XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

072 C GOLDMAN 22

072 H GOLDMAN 5

092 C DEUTSCHE BANK 997

118 C MACQUARIE FUTURES US 346

118 H MACQUARIE FUTURES US 2446

132 C SG AMERICAS 92

167 H MAREX 18

190 H BMO CAPITAL MARKETS 7740

323 C HSBC 1338 183

332 H STANDARD CHARTERED B 1399

363 H WELLS FARGO SECURITI 122

435 H SCOTIA CAPITAL (USA) 3045

555 C BNP PARIBAS SEC CORP 224

624 C BOFA SECURITIES 6

657 C MORGAN STANLEY 3

657 H MORGAN STANLEY 816

661 C JP MORGAN SECURITIES 11656 10107

686 C STONEX FINANCIAL INC 112

690 C ABN AMRO CLR USA LLC 43

709 C BARCLAYS 283

732 C RBC CAP MARKETS 172

732 H RBC CAP MARKETS 707

DLV615-T CME CLEARING

BUSINESS DATE: 09/29/2025 DAILY DELIVERY NOTICES RUN DATE: 09/29/2025

PRODUCT GROUP: METALS RUN TIME: 22:02:03

880 C CITIGROUP 200 115

880 H CITIGROUP 300

905 C ADM 18 1

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 21,258 CONTRACTs NOTICES FOR 2,125,088 OZ or 66.121 TONNES

total notices so far: 21258 contracts for 2,125,800 OR 66.121 tonnes)

SILVER NOTICES: 11 NOTICE(S) FILED FOR 0.055 MILLION OZ/

total number of notices filed so far this month : 11 CONTRACTS (NOTICES) for 0.055 million oz

INITIAL STANDING FOR OCT: 13.240 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 13.240 MILLION OZ OF NORMAL DELIVERY

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.164 TONNES OF INITIAL GOLD STANDING PLUS 1.555 TONNES OF OUR FIRST ISSUANCE EXCHANGE FOR RISK//NEW TOTALS 91.719 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT.

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 3469 CONTRACTS OI TO 166,174 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1040 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1040 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 640 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3132 CONTRACTS AND ADD TO THE 1040 E.FP. ISSUED

WE OBTAIN A MEGA MEGA HUGE SIZED LOSS OF 2429 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $0.37 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 12.145 MILLION PAPER OZ

OCCURRED WITH OUR GAIN $0.37 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

//Hang Seng CLOSED UP 232.68 PTS OR 0.87%

// Nikkei CLOSED : DOWN 111.12PTS OR 0.25% //Australia’s all ordinaries CLOSED DOWN 0.14%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1196 OFFSHORE CLOSED UP AT 7.1276/ Oil DOWN TO 62.80 dollars per barrel for WTI and BRENT UP TO 66.43 Stocks in Europe OPENED MOSTLY RED

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 4108 CONTRACTS TO 517,465 OI WITH OUR GAIN IN PRICE OF $48.65 WITH RESPECT TO MONDAY’S // TRADING COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3200). WE HAD LITTLE T.A.S. LIQUIDATION MONDAY(AS WE ARE IN OPTIONS EXPIRY WEEK FOR SEPT.) WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 7308 CONTRACTS (OR 22.73 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD A HUGE 510 CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 51,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS ISSUED ON FIRST DAY NOTICE AND THAT IS QUITE UNUSUAL FOR THEM BUT THE CENTRAL BANK OF ENGLAND MUST BE DESPERATE!!

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER:

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE FOR 510 CONTRACTS OR 51,000 OZ /1.555 TONNES OF GOLD!!

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 510 CONTRACTS FOR 51,000 OZ OR 1.555 TONNES OF GOLD.

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 118 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 118 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN DECEMBER 2024.

DETAILS ON OCTOBER COMEX MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 7308 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 1.5% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER/OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1393 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN THIS PAST WEDNESDAY WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSES TO BUCKLE!! THIS LEADS US TO TODAY, FIRST DAY NOTICE AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORTED PAPER ISSUANCE

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH PREVIOUS AUGUST AND SEPTEMBER MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS NOW BRINGS US TO OCTOBER WHERE INITIAL AMOUNT OF GOLD STANDING IS 28,988 CONTRACTS FOR 90.114 TONNES OF GOLD AND THIS WAS AUGMENTED BY AN UNUSUAL 51000 CONTRACT EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE//THUS TOTAL AMOUNT STANDING ON GOLD INITIAL EQUATES TO91,719 TONNES!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 242 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH OCTOBER AND SUBSEQUENT STANDING FOR GOLD.

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.4883 TONNES QUEUE JUMP AND 2.827 TONNES EXCHANGE FOR RISK TODAY// NEW TOTALS OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) 2.827 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY // =//TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) 0.4883 TONNES TODAY QUEUE JUMP//NORMAL DELIVERY OF 25.878 TONNES

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR INITIAL 51,000 OZ OR 1.555 TONNES OF EX FOR RISK TOTALS 91.719 TONNES

I.E.

a) INITIAL STANDING 91=0.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 510 CONTRACTS FOR 51,000 OZ OR 1.555 TONNES

EQUALS

91.719 TONNES OF GOLD!!

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3200 EFP CONTRACT WAS ISSUED: : /DEC 3200 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3200 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- LITTLE LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY AND THIS HAD NO EFFECT ON OUR TOTAL OPEN INTEREST AS IT ACTUALLY ROSE HUGELY!!

- MONTH END SPREADERS HAVE NOW COME IN THE PICTURE AND IT SURELY LOOKS LIKE THERE WILL BE DAMAGE TO THE PRICE OF GOLD AS A RAID WAS CALLED ON THIS LAST DAY OF OPTIONS EXPIRY

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED SIZED 1393 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S FIRST INITIAL ISSUANCE FOR EXCHANGE FOR RISK OF 510 CONTRACTS OR 51,000 OZ OR 1.555 TONES OF GOLD.

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP OF .4883 TONNES) +2.827 TONNES EX FOR RISK TODAY//

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY OUR INITIAL 1.555 TONNES OF GOLD EX FOR RISK/TOTALS 91.164 TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $48.65./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION MONDAY. MUCH OF THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO VERY LITTLE SPREADER LIQUIDATION BUT MOSTLY SPECULATIVE LONGS PILING INTO COMEX GOLD TRADING. THIS WAS COUPLED WITH GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION) /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS ARE TRYING AGAIN TODAY ON THIS LAST DAY OF SEPT. OPTIONS EXPIRY WEEK AND LET US HOPE THEY FAIL LIKE THEY DID IN AUGUST. COMEX EXPIRY IS CONCLUDED YESTERDAY, SEPT 25 AND LBMA LONDON EXPIRY IS FINISHING TODAY TUESDAY SEPT 30.

SATURDAY MORNING//FRIDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 22.73 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES AND THIS WAS COUPLED STRANGELY WITH OUR INITIAL 51,000 OZ EXCHANGE FOR RISK ISSUANCE//1.555 TONNES/NEW TOTAL INITIAL STANDING FOR OCTOBER: 91.719 TONNES

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $48.65

WE HAD A STRONG 705 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL. THIS IS THE HIGHEST EVER RECORDED REMOVAL OF CONTRACTS PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 7308 CONTRACTS OR 730800 0Z (22.73TONNES)

confirmed volume MONDAY 281,594 contracts// fair//

speculators have left the gold arena

INITIAL GOLD COMEX

OCT CONTRACT MONTH

SEPT 30 /2025

FIRST DAY NOTICE

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entries . |

| Deposit to the Dealer Inventory in oz | 2 ENTRIES i) Into Asahi dealer 32,013.863 oz ii) Into Stonex Delaer 64,460.940 oz (2005 kilobars) total deposit dealer: 96,474.803 oz (3.000 tonnes) |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRIES i) Into Brinks customer account: 1800.286 oz (56 kilobars) total deposit 1800.286 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 21,258 notice(s) 2,125,800 OZ 66. 121TONNES |

| No of oz to be served (notices) | 7730 contracts 773,000OZ 24.044 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,258 notices 2,125,800 oz 66.121 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 2

2 ENTRIES

i) Into Asahi dealer 32,013.863 oz

ii) Into Stonex Delaer 64,460.940 oz

(2005 kilobars)

total deposit dealer: 96,474.803 oz

(3.000 tonnes)

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRIES

i) Into Brinks customer account: 1800.286 oz

(56 kilobars)

total deposit 1800.286 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

ADJUSTMENTs 4

customer to dealer

a) Asahi 15,804.629 oz

b) Manfra: 44,947.098 oz

dealer to customer:

c) Brinks 39,487..630 oz

d) JPMorgan 5993.536

volume at the comex: MONDAY: 281,594 oz (FAIR)

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF OCTOBER STANDS AT 28,988 CONTRACTS FOR A LOSS OF 1559 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF GOLD STANDING FOR OCTOBER, A NORMALLY POOR DELIVERY MONTH IS AS FOLLOWS:

28,988 NOTICES FILED X 100 OZ PER NOTICE

EQUALS

2,898,800 OZ

OR

90.164 TONNES

TO WHICH WE ADD 1.555 TONNES OF GOLD/EXCHANGE FOR RISK

EQUATES TO

91.719 TONNES OF GOLD!!

NOVEMBER GAINED 7 CONTRACTS UP TO 4434 CONTRACTS.

DECEMBER GAINED 2987 CONTRACTS UP TO 406,043 CONTRACTS.

We had 21,258 contracts filed for today representing 2,125,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 11,656 notices issued from their client or customer account. The total of all issuance by all participants equate to21,258 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 10,107 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (21,258 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 28,988 CONTRACTS) minus the number of notices served upon today (21,258 x 100 oz per contract) equals 2,898,800 OZ OR 90.164 TONNES OF GOLD TO WHICH WE ADD OUR INITIAL 1.555 TONNES OF EXCHANGE FOR RISK//NEW TOTALS STANDING FOR GOLD OCTOBER EQUATES TO 91.719 TONNES

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (21,258 x 100 oz +we add the difference for front month of SEPT. (28,988 OI} minus the number of notices served upon today (21,258 x 100 oz) which equals 2,898,000 OZ OR 90.164 TONNES + 1.555 TONNES EXCHANGE FOR RISK//NEW TOTALS; 91.719 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 91.164 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,023,569.112 oz 62.94 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 40,044.675.826 oz

TOTAL REGISTERED GOLD 21,973,518.934 or 683.468 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,071,156.892 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,949,949oz ((REG GOLD- PLEDGED GOLD)= 620.527 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

SEPT 30 2025

INITIAL/FIRST DAY NOTICE:

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries a) Out of Asahi 598,453.800 oz b) Brinks 1200,282.07 oz c) CNT 599,494.830 oz total withdrawal: 2,398,731.250 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 entry i) Into Asahi: 1,114,342.000 oz total deposit: 1,114,342.000 oz |

| No of oz served today (contracts) | 11 CONTRACT(S) ( 55,000 OZ |

| No of oz to be served (notices) | 2637 contracts (13.185 MILLION oz) |

| Total monthly oz silver served (contracts) | 11 Contracts (55,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 entry

i) Into Asahi: 1,114,342.000 oz

total deposit: 1,114,342.000 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 entries

a) Out of Asahi 598,453.800 oz

b) Brinks 1200,282.07 oz

c) CNT 599,494.830 oz

total withdrawal: 2,398,731.250 oz

adjustments: all dealer to customer

2 adjustments//customer to dealer accounts

a) Brinks 422,869.800 oz

b) CNT 1,642,121.501 oz

TOTAL REGISTERED SILVER: 193.502 MILLION OZ//.TOTAL REG + ELIGIBLE. 530.200 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 2648 OPEN INTEREST CONTRACTS FOR A LOSS OF 198 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING IN THIS NON ACTIVE DELIVERY MONTH OF OCTOBER IS AS FOLLOWS

2648 CONTRACTS X 5000 OZ PER CONTRACT

EQUASL 13.240 MILLION OZ WHICH IS PRETTY GOOD FOR A NON ACTIVE DELIVERY MONTH.

STANDING FOR SILVER OCT: 13.240 MILLION OZ

NOVEMBER LOST 54 CONTRACTS UP TO 789.

DECEMBER LOST 3551 CONTRACTS DOWN TO 133,005

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 11 or 55,000 oz

CONFIRMED volume; ON MONDAY 121,352 huge//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 11 X5,000 oz = 0.055MILLION oz

to which we add the difference between the open interest for the front month of OCT (2648) AND the number of notices served upon today (11 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (11) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(2648) minus number of notices served upon today (11)x 5000 oz equals silver standing for the OCT.contract month equating to 13.240 MILLION OZ

New total standing: 13.240 million oz which is STILL HUGE for this NON active delivery month of OCT. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 193.502 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/530.200million. 39.75%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

GLD INVENTORY: 1011.73 TONNES, TONIGHTS TOTAL

SILVER

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

CLOSING INVENTORY 499.023 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

JAMES RICKARDS

FRANK HOLMES

He Nailed $4,000 Gold Call, Now He Says $7,000 Gold, $100 Silver Are Next

![]()

by ITM Trading

Monday, Sep 29, 2025 – 19:03

Gold at $7,000, silver at $100—Frank Holmes isn’t pulling punches. The U.S. Global Investors CEO, who called $4,000 gold back in 2020, warns that the world teeters on the edge of monetary and geopolitical chaos. Exploding global debt, record military spending, and a Fed trapped between inflation and recession are fueling the perfect storm for precious metals.

Cyberattacks, fracturing alliances, and the rise of “sovereign data” signal a new era of protectionism. In this climate, fiat currency is vulnerable, and hard assets—gold and silver—stand as the ultimate hedge against devaluation, systemic risk, and a crumbling financial order.

Follow Daniela on X: Daniela Cambone

About ITM Trading: ITM Trading has been a trusted leader in precious metals for over 28 years, helping clients protect and grow their wealth with custom gold and silver strategies designed for economic downturns and currency resets.

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 242/ROBERT KIENTZ

5. COMMODITY REPORT GOLD

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 20,25 PTS OR 0.52%

//Hang Seng CLOSED UP 232.68 PTS OR 0.87%

// Nikkei CLOSED : DOWN 111.12PTS OR 0.25% //Australia’s all ordinaries CLOSED DOWN 0.14%

//Chinese yuan (ONSHORE) CLOSED DOWN AT 7.1196 OFFSHORE CLOSED UP AT 7.1276/ Oil DOWN TO 62.80 dollars per barrel for WTI and BRENT UP TO 66.43 Stocks in Europe OPENED MOSTLY RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN DOWN IN TRADING AT 7.1196 AND WEAKER//OFF SHORE YUAN TRADING DOWN TO 7.1276 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1196

OFFSHORE YUAN: DOWN TO 7.1276

HANG SENG CLOSED UP 232.68 PTS OR 0.87%

2. Nikkei closed DOWN 111.12 PTS OR 0.25%

3. Europe stocks SO FAR: ALL RED EXCEPT SPAIN

USA dollar INDEX DOWN TO 97.46 EURO RISES TO 1.1746 UP 16 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.652//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.36…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.141 UP 2 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7076Italian 10 Yr bond yield DOWN to 3.563 SPAIN 10 YR BOND YIELD DOWN TO 3.257

3i Greek 10 year bond yield DOWN TO 3.402

3j Gold at $3809.90 Silver at: 46.20 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 71 /100 roubles/dollar; ROUBLE AT 82.36

3m oil (WTI) into the 62 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.96/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.652% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.141 UP 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7959 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9327 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.130 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.7045 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.610 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.59 UP 1 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.7040 DOWN 1 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.510 DOWN 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.185 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.749 DOWN 1 BASIS PTS.

2a New York OPENING REPORT

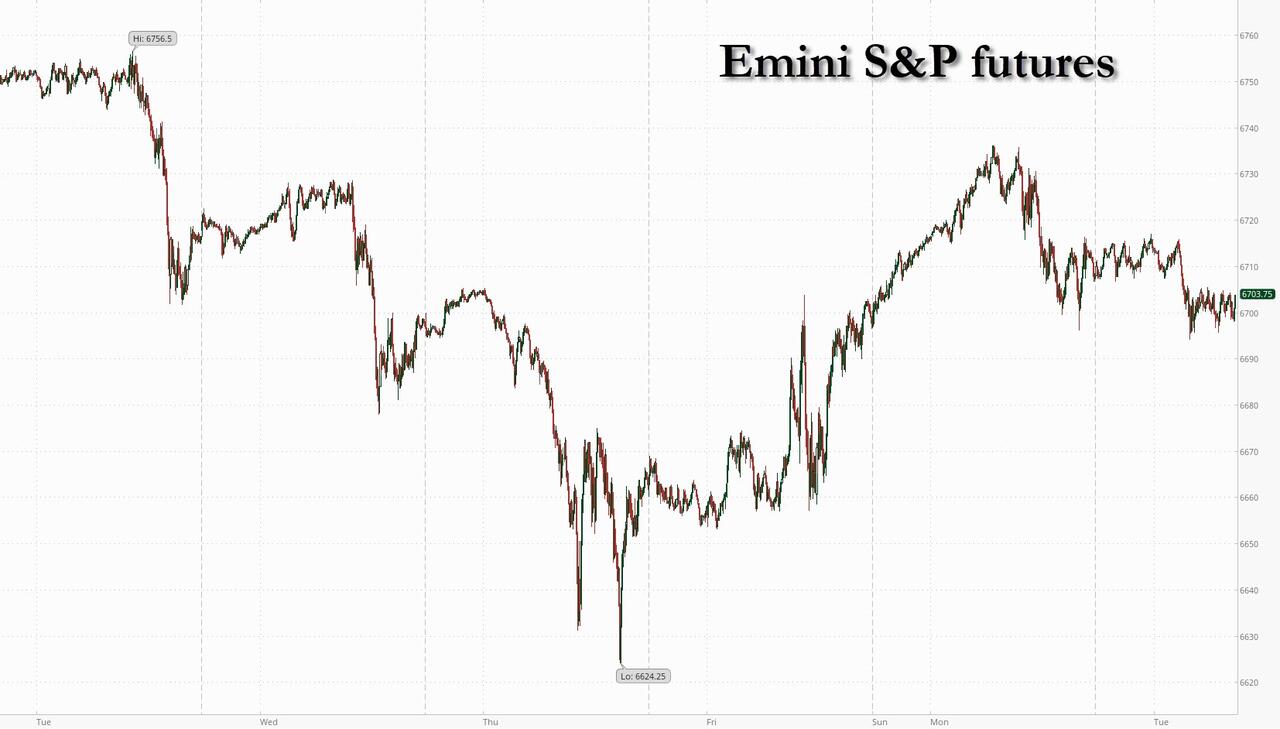

Futures, Gold Drop With Hours Left Until US Government Shutdown

Tuesday, Sep 30, 2025 – 08:35 AM

Futures are lower as we close out the quarter/month, ahead of what is a most likely (80% odds on Polymarket) government shutdown. As of 8:00am ET, S&P and Nasdaq futures are down 0.2% as sentiment sours after Monday’s optimism. Still, on the final trading day of the month, the S&P 500 is on track for its best September since 2010. Pre-market, Mag7 are all lower with Semis mixed; Defensives seeing outperformance relative to Cyclicals. Within commodities, virtually everything is lower ex-nat gas; gold/silver are down 86 and 196bps, respectively, on what looks like profit-taking / rebalancing with crude lower on potential increased OPEC+ supply. Bond yields are lower as the curve bull steepens; the USD is weaker, sitting ~1% above its 52-wk low. Gold fell toward $3,800 an ounce after touching a fresh all-time high earlier Tuesday just shy of $3900. After surging more than 10% this month on optimism over US interest rate cuts and haven demand, traders speculated that Chinese investors pared exposure ahead of the Golden Week holiday. Late on Monday, Trump set 10% tariffs on timber and 25% on kitchen cabinets as of Oct 14. Today’s macro data focus is JOLTS, Consumer Confidence, Housing Price Indices, and regional activity indicators. Expect headlines on the shutdown through the day, which most traders do not expect having a material impact on markets.

In premarket trading, Mag 7 stocks are mostly lower (Amazon -0.02%, Meta -0.1%, Nvidia +0.2%, Alphabet -0.1%, Microsoft -0.2%, Apple -0.3%, Tesla -0.7%).

- Celsius Holdings (CELH) rises 3% after Morgan Stanley upgraded the energy-drink maker to overweight from equal-weight, citing topline growth ahead.

- EchoStar (SATS) rises 8% as Verizon Communications is said to be in discussions with the company about purchasing some of its wireless spectrum.

- Energy Fuels Inc. (UUUU) falls 7% after a $550 million offering of six-year convertible bonds.

- Firefly Aerospace (FLY) is down 10% after the company disclosed an incident during a test at its facility in Texas that resulted in the loss of a rocket stage.

- Oklo (OKLO) falls 3% while NuScale Power (SMR) drops 4% after Bank of America downgraded the nuclear companies, seeing valuations as unrealistic at this stage of small modular reactor development.

- QuantumScape (QS) climbs 4% after saying it will jointly develop with Corning ceramic-separator manufacturing capabilities for QS solid-state batteries.

- Semtech (SMTC) rises 3.7% after Oppenheimer raised the stock to outperform, saying the semiconductor firm’s active copper cable offerings can win market share among hyperscalers and drive sales growth.

- Vail Resorts (MTN) slips 2% after providing a profit outlook that missed expectations as the company sold fewer passes than it previously expected for the upcoming ski season.

In corporate news:

- BHP Group Ltd. retreated in London after China’s state-run iron ore buyer temporarily halted purchases from the Australian miner. The dollar edged lower, erasing September’s advance.

- Boeing Co. has started working on a next-generation single-aisle aircraft that could eventually replace the 737 Max, the Wall Street Journal reported.

- Coty has begun a strategic review of its consumer beauty brands.

- DeepSeek updated an experimental AI model in what it called a step toward next-generation artificial intelligence.

- EchoStar Corp. shares jumped in premarket trading as the satellite-TV company engaged in talks to sell some of its wireless spectrum to Verizon Communications Inc.

- Exxon Mobil Corp. plans to cut about 2,000 jobs globally as the Texas oil company consolidates smaller offices into regional hubs as part of its long-term restructuring plan.

- Spotify Technology SA names Alex Norström and Gustav Söderström co-CEOs.

- UBS Group AG reiterated its scathing critique of Switzerland’s planned changes to banking regulation, saying they may put the firm’s role in the country at risk.

- Jefferies posted its best fiscal third-quarter revenue ever, buoyed by what the firm said is a strengthening environment for dealmaking and trading activity across the globe. Higher expenses were the “one sticking point” in the overall better-than-expected results, according to Bloomberg Intelligence’s Neil Sipes.

All eyes are on today’s government shutdown. Vice President JD Vance said the US government is on track for a shutdown after President Donald Trump’s last-ditch meeting with congressional leaders ended without a deal. Many federal operations would pause if lawmakers fail to compromise before the fiscal year ends.

The Bureau of Labor Statistics — responsible for a number of gold-standard US economic releases — would cease operations and likely delay Friday’s payroll report in the event of a shutdown. “We advise investors to look past shutdown fears and focus on other market drivers,” wrote Mark Haefele, chief investment officer at UBS Global Wealth Management. “We continue to prefer quality fixed income, particularly those with medium-term maturities, which we believe offers a compelling combination of income and resilience.”

Tariffs are back in focus. Trump ordered 10% duties on imports of softwood timber and lumber as well as 25% levies on some wood furniture products. China’s state-run iron ore buyer told major steelmakers and traders to temporarily halt purchases of all new cargoes from Australian miner BHP, widening an earlier curb as a price dispute escalated, according to people familiar.

Elsewhere, traders are looking ahead to a series of US labor reports due this week to gauge the Fed’s next move, with the release of Friday’s key payrolls report in doubt amid a budget impasse in Congress. The uncertainty comes as the S&P 500 is headed for its best September in 15 years, fueled by looser policy, strong earnings and optimism over artificial intelligence.

“The main focus will be the US labor market, which should either confirm or challenge expectations of two more rate cuts in 2025,” said Susana Cruz, a strategist at Panmure Liberum. “If the shutdown delays the release, that could spark some anxiety.”

Fed Vice Chair Philip Jefferson warned Tuesday that the central bank faces a cooling labor market alongside rising inflation pressures, complicating the policy outlook. “I see the risks to employment as tilted to the downside and risks to inflation to the upside,” Jefferson said in remarks prepared for the fourth International Monetary Policy Conference hosted by the Bank of Finland. “It follows that both sides of our mandate are under pressure.”

The Fed’s Susan Collins and Austan Goolsbee are due to deliver speeches later on Tuesday. Investors will also look at August JOLTS data, which is expected to show weakening demand for labor. “The closer the headline is to estimates, the better, as a too-hot or too-cold print could weigh on already shaky markets amid the government shutdown worries,” said Tom Essaye at The Sevens Report.

The Stoxx 600 drops 0.2%,taking the shine off the best September performance since 2019, as Bloomberg News reported that China moved to ban all iron ore cargoes from BHP Group. The market was led lower by energy names as oil prices fall for a second day – WTI crude futures slip 0.9% to $62.90 a barrel. Here are some of the biggest movers on Tuesday:

- Puma gains as much as 6.5% after BNP Paribas Exane upgrades to neutral from underperform and boosts its price target by 40%, saying the sportswear firm is “now in special situation territory.”

- Eiffage shares rise as much as 1.6% after the construction firm won a contract worth over €1.5 billion to build substations for French offshore wind farms.

- Knorr-Bremse shares rise as much as 2.6% after Hauck & Aufhaeuser upgraded the stock, saying the German firm’s acquisition of Swiss-based Duagon Group complements its train control systems offering.

- Valneva shares rise as much as 11.5% after the company reported positive antibody persistence data four years after a single shot of its chikungunya vaccine.

- European Luxury stocks fall after China’s factory activity extended its decline into a sixth month, the longest slump since 2019, indicating the country’s economy is at risk of a slowdown.

- Hornbach slumps 7.9% after the building materials and garden supplies retailer reported sales for the second quarter that missed the average analyst estimate.

- Asos slumps as much as 13% after the fashion retailer warned adjusted Ebitda will be at the lower-end of its guided range this year.

- Pandora drops as much as 4.3% following the announcement that CEO Alexander Lacik will retire next year, with RBC calling it “incrementally negative.”

- Close Brothers falls as much as 11% as the financial services group downgrades near-term adjusted earnings.

- Card Factory slides as much as 6.1% as first-half profit falls.

- European wood and forestry companies are underperforming the broader market on Tuesday after US President Donald Trump ordered tariffs on imports of softwood timber and lumber.

Earlier in the session, Asian equities climbed to cap September with their longest monthly winning streak since early 2018, led by gains in Taiwan and Hong Kong stocks. The MSCI Asia Pacific Index rose 0.6% Tuesday, with Alibaba among the top contributors. The regional benchmark gained about 4% in September, recording its sixth consecutive monthly advance. Key benchmarks also traded higher in Japan, mainland China and Singapore. Investors have remained anchored in the region, chasing potential artificial intelligence winners and driving recent tech stock gains. Many are also scouring for China’s homegrown tech developers, amid hopes for an economic revival driven by increased consumption. Hong Kong’s benchmark, up 7% for September, has posted its best month since February, while the key onshore index also climbed for a fifth straight month. The Hong Kong market will be closed Wednesday while mainland bourses will be shut through Oct. 8 for Golden Week holidays.

In FX, yen is leading gains against the dollar for a second day, rising 0.5% and taking USD/JPY below 148 after a weak JGB auction pushed Japanese two-year yields to the highest since 2008. The Aussie dollar is still outperforming after a hawkish hold by the RBA.

In rates, treasuries inch higher, pushing US 10-year yields lower by 1 bp to 4.13%. Bunds ticked lower when German state CPI data showed accelerations across the country’s biggest regions.

In commodities, gold also added to Monday’s surge before swiftly erasing gains and now sits ~$30 lower on the day.

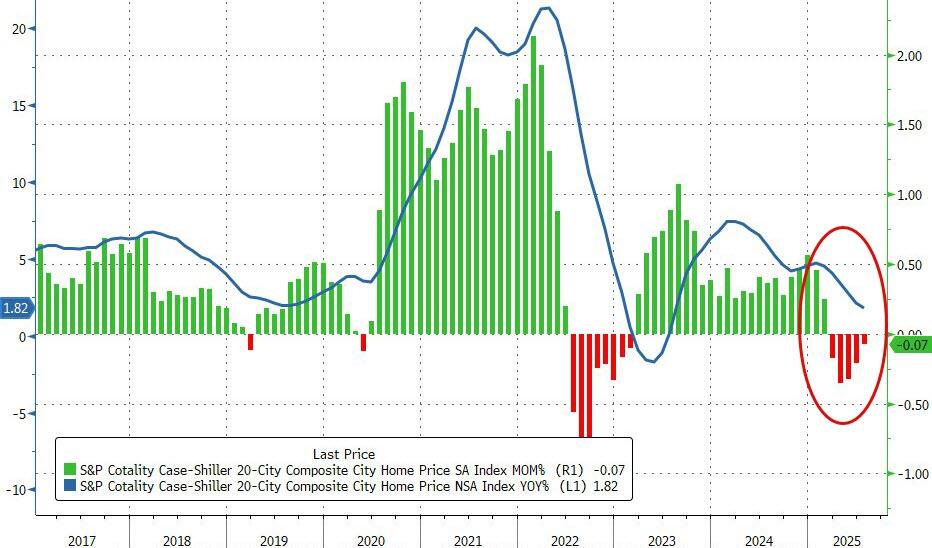

Looking at today’s calendar, data due today include job openings for August and consumer confidence for September. Bloomberg Economist Anna Wong expects to see an improvement in confidence given the continued strength in spending through August. Still, she says sentiment measures have been diverging, with the U Michigan survey reflecting growing concerns about higher inflation and potential labor market weakness. US economic data slate includes July FHFA house price index, S&O Cotality house prices (9am), September MNI Chicago PMI (9:45am), August JOLTS job openings, September consumer confidence (10am) and Dallas Fed services activity (10:30am). Fed speaker slate includes Collins (9am), Goolsbee (1:30pm, 3:30pm) and Logan (7:10pm)

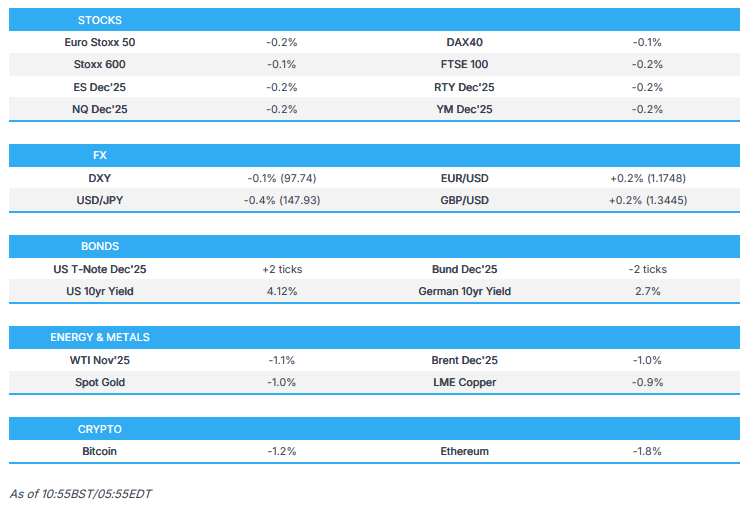

Market Snapshot

- S&P 500 mini -0.2%

- Nasdaq 100 mini -0.2%

- Russell 2000 mini -0.2%

- Stoxx Europe 600 -0.1%

- DAX little changed

- CAC 40 -0.3%

- 10-year Treasury yield -1 basis point at 4.13%

- VIX +0.4 points at 16.55

- Bloomberg Dollar Index -0.2% at 1200.18

- euro +0.2% at $1.1752

- WTI crude -0.9% at $62.88/barrel

Top Overnight News

- The US government is set for a shutdown tomorrow, JD Vance said, seeking to pin the blame on Democrats. Senate Minority Leader Chuck Schumer said he wouldn’t support a seven- or ten-day stopgap funding bill. The impasse has raised concerns that data releases, including Friday’s jobs report, may be delayed. BBG

- Senate Minority Leader Schumer said he met with President Trump, noting “we have large differences” and adding that the decision to avoid a government shutdown lies with Republicans. Democratic Leader Jefferies said Democrats will not support a partisan Republican bill that hurts healthcare, according to Reuters.

- Vice President Vance said he had frank talks with Democratic leadership, adding “you don’t shut government over disagreements,” but said “I think we’re headed to a shutdown because the Democrats won’t do the right thing.”, according to Reuters.

- Punchbowl’s Sherman said that from listening to Schumer, Jeffries, and Vance, it does not sound like there was a breakthrough in the meeting, adding that a shutdown is around the corner, via Punchbowl.

- House Speaker Johnson said they want to allow more time for negotiations, according to Reuters.

- Major airlines warned that a potential government shutdown could strain US aviation and cause flight delays, according to a statement.

- Schumer said he would not accept a 7–10 day stopgap bill, according to Reuters.

- Trump said the tariff on upholstered furniture will start at 25% and rise to 30% on Jan 1, with kitchen cabinets/bathroom vanities starting at 25% before rising to 50% (although imports from the EU and Japan will be capped at 15%, with the UK ceiling 10%). NYT

- Trump’s lumber/timber tariff details aren’t as bad as feared (the rate is only 10%, and payers of that tariff won’t be subject to the “reciprocal” tax). NYT

- China’s NBS PMIs for Sept are mixed, with modest upside on manufacturing (49.8 vs. the Street 49.6 and up from 49.3 in Aug) and a small miss on services (50 vs. the Street 50.2 and down from 50.3 in Aug). WSJ

- Japan’s factory output fell more than expected while retail sales declined for the first time in over three years in August, government data showed, heightening uncertainties about the economic outlook. Industrial production (-1.2% M/M vs. the Street -0.9%), retail sales (-1.1% M/M vs. the Street +1.2%), and housing starts (-9.8% Y/Y vs. the Street -5.2%). RTRS

- Taiwan Premier Cho Jung-tai said trade talks with the US have entered “the crucial closing stages,” indicating the global chip hub is finally nearing a deal with the Trump administration. Taiwan’s trade negotiators arrived in Washington late last week for discussions with their US counterparts aimed at lowering the 20% tariff imposed on the island. BBG

- Iron ore advanced after China’s state-run iron ore buyer told major steelmakers and traders in the world’s largest importer to temporarily halt purchases of all new BHP Group cargoes. BBG

- The SNB made its most significant sales of the franc in more than three years in the second quarter to stem a surge caused by Trump’s tariff push. BBG

- French inflation picked up on an acceleration in the services sector but remained well below the ECB’s 2% target. Consumer prices rose 1.1% in September from a year earlier. BBG

Trade/Tariffs

- The White House said US President Trump signed a proclamation adjusting imports of timber, lumber, and related derivatives into the US, imposing a 10% tariff on softwood, timber and lumber imports effective 14 October. It added that Trump intends to cap tariff rates for EU and Japanese wood products at 15%, according to Reuters.

- The White House confirmed new 25% tariffs on vanities and kitchen cabinets will take effect on 14 October, with imports of certain upholstered wooden products also subject to a 25% tariff. It announced tariffs on imported cabinets will rise from 25% to 50%, while tariffs on upholstered furniture will increase from 25% to 30% effective 1st January, unless trade agreements are reached beforehand, according to Reuters.

- South Korea’s Top Security Adviser Wi said it is challenging to strike a currency swap deal with the US, according to Reuters.

- EU Trade Commissioner Sefcovic says the EU and US are “very soon going to propose the post 2026 safeguard measures” on steel, working with tariff-rate quotas, to deal with “global overcapacity”.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded flat/mixed following a mostly but modestly firmer handover from Wall Street, with focus on the looming US government shutdown and the possibility of delayed NFP data as a result. Meanwhile, the White House announcement of further tariff details overnight capped upside in sentiment. ASX 200 gave up initial mild gains to trade flat as strength across gold miners just about offset hefty losses in energy and a subdued performance in financials, with little move seen in the index after the RBA policy announcement, in which the central bank left rates unchanged as expected in a unanimous decision but struck a hawkish tone, noting inflation risks and that the decline in underlying inflation has slowed. Nikkei 225 narrowly underperformed at the start and briefly fell back under the 45,000 mark with losses led by energy names, while some hawkish undertones from the BoJ Summary of Opinions likely weighed, with some members arguing it may be time to consider another adjustment after more than six months since the last hike, while others cautioned against surprising markets or moving prematurely given uncertainty around the US outlook. Hang Seng and Shanghai Comp varied, the former gave up earlier upside and the latter held onto mild gains with newsflow light ahead of the weeklong break, whilst Chinese PMIs showed manufacturing beat expectations, but services declined from the prior month in both the NBS and RatingDog (formerly Caixin) releases. Furthermore, China’s Securities Journal suggested experts believe the PBoC may flexibly use a variety of monetary policy tools in the future to maintain ample liquidity. KOSPI was subdued with US-South Korean trade talks seemingly at a standstill, with the South Korean national security adviser suggesting it is tough to strike an FX swap deal with the US.

Top Asian News

- RBA maintained its Cash Rate at 3.60%, as expected, in a unanimous decision, noting that the decline in underlying inflation has slowed. It said recent data suggest September quarter inflation may be higher than expected in August, though both headline and trimmed mean inflation were within the 2–3% range in Q2. The Bank added that inflation has fallen substantially since the 2022 peak as higher rates have helped bring demand and supply closer to balance. RBA noted that financial conditions have eased since the beginning of the year, and this seems to be having some impact, but it will take some time to see the full effects of earlier cash rate reductions.

- RBA Governor Bullock says Board sees risks as broadly balanced; labour market remains solid, still a little tight; economy is in a good spot; need to be a little cautious on inflation; Policy is a little bit restrictive, not expansionary. Could be a couple more rate cuts, could not be. Not giving forward guidance, will have more data in November. Impact of past easing still to come.

- BoJ Summary of Opinions noted one member suggested it may be time to consider raising the policy interest rate again, while another said the BoJ gains more information on the US outlook by waiting, and one argued the Bank should maintain accommodative conditions at this point. On the economy, members said US tariffs will still impact Japan even after being reduced to 15%, with growth likely to moderate temporarily. On prices, CPI is expected to rise below 2% in fiscal 2026 as cost-push pressures ease, warranting continued accommodative policy. Some members argued that, given it has been more than six months since the last hike, the Bank should consider raising rates again at regular intervals if activity and prices remain in line with projections. Others noted that constraints from overseas factors have abated, allowing the Bank to return to a stance of raising rates and aligning real interest rates with overseas levels. However, members also stressed that the impact of prior hikes to 0.5% has been limited, and while risks to prices are skewed to the upside, the BoJ should avoid moving rates immediately to restrictive levels, instead gradually shifting closer to neutral to prevent shocks from rapid future hikes.

- Experts believe that to maintain ample liquidity, the PBoC may flexibly use a variety of monetary policy tools in the future, according to China’s Securities Journal.

European bourses lower across the board, Euro Stoxx 50 -0.3%; broader market narrative is dictated by the looming US government shutdown. Sectors are mostly lower after a mixed start to the session, just Financial Services & Media remain in the green. Energy hit by ongoing crude softness. Gambling names impacted by late-night comments from Chancellor Reeves. Mining sector underpinned by initial XAU strength.

Top European News

- Italy is set to forecast its 2025 budget deficit at or below 3% of GDP, in line with EU rules, according to Reuters, citing sources.

- Annual UK shop price inflation rose to 1.4% in September, up from 0.9% in August, according to the latest monthly report from the British Retail Consortium (BRC) and analysts NIQ, via the Guardian.

- ECB’s Vice President Guindos says the current level of interest rate is adequate and further decisions will be made meeting by meeting.

- SNB’s Schlegel says inflation is expected to rise slightly in the coming quarters. Indicators point to a stable situation and moderate growth. Uncertainty remains high. Pharmaceutical tariffs have raised the downside risk, “a bit”.

FX