access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

GOLD: NUMBER OF NOTICES FILED FOR NOV/2025: 4755 CONTRACTs NOTICES FOR 475,500 OZ or 14.790 TONNES

total notices so far: 4755 contracts for 475,500 OR 9.970 tonnes)

SILVER NOTICES: 1994 NOTICE(S) FILED FOR 9.940 MILLION OZ/

total number of notices filed so far this month : 1994 CONTRACTS (NOTICES) for 9.970 million oz

INITIAL STANDING FOR NOV: 11.575 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

AND NOW NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ.

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1092 CONTRACTS OI TO 159,144 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 100 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1092 CONTRACTS AND ADD TO THE 100 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1192 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE GAIN OF $0.95 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 5.960 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.95

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 32.11 POINTS OR 0.81%

//Hang Seng CLOSED CLOSED DOWN 376.04 PTS OR 1.43%

// Nikkei CLOSED : UP 1085.73 PTS OR 2.12% //Australia’s all ordinaries CLOSED DOWN 0.01%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1131// OFFSHORE CLOSED DOWN AT 7.1169/ Oil UP TO 60.24 dollars per barrel for WTI and BRENT UP TO 64.06 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING DOWN TO 7.1131 // OFFSHORE YUAN TRADING DOWN TO 7.1169 :/ONSHORE YUAN TRADING ABOVE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY SMALL 155 CONTRACTS TO 456,333 OI WITH OUR GAIN IN PRICE OF $15.20 WITH RESPECT TO THURSDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2074). WE HAD LITTLE T.A.S. LIQUIDATION THURSDAY. HOWEVER AGAIN, IT WAS THE MAJOR SPECULATORS THAT WENT SHORT AGAIN AND THE BANKERS WHO TOOK THE LONG SIDE AS THE SHORTS WERE LED BY THE NOSE BY THE BANKERS. THEN MUCH TO THH SPECS HORROR, THE BANKERS TENDERED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD. THAT IS WHAT PROPELLED THE GOLD PRICE HIGHER DESPITE OPTIONS EXPIRY //LONDON OTC CONTRACTS.

WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 2230 CONTRACTS (OR 6.936 TONNES).THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

EXCHANGE FOR PHYSICAL//GOLD ISSUANCE//OCTOBER:

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT FOR GOLD REMAINS AT 14.553 TONNES OF GOLD UNDER THE GUIDANCE OF 6 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FINAL

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 127.5 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 130.3 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW NOVEMBER COMEX MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 2230 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR SIZED T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1419 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN ON LAST FRIDAY’S AND TUESDAY’S HUGE RAIDS, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS WE WE WILL PROBABLY SEE GOLD//SILVER RISE HUGELY ON OUR UPCOMING DAYS.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS:

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE FINISHING OPTION EXPIRY WEEK, THE CROOKS GOADED OUR SPECULATORS TO CONTINUE ONTO THE SHORT SIDE WITH THE BANKERS ON THE LONG SIDE…THE RAIDS THROUGHT THIS WEEK WERE FREQUENT BUT FAILED TO CAUSE ANY DAMAGE TO THE PRICE WITH OPTIONS EXPIRY FINISHING TODAY.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT:

F) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

G) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

H) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

I) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

J) A MASSIVE QUEUE JUMP OCT 9 FOR 4.979 TONNES

K) A MASSIVE AND 3RD HIGHEST EVER OCT 10 QUEUE JUMP FOR 7.504 TONNES

L) A MASSIVE QUEUE JUMP OF 4.3919 TONNES

M) A RECORD SETTING QUEUE JUMP OF 9.564 TONNES

N) A HUGE 6.469 TONNES QUEUE JUMP

0) A HUGE 8.326 TONNES QUEUE JUMP

P) A RECORD SETTING 12.031 TONNE QUEUE JUMP THE HIGHEST EVER RECORDED IN COMEX HISTORY SURPASSING TUESDAY’S 9.564 TONNES

Q/ QUEUE JUMP OF 7.695 TONES OF GOLD//

R/ TODAY’S QUEUE JUMP OF 3.8600 TONNE JUMP

S) OCT 22 QUEUE JUMP OF 8.622 TONNES//

T) 1OCT 23 1.695 TONNES

U) OCT 24. 0.8615 TONNES

V) OCT 27 0.3048 TONNE QUEUE JUMP

W) OCT 28 QUEUE JUMP OF .5069

X) OCT 29 QUEUE JUMP OF .4096 TONNES

Y) OCT 30 QUEUE JUMP OF 0.00311 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

AND NOW NOVEMBER:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503200 OZ (15.651 TONNES)

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 248 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING E.G. NOVEMBER: A HUGE 15.651 TONNES STANDING IN AN OFF MONTH!! THIS IS HUGE!!!

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH SEPT. AND SUBSEQUENT STANDING FOR GOLD.

AUGUST:

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPT:

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES WHICH INCLUDES ALL QUEUE JUMPING.

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 4300 CONTRACTS.

THAT IS A STRONG SIZED 4300 EFP CONTRACT WAS ISSUED: : /DEC 4300 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4300 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON!

WE HAD :

- SOME LIQUIDATION OF OUR T.A.S. SPREADERS//THURSDAY + GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE SEPT 30 WITH OUR ATTEMPTED FAILED RAID, FOLLOWED BY ANOTHER RAID OCT 2 AND THAT ENDED IN TOTAL FAILURE! , OCT 7 WE WITNESSED A SMALL RAID TRYING TO STOP GOLD’S ADVANCE TO THE 4000 BARRIER!! EARLY Y\OCT 8 MORNING THE BARRIER TO 4,000 DOLLAR GOLD WAS PIERCED!! AND THAT SET IN MOTION OUR CROOKS DESPERATE TO CONTROL THEIR HUGE DERIVATIVE LOSSES. (OCT 9 SAW FINALLY AFTER MANY YEARS SILVER PIERCING THE 50 DOLLAR MARK AND THAT WAS WHEN THE CROOKS THREW ANOTHER TEMPER TANTRUM WHEN GOLD FINALLY BROKE THROUGH 4,000 DOLLAR MARK ON OCT. 10 AND GOLD NEVER LOOKED BACK DESPITE OUR TWO RAIDS THIS PAST WEEK, ON OPTIONS EXPIRY WEEK

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A FAIR SIZED SIZED 1419 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING STRONG GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

AND NOW NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING NOVEMBER,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $15.20/ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A VERY FAIR GAIN IN OI FROM TWO EXCHANGES OF 2230 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION THURSDAY. HOWEVER WE DID HAVE AGAIN HUGE SPECULATOR LIQUIDATION AS THEY ARE THE ONES WHO ARE SHORT AS THE BANKERS WENT LONG AND THEN TENDERED FOR PHYSICAL. THIS WAS COUPLED WITH A) GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION). AND B) NOW THE FINALIZATION OF MONTH END SPREADER LIQUIDATION /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS EVEN THOUGH THEY TRANSFERRED THESE LOSSES ONTO THE FED’S BALANCE SHEET.THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS TRIED AGAIN LATE OCT 2 WITH CHINA OUT FOR A WEEK, WITH NOT MUCH LUCK. WITH CHINA COMING BACK THURSDAY OCT 9 THE CROOKS NEEDED TO RAID TRYING DESPERATELY TO HALT GOLD’S ADVANCE. I GUESS THAT THEIR LUCK HAS RUN OUT WITH GOLD INITIALLY PIERCING THE 4,000 DOLLAR BARRIER OCT 7-8 ALONG WITH THE PIERCING OF SILVER’S MAGIC 50 DOLLAR MARK. GOLD AND SILVER FROM OCT 10 ON, NEVER LOOKED BACK ONCE THEY PIERCED THEIR RESPECTIVE BARRIERS OF 4,000 DOLLAR GOLD AND 50 DOLLAR SILVER. THE CROOKS NOW NEED TO RAID ON EVERY OTHER DAY. BEGINNING OON OCT 21 THROUGHT THESE PAST 10 DAYS.. THEY ARE DESPERATELY TRYING TO CONTAIN PRICING ON OUR PRECIOUS METALS WITH MUCH FAILURE AS GOLD HAS REGAINED THE 4000 DOLLAR MANTLE AND SILVER BROKE INTO THE 49 DOLLAR BRACKET READY TO TAKE ON THE 50 DOLLAR BARRIER.

FRIDAY MORNING//THURSDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/ FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ NEW TOTAL STANDING 197.551 TONNE/OCTOBER FINAL

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY!

ALL OF THIS HUGE FINAL STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $15.20

WE HAD A HUGE 12,685 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

INITIAL GOLD COMEX

OCT CONTRACT MONTH

OCT 31

NOV CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 3 ENTRIES ii) Out of Brinks: 32,151.000 oz (1000 kilobars) ii) Out of Loomis 4919.103 oz (153 kilobars) iv) Out of Manfra 38,359.983 total withdrawal 75,420.056 oz or 2.348 tonnes they are draining the comex of gold |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 4755 notice(s) 475,500 OZ 14.790 TONNES OF GOLD |

| No of oz to be served (notices) | 277 contracts 27,700 OZ 0.8615 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4755notices 475,500oz 14.790 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

3 ENTRIES

ii) Out of Brinks: 32,151.000 oz (1000 kilobars)

ii) Out of Loomis 4919.103 oz (153 kilobars)

iv) Out of Manfra 38,359.983

total withdrawal 75,420.056 oz

or 2.348 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 2 dealer to customer

i) out of Asahia 600.514 oz

ii)Out of JPMorgan: 482.265 oz

volume at the comex: THURSDAY: 269,052oz ( fair)//

AMOUNT OF GOLD STANDING FOR NOVEMBER:

THE FRONT MONTH OF NOV STANDS AT 5032 CONTRACTS FOR A GAIN OF 442 CONTRACTS. THUS BY DEFINITION, THE INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF NOVEMBER IS AS FOLLOWS:

5032 NOTICES X 100 OZ PER NOTICE

EQUALS

503,200 OZ OR 15.651 TONNES OF GOLD

DECEMBER LOST 3526 CONTRACTS DOWN TO 334,944 CONTRACTS.

JANUARY GAINED 44 CONTRACTS UP TO 812

We had 4755 contracts filed for today representing 475,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 2193 notices issued from their client or customer account. The total of all issuance by all participants equate to contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 1406 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2025. contract month, we take the total number of notices filed so far for the month (4755 oz ) to which we add the difference between the open interest for the front month of NOV ( 5032 CONTRACTS) minus the number of notices served upon today (4755x 100 oz per contract) equals 503,200 OZ OR 15.651 TONNES OF GOLD

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (4755 x 100 oz +we add the difference for front month of OCT. (5032 OI} minus the number of notices served upon today (4755 x 100 oz) which equals 503,200 OZ OR 15.651 TONNES

TOTAL COMEX GOLD STANDING FOR NOV..: 15.651 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE ACTIVE DELIVERY MONTH OF NOVEMBER

volume THURSDAY confirmed 327,800 contracts huge

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,678,509.010 oz 52.20 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,168,046.747oz

TOTAL REGISTERED GOLD 19,853,726.263 or 617.53 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,314,320.482 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 18,175,217 oz ((REG GOLD- PLEDGED GOLD)= 565.325tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE NOV. 2025 SILVER CONTRACTS

OCT 31 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) Out of Asahi: 1,118,890.550 oz ii) Out of Delaware 162,169.865 oz iii) Out of Stonex: 754,542.770 oz total withdrawal 2,035,603.185 oz 5th day in a row for huge silver withdrawal |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT two entries i) Into CNT 9,886.700 oz ii) Into Manfra 1,331,090.060 oz total deposit 1,340,946.760 oz |

| No of oz served today (contracts) | 1994 CONTRACT(S) ( 9.970 MILLION OZ |

| No of oz to be served (notices) | 325 contracts (1.625 oz) |

| Total monthly oz silver served (contracts) | 1994 Contracts (9.970 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

two entries

i) Into CNT 9,886.700 oz

ii) Into Manfra 1,331,090.060 oz

total deposit 1,340,946.760 oz

`

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 entries

i) Out of Asahi: 1,118,890.550 oz

ii) Out of Delaware 162,169.865 oz

iii) Out of Stonex: 754,542.770 oz

total withdrawal 2,035,603.185 oz

5th day in a row for huge silver withdrawal

adjustments: 4

3 dealer to customer

a) Asahi: 34,865.600 oz

b) Loomis 34,236.070 oz

c) Manfra; 49,317.970 oz

one adjustment customer to dealer

d) CNT 901,832.502.20 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 164.203 MILLION OZ//.TOTAL REG + ELIGIBLE. 482.438 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF NOVEMBER /2025 OI: 2315 OPEN INTEREST CONTRACTS FOR A LOSS OF 150 CONTRACTS.

THUS

INITIAL STANDING FOR SILVER AT THE COMEX IS AS FOLLOWS

2315 CONTRACTS X 5000 OZ PER CONTRACT

EQUALS

11.575 MILLION OZ WHICH IS HUGE FOR A NOVEMBER

DECEMBER GAINED 227 CONTRACTS UP TO 106,951

JANUARY GAINED 4 CONTRACTS UP TO 763 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 or 50,000 oz

CONFIRMED volume; ON THURSDAY 68,613 good//

AND NOW NOVEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 1994 X5,000 oz = 9.970 MILLION oz

to which we add the difference between the open interest for the front month of NOV (2315) AND the number of notices served upon today (1994 )x (5000 oz)

Thus the standings for silver for the NOVEMBER 2025 contract month: (1994) Notices served so far) x 5000 oz + OI for the front month of NOV(2315) minus number of notices served upon today (1994)x 5000 oz equals silver standing for the NOV.contract month equating to 11.575 MILLION OZ

New total standing: 11.575 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 164.203 million oz of registered silver

JPMorgan as a percentage of total silver: 205.724/482.438million. 42.57%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

OCT 31 WITH GOLD DOWN $17.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1040.35 TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

OCT 23 WITH GOLD UP $78.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37 TONNES

OCT 22 WITH GOLD DOWN $78.95 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

GLD INVENTORY: 1040.35 TONNES, TONIGHTS TOTAL

SILVER

OCT 31 WITH SILVER DOWN $0.35 TODAY/SMALL CHANGES IN SILVER AT THE SLV: ///A WITHDRAWAL OF 636,000 OZ FROM THE SLV// ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

OCT 23 WITH SILVER UP $0.87 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 501.474 MILLION OZ

OCT 22 WITH SILVER DOWN $0.33 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.995 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 504.015 MILLION OZ

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

CLOSING INVENTORY 488.363 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD

Game on!

Despite recent weakness in gold and silver, the early indications are that the current consolidation phase is unlikely to last long before prices resume their uptrend.

| Alasdair MacleodOct 31∙Paid |

It may be too early to conclude that after the shakeout of the last two weeks we have seen the bottom in gold and silver prices. But current physical liquidity constraints and the reasons for buying gold and silver have not gone away, suggesting that prices are being set up for another run higher.

Gold and silver steadied this week after retreating from all-time highs the previous week. In London trading this morning gold was $4010 after a low of $3887 on Tuesday, to close a net $100 lower from last Friday’s close. Silver was more resilient at $48.80 after a low of $45.60, for a net gain of 20 cents.

Referring to relative strength indicators, technical analysts told us that gold and silver had become massively overbought, so have formed a major top. If that was the case, then it would be reflected in open interest on Comex at all-time highs, because overbought conditions by definition exist when speculation becomes excessive. But that is not the case as the next charts for gold and silver clearly show:

At 456,000 contracts gold’s open interest indicates relatively subdued speculator interest. In silver’s case, there was minimal speculator buying when the price soared from $30 to $50+. The market evidence therefore negates the mechanical relative strength evidence pointing to a massive liquidity squeeze driving prices instead.

Traders are being whipsawed, again.

This week sees the end of November contracts and options — a time when the swaps like to shake out weak holders. Next week when it’s over, we can expect to see stand for deliveries accelerate, and liquidity issues in London coming to the fore. Silver is still in backwardation, but the condition has reduced to a just a few cents. Nevertheless, it indicates the liquidity squeeze is still on. It is less obvious in gold which remains in contango.

While the bullion banks are having difficulty in silver, they appear to be more balanced in gold, perhaps with paper longs in London balancing shorts in Comex futures. They will be aware of central bank demand, and crucially aware of central banks’ reluctant to renew lease contracts after the fiasco at the Bank of England earlier this year.

Readers will also be amused to know that security staff guarding the vaults at the Bank are threatening to strike for more pay.

Yesterday, the World Gold Council released its gold demand estimates for Q3, noting that it increased by 3% measured by tonnage driven by investment demand, despite higher prices. This is reflected in buying of ETFs, shown by the WGC’s chart:

The surge in September with no region being net sellers is consistent with investment funds and individuals awakening to an asset class to which they are underexposed.

Now is time for us to indulge in a little price speculation.

The recent selloff in gold is almost certainly being met with sighs of relief from fund managers fielding questions from their clients about why they haven’t invested in gold and gold mines despite gold outperforming all other asset classes. Almost certainly, they will be telling them (wrongly) that gold’s current performance shows the dangers of chasing a speculative bubble.

If it turns out that the selloff of the last two weeks ends up supporting yet higher prices as the supply squeeze continues, fund managers will be forced to reconsider their scepticism and scramble to buy before prices embarrass them again. The lack of available bullion could then push prices far higher.

The Fed’s interest rate policy

On Wednesday, the Fed reduced its funds rate by ¼% to 3 ¾% as widely expected. But Jay Powell cautioned that a further cut by the year-end was not a slam-dunk, causing bond yields to tick higher. But despite Powells reticence it is clear that the inflation target is being abandoned in favour of preventing recession and is a clear signal for dollar weakness and gold’s strength.

late in the day:

BIS gold swaps rose 24 tonnes in September but trend remains sharply down

Submitted by admin on Fri, 2025-10-31 13:51 Section: Daily Dispatches

1p CT Friday, October 31, 2025

Dear Friend of GATA and Gold:

Gold swaps undertaken by the Bank for International Settlements, a major gold broker for central banks, increased 24 tonnes in September, from 30 tonnes to 54, GATA’s consultant on the bank, Robert Lambourne, reports.

Lambourne calculated the BIS’ swaps volume from the bank’s September statement of account, which was published today:

His calculation presumes that the bank did not sell any of its own 102 tonnes of gold, for which there are no indication

The BIS refuses to explain its gold swaps — why they are undertaken and for whom. But since the bank is an organization consisting exclusively of central banks, the swaps must involve BIS members.

According to the BIS, its mission is to “support central banks’ pursuit of monetary and financial stability through international cooperation, and to act as a bank for central banks”:

In 2005 the head of the BIS’ monetary and economic department, William R. White, gave a powerful hint about the purpose of the bank’s gold swaps. White explained at a conference at BIS headquarters in Basel, Switzerland, where he may have assumed that only fellow central bankers were listening, that a primary purpose of this “international cooperation” is “the provision of international credits and joint efforts to influence asset prices (especially gold and foreign exchange) in circumstances where this might be thought useful”:

Translated from Obscurantic, the language of central bankers when they speak in public, this means that monetary and financial stability throughout the world requires rigging the gold market, gold being money far superior to government money. Hence the gold swaps, which allow gold to be applied where needed by central banks to prevent a free market from breaking out in the monetary metal and bringing some discipline to government currencies.

That’s an older part of the gold story that can’t be told by mainstream financial news organizations and market analysts.

The newer part is that Lambourne’s calculations show that BIS gold swaps, which stood at 552 tonnes in 2021, have declined 90% since then.

This indicates a profound change of gold policy among most BIS members, apparently their defection from price suppression efforts in subservience to the U.S. dollar, to their acquisition of gold and recovery of leased and swapped gold in pursuit of national monetary and economic sovereignty.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

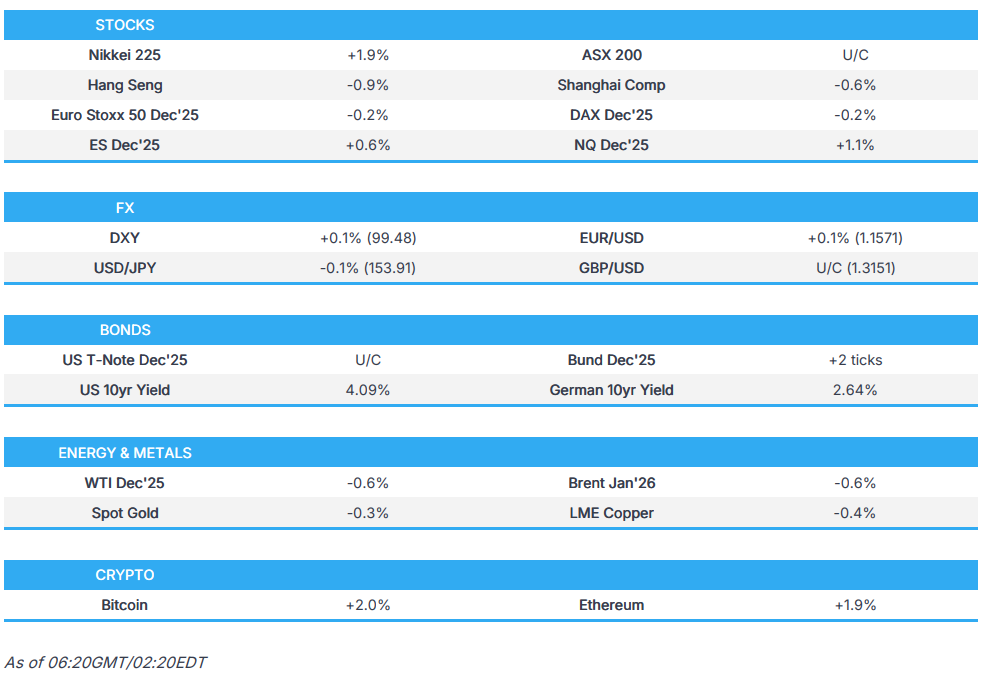

ASIAN MARKETS THIS FRIDAY MORNING:

SHANGHAI CLOSED DOWN 32.11 POINTS OR 0.81%

//Hang Seng CLOSED CLOSED DOWN 376.04 PTS OR 1.43%

// Nikkei CLOSED : UP 1085.73 PTS OR 2.12% //Australia’s all ordinaries CLOSED DOWN 0.01%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1131// OFFSHORE CLOSED DOWN AT 7.1169/ Oil UP TO 60.24 dollars per barrel for WTI and BRENT UP TO 64.06 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING DOWN TO 7.1131 // OFFSHORE YUAN TRADING DOWN TO 7.1169 :/ONSHORE YUAN TRADING ABOVE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1131

OFFSHORE YUAN: DOWN TO 7.1169

HANG SENG CLOSED DOWN 376.04 PTS OR 1.43%

2. Nikkei closed UP 1085.73 PTS OR 2.12%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 99.38 EURO FALLS TO 1.1566 DOWN 5 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.654//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.18…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.034 DOWN 1 FULL BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold FLAT /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6502// Italian 10 Yr bond yield DOWN to 3.401 SPAIN 10 YR BOND YIELD DOWN TO 3.151

3i Greek 10 year bond yield DOWN TO 3.2940

3j Gold at $4015.20Silver at: 48.88 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 42 /100 roubles/dollar; ROUBLE AT 80.46

3m oil (WTI) into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.18/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.654% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.031 DOWN 1 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8023 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9280 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.110 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.628 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.609 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.05 UP 6 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.4310 UP 0 PTS

30 YR UK BOND YIELD: 5.193 UP 0 BASIS PTS

10 YR CANADA BOND YIELD: 3.132 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.720 DOWN 1 BASIS PTS.

a New York OPENING REPORT

Futures Rebound Lifted By Strong Amazon, Apple Earnings

Friday, Oct 31, 2025 – 08:37 AM

US equity futures rebound from the Thursday drop, led by Mag 7. As of 8:00am ET, S&P futures are 0.8% higher and Nasdaq futures gain 1.2%, on pace for sixth and seventh straight monthly gains respectively, with all Mag 7 names higher premarket, led by AMZN (+12.7%) and AAPL (+1.9%) after their robust earnings release (AWS sales growth of 19.7%, best since 2022 and AAPL’s revenue guidance) yesterday after-close. Europe’s Stoxx 600 fell for a fourth day, putting the gauge on track for its longest losing streak since July; in Japan, the tech-heavy Nikkei 225 closed up and notched its best month since 1990. Bond yields are flat, the USD is higher. Commodities are mostly lower; copper fell -2.4%. Today’s calendar slate includes October MNI Chicago PMI at 9:45am (several minutes earlier for subscribers); US government data continue to be postponed by shutdown that began Oct. 1. Fed speaker slate includes Dallas Fed President Logan (9:30am) and Cleveland Fed President Hammack and Atlanta Fed President Bostic (12pm). Both CVX and XOM reporting earnings this morning.

In premarket trading, Mag 7 stocks are all higher: Amazon.com (AMZN) jumps 12% after the company’s cloud unit posted the strongest growth rate in almost three years, reassuring investors who were concerned that the largest seller of rented computing power was losing ground to rivals. Apple Inc. (AAPL) is up 2% after the company predicted a major sales surge during the holiday season after releasing new iPhones, helping assure investors that its flagship product remains a growth engine (Nvidia (NVDA) +2%, Alphabet (GOOGL) +1.2%, Meta Platforms (META) +1.4%, Tesla (TSLA) +1.2%, Microsoft (MSFT) +0.4%)

- Brighthouse Financial (BHF) soars 22% after the Financial Times reports that Aquarian Holdings is in advanced talks to take the US life insurer private.

- Charter Communications (CHTR) falls 5% after posting third-quarter results.

- Cloudflare (NET) rises 8% after the software company forecast revenue for the fourth quarter that beat the average analyst estimate.

- Coinbase (COIN) advances 4% after the largest US crypto exchanged reported third-quarter revenue that exceeded estimates following an uptick in trading as token prices climbed to record highs.

- Dexcom (DXCM) sinks 12% after the glucose-monitor company cut its adjusted gross margin forecast for the full year.

- Floor & Decor (FND) shares are up 7% after the home products retailer reported adjusted earnings per share for the third quarter that beat the average analyst estimate.

- Illumina (ILMN) gain 6% after the gene-sequencing company boosted its adjusted profit and operating margin for the full year. Analysts note the better-than-expected results for the third quarter should help ease investor concerns.

- Netflix Inc. (NFLX) gained more than 2% in premarket trading. The company approved a 10-for-1 stock split to make its share price more accessible for employees who participate in the company’s stock option program. Separately, Reuters reported the company is exploring a bid for Warner Bros. Discovery’s studio and streaming businesses.

- Pony.ai (PONY) is up 4% after the autonomous vehicle technology company said it’s been granted Shenzhen’s first citywide permit for fully driverless commercial robotaxi operations.

- Reddit (RDDT) gains 10% after the social-media company reported third-quarter results that beat expectations and gave an outlook that is above the analyst consensus.

- Roku (ROKU) shares are down 4% after the streaming-video platform company reported its third-quarter results and gave an outlook. While analysts are broadly positive, they said the results aren’t enough to meet high expectations.

- Western Digital (WDC) rises 9% as the computer-storage company reported better-than-expected 1Q results and its current quarter forecast came in largely ahead of estimates.

In corporate news, Exxon Mobil outperformed Wall Street expectations for a sixth consecutive quarter after beginning operations at its fourth oil-production project in Guyana. Chevron beat earnings estimates as profits from the $53 billion Hess Corp. acquisition were included in the results for the first time, boosting oil production and cash flow. Nvidia CEO Jensen Huang still hopes to sell chips from the company’s Blackwell lineup to customers in China, though he has no current plans to do so, he told reporters Friday. Millennium Management is raising $5 billion in a new fund to invest in private market opportunities.

US stock gains offered investors a respite from Thursday’s bruising session, amid lingering doubts over whether heavy AI spending will pay off. The S&P 500’s advance has increasingly relied on a group of tech megacaps – recent record highs were hit on record negative breadth – with warnings over lofty valuations following a blistering rally.

“Volatility has become a feature rather than a bug — day-to-day swings now regularly move major stocks by hundreds of billions of dollars,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg. “The feedback loop of investor sentiment, speculative positioning, and rapid news-driven reactions amplify these moves.”

On Friday, futures rose as Amazon jumped 13% in premarket trading, a move set to add about $300 billion to its market value after reporting the fastest cloud-unit growth in nearly three years. Apple also climbed on a revenue beat and upbeat holiday forecast. Nvidia meanwhile, unveiled new partnerships with South Korea’s biggest firms, extending a global push to expand artificial intelligence infrastructure. Friday’s market gains will seal the index’s longest monthly winning streak since August 2021, capping a rally that has withstood global trade tensions and geopolitical risks.

Earnings season remains top of mind with more than 60% of S&P 500 companies having reported to date, and a further 150 expected today and next week. Contrast of earnings receptions to AI spending has diverged within big tech, as investors seek quantification of how investments are benefiting related businesses. Earnings have also broadly topped forecasts, with about 80% of S&P 500 companies that have reported so far beating expectations.

According to BofA’s Michael Hartnett, global equities drew $17.2 billion in inflows in the week to Oct. 29. Hartnett added that AI’s leadership remains firmly in place. Market breadth remains a concern for traders, and divergence notable between US and European equities. Michael Burry, the man who made his name shorting the US housing market, sent what appears to be a cryptic warning to retail investors about market exuberance. Equity performance in 2025 has been characterized by extreme concentration of volatility episodes, according to Barclays strategists.

“The risks are mainly flows. They have been the main driver, much more than EPS growth,” said Karen Georges, an equity fund manager at Ecofi. “If flows begin to halt on risky assets, then there will be a genuine selloff. But it’s like a black swan, you never know when it’s coming.”

On the trade front, Treasury Secretary Scott Bessent said he expects the US to return to the negotiating table with China in a year. That came after Donald Trump and Xi Jinping agreed to a tariff truce, roll back export controls and reduce other trade barriers. Xi also warned against “breaking supply chains” in his first public remarks after meeting with Trump. “A comprehensive deal still looks far away and while trade tensions have eased for the time being, they have the potential to resurface,” said Mohit Kumar, chief economist and strategist at Jefferies International.

In Europe, the Stoxx 600 fell for a fourth day, putting the gauge on track for its longest losing streak since July. Telecoms, insurance and construction stocks are dragging. Treasuries and European bonds relatively steady, with small outperformance at the short-end in gilts. Here are the biggest movers Monday:

- Puig shares rose as much as 9.8% with trading volume almost 10 times the 20-day average after the Spanish group reported better-than-expected 3Q sales and upgraded its guidance for the last three months of the year

- Fuchs shares gain as much as 12%, the most since March 2020, after the chemicals company reported a stronger-than-expected Ebit as North and South American markets improved from previous softness

- Danske Bank gains as much as 2.8%, the most in a month, after the Danish lender reported solid third-quarter numbers, with analysts flagging strong core revenues and a slight beat to net interest income (NII)

- Interpump shares rise as much as 6.8%. Equita analysts upgraded the Italian hydraulics and pumps manufacturer as they expect the stock to outperform thanks to improving margins and organic trends and see M&A opportunities

- Kongsberg shares gain as much as 4.9% after a slew of analysts upgraded the stock following the Norwegian company’s results-driven declines on Thursday, leaving the firm with no sell or equivalent recommendations

- UMG shares rise as much as 1.8% after the world’s largest record label delivered a beat on both revenue and adjusted Ebitda in the third quarter, with growth in the important subscription unit ahead of expectations

- Erste shares rise as much as 4.1% as the Austrian lender raised its net interest income growth and CET1 capital ratio guidance. The bank sees its deal to buy Santander’s Polish unit on track to close around the year-end

- Viridien shares rose as much as 26%, the biggest jump since 2020, after the French group reported operating profits well above expectations

- Scor shares fall as much as 8.2%, the most since July, as analysts grew concerned about the reinsurance company’s solvency ratio and real estate amortization after it reported third-quarter results

- Spie shares fall as much as 5.9% to the lowest since May as the France-based engineering services company’s third-quarter organic growth came up short

- AXA shares dropped as much as 2.5% after the French insurer reported nine-month results. Jefferies highlighted the Solvency II ratio as the biggest news from the results, while Citi saw the update as uneventful

- Saint-Gobain falls as much as 3.2%, to the lowest since mid-April, after reporting third-quarter like-for-like sales that missed consensus estimates, and expected to trigger small downgrades to consensus numbers

- Acerinox falls as much as 3.4% after the stainless steelmaker said fourth-quarter Ebitda is expected to be lower than in the third quarter. Analysts see potential double-digit downgrades to full-year consensus

- Elis shares fall as much as 1.2% after the French cleaning services group reported growth in Central Europe that missed estimates due to softness in Germany. This morning, the firm also said it will buy Larosé

- Drax shares fall as much as 3.7% after UBS initiated coverage of the chemicals firm with a sell rating, saying too much optimism is priced in for the shares

Earlier in the session, Asia’s benchmark also pared its monthly advance. Stocks in Asia slipped as broad regional losses, led by China and Hong Kong, outweighed gains in Japan and South Korea. The MSCI Asia Pacific Index was down 0.1%, with Alibaba and Tencent among the top laggards, though it’s on track to end the month up 3.6%. The MSCI China Index is on course for its first monthly loss since April, as a liquidity-fueled AI rally gives way to concerns about lingering US-China tensions and economic concerns. In Japan, Hitachi’s better-than-expected earnings and upgraded outlook lifted sentiment. With stocks across major markets trading near record highs, investors are watching for concentration risk and strength of earnings. Results from Amazon and Apple in the US helped lift sentiment around technology names, but BYD’s sales miss raised concerns on the Chinese electric vehicle industry. Stocks also rose in New Zealand and Indonesia, while declining in Vietnam, India and Thailand.