XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

118 C MACQUARIE FUTURES US 125

118 H MACQUARIE FUTURES US 229

323 C HSBC 42

332 H STANDARD CHARTERED B 313

435 H SCOTIA CAPITAL (USA) 746

657 H MORGAN STANLEY 1052

661 C JP MORGAN SECURITIES 457 631

709 C BARCLAYS 280

732 H RBC CAP MARKETS 200

905 C ADM 5 4

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 2042 CONTRACTs NOTICES FOR 204,200 OZ or 6.3014 TONNES

total notices so far: 33,806 contracts for 3,380,600 OR 105.052 tonnes)

SILVER NOTICES: 519 NOTICE(S) FILED FOR 2.595 MILLION OZ/

total number of notices filed so far this month : 3432 CONTRACTS (NOTICES) for 17.160 million oz

INITIAL STANDING FOR OCT: 13.240 MILLION OZ PLUS 2.615 MILLION OZ QUEUE JUMP EQUATES TO 17.635 MILLION OZ//

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 28.725 MILLION OZ (WILL BE HUGE THIS MONTH)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 17.635 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH AN INITIAL HUGE 4.878 TONNES QUEUE JUMP FOLLOWED BY LAST 3 DAYS OF QUEUE JUMPS OF 11.5354 TONNES,(TODAY’S QUEUE JUMP = 6.942 TONNES) PLUS 11.353 TONNES OF OUR ISSUANCE EXCHANGE FOR RISK/5 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 118.5194 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 64.466 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 746 CONTRACTS OI TO 166,474 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A MONSTER 1470 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1470 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 875 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 781 CONTRACTS AND ADD TO THE MONSTER 1470 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 2216 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $0.89 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 11.080 MILLION PAPER OZ

OCCURRED WITH OUR LOSS OF $0.89 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED

//Hang Seng CLOSED CLOSED

// Nikkei CLOSED : DOWN 215.39 PTS OR 0.45% //Australia’s all ordinaries CLOSED DOWN 0.09%

//Chinese yuan (ONSHORE) CLOSED XXXX OFFSHORE CLOSED DOWN AT 7.1469/ Oil UP TO 62.33 dollars per barrel for WTI and BRENT UP TO 65.95 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING XXXX LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN HOLIDAY IN TRADING AT XXXX AND XXXX//OFF SHORE YUAN TRADING DOWN TO 7.1469 AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1887 CONTRACTS TO 485,559 OI WITH OUR STRONG GAIN IN PRICE OF $28.90 WITH RESPECT TO TUESDAY’S // TRADING COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3565). WE HAD NO T.A.S. LIQUIDATION MONDAY BUT DID HAVE A STRONG LIQUIDATION OF GOLD/SILVER EQUITY SHARES…GO FIGURE!!. WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 5452 CONTRACTS (OR 16.958 TONNES).THEN MUCH TO MY SURPRISE WE WERE NOTIFIED OF A MASSIVE 1000 CONTRACTS EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR 100,000 OZ OR 3.11041 TONNES OF GOLD.

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT ADVANCES TO 11.353 TONNES OF GOLD UNDER THE GUIDANCE OF 5 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 5 ISSUANCES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO TODAY, OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES TOTAL ISSUANCES 5 OCCASIONS FOR 3650 CONTRACTS OR 365,000 OZ OR 11.353 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN FINALLY OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES TOTAL ISSUANCE ON 5 OCCASIONS: 11.353 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 129.6 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 118.5 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. . PLEASE SEE THE LETTER WRITTEN TODAY AND YOU WILL FIND IT UNDER CHRIS POWELL OF GATA’S DISPATCHES. YOU WILL FIND IT FASCINATING!!

DETAILS ON OCTOBER COMEX MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 6,643 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER/OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A HUGE T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 5362 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN THIS PAST WEDNESDAY/RIGHT BEFORE FIRST DAY NOTICE, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE (MARCHING TO WILLIAM TELL’S OVERTURE) WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD. WITH MUCH FAILURES THE CROOKS DECIDED TO RAID OUR EQUITY SHARES WHERE WE WITNESSED A HUGE DOWNFALL IN PRICES DESPITE GOLD’S HUGE ADVANCE IN PRICE.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS CONTINUED LAST THURSDAY AND FRIDAY, OCT 1 AND OCT 2 AND THAT IS THE REASON WHY WE ARE HAVING HUGE DISTORTED COMEX OPEN INTEREST LOSSES IN OI. HOWEVER THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE/OCTOBER COMEX GOLD TOTALS WITH MASSIVE GOLD TONNES STANDING FOR GOLD IN OCTOBER AND THE HUGE QUEUE JUMPING THAT FOLLOWED!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS NOW BRINGS US TO OCTOBER WHERE INITIAL AMOUNT OF GOLD STANDING IS 28,988 CONTRACTS FOR 90.114 TONNES OF GOLD TO WHICH WE ADD OUR FIRST MASSIVE QUEUE JUMP OF 4.898 TONNES QUEUE JUMP FOLLOWED BY OCT 4 QUEUE JUMP OF 0.9704 TONNES TO BE FOLLOWED BY OCT 7 QUEUE JUMP OF 3.623 TONNES AND FINALLY OCT 8’S HUGE 6.942 TONNES QUEUE JUMP TO //// AND THIS WAS AUGMENTED BY AN UNUSUAL 50,000 CONTRACT EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE AND THEN ON THREE CONSECUTIVE OCCASIONS, OCT 2 THROUGH TO THE OCT 4.THEY TOOK ONE DAY OFF AND THEN ISSUED ITS 5 EXCHANGE FOR RISK ISSUANCE FOR 1000 CONTRACTS OR 100,000 OZ/3.1105 TONNES THE NEW TOTAL ON THESE 5 ISSUANCES IS 3650 CONTRACTS FOR 365,000 OZ OR 11.353 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERIES INCLUDING QUEUE JUMPS. NEW TOTALS FOR GOLD STANDING ADVANCES TO 118.5194 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 242 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH OCTOBER AND SUBSEQUENT STANDING FOR GOLD.

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 8, 6.942 TONNES OF QUEUE JUMP TO OUR 3,650 EXCHANGE FOR RISK CONTRACTS ON 5 OCCASIONS FOR 365,000 OZ OR 11.353 TONNES.! TOTAL STANDING ADVANCES TO 118.5194

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

TOTAL EXCHANGE FOR RISK OCT 5 OCCASIONS: 11.353 TONNES

E) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

F) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

G) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

H) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

EQUALS

118.5194 TONNES OF GOLD!!

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 4130 CONTRACTS.

THAT IS A STRONG SIZED 4130 EFP CONTRACT WAS ISSUED: : /DEC 4130 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4130 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY + GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE SEPT 30 WITH OUR ATTEMPTED FAILED RAID, FOLLOWED BY ANOTHER RAID OCT 2 AND THAT ENDED IN TOTAL FAILURE! TODAY OCT 7 WE WITNESSED A SMALL RAID TRYING TO STOP GOLD’S ADVANCE TO THE 4000 BARRIER!! EARLY THIS MORNING THE BARRIER TO 4,000 DOLLAR GOLD WAS PIERCED!!

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A HUGE SIZED SIZED 5362 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING STRONG GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 5 ISSUANCES FOR 11.383 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE THE GREEN LIGHT ON THE BANK OF ENGLAND’S GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY;S 6/942 TONNES OF A QUEUE JUMP WHICH MUST BE ADDED TO OUR 5 ISSUANCES OF 11.353 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 118.5194 TONNNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $29.20./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE STRONG SIZED GAIN IN OI FROM TWO EXCHANGES OF 7,695 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY .THIS WAS COUPLED WITH GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION). HOWEVER WE WITNESSED FOR NO REASON A MASSIVE LIQUIDATION IN PRICE OF OUR GOLD EQUITY SHARES LIKE AGNICO EAGLE AND BARRICK GOLD /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS TRIED AGAIN LATE WEDNESDAY-THURSDAY OCT 2 WITH CHINA OUT FOR A WEEK, WITH NOT MUCH LUCK. WITH CHINA COMING BACK ON THURSDAY OCT 9 THE CROOKS NEEDED TO RAID TODAY TRYING DESPERATELY TO HALT GOLD’S ADVANCE. I GUESS THAT THEIR LUCK HAS RUN OUT WITH GOLD PIERCING THE 4000 DOLLAR BARRIER THIS EARLY MORNING.

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN OF A TOTAL OF 16.958 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES TO BE FOLLOWED BY TODAY’S HUGE 6.942 TONNES OF QUEUE JUMP TO WHICH WE ADD OUR 11.353 TONNES EX FOR RISK/5 OCCASIONS:

/ NEW TOTAL STANDING 118.5194 TONNES.

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $29.20

WE HAD A HUGE 2243 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 5452 CONTRACTS OR 545200 0Z (16.958TONNES)

speculators have left the gold arena

INITIAL GOLD COMEX

OCT CONTRACT MONTH

OCT 8 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | i) Out of Asahi 80,028.907 oz total withdrawal 80,028.907 oz (.24 tonnes) . |

| Deposit to the Dealer Inventory in oz | 1 ENTRIES ONE ENTRY i) Into Brinks dealer: 482.265 oz (15 kilobars) total deposit; 482.265 oz |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRIES one entry i) Into Looms 32,151.000 oz (1000 kilobars) total deposit 32,151.000 oz one tonne xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 2042 notice(s) 204,200 OZ 6.3514 TONNES |

| No of oz to be served (notices) | 648 contracts 64,800OZ 2.0155 TONNES |

| Total monthly oz gold served (contracts) so far this month | 33,806 notices 3,380,600 oz 105.052 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

1 ENTRIES

ONE ENTRY

i) Into Brinks dealer: 482.265 oz (15 kilobars)

total deposit; 482.265 oz

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

one entry

i) Into Looms 32,151.000 oz (1000 kilobars)

total deposit 32,151.000 oz

one tonne

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entries

i) Out of Asahi 80,028.907 oz

total withdrawal 80,028.907 oz

(.24 tonnes)

ADJUSTMENTs 6

first 4: dealer to customer

i)Asahi 5,202.320 oz oz

ii) JPMorgan: 83,528.298 oz

iii) Stonex 51,119.657 oz

iv) Manfra 1060.983 oz

last two customer to dealer:

v) Brinks 54,785.314 oz

vi) Int Delaware: 83,528.298 oz

volume at the comex: Monday: 333,332 oz (excellent)

AMOUNT OF GOLD STANDING FOR OCTOBER

THE FRONT MONTH OF OCTOBER STANDS AT 2690 CONTRACTS FOR A GAIN OF 1067 CONTRACTS.

WE HAD 1131 CONTRACTS FILED ON TUESDAY SO WE GAINED A MONSTROUS 2232 CONTRACT QUEUE JUMP FOR 223,200 OZ OR 6.942 TONNES OF GOLD. THUS OUR NEW NORMAL DELIVERY RISES TO 107.1664 TONNES WHICH INCLUDES ALL PREVIOUS QUEUE JUMPS) PLUS OUR 11.353 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD ADVANCES TO 118.5194 TONNES

NOVEMBER GAINED 153 CONTRACTS UP TO 4705 CONTRACTS.

DECEMBER LOST 2041 CONTRACTS DOWN TO 389,335 CONTRACTS.

We had 2042 contracts filed for today representing 204,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 457 notices issued from their client or customer account. The total of all issuance by all participants equate to 2042 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 631 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (33,806 oz ) to which we add the difference between the open interest for the front month of OCT ( 2690 CONTRACTS) minus the number of notices served upon today (2042 x 100 oz per contract) equals 3,445,400 OZ OR 107.1664 TONNES OF GOLD TO WHICH WE ADD OUR 5 ISSUANCES OF 11.353 TONNES OF EXCHANGE FOR RISK //NEW TOTALS STANDING FOR GOLD OCTOBER ADVANCES TO 118.5194 TONNES

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (33,806 x 100 oz +we add the difference for front month of OCT. (2690 OI} minus the number of notices served upon today (2042 x 100 oz) which equals 3,445,400 OZ OR 107.1664 TONNES + 11.353 TONNES EXCHANGE FOR RISK//NEW TOTAL OF GOLD STANDING IN OCTOBER ADVANCES TO 118.5194 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 118.5194 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,952,857.469 oz 60.680 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 40,097.505.318 oz

TOTAL REGISTERED GOLD 21,812,144.110 or 678.449 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,285,361.208 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 1,985,928oz ((REG GOLD- PLEDGED GOLD)= 617.709 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

OCT 8 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 5 entries i) Out of Asahi 1,482,186.500 oz ii) Out of Brinks 4,779.100 oz iii) Out of Delaware 2,145,400 oz iv) Out of HSBC 15,261.100 oz v) Out of jPMorgan; 644,286.600 oz total withdrawal 2,148,618.200 oz 2 entries a) Out of Brinks 379,298.630 oz b) Out of Loomis 601,016.340 oz total withdrawal: 980,315.870 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 0 entries |

| No of oz served today (contracts) | 519 CONTRACT(S) ( 2.595 MILLION OZ |

| No of oz to be served (notices) | 101 contracts (0.505 MILLION oz) |

| Total monthly oz silver served (contracts) | 3432 Contracts (17.160 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 entries

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

5 entries

i) Out of Asahi 1,482,186.500 oz

ii) Out of Brinks 4,779.100 oz

iii) Out of Delaware 2,145,400 oz

iv) Out of HSBC 15,261.100 oz

v) Out of jPMorgan; 644,286.600 oz

total withdrawal 2,148,618.200 oz

adjustments: 4 all dealer to customer

a) Brinks 1,883,186.05 oz

b) CNT 389,614.302 oz

c) Delaware 72,738.573 oz

d) Manfra 161,613.737 oz

TOTAL REGISTERED SILVER: 186.512 MILLION OZ//.TOTAL REG + ELIGIBLE. 528.182 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 614 OPEN INTEREST CONTRACTS FOR A GAIN OF 484 CONTRACTS.

WE HAD 39 CONTRACTS SERVED ON TUESDAY, SO WE GAINED 523 CONTRACTS WHICH UNDERWENT A HUGE QUEUE JUMP OF 2.615 MILLION OZ.

STANDING FOR SILVER OCT ADVANCES TO 17.635 MILLION OZ

NOVEMBER LOST 116 CONTRACTS DOWN TO 2388

DECEMBER LOST 411 CONTRACTS DOWN TO 130,383

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 519 or 2.595 MILLION oz

CONFIRMED volume; ON TUESDAY 113,780 huge//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 3432 X5,000 oz = 17.160 MILLION oz

to which we add the difference between the open interest for the front month of OCT (614) AND the number of notices served upon today (519 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (3432) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(614) minus number of notices served upon today (519)x 5000 oz equals silver standing for the OCT.contract month equating to 17.635 MILLION OZ

New total standing: 17.635 million oz which is HUGE for this NON active delivery month of OCT. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 186.512 million oz of registered silver

JPMorgan as a percentage of total silver: 209.936/528.182million. 39.73%

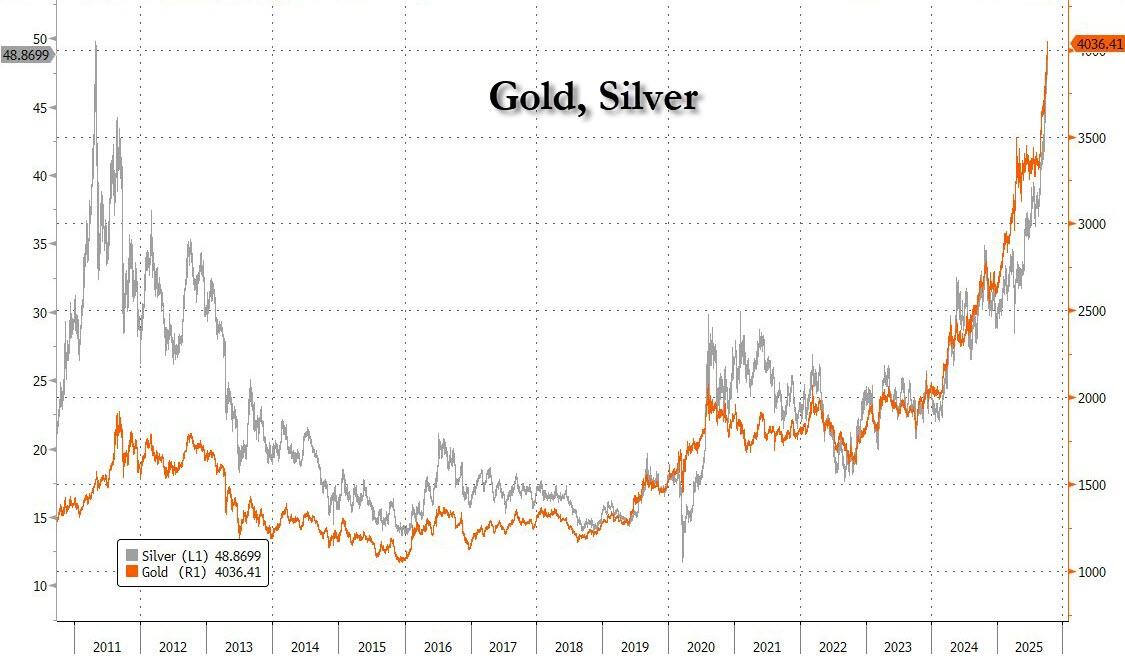

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

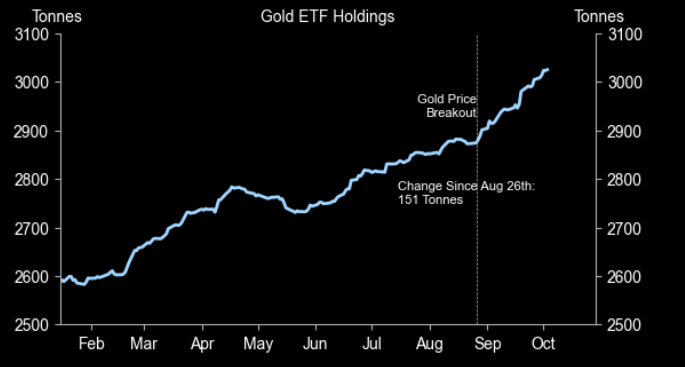

BOTH GLD AND SLV ARE MASSIVE FRAUDS

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

GLD INVENTORY: 1013.17 TONNES, TONIGHTS TOTAL

SILVER

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

CLOSING INVENTORY 494.985 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

JAMES RICKARDS

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

A brief history of the gold standard

An essay for free for all MacleodFinance Substack subscribers. It gives context to the problems we face as the fiat currency era ends and in the struggle towards solutions.

| Alasdair MacleodOct 8 |

As evidence mounts that the major western economies are heading into a debt crisis, we face the consequences of unsound money. The era of fiat is drawing to a close and its death will be painful for the highly indebted advanced economies in North America, Europe, and Japan. History and legal precedent tell us that fiat will die, and only gold can provide an anchor to credit values.

As always, there are lessons to be learned from monetary history, particularly in the context of credit-dependent post-feudal economies, when in a post-feudal world gold standards evolved to support mountains of credit in the forms of bank notes and commercial bank deposits.

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

In this article, I look at lessons from nineteenth century gold standards and the mistakes made. Mostly, they could have been easily avoided but are lessons for designing tomorrow’s monetary systems.

The debate over the return of gold backing for credit is becoming urgent, not just because the fiat currency system has run its course, but because it is increasingly in the developing world’s interests to embrace it.

Introduction

We know that from the dawn of monetary history, money is gold, silver, or copper and everything else is credit. The relationship between money and credit was codified in a series of Roman law pronouncements dating back to Rome’s Twelve Tables in 449 BC. It was the successor nations of the Roman Empire, stretching from the Atlantic seaboard to the Urals which colonised the world, apart from China and Japan. But coincidentally with the Twelve Tables, it was the era of Confucius, who had died only thirty years before, and the flowering of Chinese philosophy which confirmed similar conclusions about money in the unknown Far East. But since the end of barter, there have been numerous attempts by rulers to fraudulently misrepresent or confiscate money, usually to finance wars or disguise their debts.

The transition from agricultural feudalism to industrialisation was facilitated by the expansion of credit, not money, though above-ground stocks of gold and silver available for coining did continue to accumulate. And with its expansion, banking systems evolved to deal in credit, creating it as demanded. Banking was invented by the Romans leading to jurors such as Ulpian, Paul, and Gaius in the early Christian era ruled on the differences between money and credit.

In his 1751 treatise Della Moneta [On Money], the Italian economist Ferdinando Galiani confirmed the origins of Italian banking which spread throughout Europe:

“Notably, the first banks were in the hands of private persons with whom people deposited money and from whom they received bills of credit and who were governed by the same rules as the public banks are now. And thus, the Italians have not only been the fathers, the masters, and the arbiters of commerce so that in all Europe they have been the depositories of money and are called bankers.”

Banking as we know it today was developed in England by London’s goldsmiths, who began to receive the gold and silver coin of the merchants in deposit. They not only agreed to repay it on demand, but to pay 6% interest per annum for the use of it. Consequently, in order to enable them to pay the interest promised it necessarily became their property to trade with as they wished. They were not the trustees of the money, but its proprietors. And it was not placed with them as a depositum to be restored in identified specie, but it became the goldsmiths’ property as a mutuum to be restored to the merchant on demand. This business flourished after the Restoration in 1660, and expanded significantly under William of Orange, following the Glorious Revolution when the Catholic James II was banished.

When the goldsmith bankers received money in deposit, it was agreed in exchange that a credit or right of action be given in favour of the merchant for an equal amount of money to be restored to him on demand. It is this banker’s obligation to the depositor which in banking language today is termed a deposit.

As this business became mainstream, experience showed that if some of a banker’s customers demanded payment of their deposits or credits from day-to-day, others would probably pay in about an equal amount, so that at the end of the day they would not be much difference in his cash balance. In practice, it was found that ordinarily the bank’s balance in cash would seldom differ by more than 1/36th of total deposits from day-to-day. Therefore, if a banker retained 1/10th of his cash to meet any demands for payments that may be made, it would be ample cover for deposit outflows in ordinary conditions.

This allowed the banker to buy commercial and other bills in far larger quantities at a discount in return for a deposit credited in favour of the sellers. The sellers of these bills could draw upon their credits at the bank at will. By dealing in credit this way, the leverage the banker could apply to his own balance sheet was safely up to ten times on the assumptions above. And with the rate of discount on commercial bills typically 8% or more, the banker was able to pay 6% to his original depositors and retain a good profit.

Clearly, the value of a banker’s credit had to be expressed in money. That is to say, a deposit was expected to be encashable for specie. But with the evolution of the goldsmiths’ business and the mountains of credit created by their activities, the relationship between gold and silver on the one hand and legal obligations to pay on the other would also evolve.

The gold standard as our nineteenth century forbears knew it was basically a child of the British government and its bank in London, the Bank of England. The Bank itself opened for business on 1 August 1694 with a staff of nineteen. For most of the period between 1717 to 1931, Britain operated either a formal or de facto gold standard. The gold standard commenced after Sir Isaac Newton, as Master of the Mint, valued the gold guinea at 21 silver shillings, marking an important shift from sterling silver towards a gold standard. After a period of bimetallism, gold gradually became to be regarded as the measure of value in preference to silver. And in 1816, gold was declared to be the legal measure of value in England and the pound became the equivalent in gold of 20 silver shillings. Silver became legal tender for sums of no more than 40 shillings.

By the 1816 Regulations of the Mint, forty pounds weight of standard gold bullion are cut into £1,869 in sovereigns, fixing the mint price of gold at £3/17/6d. In modern measures, a sovereign weighs 7.99 grammes with a gold content of 7.32 grammes.

In the United States, before the War of Independence English law prevailed and in the late 1700s Blackstone’s Commentaries was the standard legal treatise among Americans. Blackstone was clear on what constituted money:

“Money is the medium of commerce. It is the King’s prerogative as the arbiter of domestic commerce to give it all authority or make it current. Money is a universal medium or common standard by comparison with which the value of all merchandise may be ascertained: a sign which represents the respective values of all commodities…

“The coining of money is in all states the act of the sovereign power that its value may be known on inspection. And with respect to coinage in general there are three things to be considered therein: the materials, the impression, and the denomination. With respect to the materials Sir Edward Coke lays it down that the money of England must be either of gold or silver…”[i]

The framers of the Constitution adapted Blackstone to replace the King’s prerogative with the new Congress, giving the federal government the power to coin money. And that money could only be coined. To get around this restriction, which is every spendthrift politician’s desire, the government would have to have a tame commercial bank to produce gold substitutes in the form of bank notes. But even that course was controversial.

In 1790, Alexander Hamilton as the first secretary of the Treasury submitted a report to Congress in which he outlined his proposal to establish a government-owned bank, the Bank of the United States, using the charter of the Bank of England as the basis for his plan. It was passed and a 20-year charter was signed into law by President Washington the following February. As well as acting as the government’s fiscal agent and making loans to the government, it also operated as a commercial bank, issuing banknotes. In 1811, Hamilton was dead, the Republican Party had taken control from the Federalists, and the charter was not renewed.[ii]

Just five years after Hamilton’s proposal, the Bank of England began experiencing a significant drain on its bullion reserve, due to the government’s need for gold to finance the war with France and also to pay for imported grain after a succession of bad harvests. In 1797, the Bank suspended payments in cash (i.e. gold and silver coin). The suspension continued through the Napoleonic Wars, during which the Bank inflated its note issue causing the price of gold to rise against the Bank’s paper currency. In 1810, this led to the appointment of a Select Committee “to enquire into the high price of bullion”, which concluded that the depreciation of the currency was due to the excessive issue of bank notes. The following which is extracted from its report to Parliament is the most relevant passage:

“…there is at present an excess of paper in circulation in this Country, of which the most unequivocal symptom is the very high price of Bullion, and next to that, the low state of the Continental Exchanges; that this excess is to be ascribed to the want of a sufficient check and control in the issues of paper from the Bank of England; and originally, to the suspension of cash payments, which removed the natural and true control. For upon a general view of the subject, Your Committee are of opinion, that no safe, certain, and constantly adequate provision against an excess of paper currency, either occasional or permanent, can be found, except in the convertibility of all such paper into specie. Your Committee cannot, therefore, but see reason to regret, that the suspension of cash payments, which, in the most favourable light in which it can be viewed, was only a temporary measure, has been continued so long; and particularly, that by the manner in which the present continuing Act is framed, the character should have been given to it of a permanent war measure.

The Committee recommended to Parliament that placing numerical restrictions on the note issue would be impossible to judge and that in the absence of an exchange facility between notes and coin, the only sure criterion was to be found in monitoring the price of bullion and the state of the foreign exchanges. It was a conclusion which has stood the test of time because ever since all attempts to manage the note issue and other forms of central bank credit to achieve price stability have failed.

Perhaps the implication that Parliament was unable to control monetary matters was unacceptable, because the Select Committee’s report was rejected. Consequently, being unrestrained the Bank of England was free to increase its note issue without restriction, reducing the gold value of the Bank’s paper pound even further.

In an inflationary free-for-all, bank notes were also being issued in increasing numbers by country banks outside London, in what would turn out to be a classic cycle of bank credit expansion. The consequence of the note expansion was rising prices: between 1808 and 1813, the general level of consumer prices is estimated to have risen 25%, admittedly this was in war-time. Inevitably, a credit squeeze followed after Napoleon was defeated at Waterloo and between 1814—1816 half of the country banks failed in the subsequent slump, reducing the total volume of paper currency circulating substantially. The shortage of bank notes led to the value of the Bank of England’s notes increasing accordingly, proving that the Bullion Report was correct in its analysis: that it was impossible to judge what restrictions to put on the note issue, and the best solution was to be found in a firm relationship with specie.

Though Parliament had rejected the Bullion Report, it became the subject of much debate with the result that businessmen and traders were won over by it. It also converted Robert Peel, who later became the first Prime Minister with a business background. Peel also became Chairman of the Bullion Committee in 1819, and he pushed through an Act initially introducing a gold bullion standard to be followed by a resumption in 1823 of the previous sovereign coin standard. But the Bank had accumulated enough gold to press for the Act to be amended so that it could resume coin payments in May 1821.

However, a run on the Bank’s reserves began only three years later, taking the bullion reserves from £13 million in January 1824 down to a little over a million in December 1825. A credit crisis developed on the back of the note issue contracting, which was only arrested by the bank issuing yet more bank notes. At last, the directors of the Bank became convinced there was something in the Bullion Report after all, and from 1827 endeavoured to ensure its balance sheet assets were maintained two-thirds in favour of government debt and one-third in coin and bullion.

From time to time the Bank had great difficulty maintaining this position, and in 1839 was forced to obtain loans from Paris and Hamburg of £3,500,000 in gold to stave off bankruptcy. The ups and downs of the Bank acting as an issuer of bank notes and operating as a commercial bank led to a debate between two schools of thought: the currency and banking schools. From experience and some would claim self-interest, the banking school was against the rules-based approach of the currency school, preferring demand for bank credit to be left to the markets, echoing the conclusions of the Bullion Committee.

The currency school argued that the issuing of bank notes should be separated from banking activities. It was a rules-based approach imposed by law, based on David Ricardo’s analysis of 1824 from which the following extract is relevant:

“The Bank of England performs two operations of banking, which are quite distinct, and have no necessary connection with each other: it issues a paper currency as a substitute for metallic one; and it advances money in the way of a loan, to merchants and others. That these two operations of banking have no necessary connection, will appear obvious from this — that they might be carried on by two separate bodies, without the slightest loss of advantage, either to the country, or to the merchants who receive accommodation from such loans.”

Accordingly, under the Bank Charter Act of 1844, the Bank of England was split into two departments: the Issue Department and the Banking Department. The Directors were to transfer to the Issue Department £14,000,000 of securities (mostly government stock) and all gold coin and gold and silver bullion not required by the Banking Department for its immediate purposes. Under Orders in Council the level of securities was subsequently increased to £15,000,000 to compensate for the private banks who ceased to issue banknotes after the introduction of the Act. The increase in the Issuing department’s balance sheet allowed it to increase its note issue.

The framers of the 1844 Act assumed that if there was a contraction of the note issue due to notes being submitted for coin, the lower quantity of notes in circulation would support their value, so that the arrangement would always ensure that a potential run on the Issue Department would be self-correcting. But crucially, a number of errors in the framing of the act transpired.

In effect, the Act attempted to set up the Issue Dept as a bank of deposit, issuing banknotes as tokens for bullion held on the asset side of its balance sheet. It was forbidden from dealing in credit. But by allowing the balance sheet to record assets of £15m in debt securities, this principle was abused, because those securities had to be bought by the issue of credit. Furthermore, it was apparent that there are irrecoverable costs in converting coin into notes and vice-versa. Presumably, the framers in the currency school thought that these could be offset by the income on securities.

The second error was more serious. The framers of the Act had assumed that only banknotes would be submitted to the Bank in exchange for coin. They had omitted to understand that cheques encashed in the Banking Department could equally be exchanged for coin or bullion, so that when there was a run on the Issue Department it came from cheques being encashed, not notes presented for payment in gold. This refuted the hope that the submission of notes for bullion would support their value through scarcity. This error led to the temporary suspensions of the Act in 1847, 1857, and 1865.

An extension of the second error was a third. When there were a number of currencies on gold standards (which were always the case de facto or de jure), a run on the Issuing Department’s gold reserves would occur if the Bank kept its discount rate too low. To illustrate this point, in 1799 there was a banking crisis in Hamburg and the discount rate there rose to 15%, drawing bullion out of London.

To understand why this is so, be it understood that both principal and interest are payable in gold or gold substitutes. Therefore, irrespective of trade imbalances and other factors which might be ascribed to the risks relative between one centre and another, when the rate of discount between two places differs by more than the cost of transmitting bullion between them, bullion will flow from where the discount is lower to where it is higher.

The Act could have worked, despite the lack of the Issue Department not being a proper bank of deposit, if as well as the powers given to it by the Act it was also given the power to set the discount rate purely with the intention of maintaining the bullion reserve. On each of the three failures above, it was this power being in the hands of the Banking Department that led to runs on the Bank’s gold reserves and the suspensions of the Act in 1847, 1857, and 1866.

The underlying point is that you cannot have a note issuing function exchangeable for gold on demand as part of a wider banking business, as the Americans clearly understood when Congress did not renew the 20-year charter of the Bank of the United States in 1811.

Before 1834, the United States was on a bimetallic (gold and silver) standard, switching to gold in 1834 at a rate of $20.67 to the ounce, confirmed by the Gold Standard Act in 1900 and which continued at that rate until 1933 when by Executive Order President Roosevelt rescinded it for US citizens. That America’s gold standard stood for nearly a century without alteration or compromise through cycles of bank credit is proof that a central bank, even split into departments of issue and banking, is so conflicted in its objectives as to be incapable of securing monetary stability. Therefore, it was the establishment of the Fed in 1913 and its post-war meddling in credit markets which led to the devaluation of the dollar.

The future of gold standards

We know from the long history of the division of labour that money and credit, however defined, have progressed the human condition following the restrictions of barter. And we also know that in a post-barter world credit must take its value from a higher form of money for which there is no counterparty risk. Both in practice, and in law for nearly 2,500 years the higher form of credit has been metallic money.

Therefore, the current situation whereby commercial bank credit takes its value from a government’s credit is an aberration. Indeed, every time the state has tried to take ultimate control over commercial credit, it has always failed. Our current monetary system, which has been in place since the suspension of the Bretton Woods Agreement in 1971 is now showing signs of having run its course. There can be little doubt that however long its ending is resisted, the legal and historical precedents will reassert themselves eventually. Gold bullion will then return as the ultimate backstop for all credit because it is accumulated by global central banks, and therefore anchors the values of all commercial activities and wealth.

There is no doubt that the return to a gold standard will face fierce resistance from western governments, which have come to depend on the expansion of their credit to finance excess spending. As we saw when the British Parliament rejected the Bullion Report of 1810, the political class has a fundamental belief that money and credit is something that can be controlled, and any evidence to the contrary is disregarded. The failure of free market economics to gain intellectual traction against statist interests has many examples in history. Germany’s historical school adopted Georg Knapp’s 1905 State Theory of Money while dismissing the Vienna-based free market intellectuals as a bunch of (Austrian) country hicks.

So it was that despite the collapse of the European paper currencies in the wake of the First World War, the lessons that should have been learned from the detachment of state credit from specie were not. “We can always prevent a monetary problem by managing it better”, was the common statist cry. And when the roaring twenties, stoked by credit expansion under Benjamin Strong’s Fed ended with the Wall Street crisis in 1929—1932 together with Smoot Hawley tariffs causing the following depression and bank failures, free market economics were blamed instead. “It must never be allowed to happen again”, the statists said. Economists have had free markets and sound money educated out of them subsequently to be replaced by macroeconomics and statistical modelling.

The establishment is simply not equipped to face the challenges of returning to monetary stability. Its experts cannot even diagnose the problems in advance, only reacting to events with an overriding motive to preserve their status quo. All we can say is that in the aftermath of Waterloo, Britain’s leadership of Liverpool, Castlemaine, Beresford, and Wellington were sound money men, understanding the importance of free markets, imbued with Adam Smith, and the importance of a gold standard, sadly absent in our leadership today.

Following Waterloo, Liverpool’s government set in motion an economy which expanded in real terms on the basis of non-intervention, allowing the government’s debt to fall from 172% of estimated 1819 GDP to 21% in 1914. According to the Bank of England’s own research, this debt declined from a total of £893 million to £706 million between those dates, the rest of its statistical decline being from economic progression. An additional benefit to government funding was the use of undated consolidated loan stock, which never had to be refinanced or redeemed.

This is the other essential policy behind sound money: government discipline over its own spending. In 1820, once war-time spending had ended government spending was just 13% of GDP, leaving businesses and individuals with 87% of their own money with which to go about their business. Today, government spending is far higher and rising, even exceeding half their economies in some European nations. Unless these excesses are dramatically reduced, there is no chance of a gold standard lasting.

[i] As quoted from Pieces of Eight, Book 1 by Edwin Vieira Jr.

[ii] For a fuller description of monetary developments in the US after Independence, see James Turk’s Money and Liberty Chapter 9 (woodlanebooks.co.uk)

END

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

extremely important: the Bank of England’s account, the EEA has its independent auditor so far refuse to sign off on it. It’s major holding of course is 310 tonnes of gold. Seems that the gold is not there and compromised which would cause the auditor headaches and thus refuse to give the Bank, the green light!

Robert Lambourne: UK’s gold account is unusually late with annual report

Submitted by admin on Tue, 2025-10-07 18:39 Section: Daily Dispatches

By Robert Lambourne

Tuesday, October 7, 2025