access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,108.600000000 USD

INTENT DATE: 10/13/2025 DELIVERY DATE: 10/15/2025

FIRM ORG FIRM NAME ISSUED STOPPED

092 C DEUTSCHE BANK 213

118 C MACQUARIE FUTURES US 304

118 H MACQUARIE FUTURES US 250

323 C HSBC 166

332 H STANDARD CHARTERED B 653

363 H WELLS FARGO SECURITI 1543

435 H SCOTIA CAPITAL (USA) 209

624 H BOFA SECURITIES 2

661 C JP MORGAN SECURITIES 250 1886

686 H STONEX FINANCIAL INC 27

737 C ADVANTAGE FUTURES 20 20

880 H CITIGROUP 27

905 C ADM 8

TOTAL: 2,789 2,789

MONTH TO DATE: 42,038

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 2789 CONTRACTs NOTICES FOR 278,900 OZ or 8.645 TONNES

total notices so far: 42.038 contracts for 4,203,800 OR 130.755 tonnes)

SILVER NOTICES: 367 NOTICE(S) FILED FOR 1.835 MILLION OZ/

total number of notices filed so far this month : 5608 CONTRACTS (NOTICES) for 28.040 million oz

INITIAL STANDING FOR OCT: 28.515 MILLION OZ (WHICH INCLUDES ALL QUEUE JUMPING)

+ 2.110 MILLION OZ EXCHANGE FOR RISK

EQUALS

30.625 MILLION OZ..

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 53.255 MILLION OZ (WILL BE HUGE THIS MONTH)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 28.515 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 30.625 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH A RECORD SETTING MONSTER 9.564 TONNES QUEUE JUMP WHICH WAS PRECEDED BY 33.009 TONNES QUEUE JUMPING FOR OCT. THEN WE MUST ADD OUR 11.353 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/5 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 144.959 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 111.885 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL SIZED 170 CONTRACTS OI TO 171,132 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A MONSTER 1800 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1800 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1330 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 170 CONTRACTS AND ADD TO THE MONSTER 1880 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1630 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE GAIN OF $1.78 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.150 MILLION PAPER OZ

OCCURRED WITH OUR GAIN OF $1.78 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 24.27 POINTS OR 0.62%

//Hang Seng CLOSED CLOSED DOWN 448.41 PTS OR 1.73%

// Nikkei CLOSED : DOWN 1214.48 PTS OR 2.58% //Australia’s all ordinaries CLOSED UP 0.27%

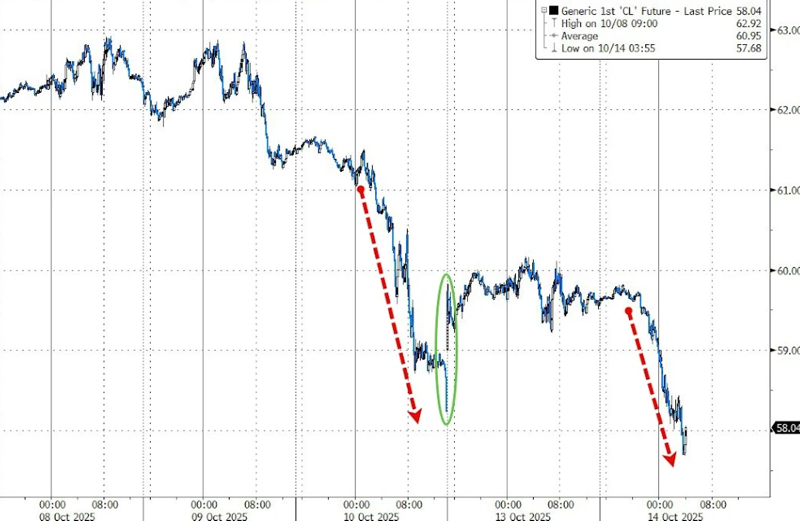

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1390// OFFSHORE CLOSED DOWN AT 7.1431/ Oil DOWN TO 59.61 dollars per barrel for WTI and BRENT DOWN TO 62.66 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING DOWN TO 7.1390 // OFFSHORE YUAN TRADING DOWN TO 7.1431 :/ONSHORE YUAN TRADING ABOVE OFF SHORE / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4631 CONTRACTS TO 485,352 OI WITH OUR MONSTER GAIN IN PRICE OF $129.00 WITH RESPECT TO MONDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (5106). WE HAD ZERO T.A.S. LIQUIDATION MONDAY. WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 6681 CONTRACTS (OR 20.78 TONNES).THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

EXCHANGE FOR PHYSICAL//GOLD ISSUANCE//OCTOBER:

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT FOR GOLD REMAINS AT 11.353 TONNES OF GOLD UNDER THE GUIDANCE OF 5 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 5 ISSUANCES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES TOTAL ISSUANCES 5 OCCASIONS FOR 3650 CONTRACTS OR 365,000 OZ OR 11.353 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN FINALLY OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES TOTAL ISSUANCE ON 5 OCCASIONS: 11.353 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 127.5 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 126.5 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .

DETAILS ON OCTOBER COMEX MONTH//

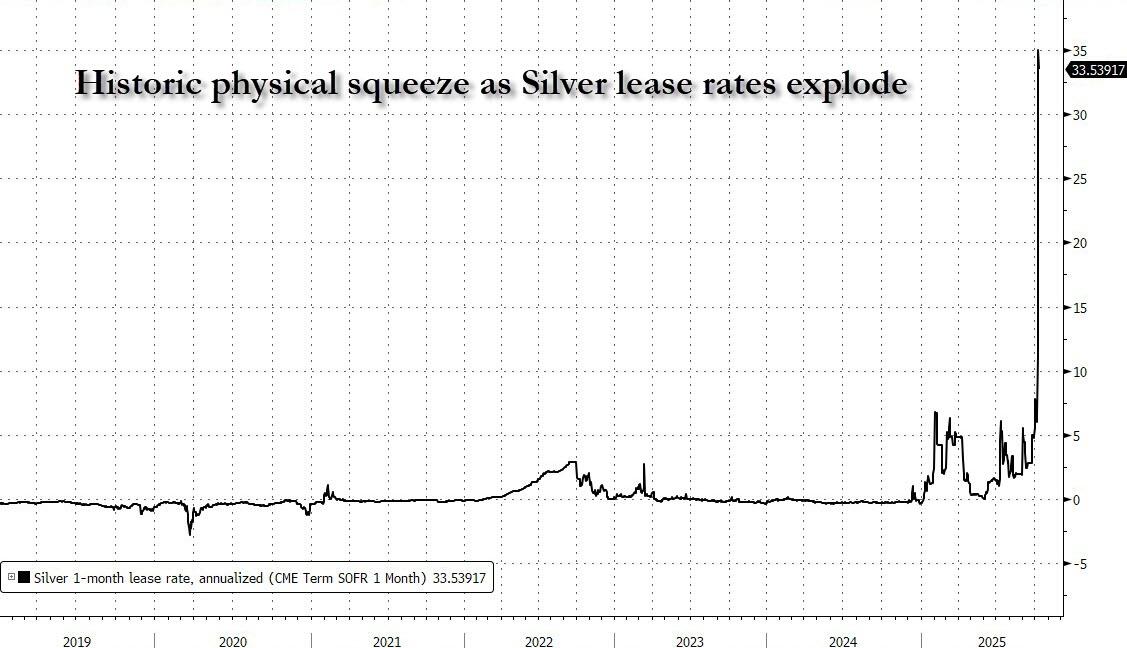

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 6680 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A HUGE T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 3927 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN YESTERDAY DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS:

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD. WITH MUCH FAILURES. THIS BRINGS US TO YESTERDAY’S MASSIVE RAID ON OUR PRECIOUS METALS. ONE SHOULD EXPECT CONSIDERABLE DAMAGE TO OUR LONGS. SHOCKINGLY AS YOU WILL SEE, ON A NET BASIS NOBODY LEFT EITHER ARENA, GOLD AND SILVER.

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS CONTINUED THURSDAY AND FRIDAY, OCT 1 AND OCT 2 AND NOW OCT 9 THROUGH 10TH AND THAT IS THE REASON WHY WE ARE HAVING HUGE DISTORTED COMEX OPEN INTEREST NUMBERS IN OI. HOWEVER THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE/OCTOBER COMEX GOLD TOTALS WITH MASSIVE GOLD TONNES STANDING FOR GOLD IN OCTOBER AND THE HUGE QUEUE JUMPING THAT FOLLOWED!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS NOW BRINGS US TO OCTOBER WHERE INITIAL AMOUNT OF GOLD STANDING IS 28,988 CONTRACTS FOR 90.114 TONNES OF GOLD TO WHICH WE ADD OUR FIRST MASSIVE QUEUE JUMP OF 4.898 TONNES QUEUE JUMP FOLLOWED BY OCT 4 QUEUE JUMP OF 0.9704 TONNES TO BE FOLLOWED BY OCT 7 QUEUE JUMP OF 3.623 TONNES, THEN OCT 8’S HUGE 6.942 TONNES QUEUE JUMP, OCT 9 HUGE 4.979 TONNES OF QUEUE JUMP, OCT 10 MASSIVE QUEUE JUMP OF 7.504 CONTRACTS(250,900 OZ//7.504 TONNES) AND THEN OCT 13: 4.3919 TONNES// AND THEN OCT 14 WITH A RECORD SETTING 9.564 TONNES //// AND THIS WAS AUGMENTED BY AN UNUSUAL 50,000 CONTRACT EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE AND THEN ON THREE CONSECUTIVE OCCASIONS, OCT 2 THROUGH TO THE OCT 4.THEY TOOK ONE DAY OFF AND THEN ISSUED ITS 5 EXCHANGE FOR RISK ISSUANCE FOR 1000 CONTRACTS OR 100,000 OZ/3.1105 TONNES THE NEW TOTAL ON THESE 5 ISSUANCES IS 3650 CONTRACTS FOR 365,000 OZ OR 11.353 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERIES INCLUDING QUEUE JUMPS. NEW TOTALS FOR GOLD STANDING ADVANCES TO 144.959 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 243 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH OCTOBER AND SUBSEQUENT STANDING FOR GOLD.

AUGUST:

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPT:

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST RECORD SETTING OCT 14 QUEUE JUMP OF 9.564 WHICH FOLLOWED PREVIOUS QUEUE JUMPS OF 33.009 TONNES TO WHICH WE ADD OUR TOTAL 3,650 EXCHANGE FOR RISK CONTRACTS ON 5 OCCASIONS FOR 365,000 OZ OR 11.353 TONNES.! TOTAL STANDING ADVANCES TO 144.959 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

TOTAL EXCHANGE FOR RISK OCT 5 OCCASIONS: 11.353 TONNES

TO WHICH WE ADD OUR QUEUE JUMPING;

E) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

F) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

G) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

H) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

I) A MASSIVE QUEUE JUMP OCT 9 FOR 4.979 TONNES

J) A MASSIVE AND 3RD HIGHEST EVER OCT 10 QUEUE JUMP FOR 7.504 TONNES

I) A MASSIVE QUEUE JUMP OF 4.3919 TONNES

J) A RECORD SETTING QUEUE JUMP OF 9.564 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

144.959 TONNES OF GOLD!!

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 5106 CONTRACTS.

THAT IS A STRONG SIZED 5106 EFP CONTRACT WAS ISSUED: : /DEC 5106 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5106 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY + GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE SEPT 30 WITH OUR ATTEMPTED FAILED RAID, FOLLOWED BY ANOTHER RAID OCT 2 AND THAT ENDED IN TOTAL FAILURE! , OCT 7 WE WITNESSED A SMALL RAID TRYING TO STOP GOLD’S ADVANCE TO THE 4000 BARRIER!! EARLY Y\OCT 8 MORNING THE BARRIER TO 4,000 DOLLAR GOLD WAS PIERCED!! AND THAT SET IN MOTION OUR CROOKS DESPERATE TO CONTROL THEIR HUGE DERIVATIVE LOSSES. (OCT 9 SAW FINALLY AFTER MANY YEARS SILVER PIERCING THE 50 DOLLAR MARK AND THAT WAS WHEN THE CROOKS THREW A TEMPER TANTRUM. THEY THREE ANOTHER TEMPER TANTRUM WHEN GOLD FINALLY BROKE THROUGH 4,000 DOLLAR MARK ON OCTO 10 AND THAT FAILED AND FROM THAT POINT GOLD NEVER LOOKED BACK!!

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A HUGE SIZED SIZED 3927 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK AND THEN OCT 9, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING STRONG GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 5 ISSUANCES FOR 11.383 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE THE GREEN LIGHT ON THE BANK OF ENGLAND’S GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY;S RECORD SETTING 9.564 TONNES OF A QUEUE JUMP TO ALL OTHER QUEUE JUMPOS IN OCT OF 33.009 TONNES WHICH MUST BE ADDED TO OUR 5 ISSUANCES OF 11.353 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 144.959 TONNNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A MONSTER $129.00./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE STRONG SIZED GAIN IN OI FROM TWO EXCHANGES OF 6681 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY .THIS WAS COUPLED WITH GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION). HOWEVER, ON TUESDAY OCT 7, WE WITNESSED FOR NO REASON A MASSIVE LIQUIDATION IN PRICE OF OUR GOLD EQUITY SHARES LIKE AGNICO EAGLE AND BARRICK GOLD /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS TRIED AGAIN LATE WEDNESDAY-THURSDAY OCT 2 WITH CHINA OUT FOR A WEEK, WITH NOT MUCH LUCK. WITH CHINA COMING BACK THURSDAY OCT 9 THE CROOKS NEEDED TO RAID TRYING DESPERATELY TO HALT GOLD’S ADVANCE. I GUESS THAT THEIR LUCK HAS RUN OUT WITH GOLD INITIALLY PIERCING THE 4,000 DOLLAR BARRIER OCT 7-8 ALONG WITH THE PIERCING OF SILVER’S MAGIC 50 DOLLAR MARK.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN OF A TOTAL OF 20.78 PAPER TONNES FROM OUR TWO EXCHANGES, DESPITE THE RAID, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES TO BE FOLLOWED BY TODAY’S RECORD SETTING 9.564 TONNES OF QUEUE JUMP TO WHICH WE ADD OUR 11.353 TONNES EX FOR RISK/5 OCCASIONS:

/ NEW TOTAL STANDING 144.959 TONNES.

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR MONSTER GAIN IN PRICE TO THE TUNE OF $26.00

WE HAD A FAIR 475 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 6681 CONTRACTS OR 668,100 0Z (20.78 TONNES)

speculators have left the gold arena

INITIAL GOLD COMEX

OCT CONTRACT MONTH

OCT 14

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entries i) out of Stonex: 64,360.400 oz total withdrawal: 64,360.400 oz or 2.00 tonnes . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 2789 notice(s) 278,900 OZ 8.645 TONNES |

| No of oz to be served (notices) | 903 contracts 90,300 OZ 2.808 TONNES |

| Total monthly oz gold served (contracts) so far this month | 42,038 notices 4,203,800 oz 130.755 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entry

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entries

i) out of Stonex: 64,360.400 oz

total withdrawal: 64,360.400 oz or 2.00 tonnes

ADJUSTMENTs 5

dealer to customer

i)Asahi 9535,714 oz

ii) Brinks: 578.718 oz

iii) HSBC 9573.086 oz

iv) Malca: 23,245.584 oz

v) Manfra 4147.479 oz

volume at the comex: MONDAY: 333,736 oz (HUGE)

AMOUNT OF GOLD STANDING FOR OCTOBER

THE FRONT MONTH OF OCTOBER STANDS AT 3692 CONTRACTS FOR A GAIN OF 1540 CONTRACTS.

WE HAD 1535 CONTRACTS FILED ON MONDAY SO WE GAINED A MONSTROUS 3075 CONTRACT QUEUE JUMP FOR 307,500 OZ OR 9.564 TONNES OF GOLD AND THIS NOW BECOMES THE HIGHEST EVER QUEUE JUMP IN COMEX HISTORY BARELY EDGING OUT LAST YEAR’S 9.4 TONNE RECORD. THUS OUR NEW NORMAL DELIVERY RISES TO 133.614 TONNES WHICH INCLUDES ALL PREVIOUS QUEUE JUMPS) PLUS OUR 11.353 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD ADVANCES TO 144.954 TONNES

NOVEMBER LOST 169 CONTRACTS UP TO 3714 CONTRACTS.

DECEMBER LOST 1743 CONTRACTS DOWN TO 373,931 CONTRACTS.

We had 2789 contracts filed for today representing 278,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 250 notices issued from their client or customer account. The total of all issuance by all participants equate to 2789 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 1886 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (42,038 oz ) to which we add the difference between the open interest for the front month of OCT ( 3692 CONTRACTS) minus the number of notices served upon today (2789 x 100 oz per contract) equals 4,294,100 OZ OR 133.606 TONNES OF GOLD TO WHICH WE ADD OUR 5 ISSUANCES OF 11.353 TONNES OF EXCHANGE FOR RISK //NEW TOTALS STANDING FOR GOLD OCTOBER ADVANCES TO 144.959 TONNES

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (42,038 x 100 oz +we add the difference for front month of OCT. (3692 OI} minus the number of notices served upon today (2789 x 100 oz) which equals 4,294,100 OZ OR 133.606 TONNES + 11.353 TONNES EXCHANGE FOR RISK//NEW TOTAL OF GOLD STANDING IN OCTOBER ADVANCES TO 144.959 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 144.959 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,957,498.686 oz 60.860 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,660,679.804 oz

TOTAL REGISTERED GOLD 21,374,292.858 or 664.83 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,286,386.946OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 1,941,679. oz ((REG GOLD- PLEDGED GOLD)= 603,94 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

OCT 13 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 5 entries i) Out of Asahi 3,113,408.610 oz ii) Out of Brinks: 600,876.730 oz iii) Out of CNT: 251,264.526 oz iv) Out of Delaware 10,897.716 oz v) Out of Malca 583,346.400 oz total withdrawal 4,559,793.482 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 0 entries |

| No of oz served today (contracts) | 367 CONTRACT(S) ( 1.835 MILLION OZ |

| No of oz to be served (notices) | 94 contracts (0.4700 MILLION oz) |

| Total monthly oz silver served (contracts) | 5608 Contracts (28.040 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 entries

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

5 entries

i) Out of Asahi 3,113,408.610 oz

ii) Out of Brinks: 600,876.730 oz

iii) Out of CNT: 251,264.526 oz

iv) Out of Delaware 10,897.716 oz

v) Out of Malca 583,346.400 oz

total withdrawal 4,559,793.482 oz

adjustments: 8 dealer to customer

a) Asahi 5,673,333.260 oz

b) Brinks: 198,682.200 oz

c) CNT: 246,439.290 oz

d) Delaware: 24,439.290 oz

e) JPMorgan: 986,525,680 oz

f) Loomis 833,367.740 oz

g) Manfra 1011,016.522 oz

h) Stonex; 151,077.810 oz

total adjusted out of dealer to customer: 9,124,785.682 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 173.918 MILLION OZ//.TOTAL REG + ELIGIBLE. 515.632 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 462 OPEN INTEREST CONTRACTS FOR A GAIN OF 25 CONTRACTS.

WE HAD 293 CONTRACTS SERVED ON MONDAY, SO WE GAINED 318 CONTRACTS WHICH UNDERWENT A MASSIVE QUEUE JUMP FOR 1.590 MILLION 0Z

THUS

NORMAL STANDING FOR SILVER OCT ADVANCES TO 28.515 MILLION OZ WHICH INCLUDES TODAY’S MASSIVE 1.590 MILLION OZ QUEUE JUMP + 2,110 MILLION OZ EX. FOR RISK = 30,625 MILLION OZ WHICH IS MASSIVE FOR A NON DELIVERY MONTH!!

NOVEMBER LOST 9 CONTRACTS UP TO 2429

DECEMBER LOST 1663 CONTRACTS DOWN TO 126,571

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 293 or 1.465 MILLION oz

CONFIRMED volume; ON MONDAY 148,529 immense//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 5608 X5,000 oz = 28/040 MILLION oz

to which we add the difference between the open interest for the front month of OCT (462) AND the number of notices served upon today (367 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (5608) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(462) minus number of notices served upon today (367)x 5000 oz equals silver standing for the OCT.contract month equating to 28.515 MILLION OZ to which we must add our initial 2.110 million oz exchange for risk issuance//new standing advances to 30.625 which is mammoth for a non active delivery monthj.

New total standing: 30.625 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 173.918 million oz of registered silver

JPMorgan as a percentage of total silver: 208,435/515.632million. 40.38%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

GLD INVENTORY: 1018.88 TONNES, TONIGHTS TOTAL

SILVER

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

CLOSING INVENTORY 506.511 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

AMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD…

Rising bond yields and the death of fiat

US Treasury yields have declined for the last two years. It’s a trap ahead of far higher yields as the credit bubble pops with consequences for gold, silver, and also all other commodities.

| Alasdair MacleodOct 14∙Paid |

A consolidation of the type delineated between the pecked lines usually precedes a breakout continuing the prior trend, suggesting a minimum target of about 10%. This flies in the face of market expectations. While admitting that inflation is somewhat sticky, investors believe that there will be further rate cuts by the year-end.

Standing back from post-covid economic and financial developments, we see that the rise in yields to late-2023 broke a strong, long-term downtrend, which tends to confirm the hypothesis that there are more bond yield rises to come:

The long-term decline was from 15% in October 1981. Breaking such an important downtrend has consequences, not least given that Federal government debt at $37.6 trillion is at about 125% of GDP —that’s a leverage of 6.8 times tax revenue. Imagine taking out a mortgage on that relationship to your income, only to be clobbered by a doubling of the interest rate.

We shall return to the economic and financial consequences later in this article.

A template for currency collapse

Every fiat currency in history commits harakiri through debt spiralling out of control, and the current cohort of currencies is not different.

The end is brought about by markets pricing default risk properly, which means higher bond yields. And higher bond yields lead to debt traps, which bankrupt all businesses with debt leverage, even those without, and eventually destroy the currency itself.

Higher bond yields leave politicians with no alternative but to support everything, from failing businesses, to banks, and to keep their governments in funds. This support comes from increasingly short-term debt, issued at suppressed interest rates to finance currency expansion to pay for it all. And as the lethal combination of debasement and loss of faith in a currency’s value do their devilish work, its purchasing power enters a final period of collapse.

While the particulars vary, every fiat currency dies in a similar fashion. At the time of the proto-Keynesian John Law, Richard Cantillon understood the process well and made a fortune shorting Law’s fiat livres for gold, just as the smarter central banks are doing today with their dollar reserves.

The similarities to the way the best recorded currency collapse in history developed are also startling, offering a template for our understanding today. We refer to Germany’s hyperinflation following the First World War.

The initial phase, which follows economic destruction is evidenced in a period of inflation as credit is expanded to support the post-war recovery by funding consumption. This is followed by a period of apparent currency stability as credit expansion is redirected to assets, with the stock market soaring and property values rising to give an illusion of prosperity. And finally, the currency enters its third period of final collapse as the credit bubble deflates.

Following covid when economic activity was effectively shut down, in all G7 nations we have seen phases one and two, with phase three yet to follow. The comparison with post-WW1 Germany is illustrated in the table below.

Following the initial phase, in the second phase from February 1920 to December 1921 Germany enjoyed a stock market boom when post-war consumer price inflation declined. The apparent wealth created by credit expansion backing stock speculation enriched the middle classes, while the conditions of the lower classes barely improved. In 2022 to today, the US and other G7 nations have experienced similar conditions. We have yet to face the third phase of currency collapse.

Gold and silver show the currency crisis is approaching

Clearly, a liquidity crisis has developed in paper gold and more noticeably, silver as physical metal is being demanded over paper. This tells us that inside money is already getting out of fiat and into legal money without counterparty risk. It’s the same trade as Richard Cantillon’s of 1718—1720 France, when he shorted John Law’s Mississippi scheme and his fiat livres for gold in London and Amsterdam, the principal foreign exchanges of the day.

Gold is essentially a proxy for all commodities. And while the current liquidity squeeze is raising its value anticipating a decline in currency purchasing powers, it means that commodity prices will rise, probably sharply, from the lowest real levels seen in over a 125 years. The chart below shows a basket of base metals priced in gold, but the story is the same for all commodities and raw materials. Metals are currently at only 20% of their long-term value, undoubtedly depressed by being priced in fiat dollars.

The Keynesian crowd, suspecting that demand for commodities will decline as the global (i.e. Western) economy goes into a much-vaunted recession, is wholly unaware of these price dynamics which is why they expect interest rates to remain under the control of central banks. Furthermore, we ignore what’s going on with Asia and the global south which under China’s leadership are rapidly industrialising. Growing commodity demand will be from the 70% of the world’s population who are not us.

This compounds the underlying fiat currency problem, which threatens to combine a recovery in real commodity values with a decline in their purchasing power. Measured in fiat, the rise in commodity prices promises to be spectacular.

America has engineered even greater problems for the dollar. Unless there is a significant and uncharacteristic jump in the savings rate, Trump’s tariffs will increase consumer prices even more. That they haven’t done so far should not mislead you. As Richard Cantillon explained in his Essay on Economic Theory, it takes time for the consequences of credit expansion to trickle through to higher prices.

The latest exchange with China is most concerning, because China has signalled that her export trade with America is not her priority, having slipped to under 10% of the total and set to continue declining. Trump’s tariff levers against her are therefore ineffective, and will only harm US consumers

Therefore, President Trump made a huge mistake in threatening an additional 100% tariff on Chinese goods in response to President Xi’s restrictions on rare earth exports. It appears unlikely that Xi will back down, because there is little to be gained from doing so.

The consequences of these errors will soon become obvious to bond markets, and the next leg of higher bond yields is set to commence. Banks will withdraw credit from asset speculation, leading to a stock market crash whose wider consequences will be dire.

The Fed will face funding the Federal government’s rising deficit as its revenue declines and welfare commitments rise. With bond yields rising along the curve, funding is bound to rely heavily on short-term T-bills, which as debt are near cash. The scale of debt issuance to rescue government finances and to support a debt-ridden private sector will have to be immense.

It will be a situation which was familiar to earlier generations of German citizens during the Weimar Republic. It is the third and final phase in our table above, marking the death of fiat currencies. The president of the Reichsbank, Rudolf Havenstein, would be all too familiar with the situation if he was alive today.

It is worth noting that after Germany’s stock market peaked in December 1921, the slide into the reichsmark’s dramatic collapse began. All values priced in gold marks sank lower, including housing and landed estates. At the end in November 1923, one gold mark was worth a trillion reichsmarks. Gold was the only protection. This is what gold is signalling to us today.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS /244 AND 243

LAST WEEK:

END

5. COMMODITY REPORT/GOLD TRADING

Gold Dealer Says ‘All-Time’ Records Broken as Aussies Rush to Buy Bullion

The 5,000 year old investment option is surging amid ongoing uncertainty with global tensions.

Gold bullion can be seen after being removed from casts at the ABC Refinery smelter in Sydney, Australia on April 29, 2025. David Gray/AFP via Getty Images

10/13/2025|Updated: 10/13/2025

Australians are returning to a 5000-year-old tradition as they stockpile gold and other precious metals amid years of global turbulence and uncertainty.

In recent days, viral footage has circulated online of a long line from one gold dealer’s doors in Sydney’s Martin Place.

According to major bullion dealer, Ainslie Bullion, investors have been spurred by a culmination of factors including the dropping value of currency due to uncontrolled government spending and budget deficits, as well as ballooning debt.

This has left mum and dad investors around the world looking for safe options to invest their money—and with difficulties breaking into the already sky-high property market—many have instead turned to precious metals.

The price of gold has soared from A$2,380.77 (US$1,550.71) in Oct. 11, 2021, to A$6,257.90 (US$4,076.08) in Oct. 13, 2025.

“There has been a massive surge in interest and transactions with our waiting rooms all full and instore and online orders both breaking all-time records—and we have been around for 51 years,” Ainslie Bullion CEO Michael Engeman told The Epoch Times.

“There is certainly a momentum play with the prices of gold, silver and platinum up very strongly this year and people jumping in.”

Gold has, throughout 5000 years of history, been what Engeman terms “the monetary asset of last resort, or safe haven.”

“That ranges from global resets that occur around every 80 years—and the last around 80 years ago—to financial crashes like we saw in the global financial crisis or COVID,” he said.

“On the latter, in the six worst years on the Australian ASX200 you would have been down on average 20.5 percent.

“In those very same years gold went up on average 35.5 percent, so you were 56 percent better off in gold than shares in those years.”

Gold maintains its value by being scarce as opposed to cash which can be printed in large batches, devaluing its worth.

Gold bars are pictured at a plant of gold refiner and bar manufacturer Argor-Heraeus SA in Mendrisio, southern Switzerland, on April 6, 2009. Sebastian Derungs/AFP via Getty Images

The precious metal is hard to find, expensive to mine and has traditionally increased in amount at about 1.6 percent annually—meaning investors used to look elsewhere if they were seeking stronger returns.

“If you compare that to the U.S. printing 40 percent of all the U.S. dollars ever in existence in one year during COVID-19 you get the reason why people are flocking to it,” Engeman said.

“Gold discoveries are becoming fewer and approval times to open a mine longer.”

Then there’s the case of the world’s central banks purchasing unprecedented amounts of gold as reserves, seemingly at the expense of the traditional preference for buying U.S. treasury bonds—something which has helped to drive up prices.

“This puts a solid floor under the price of gold as these are strategic long-terms sovereign nation reserves,” Engeman said.

“There is also a growing scepticism around the ‘paper promises’ that many synthetic vehicles for owning gold represent. This is seeing people turning to physical bullion which has zero counterparty risk. The old saying, ‘You don’t own it if you don’t hold it,’ is ringing large right now.”

The insight into gold-buying comes as Australian shares fell on the back of global trade tensions.

The S&P/ASX200 fell 75.5 points on Oct. 13, down 0.84 per cent, to 8,882.8, as the broader All Ordinaries lost 81 points, or 0.87 per cent, to 9,183.3, AAP reported.

Ten of 11 sectors were reported to have traded lower, while gold and rare earths miners held strong.

END

SILVER TRADING

Silver Increases 1.5 Percent on Monday, Up 76 Percent in 2025

Prices may jump to $70 per ounce in the case there is extreme inflation and sustained safe-haven buying.

23

8SavePrint

Silver bullion is offered for sale at the Chicago Coin Company in Chicago, Ill. Scott Olson/Getty Images

Reporter

10/13/2025|Updated: 10/13/2025

Silver spot prices were trading up on Monday after recently breaking through the $50 per-ounce level for the first time ever.

Spot silver was trading at $51.08 per oz. as of 6:50 a.m. EDT on Monday, up by more than 1.5 percent from Friday’s close. The metal had closed above the $50 level on Friday. The spot price for silver previously came close to $50 in April 2011, when it hit $49.54 per oz. Since the beginning of 2025, prices have jumped by more than 76 percent.

Silver prices have risen in tandem with gold, as investors flocked to these metals for safe-haven investments amid geopolitical and economic uncertainties.

The recent increase in silver prices comes amid the U.S. federal government shutdown that began on Oct. 1, which shows no signs of immediate resolution.

Although silver and gold are safe-haven investments, there are a few key differences.

For one, silver is more tied to the global economy, with more than half the demand coming from high-tech and heavy-industry sectors. As such, silver tends to be more responsive to economic changes than gold, said a post by Morgan Stanley.

Silver has higher price volatility, with prices potentially moving up two to three times more than gold in a day. Hence, investors looking to direct funds into silver must account for this volatility and the risks that come with it.

Silver-backed exchange-traded products (ETP) inflows have already seen a massive surge in the first half of the year, nonprofit international association The Silver Institute said in a July 9 statement.

“With net inflows of 95 million ounces … in the first half of 2025, silver ETP investment has already surpassed the total for all of last year. This surge reflects increasingly bullish price expectations,” it said.

As for futures positions at the Chicago Mercantile Exchange, “institutional investors have demonstrated a strong commitment to silver as a store of value for much of this year. This is reflected in the average net longs over the first six months of 2025, which achieved their highest level since the first half of 2021,” it said.

Earlier this year, large quantities of silver were shipped out from London’s physical market to the United States due to fear of tariffs on silver imports.

But now, the spot price for silver is higher than the metal’s futures price at the U.S. COMEX (Commodities Exchange) market, making it attractive for traders to bring back silver to London.

At the COMEX, silver was trading at around $49.62 per oz. for the most active December futures contract, $1.46 lower than the spot price.

“There’s a genuine shortage of silver (in London), but you’ve got 500 million ounces sitting in COMEX doing nothing,” Ryan Mangan, head of global metals and bulks trading at Macquarie, said at a briefing on Thursday.

Adrian Ash, head of research at online marketplace BullionVault, said, “So much silver went to the U.S. that there’s now almost four years’ worth of domestic demand stockpiled.”

He said that “in London, lease rates are a little over 11 percent, which is phenomenal.”

Lease rates refer to the cost of borrowing physical silver and can be used as a gauge of demand for the metal.

In a Sept. 30 post, financial services company EBC Financial Group said there was a 25 percent probability of silver prices moving to the $50–70 range.

“A break above $50 triggers momentum buying; $70+ becomes possible in an extreme inflation and safe-haven mix. This requires a macro shock or sustained policy pivot,” it said.

“Although extreme predictions of $100 are commonly seen on the internet, many analysts believe that $55–70 represents the plausible upper limit in 2025 in optimistic scenarios, unless a significant financial crisis occurs.”

EBC also warned about red flags that could reverse silver’s bull rally, including demand shocks in the solar or electronics sector and policy or regulatory headwinds.

END

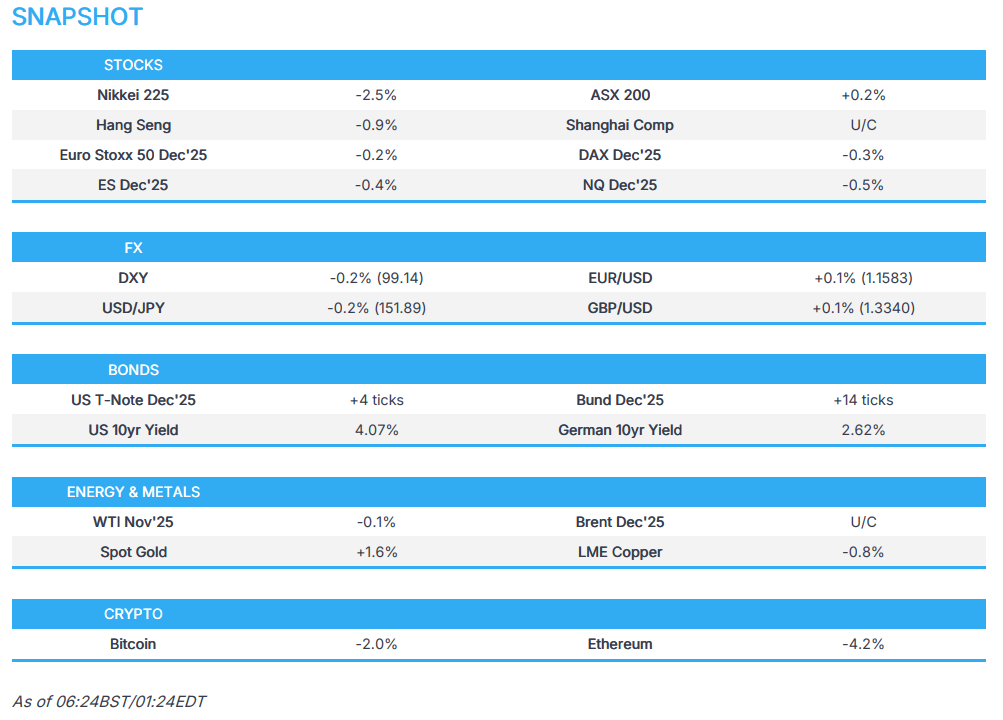

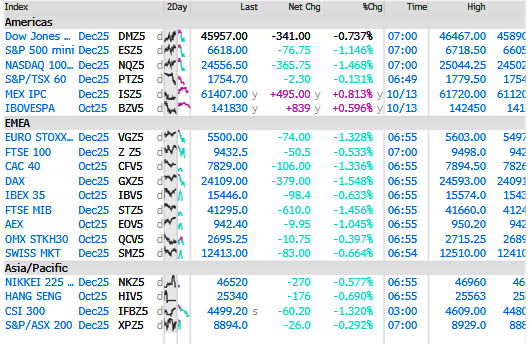

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 24.27 POINTS OR 0.62%

//Hang Seng CLOSED CLOSED DOWN 448.41 PTS OR 1.73%

// Nikkei CLOSED : DOWN 1214.48 PTS OR 2.58% //Australia’s all ordinaries CLOSED UP 0.27%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1390// OFFSHORE CLOSED DOWN AT 7.1431/ Oil DOWN TO 59.61 dollars per barrel for WTI and BRENT DOWN TO 62.66 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING DOWN TO 7.1390 // OFFSHORE YUAN TRADING DOWN TO 7.1431 :/ONSHORE YUAN TRADING ABOVE OFF SHORE / AND THUS WEAKER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1390

OFFSHORE YUAN: DOWN TO 7.1431

HANG SENG CLOSED DOWN 448.41 PTS OR 1.73%

2. Nikkei closed DOWN 1214.46 PTS OR 2.58%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 99.04 EURO RISES TO 1.1571 UP 24 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.658//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 151.74…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.229 UP 3 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR DOWN this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5980// Italian 10 Yr bond yield DOWN to 3.445 SPAIN 10 YR BOND YIELD DOWN TO 3.157

3i Greek 10 year bond yield DOWN TO 3.318

3j Gold at $4121.50 Silver at: 52.05 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 32 /100 roubles/dollar; ROUBLE AT 79.32

3m oil (WTI) into the 59 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 151.74/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.653% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.229 UP 3 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8028 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9289 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

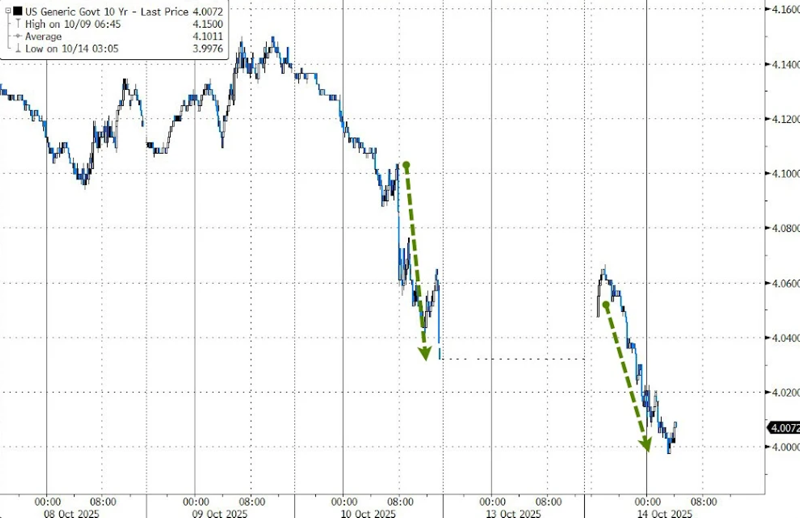

USA 10 YR BOND YIELD: 4.022 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.614 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.470 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.83 UP 2 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.6250 DOWN 4 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.4200 DOWN 4 BASIS PTS

10 YR CANADA BOND YIELD: 3.169 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.737 DOWN 0 BASIS PTS.

2a New York OPENING REPORT

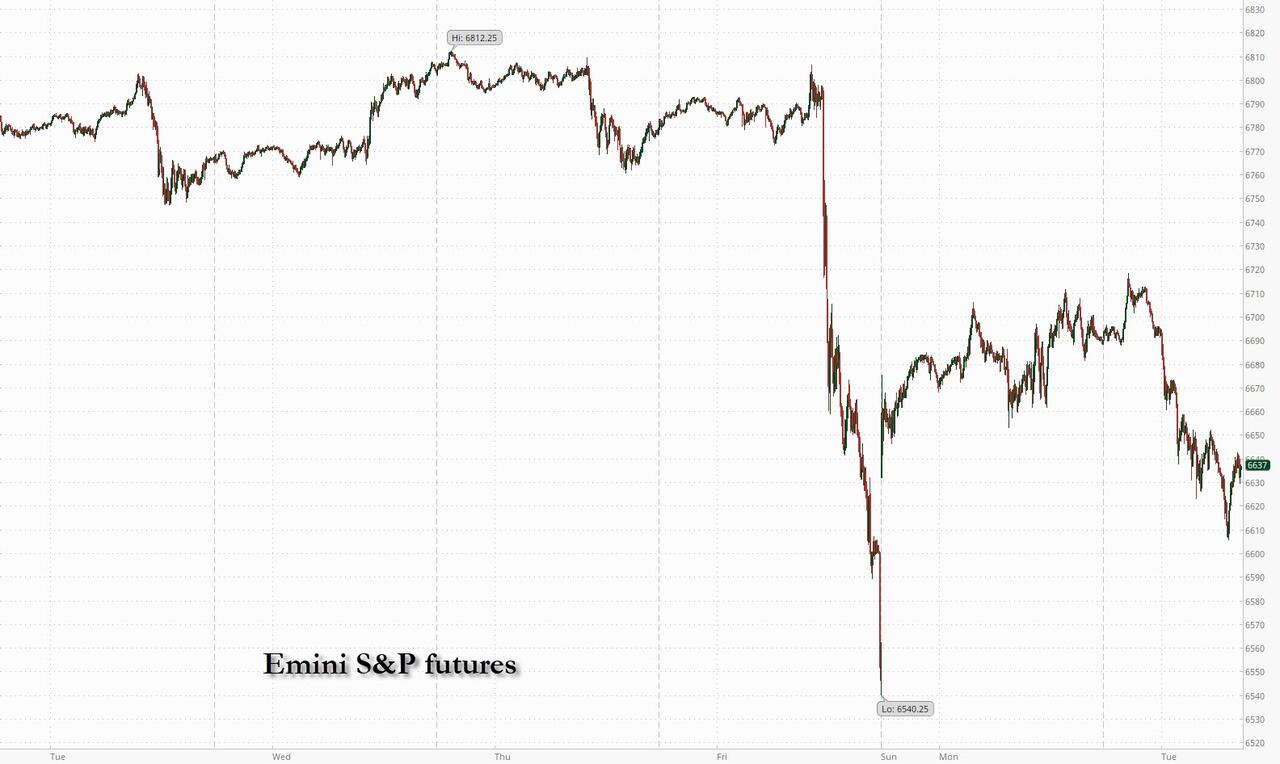

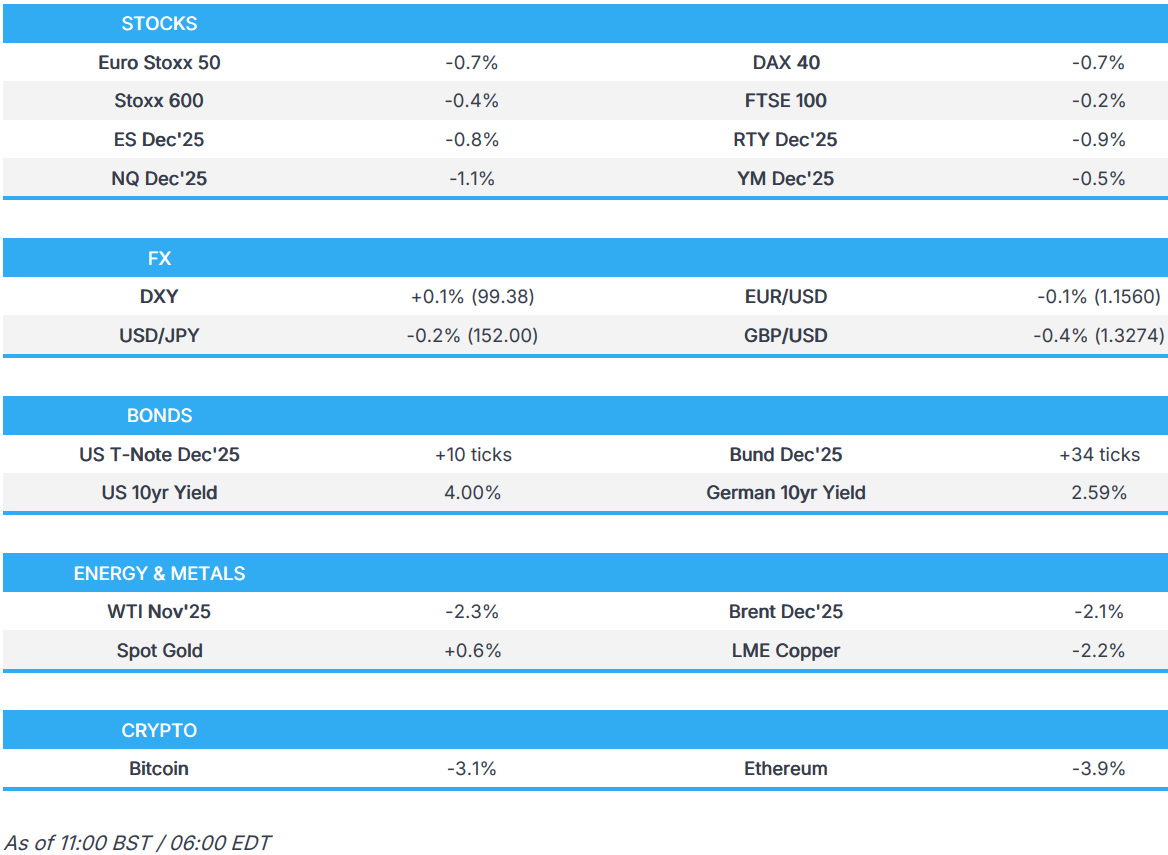

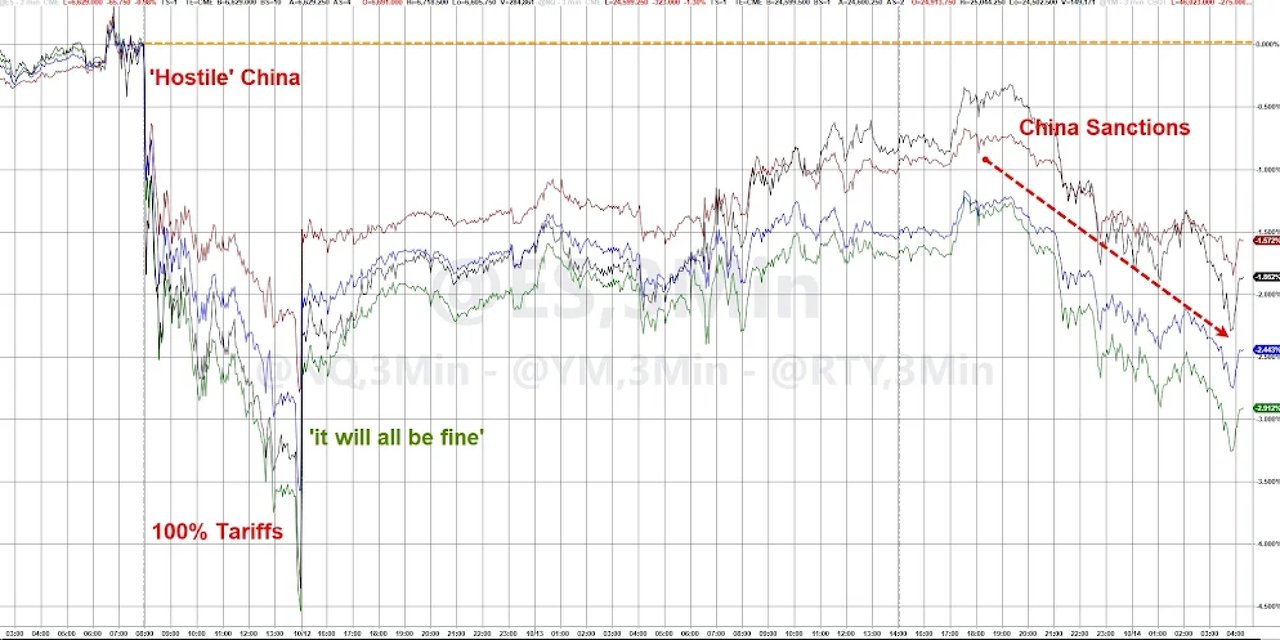

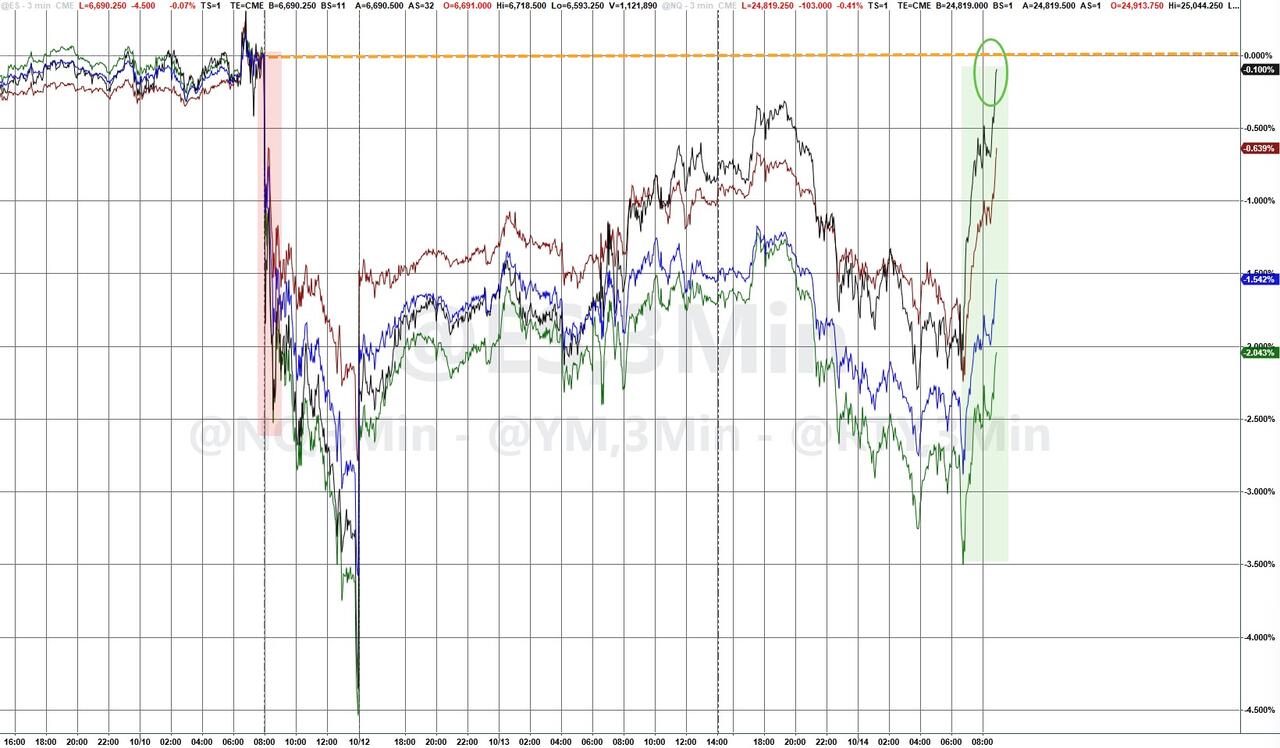

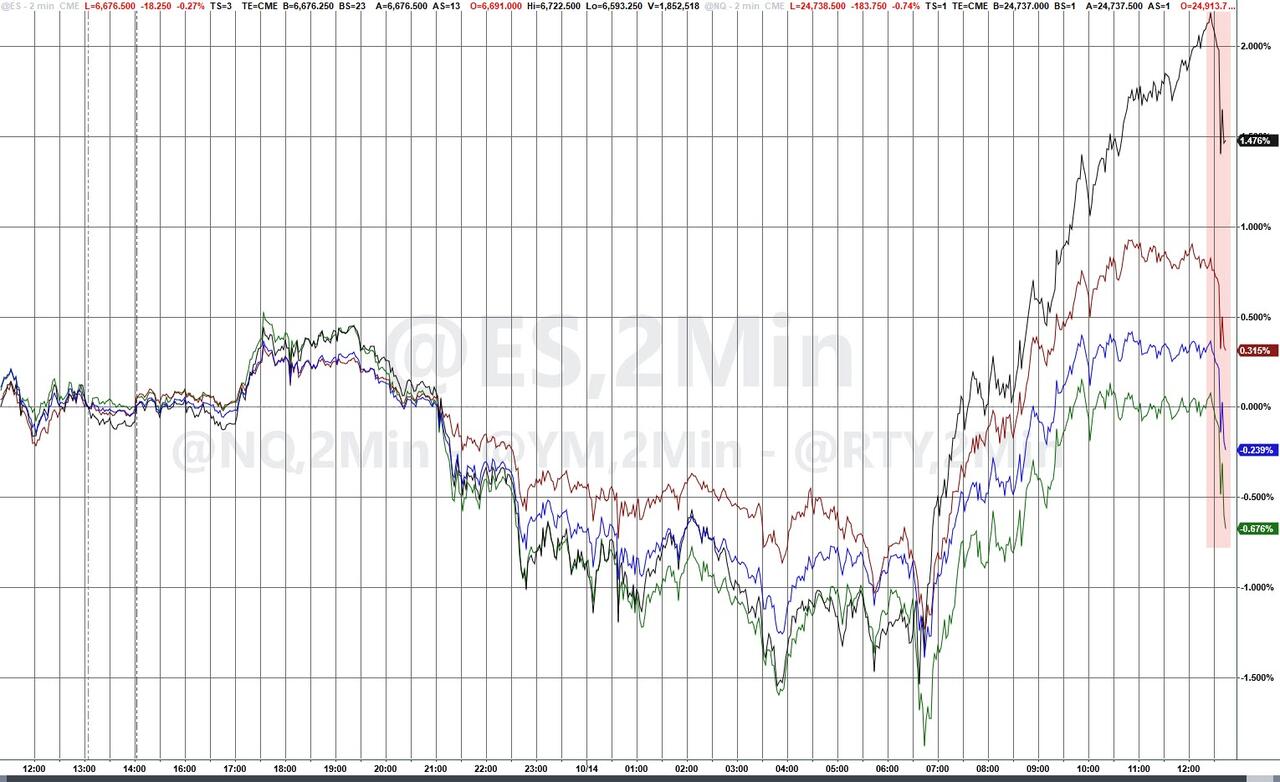

Futures Slide As Trade War Jitters Return, Q3 Earnings Begin, Powell Speaks

Tuesday, Oct 14, 2025 – 08:50 AM

The market rollercoaster continues: after Monday’s faceripping bounce, US equity futures are lower again led by tech, part of a global risk-off tone as the US/China trade war returned after Beijing vowed to “fight to the end” in the tariff and trade war, while acknowledging that the door for negotiation is open and trade talks between the two countries had resumed yesterday. Beijing also imposed curbs on the American units of Hanwha Ocean, one of South Korea’s biggest shipbuilders, as it targets US measures against the Chinese shipping sector. As of 8:00am ET, S&P futures are down 0.9% and near session lows as market may be reading the latest response by China as an ‘escalate to de-escalate’ ahead of the Trump / Xi mtg later this month. Nasdaq 100 futs were 1.1% lower with all members of the Magnificent Seven sliding in premarket trading, while European stocks slipped 0.7%. Bond yields are lower as the curve bull steepens, pushing 10Y yields briefly below 4.0%, with USD flat as the bond market returns from holiday. In addition to MegaCap Banks we have the Small Business Survey which printed below estimates, and where the section on hiring plans will be under scrutiny given the gov’t shutdown. The biggest highlight of the session is Fed Chair Powell speaking on the Economic Outlook and Monetary Policy at 12:20pm ET.