federal taxes.