XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

072 C GOLDMAN 1

092 C DEUTSCHE BANK 53

118 C MACQUARIE FUTURES US 19

118 H MACQUARIE FUTURES US 130

132 C SG AMERICAS 5

167 H MAREX 18

323 C HSBC 18

332 H STANDARD CHARTERED B 75

435 H SCOTIA CAPITAL (USA) 162

555 C BNP PARIBAS SEC CORP 11

657 H MORGAN STANLEY 28

661 C JP MORGAN SECURITIES 560

686 C STONEX FINANCIAL INC 84 3

690 C ABN AMRO CLR USA LLC 17 2

709 C BARCLAYS 10

732 C RBC CAP MARKETS 655

732 H RBC CAP MARKETS 38

880 C CITIGROUP 6

880 H CITIGROUP 329

905 C ADM 18

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 1121 CONTRACTs NOTICES FOR 112100 OZ or 3.486 TONNES

total notices so far: 22,379 contracts for 2,237,900 OR 69.608tonnes)

SILVER NOTICES: 172 NOTICE(S) FILED FOR 0.860 MILLION OZ/

total number of notices filed so far this month : 2405 CONTRACTS (NOTICES) for 12.025 million oz

INITIAL STANDING FOR OCT: 13.240 MILLION OZ PLUS 585,000 OZ QUEUE JUMP EQUATES TO 13.805 MILLION OZ//

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 3.00 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 13.805 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING PLUS 1.555 TONNES OF OUR FIRST ISSUANCE EXCHANGE FOR RISK//NEW TOTALS 91.567 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 10.2208 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FALL BY A MEGA HUGE SIZED 23,717 CONTRACTS OI TO 163,830 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 600 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 600 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 640 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2337 CONTRACTS AND ADD TO THE 600 E.FP. ISSUED

WE OBTAIN A MEGA MEGA HUGE SIZED LOSS OF 1737 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $0.34 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 8.685 MILLION PAPER OZ

OCCURRED WITH OUR LOSS $0.34 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

//Hang Seng CLOSED CLOSED

// Nikkei CLOSED : DOWN 381.78PTS OR 0.85% //Australia’s all ordinaries CLOSED UP 0.01%

//Chinese yuan (ONSHORE) CLOSED XXXX OFFSHORE CLOSED UP AT 7.1251/ Oil DOWN TO 62.20 dollars per barrel for WTI and BRENT DOWN TO 65.77 Stocks in Europe OPENED MOSTLY MIXED

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A MEGA MEGA HUGE SIZED 23,717 CONTRACTS TO 494,340 OI DESPITE OUR GAIN IN PRICE OF $18.95 WITH RESPECT TO TUESDAY’S // TRADING COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3286). WE HAD HUGE T.A.S. LIQUIDATION TUESDAY ALONG WITH MASSIVE MONTH END SPREADER LIQUIDATION. WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 20,431 CONTRACTS (OR 63.548 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD 0 CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR NIL OZ OR 0 TONNES OF GOLD. WE HAD 500 CONTRACTS OF EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE AND THAT IS QUITE UNUSUAL FOR THEM AS THE CENTRAL BANK OF ENGLAND MUST BE DESPERATE!!

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER:

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD.

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 118 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 118 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN DECEMBER 2024.

DETAILS ON OCTOBER COMEX MONTH//

IN TOTAL WE HAD A MEGA MEGA HUGE SIZED LOSS ON OUR TWO EXCHANGES OF 20,431 CONTRACTS DESPITE OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 1.5% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER/OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1401 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN THIS PAST WEDNESDAY WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSES TO BUCKLE!! THIS LEADS US TO YESTERDAY, FIRST DAY NOTICE AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORTED PAPER ISSUANCE

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS WERE JOINED WITH LIQUIDATION OF MONTH- END SPREADERS YESTERDAY AND THAT IS THE REASON WHY WE ARE HAVING HUGE DISTORTED COMEX OPEN INTEREST LOSSES IN OI. HOWEVER THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE/OCTOBER COMEX GOLD TOTALS WITH MASSIVE GOLD TONNES STANDING FOR GOLD.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS NOW BRINGS US TO OCTOBER WHERE INITIAL AMOUNT OF GOLD STANDING IS 28,988 CONTRACTS FOR 90.114 TONNES OF GOLD AND THIS WAS AUGMENTED BY AN UNUSUAL 50000 CONTRACT EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE//THUS TOTAL AMOUNT STANDING ON GOLD INITIAL EQUATES TO 91,719 TONNES!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 242 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH OCTOBER AND SUBSEQUENT STANDING FOR GOLD.

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR INITIAL 50,000 OZ OR 1.555 TONNES OF EX FOR RISK TOTALS 91.719 TONNES

I.E.

a) INITIAL STANDING 91.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

EQUALS

91.719 TONNES OF GOLD!!

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3286 EFP CONTRACT WAS ISSUED: : /DEC 3286 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3286 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- MASSIVE LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY AND THIS HAD A HUGE EFFECT ON OUR TOTAL OPEN INTEREST.

- MONTH END SPREADERS HAVE NOW COME INTO THE PICTURE AND IT WAS IN FULL FORCE YESTERDAY AS WE WITNESS THE HUGE FALL IN OPEN INTEREST. STRANGELY IT HAD NO EFFECT ON PRICE AS IT ROSE BY $18.95

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A FAIR SIZED SIZED 1401 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING MASSIVE LOSS OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S FIRST INITIAL ISSUANCE FOR EXCHANGE FOR RISK OF 510 CONTRACTS OR 51,000 OZ OR 1.555 TONES OF GOLD.

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY OUR INITIAL 1.555 TONNES OF GOLD EX FOR RISK/TOTALS 91.164 TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $18.95./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A MASSIVE SIZED LOSS IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD MASSIVE T.A.S. SPREADER LIQUIDATION TUESDAY ALONG WITH SPREADER LIQUIDATION.THIS WAS COUPLED WITH GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION) /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH WERE JOINED BY OUR MONTHLY SPREADERS) NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS ARE TRYING AGAIN TODAY WITH NOT MUCH LUCK, YESTERDAY ON THIS LAST DAY OF SEPT. OPTIONS EXPIRY WEEK, THEY FAILED LIKE THEY DID IN AUGUST. (LBMA LONDON EXPIRY FINISHED YESTERDAY TUESDAY SEPT 30).

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS SOCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A MEGA HUGE SIZED LOSS TOTAL OF 63.548 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES AND THIS WAS COUPLED STRANGELY WITH OUR INITIAL 50,000 OZ EXCHANGE FOR RISK ISSUANCE//1.555 TONNES/NEW TOTAL INITIAL STANDING FOR OCTOBER: 91.719 TONNES

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $18.95

WE HAD A LARGE 592 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 20,431 CONTRACTS OR 2,043,100 0Z (63.548TONNES)

confirmed volume TUESDAY 336,239 contracts// strong//

speculators have left the gold arena

INITIAL GOLD COMEX

OCT CONTRACT MONTH

OCT 1 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 2 entries i) Out of Asahi 16,020.280 oz ii) Out of Brinks 14,660.856 oz total withdrawal: 30,681.136 oz in tonnage: 0.9543 tonnes . |

| Deposit to the Dealer Inventory in oz | 1 ENTRIES i) Into Loomis: 64,026.230 oz total deposit dealer: 64,026.230 oz (1.991 tonnes) |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRIES i) Into Brinks customer account: 27,899.440oz total deposit 27,899.440 OZ in tonnes: .867 tonnes total tonnage dealer and customer: 2.858 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1121 notice(s) 112,100 OZ 3.486 TONNES |

| No of oz to be served (notices) | 6560 contracts 656,000OZ 20.406 TONNES |

| Total monthly oz gold served (contracts) so far this month | 22,379 notices 2,237,900 oz 69.608 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1

1 ENTRIES

i) Into Loomis: 64,026.230 oz

total deposit dealer: 64,026.230 oz

(1.991 tonnes)

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 ENTRIES

i) Into Brinks customer account: 27,899.440oz

total deposit 27,899.440 OZ

in tonnes: .867 tonnes

total tonnage dealer and customer: 2.858 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

2 entries

i) Out of Asahi 16,020.280 oz

ii) Out of Brinks 14,660.856 oz

total withdrawal: 30,681.136 oz

in tonnage: 0.9543 tonnes

ADJUSTMENTs 3

customer to dealer

a) Asahi 32,021.838 oz

b) Loomis: 3182.949 oz

dealer to customer:

c) Brinks

385.812 oz

volume at the comex: TUESDAY: 336,239 oz (strong)

AMOUNT OF GOLD STANDING FOR OCTOBER

THE FRONT MONTH OF OCTOBER STANDS AT 7681 CONTRACTS FOR A LOSS OF 21,307 CONTRACTS.

WE HAD 21,258 CONTRACTS FILED YESTERDAY. SO WE LOST A SMALL 49 CONTRACTS OR AN ADDITIONAL 4900 OZ UNDERWENT AN EFP TRANSFER TO LONDON TO TAKE DELIVERY OVER ON THAT SIDE OF THE POND!

NOVEMBER LOST 16 CONTRACTS UP TO 4418 CONTRACTS.

DECEMBER LOST 4858 CONTRACTS UP TO 401,185 CONTRACTS.

We had 1121 contracts filed for today representing 112,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to1121 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 560 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (22,379 100 oz ) to which we add the difference between the open interest for the front month of OCT ( 7681 CONTRACTS) minus the number of notices served upon today (1121 x 100 oz per contract) equals 2,893,900 OZ OR 90.012 TONNES OF GOLD TO WHICH WE ADD OUR INITIAL 1.555 TONNES OF EXCHANGE FOR RISK//NEW TOTALS STANDING FOR GOLD OCTOBER REDUCES TO 91.567 TONNES

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (22379 x 100 oz +we add the difference for front month of OCT. (7681 OI} minus the number of notices served upon today (1121 x 100 oz) which equals 2,893,900 OZ OR 90.012 TONNES + 1.555 TONNES EXCHANGE FOR RISK//NEW TOTALS; 91.567 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 91.567 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,023,569.112 oz 62.94 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 40,105,920.360 oz

TOTAL REGISTERED GOLD 22,072.364 or 686.53 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,033,556.221 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 20,048,795oz ((REG GOLD- PLEDGED GOLD)= 623.607 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

OCT 1 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries a) Out of CNT 1000.000 b) Out of Delaware 2074.100 oz total withdrawal: 3074.100 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 entry i) Into Asahi: 589,145.900 oz total deposit: 589,145.900 oz |

| No of oz served today (contracts) | 172 CONTRACT(S) ( 860,000 OZ |

| No of oz to be served (notices) | 356 contracts (1.780 MILLION oz) |

| Total monthly oz silver served (contracts) | 2405 Contracts (12.025 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 entry

i) Into Asahi: 589,145.900 oz

total deposit: 589,145.900 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

2 entries

a) Out of CNT 1000.000

b) Out of Delaware 2074.100 oz

total withdrawal: 3074.100 oz

adjustments: all customer to dealer

a) Brinks 4729.100 oz

b) Loomis 184,878.540 oz oz

TOTAL REGISTERED SILVER: 193.692 MILLION OZ//.TOTAL REG + ELIGIBLE. 530.786 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 528 OPEN INTEREST CONTRACTS FOR A LOSS OF 2116 CONTRACTS.

WE HAD 2233 CONTRACTS SERVED YESTERDAY, SO WE GAINED 117 CONTRACTS WHICH UNDERWENT A STRONG QUEUE JUMP OF 585,000 OZ

STANDING FOR SILVER OCT: 13.805 MILLION OZ

NOVEMBER GAINED 6 CONTRACTS UP TO 2295

DECEMBER LOST 775 CONTRACTS DOWN TO 132,230

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 172 or 860,000 oz

CONFIRMED volume; ON TUESDAY 109.435 huge//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 2405 X5,000 oz = 12.025MILLION oz

to which we add the difference between the open interest for the front month of OCT (528) AND the number of notices served upon today (172 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (2405) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(528) minus number of notices served upon today (172)x 5000 oz equals silver standing for the OCT.contract month equating to 13.805 MILLION OZ

New total standing: 13.805 million oz which is STILL HUGE for this NON active delivery month of OCT. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 193.692 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/530.786million. 39.57%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

GLD INVENTORY: 1012.88 TONNES, TONIGHTS TOTAL

SILVER

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

CLOSING INVENTORY 504.287 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

JAMES RICKARDS

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

Who owns all the gold?

For the last four decades, China has been cornering the physical gold market. Now that the West is turning bullish, where will the gold come from?

| Alasdair MacleodOct 1∙Paid |

The sums concerned at this stage of gold’s bull market are staggering. Large American banks manage portfolios worth trillions, and their analysts are belatedly turning bullish on gold. Already, demand for ETFs is picking up, and mining indices have doubled this year from depressed levels. A tsunami of currency is just beginning to roll gold’s way. But where is the gold going to come from?

You may need to read this article twice for its implications to sink in.

China has cornered the market

The problem with analysing gold ownership is that those that own it don’t want to be identified — whether it be individuals concealing their wealth, or entire governments for economic or geopolitical reasons. And since the death of Mao, if not before, China has been Hotel California for gold: gold flows in freely but never leaves.

Before the Shanghai Gold Exchange was opened for business in 2002, private individuals were banned from gold ownership. Yet it was clear that before then the state’s gold policy was to develop gold mining, turning China into the largest global miner by far and doré was also imported for refining by state-owned refineries from elsewhere, never to leave.

The regulations appointing the Peoples Bank (PBOC) with sole responsibility for gold and silver date from 1983. At that time, gold was in the early stages of its massive post-seventies bear market, so supplies from disillusioned Western investors were readily available at declining prices — ideal conditions for concealing a large, dedicated buyer.

Additionally, bullion was being leased and sold into the market by hedge funds to fund a carry trade into US T-bills, estimated by analyst Frank Veneroso to have amounted to between 10,000 and 14,000 tonnes by the year 2002. Veneroso quipped that this bullion was probably adorning the necks of Asian women. More likely, it was quietly being picked up by the PBOC.

The PBOC had monopoly responsibility for foreign exchange dealings, so it was a simple matter to divert a portion of these substantial capital and trade flows into purchases of gold. Bearing in mind that contemporary prices declined from about $430 to $260 per ounce between 1983-2002, only 10% of these net currency flows would have led to the acquisition of between 20,000-25,000 tonnes, secretly distributed between various government accounts.[i] This is not to be confused with the PBOC’s own gold reserves.

Whatever the actual amount, the Chinese leadership decided that they had accumulated sufficient gold to allow the public, hitherto banned, to buy gold. The Shanghai Gold Exchange (SGE) was opened for that purpose in 2002. However, it is clear that the state continued to accumulate gold when it was offered by Western markets and refiners.

Between 1983 and 2002, above-ground stocks of gold increased from 91,916 tonnes to 132,976 tonnes. With the additional supply from disillusioned investors in the West, it was certainly possible for China to accumulate gold on this scale.

We cannot know how much gold has been additionally accumulated by the state since 2002. Import-export statistics only cover non-monetary gold. All China needs to do is to categorise it as monetary for it not to be recorded. But given the increased pace of global mine production, and global scrap supplies together with her own mine output of 7,578 tonnes since 2002, a further accumulation of 15,000—20,000 tonnes of state-owned gold is easily conceivable.

There are two other sources of Chinese demand to account for. Since 2002, Chinese citizens have withdrawn 27,300 tonnes from SGE vaults, mostly turned into jewellery. Secondly, the banks offer gold accumulation accounts alongside deposits, which together with other investment schemes are backed by gold remaining in the SGE’s vaults. Given that household savings are estimated at over 30% of GDP (about $5 trillion equivalent), that these funds are no longer buying into off-plan property development, and that banks have been reducing deposit account rates, it seems reasonable to suggest that some 10,000 tonnes of investment gold have accumulated in SGE vaults since 2002, probably at an increasing pace.

New global mine supply over the 2002-2024 period was over 65,000 tonnes, exceeding our figure for total Chinese demand by about 10,000 tonnes. Given subdued demand from other markets, as a ballpark figure Chinese demand amounting to 55,000 tonnes seems reasonably close to the mark.

Putting all this together, our estimate for Chinese owned gold today totals 75,500 tonnes, including the PBOC’s reserves. It has been accumulated at an average rate of about 1,800 tonnes a year

Above ground stocks today are estimated at 198,094 tonnes, based on a paper prepared for Goldmoney by James Turk and Spanish economist Juan Castañeda in 2012 and updated by subsequent mine output. It is our source for accumulating above ground annually. This is some 20,000 tonnes less than other estimates, such as that of the WGC/GFMS. But we believe the Goldmoney calculation to be more accurate.

China’s total stake therefore represents 38% of all above-ground stock, probably over 40% allowing for gold which has been lost over the centuries.

Our estimate of China’s holdings are summarised in the table below.

We can develop our analysis even further, given that China together with Russia has extended her sphere of influence across nearly all Asia, Africa, and elsewhere. This is gold unlikely to be available to Western markets.

So far, we have accounted for 115,100 tonnes, or 58% of above-ground stocks. They do not include SCO and BRICS sovereign wealth funds other than Russia’s two funds.

The balance of 82,994 tonnes of above-ground gold is split between other central banks (27,668 tonnes), LBMA vaults and Comex warehouses (10,075 tonnes) reducing the unaccounted total to 45,251 tonnes. We cannot find any estimate for total gold storage in Switzerland, which would probably leave our unaccounted total at less than 45,000 tonnes.

Apart from gold lost through time, the bulk of this remainder will be held as jewellery in Western markets so is inherently illiquid.

Conclusion

This survey of gold ownership is purely indicative, with very little verifiable information available. Its objective is to arrive at a rough estimate of liquidity in bullion markets by identifying gold not available to markets.

This is important, given that portfolio exposure to gold in ETFs and vaulted bullion is currently estimated at only 0.5%. Portfolio managers are now looking at gold as a possible investment. Global portfolios are estimated to total $300 trillion, so at current prices an increase of 1% allocation amounts to nearly 25,000 tonnes.

Clearly, there is insufficient liquidity in bullion markets to satisfy demand even on a minor scale. With investment strategists at large US banks forecasting higher prices, should investment managers act on it gold prices would be driven significantly higher, irrespective of economic and credit factors.

It is a process which appears to be only just starting, with potentially spectacular consequences.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 242/ROBERT KIENTZ

5. COMMODITY REPORT LITHIUM

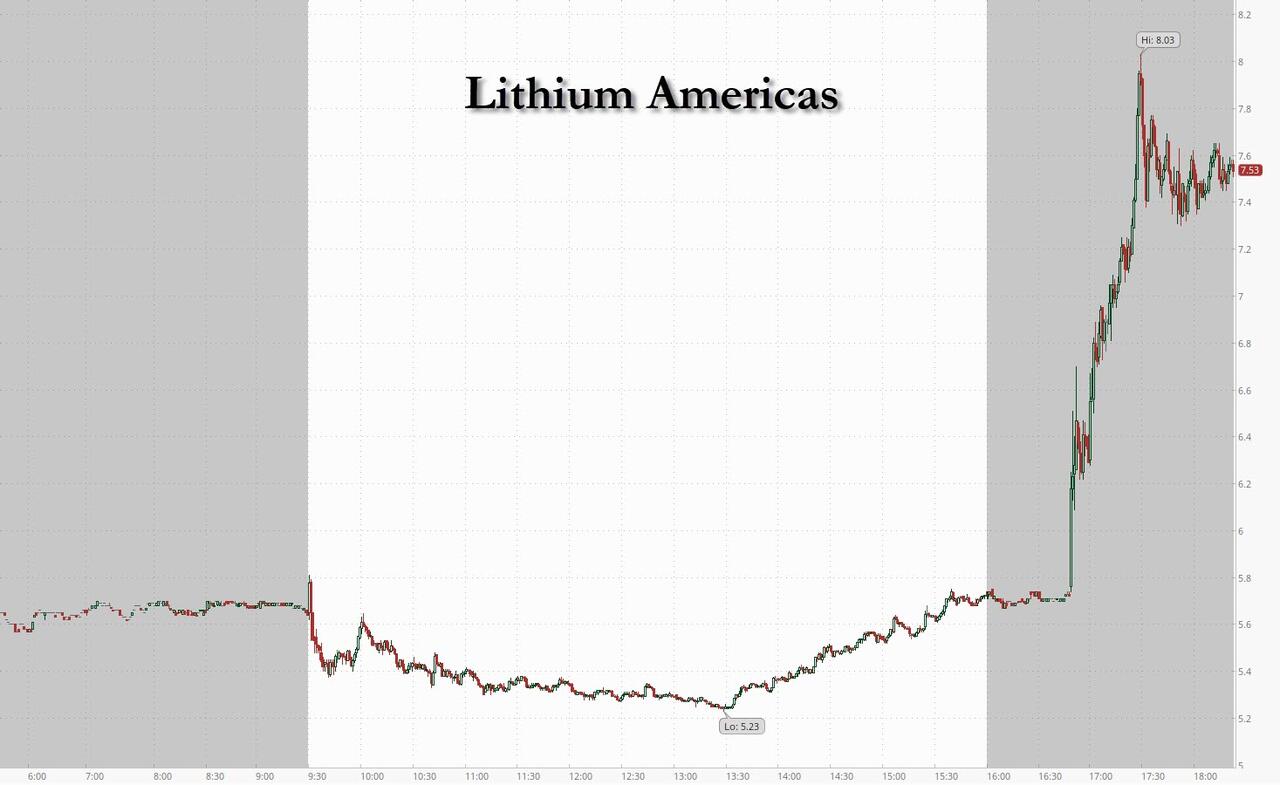

US Government Takes 10% Stake In Lithium Americas

Tuesday, Sep 30, 2025 – 10:10 PM

Trump’s Industrial Economy policies just took down their latest scalp, so to speak.

One week after Bloomberg reported that the White House was considering a 10% stake in one of the largest North American lithium mining companies, Lithium Americas, on Tuesday afternoon, the US government agreed to acquire a stake in the company, Secretary of Energy Chris Wright said Tuesday on Bloomberg TV, giving a boost to the Canadian company as it develops its Thacker Pass lithium project in Nevada.

The deal is the Trump administration’s latest effort to speed development of a domestic supply chain to counter China’s dominance over metals critical to defense, automaking and consumer electronics. In July, the US Defense Department announced a $400 million equity investment in MP Materials Corp. to fund a major new plant making rare-earth magnets.It was followed by a similar deal with chip giant Intel.

Lithium Americas’ Thacker Pass project in Nevada is forecast to become a major lithium source for a domestic industry that currently produces only small amounts of the battery metal.

Lithium Americas, which produces minerals used in electric-vehicle batteries, is also in talks with automaker General Motors over the terms of its $2.26 billion government loan for a large lithium mining project it is developing in Nevada.

Those discussions included debating whether the U.S. should take a stake in Lithium Americas as a condition for receiving a loan, the Wall Street Journal reported earlier this month.

The US-listed shares of Lithium Americas have risen 92% this year and soared 32% to $7.53 in after-hours trading Tuesday.

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED

//Hang Seng CLOSED CLOSED

// Nikkei CLOSED : DOWN 381.78PTS OR 0.85% //Australia’s all ordinaries CLOSED UP 0.01%

//Chinese yuan (ONSHORE) CLOSED XXXX OFFSHORE CLOSED UP AT 7.1251/ Oil DOWN TO 62.20 dollars per barrel for WTI and BRENT DOWN TO 65.77 Stocks in Europe OPENED MOSTLY MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN HOLIDAY IN TRADING AT XXXX AND XXXX//OFF SHORE YUAN TRADING DOWN TO 7.1251 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED HOLIDAY

OFFSHORE YUAN: DOWN TO 7.1251

HANG SENG CLOSED HOLIDAY

2. Nikkei closed DOWN 381.75 PTS OR 0.85%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 97.30 EURO RISES TO 1.1752 UP 15 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.641//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.12…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.151 UP 2 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: XXX OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7326Italian 10 Yr bond yield UP to 3.582 SPAIN 10 YR BOND YIELD UP TO 3.277

3i Greek 10 year bond yield UP TO 3.417

3j Gold at $3886.70 Silver at: 47.23 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 76 /100 roubles/dollar; ROUBLE AT 82.13

3m oil (WTI) into the 62 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.96/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.652% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.141 UP 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7958 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9348 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.152 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.745 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.600 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.59 UP 0 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.7230 UP 2 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.527 UP 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.185 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.749 DOWN 0 BASIS PTS.

2a New York OPENING REPORT

Futures Drop, Gold Jumps As US Government Shutdown Begins

Wednesday, Oct 01, 2025 – 08:14 AM

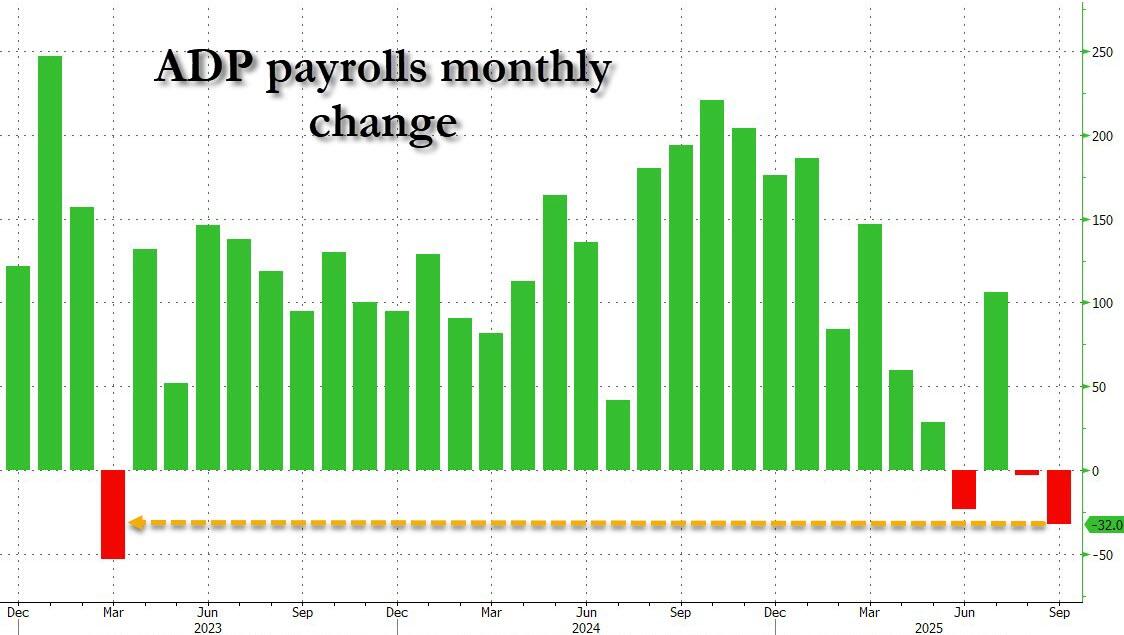

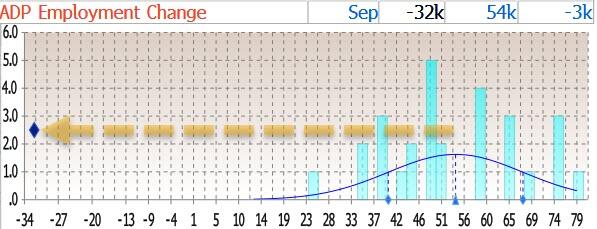

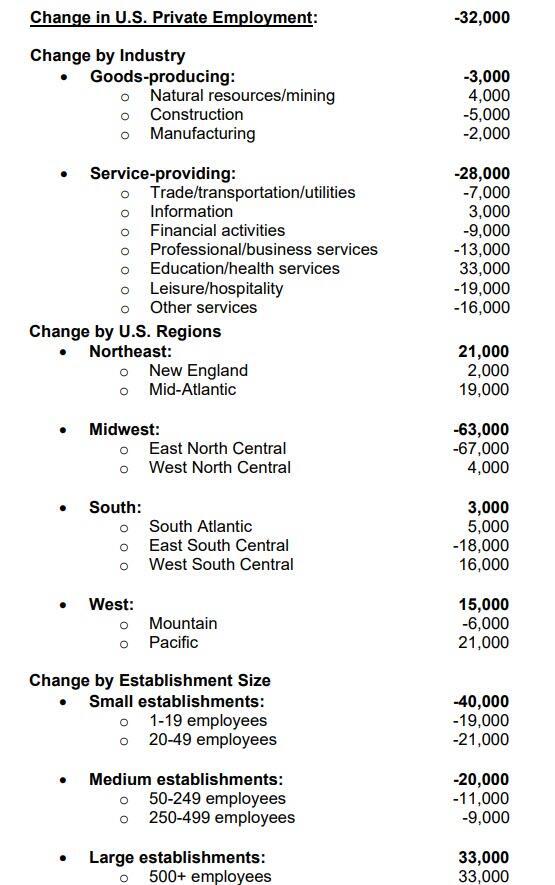

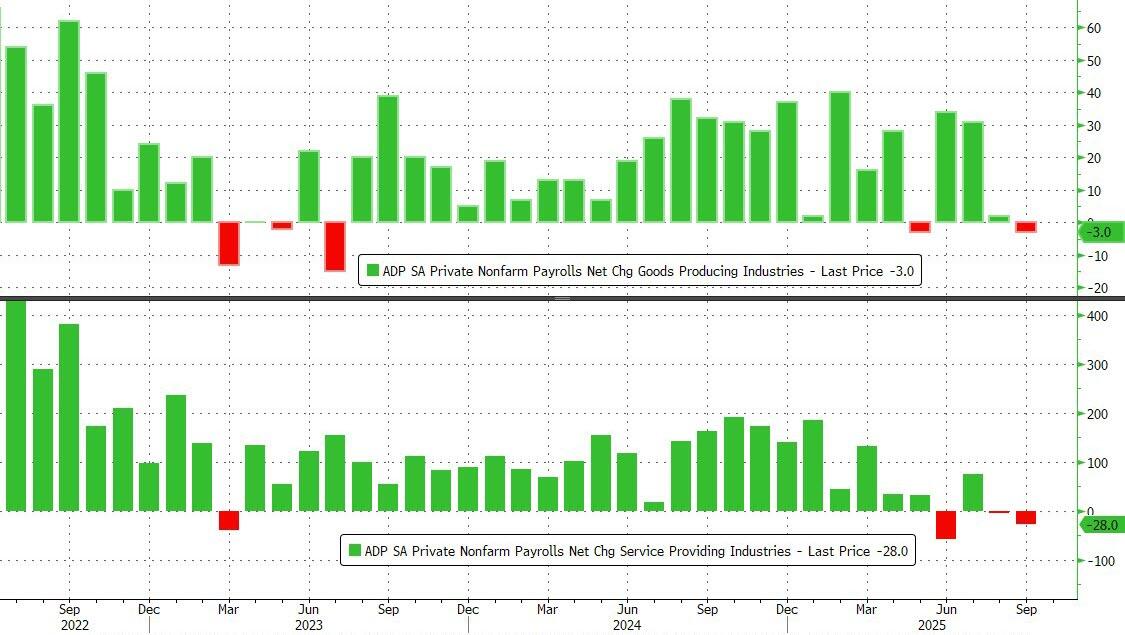

US stock futures are weaker to start the new quarter but have cut overnight losses by more than a third, as the first US government shutdown in nearly seven years begins. The first shutdown during Trump 1.0 lasted 3 days and the second shutdown 35 days: how long will this one last? As of 8:00am ET, S&P futures are down 0.4%, but well off session lows while Nasdaq futures drop 0.5%. Gold futures, up almost 1%, continue their advance toward $4,000. Pre-mkt, we are seeing a risk-off tone in US assets, including USD weakness, helping buttress international markets where Eurostoxx 50 set a new intraday ATH led by health care and communication sectors. Mag7 names are mostly lower with Semis also pressured; NKE gains 3% post solid earnings. The yield curve is twisting steeper. Commodities are weaker ex-Precious Metals with silver outperforming gold. With Friday’s NFP release all but certain to be delayed, ADP takes on heightened importance today; we also receive ISM-Mfg, construction spending, vehicle sales, and mtge applications.

In premarket trading, Magnificent Seven stocks are all lower (Apple -0.3%, Amazon -0.7%, Tesla -0.3%, Nvidia -0.5%, Alphabet -0.7%, Meta Platforms -0.7%, Microsoft -0.7%)

- AES Corp. (AES) rises 14% as BlackRock’s Global Infrastructure Partners LP is in advanced talks to acquire the power company, according to people familiar with the matter.

- Corteva (CTVA) inches 1% higher after announcing plans to separate into two independent companies, one comprising its current crop protection business and the other its current seed business.

- Lithium Americas (LAC) rises 32% after Secretary of Energy Chris Wright told Bloomberg TV that the US government agreed to acquire a stake in the company.

- Marvell Technology Inc. (MRVL) falls 2.5% after TD Cowen cut its recommendation on the chipmaker to hold from buy, citing limited visibility in a key vertical.

- Nike (NKE) climbs 3% after the sneaker retailer reported first-quarter revenue that beat the average analyst estimate, a sign its focus around specific sports such as running and basketball are starting to pay off.

- Sunrun Inc. (RUN) rises 5% after Jefferies raised its recommendation on the solar energy company to buy, citing cash and growth potential.

- Veeco Instruments (VECO) rises 4% after announcing plans to merge with Axcelis Technologies (ACLS). Axcelis falls 1.7%.

In corporate news, Apple says it did nothing wrong in choosing to partner with OpenAI — rather than Musk’s xAI — when it added generative AI to its iPhone operating system. Goldman Sachs is said to be among a cohort of financial firms planning to open offices in Kuwait. Lithium Americas shares surged after Secretary of Energy Chris Wright told Bloomberg TV that the US government agreed to acquire a stake in the company.

The US government shut down after a midnight funding deadline as Trump and Congressional Democrats clashed over health-care spending. With important economic reports now on hold, traders fear the loss of visibility will leave markets in the dark on the outlook for monetary policy. Fiona Boal, global head of equities at S&P Dow Jones Indices, said investor concern would focus on how long the shutdown may last, the disruption to economic data and potential job cuts.

The Congressional Budget Office estimates that about 750,000 employees will be furloughed at a cost per day of $400 million in lost compensation. The Trump administration’s plan to fire federal workers outright could also drive jobless claims higher at a time when employment already looks fragile.

“Government shutdowns in the US are rarely market-moving in and of themselves, but the timing matters,” said Nina Stanojevic, investment specialist at St James’s Place. “This one comes at a point where the Fed is data dependent. The absence of clean data can increase volatility.”

While the next Federal Reserve meeting is still four weeks away, policymakers might have to make decisions on an unclear picture, with the labor market softening and inflation hovering above target.

“In that case, a rate cut is likely to happen, but the uncertainty may lead to a change in expectations and increased volatility,” said Daniela Sabin Hathorn, senior market analyst at Capital.com. Money markets are currently pricing in a 90% chance of a quarter-point cut this month, and almost a 70% probability of another by year-end.

Shutdown aside, which according to many won’t have a negative impact on risk assets, traders will be wondering if technology can continue to provide upside momentum for the overall market as the final quarter of 2025 begins. Compared to earlier this year, the Magnificent 7 have had less of a role in recent gains, with some investors looking to the AI supply chain rather than the major names.

Still, the AI buzz is alive and well. There’s about $7 trillion of investment needed to finance the rapid growth of AI, according to Hadley Peer Marshall, CFO at Brookfield Asset Management. The equity buying spree has left aggregate positioning just above neutral, meaning there is still dry powder for more chasing or dip buying into typically positive fourth-quarter seasonality, according to Barclays strategists.

On the policy front, the Fed’s Logan said policymakers should be cautious about considering additional rate cuts while inflation remains above target and the labor market relatively balanced. Meanwhile, Taiwan has pushed back on a US request to move chip production stateside to cover half of America’s demand.

Unlike the US, European stocks gained 0.4%, driven mostly by pharmaceutical stocks as Pfizer’s drug pricing deal provides relief on the industry’s outlook. Here are some of the biggest movers on Wednesday:

- Greggs shares rally as much as 13% after the baker said trading improved in August and September and that its cost inflation outlook has improved, helping it to reiterate its full-year expectations.

- European drugmakers rise following Pfizer’s drug-pricing agreement with US President Donald Trump, which JPMorgan analysts say could be a potential bellwether for the sector and “reassure investors over a broadly manageable impact.”

- Ambu shares advance as much as 11% after the Danish health-care equipment maker increased its five-year revenue target and reiterated its Ebit margin goal for the fiscal year ending September 2028.

- Pirelli shares rose as much as 2.4% in Milan after Reuters reported that Chinese shareholder Sinochem might consider selling its stake in the Italian tire maker.

- Arcadis jumps as much as 9.1%, after the provider of consulting and engineering services started repurchasing its own shares.

- Soitec shares rise much as 7.7% after the wafer maker said CEO Pierre Barnabé would step down due to personal reasons.

- Pharming shares rise as much as 7.1% after the Dutch biopharmaceutical company said its supplemental new drug application for leniolisib to treat a rare primary immunodeficiency in children was granted priority review by the US FDA.

- European sportswear stocks are on the move after US peer Nike reported better-than-expected first-quarter sales.

- Tate & Lyle falls as much as 11.5%, dropping to the lowest since July 2009, after the ingredients company said in a pre-close statement that it experienced a slowdown in market demand as the first half progressed.

- European defense stocks are falling on Wednesday as EU leaders meet informally in Copenhagen to discuss how to deal with the threat posed by drone incursions into the bloc’s airspace.

- Flutter UK shares fall as much as 5.4%, extending steep declines on Tuesday amid concern over the competitive threat posed by prediction platforms being offered by the likes of Robinhood and Kalshi.

Earlier in the session, Asian stocks were mixed, as gains in South Korea, India and Taiwan were overshadowed by declines in Japanese shares on concerns over the impact of a US government shutdown. Hong Kong and Chinese markets were shut for holidays. The MSCI Asia Pacific Index held steady, as gains in the likes of TSMC and Samsung balanced out declines in stocks like Mitsubishi UFJ Financial Group and BHP Group. Japanese and Australian blue chips weighed most heavily on the regional benchmark. Most other markets traded in the green. Japan’s monetary policy is moving in the opposite direction as the world generally moves toward easing. Stocks edged higher as the central bank left its benchmark interest rate unchanged, while signaling there may be scope to ease in coming months to support an economy taking a hit from US tariffs. Australian shares fell for a second day after the Reserve Bank left its key interest rate unchanged.

In FX, the Bloomberg Dollar Spot Index fell 0.1% to take losses into a fourth day. The shutdown threatens to delay key economic reports used to gauge the Federal Reserve’s path on interest-rate cuts; the yen is outperforming and the Swiss franc lagging.

In rates, treasuries are mixed with the curve steeper as US day begins after plying small ranges overnight. Treasury front-end and belly yields are about 1bp richer on the day with long end cheaper by about 1bp, steepening 5s10s, 5s30s spreads by 1.3bp and 2.4bp; US 10-year is 2bps lower near 4.13% with bunds and gilts in the sector trading slightly cheaper. European bonds weaker, with German 10-year yields up three basis points. US Treasuries are little changed. Eurozone inflation quickened in September, in line with economist expectations. IG dollar issuance slate is scant and a subdued session is expected amid the government shutdown. September’s $207.5 billion haul was the fifth-highest month on record and this year’s highest by a $21 billion margin. Focal points of US session include ADP’s private-sector payrolls data, which may hold more sway than usual as the shutdown threatens to delay the release of Thursday’s weekly jobless claims and the monthly jobs report slated for Oct. 3.

In commodities, oil prices wiped out an earlier rise to extend declines into a third session, Brent sliding below $66/barrel and WTI slipping under $62. Gold is extending its run, up by $34 and putting $3,900/oz in sight.

Looking at today’s calendar, US economic data slate includes September ADP employment change (8:15am), September final S&P Global US manufacturing PMI (9:45am), September ISM manufacturing and August construction spending (10am). Fed speaker slate includes Barkin (12:15pm) and Goolsbee (5pm).

Market Snapshot

- S&P 500 mini -0.5%

- Nasdaq 100 mini -0.6%

- Russell 2000 mini -0.5%

- Stoxx Europe 600 +0.5%

- DAX +0.3%

- CAC 40 +0.3%

- 10-year Treasury yield little changed at 4.15%

- VIX +0.5 points at 16.82

- Bloomberg Dollar Index -0.1% at 1198.96

- euro +0.1% at $1.1747

- WTI crude -0.9% at $61.81/barrel

Government Shutdown

- The US government officially went into shutdown, with a majority of operations halted after no funding deal was reached in the Senate, marking the first shutdown since 2018.

- House and Senate GOP leaders will hold a 10:00ET/15:00BST news conference Wednesday, according to Politico, citing sources.

- Top Overnight News

- The US government shut down at midnight for the first time since 2019 — and the third under Donald Trump — after Democrats blocked a Republican stopgap funding package. There were no signs of a resolution forthcoming. BBG

- The White House pulled the nomination of EJ Antoni to lead the BLS. Brian Quintenz is also no longer Trump’s pick to chair the CFTC, after weeks of speculation about his stalled candidacy. BBG

- Republican lawmakers said that China won’t begin purchasing US agricultural products anytime soon after a closed-door briefing. As part of the fallout from Trump’s trade war, China has yet to book a single shipment of US soybeans this season, fueling anxiety among farmers as this year’s harvest moves ahead. China is the world’s largest soybean importer. BBG

- US trade representative Jamieson Greer has warned that Washington will continue to hit its trading partners with tariffs even if some are ruled illegal by the Supreme Court later this year. The Supreme Court is set to hear cases brought by businesses challenging Trump’s use of emergency powers to impose tariffs in the first week of Nov. FT

- Taiwan pushed back on a US request to move chip production stateside to cover half of America’s demand. BBG

- Japan’s business sentiment among large manufacturers improved for a second straight quarter, according to the Tankan survey. South Korea’s adjusted exports fell 6.1% year on year in September. BBG

- India’s central bank kept its policy rate unchanged (5.5%) as U.S. tariffs continued to cloud the South Asian economy’s outlook, while signaling that it remains open to further easing. WSJ

- Eurozone inflation for Sept is right inline with expectations, including headline at +2.2% (up from +2% in Aug) and core at +2.3% (same as Aug), a development that’s a modest relief given the German CPI on Tues ran ahead of expectations. BBG

- Fed’s Logan (2026 voter) said the Fed will be cautious in any further reductions and that the US may need additional labour market slack to reach the 2% inflation target. She noted resilient consumption and business investment show policy is only modestly restrictive, adding that inflation expectations cannot be taken for granted and that financial conditions are now a tailwind, further evidence that policy is modestly restrictive. Logan said it is unclear how much further the Fed can cut before hitting neutral and warned that even excluding tariff impacts, inflation may be as high as 2.4%, driven by non-housing services, according to Reuters.

- Fed to ease Morgan Stanley’s (MS) capital requirements following a review: BBG

- US Energy Secretary said the US government is taking an equity stake in Lithium Americas (LAC), via Bloomberg TV; US DoE to take a 5% stake in Lithium Americas (LAC): ZH

- BlackRock’s (BLK) GIP is said to be nearing USD 38bln takeover of utility AES (AES): FT

- Nike Inc (NKE) Q1 2026 (USD): EPS 0.49 (exp. 0.27), Revenue 11.72bln (exp. 11.00bln). Gross margin decreased 320bps to 42.2%, primarily due to lower average selling price, reflecting higher discounts and channel mix, as well as higher tariffs in North America. CFO said tariffs will cost approximately USD 1.5bln, higher than the prior estimate of around USD 1bln, and expects Q2 revenue to fall by low single digits versus estimates of a 3.1% decline, according to Reuters. Shares rose 4.5% after hours.

Trade/Tariffs

- US Deputy Secretary of State encouraged investment from South Korea, with the US and South Korea holding a working group on visas for South Korean businesses investing in the US, according to a statement.

- South Korea and the US released a joint statement on a foreign exchange policy agreement, pledging to avoid manipulating exchange rates to gain an unfair competitive advantage. The statement did not mention a bilateral currency swap or South Korea’s state-run pension fund. Both sides agreed that FX market intervention should be reserved for combating excessive volatility and would be considered for both disorderly depreciation and appreciation. They also agreed to exchange FX intervention operations on a monthly basis and said any macroprudential or capital flow measures will not target exchange rates, according to Reuters.

- Taiwan rejected a US request to produce half of its chips locally, according to Bloomberg.

- Japanese Economy Minister Akazawa said they will operate a USD 550bln US-bound investment without causing FX impact, suggesting USD 550bln is the range where there is no FX impact, according to Reuters.

- European Commission is reportedly looking to sign the EU-Mercosur partnership agreement on December 5th, via Politico citing diplomats.

- European Commission reportedly plans to raise import tariffs on foreign steel to similar levels as US and Canada, via Reuters citing sources; expected to lift the steel import tariff level to 50%.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following modest gains on Wall Street, with focus on the length of the US government shutdown after the Senate rejected the House-passed CR, whilst Chinese participants were away for Golden Week. ASX 200 fluctuated between small gains and losses, supported by gold miners at the top of the index, while Energy and Tech lagged. BHP came under pressure after China banned its iron ore cargoes amid a pricing dispute. Nikkei 225 underperformed as the regional laggard despite a relatively mixed BoJ Tankan Survey. KOSPI was modestly firmer after above-forecast trade data, whilst reports suggested the US and South Korea agreed to establish a visa desk for Korean firms investing in the US. The two sides also issued a joint statement on foreign exchange policy, though it did not mention a bilateral currency swap or South Korea’s state-run pension fund. Nifty 50 traded flat and was little changed as the RBI kept its repo rate unchanged at 5.50% as expected in a unanimous decision, maintaining a neutral policy stance. Hang Seng and Shanghai Comp were shut for Golden Week and will return next Thursday.

Top Asian News