access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XGE: COMEX

118 C MACQUARIE FUTURES US 4

118 H MACQUARIE FUTURES US 27

167 C MAREX 1

190 H BMO CAPITAL MARKETS 27

323 C HSBC 197

363 H WELLS FARGO SECURITI 108

435 H SCOTIA CAPITAL (USA) 445

661 C JP MORGAN SECURITIES 18

709 C BARCLAYS 4

880 H CITIGROUP 400

905 C ADM 25

GOLD: NUMBER OF NOTICES FILED FOR NOV/2025: 628 CONTRACTs NOTICES FOR 62,800 OZ or 1.953 TONNES

total notices so far: 6037 contracts for 603,700 OR 18.777 tonnes)

SILVER NOTICES: 335 NOTICE(S) FILED FOR 1.675MILLION OZ/

total number of notices filed so far this month : 2913 CONTRACTS (NOTICES) for 14.565million oz

INITIAL STANDING FOR NOV: 11.575 MILLION OZ

PLUS INITIAL 1.245 MILLION OZ QUEUE JUMP

THEN ADD YESTERDAY;S 1,93 MILLION OZ QUEUE JUMP

THENN TODAY;S 0.570 MILLION OZ QUEUE JUMP

EQUALS

14.830 MILLION OZ STANDING FOR SILVER.

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOV:3.355 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

AND NOW NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY OUR INITIAL QUEUE JUMP OF 1.245 MILLION OZ/ FOLLOWED BY YESTERDAY’S 1.93 MILLION OZ JUMP AND THEN TODAY;S ,570 MILLION OZ QUEUE JUMP/STANDING ADVANCES TO 14.830 MILLION OZ/

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY ITS FIRST QUEUE JUMP OF 1.245 TONNES/ FOLLOWED BT YESTERDAY;S QUEUE JUMP OF 1,368 TONNES/ AND NW TODAY’S STRONG 1,477 TONNE QUEUE JUMP.//NEW STANDING ADVANCES TO 19.760 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 15.66 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1950 CONTRACTS OI TO 155,212 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 50 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 50 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1950 CONTRACTS AND ADD TO THE 50 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 1905 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITEOUR LOSS OF $0.82 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 9.525 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $0.82

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 9.56 POINTS OR 0.23%

//Hang Seng CLOSED CLOSED DOWN 16.99PTS OR 0.07%

// Nikkei CLOSED : DOWN 1284,93 PTS OR 2.50% //Australia’s all ordinaries CLOSED DOWN 0.30%

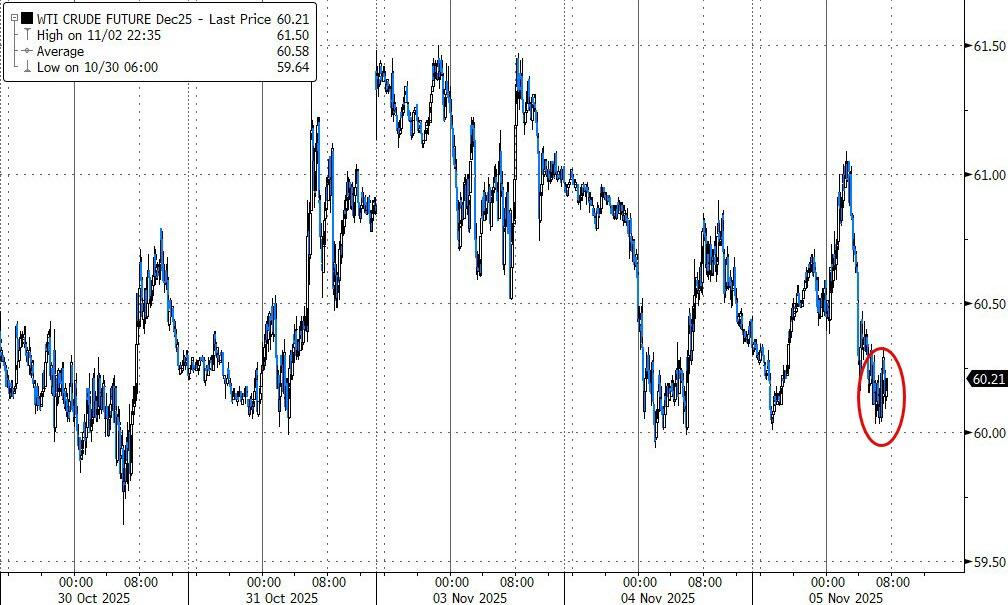

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.12075/ OFFSHORE CLOSED DOWN AT 7.1329/ Oil DOWNTO 60.20 dollars per barrel for WTI and BRENT DOWN TO 64.10 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING DOWNTO 7.1275/ OFFSHORE YUAN TRADING DOWN TO 7.1329:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR 2374 CONTRACTS TO 450,399 OI WITH THE LOSS IN PRICE OF $50.00 WITH RESPECT TO TUESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST NO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3200). WE HAD HUGE T.A.S. LIQUIDATION TUESDAY. HOWEVER AGAIN, IT WAS THE MAJOR SPECULATORS THAT WENT SHORT AGAIN AND THE BANKERS WHO TOOK THE LONG SIDE. THE LONGS ON TUESDAY NIGHT TENDERED THEIR BOUGHT CONTRACTS FOR PHYSICAL.

WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 826 CONTRACTS (OR 2.56 TONNES).THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

EXCHANGE FOR PHYSICAL//GOLD ISSUANCE//OCTOBER:

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT FOR GOLD REMAINS AT 14.553 TONNES OF GOLD UNDER THE GUIDANCE OF 6 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FINAL

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 130.3TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 130.3 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW NOVEMBER COMEX MONTH//

IN TOTAL WE HAD A SMALL SIZED GAIN ON OUR TWO EXCHANGES OF 826 CONTRACTS DESPITE OUR HUGE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT/EARLY NOVEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A STRONG SIZED T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 2647 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN ON LAST FRIDAY’S AND LAST TUESDAY’S HUGE RAIDS, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS WE WE WILL PROBABLY SEE GOLD//SILVER RISE HUGELY ON OUR UPCOMING DAYS.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS:

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE FINISHING OPTION EXPIRY WEEK, THE CROOKS GOADED OUR SPECULATORS TO CONTINUE ONTO THE SHORT SIDE WITH THE BANKERS ON THE LONG SIDE…THE RAIDS THROUGHT THIS WEEK WERE FREQUENT BUT FAILED TO CAUSE ANY DAMAGE TO THE PRICE WITH OPTIONS EXPIRY FINISHING OCT 31 AS WE NOW ENTER OUR MONTH OF NOVEMBER

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT:

F) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

G) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

H) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

I) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

J) A MASSIVE QUEUE JUMP OCT 9 FOR 4.979 TONNES

K) A MASSIVE AND 3RD HIGHEST EVER OCT 10 QUEUE JUMP FOR 7.504 TONNES

L) A MASSIVE QUEUE JUMP OF 4.3919 TONNES

M) A RECORD SETTING QUEUE JUMP OF 9.564 TONNES

N) A HUGE 6.469 TONNES QUEUE JUMP

0) A HUGE 8.326 TONNES QUEUE JUMP

P) A RECORD SETTING 12.031 TONNE QUEUE JUMP THE HIGHEST EVER RECORDED IN COMEX HISTORY SURPASSING TUESDAY’S 9.564 TONNES

Q/ QUEUE JUMP OF 7.695 TONES OF GOLD//

R/ TODAY’S QUEUE JUMP OF 3.8600 TONNE JUMP

S) OCT 22 QUEUE JUMP OF 8.622 TONNES//

T) 1OCT 23 1.695 TONNES

U) OCT 24. 0.8615 TONNES

V) OCT 27 0.3048 TONNE QUEUE JUMP

W) OCT 28 QUEUE JUMP OF .5069

X) OCT 29 QUEUE JUMP OF .4096 TONNES

Y) OCT 30 QUEUE JUMP OF 0.00311 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

AND NOW NOVEMBER:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503200 OZ (15.651 TONNES) FOLLOWED BY ITS FIRST QUEUE JUMP OF 1.2566 TONNES/ FOLLOWED BY TODAY’S QUEUE JUMP OF 1.368 TONNES// AND FINALLY TODAY’S 1,477 TONNE QUEUE JUMP//NEW STANDING ADVANCES TO 19.760TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 54+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 24 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 54 TONNES REMAIN ON THE BOOKS OF THE BIS.

THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING E.G. NOVEMBER: A HUGE 15.651 TONNES STANDING IN AN OFF MONTH!! THIS IS HUGE!!!

EXCHANGE FOR PHYSICAL ISSUANCE/NOV//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 3200 CONTRACTS.

THAT IS A STRONGSIZED 3200 EFP CONTRACT WAS ISSUED: : /DEC 3200 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3200 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 24 TONNES

WE HAD :

- HUGE LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY + GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE OCT 31 WITH OUR ATTEMPTED FAILED RAID,

T.A.S.SPREADER ISSUANCE//NOV

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A STRONG SIZED SIZED 2647 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP TUESDAY’S LOSS IN PRICE IN GOLD WITH A CORRESPONDING STRONG GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.. ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

AND NOW NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY OUR FIRST QUEUE JUMP OF THE MONTH OF 1.2566 TONNES AND THEN WE HAD A QUEUE JUMP OF 1,368 TONNES/ AND THEN TODAY AT 1,477 TONNES/STANDING ADVANCES TO 19.760TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING NOVEMBER,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $50.00/ /) BUT WERE UNUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A SMALLGAIN IN OI FROM TWO EXCHANGES OF 826 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION TUESDAY HOWEVER WE DID HAVE AGAIN HUGE SPECULATOR SHORTING AS THEY ARE THE ONES WHO ARE MASSIVELY SHORT AS THE BANKERS WENT LONG THE LAST WEEK OF OCTOBER AND EARLY NOVEMBER INCLUDING YESTERDAY. THE BANKERS TENDERED FOR PHYSICAL LAST NIGHT MUCH TO THE HORROR OF OUR SHORT SPECS WHO MUST NOW FIND THE NECESSARY PHYSICAL GOLD TO SATISFY THEM. THE COMEX IS ONE BIG MESS!!

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL

AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR FIRST QUEUE JUMP OF 1.2566 NOV 3// AND NOV 4 QUEUE JUMP OF 1.368 TONNES//NOV 5 QUEUE JUMP OF 1,477 TONNES//NEW STANDING ADVANCES TO 19.760TONNES OF GOLD.

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $50.00

WE HAD A HUGE AND RECORD 15,308 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

INITIAL GOLD COMEX

NOV 5

NOV CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 628 notice(s) 62800 OZ 1.953 TONNES OF GOLD |

| No of oz to be served (notices) | 316 contracts 31600OZ 0.902 TONNES |

| Total monthly oz gold served (contracts) so far this month | 6037notices 603700oz 18.565 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

0ENTRIES

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1/0

volume at the comex: TUESDAY: 277,749oz ( fair)//

AMOUNT OF GOLD STANDING FOR NOVEMBER:

THE FRONT MONTH OF NOV STANDS AT 946 CONTRACTS FOR A GAIN OF 56 CONTRACTS.

WE HAD 423 CONTRACTS SERVED ON TUESDAY. SO WE GAINED A STRONG 475CONTRACTS FOR 47500 OZ OF GOLD (1.477 TONNES).

DECEMBER GAINED 6503 CONTRACTS UP TO 335,787 CONTRACTS .

JANUARY GAINED 14 CONTRACTS UP TO 851

We had 628 contracts filed for today representing 62800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 628 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2025. contract month, we take the total number of notices filed so far for the month (6037 oz ) to which we add the difference between the open interest for the front month of NOV ( 946CONTRACTS) minus the number of notices served upon today (628x 100 oz per contract) equals 635,300OZ OR 19.760TONNES OF GOLD

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (6037x 100 oz +we add the difference for front month of NOV (946 OI} minus the number of notices served upon today (4628x 100 oz) which equals 635,300 OZ OR 19.760TONNES

TOTAL COMEX GOLD STANDING FOR NOV..: 19.760 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE ACTIVE DELIVERY MONTH OF NOVEMBER

volume TUESDAY confirmed 247,772 contracts ok

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,757,713.711oz 54.672 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 37,881,682.094 oz

TOTAL REGISTERED GOLD 19,868,361.391 or 617.97tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,013,320.703 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 18,109,524 oz ((REG GOLD- PLEDGED GOLD)= 563.28tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE NOV. 2025 SILVER CONTRACTS

NOV 5 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) out of CNT 303,978.959 oz ii) out of hsbc: 601,025,880 OZ iii) out of Delaware 1903,581 0z total withdrawal 906,908.629 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 entries i) into Delaware: 1069,687 oz total deposit 1069.687 oz |

| No of oz served today (contracts) | 335 CONTRACT(S) ( 1.675 MILLION OZ |

| No of oz to be served (notices) | 53 contracts (0.265MILLION oz) |

| Total monthly oz silver served (contracts) | 2913 Contracts (14.565 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 entries

i) into Delaware: 1069,687 oz

total deposit 1069.687 oz

`

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3 entries

i) out of CNT 303,978.959 oz

ii) out of hsbc: 601,025,880 OZ

iii) out of Delaware 1903,581 0z

total withdrawal 906,908.629 oz

adjustments: 5 :

first 4:dealer to customer

a) Asahi 279,498.400 oz

c) JPMorgan: 156,970.400 oz

d) Brinks 313,548,700 oz

e) CNT customer to dealer 306,237.319 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 157.503MILLION OZ//.TOTAL REG + ELIGIBLE. 481.457 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF NOVEMBER /2025 OI: 388 OPEN INTEREST CONTRACTS FOR A LOSS OF 83 CONTRACTS. WE HAD 197 NOTICES SERVED ON TUESDAY SO WE GAINED A HUGE 114 OR 0.570 MILLION OZ QUEUE JUMP.

DECEMBER LOST 2578CONTRACTS DOW TO 102,671

JANUARY GAINED 0 CONTRACTS UP TO 824 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 335 or 1,675MILLION oz

CONFIRMED volume; ON TUESDAY 69,,071good//

AND NOW NOVEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 2913 X5,000 oz = 14.565 MILLION oz

to which we add the difference between the open interest for the front month of NOV (388) AND the number of notices served upon today (335 )x (5000 oz)

Thus the standings for silver for the NOVEMBER 2025 contract month: (2913) Notices served so far) x 5000 oz + OI for the front month of NOV(388 minus number of notices served upon today (335)x 5000 oz equals silver standing for the NOV.contract month equating to 14.83 MILLION OZ

New total standing: 14.83 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 157.503 million oz of registered silver

JPMorgan as a percentage of total silver: 205.650/481,457million. 42.75%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

NOV 4 WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

NOV 3 WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 1.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1039,20 TONNES

OCT 31 WITH GOLD DOWN $17.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1040.35 TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

OCT 23 WITH GOLD UP $78.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37 TONNES

OCT 22 WITH GOLD DOWN $78.95 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

GLD INVENTORY: 1038.63 TONNES, TONIGHTS TOTAL

SILVER

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 4 WITH SILVER DOWN $0.82 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

NOV 3 WITH SILVER $0.12 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 31 WITH SILVER DOWN $0.35 TODAY/SMALL CHANGES IN SILVER AT THE SLV: ///A WITHDRAWAL OF 636,000 OZ FROM THE SLV// ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

OCT 23 WITH SILVER UP $0.87 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 501.474 MILLION OZ

OCT 22 WITH SILVER DOWN $0.33 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.995 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 504.015 MILLION OZ

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

CLOSING INVENTORY 487.650 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD

US$’s liquidity crisis

The liquidity shortage is why the Fed is resuming QE. It might perpetuate the equity bubble for a few more months until bond yields start rising again. Maybe not.

| Alasdair MacleodNov 5∙Paid |

At the October FOMC meeting, the Fed Funds Rate was cut by ¼% to a new target rate between 3.75%—4.00%, and quantitative tightened was abandoned to be replaced by quantitative easing. Effectively, it was an admission that credit in the markets is too restrictive, which combined with the most recent Beige Book indicating that the economy might be stalling, was sufficient for the Fed to abandon inflation-targeting in favour of its other mandate — protecting employment.

Much has been written about the plumbing in the monetary system and why there is a liquidity crisis. But rationalising it, the credit liquidity problem is being triggered by US Treasury borrowing, which relies heavily on short-term financing. It is sucking liquidity out of markets.

Money market mutual funds (MMMFs) have grown to $6 trillion in the last year, and they can only invest in short-term US Treasury debt, which is overwhelmingly T-bills. Issuance of T-bills dominates the Treasury’s funding activities, illustrated in the graph below:

It should be noted that the high volumes of issuance include turnover, as bills with maturities of as little as two weeks being repeatedly rolled over. But note that the increase in MMMFs of some $900 billion in the last year is funding a significant portion of the Treasury’s new debt.

The origin of MMMFs is the deposit accounts of their investors at the commercial banks. Effectively, these deposits temporarily exit the banking system into the Treasury’s general account at the Fed, pending it being spent back into public circulation. An accumulation in the general account amounts to a net withdrawal of credit liquidity from the system. Since early September, the general account balance has increased by over $350 billion:

Together with the Fed’s quantitative tightening which reduces bank reserves at the Fed, you can see why the system is under a liquidity strain. And it explains why the Fed stopped QT.

The Fed reducing its funds rate in December won’t alleviate the credit crunch, which allowed Jay Powell to back off from definitely doing so. Instead, the Fed needs to inject liquidity into the system by resuming quantitative easing. By buying treasury debt off pension funds and similar institutional investors, cash is credited to their bank accounts at the Fed, and the banks in turn credit the accounts of the investors.

Further considerations

It is no coincidence that the last round of aggressive QE preceded a sudden and generally unexpected inflation spike. A new round, albeit unlikely to be nearly as aggressive is bound to push CPI inflation higher and bond yields with it.

Last time, the yield on the 10-year US Treasury note was already rising from its low of 0.5% by the end of the covid year (2020). And by the time the Fed stopped QE its yield had risen to 3%. The Fed was forced to continue raising its funds rate to 5.25%—5.5% for a further year, bankrupting some regional banks and pushing the S&P 500 down by 25%.

We are embarking on this route again. The question we need to ask ourselves, among others, is what are the consequences for the credit bubble and equity stock valuations? If, as seems certain bond yields and CPI inflation start rising as a consequence of the Fed’s monetary easing, then the bubble is bound to implode.

It is hardly surprising that given the post-covid experience of QE there is increasing nervousness in markets. The most extreme form of equity, which has no assets and no earnings, is already threatening to lose its bullishness. We refer, of course, to bitcoin:

Breaking down through its moving averages, an apparent loss of bullish momentum, and threatening to break under $100,000 is a very good indicator of the febrile sentiment in tech stocks generally, with which bitcoin correlates. But easier credit conditions could, in the short-term, encourage one last bullish fling of equities taking it into earlier next year, before the reality of rising bond yields begins to bite.

However, don’t bank on it. Talking of banking, we can begin to see why it is that senior commercial bankers are now talking gold higher. It’s their business to worry about these things, and they can see the fix that the Fed is in, and how there is no alternative to the destruction of the dollar’s purchasing power.

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 9.56 POINTS OR 0.23%

//Hang Seng CLOSED CLOSED DOWN 16.99PTS OR 0.07%

// Nikkei CLOSED : DOWN 1284,93 PTS OR 2.50% //Australia’s all ordinaries CLOSED DOWN 0.30%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.12075/ OFFSHORE CLOSED DOWN AT 7.1329/ Oil DOWNTO 60.20 dollars per barrel for WTI and BRENT DOWN TO 64.10 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING DOWNTO 7.1275/ OFFSHORE YUAN TRADING DOWN TO 7.1329:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1275

OFFSHORE YUAN: DOWN TO 7.1329

HANG SENG CLOSED DOWN 16.99 PTS OR 0.07%

2. Nikkei closed DOWN 1284.93 PTS OR 2.50%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 100.05 EURO RISE TO 1.1486 UP 2 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.657//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 153.84…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.075 DOWN 2 FULL BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP/JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD DOWNTO +2.65395/ Italian 10 Yr bond yield UP to 3.4010SPAIN 10 YR BOND YIELD UP TO 3.164

3i Greek 10 year bond yield UP TO 3.304

3j Gold at $3977.000 Silver at: 47.96 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 39 /100 roubles/dollar; ROUBLE AT 81.39

3m oil (WTI) into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 153.84 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.657% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.075 DOWN 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8104 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9309 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.093 DOWN 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.6760 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 3.582 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.10 UP 4 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.4445 UP 2PTS

30 YR UK BOND YIELD: 5.233 UP 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.1275 DOWN1 BASIS PTS

5 YR CANADA BOND YIELD: 2.703 DOWN 2BASIS PTS.

a New York OPENING REPORT

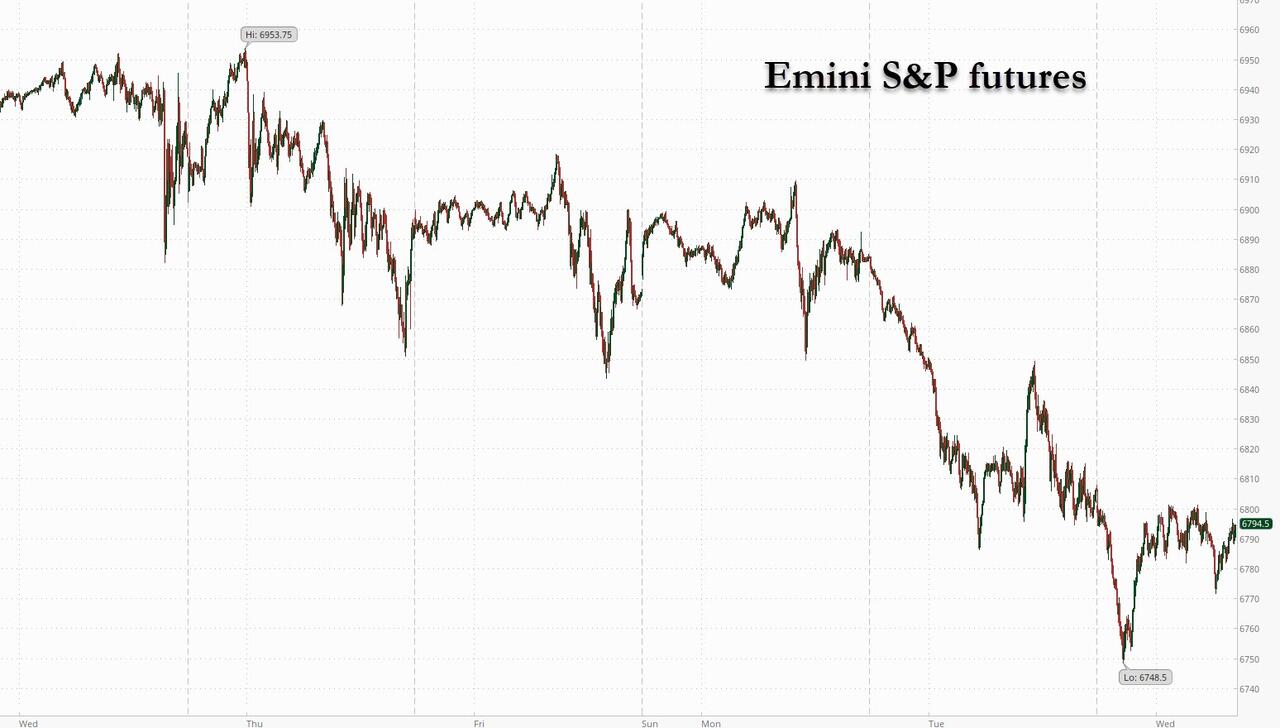

Futures Rebound From Session Lows As Government Shutdown Becomes Longest Ever

Wednesday, Nov 05, 2025 – 08:18 AM

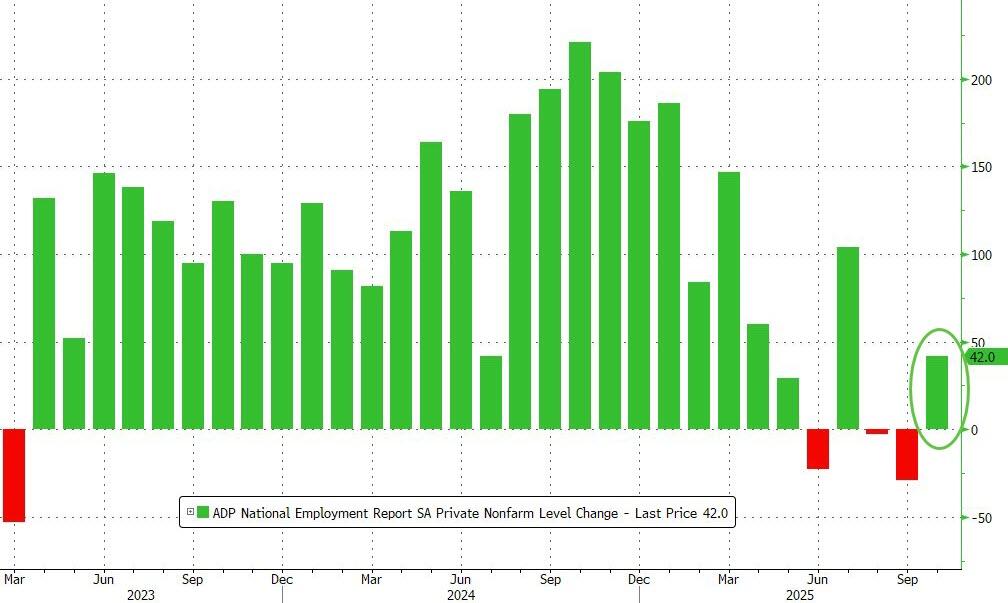

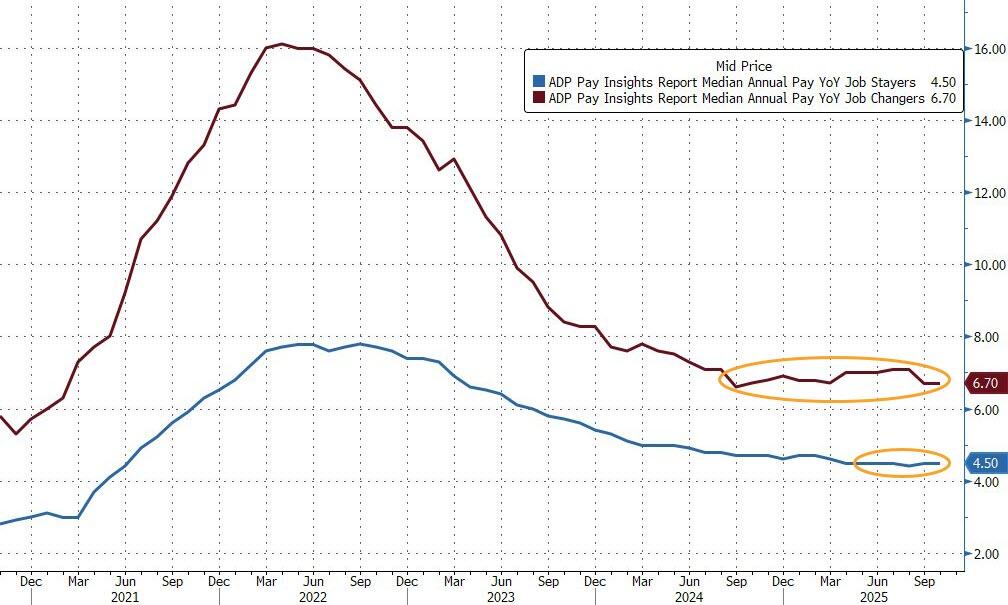

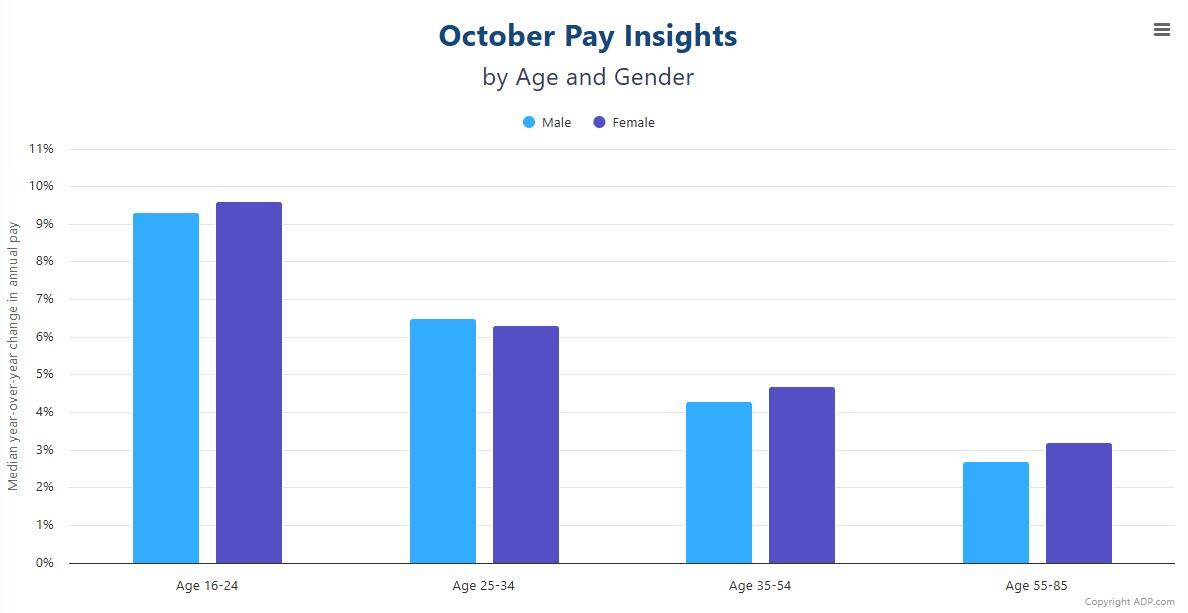

Welcome to day 36 of the government shutdown which officially makes it the longest shut down in history. Futures are trading moderately lower, following weaker Asian and European sessions, but well off session lows as Japan retraced nearly 50% of its losses during the session. As of 8:00am ET, S&P futures are down 0.2% having earlier slid far more following Tuesday’s 1.2% slump as technology shares dragged stocks lower globally; Nasdaq futures are down 0.1%, also recovering most of their losses. In premarket trading, Mag 7 stocks are mixed with Semis weaker. Confirming just how dented upward momentum is, many of the larger Tech companies that reported last night are weaker this morning. Both Cyclicals and Defensives are mixed without reflecting which will outperform today. According to JPM, so far yesterday’s price action has yet to spill over to the US session and the view that a valuation-induced sell-off with Tech underperforming was a narrative that was forming. It may be the case that as the market looks to remove froth that we see Mag7 outperform the higher beta segments of TMT / AI. In overnight news, China banned foreign-made chips in state-funded data centers. Bond yields are unchanged, erasing an earlier and the USD is also flat. Commodities are poised for a rebound with WTI, Precious Metals, and Ags all higher. Today’s macro data focus is on ADP and ISM-Srvcs. With the shutdown in Washington leaving a vacuum in official data, the private ADP employment numbers out today will get more attention than usual.

In premarket trading, Magnificent Seven stocks are mixed (Tesla +1.2%, Meta +0.3%, Apple -0.05%, Microsoft -0.1%, Alphabet -0.1%, Amazon -0.2%, Nvidia -0.7%)

- AMD (AMD) falls 4% after the chipmaker reported its third-quarter results and gave an outlook. While analysts are broadly positive, they note some issues with margins and the outlook. The stock has more than doubled this year.

- Arista Networks (ANET) slides 10% after the company’s forecast for adjusted gross margin in the fourth quarter fell short of the average analyst estimate.

- Axon (AXON) drops 18% after the Taser maker reported disappointing third-quarter adjusted EPS and agreed to buy emergency-tech company Carbyne in a deal valuing the company at $625 million.

- Biohaven (BHVN) tumbles 44% as TD Cowen calls the FDA’s Vyglxia Complete Response Letter as “highly disappointing” amid broader concerns over its impact on the firm’s R&D spending.

- Clover Health (CLOV) sinks 20% after the health insurer cut its adjusted Ebitda guidance for the full year, following third-quarter adjusted Ebitda results that fell short of expectations. The company notes high medical costs in the quarter pressured margins.

- Humana (HUM) falls 5% after the health insurer reaffirmed its forecast for medical costs for the full year, with the outlook below the average analyst estimate. The firm also reported higher medical costs for the third quarter than analysts anticipated.

- Kennedy-Wilson (KW) surges 26% after receiving a buyout proposal letter from CEO William McMorrow and Fairfax Financial Holdings to acquire all outstanding common stock.

- Kratos (KTOS) falls 8% after the defense contractor forecast revenue and adjusted Ebitda for the fourth quarter that missed the average analyst estimate.

- Mosaic (MOS) shares are up 5% after the agricultural chemicals company reported adjusted earnings per share for the third quarter that beat the average analyst estimate.

- Pinterest (PINS) is down 18% after the search platform gave a revenue outlook that is weaker than expected.

- Super Micro Computer Inc. (SMCI) falls 7% after the server maker missed reduced estimates for first-quarter sales and profit and gave a disappointing earnings forecast for the current period, reinforcing concerns about its ability to capitalize on demand for AI equipment.

- Toast (TOST) gains 3% after the restaurant software company reported third-quarter results that beat expectations and raised its full-year forecast for adjusted Ebitda.

- Trex (TREX) sinks 33% after the maker of decking products forecast net sales for the fourth quarter that fell short of the average analyst estimate.

- United Parcel Service Inc. (UPS) slips 1.8% after one of its freighter jets crashed and exploded shortly after takeoff on Tuesday from Louisville, Kentucky, killing three crew members and at least four people on the ground.

- Upstart (UPST) falls 13% after the AI lending marketplace reported third-quarter revenue that missed expectations and lowered its full-year revenue forecast.

In corporate news, Google and Fortnite game maker Epic Games reached a settlement in their long-running antitrust fight over how developers distribute and monetize apps on Android phones. A UPS freighter jet crashed and exploded shortly after takeoff from Louisville, Kentucky, killing at least seven people. Toyota’s annual profit guidance disappointed investors, a sign that the impacts of US tariffs are still weighing on its bottom line. Amazon.com is suing Perplexity AI to try and stop the startup from helping users buy items on the world’s largest online marketplace.

The VIX jumped to 19 on Tuesday but there’s no sign of panic so far in derivatives markets with the gauge holding under 20, with some 25/30 call spread buying, a likely hedge into year-end playing a moderate rise in volatility.

“There has been way more nervousness than usual during the last rally, and that’s not a good sign,” said Alexandre Baradez, chief market analyst at IG in Paris. “The market was priced for perfection so that explains why emerging questions about rate cuts, liquidity, and valuations are having such an impact.”

Crypto markets offered an early warning signal on the recent liquidity rush, with Bitcoin about 20% below a record high reached a month ago — before paring some of those losses in Wednesday trading. Holders of the cryptocurrency have offloaded around 400,000 Bitcoin over the past month, an exodus of about $45 billion that’s left the market unbalanced.

Meanwhile, the US government has reached a major milestone of dysfunction, with the federal shutdown now the longest in history — and economic pain is deepening. The CBO estimates 4Q growth could be cut by as much as 2 percentage points if the impasse continues for eight weeks.

In politics, Democrats landed a series of local election wins. Zohran Mamdani was elected the 111th Mayor of New York, and his proposals and inexperience — he’s sponsored only a handful of bills while serving three terms as a state assemblyman — is said to have unnerved business leaders and real estate groups.

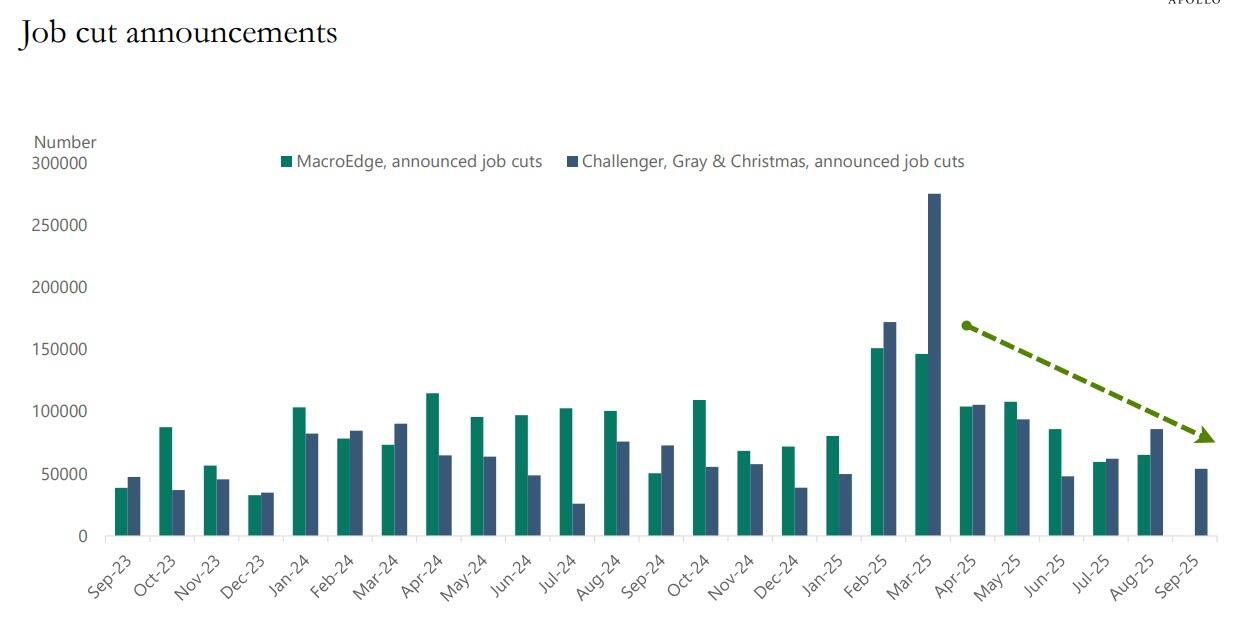

ADP jobs data today comes in the face of recent corporate cutbacks which economists fear may be a warning sign, with companies such as Starbucks, Target, and Amazon making significant job cuts.

Turning to earnings, by Tuesday night, three-quarters of S&P 500 companies had reported results this season with a positive surprise ratio of 82% — similar to 2Q, which was the highest beat percentage since the third quarter of 2021. Price reaction to AI-related earnings remains volatile, with AMD falling despite lifting guidance, perhaps reflecting elevated buyside expectations. Other AI-related names to fall on results include Tempus AI, Super Micro Computer and Arista Networks.

Emerson Electric, FIS, Humana, McDonald’s, Unity Software and Zimmer Biomet are among companies expected to report results before the market opens. Sales growth at McDonald’s is expected to accelerate to 3.6% from a 1.5% drop last year, as its enhanced value offerings resonate with consumers. Earnings from AppLovin, DoorDash, ARM, Duolingo, Figma, Fortinet, Robinhood, Qualcomm and Lyft follow later in the day.

European stocks fall for a second day, though with less severity than seen earlier in Asia. Stoxx 600 down by 0.5% with tech stocks underperforming on a drag from ASML. That followed weakness in chip stocks in the US and drops for the tech-heavy Nikkei 225 in Japan and Kospi in Korea. Here are some of the biggest movers on Wednesday:

- Barry Callebaut climbs as much as 7.8% following results on Wednesday, with analysts noting its “sober” outlook, but Vontobel saying the chocolate product manufacturer is at least setting more realistic goals.

- Vestas gains as much as 15% after the Danish wind-power manufacturer reported a strong set of earnings, with analysts highlighting outperformance for its Power Solutions division, with a new and unexpected buyback program welcome.

- Aixtron shares climb as much as 7.6%. Demand for power from AI infrastructure could drive growth at the semiconductor equipment manufacturer, according to Barclays, which upgraded the stock to overweight from equal-weight.

- Ahold Delhaize shares rise 4.6% as the retailer reported adjusted operating profit for the third quarter that beat the average analyst estimate.

- Demant gains as much as 7.6%, despite the firm saying it now expects full-year organic sales growth to come in toward the lower end of its existing 1%-3% guidance range.

- Novo shares fluctuate in morning trading before rising as much as 2.7%. The Danish drugmaker narrowed its sales guidance for the year, while its commentary around negotiated US Medicare pricing was better than expected, according to analysts.

- Ambu slumps as much as 19%, the most in three years, after the Danish health-care equipment company reported its latest earnings. JPMorgan sees a miss to 4Q estimates, and new 2026 guidance implies large cuts to Ebit consensus expectations.

- Siemens Healthineers falls as much as 13%, the most on record, after the German health-care equipment group reported earnings which analysts describe as a disappointment.

- Pandora shares fall as much as 5.2% after the jewellery manufacturer lowered guidance for 2025 like-for-like growth and its 2026 EBIT margin target, and reported revenue for the third quarter that missed the average analyst estimate.

- Nexi shares fall as much as 9.9% after the third-quarter operating revenue of the payment services provider missed estimates.

- Qiagen drops as much as 4.4% in Frankfurt as Morgan Stanley says the German life science and diagnostics firm’s fourth-quarter growth outlook potentially overshadows decent third-quarter results.

- Evotec shares fall as much as 12% after the German company reported results RBC called “dismal” with revenue and Ebitda significantly below consensus estimates.

Earlier in the session, Asian stocks fell, weighed by a selloff in tech shares amid mounting concerns over excessive valuations. The MSCI Asia Pacific Index dropped as much as 2.3%, before trimming some losses on dip-buying. Tech heavyweights TSMC, SoftBank and Samsung Electronics were among the biggest drags. Most markets were in the red, with Japan and South Korea leading the losses. The selloff follows Wall Street chiefs’ warnings about an overdue correction, while fading expectations for Federal Reserve rate cuts and the prolonged US government shutdown also contribute to the risk-off sentiment. South Korea’s equity benchmark Kospi Index finished 2.9% lower — narrowing earlier losses of as much as 6.2% — marking its steepest daily decline since August. Japan’s blue-chip Nikkei 225 gauge also pared a plunge of 4.7% to close 2.5% lower, while the broader Topix Index fell 1.3%. China’s benchmark CSI 300 Index reversed early losses to end the day in the green, helped by solid gains in solar stocks. Indonesia also posted mild gains. Markets in India were closed for a holiday.

In FX, the Bloomberg Dollar Spot Index is in a narrow range but has reversed an earlier decline. Sterling an outperformer, Swedish krona in the middle of the pack in the G-10 after the Riksbank held rates at a three-year low.

In rates, we are seeing muted moves in bond markets, with US Treasury yields little changed amid similarly muted price action in German bonds, while long-end gilts underperform slightly. US 10-year is lower by less than 1bp near 4.08% with German counterpart similar and UK’s lagging by around 1bp. Treasury 5s30s curve is around 1bp steeper on the day. Focal points of US session focus include October ADP employment change and services PMIs, as well as Treasury quarterly refunding announcement at 8:30am New York time. For the US Treasury’s quarterly refunding announcement, dealers expect two- to 30-year auction sizes will be unchanged during the November-to-January period

IG dollar issuance slate includes at least two offerings so far. Three borrowers raised a combined $2.85b Wednesday. Issuers paid about 12bps of concession on deals that were 2.9 times covered.

In commodities, gold is higher by $34 to around $3,964/oz. Oil prices up, Brent futures heading closer to $65/barrel. Bitcoin briefly fell below $100,000, though is now holding just above that level.

US economic calendar slate includes October ADP employment change (8:15am), October S&P Global US services PMI (9:45am) and October ISM services index (10am). Fed speaker slate empty for the session

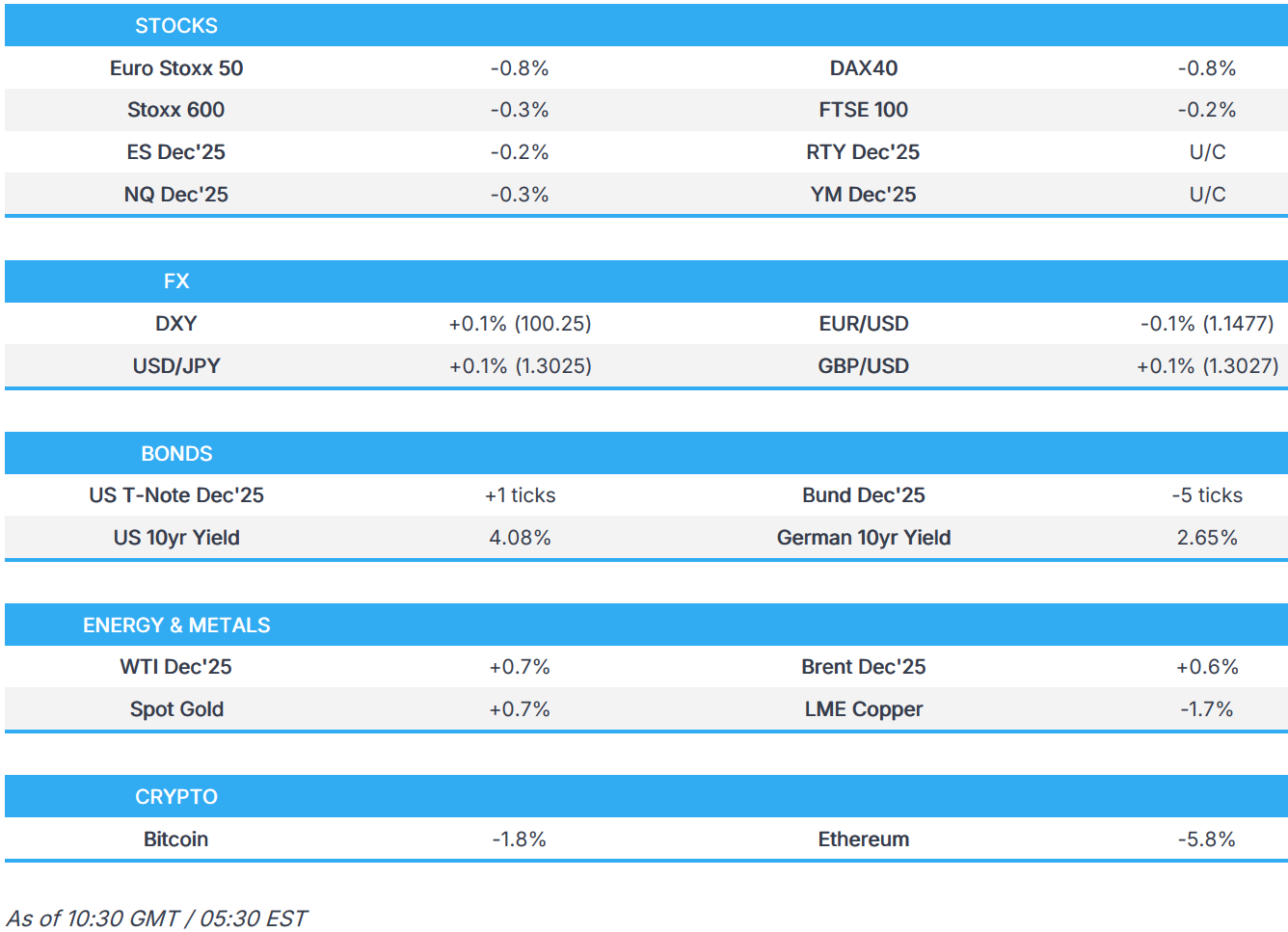

Market Snapshot

- S&P 500 mini -0.2%

- Nasdaq 100 mini -0.1%

- Russell 2000 mini little changed

- Stoxx Europe 600 -0.4%

- DAX -0.7%

- CAC 40 -0.2%

- 10-year Treasury yield little changed at 4.09%

- VIX +0.5 points at 19.54

- Bloomberg Dollar Index little changed at 1226.45

- euro little changed at $1.148

- WTI crude +0.7% at $61/barrel

Top overnight News

- The government shutdown dragged into its 36th day becoming the longest in history. Every week that passes with Congress deadlocked costs the US economy between $10 billion to $30 billion, according to analysts’ estimates, with several landing in the $15 billion range. BBG

- A “handful” of moderate Senate Democrats are considering voting to end the government shutdown. The deal would pass three full-year appropriations bills to fund some agencies, along with a short-term bill that would reopen the rest of the government: WaPo

- Democrat Mikie Sherrill won the New Jersey Governor election and Democrat Abigail Spanberger won the Virginia Governor election, while Democrat Zohran Mamdani won the New York mayoral election.

- In addition to Mamdani’s victor in New York, Democrats also scored other victories throughout the country. The party won gubernatorial races in New Jersey and Virginia around a message of economic affordability. California voters approved a new congressional map intended to create five new Democratic-leaning districts. BBG

- New Yorkers squeezed by the city’s housing crunch also voted in favor of proposals to fast-track affordable housing projects, expedite modest developments and create an appeals board, vote tallies recorded by the AP and the NYT showed. BBG

- The Chinese government has issued guidance requiring new data center projects that have received any state funds to only use domestically-made artificial intelligence chips. Order likely to affect U.S. chipmakers Nvidia, AMD, Intel as Beijing tries to cultivate domestic AI chipmakers like Huawei. RTRS

- Japan’s top currency official, Atsushi Mimura, said recent moves by the yen are deviating from what might be expected given interest rate differentials. The yen touched an eight-month low against the dollar after the BOJ left rates unchanged, despite subtle hints of a potential hike from Governor Kazuo Ueda. BBG

- A growing number of policymakers at the Bank of Japan believed that conditions were falling into place for interest rates to rise, with two members advocating an immediate increase, minutes of the central bank’s September meeting showed on Wednesday. RTRS