NOV 4/ANOTHER CLASSIC RAID ORCHESTRATED ON OUR PRECIOUS METALS: GOLD CLOSED DOWN $50.00 TO $3951.40 WITH SILVER DOWN $0.82 TO $47.56//PLATINUM CLOSED DOWN $45,10 TO $1542.50 AND PALLADIUM CLOSED DOWN $39,20 TO $1442.50//

*CANADIAN GOLD: $5,551.90 DOWN 66.81 CDN dollars per oz( * NEW ALL TIME HIGH $6135.810 CDN DOLLARS PER OZ//OCT 21 2025)

*BRITISH GOLD: 3025.35 DOWN 17.67Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//3261.88 BRITISH POUNDS/OZ) OCT 21/2025

*EURO GOLD: 3430.58 DOWN 39.53 Euros per oz //* (ALL TIME CLOSING HIGH: 3755.40 EUROS PER OZ/ OCT 16 //2025)

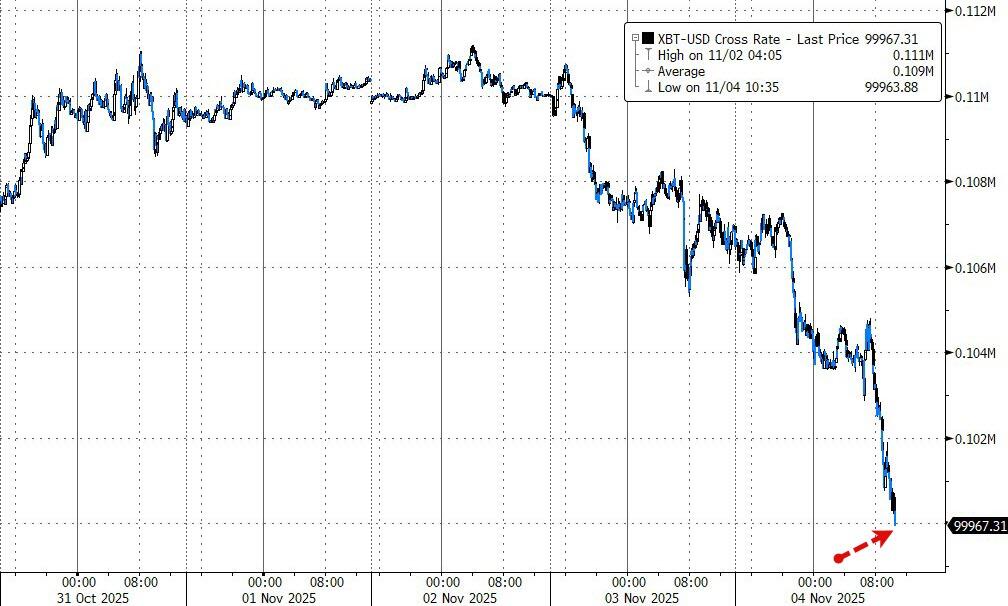

Bitcoin morning price:$103,730 down 2840 DOLLARS (MANY SWITCHING TO PHYSICAL GOLD)

Bitcoin: afternoon price: $100,470 down 6,100 DOLLARS

Platinum price closing UP $14.00 TO $1587.60

Palladium price; UP $4.10 TO $1,442.50

END

EXCHANGE: COMEX

JPMORGAN STOPPED 26/423

OCT

GOLD: NUMBER OF NOTICES FILED FOR NOV/2025: 423 CONTRACTs NOTICES FOR 42,300 OZ or 1.3157 TONNES

total notices so far: 5409 contracts for 540,900 OR 16,824 tonnes)

FOR OCT

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 197 NOTICE(S) FILED FOR 0.985 MILLION OZ/

total number of notices filed so far this month : 2578 CONTRACTS (NOTICES) for 12.890 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $50.00 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD.

INVENTORY RESTS AT 1041.78TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.82 AT THE SLV:

NO CHANGES IN SILVER INVENTORY AT THE SLV:/ //

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 488.363 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A ROSE GIGANTIC SIZED 1122 CONTRACTS TO 157,213 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL LOSS OF $0.12 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S // TRADING.! IT WAS THE SHORT SPECULATORS THAT ARE CONTINUALLY IN TROUBLE AS THE BANKERS TOOK THE LONG SIDE AND THEN TENDERED. WE FINALLY ARE MOVING TO A MUCH HIGHER BASE SURPASSING THE $34.40 SILVER PRICE BARRIER TO A HIGH DEGREE, AND NOW TRYING TO SURPASS OUR LAST MAJOR HURDLE OF $50.00 SILVER AGAIN. WE HAD A HUGE SIZED GAIN OF 1322 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL 200 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO MONDAY’S TRADING / WITH AS YOU WILL WITNESS, WITH LITTLE SUCCESS AS THEY DESPERATELY AGAIN TODAY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $50.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON MONDAY WITH SILVER’S LOSS IN PRICE. THE PRICE FINISHED MILES BELOW THE MAGIC NUMBER OF $50.00 SILVER SPOT PRICE CLOSING AT $48.38 DOWN $0.12 . WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS AT A HUMONGOUS SIZED 853T.A.S. CONTRACTS. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING AGAIN THE 50.00 DOLLAR MARK!!. THERE IS NO NEXT LINE IN THE SAND ONCE THE 50.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A 200 SIZED CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 953 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//RAIDS AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUGE SIZED 1322 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR SMALL LOSS IN PRICE OF $0.12. WE HAD HUGE GOVERNMENT COMEX CONTRACTS TRADING MONDAY AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE SHORT SPECULATORS HAVE NOW BEEN BURIED AS WE WILL EVENTUALLY GO TO OUR NORMAL SPECS LONG AND BANKERS SHORT MANTRA FOR NOVEMBER TRADING.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT//TUESDAY MORNING: A HUGE SIZED 953 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THE BANKERS HAVE BURIED OUR SHORT SPECULATORS AS THEY TOOK THE LONG SIDE OF TRADING THIS PAST WEEK AND THEN THEY TENDERED FOR PHYSICAL SILVER. THE PROBLEM FOR THE SHORT SPECULATORS WILL BE TO FIND THE NECESSARY PHYSICAL SILVER

WE HAD A 200CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 11.575 MILLION OZ FOLLOWED BY OUR INITIAL 1.245 MILLION OZ QUEUE JUMP/ FOLLOWED BY TODAY;S 1,93 MILLION OZ QUEUE JUMP/STANDING ADVANCES TO 14.260 MILLION OZ/

THUS:

INITIAL STANDING FOR NOV: 11.575 MILLION OZ

PLUS INITIAL 1.245 MILLION OZ QUEUE JUMP

THEN ADD TODAY;S 1,93 MILLION OZ QUEUE JUMP

EQUALS

14.260MILLION OZ STANDING FOR SILVER.

WE HAD:

/ MEGA HUGE COMEX OI GAIN+// A 200 EFP ISSUANCE CONTRACTS (/ VI) A HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE 893CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: A HUGE 462 CONTRACTS WERE REMOVED!!!!!!

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV.. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV.

TOTAL CONTRACTS for 2 DAY(S), total 660 contracts: OR 3.300 MILLION OZ (330 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 3.300 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOV:3.300 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1122 CONTRACTS DESPITE OUR LOSS IN PRICE OF $0.12 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A 200 SIZED CONTRACT EFP ISSUANCE : 200 ISSUED FOR DEC., AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 8 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

AND NOW NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY OUR INITIAL QUEUE JUMP OF 1.245 MILLION OZ/ FOLLOWED BY TODAY’S 1.93 MILLION OZ JUMP/STANDING ADVANCES TO 14.260 MILLION OZ/

THE NEW TAS ISSUANCE MONDAY NIGHT (953) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!!

WE HAD 197 NOTICE(S) FILED TODAY FOR 0.985million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON A MASSIVE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR 2873 OI CONTRACTS TO 452,773 OI AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A RELATIVELY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED AHUGE AND CRIMINAL 5883 CONTRACTS //HUGE GOVERNMENT REMOVALS//CLOSE TO RECORD ADJUSTMENTS

WE HAD A FAIR INCREASE IN COMEX OI (3673 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $17.90 IN PRICE// MONDAY///.

LAST 7 MONTHS OF GOLD DELIVERIES:

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY ITS FIRST QUEUE JUMP OF 1.245 TONNES/ FOLLOWED BT TODAT;S QUEUE JUMP OF 1,368 TONNES/NEW STANDING ADVANCES TO 18.276 TONNES OF GOLD.

E.F.P. ISSUANCE/FOR OPENING NOV GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 800 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 452,773/ AND WE NOW WITNESSING A STRONG COMEX OI WITH AN EXTREMELY HIGH PRICE OF GOLD

SILVER ALSO HAS A STRONG SIZED COMEX OI OF 157,212CONTRACTS

IN ESSENCE WE HAVE A STRONG INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3673 CONTRACTS WITH 2873 CONTRACTS INCREASED AT THE COMEX// AND A SMALLLSIZED 800 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3673 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1051 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON LIKE WE WITNESSED DURING THIS PAST WEEK (4 RAIDS)

GOLD PRICE ON FRIDAY ROSE BY $17.90

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(800) ACCOMPANYING THE GAIN IN COMEX OI OF 2873 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3673 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR ORIGINAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) STRONG INITIAL STANDING FOR GOLD FOR NOV AT 15.651 TONNES OF NORMAL DELIVERY TO WHICH WE ADD OUR FIRST QUEUE JUMP OF 1.2566 TONNES AND THEN TODAY;S 1,368 TONNES/NEW STANDING ADVANCES TO 18.276 TONNES.

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(800) ACCOMPANYING THE GAIN IN COMEX OI OF 2873CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 9556 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) STRONG INITIAL STANDING FOR GOLD FOR NOV AT 15.575 TONNES PLUS INITIAL 1.2566 TONNES QUEUE JUMP FOLLOWED BY TODAY;S 1,368 TONNES= 18.276 TONNES.

NEW STANDING FOR GOLD, NOV CONTRACT AT 18.276 TONNES OF GOLD

3) LITTLE T.A.S. LIQUIDATION (AND CONSIDERABLE GOVT LIQUIDATION AND ZERO LIQUIDATION OF EQUITY SHARES) AS WE HAD 1)A $17.90 COMEX PRICE GAIN WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG SIZED GAIN OF 3673 CONTRACTS ON OUR TWO EXCHANGES. HOWEVER WE HAD SOME SHORT SPECULATOR CONTRACTS BEING LIQUIDATED AS THE BANKERS TENDERED FOR PHYSICAL./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4) FAIR SIZED COMEX OI GAIN/ 5) V) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (2024)

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV. :

TOTAL EFP CONTRACTS ISSUED: 1835 CONTRACTS OR 183,500OZ OR 5.765 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 917 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN2TRADING DAY(S) IN TONNES: 5.765 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 5.765 TONNES DIVIDED BY 3550 x 100% TONNES = 0.1662% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 5.765 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1122 CONTRACTS OI TO 157,212 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 200 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1122 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1322 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITEOUR LOSS OF $0.12 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 6.850 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 16.34 POINTS OR 0.41%

//Hang Seng CLOSED CLOSED DOWN 205.96 PTS OR 0.79%

// Nikkei CLOSED : DOWN 914.14PTS OR 1,74% //Australia’s all ordinaries CLOSED DOWN 0.92%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1254// OFFSHORE CLOSED DOWN AT 7.1305/ Oil DOWN TO 60.22 dollars per barrel for WTI and BRENT DOWN TO 64.04 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING DOWNTO 7.1254// OFFSHORE YUAN TRADING DOWN TO 7.1305:/ONSHORE YUAN TRADING ABOVE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR 2873CONTRACTS TO 452,773 OI WITH THE GAIN IN PRICE OF $17.90 WITH RESPECT TO MONDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (800). WE HAD LITTLE T.A.S. LIQUIDATION MONDAY. HOWEVER AGAIN, IT WAS THE MAJOR SPECULATORS THAT WENT LONG AGAIN AND THE BANKERS WHO TOOK THE SHORT SIDE. THE LONGS ON MONDAY NIGHT TENDERED THEIR BOUGHT CONTRACTS FOR PHYSICAL.

WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3673 CONTRACTS (OR 11.42 TONNES).THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

EXCHANGE FOR PHYSICAL//GOLD ISSUANCE//OCTOBER:

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT FOR GOLD REMAINS AT 14.553 TONNES OF GOLD UNDER THE GUIDANCE OF 6 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FINAL

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 130.3TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 130.3 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW NOVEMBER COMEX MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 3673 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT/EARLY NOVEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR SIZED T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1051 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN ON LAST FRIDAY’S AND LAST TUESDAY’S HUGE RAIDS, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS WE WE WILL PROBABLY SEE GOLD//SILVER RISE HUGELY ON OUR UPCOMING DAYS.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS:

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE FINISHING OPTION EXPIRY WEEK, THE CROOKS GOADED OUR SPECULATORS TO CONTINUE ONTO THE SHORT SIDE WITH THE BANKERS ON THE LONG SIDE…THE RAIDS THROUGHT THIS WEEK WERE FREQUENT BUT FAILED TO CAUSE ANY DAMAGE TO THE PRICE WITH OPTIONS EXPIRY FINISHING OCT 31 AS WE NOW ENTER OUR MONTH OF NOVEMBER

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT:

F) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

G) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

H) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

I) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

J) A MASSIVE QUEUE JUMP OCT 9 FOR 4.979 TONNES

K) A MASSIVE AND 3RD HIGHEST EVER OCT 10 QUEUE JUMP FOR 7.504 TONNES

L) A MASSIVE QUEUE JUMP OF 4.3919 TONNES

M) A RECORD SETTING QUEUE JUMP OF 9.564 TONNES

N) A HUGE 6.469 TONNES QUEUE JUMP

0) A HUGE 8.326 TONNES QUEUE JUMP

P) A RECORD SETTING 12.031 TONNE QUEUE JUMP THE HIGHEST EVER RECORDED IN COMEX HISTORY SURPASSING TUESDAY’S 9.564 TONNES

Q/ QUEUE JUMP OF 7.695 TONES OF GOLD//

R/ TODAY’S QUEUE JUMP OF 3.8600 TONNE JUMP

S) OCT 22 QUEUE JUMP OF 8.622 TONNES//

T) 1OCT 23 1.695 TONNES

U) OCT 24. 0.8615 TONNES

V) OCT 27 0.3048 TONNE QUEUE JUMP

W) OCT 28 QUEUE JUMP OF .5069

X) OCT 29 QUEUE JUMP OF .4096 TONNES

Y) OCT 30 QUEUE JUMP OF 0.00311 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

AND NOW NOVEMBER:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503200 OZ (15.651 TONNES) FOLLOWED BY ITS FIRST QUEUE JUMP OF 1.2566 TONNES/ FOLLOWED BY TODAY’S QUEUE JUMP OF 1.368 TONNESNEW STANDING ADVANCES TO 18.276 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 54+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 24 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 54 TONNES REMAIN ON THE BOOKS OF THE BIS.

THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING E.G. NOVEMBER: A HUGE 15.651 TONNES STANDING IN AN OFF MONTH!! THIS IS HUGE!!!

EXCHANGE FOR PHYSICAL ISSUANCE/NOV//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1051 CONTRACTS.

THAT IS A FAIR SIZED 1051 EFP CONTRACT WAS ISSUED: : /DEC 1051 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1051 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 24 TONNES

WE HAD :

LITTLE LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY + GOVERNMENT LIQUIDATION

MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE OCT 31 WITH OUR ATTEMPTED FAILED RAID,

T.A.S.SPREADER ISSUANCE//NOV

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED SIZED 1889 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP MONDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING STRONG GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS WITH THE FOLLOWING;

WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.. ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

AND NOW NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY OUR FIRST QUEUE JUMP OF THE MONTH OF 1.2566 TONNES AND THEN TODAY’S QUEUE JUMP OF 1,368 TONNES//STANDING ADVANCES TO 18.276TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING NOVEMBER,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $17.90/ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG GAIN IN OI FROM TWO EXCHANGES OF 9556 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD LITTLE T.A.S. SPREADER LIQUIDATION MONDAY. HOWEVER WE DID HAVE AGAIN HUGE SPECULATOR LIQUIDATION AS THEY ARE THE ONES WHO ARE SHORT AS THE BANKERS WENT LONG THE LAST WEEK OF OCTOBER AND EARLY NOVEMBER AS THEY TENDERED FOR PHYSICAL. THIS WAS COUPLED WITH A) GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION). /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS EVEN THOUGH THEY TRANSFERRED THESE LOSSES ONTO THE FED’S BALANCE SHEET.THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS EVERY OTHER DAY!!

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL

AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR FIRST QUEUE JUMP OF 1.2566 NOV 3// AND NOV 4 QUEUE JUMP OF 1.368 TONNESNEW STANDING ADVANCES TO 18.276TONNES OF GOLD.

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $17.90

WE HAD A HUGE AND RECORD 5883 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES : 3673 CONTRACTS OR 367,300 OZ OR 11.42TONNES

i) Out of JPMorgan 42,149.961 oz (1311 kilobars) ii) Out of Malca: 77,162.400 (2400 kilobars)

total withdrawal: 119,312.361 oz 3.711 tonnes 3711 kilobars

they are draining the comex of gold

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

DEPOSITS/CUSTOMER

0 entries

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

423notice(s) 42,300 OZ

1.3197 TONNES OF GOLD

No of oz to be served (notices)

467 contracts 46,700 OZ 1.452 TONNES

Total monthly oz gold served (contracts) so far this month

5409notices 540,900oz 16.824 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

2 ENTRIES

i) Out of JPMorgan 42,149.961 oz (1311 kilobars) ii) Out of Malca: 77,162.400 (2400 kilobars)

total withdrawal: 119,312.361 oz 3.711 tonnes 3711 kilobars

they are draining the comex of gold

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1/customer to dealer

Asahi: 600.154 oz

volume at the comex: FRIDAY: 269,851oz ( fair)//

AMOUNT OF GOLD STANDING FOR NOVEMBER:

THE FRONT MONTH OF NOV STANDS AT 890 CONTRACTS FOR A GAIN OF 209 CONTRACTS.

WE HAD 231 CONTRACTS SERVED ON MONDAY. SO WE GAINED A STRONG 440 CONTRACTS FOR 44000 OZ OF GOLD (1.368 TONNES).

DECEMBER LOST 880 CONTRACTS DOWN TO 327,572 CONTRACTS .

JANUARY GAINED 4 CONTRACTS UP TO 837

We had 423 contracts filed for today representing 42,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 423 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 26 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2025. contract month, we take the total number of notices filed so far for the month (5409 oz ) to which we add the difference between the open interest for the front month of NOV ( 890 CONTRACTS) minus the number of notices served upon today (423x 100 oz per contract) equals 587,600OZ OR 18.276 TONNES OF GOLD

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (5409x 100 oz +we add the difference for front month of OCT. (890 OI} minus the number of notices served upon today (423 x 100 oz) which equals 587,600OZ OR 18.276 TONNES

TOTAL COMEX GOLD STANDING FOR NOV..: 18.276 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE ACTIVE DELIVERY MONTH OF NOVEMBER

volume THURSDAY confirmed 247,772 contracts ok

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,757,713.711oz 54.672 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 37,881,682.094 oz

TOTAL REGISTERED GOLD 19,868,361.391 or 617.97tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,013,320.703 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 18,109,524 oz ((REG GOLD- PLEDGED GOLD)= 563.28tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE NOV. 2025 SILVER CONTRACTS

NOV 4 2025

INITIAL/

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

2 entries

i) out of CNT 598,740.550 oz ii) out of Loomis: 600,148.700

total withdrawal 1,198,889.250 oz

Deposits to the Dealer Inventory

0 ENTRY

Deposits to the Customer Inventory

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 entries

i) into Loomis 600,148.700 oz ii) Into CNT: 598,740.550 oz

total deposit 1,198,889.250 oz

No of oz served today (contracts)

197 CONTRACT(S) ( 0.985 MILLION OZ

No of oz to be served (notices)

274 contracts (1.370 MILLION oz)

Total monthly oz silver served (contracts)

2578 Contracts (12.890 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) out of CNT 598,740.550 oz ii) out of Loomis: 600,148.700

total withdrawal 1,198,889.250 oz

adjustments: 3 and huge: dealer to customer

a) Asahi 3,199,234.340 oz

b) CNT: 2,400,803.253 oz

c) JPMorgan: 602,343.100 oz

total 6.242 million oz moves from dealer to customer acct

comex is in turmoil

TOTAL REGISTERED SILVER: 158,001 MILLION OZ//.TOTAL REG + ELIGIBLE. 482.363 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF NOVEMBER /2025 OI: 471 OPEN INTEREST CONTRACTS FOR A LOSS OF 99 CONTRACTS. WE HAD 387 NOTICES SERVED ON MONDAY SO WE GAINED A HUGE 386 OR 1.93 MILLION OZ QUEUE JUMP.

DECEMBER GAINED 19 CONTRACTS UP TO 105,295

JANUARY GAINED 35 CONTRACTS UP TO 824 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 197 or 0.985MILLION oz

CONFIRMED volume; ON MONDAY 60,898good//

AND NOW NOVEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 2578 X5,000 oz = 12.890MILLION oz

to which we add the difference between the open interest for the front month of NOV (471) AND the number of notices served upon today (197 )x (5000 oz)

Thus the standings for silver for the NOVEMBER 2025 contract month: (2578) Notices served so far) x 5000 oz + OI for the front month of NOV(471) minus number of notices served upon today (197)x 5000 oz equals silver standing for the NOV.contract month equating to 14.260 MILLION OZ

New total standing: 14.260 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 158.001 million oz of registered silver

JPMorgan as a percentage of total silver: 205.650/482.363million. 42.63%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

NOV 3 WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 1.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1039,20 TONNES

OCT 31 WITH GOLD DOWN $17.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1040.35 TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

OCT 23 WITH GOLD UP $78.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37 TONNES

OCT 22 WITH GOLD DOWN $78.95 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

GLD INVENTORY: 1041.78TONNES, TONIGHTS TOTAL

SILVER

NOV 4 WITH SILVER $0.82 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

NOV 3 WITH SILVER $0.12 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 31 WITH SILVER DOWN $0.35 TODAY/SMALL CHANGES IN SILVER AT THE SLV: ///A WITHDRAWAL OF 636,000 OZ FROM THE SLV// ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

OCT 23 WITH SILVER UP $0.87 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 501.474 MILLION OZ

OCT 22 WITH SILVER DOWN $0.33 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.995 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 504.015 MILLION OZ

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

CLOSING INVENTORY 488.363 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD

3. CHRIS POWELL AND HIS GATA DISPATCHES

Chris Powell: First they ignore you, then they laugh at you, then they fight you, and then. …?

Submitted by admin on Sun, 2025-11-02 22:39 Section: Daily Dispatches

Illustrations for this presentation are posted here.

* * *

Remarks by Chris Powell Secretary/Treasurer Gold Anti-Trust Action Committee Inc. New Orleans Investment Conference Sunday, November 2, 2025

ILLUSTRATION 1 — INTRODUCTION

There is a saying about political struggle: “First they ignore you, then they laugh at you, then they fight you, and then you win.”

My organization, the Gold Anti-Trust Action Committee, gets the point about struggle. Bill Murphy and I started GATA 27 years ago, in 1998, with the objective of exposing and stopping the rigging of the gold market.

The purpose of gold market rigging, as we have documented extensively, has been to depress and control gold prices to defend government currencies and bonds, and particularly to defend the U.S. dollar, the world reserve currency, and U.S. government bonds, against competition from the former world reserve currency.

The rigging — starting with the Bretton Woods agreement of 1944, which pegged the official gold price at $35 per ounce — worked pretty well for decades, but started to falter seriously as central banks sold or lent so much of their gold reserves into the market for price control and then discovered in the 1960s, 1990s, and early 2000s that they couldn’t recover all their metal without exploding the gold market and crashing their currencies and the investment banks that had been borrowing the gold and using it in a carry trade with government bonds.

he rigging — starting with the Bretton Woods agreement of 1944, which pegged the official gold price at $35 per ounce — worked pretty well for decades, but started to falter seriously as central banks sold or lent so much of their gold reserves into the market for price control and then discovered in the 1960s, 1990s, and early 2000s that they couldn’t recover all their metal without exploding the gold market and crashing their currencies and the investment banks that had been borrowing the gold and using it in a carry trade with government bonds.

And then, in this decade, U.S. freezing of Russian foreign-exchange assets amid the conflict over Ukraine signified that foreign assets assigned to U.S. custody weren’t safe and that U.S. dollars and Treasury bonds weren’t safe either. Governments and central banks began to realize that the only financial assets that are safe are gold and maybe silver held in their own vaults in their own countries.

So the new gold and silver rush began, seemingly led by China, which long has been accumulating gold — far more than it has been reporting officially — and now is even opening gold vaults and exchanges in other countries to help take gold and currency pricing power away from London and New York and to help internationalize the Chinese currency, the renminbi.

A few months ago we at GATA began to wonder if the metals had won because of the breakup of the longstanding government and central bank coalition against gold. Then a couple of weeks ago came big smashdowns in gold and silver.

Mainstream financial news organizations tried to contrive explanations for the smashes. Nobody in mainstream financial news organizations asked the crucial questions: Exactly WHO was doing all that selling, and exactly WHAT was being sold — real metal or just derivatives and futures contracts?

Since the bulk of the selling came out of the London and New York markets, the evidence is that the smashes were probably interventions by the U.S. Federal Reserve and its ally, the Bank of England, to break the enthusiasm in the monetary metals markets and get them down in advance of the Fed’s imminent reduction in interest rates, whereupon the metals might rise again but from a lower base and not excite the world so much.

In any case the main point about gold is that it is the playground and battlefield of governments and central banks, and probably will remain so forever.

*

Soon after GATA got started in 1998 we got a huge contribution, $50,000, from a mining entrepreneur. We used it as a retainer for a major national antitrust law firm. They did a lot of research and gave us some bad news — that gold market rigging is perfectly legal when perpetrated by the government, even through intermediaries, and that the rigging was almost certainly a government operation, in which investment banks act only as the government’s brokers, providing camouflage.

ILLUSTRATION 2 — Treasury Department’s ESF page

The lawyers noted that the Gold Reserve Act of 1934, as amended over the years, gives the U.S. Treasury Department the authority to use its Exchange Stabilization Fund to intervene secretly in and rig not just the gold market but any market in the world:

The problem for the U.S. government as the issuer of the world reserve currency is that gold is not just money but the best form of money — not just divisible, durable, portable, and in limited supply, the ideal characteristics for money as identified by Aristotle — but is also without counterparty risk.

So any government issuing a different form of money is always competing with gold. Governments try to control the price of gold to protect their own money.

Learning that gold market rigging by the government is perfectly legal was an expensive lesson for us. We were chastened, having been told that while we were almost certainly right that the gold market was being rigged, antitrust law wasn’t going to help us.

But all was not lost. We figured that we might be just as effective to compile the documentation of gold market manipulation and publicize it to investors, mining companies, and financial news organizations. After all, the manipulation was being conducted largely in secret precisely because publicity would destroy the scheme, liberating gold from price manipulation, and then gold would destroy inflationary government currencies and U.S. imperialism.

Discovering and compiling the records of official manipulation of the gold market turned out to be easy. The records were all over the place — in government archives and the speeches and memoirs of central bankers who thought that no one besides other central bankers would be reading or listening.

As we began to publicize these documents through GATA’s internet site, friends of gold around the world alerted us to more.

ILLUSTRATION 3 — Greenspan testimony

In 1998, just as GATA was being organized, Federal Reserve Chairman Alan Greenspan told Congress that it shouldn’t bother trying to regulate financial market derivatives, particularly derivatives involving gold, because the gold market was beyond cornering by traders OUTSIDE government.

Greenspan explained: “Nor can private counterparties restrict supplies of gold, another commodity whose derivatives are often traded over-the-counter, where central banks stand ready to lease gold in increasing quantities should the price rise”:

Greenspan’s assertion had profound significance for gold prices. The chairman of the Fed was telling Congress that the gold market was in no danger of being cornered by “private counterparties” because central banks had already cornered it by lending gold for price suppression.

ILLUSTRATION 4 — Veneroso Gold Book

Also in 1998 the financial analyst Frank Veneroso published a compendium of gold-related data he titled “The Gold Book” in which he documented extensive gold leasing and swapping by central banks.

ILLUSTRATION 5 — Warburton photo and book

Three years later, in 2001, the British economist Peter Warburton may have been the first analyst to figure things out comprehensively.

In a brilliant essay titled “The Debasement of World Currency — It Is Inflation, But Not as We Know It” — Warburton speculated that central banks had encouraged the use of derivatives by major investment banks for commodity price suppression to help conceal the vast inflation central banks were creating in the world’s money supply and to divert this inflation away from commodities, whose price increases would show up in the cost of living. Inflation would go into financial assets instead.

ILLUSTRATION 6 — Wikipedia page about the London Gold Pool

Understanding their competition with gold, the United States and seven of its European allies controlled world gold prices from 1961 to 1968 through what was called the London Gold Pool, a mechanism of coordinated dishoarding from official gold reserves to hold the metal to the official price of $35 per ounce:

But when inflation and heavy demand for real metal collapsed the gold pool in March 1968, other mechanisms of price control had to be found — like the gold leasing Greenspan acknowledged to Congress.