OCT 20/GOLD REGAINS ALL OF ITS LOSSES, CLOSING UP $137.70 TO $4,340.65/WITH SILVER GAINING $0.94 TO $52.14/PLATINUM GAINED $28.30 TO $1,643.25 WITH PALLADIUM CLOSING UP $23.05 TO $1,507.03//COMMODITY REPORT TODAY ON SILVER//GOLD AND SILVER EQUITY REPORTS COURTESY OF ALASDAIR MACLEOD AND JOHN RUBINO//AND A SPECIAL REPORT ON OUR PRECIOUS METALS FROM RAY DALIO//COMMENTARY TONIGHT ON THE LACK OF GDP FOR CHINA//ALSO HAS CHINA (XI) LOST CONTROL OVER THE ARMY?//TWO EUROPEAN COMMENTARIES TONIGHT FROM KOLBE//ISRAEL VS HAMAS//HAMAS BREAKS CEASEFIRE WITH ATTACKS AND COUNTER ATTACKS BY THE ISRAELIS//CEASEFIRE NOW HOLDING//VACCINE INJURY REPORTS: MARK CRISPIN MILLER/AN LPG SHIP ATTACKED NEAR YEMEN WITH A MYSTERY DRONE ATTACK (USA?)//IN USA JACK SMITH REFERRED FOR CRIMINAL PROSECUTION/COMMENTARY TONIGHT FROM VICTOR DAVIS HANSON/SWAMP STORIES FOR YOU TONIGHT//

072 C GOLDMAN 105 099 H DEUTSCHE BANK AG 564 132 C SG AMERICAS 1 190 H BMO CAPITAL MARKETS 8 323 C HSBC 1050 363 H WELLS FARGO SECURITI 479 435 H SCOTIA CAPITAL (USA) 12 657 H MORGAN STANLEY 525 661 C JP MORGAN SECURITIES 261 686 C STONEX FINANCIAL INC 1 709 C BARCLAYS 229 732 C RBC CAP MARKETS 1076 905 C ADM 9 2

TOTAL: 2,161 2,161 MONTH TO DATE: 53,544

JPMORGAN STOPPED 0/2,161

OCT

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 2161 CONTRACTs NOTICES FOR 216100 OZ or 6.7216 TONNES

total notices so far: 53,544 contracts for 5,354,400 OR 166.544 tonnes)

FOR OCT

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 312 NOTICE(S) FILED FOR 1.560 MILLION OZ/

total number of notices filed so far this month : 6454 CONTRACTS (NOTICES) for 32.270 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $137.70 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A FRAUDULENT DEPOSIT OF 12.59 TONNES OF GOLD INTO THE GLD.

INVENTORY RESTS AT 1047.21 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.94 AT THE SLV:

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:/ //A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 498.253 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 362 CONTRACTS TO 176,068 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS GOOD SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR MEGA HUGE LOSS OF $2.85 IN SILVER PRICING AT THE COMEX WITH RESPECT TO FRIDAY’S // TRADING.! WE FINALLY ARE MOVING TO A MUCH HIGHER BASE SURPASSING THE $34.40 SILVER PRICE BARRIER TO A HIGH DEGREE, AND NOW SURPASSING OUR LAST MAJOR HURDLE OF $50.00 SILVER. WE HAD A HUGE SIZED GAIN OF 1137 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE SIZED 775 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO FRIDAY’S RAID / WITH AS YOU WILL WITNESS, WITH SOME SUCCESS AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $42.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON FRIDAY WITH SILVER’S LOSS IN PRICE. THE PRICE STILL FINISHED MILES ABOVE THE MAGIC NUMBER OF $50.00 SILVER SPOT PRICE CLOSING AT $51.20 DOWN $2.85 . WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS AT A HUMONGOUS SIZED 1518 T.A.S. CONTRACTS. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING WELL ABOVE THE 50.00 DOLLAR MARK!!. THERE IS NO NEXT LINE IN THE SAND ONCE THE 50.00 DOLLAR SILVER WAS PIERCED. WE HAD A HUMONGOUS SIZED 775 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR MEGA HUGE SIZED 1518 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//RAIDS AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 1137 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR HUGE LOSS IN PRICE OF $2.85. WE HAD HUGE GOVERNMENT COMEX CONTRACTS TRADING FRIDAY AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS)

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT//SATURDAY MORNING: A HUMONGOUS SIZED 1518 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $2.85) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A MEGA MEGA HUGE SIZED GAIN OF 2084 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE..THE COMEX IS IN ONE BIG SIZED MESS!!

WE HAD A HUGE 775 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 13.240 MILLION OZ FOLLOWED BY TODAY’S 1.615 MILLION OZ CONTRACT QUEUE JUMP ALONG WITH OUR INITIAL 2.11 MILLION OZ EXCHANGE FOR RISK ISSUANCE//NEW STANDING ADVANCES TO 34.515 MILLION OZ.

THUS:

INITIAL STANDING FOR OCT: 32.405 MILLION OZ (WHICH INCLUDES ALL QUEUE JUMPING)

+ 2.110 MILLION OZ EXCHANGE FOR RISK

EQUALS

34.515 MILLION OZ..

WE HAD:

/ GOOD HUGE COMEX OI GAIN+// A HUGE SIZED EFP ISSUANCE 775 CONTRACTS (/ VI) A HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE 1578 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: A HUMONGOUS 947 CONTRACTS WERE REMOVED!!!!!!

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT.. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT.

TOTAL CONTRACTS for 14 DAY(S), total 13,760 contracts: OR 68.800 MILLION OZ (982 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 68.800 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 68.800 MILLION OZ (WILL BE HUGE THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 362 CONTRACTS DESPITE OUR LOSS IN PRICE OF $2.85 IN SILVER PRICING AT THE COMEX// FRIDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE SIZED 775 CONTRACT EFP ISSUANCE CONTRACTS: 775 ISSUED FOR DEC., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 6 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 32.405 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 34.515 MILLION OZ

THE NEW TAS ISSUANCE FRIDAY NIGHT (1518) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!!

WE HAD 312 NOTICE(S) FILED TODAY FOR 1.5600 million OZ

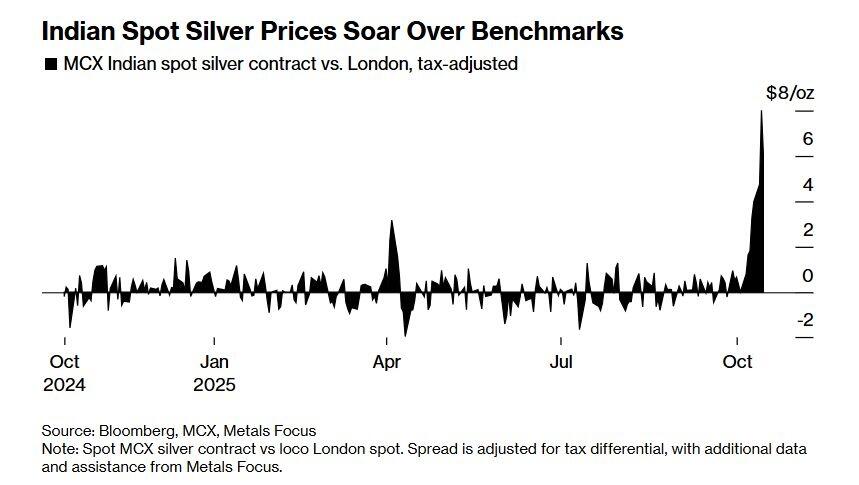

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON A MASSIVE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST SHOCKINGLY FELL BY A SMALLER SIZED 3799 OI CONTRACTS TO 479,971 OI AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A RELATIVELY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 7278 CONTRACTS //ALL GOVERNMENT RELEATED REMOVALS

WE HAD A DECREASE IN COMEX OI (3799 CONTRACTS) . THIS OCCURRED DESPITE OUR MONSTER LOSS OF $90.00 IN PRICE// FRIDAY///.

LAST 6 MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S HUGE 7.695 TONNES OF QUEUE JUMP WHICH FOLLOWED FRIDAY’S RECORD SETTING, 12.031 TONNES QUEUE JUMP TO WHICH WE ADD: 8.326 TONNES QUEUE JUMP/WEDNESDAY// WHICH FOLLOWED TUESDAY’S RECORD SETTING MONSTER 9.564 TONNES QUEUE JUMP AND WHICH WAS PRECEDED BY 42.549 TONNES QUEUE JUMPING FOR OCT. THEN WE MUST ADD OUR 11.353 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/5 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 179.471 TONNES OF GOLD.

E.F.P. ISSUANCE/FOR OPENING OCT GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2873 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 479,971 / AND WE NOW WITNESSING A STRONG COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A STRONG SIZED COMEX OI OF 176,068 CONTRACTS

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2141 CONTRACTS WITH 3799 CONTRACTS DECREASED AT THE COMEX// AND A HUGE SIZED 5940 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2,141 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED AND CRIMINAL 2338 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON LIKE THURSDAY, OCT 9. AND TODAY’S ATTEMPTED RAID!

GOLD PRICE ON FRIDAY FELL BY $90.00

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(5940) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI OF 3799 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2,141 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING FOR GOLD FOR OCT AT 90.012 TONNES OF NORMAL DELIVERY+TODAY’S QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED FRIDAY’S RECORD SETTING, 12.021 WHICH FOLLOWED THURSDAY’S 8.326 WHICH FOLLOWED WEDNESDAY’S 6.469 TONNES + PREVIOUS QUEUE JUMPS OF 42.549 TONNES+ 11.353 TONNES TOTAL EX FOR RISK//5 OCCASIONS//NEW TOTAL OF GOLD STANDING; 179.471 TONNES

NEW STANDING FOR GOLD, OCT CONTRACT AT 179.471 TONNES OF GOLD

/ 3) HUGE T.A.S. LIQUIDATION (AND CONSIDERABLE GOVT LIQUIDATION AND STRONG LIQUIDATION OF EQUITY SHARES) AS WE HAD 1)A HUGE $90.00 COMEX PRICE LOSS. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A FAIR GAIN OF 2141 CONTRACTS ON OUR TWO EXCHANGES. THIS WAS COUPLED WITH CONSIDERABLE GOVERNMENT LIQUIDATED CONTRACTS ALONG WITH HUGE TAS LIQUIDATION AND HUGE GOLD EQUITY SHARES/./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND YOU CAN VISUALIZE THIS BY THE HUGE AMOUNTS OF QUEUE JUMPING WE HAVE BEEN HAVING LATELY

4) FAIR SIZED COMEX OI GAIN// 5) V) HUGE SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (2873)

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT. :

TOTAL EFP CONTRACTS ISSUED: 52,268 CONTRACTS OR 5,226,800 OZ OR 162.575 TONNES IN 14 TRADING DAY(S) AND THUS AVERAGING: 3733 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN14 TRADING DAY(S) IN TONNES: 162.575 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 162.575 TONNES DIVIDED BY 3550 x 100% TONNES = 4.57% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 162.575 TONNES//CERTAINLY MUCH LARGER THIS MONTH

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A GOOD SIZED 362 CONTRACTS OI TO 177,015 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A HUGE 775 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 775 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 775 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1309 CONTRACTS AND ADD TO THE SMALL 775 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 2084 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $2.85 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 5.685 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS MONDAY MORNING:

SHANGHAI CLOSED UP 24.14 POINTS OR 0.63%

//Hang Seng CLOSED CLOSED UP 611.73 PTS OR 2.42%

// Nikkei CLOSED : UP 1603.35 PTS OR 3.39% //Australia’s all ordinaries CLOSED UP 0.34%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1215// OFFSHORE CLOSED UP AT 7.1239/ Oil UP TO 57.20 dollars per barrel for WTI and BRENT DOWN TO 61.09 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING UP TO 7.1215 // OFFSHORE YUAN TRADING DOWN TO 7.1239 :/ONSHORE YUAN TRADING ABOVE OFF SHORE / AND THUS STRONGER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST SHOCKINGLY FELL BY A MUCH SMALLER FAIR SIZED 3799 CONTRACTS TO 479,971 OI DESPITE OUR HUGE LOSS IN PRICE OF $90.00 WITH RESPECT TO FRIDAY’S RAID // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, DESPITE THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A HUMONGOUS NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (5940). WE HAD HUGE T.A.S. LIQUIDATION FRIDAY. WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 2,141 CONTRACTS (OR 6.66 TONNES).THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

EXCHANGE FOR PHYSICAL//GOLD ISSUANCE//OCTOBER:

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT FOR GOLD REMAINS AT 11.353 TONNES OF GOLD UNDER THE GUIDANCE OF 5 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 5 ISSUANCES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES TOTAL ISSUANCES 5 OCCASIONS FOR 3650 CONTRACTS OR 365,000 OZ OR 11.353 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN FINALLY OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES TOTAL ISSUANCE ON 5 OCCASIONS: 11.353 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 127.5 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 126.5 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OCTOBER COMEX MONTH//

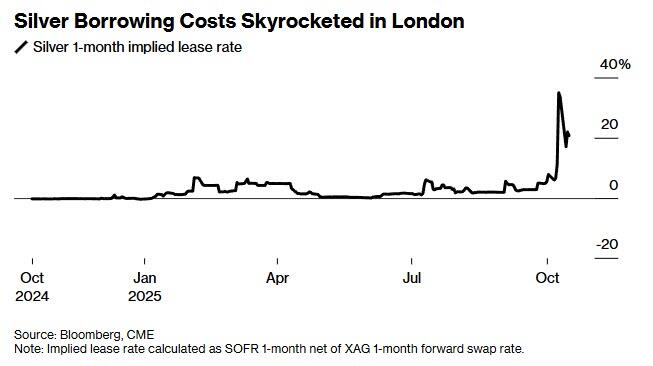

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 2,141 CONTRACTS DESPITE OUR HUGE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A GOOD SIZED T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 2,338 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN ON FRIDAY’S HJUGE RAID, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS WE WE WILL PROBABLY SEE GOLD//SILVER RISE HUGELY ON MONDAY.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS: (LIKE TODAY)

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING)

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS NOW BRINGS US TO OCTOBER WHERE INITIAL AMOUNT OF GOLD STANDING IS 28,988 CONTRACTS FOR 90.114 TONNES OF GOLD TO WHICH WE ADD OUR FIRST MASSIVE QUEUE JUMP OF 4.898 TONNES QUEUE JUMP FOLLOWED BY OCT 4 QUEUE JUMP OF 0.9704 TONNES TO BE FOLLOWED BY OCT 7 QUEUE JUMP OF 3.623 TONNES, THEN OCT 8’S HUGE 6.942 TONNES QUEUE JUMP, OCT 9 HUGE 4.979 TONNES OF QUEUE JUMP, OCT 10 MASSIVE QUEUE JUMP OF 7.504 CONTRACTS(250,900 OZ//7.504 TONNES) AND THEN OCT 13: 4.3919 TONNES// AND THEN OCT 14 WITH A RECORD SETTING 9.564 TONNES AND THEN WEDNESDAY’S MASSIVE 6.469 TONNES QUEUE JUMP AND THEN THURSDAY’S QUEUE JUMP AT 8.326 TONNES. YESTERDAY’S HUGE RECORD SETTING 12.031 TONNES QUEUE JUMP //// AND THIS WAS AUGMENTED BY AN UNUSUAL 50,000 CONTRACT EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE AND THEN ON THREE CONSECUTIVE OCCASIONS, OCT 2 THROUGH TO THE OCT 4.THEY TOOK ONE DAY OFF AND THEN ISSUED ITS 5 EXCHANGE FOR RISK ISSUANCE FOR 1000 CONTRACTS OR 100,000 OZ/3.1105 TONNES THE NEW TOTAL ON THESE 5 ISSUANCES IS 3650 CONTRACTS FOR 365,000 OZ OR 11.353 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERIES INCLUDING QUEUE JUMPS. NEW TOTALS FOR GOLD STANDING ADVANCES TO 179.471 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 243 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH OCTOBER AND SUBSEQUENT STANDING FOR GOLD.

AUGUST:

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPT:

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES WHICH INCLUDES ALL QUEUE JUMPING.

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 3,650 EXCHANGE FOR RISK CONTRACTS ON 5 OCCASIONS FOR 365,000 OZ OR 11.353 TONNES.! TOTAL STANDING ADVANCES TO 179.471 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

TOTAL EXCHANGE FOR RISK OCT 5 OCCASIONS: 11.353 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT:

E) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

F) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

G) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

H) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

I) A MASSIVE QUEUE JUMP OCT 9 FOR 4.979 TONNES

J) A MASSIVE AND 3RD HIGHEST EVER OCT 10 QUEUE JUMP FOR 7.504 TONNES

I) A MASSIVE QUEUE JUMP OF 4.3919 TONNES

J) A RECORD SETTING QUEUE JUMP OF 9.564 TONNES

K) A HUGE 6.469 TONNES QUEUE JUMP

L) A HUGE 8.326 TONNES QUEUE JUMP

M) A RECORD SETTING 12.031 TONNE QUEUE JUMP THE HIGHEST EVER RECORDED IN COMEX HISTORY SURPASSING TUESDAY’S 9.564 TONNES

N/ QUEUE JUMP OF 7.695 TONES OF GOLD//

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

179.471 TONNES OF GOLD!!

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A MEGA HUGE SIZED EXCHANGE FOR PHYSICAL OF 5948 CONTRACTS.

THAT IS A STRONG SIZED 5948 EFP CONTRACT WAS ISSUED: : /DEC 5948 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5948 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON!

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//FRIDAY + GOVERNMENT LIQUIDATION

MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE SEPT 30 WITH OUR ATTEMPTED FAILED RAID, FOLLOWED BY ANOTHER RAID OCT 2 AND THAT ENDED IN TOTAL FAILURE! , OCT 7 WE WITNESSED A SMALL RAID TRYING TO STOP GOLD’S ADVANCE TO THE 4000 BARRIER!! EARLY Y\OCT 8 MORNING THE BARRIER TO 4,000 DOLLAR GOLD WAS PIERCED!! AND THAT SET IN MOTION OUR CROOKS DESPERATE TO CONTROL THEIR HUGE DERIVATIVE LOSSES. (OCT 9 SAW FINALLY AFTER MANY YEARS SILVER PIERCING THE 50 DOLLAR MARK AND THAT WAS WHEN THE CROOKS THREW ANOTHER TEMPER TANTRUM WHEN GOLD FINALLY BROKE THROUGH 4,000 DOLLAR MARK ON OCTO 10 AND THAT FAILED AND FROM THAT POINT GOLD NEVER LOOKED BACK!!

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT/SATURDAY MORNING WAS A STRONG SIZED SIZED 2338 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK AND THEN OCT 9, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING FAIR GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

TO BE FOLLOWED BY OCTOBER’S 5 ISSUANCES FOR 11.383 TONNES

THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S MEGA HUGE 7.695 TONNES WHICH FOLLOWED FRIDAY’S HUGE: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S 8.326 TONNES, FOLLOWING WEDNESDAY’S HUGE 6.469 TONNES WHICH FOLLOWED TUESDAY;S RECORD SETTING 9.564 TONNES OF A QUEUE JUMP TO WHICH WE ADD ALL OTHER QUEUE JUMPS IN OCT OF 33.009 TONNES WHICH MUST BE ADDED TO OUR 5 ISSUANCES OF 11.353 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 179.471 TONNNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $90.00./ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE FAIR SIZED GAIN IN OI FROM TWO EXCHANGES OF 2,141 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION FRIDAY .THIS WAS COUPLED WITH GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION). ON TUESDAY OCT 7, WE WITNESSED FOR NO REASON A MASSIVE LIQUIDATION IN PRICE OF OUR GOLD EQUITY SHARES LIKE AGNICO EAGLE AND BARRICK GOLD /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS EVEN THOUGH THEY TRANSFERRED THESE LOSSES ONTO THE FED’S BALANCE SHEET.THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS TRIED AGAIN LATEOCT 2 WITH CHINA OUT FOR A WEEK, WITH NOT MUCH LUCK. WITH CHINA COMING BACK THURSDAY OCT 9 THE CROOKS NEEDED TO RAID TRYING DESPERATELY TO HALT GOLD’S ADVANCE. I GUESS THAT THEIR LUCK HAS RUN OUT WITH GOLD INITIALLY PIERCING THE 4,000 DOLLAR BARRIER OCT 7-8 ALONG WITH THE PIERCING OF SILVER’S MAGIC 50 DOLLAR MARK. GOLD AND SILVER FROM OCT 10 ON NEVER LOOKED BACK ONCE THEY PIERCED THEIR RESPECTIVE BARRIERS OF 4,000 DOLLAR GOLD AND 50 DOLLAR SILVER.

SATURDAY MORNING//FRIDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL FRIDAY EVENING/ SATURDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A FAIR SIZED GAIN OF A TOTAL OF 6.66 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES TO BE FOLLOWED BY FRIDAY’S HUGE 7.695 TONNES/QUEUE JUMP WHICH FOLLOWED FRIDAY’S MASSIVE 12.031 TONNES OF QUEUE JUMP AND THEN 57.356 TONNES OF PREVIOUS QUEUE JUMPS TO WHICH WE ADD OUR 11.353 TONNES EX FOR RISK/5 OCCASIONS:

/ NEW TOTAL STANDING 179.471 TONNES.

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $90.00

WE HAD A HUGE 7278 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 2141 CONTRACTS OR 214,100 0Z (6.66 TONNES)

i) Out of Brinks 64,302.000oz (2000 kilobars) ii) Out of JPM 10,904.358 oz

total withdrawal 75,206.358oz or 2.333 tonnes of gold//

.

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

DEPOSITS/CUSTOMER

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

2161 notice(s) 216,100 OZ 6.7216 TONNES

No of oz to be served (notices)

506 contracts 50,600 OZ 1.573 TONNES

Total monthly oz gold served (contracts) so far this month

53,544notices 5,354,400oz 166.544 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

2 entries

i) Out of Brinks 64,302.000oz (2000 kilobars) ii) Out of JPM 10,904.358 oz

total withdrawal 75,206.358oz or 2.333 tonnes of gold//

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 3

a) dealer to customer account

Brinks 283,404.417 oz

HSBC: 12,635.343 oz

JPMorgan 16,789.330 oz

volume at the comex: Monday: 611,632oz (mega humongous//highest volume in over a decade)

AMOUNT OF GOLD STANDING FOR OCTOBER

THE FRONT MONTH OF OCTOBER STANDS AT 2667 CONTRACTS FOR A LOSS OF ONLY 1860 CONTRACTS.

WE HAD 4334 CONTRACTS FILED ON FRIDAY SO WE GAINED A MEGA MEGA HUGE 2474 CONTRACT QUEUE JUMP FOR 247,900 OZ OR 7.695 TONNES OF GOLD, WHICH FOLLOWED FRIDAY’S, HIGHEST EVER QUEUE JUMP RECORDED IN COMEX HISTORY OF 12.54 TONNES TONNES OF GOLD WHICH FOLLOWED BY ALL THE REST OF OCTOBER QUEUE JUMP OF 57.356 TONNES

THUS OUR NEW NORMAL DELIVERY RISES TO 168.118 TONNES WHICH INCLUDES ALL PREVIOUS QUEUE JUMPS) PLUS OUR 11.353 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD ADVANCES TO 179.471 TONNES

NOVEMBER GAINED 2002 CONTRACTS UP TO 5872 CONTRACTS.

DECEMBER LOST 3246 CONTRACTS DOWN TO 365,862 CONTRACTS.

We had 2161 contracts filed for today representing 216,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 261 notices issued from their client or customer account. The total of all issuance by all participants equate to 2161 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (53,544 oz ) to which we add the difference between the open interest for the front month of OCT ( 2667 CONTRACTS) minus the number of notices served upon today (2161x 100 oz per contract) equals 5,405,000 OZ OR 168.118TONNES OF GOLD TO WHICH WE ADD OUR 5 ISSUANCES OF 11.353 TONNES OF EXCHANGE FOR RISK //NEW TOTALS STANDING FOR GOLD OCTOBER ADVANCES TO 179.471 TONNES. NO WONDER THE COMEX IS IN TURMOIL WITH THIS MAMMOTH STANDING FOR GOLD.

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (53,544 x 100 oz +we add the difference for front month of OCT. (2667 OI} minus the number of notices served upon today (2161 x 100 oz) which equals 5,405,000 OZ OR 168.118 TONNES + 11.353 TONNES EXCHANGE FOR RISK//NEW TOTAL OF GOLD STANDING IN OCTOBER ADVANCES TO 179.471 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 179.471 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

volume Wednesday confirmed 327,800 contracts huge

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,900,526.493 oz 59.11 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,031,591.937oz

TOTAL REGISTERED GOLD 20,688,092.605 or 643.48tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,343,,797.332 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 1,878,755 oz ((REG GOLD- PLEDGED GOLD)= 584.37tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

OCT 20 2025

INITIAL/

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

5 entries

i) Out of Asahi 300,552,800 oz ii) Out of Brinks 200,512.860 oz

iii) Out of CNT: 591,839.530 oz iv) Out of Loomis 3,001,048.900oz v) Out of Stonex: 151,072.800 oz

total withdrawal 4,245,027.890 oz

Deposits to the Dealer Inventory

0 ENTRY

Deposits to the Customer Inventory

2 entries

i) Into CNT 653,637.500 oz ii) Into Stonex 599,687,300 oz

total deposit 1,253,324.800oz

No of oz served today (contracts)

312 CONTRACT(S) ( 1.560 MILLION OZ

No of oz to be served (notices)

27 contracts (0.135 MILLION oz)

Total monthly oz silver served (contracts)

6454 Contracts (32.270 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 entries

2 entries

i) Into CNT 653,637.500 oz ii) Into Stonex 599,687,300 oz

i) Out of Asahi 300,552,800 oz ii) Out of Brinks 200,512.860 oz

iii) Out of CNT: 591,839.530 oz iv) Out of Loomis 3,001,048.900oz v) Out of Stonex: 151,072.800 oz

total withdrawal 4,245,027.890 oz

adjustments: 4

2 dealer to customer

a) JPMorgan: 70,143,580oz

b) Brinks: 261,174.660oz

customer to dealer

c)Loomis 25,634.360 ozoz

d)Delaware 14,873.518 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 171.280 MILLION OZ//.TOTAL REG + ELIGIBLE. 506.467 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 339 OPEN INTEREST CONTRACTS FOR A GAIN OF 17 CONTRACTS.

WE HAD 308 CONTRACTS SERVED ON FRIDAY, SO WE GAINED 325 CONTRACTS WHICH UNDERWENT A STRONG QUEUE JUMP FOR 1.625 MILLION 0Z

THUS

NORMAL STANDING FOR SILVER OCT ADVANCES TO 32.405 MILLION OZ WHICH INCLUDES TODAY’S STRONG 1.625 MILLION OZ QUEUE JUMP + 2,110 MILLION OZ EX. FOR RISK = 34.515 MILLION OZ WHICH IS MASSIVE FOR A NON DELIVERY MONTH!!

NOVEMBER LOST 1 CONTRACTS UP TO 2399

DECEMBER LOST 102 CONTRACTS UP TO 127,367

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 312 or 1.56 MILLION oz

CONFIRMED volume; ON FRIDAY 195,510 mega immense++++//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 6454 X5,000 oz = 32.270 MILLION oz

to which we add the difference between the open interest for the front month of OCT (339) AND the number of notices served upon today (312 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (6454) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(339) minus number of notices served upon today (312)x 5000 oz equals silver standing for the OCT.contract month equating to 32.405 MILLION OZ to which we must add our initial 2.110 million oz exchange for risk issuance//new standing advances to 34.515 which is mammoth for a non active delivery monthj.

New total standing: 34.515 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 171.280 million oz of registered silver

JPMorgan as a percentage of total silver: 208,118/506.467million. 41.08%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12/59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

GLD INVENTORY: 1047.21 TONNES, TONIGHTS TOTAL

SILVER

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

Once again, the regional banks are in trouble. This time, the crisis began with several commercial/industrial loan defaults and is progressing into yet another multi-billion-dollar bailout via the repo market. Here’s a concise X post with the details: Echo 𝕏@echodatruth

While Everyone’s Distracted… Most people have no idea what just happened. On October 16th, 2025, the Federal Reserve Bank of New York quietly injected $8.35 BILLION into the financial system through something called a Repo Operation, and that’s just what they admitted publicly. Nearly 80% of that was backed by mortgage-backed securities, not Treasuries. Translation: the banks are running out of cash, and they’re now pawning off their riskiest assets just to get short-term liquidity. Let me break it down: The Repo Market is basically a virtual pawn shop for banks. They bring their “valuables” government bonds or mortgage-backed securities and the Fed gives them a quick cash loan overnight. The next day, they “repurchase” their collateral. That’s why it’s called a repurchase (repo) agreement. Now here’s the problem When banks start pawning mortgage-backed securities instead of safe Treasuries, it means they’re desperate for cash. It’s like someone pawning their TV, their car, and then finally their wedding ring. And the Fed knows it. That’s why they quietly announced a $491.65 BILLION Standing Repo Facility for later that same day — nearly half a trillion dollars in emergency overnight liquidity. They don’t prep half a trillion unless something behind the curtain is breaking. Meanwhile, what’s trending right now? Protests. Political drama. Manufactured headlines designed to divide and distract. While the world argues, the monetary system is quietly unraveling in real time. This isn’t a conspiracy. It’s public data straight from the Fed’s own website. We’ve passed the point of no return. You can’t print your way out of a debt-based system forever. You can’t keep pretending it’s fine when the repo window is catching fire again.

Accident Waiting to Happen Regional banks own a lot of commercial and residential real estate loans, and — with office buildings and car mortgages leading the way — much of that paper is going bad. When one borrower defaults, everyone starts wondering who’s next. And they find plenty of likely suspects, which triggers an exodus of capital from the riskiest banks, in turn leading to a government bailout. This shifts the pressure from banks to the currency, sending capital out of financial assets and into real things. Hence, the gold bull market. And this is just the start. Keep stacking.

Friday’s knockdown was severe and shocked investors, particularly those who just recently jumped on the gold/silver bandwagon. But that was what it was designed to do!

Kipling’s famous lines are called to mind:If you can keep your head when all about you are losing theirs… They seem apt in these markets. A cold rational examination of the following simple facts is timely:

· Recently, overnight buying seemed to have come from Asia, with Europe waking up to higher prices and being squeezed, particularly in silver. But on Friday, there was some profit-taking in Hong Kong / China. Consequently, prices were steady in London until New York opened and after an hour’s trading prices slid sharply lower. Ahead of the weekend, buyers in London where the silver squeeze is acute were happy to watch from the sidelines. Weekend factors played an important part in timing.

· The slide was a Comex affair only, coinciding with increased margin requirements. However, current speculative positions usually shaken out by margin increases are not extreme, so the margin factor should not be overemphasised.

· The backwardation between London spot and Comex futures remains at $1.24 indicating the silver squeeze is still on.

· Friday’s knockdown is unlikely to change a worldwide panic into gold and silver by ordinary people. And rising demand for ETFs appears to have only just started.

We have always cautioned against trading gold and silver futures, because you get whipsawed. This knockdown in paper markets is a classic.

The reason for owning gold and silver is to get out of credit, which is in an enormous bubble. So much so that even central bankers and the likes of Jamie Dimon are now warning us of the dangers. The next chart, of margin debt says more about the stock bubble than anything else:

Well over a trillion dollars in soaring margin debt finances stock positions worth $3 to $4 trillion. And punters who leverage their positions are inherently weak momentum players.

As well as this elephant in the room, there are increasing concerns about the banking and shadow banking systems. In the latter case, private equity and hedge funds are borrowing from the banks to lend at higher rates to businesses that are invariably zombies because the banks won’t lend to them. It is a situation that rings loud alarm bells (cf. Jamie Dimon’s ‘cockroach’ statement about bad debts — see one and there will always be lots more).

Increasing caution expressed by leading bankers inevitably leads to credit being withdrawn from the private equity and hedge funds playing this game. And we are beginning to see that that most sensitive financial asset, bitcoin, is losing momentum and beginning to slide.

This pseudo money, like tulipomania, is a classic bubble play and an important timing signal. As the next chart shows, it appears to be falling out of a broadening top formation which is a very bad sign, particularly when hodlers believe it to be a credit hedge:

The reason for emphasising the credit bubble in an article about gold and silver is that when it implodes, which bubbles always do, it is the value and not the quantity of credit that takes it on the chin. The reason is simple: central banks and their political masters become frightened about the other side of credit, which is debt. They simply cannot afford to stand by and watch escalating defaults in the banks and other financial intermediaries as the combined credit and debt bubble implodes. Rescuing insolvent borrowers and banks simply kills the value of credit, including that of fiat currencies, which are the top level of credit. This is why the gold price soars after a central bank rides to the rescue of everything.

Today, there are additional uncertainties — a US president who is capricious and at loggerheads with Jay Powell, and a government that is hampered by being shut down due to the debt ceiling. Increasing credit risk could not happen at a worst time. And we haven’t even considered weaknesses in other jurisdictions, which make a coordinated G7 response to a credit implosion difficult to envisage.