WE HAVE NOW ENTERED OPTION EXPIRY MONTH:

COMEX OPTION EXPIRED YESTERDAY,SEPT 25. AND SEPT 30 IS LBMA LONDON EXPIRY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

118 H MACQUARIE FUTURES US 112

190 H BMO CAPITAL MARKETS 820

323 C HSBC 2 60

363 H WELLS FARGO SECURITI 465

435 H SCOTIA CAPITAL (USA) 1

624 H BOFA SECURITIES 601

657 H MORGAN STANLEY 10

661 C JP MORGAN SECURITIES 1

686 C STONEX FINANCIAL INC 9 14

732 C RBC CAP MARKETS 42

737 C ADVANTAGE FUTURES 3

880 C CITIGROUP 3

880 H CITIGROUP 218

905 C ADM 33

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 1157 CONTRACTs NOTICES FOR 115,700 OZ or 3.923 TONNES

total notices so far: 8119 contracts for 811,900 OR 25.253 tonnes)

SILVER NOTICES: 56 NOTICE(S) FILED FOR 0.280 MILLION OZ/

total number of notices filed so far this month : 13,584 CONTRACTS (NOTICES) for 67.920 million oz

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 41.810 MILLION OZ.(QUITE SMALL)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 3.586 TONNES PLUS 0.000 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 20.096//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 45.349 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 100.703 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE SIZED 1489 CONTRACTS OI TO 167,627 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 350 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 640 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1489 CONTRACTS AND ADD TO THE 350 E.FP. ISSUED

WE OBTAIN A MEGA MEGA HUGE SIZED GAIN OF 1839 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE GAIN OF $1.44 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 9.195 MILLION PAPER OZ

OCCURRED WITH OUR GAIN $1.44 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS THURSDAY MORNING:

//Hang Seng CLOSED DOWN 356.48 PTS OR 1.35%

// Nikkei CLOSED : DOWN 399.94PTS OR 0.87% //Australia’s all ordinaries CLOSED UP 0.17%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1344 OFFSHORE CLOSED DOWN AT 7.1417/ Oil UP TO 65.09 dollars per barrel for WTI and BRENT UP TO 69.41 Stocks in Europe OPENED ALL GREEN

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 9755 CONTRACTS TO 516,312 OI with OUR GAIN IN PRICE OF $5.70 WITH RESPECT TO THURSDAY’S // TRADING COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2623). WE HAD CONSIDERABLE T.A.S. LIQUIDATION(AS WE ARE IN OPTIONS EXPIRY WEEK FOR SEPT.) WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 7132 CONTRACTS (OR 22.183 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD 0 CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 3 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 3 MONTHS 68.542 TONNES//BANK OF ENGLAND TOTAL RESERVES 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

AND NOW:

SEPT:

SEPTEMBER: SIX ISSUANCES SO FAR TOTALLING 6,461 CONTRACTS OR 646,100 OZ OR 20.096 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SIX ISSUANCES FOR 6461 CONTRACTS SO FAR FOR 646,100 OZ OR 20.096 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 113 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH SEPT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 113 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN DECEMBER 2024.

DETAILS ON SEPTEMBER COMEX MONTH//

IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 7132 CONTRACTS DESPITE OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A STRONG T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 2776 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN WEDNESDAY WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSES TO BUCKLE!!

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH PREVIOUS AUGUST MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 3.586 TONNES QUEUE JUMP TO GO ALONG WITH THE 0.000. TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 20.096 TONNES//NEW TOTALS STANDING ADVANCES TO 45.349 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 242 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

AND NOW SEPTEMBER:

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 3.586 TONNES QUEUE JUMP AND 0.0000 TONNES EXCHANGE FOR RISK TODAY// NEW TOTALS OF 20.096 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.253 TONNES

THAT IS;

A) 0.0000 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY // =//TOTAL FOR MONTH EX FOPR RISK: 20.096 TONNES EX FOR RISK!!

B) 3.586 TONNES TODAY QUEUE JUMP//NORMAL DELIVERY OF 25.363 TONNES

TOTALS: 45.349 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2623 EFP CONTRACT WAS ISSUED: : /DEC 2623 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2623 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY BUT THIS HAD NO EFFECT ON OUR TOTAL OPEN INTEREST!!

- MONTH END SPREADERS HAVE NOW COME IN THE PICTURE AND IT SURELY LOOKS LIKE THERE WILL BE NO DAMAGE TO THE PRICE OF GOLD SIMILAR TO WHAT HAPPENED DURING AUGUST EXPIRY MONTH.

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A FAIR SIZED SIZED 1679 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

3) TO BE FOLLOWED BY SEPTEMBER’S 6 ISSUANCES FOR EXCHANGE FOR RISK FOR 20.096 TONNES.

GOLD STANDING AT THE COMEX FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

AND NOW SEPT:

SEPT: 25.233 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) +0.0000 TONNES EX FOR RISK TODAY//

TOTAL EX FOR RISK// FOR MONTH = 20.096//NEW TOTALS FOR GOLD STANDING SEPTADVANCES TO 45.349 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $5.70./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION THURSDAY. MUCH OF THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO SPREADER LIQUIDATION WITH SPECULATIVE LONGS PILING INTO COMEX GOLD TRADING COUPLED WITH GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!! /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS NOW IN ORDER TO FORMALIZE RAIDS, LET US SEE IF OUR CROOKS AGAIN FAIL AGAIN ON THIS SEPT. OPTIONS EXPIRY WEEK , LIKE THEY DID IN AUGUST. COMEX EXPIRY IS CONCLUDED YESTERDAY, SEPT 25 AND LBMA LONDON EXPIRY IS FINISHING TUESDAY SEPT 30.

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A STRONG SIZED LOSS TOTAL OF 22.183 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 3.586 TONNES OF GOLD ALONG WITH 0.0000 TOTAL TONNES OF EXCHANGE FOR RISK TODAY/// TOTAL FOR MONTH TOTALS EX FOR RISK// MONTH = 20.096//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 45.349 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $5.70

WE HAD A MAMMOTH 10,738 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 7132 CONTRACTS OR 713,200 0Z (22.183TONNES)

confirmed volume THURSDAY 330,734 contracts// strong//

speculators have left the gold arena

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

SEPT 25 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2 entries a) Out of Brinks 289.359 oz (9 kilobars) b) Out of JPMorgan: 289,356.9 (9 kilobars) total withdrawal 578.315 ox (18 kilobars) . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRIES i) Into JPMorgan: 24,113.250 oz (750 kilobars) total deposit: 24,113.250 oz 0.75 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1197 notice(s) 119,700 OZ 3.723 TONNES |

| No of oz to be served (notices) | 00 contracts 00 OZ 0.000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 8119 notices 811,900 oz 25.253 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRIES

i) Into JPMorgan: 24,113.250 oz

(750 kilobars)

total deposit: 24,113.250 oz

0.75 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

2 entries

a) Out of Brinks 289.359 oz (9 kilobars)

b) Out of JPMorgan: 289,356.9 (9 kilobars)

total withdrawal 578.315 ox (18 kilobars)

ADJUSTMENTs 1

ADJUSTMENTs 3

customer to dealer:

a) Asahi 32,009.349 oz

volume at the comex: THURSDAY 299,614 oz (good)

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 1197 CONTRACTS FOR A GAIN OF 841 CONTRACTS. WE HAD 312 CONTRACTS FILED ON THURSDAY SO WE GAINED A MONSTROUS 1153 CONTRACTS OR 115,300 OZ ENTERTAINED A QUEUE JUMP OF 3.586 TONNES. WE NOW MUST ADD TO OUR INITIAL 8.093 TONNES OF GOLD STANDING TO TODAY’S QUEUE JUMP OF 3.586 TONNES, ADDING TO PREVIOUS QUEUE JUMPS AND THEN ADD MONTH SEPT// EX FOR RISK = 20.096//(WHICH INCLUDES TODAY’S 0.000 TONNES EX. FOR RISK) THUS NEW TOTAL OF GOLD STANDING ADVANCES TO 45.349 TONNES

OCTOBER LOST 9486 CONTRACTS DOWN TO 34,081

NOVEMBER GAINED 153 CONTRACTS UP TO 4396 CONTRACTS.

We had 1197 contracts filed for today representing 119,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1197 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 1 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (8119 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 1197 CONTRACTS) minus the number of notices served upon today (1197 x 100 oz per contract) equals 811,900 OZ OR 25.253 TONNES OF GOLD TO WHICH WE ADD OUR TOTAL EX FOR RISK/SEPT MONTH OF 20.096 TONNES//NEW TOTAL STANDING ADVANCES TO 45.349 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (8119 x 100 oz +we add the difference for front month of SEPT. (1197 OI} minus the number of notices served upon today (1197 x 100 oz) which equals 811,900 OZ OR 25.233 TONNES PLUS 20.096 TONNES EXCHANGE FOR RISK = 45.349 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 45.349 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,996,286.363 oz 62.09 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,946,410.448 oz

TOTAL REGISTERED GOLD 21,813,553.599 or 678.49 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,132,856.849 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,817.267oz ((REG GOLD- PLEDGED GOLD)= 616.40 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 26 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entry a) Out of Loomis: 91,238.350 oz total withdrawal: 91,278.350 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 2 entries i) Into CNT 506,764.780 oz iii) Into Delaware 1074.413 oz total deposit 507,839.193 oz oz |

| No of oz served today (contracts) | 56 CONTRACT(S) ( 0.280 million OZ |

| No of oz to be served (notices) | 24 contracts (0.120 MILLION oz) |

| Total monthly oz silver served (contracts) | 13,584 Contracts (67.920 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 entries

i) Into CNT 506,764.780 oz

iii) Into Delaware 1074.413 oz

total deposit 507,839.193 oz oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 entry

1 entry

a) Out of Loomis: 91,238.350 oz

total withdrawal: 91,278.350 oz

adjustments:

1

out of CNT dealer to customer acccount: 599,143.700 oz

TOTAL REGISTERED SILVER: 195.699 MILLION OZ//.TOTAL REG + ELIGIBLE. 530.344 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPT.

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 80 OPEN INTEREST CONTRACTS FOR A LOSS OF 104 CONTRACTS. WE HAD 88 CONTRACTS SERVED ON THURSDAY SO WE LOST A SMALL SIZED 16 CONTRACTS OR 80,000 OZ ENTERTAINED AN E.F.P. TRANSFER TO LONDON TO TAKE DELIVERY OVER ON THAT SIDE OF THE POND..//NEW STANDING FOR SILVER COMEX DECREASES TO 68.040 MILLION OZ. THEN WE MUST ADD OUR INITIAL ISSUANCE OF 600 CONTRACTS FOR EXCHANGE FOR RISK OR 3.0 MILLION OZ//NEW STANDING ADVANCES TO 71.040 MILLION OZ. OUR BANKERS NOW FIND IT NECESSARY TO TAKE SOME OF THEIR DELIVERIES AT THE LBMA IN LONDON.

STANDING FOR SILVER: 71.040 MILLION OZ

OCTOBER LOST 182 CONTRACTS TO 2959

NOVEMBER GAINED 28 CONTRACTS UP TO 2227.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 56 or 0.280 MILLION oz

CONFIRMED volume; ON THURSDAY 108,588 huge//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 13,584 X5,000 oz = 67.640 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (80) AND the number of notices served upon today (56 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (13,584) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(80) minus number of notices served upon today (56)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 68.040 MILLION OZ TO WHICH WE ADD OUR INITIAL EXCHANGE FOR RISK SEPT TOTALLING 3.0 MILLION OZ//NEW STANDING REDUCES TO 71.040 MILLION OZ

New total standing: 71.040 million oz which is STILL HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 195/699 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/530.344 million. 39.62%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

GLD INVENTORY: 996.85 TONNES, TONIGHTS TOTAL

SILVER

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

CLOSING INVENTORY 494.802 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

JAMES RICKARDS

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

A horror story in paper markets

Our headline chart shows silver storming ahead amid reports of backwardations and soaring lease rates. Will it continue, and will gold be next?

| Alasdair MacleodSep 26∙Paid |

Driven by poor liquidity, in Europe this morning silver was $45.03, up $2.00 from last Friday’s close. Gold was up a less spectacular $68 at $3750 on the week, but with a firm undertone.

In this report, we look at what is currently driving gold and silver prices higher, and whether it will continue.

The chart below illustrates the paper market problem with the silver futures contract.

Having soared to over 184,000 Comex contracts by 17 June, open interest declined to 154,000 on 1 September. Meanwhile the price continued rising strongly to $40. A falling open interest and rising price can only happen in a vicious bear squeeze on the establishment shorts — principally the swap traders. But open interest stopped falling after 1 September, and is now rising because long speculators realise that precious metals are in a bull market and are joining the chase.

This is tightening the screws on the shorts, who must really be panicking. The technical chart shows a rare runaway situation, with no sign of stopping.

Additionally, investors are beginning to buy ETFs, putting further strains on physical liquidity, so higher lease rates and backwardations in London are likely to persist. And stand for deliveries on Comex, presumably going into hoarding hands amount to 10,842 tonnes so far this year, about 58% of global mine supply for nine months.

You read that right!

The problem is that instead of a rising silver price leading to profit-taking, it is likely to reaffirm the fundamental reasons for hoarding silver, which is to hedge failing fiat currencies. Buyers are still flocking to physical and appear likely to accelerate the pace of their buying in these extremely tight conditions.

This brings us to gold. Next up is the technical chart:

As is the case with silver, gold appears to be rising vertically. Again, investors have missed out on a major bull market and wondering whether they should buy. At the margin they are doing this by going down the ETF route. Furthermore, major US banks with trillions under management are now forecasting higher prices which are bound to put pressure on their investment managers who have next to no exposure to gold for their clients.

While the market for gold is more liquid than silver’s, a similar situation exists, with 900 tonnes stood for delivery on Comex nearly all of which presumably are being hoarded. At the same time ETF demand is beginning to take off, putting further strains on physical liquidity. And as the chart below shows, there are similarities with the silver squeeze.

China and Bretton Woods 2

As a backdrop to problems in western capital markets, China has effectively cornered the physical market, and it now emerges that she plans to link her currency with gold for intranational trade settlement purposes. This is why the Shanghai Gold Exchange is opening vaults in Hong Kong and Saudi Arabia, as well as planning for yuan-gold exchange facilities elsewhere in SE Asia. This is sending a clear signal to other SCO and BRICS nations as well as the Global South generally that in a post-dollar world they will need gold reserves of their own.

Consequently, there are central bank buyers for all available bullion, which with growing ETF demand is bound to keep the physical supply side very tight.

At some stage, this gathering rush into physical gold and silver could slacken. Joining the herd of buyers are likely to be paper speculators hoping for a quick profit, and they will be shaken out. But that won’t change the underlying bullion shortages, which look like worsening.

The authorities will hope that it won’t lead to systemic problems.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 242/ROBERT KIENTZ

5. COMMODITY REPORT SILVER

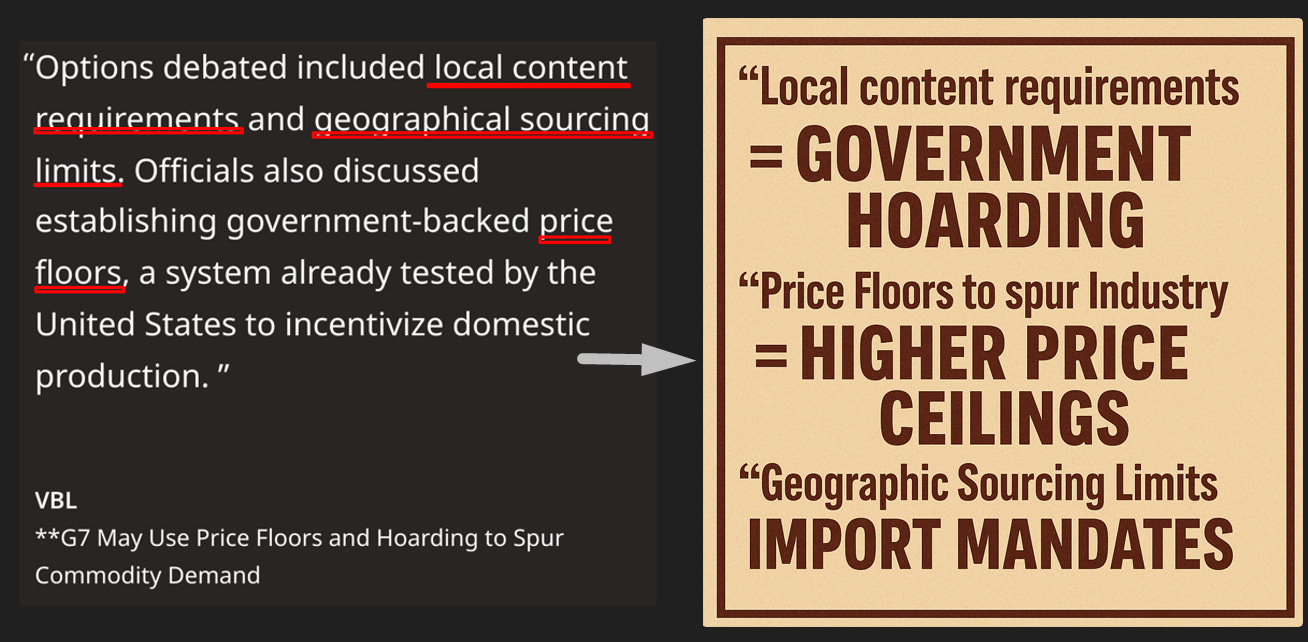

Silver: G7 Looks At Price Floors and Critical Mineral Hoarding

by VBL

Thursday, Sep 25, 2025 – 12:55

G7 weighs critical mineral price floors, hoarding to curb China’s dominance

Authored by GoldFix ZH Edit

Group of Seven (G7) nations and the European Union are considering the use of price floors and new trade measures to boost rare earth production outside China, according to four people familiar with the talks. The measures could include subsidies, carbon-based tariffs on Chinese exports, and restrictions in public procurement tenders.

Reuters reports that the discussions come amid renewed supply chain concerns following China’s imposition of export controls on rare earths and related magnets earlier this year. The restrictions, initially a response to U.S. tariffs, disrupted European automakers and highlighted the bloc’s reliance on Chinese supply. Despite temporary licensing relief, bottlenecks remain and fresh shutdown risks are emerging.

Are You Ready for $144 Silver and $9.00 Copper?

Aug 26

Housekeeping: These commodities could be significantly higher or lower than the analog projects. Read this

Technical teams met in Chicago this month under the G7’s Critical Minerals Action Plan. “The heart of the conversation was whether to raise the bar on regulation of foreign investment in critical materials in order to avoid companies going to China,” one source told Reuters.

Options debated included local content requirements and geographical sourcing limits. Officials also discussed establishing government-backed price floors, a system already tested by the United States to incentivize domestic production.

The U.S. has signaled interest in broader coordinated measures with allies to counter potential Chinese price dumping in rare earth markets. As one source noted, divisions remain within the G7 on how directly to confront Beijing.

More GoldFix here

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 26.20 PTS OR 0.65%

//Hang Seng CLOSED DOWN 356.48 PTS OR 1.35%

// Nikkei CLOSED : DOWN 399.94PTS OR 0.87% //Australia’s all ordinaries CLOSED UP 0.17%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1344 OFFSHORE CLOSED DOWN AT 7.1417/ Oil UP TO 65.09 dollars per barrel for WTI and BRENT UP TO 69.41 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1344 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1417 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1344

OFFSHORE YUAN: DOWN TO 7.1417

HANG SENG CLOSED DOWN 356.48 PTS OR 1.35%

2. Nikkei closed DOWN 399.84 PTS OR 0.87%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 98.00 EURO RISES TO 1.1684 UP 23 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.646//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 149.67…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.161 UP 3 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7610 Italian 10 Yr bond yield UP to 3.620 SPAIN 10 YR BOND YIELD DOWN TO 3.18

3i Greek 10 year bond yield UP TO 3.457

3j Gold at $3753.60 Silver at: 45.10 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 23 /100 roubles/dollar; ROUBLE AT 83.71

3m oil (WTI) into the 65 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 149.41/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.646% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.161 UP 3 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7990 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9336 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.176 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.754 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 3.653 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.57 UP 10 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.7420 UP 2 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.555 UP 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.231 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.774 UP 3 BASIS PTS.

2a New York OPENING REPORT

Futures Flat Ahead Of Fed’s Favorite Inflation Indicator

Friday, Sep 26, 2025 – 08:25 AM

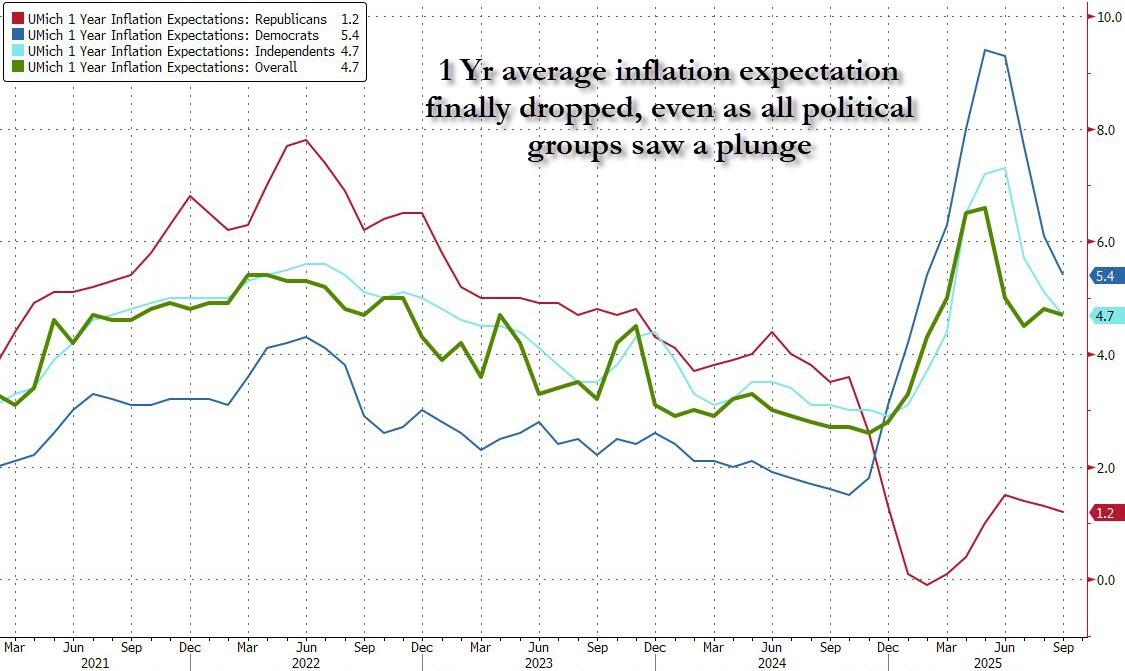

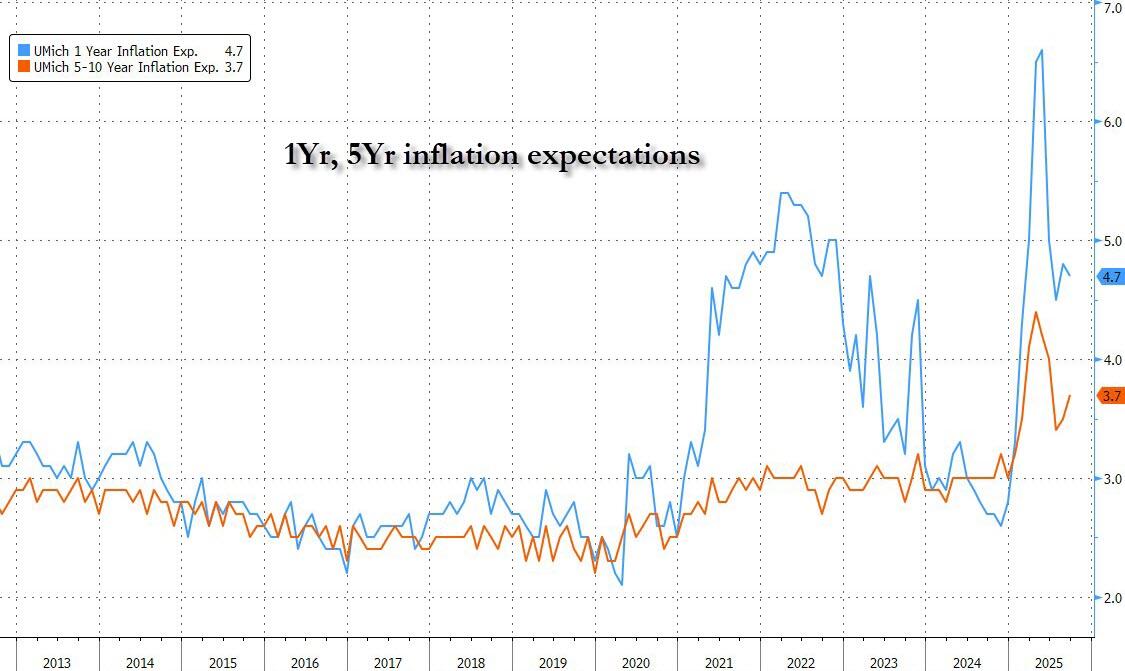

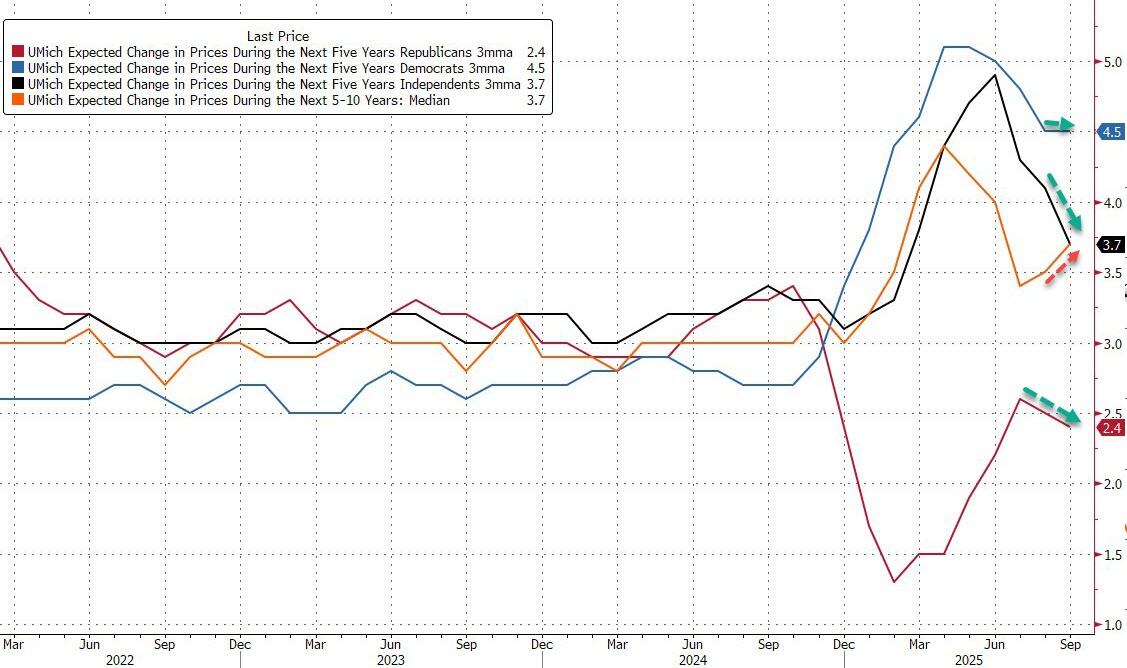

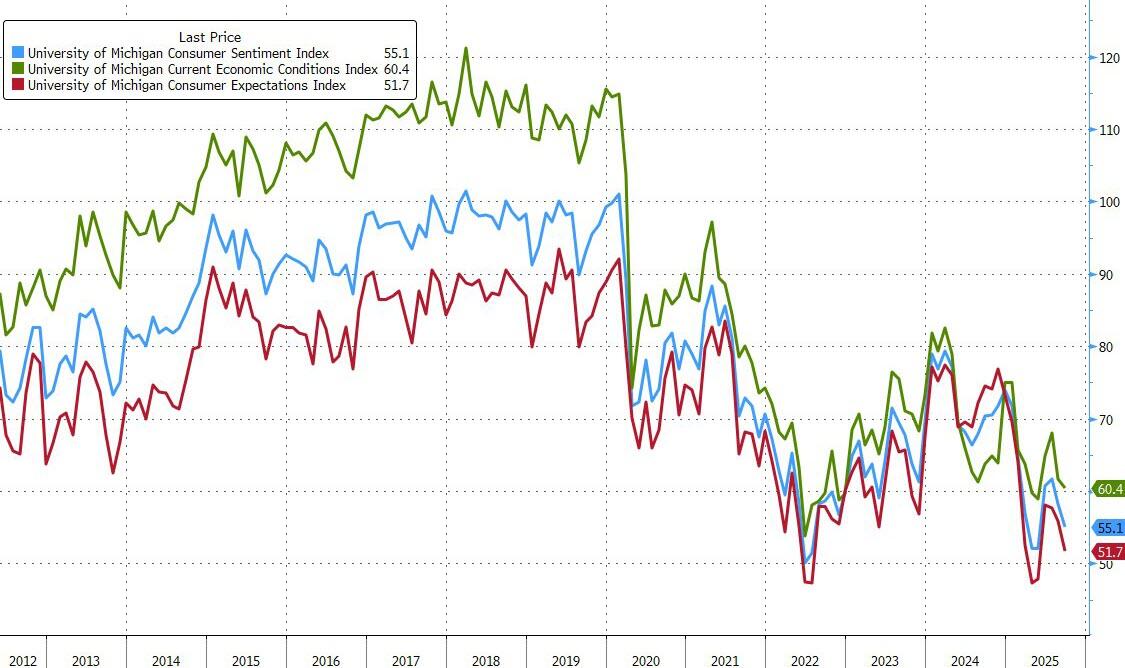

US equity futures are flat as the market struggled for traction ahead of today’s core PCE report and as investors ponder the Fed’s next policy move following a raft of much stronger than expected US data. As of 8:00am, S&P futures are unchanged while Nasdaq futures drop 0.1% leaving stocks poised to extend their recent run of losses once the cash market reopens; in premarket trading Mag 7 names are mixed with NVDA (-0.8%) being the largest underperformer. Bond yields are also flat as is the USD which set for its biggest weekly advance since the start of August. Brent crude reversed an earlier drop and was trading at session highs not far from $70. Overnight, the biggest headline was a series of 232 tariffs announced by Trump, including 100% on branded pharma, 50% on housing products, 30% on furniture and 25% on heavy trucks, which sent truckmaker PACCAR up more than 5%, while shares in several European peers dropped. However, the details on the pharma tariff suggest easier conditions on the exemptions. WSJ also released an article suggesting the possible chips tariff from the White House to boost domestic production. Today’s economic data slate includes August personal income and spending, the PCE price index (8:30am), the final U. of Michigan sentiment and inflation expectations (10am), Kansas City Fed services activity and Bloomberg US economic survey (11am).

In premarket trading, Mag 7 stocks are mixed (Amazon +0.3%, Microsoft +0.5%, Alphabet +0.3%, Meta Platforms -0.08%, Apple -0.9%, Tesla +0.4%, Nvidia -0.5%).

- Drugmakers are inching higher after President Donald Trump announced a plan to impose a 100% tariff on branded and patented drug imports and included exemptions for companies with US manufacturing. Citi says the news “lifts a significant overhang, as political uncertainties have kept investor interest at bay for most of this year.” Eli Lilly & Co (LLY) +1%, Merck (MRK) +1.2%.

- Apellis Pharmaceuticals (APLS) falls 6.2% as Goldman Sachs cuts its rating on the clinical-stage biopharmaceutical company to sell.

- Concentrix (CNXC) slumps 21% after the call-center operator gave a fourth-quarter profit outlook below consensus estimates.

- Harrow (HROW) rises 1.6% after entering into an agreement to acquire Melt Pharmaceuticals Inc.

- Intel (INTC) climbs 4% and GlobalFoundries (GFS) gains 9% after the Wall Street Journal reported that the Trump administration is weighing a new plan to reduce US reliance on chips made overseas.

- Paccar (PCAR) gains 6% as Trump sets a 25% tariff rate on heavy trucks made outside of the US.

- Wayfair

declines 2% after President Trump announced new industry-specific tariffs targeting heavy trucks, kitchen cabinets, bathroom vanities, and upholstered furniture.

declines 2% after President Trump announced new industry-specific tariffs targeting heavy trucks, kitchen cabinets, bathroom vanities, and upholstered furniture.

After a $15 trillion rebound in global equities from April’s lows, traders now face a wall of uncertainty as tariff headlines return to unsettle markets and investors fret about inflated valuations for big tech companies. Fed policy, the upcoming earnings season, and the threat of a US government shutdown are also weighing on sentiment. Attention now turns to Friday’s inflation report and key monthly jobs data next week.

“Excitement on AI and Fed rate cuts turbo-charged the bull market and sent global and US equities to new highs,” Barclays Plc strategists led by Emmanuel Cau wrote in a note. “But with much of the Goldilocks narrative arguably in the price now, and positioning higher, investor fatigue is palpable as we hit an air pocket ahead of next week’s non-farm payrolls report and third-quarter earnings.”

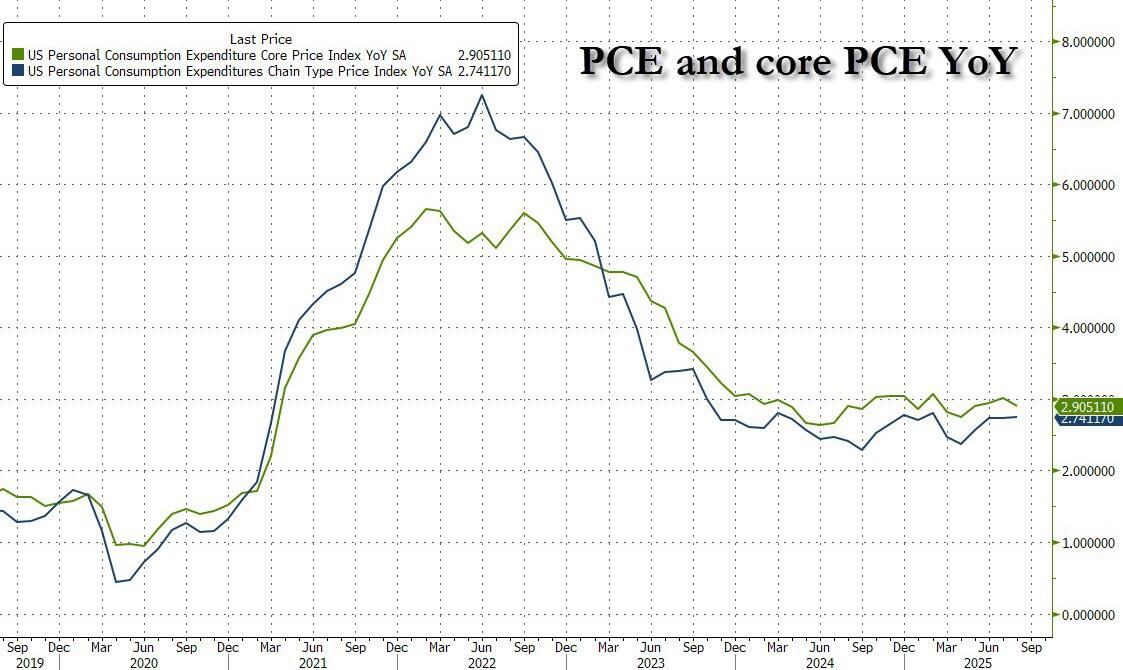

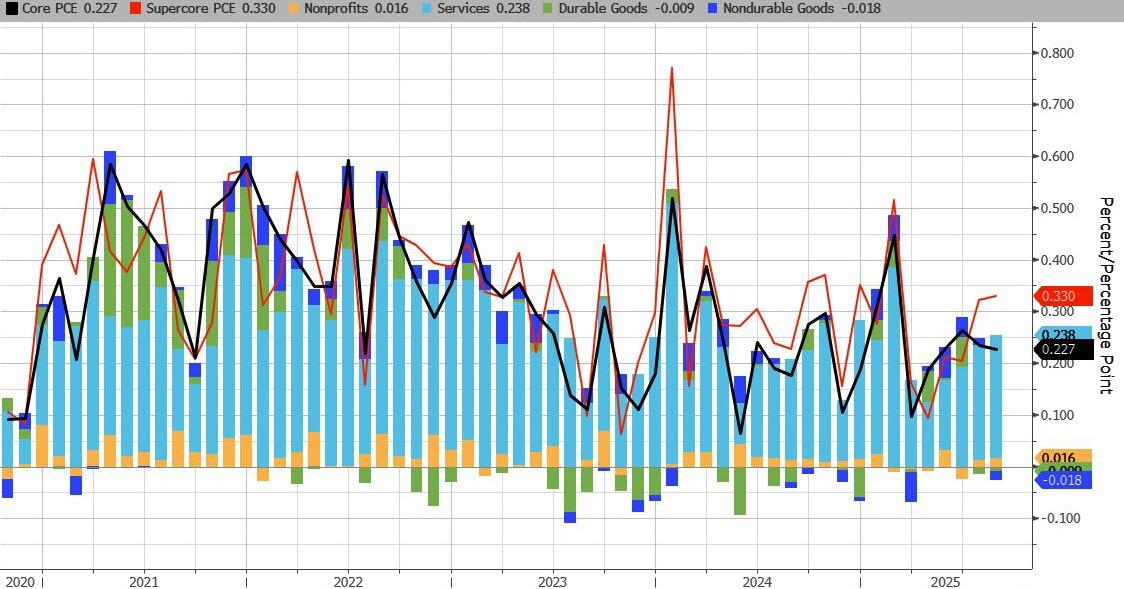

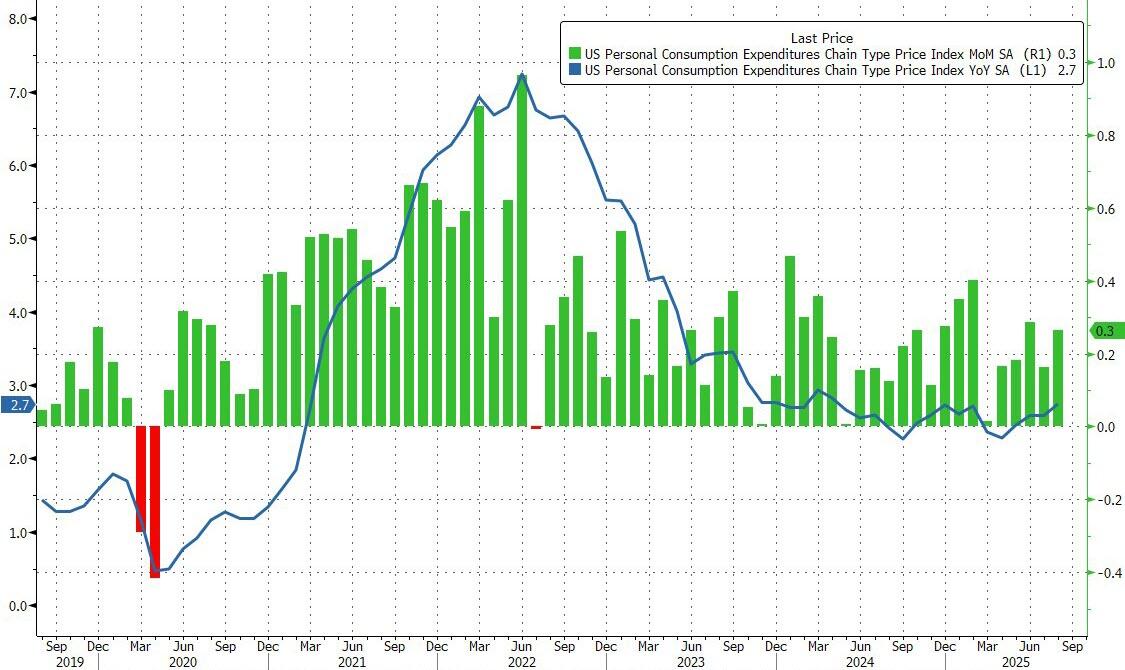

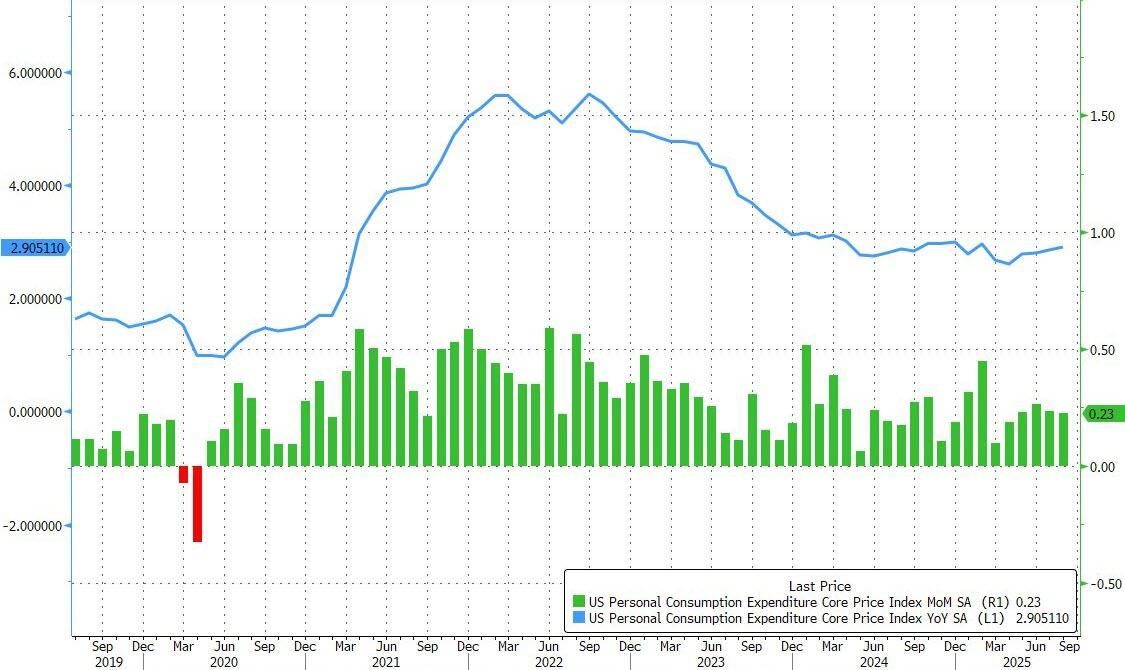

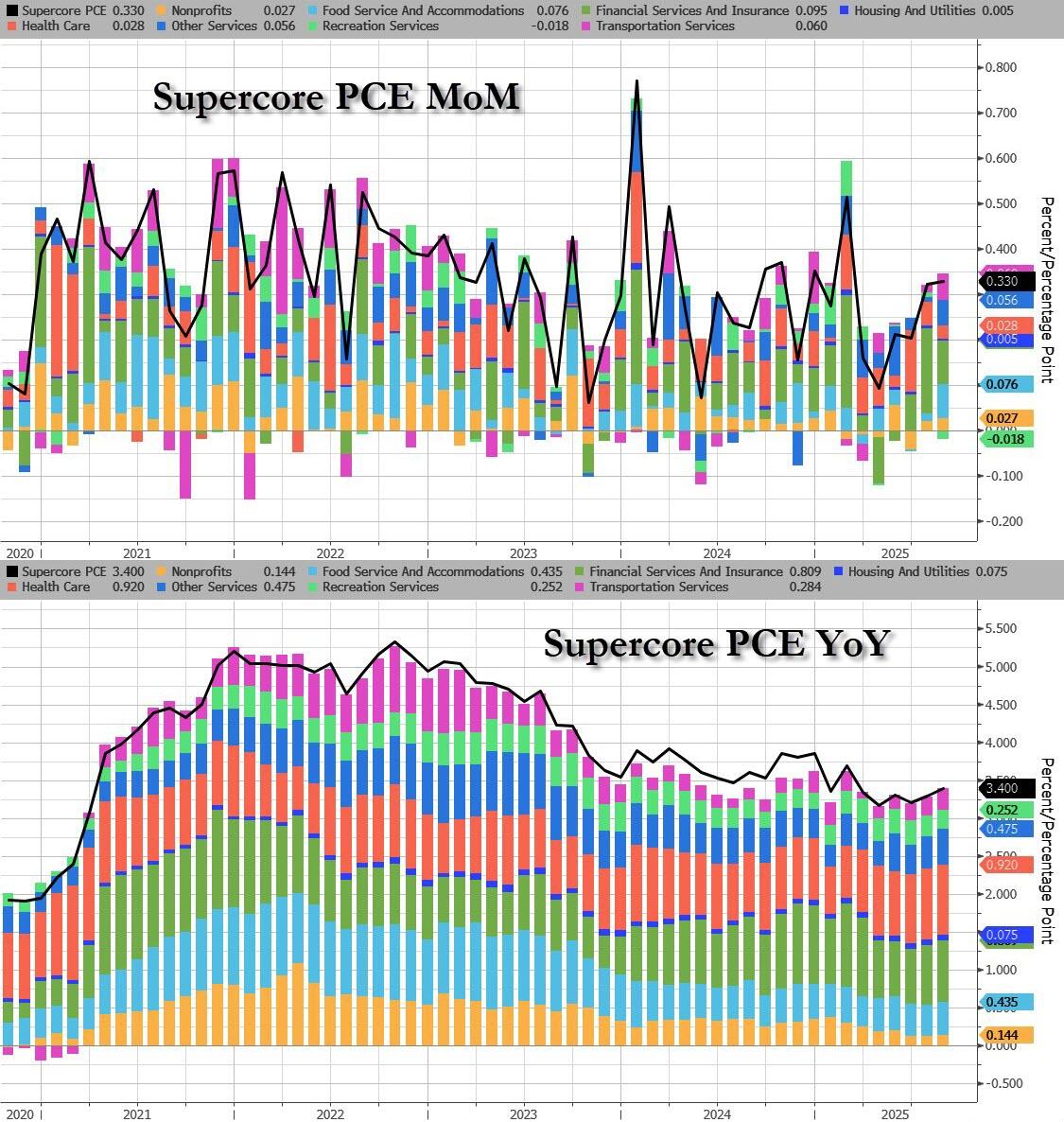

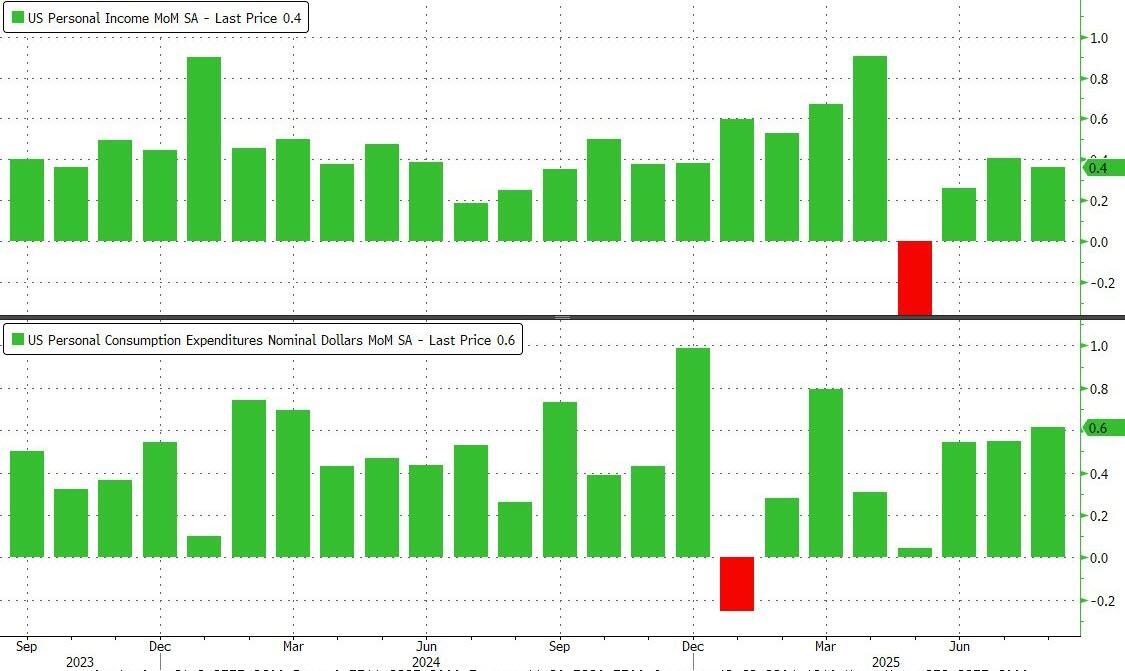

There shouldn’t be any big surprises in today’s core PCE print: economists are predicting core PCE rose 2.9% y/y in August, the same pace as the previous month. Goldman estimates that “both personal income and personal spending increased by 0.4% in August. We estimate that the core PCE price index rose 0.21% in August, corresponding to a year-over-year rate of +2.92%. Additionally, we expect that the headline PCE price index increased 0.25% in August, or increased 2.72% from a year earlier.“

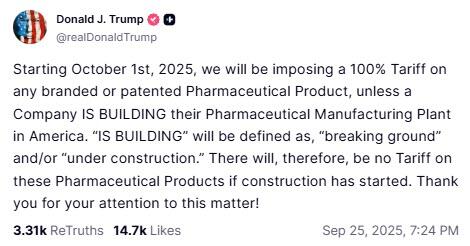

Truckmaker PACCAR Inc. climbed more than 5% in premarket trading after President Donald Trump levied new tariffs on imports of heavy vehicles. Shares in several European peers dropped. However, market expectations for the real-world impact of a 100% product-based drug tariff remain low, given the large spending commitments already made by large-cap pharma over the next five years (AZN $50 bn, ROG $50 bn, GSK $30 bn, NOVN $23 bn, UCB $2 bn, SAN $20 bn). In some respects, this could be seen as a positive if there is a line in the sand over Section 232, particularly given the exemptions many products could see.

Europe’s Stoxx Europe 600 index edged higher by 0.3% as investors look past President Trump’s latest tariff announcements (including a 100% duty on branded or patented pharmaceuticals starting Oct. 1), but is still set for back-to-back weekly declines for the first time since June. Daimler Truck Holdings AG and Volkswagen AG’s Traton SE declined, while Sweden’s Volvo AB, which manufactures trucks in the US, gained. Healthcare stocks underperformed following new US duties on pharmaceutical products. Here are the biggest movers Friday:

- Noba Bank jumps as much as 30% from its SEK70 offer price as the Swedish financial services firm’s shares began trading in Stockholm on Friday, opening at SEK84.9 and trading as high as SEK90.9

- EssilorLuxottica gains as much as 2.1% after its Stellest eyeglass lenses receive FDA marketing authorization for myopia correction. RBC highlights that this becomes the first and only spectacle lens of this type to be approved

- ArcelorMittal rises as much as 5% in Amsterdam trading, hitting the highest level since March. Traders cite a report in German business daily Handelsblatt that the EU Commission plans to impose tariffs in the next few weeks

- Gulf Keystone Petroleum rises as much as 8.4% on confirmation that oil exports from the Kurdistan region of Iraq will resume soon

- InterContinental Hotels shares climb as much as 3.4% after the firm receives a double upgrade to overweight at JPMorgan, which highlights its earnings visibility “in times of RevPAR uncertainty”

- Most European Big Pharma stocks were broadly flat on Friday morning after US President Donald Trump announced a fresh round of tariffs, including a 100% duty on branded or patented pharmaceuticals starting Oct. 1

- Pennon Group falls as much as 2.3% as analysts say the water company’s guidance implies slightly slower FY earnings growth, with JPMorgan saying the update may result in some Ebitda downgrades

- Brunello Cucinelli shares extend Thursday’s plunge triggered by a report from Morpheus Research. The short seller alleged that the luxury company is misleading investors about its Russian business, claims the firm rejected

- Ceres falls as much as 16%, the most in over seven months, after the clean energy technology developer reported an operating loss of £18.7 million for the first half of the year

- Health care stocks did fall at the open but were quick to erase losses. Technology names underperform, as they did in Asia, after the Wall Street Journal reported the White House is weighing a plan to reduce semiconductor imports.

Asian stocks fell, with a key regional benchmark falling by the most in over three weeks, as chipmakers and Chinese tech shares pulled back after recent gains. The MSCI Asia Pacific Index fell 1%, with TSMC, Xiaomi and Alibaba among the biggest drags. Equities declined in South Korea, Hong Kong, mainland China, Taiwan and India. Health-care stocks slipped after US President Donald Trump unveiled 100% tariffs on branded or patented pharmaceutical products effective from Oct. 1. A gauge of Asian tech hardware stocks followed US peers lower amid valuation concerns after recent rallies. Korea’s Kospi fell more than 2%, the most in nearly two months, as foreigners sold chip shares. The Hang Seng Tech Index dropped by a similar measure, its worst decline since May. India’s Nifty 50 declined for a sixth-straight session, poised for its longest losing streak since March.

In FX, the Bloomberg Dollar Spot Index falls 0.1% with muted price action across the G-10 complex. The dollar is on track for its best week since early August as a run of data showing resilience in the US economy forced traders to reassess the Federal Reserve’s scope for cuts

In rates, treasuries are a touch stronger with yields richer on the day, although remain within a basis point of Thursday’s close, after trading in a narrow range overnight with modest selling flows in the long end. Treasury 10-year yields remain near Thursday’s closing levels, trading at around 4.17% with European bonds slightly firmer over the early London session. European government bonds edge higher.

In commodities, WTI crude futures are little changed near $65 a barrel. Gold is unchanged around $3,748/oz. Bitcoin is flat around $109,000.

Looking at today’s calendar, US economic data slate includes August personal income and spending, the PCE price index (8:30am) U. of Michigan sentiment and inflation expectations (10am), Kansas City Fed services activity and Bloomberg US economic survey (11am). Fed speaker slate includes Barkin at 9am, delivering keynote remarks on the outlook for the economy, followed by a Q&A. Bowman at 1pm discussing the monetary policy with Q&A.

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini -0.1%

- Russell 2000 mini -0.2%

- Stoxx Europe 600 +0.2%

- DAX +0.3%

- CAC 40 +0.4%

- 10-year Treasury yield little changed at 4.17%

- VIX +0.2 points at 16.95

- Bloomberg Dollar Index little changed at 1207.85

- euro little changed at $1.1677

- WTI crude -0.2% at $64.87/barrel

Top Overnight News

- David Einhorn warned that the trillion-dollar AI infrastructure spending spree — by companies such as Apple and OpenAI — may lead to “tremendous” capital destruction, even if the technology proves transformative. BBG

- Tech giants are on a debt-fueled AI spending spree, raising roughly $157 billion so far this year — up about 70% from the same period last year. Some worry the hype may be overblown, drawing parallels to the dot-com bubble. BBG

- The AI boom has ushered in one of the costliest building sprees in world history. Over the past three years, leading tech firms have committed more toward AI data centers, chips, and energy than it cost to build the interstate highway system over four decades, when adjusted for inflation. WSJ

- Trump announced that imported heavy trucks will be subject to a 25% levy, while kitchen cabinets and bathroom vanities will be hit with a 50% charge. BBG

- Trump said there could be a government shutdown; he also called on the Fed to lower rates again, saying the US is the only country where strong numbers are reported and stocks still go down.

- The Trump administration is weighing a new plan to reduce dramatically the U.S.’s reliance on semiconductors made overseas, hoping to spur domestic manufacturing and reshape global supply chains. The policy’s goal is to have chip companies manufacture the same number of semiconductors in the U.S. as their customers import from overseas producers, with companies who don’t maintain a 1:1 ratio paying a tariff. WSJ

- European Big Pharma shares held steady following Donald Trump’s threat to slap a 100% tariff on branded or patented drugs unless they invest in the US. Many European firms already have factories under construction, Panmure Liberum said. BBG

- Indonesia’s central bank said it is intervening “boldly” in financial markets to stabilize the rupiah as it falls toward a record low. BBG

- Japan’s Tokyo CPI comes in cooler than anticipated, with headline at +2.5% (vs. +2.5% in Aug and below the Street’s +2.8% forecast) and core at +2.5% (down from +3% in Aug and below the consensus estimate of +2.9%) BBG

- Meta is set to face a charge sheet from the EU for failing to adequately police illegal content, risking fines for violating the bloc’s content moderation rulebook: BBG

- Oracle, Silver Lake, and MGX will be the main investors in TikTok US with a combined 45% ownership: CNBC

- Meta is reportedly in talks with Alphabet’s Google to integrate Gemini for enhanced ad-targeting capabilities, according to The Information.

- Punchbowl surmises, on the US shutdown situation, that “with just four days until government funding runs out, both Republicans and Democrats seem unnaturally comfortable with their positions in the fight.”

Trade/Tariffs

- US President Trump said that as of October 1st, 2025, a 25% tariff will be imposed on all “Heavy Trucks” made in other parts of the world, according to Truth Social.

- US President Trump said that as of October 1st, 2025, the US will impose a 50% tariff on all kitchen cabinets, bathroom vanities, and associated products, and a 30% tariff on upholstered furniture, according to Truth Social.

- US President Trump said that as of October 1st, 2025, the US will impose a 100% tariff on any branded or patented pharmaceutical product unless the company is building its pharmaceutical manufacturing plant in America, according to Truth Social.

- The Trump administration is reportedly weighing a new plan to dramatically reduce the US’ reliance on semiconductors made overseas, according to WSJ sources. Companies that do not maintain a 1:1 ratio over time would have to pay a tariff, sources said.

US-China

- US President Trump signed an executive order on TikTok, saying he had good talks with Chinese President Xi and that China is fully on board. He noted that American investors will take over the platform, with TikTok investors to include Ellison, Michael Dell, and Rupert Murdoch. Trump said he is satisfied with security concerns, praised Xi’s approval, and highlighted that Oracle (ORCL) is playing a very big part, according to Reuters.

- US Vice President Vance said TikTok will be valued at around USD 14bln, adding that Americans will control the algorithm and that he wants it to be fair, according to Reuters.

- In a sign of the fragile engagement, people close to the White House said Trump has not committed to going to Beijing, with a firm date for the visit contingent on China’s continued cooperation on issues ranging from trade to fentanyl, according to WSJ.

- US Deputy Secretary of State confirmed a meeting with her Chinese counterpart took place on Thursday evening, according to Reuters.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly lower after being subdued for a bulk of the session following a similar performance stateside after hot US data, with traders now looking ahead to the Fed’s preferred gauge of inflation. Sentiment in the region was hampered by US President Trump announcing tariffs of 100% on pharmaceuticals, 50% on kitchen cabinets, bathroom vanities and associated products, 30% on upholstered furniture, and 25% on all heavy trucks made outside the US. ASX 200 eventually eked out mild gains, but the healthcare sector was the biggest laggard after Trump’s 100% tariff announcement on pharmaceuticals. Tech also weakened, though losses were cushioned by outperformance in metals and mining. Nikkei 225 was modestly softer but held above the 45,500 level after briefly dipping below, with pharma stocks weighing following Trump’s tariff announcement, and with little follow-through from softer-than-expected but prior-matching Tokyo CPI data. Hang Seng and Shanghai Comp largely conformed to regional losses, with little follow-through from Trump signing the executive order on TikTok, in which he also noted he had good talks with Chinese President Xi, although the Mainland later oscillated on either side of the unchanged mark. KOSPI was the regional laggard, heavily pressured by the tech sector and pharma, whilst reports also suggested South Korea fired warning shots at a North Korean commercial vessel for crossing the maritime border, according to Yonhap. Nifty 50 was also subdued with the nation’s pharma stocks pressured after President Trump’s tariff announcement.

Top Asian News

- Japanese government revised July real wages to -0.2% vs preliminary estimate of +0.5%, according to Reuters.

- Japanese Finance Minister Kato said he will not comment on FX levels, according to Reuters.

- India’s government has drafted a proposal to relax foreign investment rules for e-commerce exports, according to Reuters.

- PBoC injected CNY 165.8bln via 7-day reverse repos with the rate at 1.40%; injected CNY 400bln via 14-day reverse repo.

European bourses (STOXX 600 +0.2%) are modestly firmer across the board and have traded with a slight upward bias throughout the morning. The region has seemingly shrugged off the latest barrage of tariff levies announced by Trump, but with some analysts suggesting that the pharma-specific ones are not as bad as feared. European sectors hold a strong positive bias, with only a couple of sectors marginally lower. Most of the focus this morning has been on the latest Trump tariffs, where he announced 100% tariffs on Pharma, 50% on kitchen cabinets, and 25% on heavy trucks.”; for the latter, Daimler Truck (-2.5%) moves lower, whilst Volvo (+3%) remains in the green. Bernstein writes that Daimler Truck could be most affected by these tariffs, given its high exposure to the US; analysts add that Paccar (+5% pre-market) stands to benefit the most. Delving into the pharma tariffs, some analysts have suggested the announcement may actually provide some relief for traders; focus is on the caveat that a Co. will not be subject to the tariff rate if they are building a pharma plant in the US. So, whilst the sector was initially underperforming, some heavyweights have managed to climb out of negative territory – namely those which have already announced plans for plants in the US; Roche (+0.2%), AstraZeneca (U/C). Jefferies writes that “overall, we think this is a win for Pharma and shouldn’t have a material impact”. In US pre-market trade, the likes of Eli Lilly (+1.7%) and Viking (+1.4%) both move higher.

Top European News

- Italy’s Economy Minister said the digital euro plan will take two years to be implemented, according to Reuters.

- Volkswagen (VOW3 GY) cut output and paused production at its German EV plants, according to Bloomberg.

- French PM Lecornu’s interview is now expected to be published within Saturday’s edition of Le Parisien, via Politico; delayed due to an editorial strike.

- ECB SCE: 1yr and 5yr inflation forecasts rise. Inflation: 1yr: 2.8% (prev. 2.6%) 3yr: 2.5% (prev. 2.5%). 5yr: 2.2% (prev. 2.1%) Growth 1yr: -1.2% (prev. -1.2%).

FX

- After two sessions of solid gains for DXY, the rally has paused for breath. Whilst the price action on Wednesday left many desks scratching their heads, yesterday’s upside was clearly driven by US data; Q2 GDP, weekly claims and durables. ING adds that the surge in the USD has likely also been assisted by positioning. The next potential inflection point for the USD comes via today’s PCE data with Y/Y core PCE expected to hold steady at 2.9% (a view backed by Powell earlier this week) and the M/M rate seen declining to 0.2% from 0.3%. Tariff headlines have re-emerged over the past 24 hours with focus on pharma, furniture and several other sectors. However, the vague language around the pharma actions has seen equity indices take the news in their stride. DXY has ventured as high as 98.53 but has been unable to test Thursday’s best at 98.60.

- EUR is a touch firmer vs. the USD after a couple of bruising sessions, which have seen the pair pull back from a 1.1820 peak on Wednesday to a 1.1645 low yesterday. Price action has largely been driven by the USD rather than anything EUR-specific. This morning’s ECB SCE saw little follow-through into EUR, with the report seeing a 20bps pick-up in the 1yr inflation forecast to 2.8% and the 5yr projection rise to 2.2% from 2.1%. EUR/USD inched above its 50DMA at 1.1679.