access market

GOLD $4024.15 (3:30 PM)

SILVER: 48.90 (3:30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 3 CONTRACTs NOTICES FOR 300 OZ or 0.00933 TONNES

total notices so far: 58,822 contracts for 5,882,200 OR 182.961 tonnes)

SILVER NOTICES: 10 NOTICE(S) FILED FOR 0.050 MILLION OZ/

total number of notices filed so far this month : 7912 CONTRACTS (NOTICES) for 39.560 million oz

INITIAL STANDING FOR OCT: 39.565 MILLION OZ (WHICH INCLUDES ALL QUEUE JUMPING)

+ 2.110 MILLION OZ EXCHANGE FOR RISK

EQUALS

41.675 MILLION OZ..

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 81.520 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 246.2706 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A TINY SIZED 135 CONTRACTS OI TO 158,052 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 300 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 300 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 135 CONTRACTS AND ADD TO THE 300 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF 165 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR HUGE GAIN OF $0.95 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 1.225 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.95

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 29.43 POINTS OR 0.73%

//Hang Seng CLOSED CLOSED DOWN 63.45 PTS OR 0.24%

// Nikkei CLOSED : UP 17.96 PTS OR 0.04% //Australia’s all ordinaries CLOSED DOWN 0.43%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1092// OFFSHORE CLOSED DOWN AT 7.1083/ Oil UP TO 60.04 dollars per barrel for WTI and BRENT UP TO 64.43 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING DOWN TO 7.1092 // OFFSHORE YUAN TRADING DOWN TO 7.1083 :/ONSHORE YUAN TRADING BELOW AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMAL 944 CONTRACTS TO 456,178 OI DESPITE OUR GAIN IN PRICE OF $15.20 WITH RESPECT TO THURSDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST NO NET LONGS, DESPITE THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4300). WE HAD CONSIDERABLE T.A.S. LIQUIDATION TUESDAY. HOWEVER AGAIN, IT WAS THE MAJOR SPECULATORS THAT WENT SHORT AND THE BANKERS WHO TOOK THE LONG SIDE AS THE SHORTS WERE LED BY THE NOSE BY THE BANKERS. THEN MUCH TO THH SPECS HORROR, THE BANKERS TENDERED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD.

WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3356 CONTRACTS (OR 10.43 TONNES).THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

EXCHANGE FOR PHYSICAL//GOLD ISSUANCE//OCTOBER:

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT FOR GOLD REMAINS AT 14.553 TONNES OF GOLD UNDER THE GUIDANCE OF 6 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 127.5 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 130.3 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OCTOBER COMEX MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 3356 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR SIZED T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1517 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN ON LAST FRIDAY’S AND TUESDAY’S HUGE RAIDS, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS WE WE WILL PROBABLY SEE GOLD//SILVER RISE HUGELY ON OUR UPCOMING DAYS.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS:

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE SET TO BEGIN OPTION EXPIRY WEEK, THE CROOKS HAVE DECIDED TO RAID AGAIN. IT WILL BE QUITE A TRADING WEEK //OTC OPTIONS EXPIRY FRIDAY OCT 31..COMEX EXPIRY TUESDAY OCT 28. THE FED IS MOST LIKELY TRYING TO CONTAIN THE PRICE OF GOLD AND SILVER PRIOR TO THEIR MEETING OCT 29 WHERE HE WILL LOWER INTEREST RATES (MAYBE 1/2 PT) AND THAT WILL SET A FIRESTORM OF PRICE INFLATION.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT:

F) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

G) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

H) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

I) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

J) A MASSIVE QUEUE JUMP OCT 9 FOR 4.979 TONNES

K) A MASSIVE AND 3RD HIGHEST EVER OCT 10 QUEUE JUMP FOR 7.504 TONNES

L) A MASSIVE QUEUE JUMP OF 4.3919 TONNES

M) A RECORD SETTING QUEUE JUMP OF 9.564 TONNES

N) A HUGE 6.469 TONNES QUEUE JUMP

0) A HUGE 8.326 TONNES QUEUE JUMP

P) A RECORD SETTING 12.031 TONNE QUEUE JUMP THE HIGHEST EVER RECORDED IN COMEX HISTORY SURPASSING TUESDAY’S 9.564 TONNES

Q/ QUEUE JUMP OF 7.695 TONES OF GOLD//

R/ TODAY’S QUEUE JUMP OF 3.8600 TONNE JUMP

S) OCT 22 QUEUE JUMP OF 8.622 TONNES//

T) 1OCT 23 1.695 TONNES

U) OCT 24. 0.8615 TONNES

V) OCT 27 0.3048 TONNE QUEUE JUMP

W) OCT 28 QUEUE JUMP OF .5069

X) OCT 29 QUEUE JUMP OF .4096 TONNES

Y) OCT 30 QUEUE JUMP OF 0.00311 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 245 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH SEPT. AND SUBSEQUENT STANDING FOR GOLD.

AUGUST:

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPT:

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES WHICH INCLUDES ALL QUEUE JUMPING.

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 4300 CONTRACTS.

THAT IS A STRONG SIZED 4300 EFP CONTRACT WAS ISSUED: : /DEC 4300 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4300 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON!

WE HAD :

- SOME LIQUIDATION OF OUR T.A.S. SPREADERS//WEDNESDAY + GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE SEPT 30 WITH OUR ATTEMPTED FAILED RAID, FOLLOWED BY ANOTHER RAID OCT 2 AND THAT ENDED IN TOTAL FAILURE! , OCT 7 WE WITNESSED A SMALL RAID TRYING TO STOP GOLD’S ADVANCE TO THE 4000 BARRIER!! EARLY Y\OCT 8 MORNING THE BARRIER TO 4,000 DOLLAR GOLD WAS PIERCED!! AND THAT SET IN MOTION OUR CROOKS DESPERATE TO CONTROL THEIR HUGE DERIVATIVE LOSSES. (OCT 9 SAW FINALLY AFTER MANY YEARS SILVER PIERCING THE 50 DOLLAR MARK AND THAT WAS WHEN THE CROOKS THREW ANOTHER TEMPER TANTRUM WHEN GOLD FINALLY BROKE THROUGH 4,000 DOLLAR MARK ON OCT. 10 AND GOLD NEVER LOOKED BACK DESPITE OUR TWO RAIDS THIS PAST WEEK, ON FRIDAY AND OCT 21 AND ATTEMPTED RAID OCT 24

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A FAIR SIZED SIZED 1517 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK AND THEN OCT 9 AND THEN OCT 21 AND NOW OCT 24, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING FAIR GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $15.20./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR GAIN IN OI FROM TWO EXCHANGES OF 3356 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD SOME T.A.S. SPREADER LIQUIDATION WEDNESDAY. HOWEVER WE DID HAVE HUGE SPECULATOR LIQUIDATION AS THEY ARE THE ONES WHO ARE SHORT AS THE BANKERS WENT LONG AND THEN TENDERED FOR PHYSICAL. THIS WAS COUPLED WITH A) GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION). AND B) NOW THE COMMENCEMENT OF MONTH END SPREADER LIQUIDATION /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS EVEN THOUGH THEY TRANSFERRED THESE LOSSES ONTO THE FED’S BALANCE SHEET.THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS TRIED AGAIN LATE OCT 2 WITH CHINA OUT FOR A WEEK, WITH NOT MUCH LUCK. WITH CHINA COMING BACK THURSDAY OCT 9 THE CROOKS NEEDED TO RAID TRYING DESPERATELY TO HALT GOLD’S ADVANCE. I GUESS THAT THEIR LUCK HAS RUN OUT WITH GOLD INITIALLY PIERCING THE 4,000 DOLLAR BARRIER OCT 7-8 ALONG WITH THE PIERCING OF SILVER’S MAGIC 50 DOLLAR MARK. GOLD AND SILVER FROM OCT 10 ON, NEVER LOOKED BACK ONCE THEY PIERCED THEIR RESPECTIVE BARRIERS OF 4,000 DOLLAR GOLD AND 50 DOLLAR SILVER. THE CROOKS NOW NEED TO RAID ON EVERY OTHER DAY. AS OCT 21 WAS ANOTHER MASSIVE RAID ON OUR PRECIOUS METALS AND EQUITY SHARES. THEY ARE TRYING TO CONTAIN PRICING ON OUR PRECIOUS METALS , OCT 24 AND THEN OCT 28, THE LAST DAY FOR COMEX OPTIONS EXPIRY.

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN OF A TOTAL OF 10.43 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES TO BE FOLLOWED BY TODAY’S 0.4096 TONNES QUEUE JUMP FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ NEW TOTAL STANDING 197.551 TONNES.

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $15.20

WE HAD A HUGE XXXX CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 3356 CONTRACTS OR 335,600 0Z (10.43 TONNES)

speculators have left the gold arena

INITIAL GOLD COMEX

OCT CONTRACT MONTH

OCT 31

OCT CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 4 ENTRIES ii) Out of Brinks: 102,915.35 oz (3201 kilobars) ii) Out of Malca 32,890.473 oz (1023 kilobars) iii) Out of JPMorgan: 90,377.500 oz(2500 kilobars) iv) Out of Manfra 48,365 oz 15 kilobars total withdrawal 216,665.589 oz or 6.739 tonnes they are draining the comex of gold |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 3 notice(s) 300 OZ 0.00933 TONNES OF GOLD |

| No of oz to be served (notices) | 0 contracts 000 OZ 0.0000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 58,822notices 5,882,200oz 182.961 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

4 ENTRIES

ii) Out of Brinks: 102,915.35 oz (3201 kilobars)

ii) Out of Malca 32,890.473 oz (1023 kilobars)

iii) Out of JPMorgan: 90,377.500 oz(2500 kilobars)

iv) Out of Manfra 48,365 oz 15 kilobars

total withdrawal 216,665.589 oz

or 6.739 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1 dealer to customer

i) out of HSBC: 563,202.323 oz

volume at the comex: TUESDAY: 312,358oz ( VERY STRONG//

AMOUNT OF GOLD STANDING FOR OCTOBER

THE FRONT MONTH OF OCTOBER STANDS AT 13 CONTRACTS FOR A LOSS OF 179 CONTRACTS.

WE HAD 180 CONTRACTS FILED ON WEDNESDAY SO WE GAINED 1 CONTRACT QUEUE JUMP FOR 100 OZ OR 0.00311 TONNES OF GOLD, WHICH FOLLOWS ALL THE OTHER OCTOBER QUEUE JUMP OF 75.8979 TONNES

THUS OUR NEW NORMAL DELIVERY RISES TO 182.9611 TONNES WHICH INCLUDES ALL PREVIOUS QUEUE JUMPS) PLUS OUR 14.553 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD ADVANCES TO 197.5141 TONNES

NOVEMBER GAINED 225 CONTRACTS UP TO 4590 CONTRACTS.

DECEMBER LOST 3824 CONTRACTS DOWN TO 342,181 CONTRACTS.

We had 3 contracts filed for today representing 300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 3 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (58,822 oz ) to which we add the difference between the open interest for the front month of OCT ( 3 CONTRACTS) minus the number of notices served upon today (3x 100 oz per contract) equals 5,882,200 OZ OR 182.961 TONNES OF GOLD TO WHICH WE ADD OUR 6 ISSUANCES OF 14.553 TONNES OF EXCHANGE FOR RISK //NEW TOTALS STANDING FOR GOLD OCTOBER ADVANCES TO 197.5141 TONNES. NO WONDER THE COMEX IS IN TURMOIL WITH THIS MAMMOTH STANDING FOR GOLD.

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (58,822 x 100 oz +we add the difference for front month of OCT. (3 OI} minus the number of notices served upon today (3 x 100 oz) which equals 5,882,200 OZ OR 182.961 TONNES + 14.553 TONNES EXCHANGE FOR RISK//NEW TOTAL OF GOLD STANDING IN OCTOBER ADVANCES TO 197.5141 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 197.5141 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

volume WEDNESDAY confirmed 327,800 contracts huge

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,689,307.185 oz 52.54 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,243,476.833oz

TOTAL REGISTERED GOLD 19,854,809.094 or 617.567 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,388,667.789 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 18,165,502 oz ((REG GOLD- PLEDGED GOLD)= 565.023tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

OCT 31 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 6 entries i) Out of Asahi: 1,581,035.870 oz ii) Out of CNT 359,556.156 oz iii) Out of Delaware 11,102.100 oz iv) Out of HSBC 600,032,620 oz v) Out of JPMorgan 14,924.500 oz vi) Out of Stonex: 297,709.400 oz total withdrawal 2,864,360.646 oz 4th day in a row for huge silver withdrawal |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT one i) Into Manfra: 410,419.260 oz total deposit 410,419.260 oz |

| No of oz served today (contracts) | 10 CONTRACT(S) ( 0.050 MILLION OZ |

| No of oz to be served (notices) | 1 contracts (5,000 oz) |

| Total monthly oz silver served (contracts) | 7912 Contracts (39.560 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

one

i) Into Manfra: 410,419.260 oz

total deposit 410,419.260 oz

`

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

6 entries

i) Out of Asahi: 1,581,035.870 oz

ii) Out of CNT 359,556.156 oz

iii) Out of Delaware 11,102.100 oz

iv) Out of HSBC 600,032,620 oz

v) Out of JPMorgan 14,924.500 oz

vi) Out of Stonex: 297,709.400 oz

total withdrawal 2,864,360.646 oz

4th day in a row for huge silver withdrawal

adjustments: 5

5 dealer to customer

a) Asahi: 9,945.260 oz

b) Loomis 4804.820 oz

c) Manfra; 97,658.258 oz

d) Brinks 56,631.700 oz

e) CNT 196,966.380 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 163.420 MILLION OZ//.TOTAL REG + ELIGIBLE. 483.133 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 11 OPEN INTEREST CONTRACTS FOR A LOSS OF 22 CONTRACTS.

WE HAD 33 CONTRACTS SERVED ON WEDNESDAY, SO WE GAINED 11 CONTRACTS WHICH UNDERWENT A STRONG QUEUE JUMP FOR 55,000 0Z

THUS

NORMAL STANDING FOR SILVER OCT ADVANCES TO 39.565 MILLION OZ WHICH INCLUDES TODAY’S 55,000 OZ QUEUE JUMP + 2,110 MILLION OZ EX. FOR RISK = 41.675 MILLION OZ WHICH IS MASSIVE FOR A NON ACTIVE DELIVERY MONTH!!

NOVEMBER LOST 221 CONTRACTS DOWN TO 2465

DECEMBER LOST 789 CONTRACTS DOWN TO 106,724

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 or 50,000 oz

CONFIRMED volume; ON WEDNESDAY 153,852 humongous//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 7912 X5,000 oz = 39.560 MILLION oz

to which we add the difference between the open interest for the front month of OCT (11) AND the number of notices served upon today (10 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (7912) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(11) minus number of notices served upon today (10)x 5000 oz equals silver standing for the OCT.contract month equating to 39.565 MILLION OZ to which we must add our initial 2.110 million oz exchange for risk issuance//new standing advances to 41.675 which is mammoth for a non active delivery monthj.

New total standing: 41.675 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 163.420 million oz of registered silver

JPMorgan as a percentage of total silver: 205.739/483.133million. 42.64%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

OCT 31 WITH GOLD UP $XXXX TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT XXXX TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

OCT 23 WITH GOLD UP $78.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37 TONNES

OCT 22 WITH GOLD DOWN $78.95 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

GLD INVENTORY: 1036.05 TONNES, TONIGHTS TOTAL

SILVER

OCT 31 WITH SILVER UP $XXX TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT XXXX MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

OCT 23 WITH SILVER UP $0.87 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 501.474 MILLION OZ

OCT 22 WITH SILVER DOWN $0.33 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.995 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 504.015 MILLION OZ

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

CLOSING INVENTORY 488.999 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD

END

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS /245 AND 246

5. COMMODITY REPORT/silver

VBL/Chris Marcus…

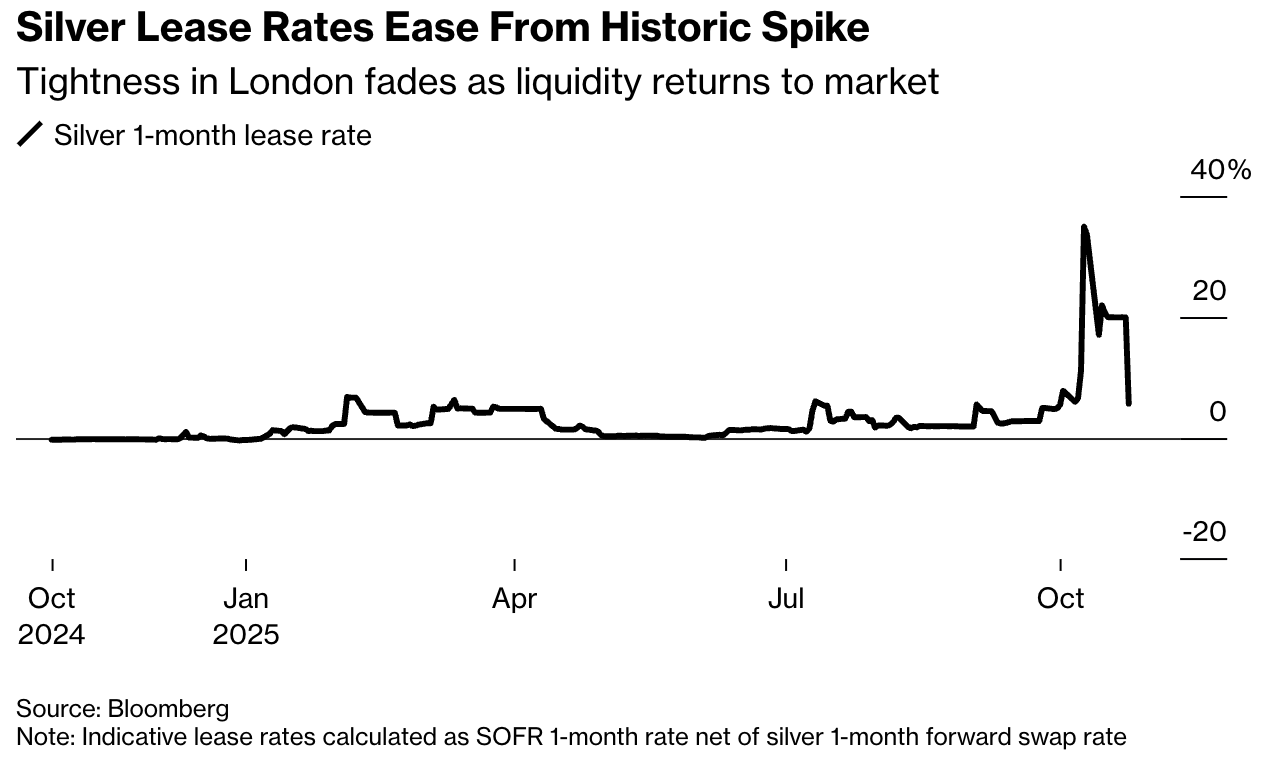

silver lease rates are now still a very high 5.6%.

No silver has arrived into India as of yet.

Silver Lease Rates Fall. But LBMA Elephant Remains

by VBL

Wednesday, Oct 29, 2025 – 13:58

Silver Price & Lease Rate Fall From Peak, But Large Elephant Remains In The Room…

Submitted by GoldFix; Authored by Chris Marcus

Earlier this week Bloomberg reported on how the pressure in the silver market has eased. And while they didn’t specifically say this, the change in the price and the silver lease rate is the result of silver leaving the Comex and China, and presumably flowing to London and/or India.

The cost of borrowing silver in London has retreated from a record high, a sign that greater liquidity has returned to the market and brought some relief from a squeeze earlier this month.

Silver lease rates – which represent the annualized cost of borrowing metal in the London market – fell to 5.6% on Monday after surging to an all-time peak of 34.9% on Oct. 9, data compiled by Bloomberg show.

I’ve been searching for any indication that silver has started to reach India and resolve their shortage, although it doesn’t appear that’s happened yet (and a Bloomberg article from a week and a half ago said that JP Morgan is telling clients that they’re not expecting any silver in India until November). But the Times of India confirms what I mentioned above about the silver shipments easing this current phase of the squeeze.

So that’s helped to resolve the London shortage, although what’s less clear is how permanent of a solution that actually is.

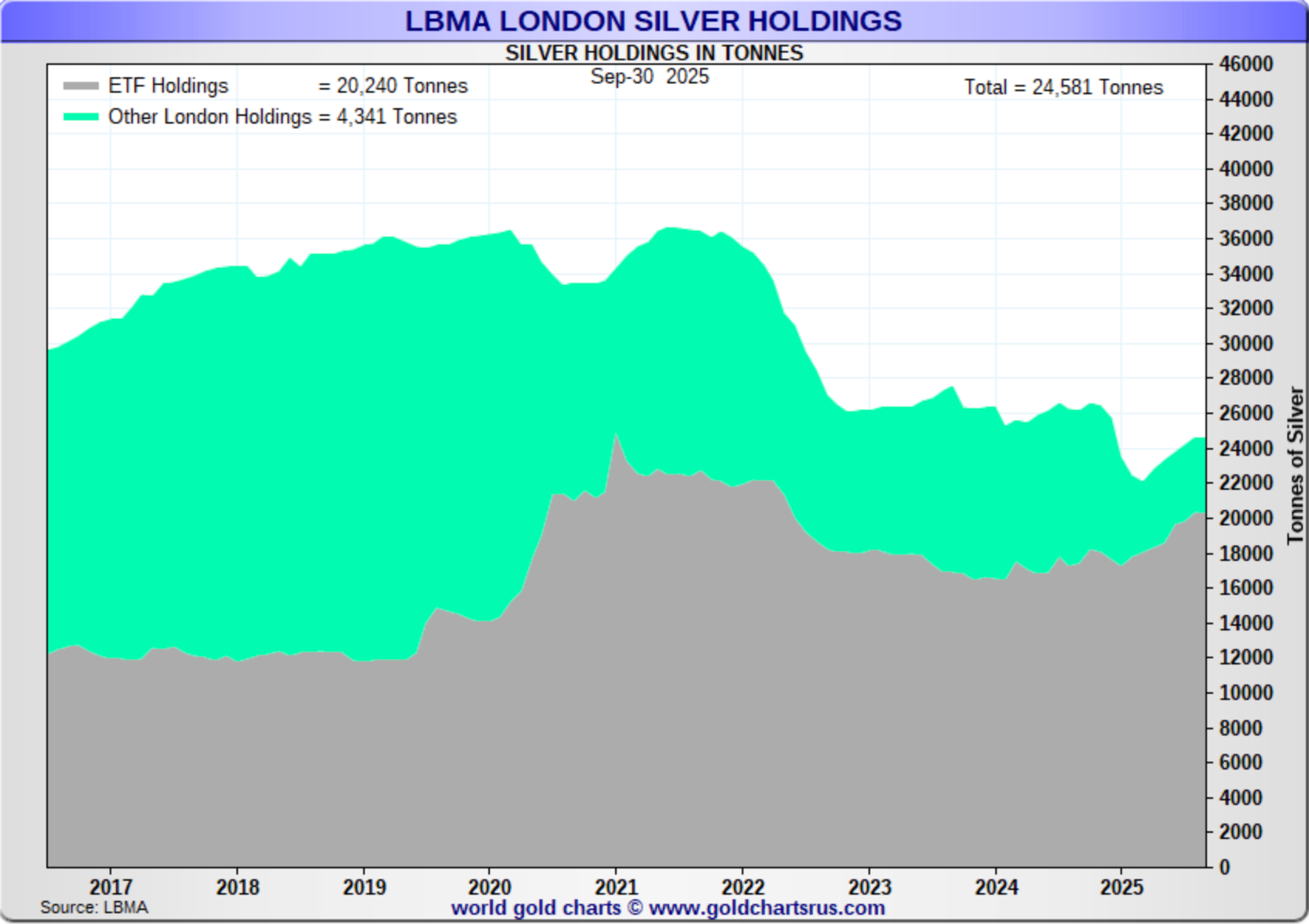

About 30 million ounces of silver have left the Comex vaults since the breakage in the market on October 9th. Although given that the average daily turnover at the LBMA is about 250 million ounces, and the free float is currently at 153 million ounces, is 30-40 million ounces going to resolve the situation, or just buy a little more time?

(the green ‘other’ is the London free float)

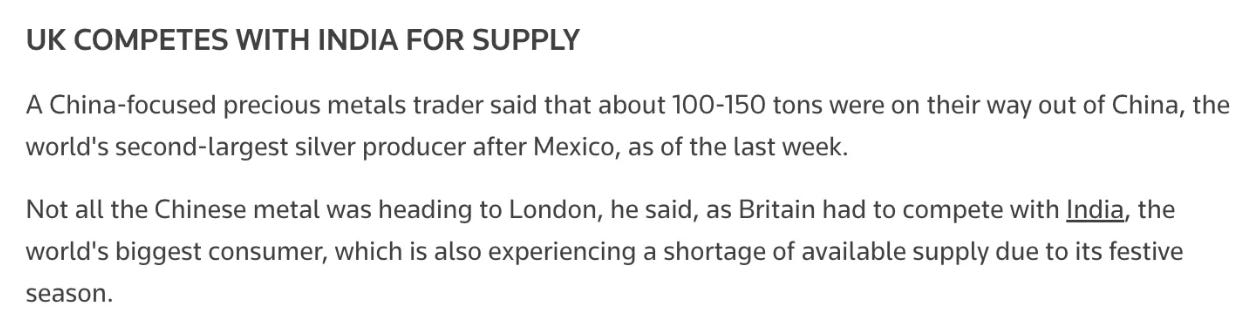

Former JP Morgan Precious Metals Managing Director Robert Gottlieb was on KITCO last week, and he said that he thinks 100-150 million ounces would be needed to normalize the silver market.

Reuters noted that 100-150 tons have come from China, which comes out to 3.2-4.8 million ounces, so that’s not exactly going to bridge the gap either.

Given how the lease rates have dropped back down, which is perhaps one of the best true indicators of how tight or fragile the London market is, it’s not surprising to see the price fall, especially given how gold was getting clobbered at the same time too.

Although for a better understanding of why it seems like the gold and silver prices will almost have to rise over the longer term, I think it would be worthwhile to watch this video about how the thinking regarding gold in Washington is likely changing as we speak.

Even despite the volatile sell-off over the past two weeks, silver is still above $48, while gold is back over $4,000. And especially on the silver side, until there’s some sort of more sustainable longer-term solution (which given the underlying dynamics is somewhat difficult to see happening), there’s a high probability that we haven’t seen the end of this yet.

Sincerely,

Chris Marcus

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED DOWN 29.43 POINTS OR 0.73%

//Hang Seng CLOSED CLOSED DOWN 63.45 PTS OR 0.24%

// Nikkei CLOSED : UP 17.96 PTS OR 0.04% //Australia’s all ordinaries CLOSED DOWN 0.43%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1092// OFFSHORE CLOSED DOWN AT 7.1083/ Oil UP TO 60.04 dollars per barrel for WTI and BRENT UP TO 64.43 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING DOWN TO 7.1092 // OFFSHORE YUAN TRADING DOWN TO 7.1083 :/ONSHORE YUAN TRADING BELOW AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1092

OFFSHORE YUAN: DOWN TO 7.1083

HANG SENG CLOSED DOWN 63.45 PTS OR 0.24%

2. Nikkei closed UP 17.96 PTS OR 0.04%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX DOWN TO 98.94 EURO FALLS TO 1.1623 DOWN 21 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.6490//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 153.70…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.041 DOWN 1 FULL BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6439// Italian 10 Yr bond yield UP to 3.415 SPAIN 10 YR BOND YIELD UP TO 3.161

3i Greek 10 year bond yield UP TO 3.2990

3j Gold at $4005.20Silver at: 48.22 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 42 /100 roubles/dollar; ROUBLE AT 80.46

3m oil (WTI) into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 153.70/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.649% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.041 DOWN 1 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7984 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9279 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.071 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.627 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.592 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.99 UP 4 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.4310 UP 4 PTS

30 YR UK BOND YIELD: 5.193 UP 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.158 UP 12 BASIS PTS

5 YR CANADA BOND YIELD: 2.744 UP 12 BASIS PTS.

a New York OPENING REPORT

Futures Drop As Trump-Xi Summit Underwhelms; Mag 7 Earnings Disappoint

Thursday, Oct 30, 2025 – 08:36 AM

US equity futures drop as the Trump-Xi trade truce was in line with expectations and hasn’t provided impetus for stocks to move another leg higher, after Fed Chair Powell’s pushback on another rate cut in December being a lock, while Mag7 stocks are under pressure (META -7.8%, MSFT -3.2%) as we await AAPL and AMZN tonight. As of 8:00am ET, S&P futures are down 0.2% with another wave of results due and nearly half of S&P 500 companies now having reported. Pre-market we are seeing Defensives over Cyclicals, with the exception of Metals / Miners. Gold / Silver continue their rebound as Ags and Energy are lower. Bond yields are trading near session highs, up 2bps to 4.10%, while the USD is near session highs. Besides the trade deal with China, US / Canada resumed talks and US / Mexico extended their trade truce an additional 90 days, earlier this week. The US economic calendar remains blank as government shutdown delays publication of weekly jobless claims data and 3Q GDP estimate. Fed speaker slate includes Bowman (9:55am) and Logan (1:15pm). Besides Amazon and Apple reporting after the close, the non-Mag7 earnings focus is mostly on healthcare. Ex-US, the ECB rate decision comes at 9.15a EST.

In premarket trading, Mag 7 stocks mixed: Alphabet (GOOGL) gained 7% on Q3 results that beat expectations. Analysts are especially positive on its cloud-computing business. Meta Platforms (META) sank 8% after the Facebook parent reported third-quarter results and gave an outlook. Analysts noted some concern over the company’s heavy spending. Microsoft (MSFT) was down 2% after the software company reported its first-quarter results. Analysts are broadly positive on the report, especially growth in its Azure cloud-computing business, but said investor expectations were elevated (Apple (AAPL) +0.7%, Nvidia (NVDA) is flat, Tesla (TSLA) -0.5%, Amazon (AMZN) -0.5%)

- Calix (CALX) rises 8% after the application software company reported third-quarter results that beat expectations and gave an outlook that is above the analyst consensus.

- Carvana (CVNA) falls 7% after the used-car retailer failed to live up to “elevated buy-side bar.” The company said its loan performance was solid amid rising concerns about delinquencies and distress in subprime auto lending.

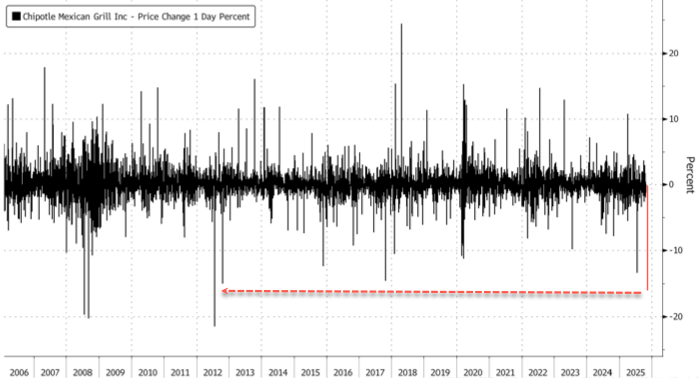

- Chipotle (CMG) falls 17% after the restaurant chain lowered its full-year projection for comparable sales for a third time this year as customer traffic at its restaurants fell.

- Eli Lilly & Co. (LLY) gains 4% after raising its full-year guidance as revenue from its blockbuster weight loss and diabetes drugs beat analysts’ estimates in the third quarter.

- FMC Corp (FMC) sinks 29% after the agricultural chemical company reported worse-than-expected revenues and cut its guidance for the full year below analyst estimates.

- FormFactor (FORM) rises 14% after the semiconductor manufacturing company reported third-quarter results that beat expectations and gave an outlook that is seen as strong, prompting an upgrade.

- Guardant Health (GH) rallies 26% after the biotech company boosted its revenue guidance for the full year, beating the average analyst estimate.

- Huntington Ingalls (HII) rises 3% after the military shipbuilder reported revenue for the third quarter that beat the average analyst estimate.

- Insmed (INSM) climbs 12% after the biotech firm posted quarterly results.

- MediaAlpha (MAX) climbs 11% after the insurance technology company reported its third-quarter results and gave an outlook that analysts are positive on.

- REV Group (REVG) rises 6% after Terex agreed to buy the manufacturer of specialty vehicles.

- Sprouts Farmers Market (SFM) tumbles 23% after the grocery store chain reported comparable store sales that missed estimates and lowered its forecast for full-year comp sales.

- TransMedics (TMDX) drops 10% after the transplant-therapy company reported total revenue for the third quarter that fell short of the average analyst estimate.

In corporate news, AI startup OpenAI may target a $1 trillion valuation in an IPO as soon as next year, Reuters reported citing unidentified sources. Calpers is is planning to vote against Elon Musk’s $1 trillion Tesla compensation agreement.

On Wednesday, the Fed delivered its second straight rate reduction to support a softening labor market and said they would stop shrinking the portfolio of assets from December. Still, Chair Jerome Powell cautioned that another cut this year wasn’t a foregone conclusion, prompting money markets to pare the odds of a quarter-point move to about 60% from near certainty. The European Central Bank is due to announce its policy decision later Thursday.

“After a month of strong growth across global equity markets, I think it’s quite healthy, frankly, to take a breather,” said David Kruk, head of trading at La Financiere de l’Echiquier. “The path of the Fed — with Powell’s surprise hawkish tilt yesterday — is a big question, as is the extent of capex announced by the Mag 7.”

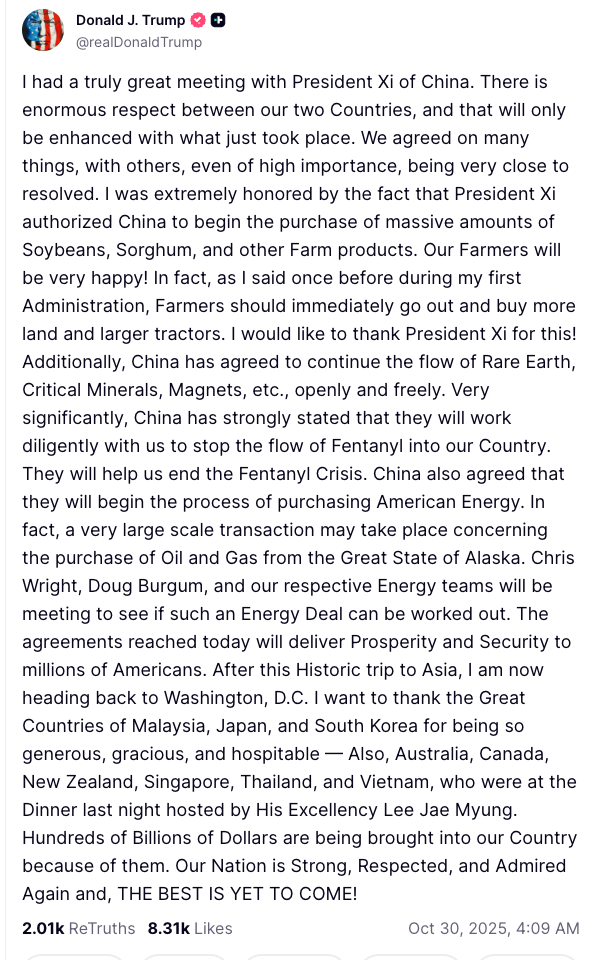

Trump and Xi agreed to extend a tariff truce, roll back export controls and reduce other trade barriers in the first sitdown between leaders since Trump’s return to the White House. Despite speculation over potential additional concessions, including opening access to Nvidia’s Blackwell chips, the President indicated such issues hadn’t been part of the discussions.

Mag 7 sentiment was muted with META and MSFT both under pressure; reaction to releases from tech giants was mixed as investors sought evidence that huge outlays are paying off. Alphabet demonstrated that its spending is fueling growth across Google’s businesses, particularly in cloud computing and search advertising, and said capex for the year will be $91 to $93 billion. Meta said capex in 2026 will be “notably larger” than in 2025, when it expects to spend as much as $72 billion, while Microsoft’s CFO reiterated the company can’t meet current demand for AI and other services, even after spending tens of billions in recent quarters. The three bellwethers together spent $78 billion in capex last quarter, up 89% from a year earlier.

Taking a broader look at Q3 earnings, out of the 248 S&P 500 companies that have reported so far in the earnings season, 81% have managed to beat analyst forecasts, while 15% have missed. Advance Auto Parts, Biogen, Bristol-Myers, Cigna, Comcast, Estee Lauder, Hershey, Eli Lilly, Mastercard, Altria, Merck, Roblox and S&P Global are among companies expected to report results before the market opens. Lilly’s ability to meaningful increase guidance at 3Q results may hinge on the effect of the partial loss of CVS-Caremark formulary coverage for Zepbound that started in July, according to BI.

“There has been a lot of good news priced in,” Nancy Curtin, global chief investment officer at Alti Tiedemann Global, told Bloomberg TV. “Having said that, we are still in the midst of the third-quarter earnings. If we end up again with 12-13% earnings growth in this quarter, with expectations on the rise for next quarter – that helps sustain markets.”

Carmakers around the world are planning to scale back production after an export freeze on Chinese semiconductor company Nexperia threatened to disrupt the industry’s supply chains, with Volkswagen the latest to caution that its outlook depends on sufficient supply of chips.

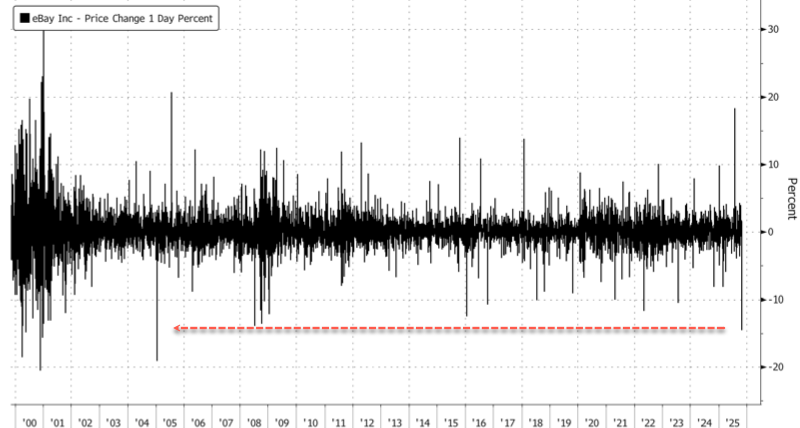

Consumer trends are in focus with Chipotle lowering projections for a third time this year as customer traffic fell, while eBay gave a weak profit outlook for the holiday period. In Europe, Carlsberg sees lower beer sales on weaker consumer demand and Remy Cointreau cut its outlook amid subdued demand across markets including China, Europe and the US.

European stocks fell as investors responded to a busy roster of earnings and looked ahead to an interest-rate decision by the European Central Bank. Drinkmaker Campari leads gains on the Stoxx 600 after a strong report, while at the other end of the index, weaker results hurt the shares of Norwegian defense group Kongsberg and advertising agency WPP. Stoxx 600 falls 0.3% to 573.49 with 374 members down, 216 up, and 10 unchanged. Here are the biggest movers Thursday:

- Campari jumps as much as 9.6% and was the best performing stock on the Stoxx 600 after the Italian spirits group announced surprising progress in terms of profitability despite disappointing sales for its Aperol brand

- Jeromino Martins jumps as much as 8.1% after retailer reported higher-than-expected profitability in 3Q. For analysts it shows that the company was able to mitigate slowing like-for-like sales in Poland by higher cost discipline

- Lufthansa shares rise as much as 5.4%, the most since June 24. The German flag carrier reiterated its expectation for a significant increase in full-year adjusted Ebit and reported a slight profit beat in the third quarter

- Raiffeisen shares rise as much as 5.9% after the Austrian lender delivers consensus-beating third-quarter results; KBW sees a good set of results supported by another quarter of benign asset quality

- Airbus gains as much as 2.7%, setting a new record high, after the airplane and military equipment manufacturer reports third-quarter adjusted Ebit that beat consensus expectations

- ING Groep shares rise as much as 3.3%, the most in four months, as the Amsterdam-headquartered bank’s third-quarter profits come in ahead of forecasts, largely driven by higher revenues

- Ayvens gains as much as 11%, the most since May 2024, as analysts welcomed the car leasing company’s third-quarter results, which included a share buyback and a special dividend

- Kongsberg shares drop as much as 15%, the most since May 2022, after the military technology company reported Ebitda for the third quarter that missed the average analyst estimate

- Stellantis falls as much as 6.4% as analysts focus on the potential one-off charges in the second half of the year and what they could mean for cash flow. JPMorgan notes that the carmaker’s pricing failed to fully offset FX impact

- Prysmian falls as much as 8% after the cables manufacturer’s guidance disappointed investors; JPMorgan says the extend of the upgrade is likely to disappoint the market going forward

- Credit Agricole falls as much as 3.4% as a miss on costs saw pre-provision operating profit come in broadly in-line with expectations despite a small beat on revenue

- Schneider Electric falls as much as 5% on solid albeit merely in-line third-quarter report, according to analysts, with JPMorgan flagging buy-side expectations may have been more elevated leading into the report

- WPP shares slump as much as 13% to the lowest since 2008, after the advertising agency reduced organic growth guidance that was already slashed in July. Its 3Q revenue drop was also more severe than analysts had expected

- Amplifon drops as much as 6.4%, the most since July 30, after trimming its full-year sales growth guidance, while maintaining its adjusted Ebitda margin goal. JPMorgan says 3Q results fell short of expectations

- Carlsberg shares slip after the brewer reported third-quarter results in line with low expectations, with consumer weakness in markets including China and Ukraine weighing on volumes

Earlier in the session, Asian stocks turned lower after Donald Trump and Xi Jinping concluded a meeting that was seen as easing tensions between the world’s two largest economies but may have been largely priced into assets. The MSCI Asia Pacific Index fell 0.4%, reversing an early advance of as much as 0.5%. Softbank and Wesfarmers were among key drags. South Korean stocks gained after the nation sealed a trade deal with the US and Samsung Electronics posted a big bump in profits from its chip business. Details on further aspects of the agreement will be key for the Asian stock rally, with the regional benchmark on course for its seventh straight monthly gain. Stocks rose in Japan after the central bank held interest rates. Shares fell in Australia, India, Vietnam and the Philippines.

In FX, the Bloomberg Dollar Spot Index edges higher. The yen weakened below 154 per dollar after the Bank of Japan left its benchmark interest rate unchanged and offered no new hints on when it might hike.

In rates, treasuries are lower with most yields about 1-2bps higher vs Wednesday’s closing levels. US 10-year near 4.09% slightly exceeds Wednesday’s high, adding to losses that lifted tenors other than the 30-year at least 10bp; German and UK yields are cheaper by 2bp to 4bp across curves. Fed-dated OIS also hover around Wednesday’s closing levels, pricing in around 15bp of easing for the December rate decision. German 2-year topped 2% for the first time in three weeks ahead of the ECB monetary-policy decision at 9:15am New York time. European yields are higher across the curve. French GDP comfortably topped estimates, German output stagnated. Focal points of US session include speeches by Fed’s Bowman and Logan. S&P 500 are down slightly amid evaluation of US-China trade truce.

In commodities, gold prices rising and testing $4,000/oz, oil slipping with WTI sitting around $60/barrel and Brent short of $65/barrel.

Looking ahead, the US economic calendar remains effectively blank as government shutdown delays publication of weekly jobless claims data and 3Q GDP estimate. Fed speaker slate includes Bowman (9:55am) and Logan (1:15pm)

Market Snapshot

- S&P 500 mini -0.1%

- Nasdaq 100 mini little changed

- Russell 2000 mini +0.2%

- Stoxx Europe 600 -0.3%

- DAX little changed

- CAC 40 -0.4%

- 10-year Treasury yield -1 basis point at 4.07%

- VIX -0.9 points at 16.05

- Bloomberg Dollar Index little changed at 1214.55

- euro +0.2% at $1.1624

- WTI crude -0.5% at $60.15/barrel

Top Overnight News

- Donald Trump hailed an “amazing meeting” with Xi Jinping that resulted in them extending a tariff truce for another year, rolling back export controls and reducing other trade barriers. Beijing agreed to pause controls on rare-earth magnets and, as Trump put it, buy “tremendous” amounts of American soybeans. The leaders didn’t discuss approving sales of NVDA’s Blackwell chips to China. BBG

- The Senate votes 50-46 to block Trump’s tariffs on Canada (this action, the second in as many days after the Senate voted to remove Trump’s Brazil tariffs, is most likely symbolic since it likely will not pass in the house). WaPo