XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

118 C MACQUARIE FUTURES US 135

118 H MACQUARIE FUTURES US 163

323 C HSBC 195

363 H WELLS FARGO SECURITI 91

435 H SCOTIA CAPITAL (USA) 959

661 C JP MORGAN SECURITIES 15 1055

685 C RJ OBRIEN 38

737 C ADVANTAGE FUTURES 39

905 C ADM 12 3

991 H CME 17

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 1131 CONTRACTs NOTICES FOR 113,100 OZ or 3.5178 TONNES

total notices so far: 31,764 contracts for 3,176,400 OR 98.799 tonnes)

SILVER NOTICES: 39 NOTICE(S) FILED FOR 0.195 MILLION OZ/

total number of notices filed so far this month : 2913 CONTRACTS (NOTICES) for 14.565 million oz

INITIAL STANDING FOR OCT: 13.240 MILLION OZ PLUS 175,000 OZ QUEUE JUMP EQUATES TO 15.020 MILLION OZ//(

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 21.375 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 15.020 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH AN INITIAL HUGE 4.878 TONNES QUEUE JUMP FOLLOWED BY LAST 2 DAYS OF QUEUE JUMPS OF 4.5934 TONNES,(TODAY’S QUEUE JUMP = 3.623 TONNES) PLUS 8.2426 TONNES OF OUR ISSUANCE EXCHANGE FOR RISK//NEW TOTAL OF GOLD STANDING ADVANCES TO 108.5723 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 53.378 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 1402 CONTRACTS OI TO 165.859 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A MONSTER 1840 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 760 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 875 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1271 CONTRACTS AND ADD TO THE MONSTER 1840 E.FP. ISSUED

WE OBTAIN A STRONG SIZED GAIN OF 438 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $0.63 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 2.190 MILLION PAPER OZ

OCCURRED WITH OUR GAIN OF $0.63 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED

//Hang Seng CLOSED CLOSED

// Nikkei CLOSED : UP 6.12 PTS OR 0.01% //Australia’s all ordinaries CLOSED DOWN 0.28%

//Chinese yuan (ONSHORE) CLOSED XXXX OFFSHORE CLOSED DOWN AT 7.1438/ Oil DOWN TO 61.60 dollars per barrel for WTI and BRENT UP TO 65.34 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING XXXX LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN HOLIDAY IN TRADING AT XXXX AND XXXX//OFF SHORE YUAN TRADING DOWN TO 7.1435 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4147 CONTRACTS TO 483,672 OI WITH OUR STRONG GAIN IN PRICE OF $68.70 WITH RESPECT TO MONDAY’S // TRADING COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1510). WE HAD NO T.A.S. LIQUIDATION MONDAY. WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 5657 CONTRACTS (OR 17.575 TONNES).THEN WE WERE NOTIFIED A ZERO CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0.00 TONNES OF GOLD.

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED REMAIN AT 8.2426 TONNES OF GOLD FOOR THE MONTH OF OCTOBER.\

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 4 ISSUANCES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES: TOTAL ISSUANCES 4 TIMES FOR 2650 CONTRACTS OR 26500 OZ OR 8.2426 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. TOTAL ISSUANCE ON 4 OCCASIONS: 8.2426 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 126.5 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 118.5 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024

DETAILS ON OCTOBER COMEX MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 6,643 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER/OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1603 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN THIS PAST WEDNESDAY/RIGHT BEFORE FIRST DAY NOTICE, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE (MARCHING TO WILLIAM TELL’S OVERTURE) WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS CONTINUED LAST THURSDAY AND FRIDAY, OCT 1 AND OCT 2 AND THAT IS THE REASON WHY WE ARE HAVING HUGE DISTORTED COMEX OPEN INTEREST LOSSES IN OI. HOWEVER THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE/OCTOBER COMEX GOLD TOTALS WITH MASSIVE GOLD TONNES STANDING FOR GOLD AND THE HUGE QUEUE JUMPING THAT FOLLOWED!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS NOW BRINGS US TO OCTOBER WHERE INITIAL AMOUNT OF GOLD STANDING IS 28,988 CONTRACTS FOR 90.114 TONNES OF GOLD TO WHICH WE ADD OUR FIRST MASSIVE QUEUE JUMP OF 4.898 TONNES QUEUE JUMP FOLLOWED BY OCT 4 QUEUE JUMP OF 0.9704 TONNES TO BE FOLLOWED BY OCT 7 QUEUE JUMP OF 3.623 TONNES AND THIS WAS AUGMENTED BY AN UNUSUAL 50,000 CONTRACT EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE AND THEN ON THREE CONSECUTIVE OCCASIONS, OCT 2 THROUGH TO THE OCT 4. THE NEW TOTAL ON THESE 4 ISSUANCES IS 2650 CONTRACTS FOR 26500 OZ OR 8.2426 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERIES INCLUDING QUEUE JUMPS. NEW TOTALS FOR GOLD STANDING: 108/5723 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 242 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH OCTOBER AND SUBSEQUENT STANDING FOR GOLD.

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 7, 3.623 TONNES OF QUEUE JUMP TO OUR INITIAL 50,000 OZ OR 1.555 TONNES OF EX FOR RISK. THIS WAS FOLLOWED ON OCT 2 , OCT 3, OCT 4 FOR 2150 CONTRACTS EXCHANGE FOR RISK//215,000 OZ//NEW TOTALS EXCHANGE FOR RISK/4 OCCASIONS IS 2,650 CONTRACTS FOR 265,000 OZ OR 8.2426 TONNES.!

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

TOTAL EXCHANGE FOR RISK OCT: 8.2426 TONNES

D) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

E) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

F) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

EQUALS

108.5723 TONNES OF GOLD!!

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1510 CONTRACTS.

THAT IS A FAIR SIZED 1510 EFP CONTRACT WAS ISSUED: : /DEC 1510 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1510 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY + GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE SEPT 30 WITH OUR ATTEMPTED FAILED RAID, FOLLOWED BY ANOTHER RAID OCT 2 AND THAT ENDED IN TOTAL FAILURE! TODAY OCT 7 WE WITNESS A SMALL RAID TRYING TO STOP GOLD’S ADVANCE TO THE 4000 BARRIER!!

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED SIZED 1603 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING MASSIVE LOSS OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 4 ISSUANCES FOR 8.2436 TONNES

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY;S 3.623 TONNES OF A QUEUE JUMP WHICH MUST BE ADDED TO OUR 4 ISSUANCES OF 8.2426 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH IS 108.5723 TONNNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $68.70./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY .THIS WAS COUPLED WITH GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION) /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS TRIED AGAIN LATE WEDNESDAY-THURSDAY OCT 2 WITH CHINA OUT FOR A WEEK, WITH NOT MUCH LUCK. WITH CHINA COMING BACK ON THURSDAY OCT 9 THE CROOKS NEEDED TO RAID TODAY TRYING DESPERATELY TO HALT GOLD’S ADVANCE.

SATURDAY MORNING//FRIDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN OF A TOTAL OF 17.575 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES TO BE FOLLOWED BY TODAY’S HUGE 3.623 TONNES OF QUEUE JUMP TO WHICH WE ADD OUR 8.2426 TONNES EX FOR RISK/4 OCCASIONS:

/ NEW TOTAL STANDING 108.5723 TONNES.

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $68.70

WE HAD A HUGE 986 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 5657 CONTRACTS OR 565,700 0Z (17.595TONNES)

speculators have left the gold arena

INITIAL GOLD COMEX

OCT CONTRACT MONTH

OCT 7 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 3 entries i) Out of Loomis: 48,226.500 oz (2545 kilobars) ii) Out of Malca: 49,930.503 oz (1553 kilobars) iii) Out of Manfra 44,947.098 oz (1398 kilobars) total withdrawal 143,104.1012 oz or 4.451 tonnes of gold . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 2 ENTRIES i) Into Brinks customer account: 81,824.295oz (2545 KILOBARS) ii) Into Loomis: 48,226.500 (1500 kilobars) total deposit 130,050.795 OZ in tonnes: 4,045 tonnes xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1131 notice(s) 113,100 OZ 3.5178 TONNES |

| No of oz to be served (notices) | 492 contracts 49,200OZ 1.530 TONNES |

| Total monthly oz gold served (contracts) so far this month | 31,764 notices 3,176,400 oz 98.799 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

total deposit dealer: nil oz

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

2 ENTRIES

i) Into Brinks customer account: 81,824.295oz (2545 KILOBARS)

ii) Into Loomis: 48,226.500 (1500 kilobars)

total deposit 130,050.795 OZ

in tonnes: 4,045 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

3 entries

i) Out of Loomis: 48,226.500 oz (2545 kilobars)

ii) Out of Malca: 49,930.503 oz (1553 kilobars)

iii) Out of Manfra 44,947.098 oz (1398 kilobars)

total withdrawal 143,104.1012 oz

or 4.451 tonnes of gold

ADJUSTMENTs 4

2 dealer to customer

i)Asahi 20,278.939 oz

ii) JPMorgan: 13,692.774 oz

last two customer to dealer:

c) Brinks 177,289.405 oz

d) Loomis 180,270.657 oz

volume at the comex: Monday: 295,216 oz (good)

AMOUNT OF GOLD STANDING FOR OCTOBER

THE FRONT MONTH OF OCTOBER STANDS AT 1623 CONTRACTS FOR A GAIN OF 980 CONTRACTS.

WE HAD 185 CONTRACTS FILED ON MONDAY SO WE GAINED A MONSTROUS 1,165 CONTRACT QUEUE JUMP FOR 116,500 OZ OR 3.623 TONNES OF GOLD. THUS OUR NEW NORMAL DELIVERY RISES TO 100.3297 TONNES WHICH INCLUDES A PREVIOUS QUEUE JUMP) PLUS OUR 8.2426 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD; 108.5723 TONNES

NOVEMBER GAINED 91 CONTRACTS UP TO 4552 CONTRACTS.

DECEMBER GAINED 1437 CONTRACTS UP TO 391,376 CONTRACTS.

We had 1131 contracts filed for today representing 113,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 15 notices issued from their client or customer account. The total of all issuance by all participants equate to 1131 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 1055 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (31,764 oz ) to which we add the difference between the open interest for the front month of OCT ( 1623 CONTRACTS) minus the number of notices served upon today (1131 x 100 oz per contract) equals 3,225,600 OZ OR 100.3297 TONNES OF GOLD TO WHICH WE ADD OUR 4 ISSUANCES OF 8.2426 TONNES OF EXCHANGE FOR RISK //NEW TOTALS STANDING FOR GOLD OCTOBER ADVANCES TO 108.5723 TONNES

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (31,764 x 100 oz +we add the difference for front month of OCT. (1623 OI} minus the number of notices served upon today (1131 x 100 oz) which equals 3,225,600 OZ OR 100.3297 TONNES + 8.2426 TONNES EXCHANGE FOR RISK//NEW TOTAL OF GOLD STANDING IN OCTOBER: 108.5723 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 108.5723 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,958,564.190 oz 60.888 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 40,1944,494.314 oz

TOTAL REGISTERED GOLD 21,795,091.673 or 667.85 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,379,402.637 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 1,983,652oz ((REG GOLD- PLEDGED GOLD)= 616.999 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

OCT 7 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries 2 entries a) Out of Brinks 379,298.630 oz b) Out of Loomis 601,016.340 oz total withdrawal: 980,315.870 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 entries i) Into Asahi 379,299.630 oz total deposit; 379,299.630 oz oz |

| No of oz served today (contracts) | 39 CONTRACT(S) ( 0.195 MILLION OZ |

| No of oz to be served (notices) | 101 contracts (0.505 MILLION oz) |

| Total monthly oz silver served (contracts) | 2913 Contracts (14.565 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 entries

i) Into Asahi 379,299.630 oz

total deposit: 379,299.630 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

2 entries

a) Out of Brinks 379,298.630 oz

b) Out of Loomis 601,016.340 oz

total withdrawal: 980,315.870 oz

adjustments: 3 all dealer to customer

a) Brinks 361,763.780 oz

b) JPMorgan: 367,118.200 oz

c) Out of Loomis: 92,818.620 oz

TOTAL REGISTERED SILVER: 188.874 MILLION OZ//.TOTAL REG + ELIGIBLE. 530.331 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 130 OPEN INTEREST CONTRACTS FOR A LOSS OF 20 CONTRACTS.

WE HAD 55 CONTRACTS SERVED ON MONDAY, SO WE GAINED 35 CONTRACTS WHICH UNDERWENT A STRONG QUEUE JUMP OF 175,000 OZ.

STANDING FOR SILVER OCT ADVANCES TO 15.020 MILLION OZ

NOVEMBER LOST 4 CONTRACTS UP TO 2504

DECEMBER LOST 1979 CONTRACTS DOWN TO 130,757

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 39 or 195,000 oz

CONFIRMED volume; ON MONDAY 90,955 huge//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 2913 X5,000 oz = 14.565 MILLION oz

to which we add the difference between the open interest for the front month of OCT (130) AND the number of notices served upon today (39 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (2913) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(130) minus number of notices served upon today (39)x 5000 oz equals silver standing for the OCT.contract month equating to 15.020 MILLION OZ

New total standing: 15.020 million oz which is HUGE for this NON active delivery month of OCT. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 188.874 million oz of registered silver

JPMorgan as a percentage of total silver: 210.514/530.331million. 39.70`%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

GLD INVENTORY: 1013.17 TONNES, TONIGHTS TOTAL

SILVER

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

CLOSING INVENTORY 492.262 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

Recession Watch: How Is This Economy Still Growing?

Answer: It isn’t

| John RubinoOct 7 |

The stock market is a pretty good barometer of economic health…except when it’s contradicted by employment. Currently, even profitable companies aren’t hiring:

When job openings dry up, the unemployed stay that way for longer:

Government hiring usually counteracts weakness in the private sector. But not this time:

The longer someone is unemployed, the harder it is to manage their debts:

Including their mortgages:

The further down one is on the economic ladder, the harder the hit:

McDonald’s CEO says lower-income customers are skipping breakfast

(MSN) – In an interview with CNBC on September 3, Kempczinski highlighted that traffic for lower-income customers is “down double digits.”

“And it’s because people are either choosing to skip a meal — so we’re seeing breakfast, people are actually skipping breakfast — or they’re choosing to just eat at home.”

Delaying the Inevitable

So why isn’t the US already in a deep recession? Because governments are borrowing record amounts of money and spending it on social programs, weapons procurement, and infrastructure. This keeps people spending, but at the cost of soaring debt:

Why can’t governments just keep doing this? Because the bond markets won’t let them. Below are the 10-year government bond yields for Japan and France. Note that while their debt is soaring, their interest costs are rising even faster as bond investors demand higher yields.

This, in short, is a classic setup for a financial death spiral.

end

JAMES RICKARDS

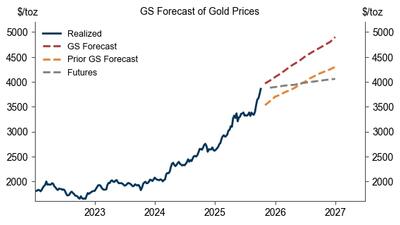

GOLDMAN SACHS HEADLINE;

Goldman Hikes Gold Forecast To $4,900 As Ken Griffin Worries About “Substantial De-Dollarization”

Gold futures (Dec) topped $4,000 for the first time this morning (though spot prices not quite there yet)…

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

Mike Maharrey: Who in his right mind would hold dollars now?

Submitted by admin on Mon, 2025-10-06 11:30 Section: Daily Dispatches

By Mike Maharrey

Money Metals Exchange, Eagle, Idaho

Monday, October 6, 2025

Nobody in their right mind would hold their reserves in dollars.

That’s the conclusion of Catalyst Funds CIO David Miller. And he’s right.

Gold is up over 87% since January 2024 and is knocking on the door of $4,000 an ounce. But even with the rapid price surge, Miller said gold is not overpriced.

The appreciation of gold is the flip side of the dollar’s depreciation. In other words, gold is tracking inflation. …

… For the remainder of the commentary:

END

Byron King: The New York Times has missed the silver and gold story

Submitted by admin on Tue, 2025-10-07 11:11 Section: Daily Dispatches

By Byron King

Daily Reckoning, Baltimore

Tuesday, October 7, 2025

I read the New York Times — but only so that you don’t have to. Often as not, it’s painful to peruse the raw sophistry and unreflective bias in many of the news articles, let alone the poison-pen editorial page, but still I power through.

Fortunately, though, the world offers many other news sources which help me figure out what’s happening across the globe

And much is happening. So much, in fact, that I’m not entirely sure where to begin. And when I’m not sure how to approach a vast mix of events, my default position is to begin with a look at the price of silver and gold, which together tend to distill quite a few earthly matters into a couple of easily understandable numbers. …

… For the remainder of the commentary:

END

Craig Hemke: Gold and silver shortages are exploding

Submitted by admin on Sat, 2025-10-04 20:00 Section: Daily Dispatches

By Craig Hemke

Sprott Money, Toronto

Wednesday, October 1, 2025

As September 2025 came to a close, gold closed up 11% for the month, pushing well into all-time high territory. In this month-end wrap-up, market analyst and mining executive David Jensen offered a stark and data-rich breakdown of the underlying dynamics fueling this rally.

While many market watchers cheer rising prices, Jensen’s analysis paints a deeper, more structural concern.

“We’ve got price backwardation where the spot price is higher than the futures price all the way out to 12 months,” Jensen explained, signaling an intense demand for physical metal in the here and now — demand that outpaces supply by a wide margin.

Beyond the headlines and price charts, Jensen emphasized that the physical precious metals markets, especially gold and silver, are in deep distress, mainly due to the fractional-reserve-style paper trading systems in places like London.

“This market is dominated with price setting in the UK and in London. … You don’t have to have the metal to sell immediate ownership of metal,” he said, revealing the core of the issue: Promissory notes are outstripping physical inventory. With lease rates now exceeding 5% and backlogs building, the system is under growing pressure. …

… For the remainder of the analysis:

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 243/

5. COMMODITY REPORT SILVER

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED

//Hang Seng CLOSED CLOSED

// Nikkei CLOSED : UP 6.12 PTS OR 0.01% //Australia’s all ordinaries CLOSED DOWN 0.28%

//Chinese yuan (ONSHORE) CLOSED XXXX OFFSHORE CLOSED DOWN AT 7.1438/ Oil DOWN TO 61.60 dollars per barrel for WTI and BRENT UP TO 65.34 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING XXXX LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN HOLIDAY IN TRADING AT XXXX AND XXXX//OFF SHORE YUAN TRADING DOWN TO 7.1435 AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED HOLIDAY

OFFSHORE YUAN: DOWN TO 7.1435

HANG SENG CLOSED HOLIDAY

2. Nikkei closed UP 6.12 PTS OR 0.01%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 98.12 EURO FALLS TO 1.1669 DOWN 40 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.6710//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.77…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.275 DOWN 2 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: XXX OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7353// Italian 10 Yr bond yield UP to 3.596 SPAIN 10 YR BOND YIELD UP TO 3.278

3i Greek 10 year bond yield UP TO 3.434

3j Gold at $3954.75 Silver at: 48.30 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 23 /100 roubles/dollar; ROUBLE AT 81.76

3m oil (WTI) into the 61 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.07/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.671% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.275 DOWN 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7976 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9308 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.175 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.767 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.599 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.70 UP 1 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.7520 UP 2 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.576 UP 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.222 UP 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.754 UP 2 BASIS PTS.

2a New York OPENING REPORT

Futures Flat As AI Bubble Euphoria Takes A Break

Tuesday, Oct 07, 2025 – 08:36 AM

Futures are flat after the S&P, Nasdaq and Russell all made new ATHs yesterday, driven by the AI theme and a broad-based rally. As of 8:15am, S&P futures are unchanged while Nasdaq futures eke out a 0.1% gain as trader keep an eye on TSLA’s new car announcement with Mag7 names mixed pre-mkt but Semis seeing a bid led by AMD (+3.6%), MU (+2%). Bond yields are higher while the USD gained for a second day as President Trump sent mixed messages about the state of talks with Democrats on their biggest demand to end the shutdown; the stronger dollar may pressure international/ADR plays today according to JPM. There are four Fed speakers today and a 3Y bond auction with the shutdown pausing official data.

In premarket trading, Mag 7 stocks are mixed (Tesla -0.6%, Nvidia +0.3%, Alphabet -0.5%, Microsoft -0.2%, Apple -0.3%, Amazon +0.1%, Meta Platforms +0.2%).

- Advanced Micro Devices (AMD) rises 3%, set to extend Monday’s rally, as Jefferies upgrades to buy following the chipmaker’s deal with OpenAI.

- Aehr Test Systems (AEHR) falls 21% after the maker of semiconductor equipment posted fiscal first-quarter revenue that fell from the year-ago period.

- Amkor (AMKR) is up 10% after the company broke ground on an outsourced semiconductor advanced packaging and test campus in Arizona.

- Constellation Brands (STZ) is up 3% after the owner of the Corona and Modelo Especial brands in the US reported comparable earnings per share for the second quarter that beat the average analyst estimate.

- Ford (F) slips 1% after the Wall Street Journal reported that the company faces months of disruptions to its business after a major fire at an aluminum plant in New York.

- IBM (IBM) rises 4% after the technology firm said it will integrate Anthropic’s Claude family of large language models into its software portfolio.

- Intercontinental Exchange (ICE), owner of the New York Stock Exchange, climbs 3% amid plans to invest $2 billion in Polymarket, a crypto-based betting platform.

- Trilogy Metals (TMQ) gains 220% as the White House said US will take a 10% stake in the small-cap mineral exploration company.

In corporate news, Tesla is said to plan unveiling a cheaper version of the Model Y today. Ford faces months of disruptions to its business after a major fire at an aluminum plant in New York, the WSJ reported. Elon Musk named a former Morgan Stanley executive as the CFO of xAI, the FT reported.

After hitting yet another AI-driven record high, stocks are seeing some fatigue as the rally runs on fumes. It’s hardly surprising, after the latest meltup, as traders contemplate the government shutdown stretching into a second week, political shocks overseas and the latest tariffs. Even tech might struggle, with Citi strategists cautioning that investors may want to cash in.

The market’s latest winning streak has been fueled by AI euphoria and optimism about earnings, but those drivers could reach a limit. “Profit-taking risks have rapidly risen across markets, and are particularly elevated for Nasdaq, potentially hampering further upside,” according to Citi’s Chris Montagu. Meanwhile, AI valuations are nearing extremes, with the SOX Index’s forward P/E ratio approaching three standard deviations above the 15-year average. Still, tech news keeps coming, and it seems like anything OpenAI touches turns to gold.

Monday’s AMD deal was the latest big-budget data center agreement this year. It follows last month’s announcement that Nvidia Corp. was planning to invest as much as $100 billion in OpenAI amid demand for tools like ChatGPT and the computing power needed to make them run. Tech firms are spending hundreds of billions of dollars on advanced chips and data centers, and the final bill may run into the trillions. The financing is coming from venture capital, debt and, lately, some more unconventional arrangements that have raised eyebrows on Wall Street.

While equities worldwide have surged to successive record highs, worries over the US government stalemate and the political crisis in France have driven investors toward alternative assets such as gold and Bitcoin, sending both to new peaks in what has been dubbed the “debasement trade.” At the same time, a flurry of AI-related deals among chipmakers has propelled shares higher and fueled some concerns of a speculative bubble reminiscent of the late-1990s dot-com era.

“Enthusiasm for stocks is starting to wane after another record-breaking start to the week for Wall Street,” said Kathleen Brooks, research director at XTB Ltd. That keeps the debasement trade in play, she said. “As global political risks rise, this is continuing to drive demand, and we think that the early morning pullback in the gold price is likely to be used as a buying opportunity.”

In political news, the government shutdown extends into a 7th day and Trump said he would negotiate with Democrats over health care subsidies, a move that could open the door to resolving the shutdown. Carlyle Group is releasing its own estimates of US data to fill the void. The investment manager estimates that just 17,000 jobs were created in September, among the weakest results since the US economy emerged from the 2020 recession.

Meanwhile, Citadel’s Ken Griffin warned that investors are starting to view gold as a safer asset than the dollar, a development that the billionaire investor called “really concerning.”

Not everyone is concerned about the AI bubble however: there are the usual commission-based traders whose paycheck depends on a continuation of the status quo, like Pepperstone’s Michael Brown. The Mag 7 group of tech giants that have powered the bulk of the S&P 500 rally in recent years are trading at valuations in line with their five-ear averages, he said.

“If you’re now about to tell me that they’ve been expensive for five years, well those seven stocks have delivered a total return of >300% in that period of time, and look set to rally even further in the coming months,” Brown said. “In fact, the path of least resistance for the market at large continues to lead to the upside, as earnings growth remains strong, the underlying economy remains resilient, and as the monetary policy backdrop becomes increasingly loose.”

Elsewhere, Europe’s Stoxx 600 benchmark edged higher. France’s CAC 40 reversed an early decline as President Emmanuel Macron made a last-ditch effort to salvage the government after Prime Minister Sebastien Lecornu’s resignation on Monday. Truckmakers including Volvo AB and Daimler Truck Holding AG fell after US President Donald Trump said 25% duties on medium- and heavy-duty trucks would begin next month. Here are the biggest movers Tuesday:

- Kering shares rise as much as 5.4% to the highest since July 2024, after the Gucci owner was named the top pick among luxury stocks at Morgan Stanley and upgraded to overweight alongside LVMH

- NKT jumps to a record high after Jefferies raises its recommendation on the Danish energy transmission firm to buy, predicting strong expansion in high voltage capacity. French peer Nexans slips as much as 5.1%, on cut to hold

- Shell shares rise as much as 2.3%, the most since July. The company gave an October trading update that analysts saw as upbeat, forecasting higher 3Q integrated gas production and upstream volumes

- Ambu gains as much as 4.9% after Bernstein raised the recommendation to outperform from market perform, citing the medical device firm’s unique growth profile and strong market position

- Skanska shares rise as much as 5%, the most since April 10, after Jefferies upgraded the Swedish construction group to buy from hold, saying growing momentum in end markets like commercial property is underappreciated

- CVS Group shares rise as much as 10%, to the highest since March 2024, after the UK veterinary service and animal medicines company reported full-year results. Analysts were cheered by a year-on-year improvement in margins

- Imperial Brands shares rise as much as 3.7%, rebounding from a two-month low, after the tobacco company said it will increase its share buyback in FY26. RBC Capital Markets also sees scope for small upgrades to consensus

- Rentokil gains as much as 4.6% after Bernstein double-upgrades to outperform and installs a new Street-high 570p price target, saying the pest controller has a path toward stronger organic growth

- TomTom gains as much as 6.6%, the most in a month, after Kepler Cheuvreux upgraded the Dutch mapping and navigation company to buy on improving near-term free cash flow and attractive long-term prospects

- B&M European Value Retail shares drop as much as 22%, marking a record drop that has sent shares to an all-time low. CEO Tjeerd Jegen warned operational execution has been “weak” and weighed on first-half performance

- Rheinmetall shares fall as much as 2.8%, to the lowest level in nearly a month as analysts came away from a conference call expecting a slow 3Q. Deutsche Bank analysts say the firm’s quarterly results are likely to fall short

- HelloFresh shares drop as much as 7.1%, slipping to their lowest level in almost a month, after the USDA’s Food Safety and Inspection Service issued a public health alert concerning ready-to-eat meals sold by the company

- Liontrust drops as much as 6.7% after reporting net outflows and a drop in assets under management in the second quarter. RBC said there has been a reversal in progress following two consecutive quarters in net flows

Asian shares traded steady after a six-day rally, as Japanese markets failed to hold initial gains amid an indecisive mood across global peers. The MSCI Asia Pacific Index gained as much as 0.4% before giving up the advance to trade little changed. Tech-heavy Taiwan shares were among key gainers, while stocks in Singapore and India also gained. Japanese shares ended flat. Markets in China, Hong Kong and South Korea remained closed for holidays. Australian stocks fell, bucking the broader region’s advance. A financial regulator approved Cboe Global Markets’ application to conduct local stock listings, spurring a decline in shares of the nation’s main exchange operator ASX Ltd. Stocks in India rallied for fourth straight session as the central bank’s recent credit easing measure boost local lenders.

In FX, the Bloomberg Dollar Spot Index rises 0.2% and stronger against most G-10 currencies, New Zealand dollar lags as investors ramp up bets on cuts by the central bank, which announces its latest decision on Wednesday.

In rates, treasury yields continue to grind higher led by long-end tenors, extending Monday’s curve-steepening selloff. Bunds underperform along with French bonds, which extend declines as President Macron seeks last-ditch talks to avoid a government collapse, giving outgoing Prime Minister Sebastian Lecornu 48 hours to negotiate. US yields are 1bp-3bp cheaper on the day with 2s10s and 5s30s curves steeper by less than 1bp; 10-year near 4.17% is up about 2bp vs Monday’s close with Germany’s cheaper by an additional basis point. Treasury auction cycle begins at 1pm New York time with $58 billion 3-year new issue, to be followed by $39 billion 10-year and $22 billion 30-year reopenings Wednesday and Thursday. Focal points of US session include 3-year note auction, first of this week’s three coupon sales, and several Fed speakers.

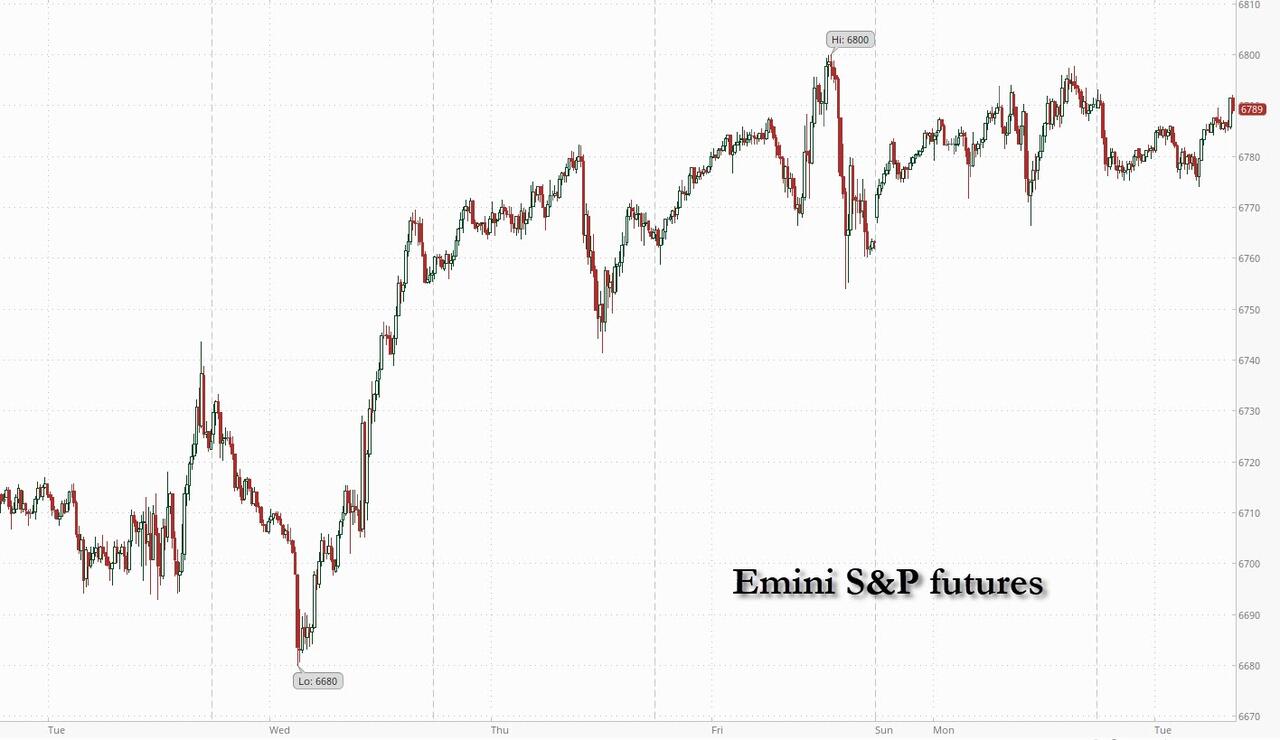

In commodities, gold swooned after hitting another record, but recovers to trade little changed at $3,959/oz. Oil prices falling, with Brent trading around $65.20/barrel.

The US economic calendar — still subject to delays from the ongoing government shutdown — includes August trade balance (8:30am), New York Fed 1-year inflation expectations (11am) and consumer credit (3pm). Fed speaker slate includes Bostic (10am), Bowman (10:50am), Miran (10:30am, 4:05pm) and Kashkari (11:30am).

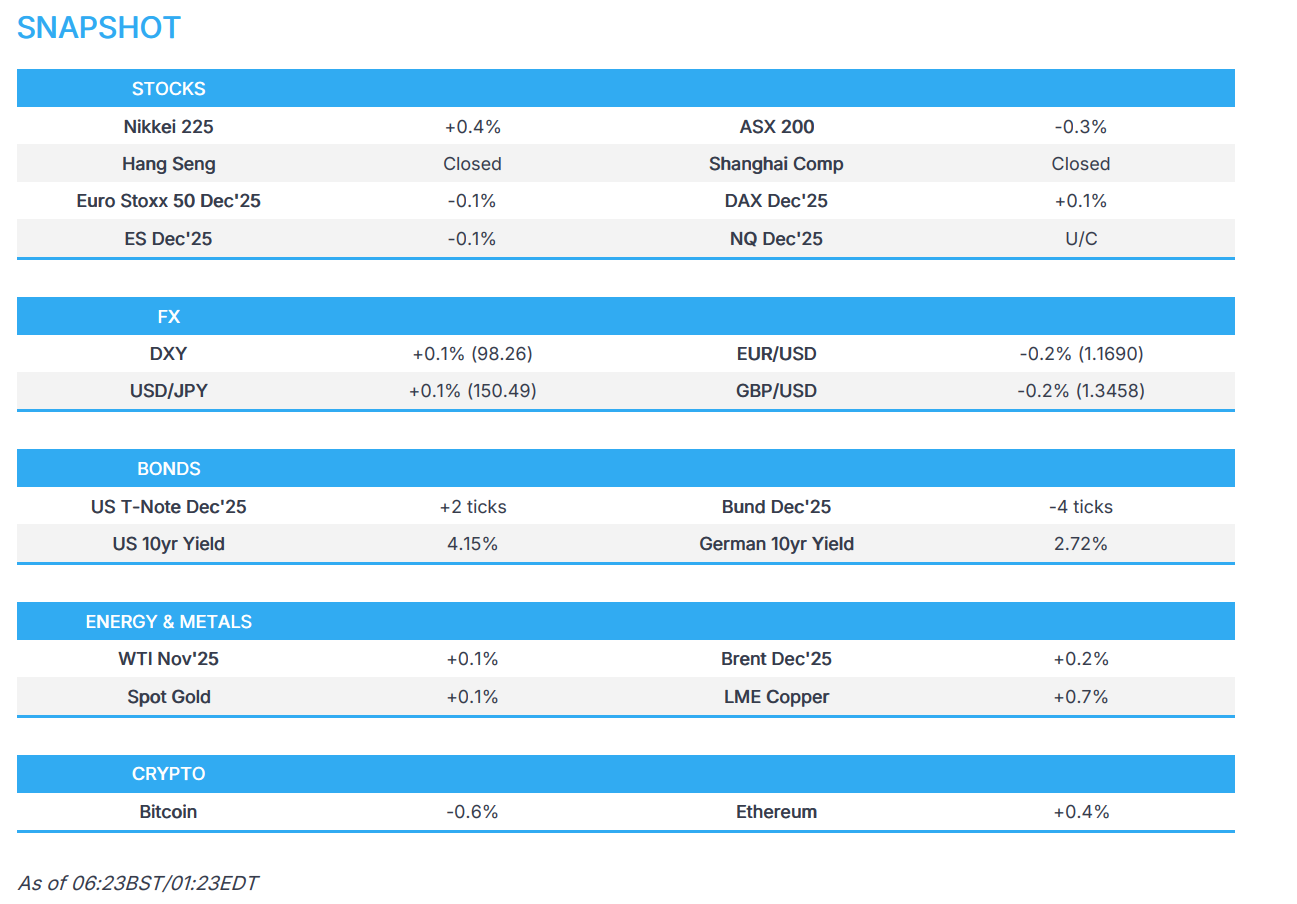

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini little changed

- Russell 2000 mini little changed

- Stoxx Europe 600 little changed

- DAX little changed

- CAC 40 little changed

- 10-year Treasury yield +1 basis point at 4.17%

- VIX +0.2 points at 16.55

- Bloomberg Dollar Index +0.2% at 1207.19

- euro -0.4% at $1.1665

- WTI crude -0.6% at $61.34/barrel

Top Overnight News

- The Trump administration is expected to announce a plan as soon as Tuesday to bail out U.S. farmers stung by trade disputes and big harvests, with the initial outlay potentially totaling up to $15 billion, according to sources familiar with the matter. RTRS

- In the midst of the shutdown, Senate Minority Leader Chuck Schumer said Monday there are no pending bipartisan talks over expiring health insurance subsidies despite a claim from President Donald Trump. Politico

- US White House memo says furloughed federal workers are not entitled to back pay for the time that is taken off during the government shutdown: Axios.

- A paycheck scheduled on Oct. 15 for the 1.3 million members in the armed services might convince legislators and the White House that missing the date won’t be worth the political cost. While the respective sides have dug in their heels regarding the fiscal budget, missing a pay period could rile public anger. At the least, it encourages a temporary bill known as a continuing resolution. CNBC

- Trump said layoffs could be triggered if the Senate vote on the shutdown fails, while he added that negotiations are ongoing with Democrats and he would make a deal on Affordable Care Act subsidies. Trump later posted “Democrats have SHUT DOWN the United States Government right in the midst of one of the most successful Economies, including a Record Stock Market, that our Country has ever had…I am happy to work with the Democrats on their Failed Healthcare Policies, or anything else, but first they must allow our Government to re-open.”

- Schumer said Democrats will be at the table if President Trump is ready to work with Democrats on ending the government shutdown and get something done on health care for American families, while Schumer stated that Trump is not yet negotiating with US Congress Democratic leaders. Furthermore, he separately commented that they are making progress on the government shutdown.

- Democrat and Republican bills to end the US government shutdown failed to secure sufficient votes for passage in the Senate, as expected.

- Trump said he would invoke the Insurrection Act if people were being killed, and courts and local officials were holding us up, while it was later reported that Trump said what’s happening in Portland is insurrection, according to a Newsmax interview. Furthermore, Trump said he called into federal service at least 300 members of the Illinois National Guard until the governor consents to a federally funded mobilization.

- US federal judge declined to immediately block President Trump’s deployment of National Guard troops to Illinois, according to the New York Times.

- China is rapidly building oil storage capacity as the country rushes to accumulate energy stockpiles. RTRS

- French shares declined for a second consecutive session as President Emmanuel Macron made a last-ditch effort to salvage his government, giving PM Sebastien Lecornu until Wednesday night to form a plan. BBG

- The White House is looking to sell parts of the government’s $1.6T portfolio of student loans although doing so will be extremely complicated from a logistical and legal standpoint. Politico

- Japan had a solid 30-year bond auction with firm demand, calming a jittery market following the surprise victory of pro-stimulus conservative Sanae Takaichi in the ruling party leadership race. BBG

- The US Labor Department’s September employment report, whose scheduled release on Oct. 3 was among those that have been postponed since the shutdown began last week, was expected by economists in a Bloomberg poll to show a 54,000 increase in nonfarm payrolls from August’s total of about 159 million. Carlyle estimates that just 17,000 jobs were created, among the weakest results since the US economy emerged from the 2020 recession. BBG

- Goldman raised its Dec 2026 gold price forecast to $4,900/toz (vs. $4,300 prior) because the inflows driving the 17% rally since August 26th – Western ETF inflows and likely central bank buying – are sticky, effectively lifting the starting point of the price forecast. In contrast, noisier speculative positioning has remained broadly stable: GS

Trade/Tariffs

- Japan’s Chief Cabinet Secretary Hayashi said he is aware of US President Trump’s comments on truck tariffs, while he added that they will assess the details once clarified and will respond appropriately.

- Trump will meet with Carney at 11.45EDT/16:45BST on Tuesday.

A more detailed look at global markets courtesy of Newsquawk

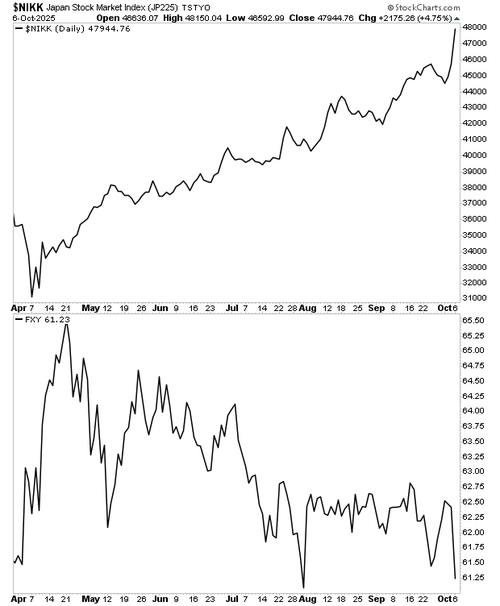

APAC stocks traded mixed despite the tech-led advances on Wall St with several holiday closures including Mainland China, Hong Kong and South Korea, while Japanese stocks rallied again as the post-LDP election euphoria persisted. ASX 200 was subdued amid losses in Telecoms, Consumer Discretionary and Tech, with sentiment also not helped by weaker Consumer Confidence. Nikkei 225 printed fresh record highs once again amid ongoing tailwinds from the dovish expectations associated with the incoming Takaichi government, while Japanese Household Spending also topped forecasts.

Top Asian News

- Japanese LDP chief Takaichi said she is truly hoping to work together with US President Trump to make their alliance even stronger and more prosperous, as well as advance a free and open Indo-Pacific.