WE HAVE NOW ENTERED OPTION EXPIRY MONTH:

COMEX OPTION EXPIRY TOMORROW SEPT 25 AND SEPT 30 IS LBMA LONDON EXPIRY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

TODAY’S REPORT IS SMALL AS I WAS OUT FOR MOST OF THE DAY

BUT ALL THE DATA IS COMPLETE!!

323 C HSBC 160

363 H WELLS FARGO SECURITI 29

624 H BOFA SECURITIES 40

686 C STONEX FINANCIAL INC 33 16

726 C PLUS500US FINANCIAL 1

732 C RBC CAP MARKETS 72

737 C ADVANTAGE FUTURES 1 2

880 C CITIGROUP 18

905 C ADM 1 19

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 196 CONTRACTs NOTICES FOR 19,600 OZ or 0.6096 TONNES

total notices so far: 6610 contracts for 661,000 OR 20.559 tonnes)

SILVER NOTICES: 190 NOTICE(S) FILED FOR 0.950 MILLION OZ/

total number of notices filed so far this month : 13,440 CONTRACTS (NOTICES) for 67.200 million oz

INVENTORY RESTS AT 1000.67 TONNES

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 37.500 MILLION OZ.(QUITE SMALL)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.005 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.005 MILLION OZ. THIS IS THE FIRST ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.8834 TONNES PLUS 0.000 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 20.096//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 41.514 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 90.678 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1198 CONTRACTS OI TO 165,805 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 200 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 640 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3946 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 1618 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE OF $0.32 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.99 MILLION PAPER OZ

OCCURRED DESPITE OUR GAIN $0,32 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

//Hang Seng CLOSED UP 359.53 PTS OR 1.37%

// Nikkei CLOSED : UP 136.65 PTS OR .30 //Australia’s all ordinaries CLOSED DOWN 0.88%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1216 OFFSHORE CLOSED DOWN AT 7.1274/ Oil UP TO 63.51 dollars per barrel for WTI and BRENT UP TO 67.66 Stocks in Europe OPENED ALL RED

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1618 CONTRACTS TO 528,789 OI DESPITE OUR HUGE GAIN IN PRICE OF $42.10 WITH RESPECT TO TUESDAY’S // TRADING COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT HUGE PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2018). WE HAD ZERO T.A.S. LIQUIDATION AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 350 CONTRACTS (OR 7.22 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD 0 CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 3 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 3 MONTHS 68.542 TONNES//BANK OF ENGLAND TOTAL RESERVES 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

AND NOW:

SEPT:

SEPTEMBER: SIX ISSUANCES SO FAR TOTALLING 6,461 CONTRACTS OR 646,100 OZ OR 20.096 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SIX ISSUANCES FOR 6461 CONTRACTS SO FAR FOR 646,100 OZ OR 20.096 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 113 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH SEPT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 113 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN DECEMBER 2024.

DETAILS ON SEPTEMBER COMEX MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 2322 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1655 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN DURING LAST NIGHT WITH MUCH FAILURE!!

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH PREVIOUS AUGUST MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 1.135 TONNES QUEUE JUMP TO GO ALONG WITH THE 0.000. TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 20.096 TONNES//NEW TOTALS STANDING ADVANCES TO 41.514 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 241 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

AND NOW SEPTEMBER:

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 1.135 TONNES QUEUE JUMP AND 0.0000 TONNES EXCHANGE FOR RISK TODAY// NEW TOTALS OF 20.096 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH:

THAT IS;

A) 0.0000 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY // =//TOTAL FOR MONTH EX FOPR RISK: 20.096 TONNES EX FOR RISK!!

B) 1.135 TONNES TODAY QUEUE JUMP

TOTALS: 41.514 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2018 EFP CONTRACT WAS ISSUED: : /DEC 2068 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2018 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY AND THUS NO EFFECT ON OUR TOTAL OPEN INTEREST!!

- MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE.

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A STRONG SIZED SIZED 2068 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

3) TO BE FOLLOWED BY SEPTEMBER’S 6 ISSUANCES FOR EXCHANGE FOR RISK FOR 20.096 TONNES.

GOLD STANDING AT THE COMEX FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

AND NOW SEPT:

SEPT: 21.415 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) +0.0000 TONNES EX FOR RISK TODAY//

TOTAL EX FOR RISK// FOR MONTH = 20.096//NEW TOTALS FOR GOLD STANDING SEPT = 41.514 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A STRONG $42.10./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A SMALL SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION TUESDAY. MUCH OF THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO SPECULATIVE LONGS PILING INTO COMEX GOLD TRADING COUPLED WITH GOVERNMENT LIQUIDATED THEIR CONTRACTS OUT OF SEVERE FEAR!! /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS NOW IN ORDER TO FORMALIZE RAIDS, LET US SEE IF OUR CROOKS AGAIN FAIL ON OPTIONS EXPIRY WEEK THIS WEEK, LIKE THEY DID IN AUGUST. COMEX EXPIRY IS TOMORROW SEPT 25 AND LBMA LONDON EXPIRY IS TUESDAY SEPT 30

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A FAIR SIZED GAIN TOTAL OF 1.088 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 1.135 TONNES OF GOLD ALONG WITH 0.0000 TOTAL TONNES OF EXCHANGE FOR RISK TODAY/// TOTAL FOR MONTH TOTALS EX FOR RISK// MONTH = 20.096//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 41.514 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED WITH OUR HUGE GAIN IN PRICE TO THE TUNE OF $42.10

WE HAD A MAMMOTH 1972 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 350 CONTRACTS OR 35000 0Z (1.088 TONNES)

confirmed volume TUESDAY 330,734 contracts// strong//

speculators have left the gold arena

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

SEPT 24 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entries . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 2 ENTRIES i) Into Asahi 32,007.860 oz ii) Into Manfra 30,024.310 oz total deposit: 62,032.179 oz 1.929 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 196 notice(s) 19,600 OZ 0.6096 TONNES |

| No of oz to be served (notices) | 276 contracts 27,600 OZ 0.8584 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6610 notices 661,000 oz 20.553 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER 4

DEPOSITS/CUSTOMER

2 ENTRIES

2 ENTRIES

i) Into Asahi 32,007.860 oz

ii) Into Manfra 30,024.310 oz

total deposit: 62,032.179 oz

1.929 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

ADJUSTMENTs 2

a) customer to dealer Manfra: 63,080.266 oz

b) dealer to customer jPMorgan: 8,002.615 oz

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 474 CONTRACTS FOR A GAIN OF 79 CONTRACTS. WE HAD 286 CONTRACTS FILED ON TUESDAY SO WE GAINED 365 CONTRACTS OR 36,500 OZ ENTERTAINED A QUEUE JUMP OF 1.135 TONNES. WE NOW MUST ADD TO OUR INITIAL 8.093 TONNES OF GOLD STANDING TO TODAY’S QUEUE JUMP OF 1.135 TONNES, ADDING TO PREVIOUS QUEUE JUMPS AND THEN ADD MONTH SEPT// EX FOR RISK = 20.096//(WHICH INCLUDES TODAY’S 0.000 TONNES EX. FOR RISK) THUS NEW TOTAL OF GOLD STANDING ADVANCES TO 41.514 TONNES

OCTOBER LOST 6507 CONTRACTS DOWN TO 49,734

NOVEMBER LOST 50 CONTRACTS UP TO 4038 CONTRACTS.

We had 196 contracts filed for today representing 19,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 196 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (6610 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 474 CONTRACTS) minus the number of notices served upon today (196 x 100 oz per contract) equals 688,600 OZ OR 21.418 TONNES OF GOLD TO WHICH WE ADD OUR TOTAL EX FOR RISK/SEPT MONTH OF 20.096 TONNES//NEW TOTAL STANDING ADVANCES TO 41.514 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (6610 x 100 oz +we add the difference for front month of SEPT. (474 OI} minus the number of notices served upon today (196 x 100 oz) which equals 688,600 OZ OR 21.418 TONNES PLUS 20.096 TONNES EXCHANGE FOR RISK = 41.514 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 41.514 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,998,022.517 oz 62.14 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,807,323.454 oz

TOTAL REGISTERED GOLD 21,595,493.814 or 671,71 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,211,789.640 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,597.471oz ((REG GOLD- PLEDGED GOLD)= 609.56 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 24 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 2 entries a) Out of Delaware: 9915.830 oz ii) Out of HSBC 10,074.080 oz total withdrawal 19,880.910 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 2 entries i) Into Brinks 425,706.100 oz II) Into Delaware: 1061.585 oz total 420,767.685 oz |

| No of oz served today (contracts) | 190 CONTRACT(S) (0.950 million OZ |

| No of oz to be served (notices) | 161 contracts (0.805 MILLION oz) |

| Total monthly oz silver served (contracts) | 13,440 Contracts (67.200 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 entries

i) Into Brinks 425,706.100 oz

II) Into Delaware: 1061.585 oz

total 420,767.685 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

2 entries

a) Out of Delaware: 9915.830 oz

ii) Out of HSBC 10,074.080 oz

total withdrawal 19,880.910 oz

ADJUSTMENTs

customer to dealer:

a) Asahi 2,949,733.700 oz

TOTAL REGISTERED SILVER: 196.289 MILLION OZ//.TOTAL REG + ELIGIBLE. 527.153 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPT.

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 351 OPEN INTEREST CONTRACTS FOR A LOSS OF 18 CONTRACTS. WE HAD 22 CONTRACTS SERVED ON TUESDAY SO WE GAINED A SMALL 4 CONTRACTS OR 20,000 OZ ENTERTAINED A QUEUE JUMP TO TAKE DELIVERY OVER ON THIS SIDE OF THE POND..//NEW STANDING FOR SILVER COMEX INCREASES TO 68.015 MILLION OZ. THEN WE MUST ADD OUR INITIAL ISSUANCE OF 600 CONTRACTS FOR EXCHANGE FOR RISK OR 3.0 MILLION OZ//NEW STANDING REDUCES TO 71.005 MILLION OZ

STANDING FOR SILVER: 71.005 MILLION OZ

OCTOBER GAINED 106 CONTRACTS TO 3106

NOVEMBER GAINED 99 CONTRACTS UP TO 2142.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 190 or 0.950 MILLION oz

CONFIRMED volume; ON TUESDAY 82,029 huge//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 13,440 X5,000 oz = 67.200 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (351) AND the number of notices served upon today (190 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (13,440) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(351) minus number of notices served upon today (190)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 68.005 MILLION OZ TO WHICH WE ADD OUR INITIAL EXCHANGE FOR RISK SEPT TOTALLING 3.0 MILLION OZ//NEW STANDING REDUCES TO 71.005 MILLION OZ

New total standing: 71.005 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 196.289 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/527.153 million. 39.84%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

GLD INVENTORY: 1000.67 TONNES, TONIGHTS TOTAL

SILVER

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

CLOSING INVENTORY 494.121 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

JAMES RICKARDS

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

Investment managers still don’t get gold

Bloomberg: “Investment experts see opportunities ranging from dividend-paying stocks to crypto lending platform Aave.” Not one of them mentioned gold or silver.

| Alasdair MacleodSep 23 |

Bloomberg posted an article this evening, having asked four wealth advisors how they would invest a $100,000 portfolio. Putting to one side the lady who only invests in cryptos (I hope no one takes her seriously, because that’s not investment — it’s outrageous speculation) none of the other three mentioned gold.

The chart below compares gold with the S&P since January 2023.

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Both gold and the S&P more or less tracked each other until 25 February this year, when the S&P took a tumble. Until then, performance-oriented investment advisors could, indeed should have advised investors to start looking at gold, even putting a toe into the water. At least that would have been some protection when equities took a 20% tumble, finally selling off on Trump’s 2 April tariff fiasco.

That pushed the S&P to a low point, while gold recognising increasing dollar risk soared to test $3450 briefly.

Now there’s no question about it. Gold is outperforming equities, and equities are losing upside momentum. Yet Bloomberg’s esteemed advisors stubbornly persist in ignoring gold, and even the miners. When will they adjust their portfolio allocation to take account of reality??

Conclusion: The message gold is sending is clear. The risk of a dollar credit crisis is mounting, and equities are the wrong place to be. Even bitcoin is losing momentum compared with the Magnificent Seven:

I give all Bloomberg’s chosen investment advisors nought out of ten.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 241

5. COMMODITY REPORT BEEF

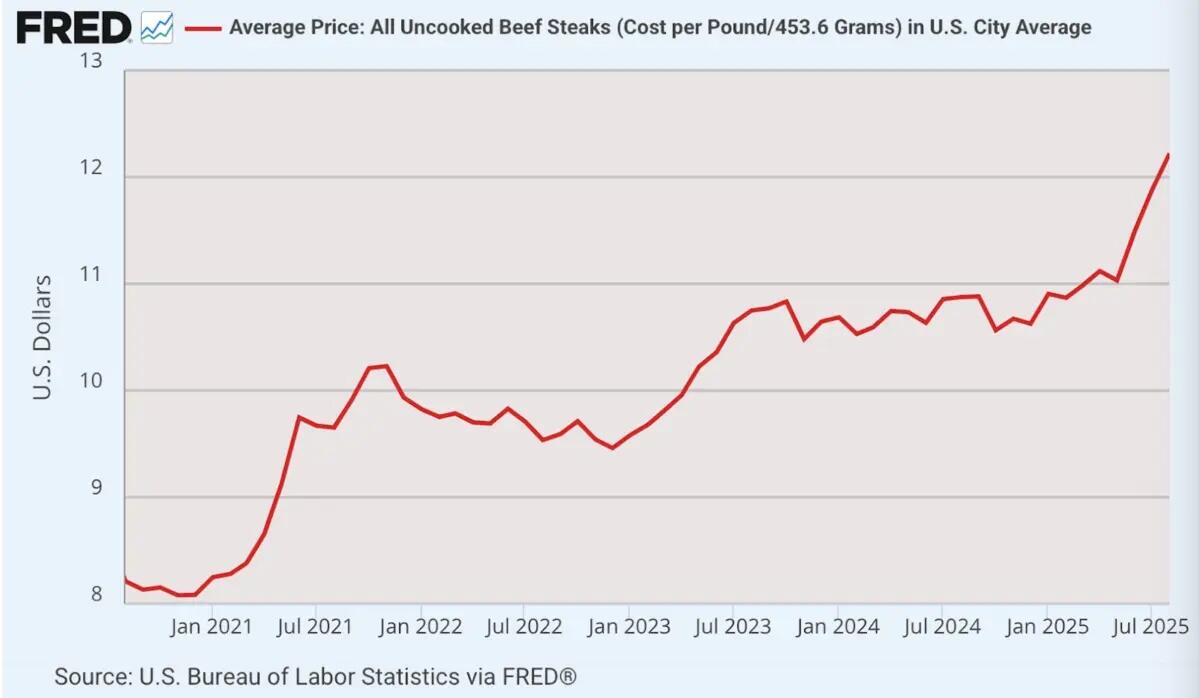

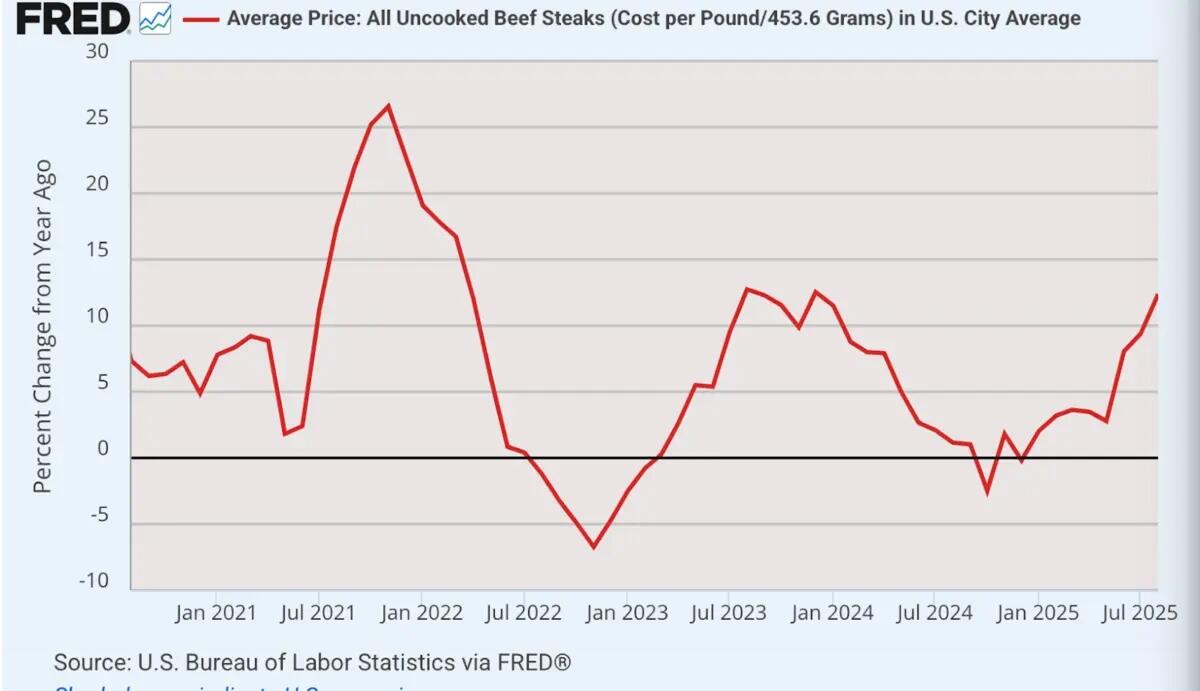

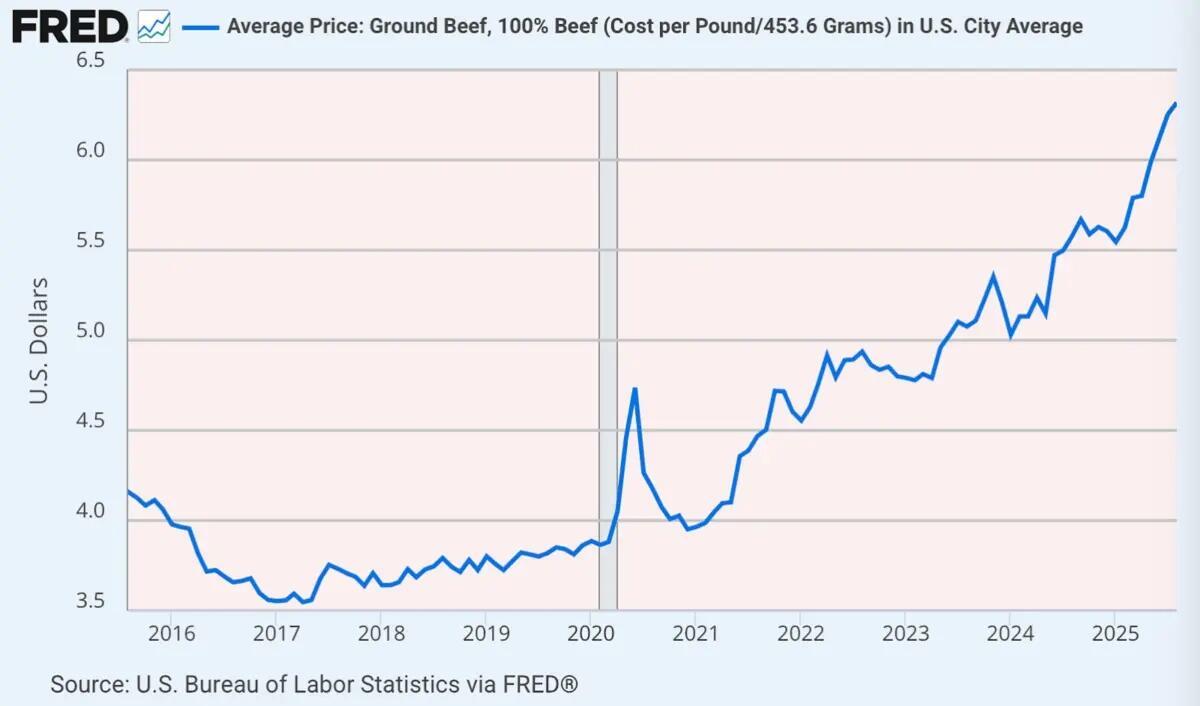

The Soaring Price Of Beef

Tuesday, Sep 23, 2025 – 10:35 PM

Authored by Jeffrey Tucker via The Epoch Times,

You have doubtless seen the price of beef at the store. It is shocking, outrageous really, ticking up higher and higher each week. When all this began four years ago, many people assumed that prices would settle back down after the crisis ended. That has not happened. The problem is getting worse, not better.

Checking in on the CPI for ground beef, we were shocked to see double-digit rates of inflation. The price of beef steaks in five years has gone up fully 50 percent and keeps rising.

Right now, the beef inflation rate is running at an astonishing 12.4 percent.

The price of ground beef has fully doubled in 10 years.

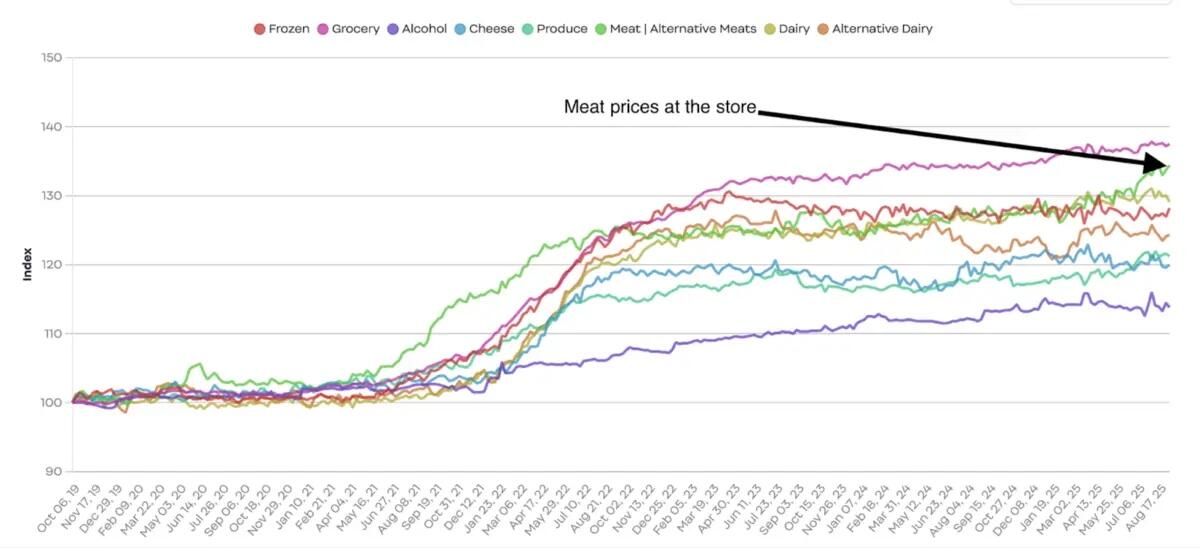

This isn’t just government data. Industry sources are showing beef prices running far ahead of other groceries.

This is happening just as more science is showing how essential beef is for human health. It is not the only good meat but it contains the most of what we need for health, weight control, energy, building muscle, and organ strength. There is growing market demand for everything from ground beef to steaks.

The growing demand is coinciding with a 50-year decline in the size of herds. Feedlot reports: “The USDA National Agricultural Statistics Service (NASS) released its Cattle report on January 31st. The total of all cattle and calves on January 1, 2025, was estimated at 86.662 million head, about 0.5 million fewer than the previous year. This marks the 6th year of contraction for aggregate beef and dairy cattle inventories and the 11th year overall of the current cattle cycle—the cyclical expansion and contraction of the national cattle herd over time. The cycle is influenced by the combined effects of cattle prices, input costs that drive cow-calf producer profitability, the gestation period for cattle, the time needed for raising calves to market weight, and climate conditions.”

This could become a huge problem for the Trump administration. If inflation in food prices and beef in particular keep going like this, there is a genuine risk to the presidency and the entire Republican Party. People who are not actually very political tend to judge the party in power by how much they have to spend at the grocery. If they find themselves switching from beef to rice and beans, they will blame the ruling party regardless.

So far, it does not appear to be a priority with Agriculture Secretary Brooke Rollins to address this huge problem with anything more than the status quo. This has to change.

I would suggest a three-point agenda for the Trump administration. It needs to be enacted immediately to keep this problem from spinning out of control.

First, there needs to be emergency deregulation of any existing barriers that keep farmers and other middle sources from getting product to the stores.

Two main regulatory bodies deal with this problem: the U.S. Department of Agriculture (USDA) Food Safety and Inspection Service (FSIS) and the Animal and Plant Health Inspection Service (APHIS). Vast paperwork and technology are required just to track the sourcing and every state has rules on storage and more. It’s a system worthy of a Soviet-style central plan. All these are clogging up supply chains such that many bureaucrats are intervening at each stage.

All these regulations consolidate the industry into only the largest players who know the ropes and can navigate the bureaucracies. All these rules need to be relaxed so that sellers can work directly with wholesalers to assure safe and good products. Fixing this problem could even require a fast executive order, backed by legislation.

Second, there must be focus on the problem of the USDA’s strict monopoly on processing meat. This adds dramatically to time and expense, and pointlessly so. Farmers must have the absolute right to on-site processing followed by sales of all sorts. The entire USDA system must be crushed and competition in meat processing permitted. The monopoly must end.

The PRIME act needs a quick passage. It stands for Processing Revival and Intrastate Meat Exemption Act. This act would: Allow states to permit the intrastate sale (within state borders) of custom-slaughtered meat—such as beef, pork, or lamb—from these facilities to consumers, restaurants, grocery stores, hotels, and other food service outlets. Meat would no longer require full federal USDA inspection for intrastate transactions. This would allow genuine farm-to-table meat, vastly reduce costs, and immediately increase supply on the shelves.

In addition, this would reduce the costs of slaughter and incentivize a bolstering of herds, relaxing existing price pressure.

Third, all meat imported from abroad should be exempt from tariffs and quotas that are currently increasing wholesale and retail pricing. This should be done in the name of saving the American diet, and maybe even saving the Trump presidency. I get that Trump believes that tariffs are necessary to protect the U.S. industry, but right now they risk pillaging the U.S. consumer. These tariffs should not apply to meat in a time of crisis.

The laws governing meat in this country are ancient, dating even from 1906. They were put in place to help large industry players in a time of grave doubt about the safety and cleanliness of the industry. Contrary to myth, the industry fully supported the regulations because they knew for sure that they would consolidate the industry and bolster consumer confidence. Unfortunately, the new rules bogged down the local farmer and added costs. All these many years later, they are still in place but serve no real function.

The remaining independent beef farmers in this country need the freedom to sell directly to stores and restaurants and to customers. People would absolutely love the chance to buy directly, knowing exactly the farmer and rancher they are supporting. The existing system does not allow this.

The Trump administration needs to place an urgent call to The Beef Initiative, founded in 2021 to make “food more localized, redundant, and secure. We serve our community by providing market access to producers and consumers who understand the importance of food integrity.”

There are many such organizations and knowledgeable farmers. Joel Salatin of Polyface must be a top consultant to guide the White House.

Such efforts are completely consistent with the agenda of MAHA. Currently, prioritizing this is not on the agenda but it must be. The last thing we need are price controls or an angry public that can no longer afford real beef.

No one wants the fake product being pushed by those who favor “lab-grown meat” or the “impossible burger,” much less the agenda to eat bugs instead of cows, chicken, and pigs. So far, inflation in beef has not been so terrible as to make it forbidding to the average family. That is changing and quickly.

The Trump administration dealt well with the egg crisis by increasing supply and stopping the hen slaughter. Egg prices are down substantially. The same needs to happen with cows now.

END

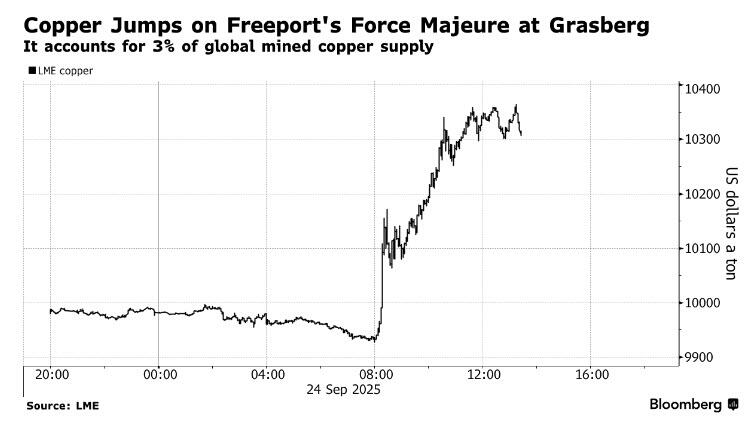

COPPER

“A Black Swan Event”: Copper Prices Soar After FCX Declares Force Majeure At World’s 2nd Largest Mine

Wednesday, Sep 24, 2025 – 02:05 PM

In what Goldman’s commodity team dubbed a “black swan event”, copper mining giaint Freeport-McMoRan (FCX) declared force majeure on contracted supplies from its giant Grasberg mine in Indonesia, the second-largest source of the metal, sending prices of the metal soaring.

The US company also cut its copper and gold sales guidance for the quarter, now seeing 4% lower copper sales and 6% lower for gold than July 2025 estimates – as it continues to search for five missing workers following an accident at the site two weeks ago. Two employees are confirmed to have died following a flow of about 800,000 metric tons of mud into Grasberg’s underground levels.

Production in the Grasberg minerals district had been halted following the incident. A prolonged disruption at the copper mine may further lift benchmark prices, while posing an additional challenge for the smelting industry as processors deal with a severe shortage of feedstock. Force majeure gives producers the right to miss supply obligations due to unforeseen events.

Teams are working around the clock at Grasberg in the province of Central Papua to clear mud and debris, and are making steady progress to reach areas where the workers were located at the time of the Sept. 8 incident, Freeport said in a statement.

While the company tried to minimize the impact as much as possible, Goldman’ commodity specialist James McGeoch was far less sanguine, calling the shocking development a “black swan event”. This is what he wrote this morning:

Force Majeure at Grasberg: Q3 loses 4% Copper and 6% Gold (incident was Sept 8 at Grassberg), Q4 will only see unaffected areas back operating my mid Nov (2 out of 5 areas), with sales “insignificant” (does that mean zero?), prev estimates 201kt Cu, and 345koz gold… Wow that’s material…. phased restart in 2026, 2/5 blocks and third in 2H and last 2 in 2027… Guide to 2026 being 35% of prev guide, which is 270kt of copper lost and 1.04m oz Gold. GIR model we model 700kt in 2025 and 730kt in 2026….

Summary: you are losing 500kt Copper over next 12-15 months, with a ramp in 2027, could argue another 100-200kt lost….. This is Cobre + Komao + Los Bronces all at once.

FCX: looking at 2026 cons this is c.39% of their Copper and 60% of the Gold. Grasberg to those in the weeds is a Gold mine (largest in the world). REMEMBER FCX owns 48.76%…so this is not as painful as it looks.

Copper has to rally on this. Remember what I say. Demand moves are linear, supply moves are exponential.

The below is a chart looking at these periods, obv there are many factors at play in each of these moves, i have been arguing for a number of days/weeks that Copper is poised, interest has been low (despite CTA creeping to record long on GS strat data and Managed money back at a reasonable level). Commodity franchise has been almost exclusively looking at precious for discretionary/macro accounts. This will light the fuse.

Here is a separate fact sheet, also from Goldman, only this time from trader trader Adam Gillard:

- Summary: We think the realized production loss will be smaller than headline given lower YTD reported disruptions, but ~150k MT this year should have a disproportionate impact on SHFE + LME given the surplus is trapped in the US (from tariff related stock build). Expect SHFE / LME arb to perform, Asian LME inventory to draw, and LME spreads to stay tight. Vol bid; 6M 25% delta calls +2v (from a 5y low), and skew also rallied to +1.5v, highest level since May24 when CMX “broke”. We’re trading from the long side via skew and flat price.

- What happened? Freeport downgraded bal-25 production by 250-260k MT, and cal-26 production by ~270k MT, causing price to rally 3.5%

- Balance pre Grasberg disruptions: 2025: 105k surplus / 2026: 55k deficit / 2027: 134k deficit

- Are there any mitigants: YTD disruptions are ~90k MT below our allowance; think the salient point is whether q4 disruptions are in line with YTD average, or our pro-rata allowance. Think we likely lose ~150k MT this year, although we acknowledge the potential for concentrate inventory at mine, port or Tank House, to be exported if Freeport can get a permit from Indo Gvt. 2026 impact harder to model; we had 5% / 1.1mn MT disruption allowance vs 2.2% supply growth, probably lose another 100-150k MT. It’s a lot. Price should rally we think.

- Where do Indonesian exports go: Refined exports are low-ish at 25k MT pm as Gresik ramps, 25% goes to China, the rest Asia ex-China. Concentrate exports are ~160k DMT per month, of which 65% goes to China (which explains the onshore bid during their night session, see below).

- Does the CMX stock build exacerbate the LME + SHFE tightness: Yes. Combination of a) tariff related onshore (US) stock-build and b) Still positive CMX / LME ARB (explanation here) incentivising the marginal unit to the US, is keeping the surplus trapped (in the US), meaning lost Grasberg metal will have a disproportionate impact on Shanghai and London.

- What did China do: Bought a lot, largest open interest change in 5 years. But total positioning is ~23% off the local high

- LME volume also strong at ~49k lots

Copper for delivery in three months rose as much as 3.7% to $10,341 a ton on the London Metal Exchange, the biggest intraday jump since April 10, while FCX shares tumbled as much as 11% and rivals including Glencore and Teck Resources climbed.

As Bloomberg notes, the accident highlights the copper market’s vulnerability to global supply shocks, and is just the latest disruption to the industry. It follows Hudbay Minerals’ disclosure late Tuesday that it was shutting operations at a mill at its Constancia mine site in Peru due to ongoing political protests.

The development at Freeport shows “how little it takes to tighten up this market,” especially when two of the world’s top copper mines have problems at the same time, said Ole Hansen, head of commodity strategy at Saxo Bank. “Traders buy first before asking questions.”

The Grasberg mine accounted for about 3.2% of mined copper supply for this year prior to the disruptions, according to Grant Sporre, global head of metals and mining at Bloomberg Intelligence. It contributes nearly 30% of Freeport’s total copper production and 70% of gold output, underscoring the scale of the disruption.

“An accident of such scale is unheard of in Freeport’s history,” said Bernard Dahdah, an analyst at Natixis.

Glencore shares rose as much as 3.6% in London, while Antofagasta Plc added 9.6%. Teck Resources gained as much as 6% and Southern Copper Corp. climbed 10% in New York.

* END

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 31.81 PTS OR 0.83%

//Hang Seng CLOSED UP 359.53 PTS OR 1.37%

// Nikkei CLOSED : UP 136.65 PTS OR .30 //Australia’s all ordinaries CLOSED DOWN 0.88%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1216 OFFSHORE CLOSED DOWN AT 7.1274/ Oil UP TO 63.51 dollars per barrel for WTI and BRENT UP TO 67.66 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1216 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1274 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1261

OFFSHORE YUAN: UP TO 7.1274

HANG SENG CLOSED UP 359.53 PTS OR 1.37%

2. Nikkei closed UP 136.65 PTS OR 0.30%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 97.21 EURO FALLS TO 1.1770 DOWN 46 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.642//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.53…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.159 DOWN 2 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7311 Italian 10 Yr bond yield DOWN to 3.573 SPAIN 10 YR BOND YIELD DOWN TO 3.282

3i Greek 10 year bond yield DOWN TO 3.426

3j Gold at $3771.00 Silver at: 44.14 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 16 /100 roubles/dollar; ROUBLE AT 83.81

3m oil (WTI) into the 63 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148/20/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.640% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.159DOWN 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7935 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9344 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.103 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.716 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.563 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.47

10 YR UK BOND YIELD: 4.668 DOWN 2 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.479 DOWN 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.186 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.733 DOWN 1 BASIS PTS.

2a New York OPENING REPORT

Futures Rise As Alibaba Capex Promise Boosts AI Sentiment Again

Wednesday, Sep 24, 2025 – 08:33 AM

US futures are once again higher after taking a brief pause yesterday, led by Tech, with all of Mag7 higher pointing to a stronger open as Alibaba’s spending promise and Micron’s upbeat outlook lift sentiment on AI. Global stocks resumed their rally after a pledge by China’s Alibaba for more spending (now the mere promise of more capex is sufficient to send your stock ripping) and Micron’s upbeat forecast lifted sentiment on AI (even higher… if that’s possible). As of 8:00am ET, S&P and Nasdaq futures rose 0.2% after big tech’s slide in the prior session broke a streak of records; Mag 7 are all green led by AMZN, +1.6% while TMT is boosted by Micron rising +1.5% after strong earnings underscored the boom’s ongoing momentum. Semis were bid after Alibaba jumped 9% in typhoon-hit Hong Kong on plans to boost AI spending beyond an initial $50 billion target. According to JPM, the AI-theme should perform well today (when does it not), including Critical Metals. Cyclicals are leading Defensives. The curve is steepening as 2Y yields are -2bps and the 10Y rises 3bps to 4.13% as the USD is bid up for first time this week. Trump said that Ukraine, with NATO help, has the tools to win back all of its Russian-occupied territory, included continued US weapons sales to NATO, and should shoot down Russian planes that enter its airspace. Gold held near all-time highs. Today’s macro data focus is on Home Sales, Building Permits and Mortgage Apps.

In premarket trading, Mag 7 stocks are all higher: Amazon (AMZN) gains 1.4% following an upgrade at Wells Fargo on greater conviction in the company’s Amazon Web Services division (Tesla +0.7%, Nvidia +0.6%, Meta +0.2%, Microsoft +0.2%, Alphabet +0.1%, Apple +0.07%).

- Acadia Pharmaceuticals (ACAD) shares are halted after the company said its Phase 3 trial of intranasal carbetocin (ACP-101) in patients with hyperphagia in Prader-Willi syndrome failed to meet its primary endpoint.

- Adobe (ADBE) is down 1.3% as Morgan Stanley downgrades to equal-weight from overweight on decelerating digital media annual recurring revenue.

- Alibaba Group Holding (BABA) shares surged 9% after revealing plans to ramp up AI spending past an original $50 billion-plus target, joining tech leaders pledging ever-greater sums toward a global race for technological breakthroughs.

- Bloom Energy Corp. (BE) falls 6% after Jefferies cut its recommendation on the fuel cell power generator to underperform from hold, saying that valuation reflects high expectations. Analysts see difficulty for the firm to reach 1 GW of power in the near term.

- Lithium Americas (LAC) soars 68% after reports revealed the US is seeking an equity stake in the company as it renegotiates terms of a $2.3 billion government loan.

- PayPal Holdings Inc. (PYPL) climbs 1.3% after Blue Owl Capital Inc. agreed to buy about $7 billion of buy now, pay later loans from the company.

- UniQure (QURE) shares are halted after the company said phase I/II trial of AMT-130 in Huntington’s disease met its prespecified primary endpoint.

In corporate news, OpenAI plans to invest roughly $400 billion it does not have to develop five new US data center sites in partnership with Oracle and SoftBank. Tether is in talks with investors to raise as much as $20 billion, a deal that could propel the crypto firm into the highest ranks of the world’s most valuable private companies. Apollo is rolling out three new private capital funds for wealthy individual investors in Europe.

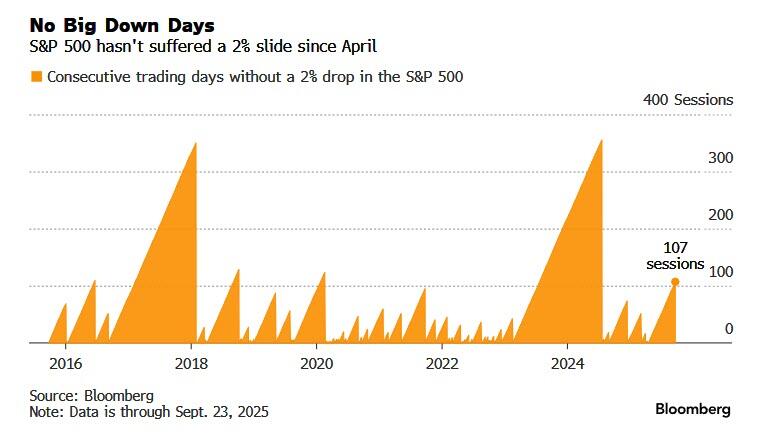

Turning back to the broader market, down days are few and far between at the moment, and the overall sentiment for stocks is becoming euphoric. JPMorgan’s head of market intelligence, Andrew Tyler, sums it up nicely: “several conversations yesterday focused on what could derail this bullish run. My favorite response was an asteroid hitting the earth.” Internal market metrics underscore just how bullish investors have become. Systematic strategies were already almost maxed-out. Now, discretionary investors are stretching to more bullish levels, with room to go further. Options volume is firmly skewed toward chasing the upside. Still, impending portfolio rebalancing may create a technical headwind as the month comes to an end.

In any case, the S&P 500 has gone 107 sessions without a drop of 2% or more, the longest streak in more than a year as hopes for rapid Fed easing have added to the buoyant mood.

Traders are paying little attention to a range of risks, with the threat emphasized Tuesday when Fed Chair Jerome Powell warned that policymakers still face a difficult path ahead. Bullishness over AI’s vast potential has fueled multiple all-time highs in stocks this year, offsetting all worries about rising geopolitical risks and trade tensions.

In the Middle East, Saudi Arabia’s move to ease foreign ownership rules added $123 billion to the country’s stock market. Banking stocks on the Tadawul All Share Index surged a record 9%.

Alibaba shares soared in Asia after CEO Eddie Wu revealed plans to ramp up AI spending above an original target of $50 billion-plus over three years. Micron, which has seen its shares almost double this year, gave an upbeat outlook driven by demand for AI equipment. Also top of mind for tech traders — California’s AG is looking at whether Trump’s $100,000 application fee for H-1B visas can be challenged by law.

“AI is back as the key driver for global markets. Investment continues apace and that’s keeping the AI theme relevant,” said Guy Miller, chief strategist at Zurich Insurance Co. “That leads to the question, is this getting to the last innings with overinvestment and misallocation of capital? From an investor perspective, all that actually tells you there’s a bit further to run.”

According to Bloomberg, the danger now is that officials scale back expectations for further cuts, leaving Wall Street disappointed. San Francisco Fed President Mary Daly speaks later Wednesday, in what is otherwise a light day for the events calendar.

“There’s going to be lots of chatter about the Fed and that’s going to dominate,” said Daniel Murray, deputy chief investment officer at EFG Asset Management. “I expect we’re going to drift for a couple of weeks. The next catalyst is going to be the third-quarter earnings season.”

European stocks slipped 0.3% diverging from gains in Asia and the US, as autos, consumer products and financials underperform. The region’s defense stocks rallied after US President Donald Trump’s latest criticism of Russia. Here are the biggest movers Wednesday:

- European defense stocks rise after President Donald Trump said on Tuesday NATO nations should shoot down Russian aircraft that violated their airspace and struck a more sympathetic tone on Ukraine’s chances of winning the war

- JD Sports shares rise 3.6% after the retailer’s 1H results showed “limited tariff impact,” according to RBC. Analysts said the update also showed market share gains in North America and Europe, and supported an outlook for a better 2H

- Electrolux Professional gains as much as 5.9% after Handelsbanken reiterated its buy rating on the Swedish professional kitchen and laundry equipment maker, saying the upcoming 3Q report and CMD as potential positive triggers

- Bouygues shares rise as much as 2.7% after the construction and telecommunications company was upgraded by Morgan Stanley, which sees limited downside to the current share price

- Metso falls as much as 4.9%, the most since July, after its new financial targets fell short of the most bullish hopes for the Finnish industrial equipment company, which slightly hiked its Ebita margin target

- Lanxess shares fall as much as 5.3% after being downgraded by Deutsche Bank, as analysts say the chemical company is now fairly valued and that the upside from the recent Envalior announcement has been captured

- Asker Healthcare Group falls as much as 6.4% after Swedish pension fund AP6 sold its entire holding in the company at SEK81 per share, representing a 8.9% discount from the previous close

- NCAB falls as much as 7.6%, the most since July, after SEB cut its recommendation on the Swedish printed circuit board maker to hold from buy, saying the company’s valuation has come up and is trading at a 10-21% premium

- Baltic Classifieds falls as much as 15% to the lowest in more than a year, after the firm said in a trading update that full-year revenue and profit is expected to be 3%-4% below its previously communicated guidance

- Pinewood Technologies shares plunge as much as 14% after the software maker’s 2025 Ebitda target disappointed. Berenberg analysts noted a one-off accounting impact and the delay in implementation with a major customer

- On the Beach shares slide as much as 20%, the most since May 2023, after the online package holiday firm’s full-year profit before tax undershot expectations, due to loss-making B2B operations

- Exail Technologies drops as much as 7.7% after completing an offer of its convertible bonds, which led to TP ICAP downgrading the industrial company. That has broken the clean-sweep of buy ratings on the stock

Earlier in the session, Asian stocks advanced, as a boost from Alibaba’s AI spending plans countered a broader regional selloff in tech shares. The MSCI Asia Pacific Index gained 0.2%, with Alibaba the biggest boost while banks including Westpac Banking Corp. and Commonwealth Bank of Australia weighed on the gauge. Equity benchmarks rose in Japan and mainland China, and fell in South Korea, Taiwan and Australia. Meanwhile, the Hang Seng Tech Index surged more than 2% after Alibaba said it would beef up its AI budget and unveiled its new Qwen3-Max large language model. Shares of peers and China’s homegrown tech suppliers climbed, boosting key equity measures on the mainland as well as in Hong Kong. Australia’s main index declined nearly 1% after monthly consumer prices rose more than economists expected, weakening the case for a rate cut next week.

“Asian markets are treading cautiously today, caught between profit-taking and lack of new catalysts,” said Dilin Wu, a research strategist at Pepperstone Group. “After yesterday’s strong US tech rally, much of the initial enthusiasm has faded.”

In FX, the dollar climbs 0.3% after two days of declines. The Australian dollar is the only G-10 currency to outperform the greenback, while the yen is the weakest of the group. The euro slips after an unexpected drop in German business confidence.

In rates, front-end Treasuries outperform while 10Y yields rose 3bps to 4.13% as the curve steepened. Treasury auctions resume at 1pm New York with $70 billion 5-year note sale, follows a solid 2-year note auction Tuesday which stopped 0.1bp through the WI.

In commodities, oil extended its biggest gain in a week, as Trump ramped up his rhetoric against Russia and traders watched for supply disruptions from the OPEC+ member. Brent rose above $68 a barrel and WTI adds 0.4% to $63.64. Sot gold rises about $5 to $3,769 an ounce.

US economic data slate includes August new home sales/building permits (10am). Fed speaker slate includes Daly at 4:10pm, delivering keynote remarks on the outlook for the economy

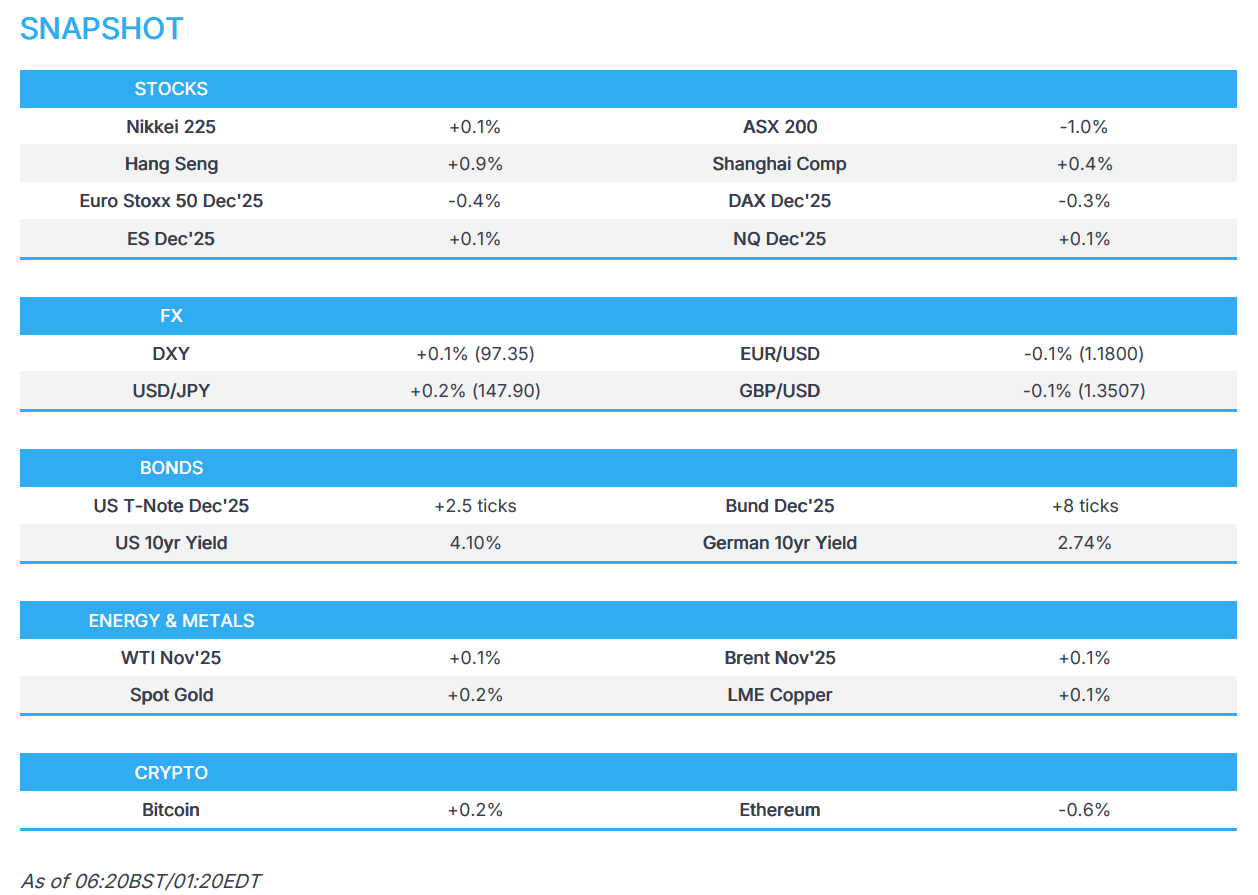

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.3%

- Russell 2000 mini +0.1%

- Stoxx Europe 600 -0.3%

- DAX -0.2%

- CAC 40 -0.3%

- 10-year Treasury yield little changed at 4.11%

- VIX -0.2 points at 16.42

- Bloomberg Dollar Index +0.3% at 1199.14

- euro -0.4% at $1.1768

- WTI crude +0.4% at $63.66/barrel

Top Overnight News

- House Democrats will meet on September 29th in Washington, D.C. to discuss government funding: BBG

- Volodymyr Zelenskiy told Fox News that Donald Trump’s remarks on Ukraine winning back territory from Russia were a big shift and said the leaders have better relations than before. The Ukrainian president speaks today at the UNGA. BBG