SEPT 23/GOLD CLOSED UP ANOTHER $42.10 TODAY TO $3782.50 WHILE SILVER WAS UP 32 CENTS TO $44.30//PLATINUM CONTINUES ON A TEAR UP ANOTHER $70.90 TO $1491.50 WITH PALLADIUM UP $33.60 TO $1223.50//CHINA CONTINUES ITS PRESSURE IN DISPUTED WATERS//ITALY’ MILAN WITNESSES MASSIVE PROTESTS BY ANTIFA AND PALESTINIAN DISSIDENTS//ISRAEL VS HAMAS UPDATES:; LAST 24 HRS PODCAST TBN ISRAEL//HEALTH ISSUES //DR PAUL ALEXANDER/NEWS ADDICTS NEWSWIZE/EVOL NEWS/TRUMP GOING AFTER ANTIFA//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 281 363 H WELLS FARGO SECURITI 72 661 C JP MORGAN SECURITIES 3 686 C STONEX FINANCIAL INC 5 35 732 C RBC CAP MARKETS 98 737 C ADVANTAGE FUTURES 1 880 C CITIGROUP 37 905 C ADM 40

TOTAL: 286 286 MONTH TO DATE: 6,414

JPMORGAN STOPPED 0/22

SEPT

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 286 CONTRACTs NOTICES FOR 28600 OZ or 0.0684 TONNES

total notices so far: 6414 contracts for 641.400 OR 19.950 tonnes)

FOR SEPT

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 22 NOTICE(S) FILED FOR 0.110 MILLION OZ/

total number of notices filed so far this month : 13,250 CONTRACTS (NOTICES) for 66.250 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $42.10 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MAMMOTH 6.11 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD//

INVENTORY RESTS AT 1000.67 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.32 AT THE SLV:

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:/ // A MASSIVE 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 494.121 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA MEGA HUMONGOUS SIZED 3946 CONTRACTS TO 167,003 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS MEGA HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR MAMMOTH GAIN OF $1.16 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE FINALLY ARE MOVING TO A MUCH HIGHER BASE SURPASSING THE $34.40 SILVER PRICE BARRIER TO A HIGH DEGREE, CLOSING IN ON THE MAGIC ALL TIME HIGH OF $50.00. WE HAD A MEGA MEGA HUMONGOUS SIZED GAIN OF 4346 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A GOOD SIZED 400 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO MONDAY’S TRADING AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $42.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON MONDAY WITH SILVER’S HUGE GAIN IN PRICE. THE PRICE FINISHED MILES ABOVE THE MAGIC NUMBER OF $40.00 SILVER SPOT PRICE CLOSING AT $43.98 GAINING $1.16 . WE FINALLY STOPPED HAVING THOSE MEGA MEGA HUGE T.A.S. ISSUANCE BUT STILL WITNESSING SOMETIMES LARGE ISSUANCE: HOWEVER TODAY’S TOTAL ISSUANCE WAS RECORDED AT A GOOD SIZED 400 CONTRACTS. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 40.00 DOLLAR MARK!!. THE NEXT LINE IN THE SAND IS THE ORIGINAL HIGH POINT OF 50.00 DOLLAR SILVER. WE HAD A GOOD SIZED 400 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUMONGOUS SIZED 1062 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING / AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUMONGOUS SIZED 4346 CONTRACTS ON OUR TWO EXCHANGES WITH OUR MAMMOTH GAIN IN PRICE OF $1.16.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A HUMONGOUS SIZED 1062 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.16) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A MEGA MEGA HUMONGOUS SIZED GAIN OF 4346 CONTRACTS ON OUR TWO EXCHANGES,

WE HAD A 400 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 49.825 MILLION OZ COUPLED WITH TODAY’S 0.210 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON TO WHICH WE ADD OUR INITIAL 3.0 MILLION OZ OF EXCHANGE FOR RISK SEPT. ISSUANCE//NEW STANDING REDUCES TO TO 70.985 MILLION OZ///

THUS:

INITIAL STANDING FOR SEPT: 70.985 MILLION OZ

WE HAD:

/ MEGA HUGE COMEX OI GAIN+// A GOOD SIZED EFP ISSUANCE 400 CONTRACTS (/ VI) A HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE 1062 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: 242 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT.. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 15 DAY(S), total 7300 contracts: OR 36.500 MILLION OZ (486 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 36.500 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 36.500 MILLION OZ.(QUITE SMALL)

RESULT: WE HAD A MEGA MEGA HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4488 CONTRACTS WITH OUR GAIN IN PRICE OF $1.16 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A GOOD SIZED 400 CONTRACT EFP ISSUANCE CONTRACTS: 400 ISSUED FOR DEC., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 6 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 67.985 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 70.985 MILLION OZ. THIS IS THE FIRST ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.

THE NEW TAS ISSUANCE MONDAY NIGHT (1062) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!!

WE HAD 22 NOTICE(S) FILED TODAY FOR 0.110 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON COMPLETE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG SIZED 8151 OI CONTRACTS TO 530,457 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A RELATIVELY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A huge 1405 CONTRACTS //.(ALL GOVERNMENT)

WE HAD AN INCREASE IN COMEX OI (8151 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $68.40 IN PRICE// MONDAY///.

LAST 5 MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.8834 TONNES PLUS 0.000 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 20.096//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 40.385 TONNES!!

E.F.P. ISSUANCE/FOR OPENING SEPT GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1050 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 531,862 / GETTING MUCH HIGHER AND WE NOW WITNESS A STRONG COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A FAIR SIZED COMEX OI OF 167,245 CONTRACTS

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8572 CONTRACTS WITH 8151 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 440 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8592 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 2068 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON LIKE ON THURSDAY. GOLD PRICE ON MONDAY ROSE BY $68.40

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(440) ACCOMPANYING THE VERY STRONG SIZED INCREASE IN COMEX OI OF 8151 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 8592 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR SEPT AT 8.093 TONNES PLUS 0.8834 TONNES QUEUE JUMP PLUS 0.000 TONNES EXCHANGE FOR RISK TODAY AND FOR THE MONTH 20.096 TONNES//NEW STANDING ADVANCES TO = 40.385 TONNES.@!!!

NEW STANDING FOR GOLD, SEPT CONTRACT AT 40.384 TONNES OF GOLD

.

/ 3) ZERO T.A.S. LIQUIDATION AS WE HAD 1)A $68.40 COMEX PRICE GAIN. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG SIZED GAIN OF 8,592 CONTRACTS ON OUR TWO EXCHANGES /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND YOU CAN VISUALIZE THIS BY THE HUGE AMOUNTS OF QUEUE JUMPING WE HAVE BEEN HAVING LATELY (TODAY = 0.8834 TONNES)

4) VERY STRONG SIZED COMEX OI GAIN// 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (440 CONTRACTS)/// STRONG T.A.S. ISSUANCE: 2068 T.A.S.CONTRACTS/

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

TOTAL EFP CONTRACTS ISSUED: 27,135 CONTRACTS OR 2,713,500 OZ OR 84.401 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 1809 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN15 TRADING DAY(S) IN TONNES: 84.401 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 84.401 TONNES DIVIDED BY 3550 x 100% TONNES = 2.37% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

UNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 84.401 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA MEGA HUMONGOUS SIZED 3946 CONTRACTS OI TO 167,003 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 400 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 400 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 640 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3946 CONTRACTS AND ADD TO THE 400 E.FP. ISSUED

WE OBTAIN A MEGA MEGA HUMONGOUS SIZED GAIN OF 4346 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR MAMMOTH GAIN IN PRICE OF $1.16 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 21.73 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 6.74 PTS OR 0.18%

//Hang Seng CLOSED DOWN 185.02 PTS OR 0.70%

// Nikkei CLOSED : HOLIDAY //Australia’s all ordinaries CLOSED UP .39%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1048 OFFSHORE CLOSED UIP AT 7.1126/ Oil UP TO 62.49 dollars per barrel for WTI and BRENT UP TO 66.77 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1048 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1261 AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY STRONG SIZED 8151 CONTRACTS TO 530,457 OI WITH OUR HUGE GAIN IN PRICE OF $68.40 WITH RESPECT TO MONDAY’S // TRADING COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT HUGE PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (400). WE HAD ZERO T.A.S. LIQUIDATION AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 8592 CONTRACTS (OR 26.72 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD 0 CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 3 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 3 MONTHS 68.542 TONNES//BANK OF ENGLAND TOTAL RESERVES 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

AND NOW:

SEPT:

SEPTEMBER: SIX ISSUANCES SO FAR TOTALLING 6,461 CONTRACTS OR 646,100 OZ OR 20.096 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SIX ISSUANCES FOR 6461 CONTRACTS SO FAR FOR 646,100 OZ OR 20.096 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 113 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH SEPT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 113 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN DECEMBER 2024.

DETAILS ON SEPTEMBER COMEX MONTH//

IN TOTAL WE HAD A VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 8592 CONTRACTS WITH OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A STRONG T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 2068 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN DURING LAST NIGHT WITH MUCH FAILURE!!

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH PREVIOUS AUGUST MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.8834 TONNES QUEUE JUMP TO GO ALONG WITH THE 0.000. TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 20.096 TONNES//NEW TOTALS STANDING ADVANCES TO 40.385 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 241 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

AND NOW SEPTEMBER:

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.8834 TONNES QUEUE JUMP AND 0.0000 TONNES EXCHANGE FOR RISK TODAY// NEW TOTALS OF 20.096 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH:

THAT IS;

A) 0.0000 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY // =//TOTAL FOR MONTH EX FOPR RISK: 20.096 TONNES EX FOR RISK!!

B) 0.8834 TONNES TODAY QUEUE JUMP

TOTALS: 40.385 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2068 EFP CONTRACT WAS ISSUED: : /DEC 2068 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2068 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY AND THUS NO EFFECT ON OUR TOTAL OPEN INTEREST!!

MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE.

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A STRONG SIZED SIZED 2068 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

3) TO BE FOLLOWED BY SEPTEMBER’S 6 ISSUANCES FOR EXCHANGE FOR RISK FOR 20.096 TONNES.

GOLD STANDING AT THE COMEX FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

AND NOW SEPT:

SEPT: 20.389 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) +0.0000 TONNES EX FOR RISK TODAY//

TOTAL EX FOR RISK// FOR MONTH = 20.096//NEW TOTALS FOR GOLD STANDING SEPT = 40.385 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A STRONG $68.40./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A HUGE SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY. MUCH OF THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO SPECULATIVE LONGS PILING INTO COMEX GOLD TRADING /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS NOW IN ORDER TO FORMALIZE RAIDS, LET US SEE IF OUR CROOKS AGAIN FAIL ON OPTIONS EXPIRY WEEK THIS WEEK, LIKE THEY DID IN AUGUST.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 26.72 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 0.8834 TONNES OF GOLD ALONG WITH 0.0000 TOTAL TONNES OF EXCHANGE FOR RISK TODAY/// TOTAL FOR MONTH TOTALS EX FOR RISK// MONTH = 20.096//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 40.385 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED WITH OUR HUGE GAIN IN PRICE TO THE TUNE OF $68.40

WE HAD A MAMMOTH 11,968 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 8592 CONTRACTS OR 859200 0Z (26.72 TONNES)

i) 31,057.866 OZ ( HSBC) 966 kilobars ii) Into: Malca; 32,151.000 oz (1000 kilobars)

total deposit 63,205.866 oz 1966 kilobars

1.966 tonnes

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

286 notice(s) 28600 OZ 0.7962 TONNES

No of oz to be served (notices)

109 contracts 10900 OZ 0.3390 TONNES

Total monthly oz gold served (contracts) so far this month

6414 notices 6414,000 oz 19.950 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER 4

DEPOSITS/CUSTOMER

2 ENTRIES

i) 31,057.866 OZ ( HSBC) 966 kilobars ii) Into: Malca; 32,151.000 oz (1000 kilobars)

total deposit 63,205.866 oz 1966 kilobars

1.966 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entries

i) Out of Brinks 803.775 oz

total withdrawal 803.775 oz

ADJUSTMENTs 1

a) customer to dealer Manfra: 27,441.714 oz

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 395 CONTRACTS FOR A GAIN OF 262 CONTRACTS. WE HAD 22 CONTRACTS FILED ON MONDAY SO WE GAINED 284 CONTRACTS OR 25,400 OZ ENTERTAINED A QUEUE JUMP OF 0.8834 TONNES. WE NOW MUST ADD TO OUR INITIAL 8.093 TONNES OF GOLD STANDING TO TODAY’S QUEUE JUMP OF 0.8834 TONNES AND THEN ADD MONTH SEPT// EX FOR RISK = 20.096//(WHICH INCLUDES TODAY’S 0.000 TONNES EX. FOR RISK) THUS NEW TOTAL OF GOLD STANDING ADVANCES TO 40.385 TONNES

OCTOBER LOST 2697 CONTRACTS DOWN TO 54,241

NOVEMBER GAINED 324 CONTRACTS UP TO 4088 CONTRACTS.

We had 286 contracts filed for today representing 28,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 286 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 3 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (6414 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 395 CONTRACTS) minus the number of notices served upon today (286 x 100 oz per contract) equals 652,300 OZ OR 20.289 TONNES OF GOLD TO WHICH WE ADD OUR TOTAL EX FOR RISK/SEPT MONTH OF 20.096 TONNES//NEW TOTAL STANDING ADVANCES TO 40.385 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (6414 x 100 oz +we add the difference for front month of SEPT. (395 OI} minus the number of notices served upon today (286 x 100 oz) which equals 652,300 OZ OR 20.289 TONNES PLUS 20.096 TONNES EXCHANGE FOR RISK = 40.385 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 40.385 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,017,117.237 oz 62.740 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,745,191/275 oz

TOTAL REGISTERED GOLD 21,539,073.009 or 669.95 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,206,118.266 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,521959oz ((REG GOLD- PLEDGED GOLD)= 607/21 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 23 2025

INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

0

Deposits to the Dealer Inventory

0 ENTRY

Deposits to the Customer Inventory

2 entries

i) Into Asahi 1,769.766.490 oz ii) Into CNT 610,220.280 oz

total deposit 2,369,986.870 oz

No of oz served today (contracts)

22 CONTRACT(S) (0.110 million OZ

No of oz to be served (notices)

347 contracts (1.735 MILLION oz)

Total monthly oz silver served (contracts)

13,250 Contracts (66.250 million oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 entries

i) Into Asahi 1,769.766.490 oz ii) Into CNT 610,220.280 oz

TOTAL REGISTERED SILVER: 193.349 MILLION OZ//.TOTAL REG + ELIGIBLE. 526/745 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPT.

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 369 OPEN INTEREST CONTRACTS FOR A LOSS OF 82 CONTRACTS. WE HAD 40 CONTRACTS SERVED ON MONDAY SO WE LOST A CONSIDERABLE SIZED 42 CONTRACTS OR 0.210 MILLION OZ ENTERTAINED AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON TO TAKE DELIVERY OVER ON THAT SIDE OF THE POND..//NEW STANDING FOR SILVER COMEX DECREASES TO 67.985 MILLION OZ. THEN WE MUST ADD OUR INITIAL ISSUANCE OF 600 CONTRACTS FOR EXCHANGE FOR RISK OR 3.0 MILLION OZ//NEW STANDING REDUCES TO 70.985 MILLION OZ

STANDING FOR SILVER: 70.985 MILLION OZ

OCTOBER GAINED 35 CONTRACTS TO 3000

NOVEMBER GAINED 111 CONTRACTS UP TO 2043.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 22 or 0.110 MILLION oz

CONFIRMED volume; ON MONDAY 84.925 huge//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 13,250 X5,000 oz = 66.250 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (369) AND the number of notices served upon today (22 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (13,250) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(369) minus number of notices served upon today (22)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 67.985 MILLION OZ TO WHICH WE ADD OUR INITIAL EXCHANGE FOR RISK SEPT TOTALLING 3.0 MILLION OZ//NEW STANDING REDUCES TO 70.985 MILLION OZ

New total standing: 70.985 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 193/349 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/526.745 million. 39.90%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

GLD INVENTORY: 1000.67 TONNES, TONIGHTS TOTAL

SILVER

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

CLOSING INVENTORY 494.121 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

JAMES RICKARDS

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 241

5. COMMODITY REPORT URANIUM

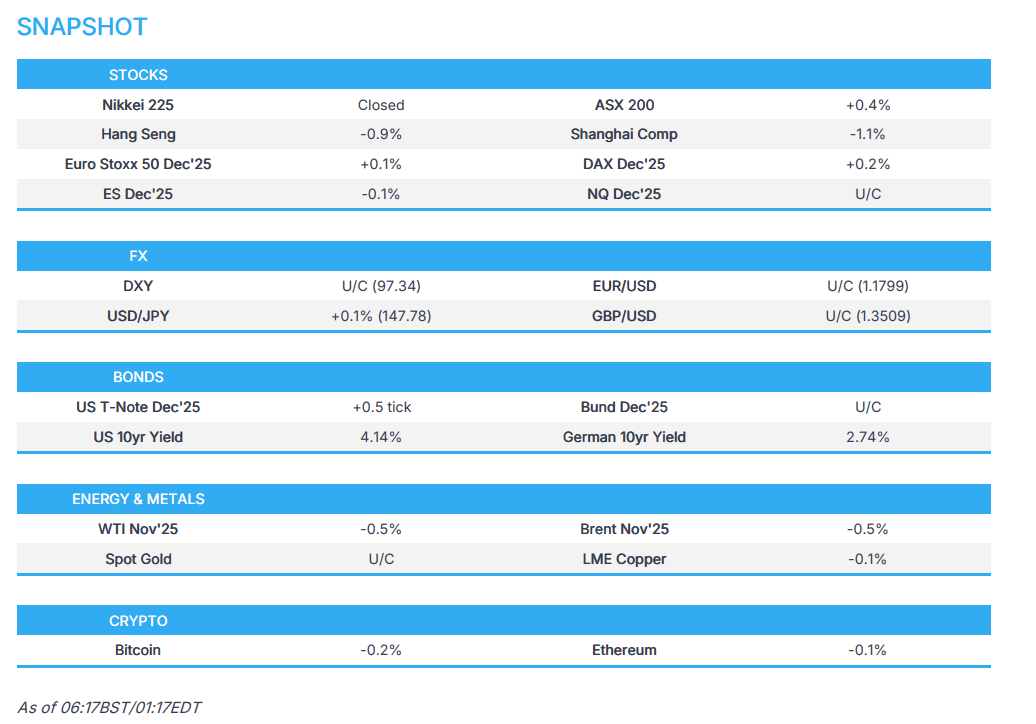

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 6.74 PTS OR 0.18%

//Hang Seng CLOSED DOWN 185.02 PTS OR 0.70%

// Nikkei CLOSED : HOLIDAY //Australia’s all ordinaries CLOSED UP .39%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1048 OFFSHORE CLOSED UIP AT 7.1126/ Oil UP TO 62.49 dollars per barrel for WTI and BRENT UP TO 66.77 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1048 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1261 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1048

OFFSHORE YUAN: UP TO 7.1126

HANG SENG CLOSED DOWN 185.02 PTS OR 0.70%

2. Nikkei closed

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 96.89 EURO RISES TO 1.1809 UP 9 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.659//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.53…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.174 DOWN 1/ 2 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7448 Italian 10 Yr bond yield UP to 3.567 SPAIN 10 YR BOND YIELD UP TO 3.208

3i Greek 10 year bond yield UP TO 3.428

3j Gold at $3782.80 Silver at: 44.19 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 31 /100 roubles/dollar; ROUBLE AT 83.31

3m oil (WTI) into the 62 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.53/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.659% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.174 DOWN 1/2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7917 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9345 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.134 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.752 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3..592 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.42

10 YR UK BOND YIELD: 4.6910 DOWN 3 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.520 DOWN 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.200 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.739 DOWN 0 BASIS PTS.

2a New York OPENING REPORT

Market Rally Pauses Ahead Of Powell Speech While Gold Propels To New Record Highs

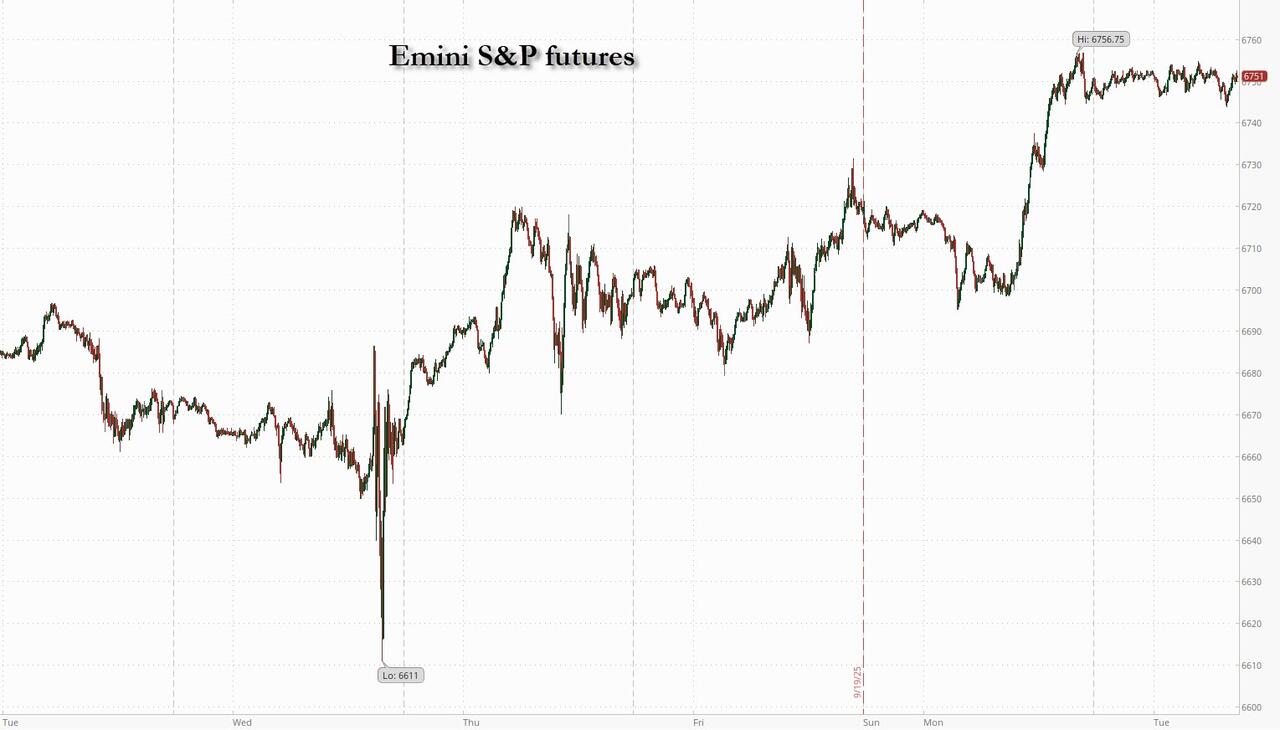

Tuesday, Sep 23, 2025 – 08:33 AM

US equity futures are flat after Monday’s latest dose of AI excitement (where nobody seems to know where the funds will come from, but then again nobody seems to care) drove indexes to fresh highs. S&P futures are unchnaged, with Nasdaq 100 futures fractionally in the red, with Mag7 names mixed in premarket trading as Semis have a slight bid. BA is +2.3% on a potential order stemming from the US/China trade talks. There’s a lot going on – from a looming government shutdown to surging Chinese exports – but no clear way to play it. Bond yields 1-2bps lower as the yield curve shifts lower; USD is flat. Cmdtys are mixed with crude and precious leading; gold +90bp as China moves to custody gold similar to NY Fed. OECD hikes global growth estimate for FY25 from 2.9% to 3.2% with US growth est. moving from 1.6% to 1.8% and 1.5% for FY26. OECD also predicts that the full impacts from tariffs have yet to be felt. The macro data focus is on Flash PMIs and regional Fed activity measures. Today’s main event is Fed Chair Powell’s economic outlook.

In premarket trading, Mag 7 stocks are mostly higher (Tesla +1%, Meta +0.3%, Amazon +0.2%, Alphabet +0.2%, Microsoft +0.03%, Apple -0.4%, Nvidia -1%).

ACM Research (ACMR) gains 5% as the stock is to replace WK Kellogg Co. in the S&P SmallCap 600 prior to the opening of trading on Sept. 26.

AutoZone (AZO) slips 2% after posting fourth-quarter results.

Boeing (BA) is up 2% after Uzbekistan Airways announced an order for as many as 22 of the US planemaker’s 787 Dreamliner jets, while US Ambassador to China David Perdue said the US and China are weeks away from finalizing negotiations on a “huge” Boeing order.

CoreWeave Inc. (CRWV) climbs 2% after Melius Research upgraded the cloud-computing provider to buy, saying the firm is one of the beneficiaries “of accelerating cloud demand both right now and well into the future.”

Firefly Aerospace (FLY) falls 10% after the space and defense technology company reported revenue for the second quarter that missed the average analyst estimate.

Kenvue (KVUE) gains 4% as President Donald Trump’s call for pregnant women to avoid Tylenol draws sharp criticism from researchers who say the advice ignores decades of evidence and could endanger mothers and babies.

Vistra Corp. (VST) slips 2% after the power producer was downgraded at Jefferies, which voiced concerns about the lack of announcement for a data-center deal for its Comanche Peak nuclear-power plant.

In corporate news, Disney said Jimmy Kimmel Live! will return to the air on Tuesday following a backlash. Nvidia assured customers that its landmark deal with OpenAI won’t affect the chipmaker’s relationship with other clients. Zijin Gold International Co., which is currently taking orders to raise $3.2 billion in the world’s biggest initial public offering in months, may have to delay its trading debut in Hong Kong next week because of super typhoon Ragasa. China Vanke Co. is in talks with major domestic creditors to cut borrowing costs on private debt worth tens of billions of yuan, as the embattled developer seeks to ease liquidity stress, according to people familiar with the matter.

US stock futures wavered early on, repeating a pattern of the past two sessions that gave way to extended rallies. There was no pause for Gold however: the yellow metal’s unprecedented rally pushed higher on efforts by China to bolster its role in global bullion markets. Bullion powered beyond $3,780 an ounce, putting the metal on track for its best month since 2020. The rally gained fresh momentum on Tuesday after Bloomberg reported that the People’s Bank of China is looking to be a custodian of sovereign reserves, courting friendly countries to buy bullion and store it within its borders.

Investors are rushing to gold as the prospect of rapid US interest rate cuts enhances the appeal of non-interest-bearing assets. The metal is also drawing haven demand amid geopolitical upheaval and pressure on the Federal Reserve from the Trump administration to lower rates, stocking fears about inflation.

Traders are awaiting fresh Fed signals ahead of a speech by Chair Jerome Powell on Tuesday as earnings season looms as the next big test for stocks. Coming up as well is the first of three shorter-term debt auctions, beginning with a $69 billion sale of two-year notes.

“The cross-asset landscape is defined by the duality of tech-driven sentiment, embodied by Nvidia’s outsized role in AI, and policy scrutiny over Fed independence,” wrote Pepperstone research strategist Ahmad Assiri. “Equities continue to enjoy a positive tilt, the dollar struggles to find upside traction while gold has cemented itself as the market’s most compelling anchor.”

US stocks are holding gains from a $15 trillion rally since April’s lows, shaking off trade tensions and concerns about stretched valuations as traders bet a dovish Fed will fuel earnings amid excitement over artificial intelligence. The view was reinforced Monday as Nvidia pledged to invest as much as $100 billion in OpenAI, although this has sparked questions about the circular nature of funding in AI and making many wonder where the money will come from:

While AI companies have been quick to unveil plans for spending, they’ve been slower to show how they will pull in revenue to cover those expenses. Consulting firm Bain & Co. predicted that firms will need to find a combined $2 trillion to fund computing power by 2030, but their revenue is likely to fall $800 billion short of that.

“With the Fed turning dovish, the risk is that if you’re on the sidelines and the market moves away from you, you’ll never be able to catch up,” said Patrick Brenner, chief investment officer of multi-asset at Schroders Plc. “We have some exposure but we’re not completely risk-on. If we see a dip, we are ready to buy more.”

Europe’s Stoxx 600 rose 0.5% after data showed the euro area’s private sector expanded at the fastest pace in 16 months. Nearly all European sectors in the green, lifted by utilities and European wind energy companies, after a US judge ruled Denmark’s Orsted could resume work on its nearly-completed wind farm. The retail sector is the best performer, lifted by Kingfisher, which rose as much as 20% after the home-improvement group raised its full-year guidance. The biggest laggards are healthcare and insurance equities. Here are the biggest movers Tuesday:

Kingfisher shares rise as much as 20%, the most since September 2008, after first-half earnings surpassed analysts’ estimates and the home-improvement retailer raised its full-year guidance to the upper end of the expected range

Orsted shares gain as much as 12% after a US judge ruled that the Danish wind-farm developer can resume work on its nearly-completed wind farm off the coast of Rhode Island during a lawsuit challenging the Trump administration’s stop-work order

Heineken shares climb as much as 2.4%, the most in more than a month, after the brewer said it will buy Florida Ice and Farm Company’s beverage and retail businesses in a $3.2 billion cash deal

Smiths shares rise to the highest level on record, climbing as much as 7.2%, after reporting group operating profit for the full year that beat the average analyst estimate

Hoist Finance shares rise as much as 11%, the most since July, after Kepler Cheuvreux upgraded the stock to buy from hold, saying that an expected change in the Swedish debt restructuring firm’s status should allow for payouts to shareholders

Land Securities rises as much as 4.4%, the most since April, after the commercial real estate firm said it remains on track to deliver its growth guidance this year ahead of its capital markets day

THG shares rise as much as 8.5% to the highest since February after JP Morgan upgraded its rating on the the online retailer to neutral from underweight

ASM International shares fall as much as 6.4% after the Dutch chip equipment maker reduced its outlook for second half of the year, citing lower-than-expected demand among both leading-edge logic and mature chip markets

Hanza falls as much as 12%, the most since February, after Pareto Securities cut its recommendation on the Swedish contract manufacturer to hold from buy, saying it’s time to move to the sidelines after shares climbed over 100% in the past 12 months

Raspberry Pi shares fall as much as 8.4% after the British PC maker reported a 6% drop in first-half sales, against a high comparison basis last year due to the launch of Pi 5

Earlier in the session, Asian stocks struggled for direction as a rally in semiconductor companies was offset by losses in China and Hong Kong. The MSCI Asia Pacific Index excluding Japan was little changed, after earlier rising 0.4%. Chipmakers TSMC and Samsung Electronics provided the biggest boost following Nvidia’s announcement of as much as $100 billion investment in OpenAI to build data centers. Japanese markets were closed for a holiday. Equity benchmarks in Hong Kong and mainland China fell more than 1% as a months-long rally took a breather. Baidu’s shares slumped most since April after a 50% jump in the stock price this month. Asian stocks have had a stellar run this year as a weaker US dollar and cheaper valuations drove investors away from American assets. The region’s equities are on track to outperform US peers by the most since 2017.

In FX, the pound falls after UK PMIs miss expectations across the board. Swedish krona tops G-10 currencies after surprise cut but a hawkish outlook from the Riksbank.

In rates, Treasuries see small rally across the curve with yields lower by 1bp to 2bp on the day. UK Gilts outperform in fixed income, with 10-year yields falling about three basis points following lower-than-expected UK PMI data for September. At the same time, the UK’s 30-year bond sale got the fewest orders since 2022. The rally in gilts supports gains in Treasuries after the UK curve bull flattened. US session focus includes manufacturing PMIs and 2-year note auction. Fed Chair Powell is scheduled to speak on the economic outlook at 12:35pm New York.

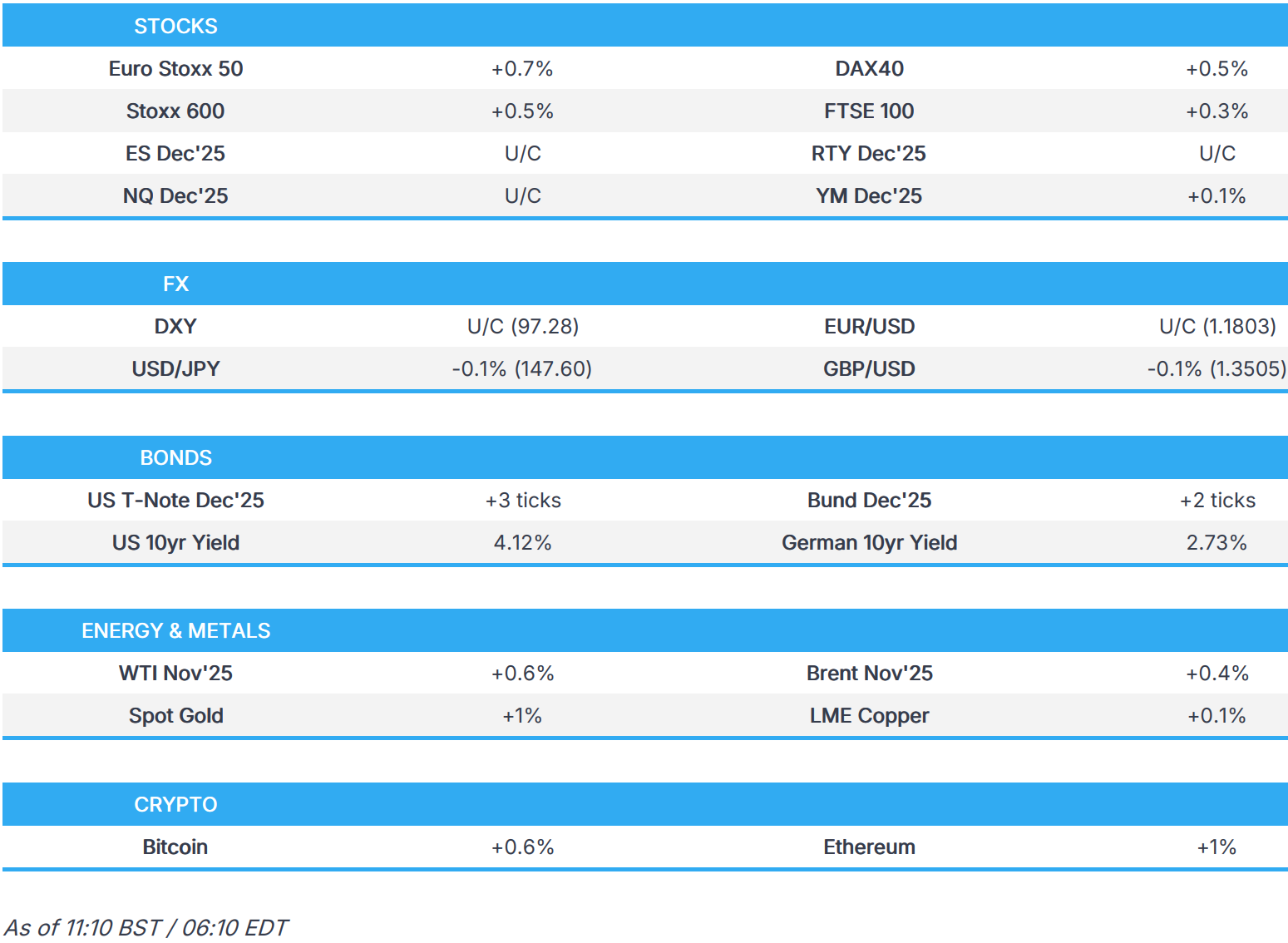

In commodities, WTI futures push higher into early US session and trade over 1% up on the day, capping additional gains in Treasuries. Brent trades above $67/barrel. Gold blows past more records, up about $42 for the session to $3,789/oz.

Today’s US economic data slate includes September Philly Fed non-manufacturing, 2Q current account balance (8:30am), September manufacturing PMI (9:45am) and Richmond Fed manufacturing (10am). Fed speaker slate includes Goolsbee (8:30am, 3:30pm), Bowman (9am), Bostic (10am) and Powell (12:35pm)

Market Snapshot

S&P 500 mini little changed

Nasdaq 100 mini little changed

Russell 2000 mini little changed

Stoxx Europe 600 +0.5%

DAX +0.7%

CAC 40 +0.9%

10-year Treasury yield -2 basis points at 4.13%

VIX little changed at 16.07

Bloomberg Dollar Index little changed at 1195.71

euro little changed at $1.1809

WTI crude +0.5% at $62.57/barrel

Top Overnight News

President Trump to speak at 09:50 ET /14:50 BST at the UN General Assembly

Ukrainian President Volodymyr Zelenskiy will seek more support from allies when he addresses the UN and meets Donald Trump this week, but behind the scenes Kyiv is quietly preparing for a new phase of the war in which it relies more on itself and its hopes of winning tough new US sanctions on Russia are fading. RTRS

US President Trump said the FDA will warn physicians about a potential link between acetaminophen (Tylenol) use in pregnancy and autism risk; he advised pregnant women to avoid Tylenol and said do not take it. Trump also said MMR vaccines should be taken separately and that there is no reason for newborns to be given the Hepatitis B vaccine, according to Reuters.

Trump will meet this week with House Minority Leader Hakeem Jeffries and Senate Minority Leader Chuck Schumer to discuss government funding ahead of a looming shutdown deadline. Politico

AI companies face an $800 billion revenue shortfall by 2030, Bain warned, threatening their ability to fund computing power needed to meet demand. BBG

Jamie Dimon, on Fed rate cuts, said further reductions will be difficult: CNBC

The OECD warned that the world economy has yet to feel the full impact of Donald Trump’s tariffs, despite recent resilience. It raised its forecast for world growth to 3.2% this year, but expects it to moderate to 2.9% in 2026 amid higher import duties. BBG

Senior Chinese trade negotiator Li Chenggang met political and business leaders from the U.S. Midwest, the commerce ministry said on Tuesday, with analysts speculating the region’s food exports will be key to any U.S.-China trade deal. U.S.-China commercial ties had featured in Monday’s talks, the ministry said in a statement, without giving details. RTRS

China is pushing to become custodian of foreign sovereign gold reserves, people familiar said. The PBOC is using the Shanghai Gold Exchange to court central banks in friendly countries to buy bullion and store it within the country’s borders. BBG

The euro-area private sector expanded at the quickest pace in 16 months, driven by strong German services offsetting a slump in France. The PMI rose to 51.2, beating expectations. UK PMIs missed across the board. BBG

Sweden’s Riksbank eased interest rates to 1.75% and signaled a pause ahead, aiming to support economic recovery. No further easing is expected through 2028. BBG

ASM International shares fell after cutting its second-half revenue outlook, citing weaker demand from some its clients. BBG

Trade/Tariffs

JPMorgan (JPM) CEO Dimon noted tariffs could be modestly inflationary but uncertain if the impact is temporary, via Times of India interview.

US lawmaker Smith noted the intention to improve communication channels between China and the US.

A more detailed look at global markets courtesy of Newquawk