access market

GOLD $4194.80 (3:30 PM)

SILVER: 53.52 3;30 PM

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XGE: COMEX

099 H DEUTSCHE BANK AG 2

190 H BMO CAPITAL MARKETS 318

363 H WELLS FARGO SECURITI 126

435 H SCOTIA CAPITAL (USA) 44

661 C JP MORGAN SECURITIES 58

686 C STONEX FINANCIAL INC 1

880 H CITIGROUP 500

905 C ADM 47

GOLD: NUMBER OF NOTICES FILED FOR NOV/2025: 548 CONTRACTs NOTICES FOR 54,800 OZ or 1.7045 TONNES

total notices so far: 7832 contracts for 783,200 OR 24.340 tonnes)

SILVER NOTICES: 55 NOTICE(S) FILED FOR 275,000 OZ/

total number of notices filed so far this month : 3132 CONTRACTS (NOTICES) for 15.680 million oz

INITIAL STANDING FOR NOV: 11.575 MILLION OZ

PLUS INITIAL 1.245 MILLION OZ QUEUE JUMP

THEN ADD TUESDAY;S 1,93 MILLION OZ QUEUE JUMP

THEN WEDNESDAY;S 0.570 MILLION OZ QUEUE JUMP

THEN 0.080 MILLION OZ

THEN MONDAY’S 425,000 0Z

THEN TUESDAY: 275,000 OZ

THEN TODAY;S 295,000

EQUALS

15.975 MILLION OZ STANDING FOR SILVER.

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOV: 11.165 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

AND NOW NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY;S QUEUE JUMP OF 0.295 MILLION OZ WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 4.95 MILLION OZ//STANDING ADVANCES TO 15.975 MILLION OZ/

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 1.707 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 7.5511 TONNES//NEW STANDING ADVANCES TO 24.824 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 32.037 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 954 CONTRACTS OI TO 160,603 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 374 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 374 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1311 CONTRACTS AND ADD TO THE 374 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 1328 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $0.63 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 6.640 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.63

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED DOWN 2.62 POINTS OR 0.07%

//Hang Seng CLOSED CLOSED UP 226.32 PTS OR 0.85%

// Nikkei CLOSED : UP 220.38 PTS OR 0.43% //Australia’s all ordinaries CLOSED DOWN 0.21%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1175/ OFFSHORE CLOSED UP AT 7.1205/ Oil DOWN TO 60.43 dollars per barrel for WTI and BRENT DOWN TO 64.55 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING UP TO 7.1175 OFFSHORE YUAN TRADING UP TO 7.1205:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED SIZED 6034 CONTRACTS TO 466,031 OI DESPITE THE SMALL LOSS IN PRICE OF $3.80 WITH RESPECT TO TUESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST NO NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2065). WE HAD ZERO T.A.S. LIQUIDATION TUESDAY. HOWEVER IT WAS THE MAJOR SPECULATORS THAT CONTINUALLY WENT MASSIVELY LONG AGAIN AND THE BANKERS WHO TOOK THE SHORT SIDE SUPPLYING THE NECESSARY PAPER.

WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 8049 CONTRACTS (OR 25.19TONNES).THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

EXCHANGE FOR PHYSICAL//GOLD ISSUANCE//OCTOBER:

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT FOR GOLD REMAINS AT 14.553 TONNES OF GOLD UNDER THE GUIDANCE OF 6 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FINAL

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 130.3TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 54 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES IN AUGUST AND THEN ADDED 24 TONNES IN SEPT. AND THUS THEIR SHORTFALL TO THE BIS IS 54 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 130.3 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW NOVEMBER COMEX MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 8034 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT/EARLY NOVEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS ANOTHER MEGA HUGE SIZED T.A.S ISSUANCE CONTRACTS AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 20,344 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEKS HUGE RAIDS, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS WE WE WILL PROBABLY SEE GOLD//SILVER RISE HUGELY ON OUR UPCOMING DAYS. THIS IS THE 3RD DAY IN A ROW FOR A HUGE T.A.S. ISSUANCE!!

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS:

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE FINISHING OPTION EXPIRY WEEK, THE CROOKS GOADED OUR SPECULATORS TO CONTINUE ONTO THE SHORT SIDE WITH THE BANKERS ON THE LONG SIDE…THE RAIDS THROUGHT THIS WEEK WERE FREQUENT BUT FAILED TO CAUSE ANY DAMAGE TO THE PRICE WITH OPTIONS EXPIRY FINISHING OCT 31 AS WE NOW ENTER OUR MONTH OF NOVEMBER WITH FAILED RAID ATTEMPTS

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

AND NOW NOVEMBER:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 1.707TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 7.5511 TONNES/NEW STANDING ADVANCES TO 24.824 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 54+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 24 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 54 TONNES REMAIN ON THE BOOKS OF THE BIS.

THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING E.G. NOVEMBER: A HUGE INITIAL 15.651 TONNES STANDING IN AN OFF MONTH!! THIS IS HUGE!!!//WITH QUEUE JUMPS NOW AT 24.824 TONNES

EXCHANGE FOR PHYSICAL ISSUANCE/NOV//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 2065 CONTRACTS.

THAT IS A FAIR SIZED 2065 EFP CONTRACT WAS ISSUED: : /DEC 725 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2065 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 54 TONNES

WE HAD :

- ZER0 LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY + GOVERNMENT LIQUIDATION AND CONSIDERABLE LIQUIDATION THIS EARLY WEDNESDAY MORNING!!!

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE OCT 31 WITH OUR ATTEMPTED FAILED RAID,

T.A.S.SPREADER ISSUANCE//NOV

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A HUGE SIZED SIZED 20,344 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP TUESDAY’S SMALL LOSS IN PRICE IN GOLD WITH A CORRESPONDING STRONG GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

AND NOW NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF1.707 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 7.5511 TONNES

/STANDING ADVANCES TO 24.824TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING NOVEMBER,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $3.80/ /) BUT WERE UNUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A MEGA MEGA HUGE GAIN IN OI FROM TWO EXCHANGES OF 24,862 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION TUESDAY COMEX TRADING BUT CONSIDERABLE LIQUIDATION THIS EARLY WEDNESDAY MORNING. HOWEVER WE DID HAVE AGAIN HUGE SPECULATOR SHORT COVERING TUESDAY AS THEY ARE THE ONES WHO WERE MASSIVELY SHORT ALL LAST WEEK AS OTHER CENTRAL BANKERS WENT MASSIVELY LONG . THOSE OTHER CENTRAL BANKERS TENDERED FOR PHYSICAL LAST NIGHT. THE COMEX IS ONE BIG MESS!! THIS WEEK, THE BANKERS (FRBNY) ARE ON THE SHORT SIDE AND SPECS ON THE LONG SIDE AND THEY WERE RINSED OUT QUITE NICELY BY THE FRBNY BANKERS USING THEIR NEWFOUND T.A.S. CONTRACTS LATE TUESDAY NIGHT EARLY WEDNESDAY MORNING.

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL

AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 1.707 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 7.5511 TONNES

NEW STANDING ADVANCES TO 24.824 ONNES OF GOLD.

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $3.80

WE HAD A HUGE AND 2ND HIGHEST EVER RECORDED AT 16,763 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

INITIAL GOLD COMEX

NOV 12

NOV CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES i) Out of Malca: 31,540.136 oz 981 tonnes total withdrawal: 31,540.136 oz .981 TONNES |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 548 notice(s) 54,800 OZ 1.7045TONNES OF GOLD |

| No of oz to be served (notices) | 149 contracts 14,900 OZ 0.4624 TONNES |

| Total monthly oz gold served (contracts) so far this month | 7832notices 783,200 0z 24.360 ONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

1 ENTRIES

i) Out of Malca: 31,540.136 oz

981 tonnes

total withdrawal: 31,540.136 oz

.981 TONNES

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1

Dealer to customer

a) Brinks 283,376.724 oz

volume at the comex: TUESDAY: 326,838 oz ( strong)//

AMOUNT OF GOLD STANDING FOR NOVEMBER:

THE FRONT MONTH OF NOV STANDS AT 697 CONTRACTS FOR A GAIN OF 385 CONTRACTS.

WE HAD 165 CONTRACTS SERVED ON TUESDAY. SO WE GAINED A STRONG 550 CONTRACTS FOR 55,000 OZ OF GOLD (1.7107 TONNES).

DECEMBER LOST 13,785 CONTRACTS DOWN TO 278,065 CONTRACTS .

JANUARY GAINED 77 CONTRACTS UPTO 925

We had 548 contracts filed for today representing 54,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 00 notices issued from their client or customer account. The total of all issuance by all participants equate to 548 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 58 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2025. contract month, we take the total number of notices filed so far for the month (7832 oz ) to which we add the difference between the open interest for the front month of NOV ( 697 CONTRACTS) minus the number of notices served upon today (548x 100 oz per contract) equals 798,100 OZ OR 24.824 ONNES OF GOLD

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (7832x 100 oz +we add the difference for front month of NOV (697 OI} minus the number of notices served upon today (548)x 100 oz) which equals 798,100 OZ OR 24.824 TONNES

TOTAL COMEX GOLD STANDING FOR NOV..: 24.824 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE ACTIVE DELIVERY MONTH OF NOVEMBER

volumeMONIDAY confirmed 247,772 contracts ok

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,756,376.330 oz 54.63tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 37,543,598.451 oz

TOTAL REGISTERED GOLD 19,330,565.467 or 601.26onnes

TOTAL OF ALL ELIGIBLE GOLD 18,213,053.984 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,574,189 oz ((REG GOLD- PLEDGED GOLD)=

546.63 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE NOV. 2025 SILVER CONTRACTS

NOV 12 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out CNT 598,605.607 oz ii) Out of Delaware 3938.890 oz iii) Out of JPMorgan: 305,481.300 oz iv) Out of Loomis 602,878.990 oz total withdrawal 1,510,905.267 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 2 entries i) Into CNT 547,419.960 oz ii) Into Loomis 597,298.780 oz total deposit 1,144,718.740 oz |

| No of oz served today (contracts) | 55 CONTRACT(S) ( 0.275 MILLION OZ |

| No of oz to be served (notices) | 59 contracts (0.295MILLION oz) |

| Total monthly oz silver served (contracts) | 3136Contracts (15.680 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 entries

i) Into CNT 547,419.960 oz

ii) Into Loomis 597,298.780 oz

total deposit 1,144,718.740 oz

`

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

4 entries

i) Out CNT 598,605.607 oz

ii) Out of Delaware 3938.890 oz

iii) Out of JPMorgan: 305,481.300 oz

iv) Out of Loomis 602,878.990 oz

total withdrawal 1,510,905.267 oz

adjustments: 1:

dealer to customer

a) Brinks 289,657.680 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 156.106 MILLION OZ//.TOTAL REG + ELIGIBLE. 478.191 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF NOVEMBER /2025 OI: 114 OPEN INTEREST CONTRACTS FOR A GAIN OF 7 CONTRACTS. WE HAD 52 NOTICES SERVED ON TUESDAY SO WE GAINED 59 OR 0.295MILLION OZ QUEUE JUMP.

DECEMBER LOST 5753 CONTRACTS DOWN TO 88,600

JANUARY LOST 62 CONTRACTS UP TO 835 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 55 or 0.275 MILLION oz

CONFIRMED volume; ON TUESDAY 98,397 huge//

AND NOW NOVEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 3136 X5,000 oz = 15.680MILLION oz

to which we add the difference between the open interest for the front month of NOV (114) AND the number of notices served upon today (55 )x (5000 oz)

Thus the standings for silver for the NOVEMBER 2025 contract month: (3136) Notices served so far) x 5000 oz + OI for the front month of NOV(114) minus number of notices served upon today (55)x 5000 oz equals silver standing for the NOV.contract month equating to 15.975 MILLION OZ

New total standing: 15.975million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 156.106 million oz of registered silver

JPMorgan as a percentage of total silver: 204.056/478.191million. 42.67%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1046.36 TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

NOV 3 WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 1.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1039,20 TONNES

OCT 31 WITH GOLD DOWN $17.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1040.35 TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

OCT 23 WITH GOLD UP $78.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37 TONNES

OCT 22 WITH GOLD DOWN $78.95 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

GLD INVENTORY: 1046.36 TONNES, TONIGHTS TOTAL

SILVER

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 4 WITH SILVER DOWN $0.82 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

NOV 3 WITH SILVER $0.12 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 31 WITH SILVER DOWN $0.35 TODAY/SMALL CHANGES IN SILVER AT THE SLV: ///A WITHDRAWAL OF 636,000 OZ FROM THE SLV// ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

OCT 23 WITH SILVER UP $0.87 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 501.474 MILLION OZ

OCT 22 WITH SILVER DOWN $0.33 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.995 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 504.015 MILLION OZ

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

CLOSING INVENTORY 485.110 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

Recession Watch: Spooked For Good Reasons

| John RubinoNov 12 |

A widely-followed consumer sentiment index just hit its second-worst level on record:

Why are Americans so spooked? Perhaps it’s the prospect of being replaced by AI. So far in 2025, major layoff announcements include:

- Amazon: 14,000 job cuts

- UPS: 48,000

- Intel: 20,000

- Microsoft: 6,000

- Target: 1,800

- Meta: 600 (from its AI division!)

- Salesforce: 4,000

Or maybe it’s that student loan payments have resumed, and for some, it’s one bill too many. See the red line on the following chart:

Or maybe it’s those “car mortgages” that were so popular for a while:

Here Come The Stimmy Checks

With busts looming on multiple fronts, how far off can some form of bailout be? Not far at all, apparently:

Trump floats $2,000 tariff rebate checks: Here’s what you need to know

(CNBC) – Over the weekend, President Donald Trump suggested paying Americans directly for their health-care costs and sending tariff rebate checks to families, not unlike the stimulus payments issued during the Covid-19 pandemic.

In a Truth Social post on Saturday, Trump wrote, “Republicans should give money DIRECTLY to your personal HEALTH SAVINGS ACCOUNTS.”

The president also floated the idea that a tariff “dividend” was possible. “A dividend of at least $2000 a person (not including high income people!) will be paid to everyone,” he wrote in another post Sunday on Truth Social.

Panic Time

Stimmy checks are the most blatant and least effective tool for managing an overindebted economy. They are, however, a good way to telegraph panic in a way that smart investors can understand. Keep stacking:

You’re currently a free subscriber to John Rubino’s Substack. For the full experience, upgrade your subscription.

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS /248 AND 247

The Problem Of The Meatpackers

JEFFREY TUCKER…

Wednesday, Nov 12, 2025 – 11:05 AM

Authored by Jeffrey Tucker via The Epoch Times,

President Trump is boldly facing the problem of high meat prices but also dealing with the financial strains on farmers themselves.

The issue is reconciling the two.

Lower prices are great for consumers but also add to the financial problems of small farmers.

Gradually, Trump has come to the conclusion that the real bottleneck is with meatpackers themselves, which is one of the oldest corporate monopolies in U.S. history.

He has posted the following:

“I have asked the DOJ to immediately begin an investigation into the Meat Packing Companies who are driving up the price of Beef through Illicit Collusion, Price Fixing, and Price Manipulation. We will always protect our American Ranchers, and they are being blamed for what is being done by Majority Foreign Owned Meat Packers, who artificially inflate prices, and jeopardize the security of our Nation’s food supply. Action must be taken immediately to protect Consumers, combat Illegal Monopolies, and ensure these Corporations are not criminally profiting at the expense of the American People. I am asking the DOJ to act expeditiously. Thank you for your attention to this matter!”

With this posting, he has put his finger on the problem. Rep Thomas Massie (R-Ky.) points out that “Four meat packers control 85 percent of the meat processed in the U.S.”

Immediately, however, friends of mine in the free-market movement cried foul. He is blaming private enterprise whereas these corporations should be left alone by government to do whatever they want. They treated Trump’s call for intervention as some kind of imposition of government force on the freedom of commerce.

Who is correct here?

Once you understand the history, which goes very deep, you can see that Trump has hit an important point.

The meatpacking industry has been consolidating since the 1880s. This was codified with the Pure Food and Drug Act signed into law by President Theodore Roosevelt in 1906, alongside the Meat Inspection Act.

It was the first federal law to regulate food and pharmaceutical products. It not only prohibited the manufacture, sale, or transportation of adulterated or misbranded food, drugs, medicines, and liquors, it forced inspection on all U.S. meat processing and laid the foundation for the modern Food and Drug Administration, or FDA. It thereby created or really codified the meat cartel in America, something that has vexed small meat producers ever since.

Part of the reason for the lack of understanding here traces to a false historical understanding.

In the conventional historiography, Upton Sinclair wrote the novel called “The Jungle” that exposed the evils of the industry. As a result, Congress intervened to clean up the industry with new regulations. This became the headline legislation and event that set the agenda for the construction of the entire regulatory state in the United States.

The trouble is that this history is not true. It’s a fable.

The real story was told by Murray Rothbard and many other economic historians. Keep in mind that meatpacking as an industry separate from farming and ranching was a relatively new development. Traditionally, the industry was vertically integrated such that the people who raised the animals also slaughtered and processed them. The meatpackers and processors were attempting to replace these traditional practices. There is nothing wrong with that except that they used government power to unfairly tilt the scales in their favor.

The problems began in the 1880s when meatpackers sought to penetrate European markets. Imports were banned because the Europeans did not trust the quality. The industry then went to the government to certify the cleanliness and safety of their meat. The scheme worked and set forth a model for a different kind of competition. Industry would unite with government as a way of assuring consumers and also driving up the costs of entry into markets such that small processing could not afford them.

As Rothbard writes:

“In February 1906, Upton Sinclair’s The Jungle was published and revealed many alleged horrors of the meat packing industry. Shortly thereafter, Roosevelt sent two Washington bureaucrats, Commissioner of Labor Charles P. Neill and civil service lawyer James B. Reynolds, to investigate the Chicago industry. The famous ‘Neill-Reynolds’ report that apparently confirmed Sinclair’s findings, in fact, only revealed the ignorance of the officials, as later congressional hearings indicated that they poorly understood how slaughterhouses worked and confused their inherently foul nature with unsanitary conditions.”

After “The Jungle” came out, J. Ogden Armour, owner of one of the biggest packing firms, defended government inspection of meat and said that the large packers had always favored and pushed for inspection. Armour wrote:

“Attempt to evade it [government inspection] would be, from the purely commercial viewpoint, suicidal. No packer can do an interstate or export business without Government inspection. Self-interest forces him to make use of it. Self-interest likewise demands that he shall not receive meats or by-products from any small packer, either for export or other use, unless that small packer’s plant is also ‘official’—that is, under United States Government inspection.”

There you have it. The big players in the industry actually favored government intervention.

Thomas E. Wilson, representing the large Chicago packers, said the following during the Congressional debate: “We are now and have always been in favor of the extension of the inspection, also to the adoption of the sanitary regulations that will insure the very best possible conditions. … We have always felt that Government inspection, under proper regulations, was an advantage to the live stock and agricultural interests and to the consumer.”

Imagine, that was 120 years ago, and we are still dealing with the same problem. No meat can be sold to the consumer without being processed by a plant certified by the U.S. Department of Agriculture. Even the quality of meats on the shelves are named according to official processing: USDA Prime, USDA Choice, and so on.

This has gradually put enormous pressure on small farmers who have to pay exorbitant prices for processing, when cheaper alternatives are readily available. Most small farmers would love to process their own meat on site and sell it directly to the consumers. But federal law forbids them from doing so. This has been true since 1906 and remains true today. The devastating results are the crisis we see today.

What about the issue of safety? Federal regulation did nothing to improve it and much to degrade it. They used the “poke and sniff” method to investigate safety, and did so for decades after, even though this method was known to spread pathogens from one carcass to another. It would have been much safer without federal intervention.

I’m thrilled and surprised that we are finally getting some discussion of this important topic today. The meat cartel certainly needs to be broken up. But the best method of doing so is simply to dismantle the regulatory impediments to competition. Farmers should be allowed to process and sell meat in any way that is advantageous to them. You would think that this would be an easy sell in Congress.

Part of the reason this topic is so triggering is that people do not understand the real history of the U.S. meat industry. If people did understand, it would become much clearer how it is that so many federal agencies are captured by industry interests. Indeed, capture might be the wrong word. They were set up to help big business in the first place. Helping small business instead requires the real restoration of a genuine free market.

END

COFFEE BANANAS

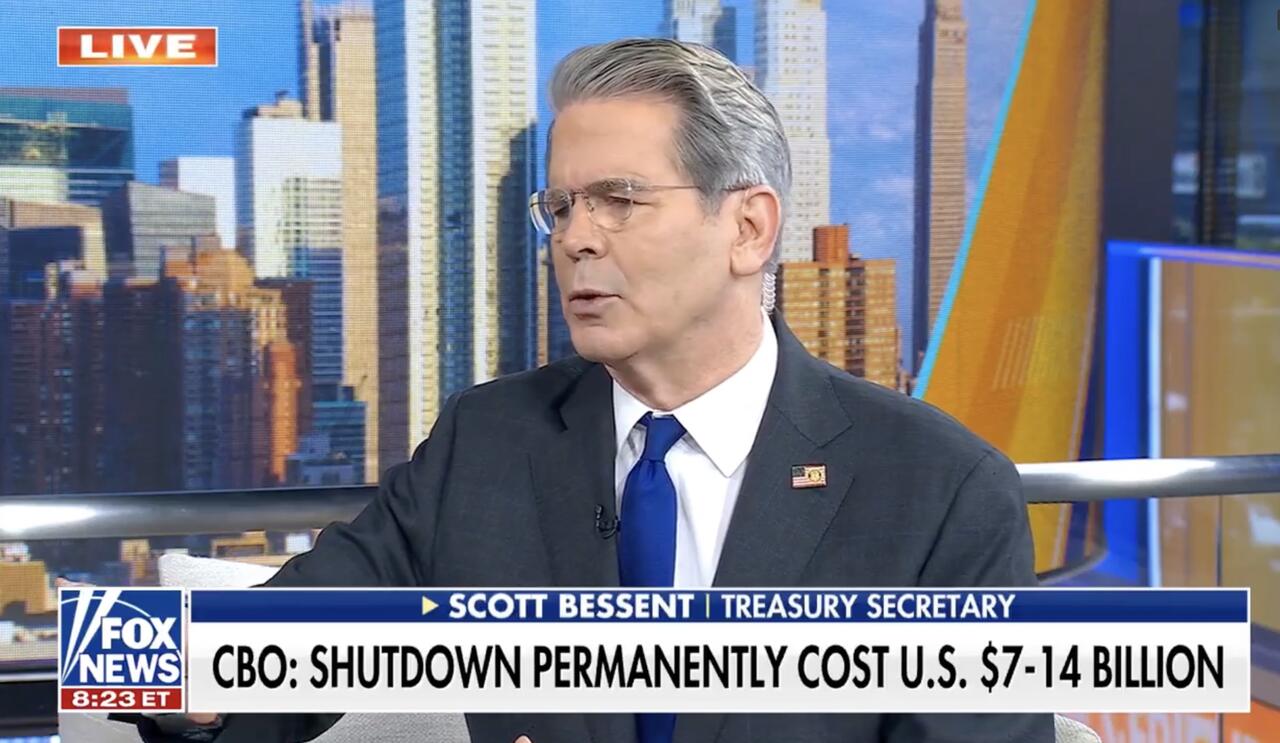

Bessent: Major U.S. Moves Coming To Cut Coffee And Food Prices

Wednesday, Nov 12, 2025 – 03:20 PM

U.S. Treasury Secretary Scott Bessent said Americans can expect “substantial announcements” in the coming days aimed at cutting prices on imported products such as coffee, bananas, and other goods not produced in the United States. Speaking on Fox and Friends, he explained that these steps would bring prices down “very quickly” and predicted that “people would start feeling better about the economy in the first half of 2026.”

The comments followed a steep drop in U.S. coffee prices as markets reacted to reports that the government plans to reduce certain import tariffs, according to Reuters.

President Donald Trump recently told Fox News that the administration would lower tariffs on coffee imports, a position he first mentioned during his October trip to Asia. His remarks come as the White House faces voter frustration over the cost of living, which Democrats made a central theme in their recent election victories across New Jersey, New York, and Virginia. Economists have linked continuing inflation in part to the high import tariffs imposed by Trump earlier in his term.

Reuters reports that following those political setbacks, Trump has discussed giving households rebate checks funded by tariffs and has floated the idea of a 50-year mortgage. Bessent said the $2,000 rebate plan, targeted at individuals earning less than $100,000 annually, is “in discussion” but not yet approved. He did not address the long-term mortgage proposal, which has drawn criticism from some conservative lawmakers and business leaders.

When asked about potential tariff cuts for coffee suppliers such as Brazil and Vietnam, Bessent replied, “you’re going to see some specific announcements in coming days in terms of things we don’t grow here in the United States, coffee, coffee being one of them, bananas, other fruits, things like that.” The United States grows limited quantities of bananas in Hawaii and Florida, but most are imported due to cheaper labor and land abroad.

Bessent also pointed to other Trump administration policies expected to support household income, including lower taxes on overtime pay and tips, and efforts to attract foreign investment in domestic manufacturing. “Real wages are going to increase,” he said. “I would expect in the first quarter, second quarter of next year… Americans are going to start feeling better.”

He added that many families will receive larger tax refunds in 2026 thanks to new deductions for car loans and the elimination of taxes on some Social Security benefits. Parents of children born between the end of 2024 and the start of 2029 could receive a $1,000 initial deposit if they open a Trump account for their newborns.

Watch Bessent’s full appearance here:

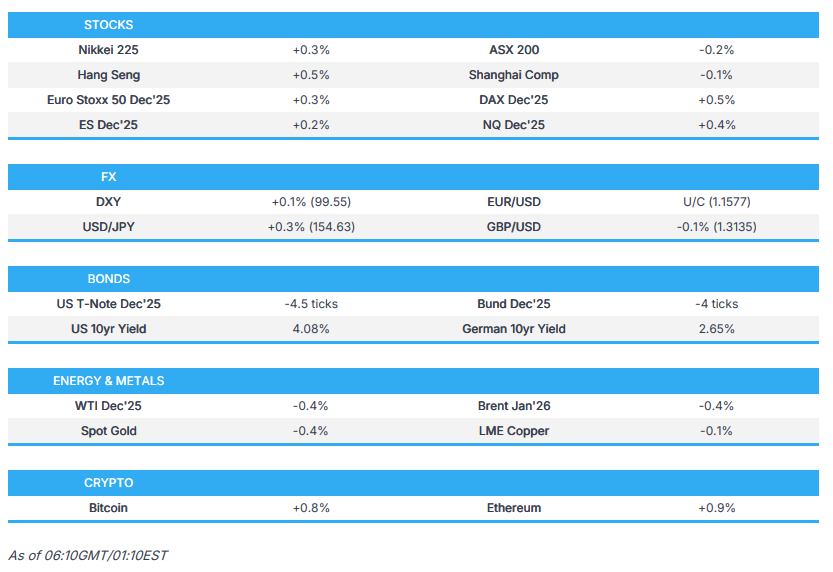

SHANGHAI CLOSED DOWN 2.62 POINTS OR 0.07%

//Hang Seng CLOSED CLOSED UP 226.32 PTS OR 0.85%

// Nikkei CLOSED : UP 220.38 PTS OR 0.43% //Australia’s all ordinaries CLOSED DOWN 0.21%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1175/ OFFSHORE CLOSED UP AT 7.1205/ Oil DOWN TO 60.43 dollars per barrel for WTI and BRENT DOWN TO 64.55 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING UP TO 7.1175 OFFSHORE YUAN TRADING UP TO 7.1205:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1175

OFFSHORE YUAN: UP TO 7.1205

HANG SENG CLOSED UP 226.82 PTS OR 0.85%

2. Nikkei closed UP 220.38 PTS OR 0.43%

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX UP TO 99.81 EURO FALLS TO 1.1569 DOWN .0007 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.691//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.84…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.183 UP 1 FULL BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP/JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6664/ Italian 10 Yr bond yield DOWN to 3.409 SPAIN 10 YR BOND YIELD DOWN TO 3.167

3i Greek 10 year bond yield DOWN TO 3.308

3j Gold at $4124.30 Silver at: 51.79 1 am est) SILVER NEXT RESISTANCE LEVEL AT $54.00//AFTER 50.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 16/100 roubles/dollar; ROUBLE AT 81.11

3m oil (WTI) into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.84 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.691% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.183 UP 1 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7994 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9248 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.083 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.685 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.567 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.24 UP 0 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.4180 UP 3 PTS

30 YR UK BOND YIELD: 5.211 UP 4 BASIS PTS

10 YR CANADA BOND YIELD: 3.174 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.754 UP 0 BASIS PTS.

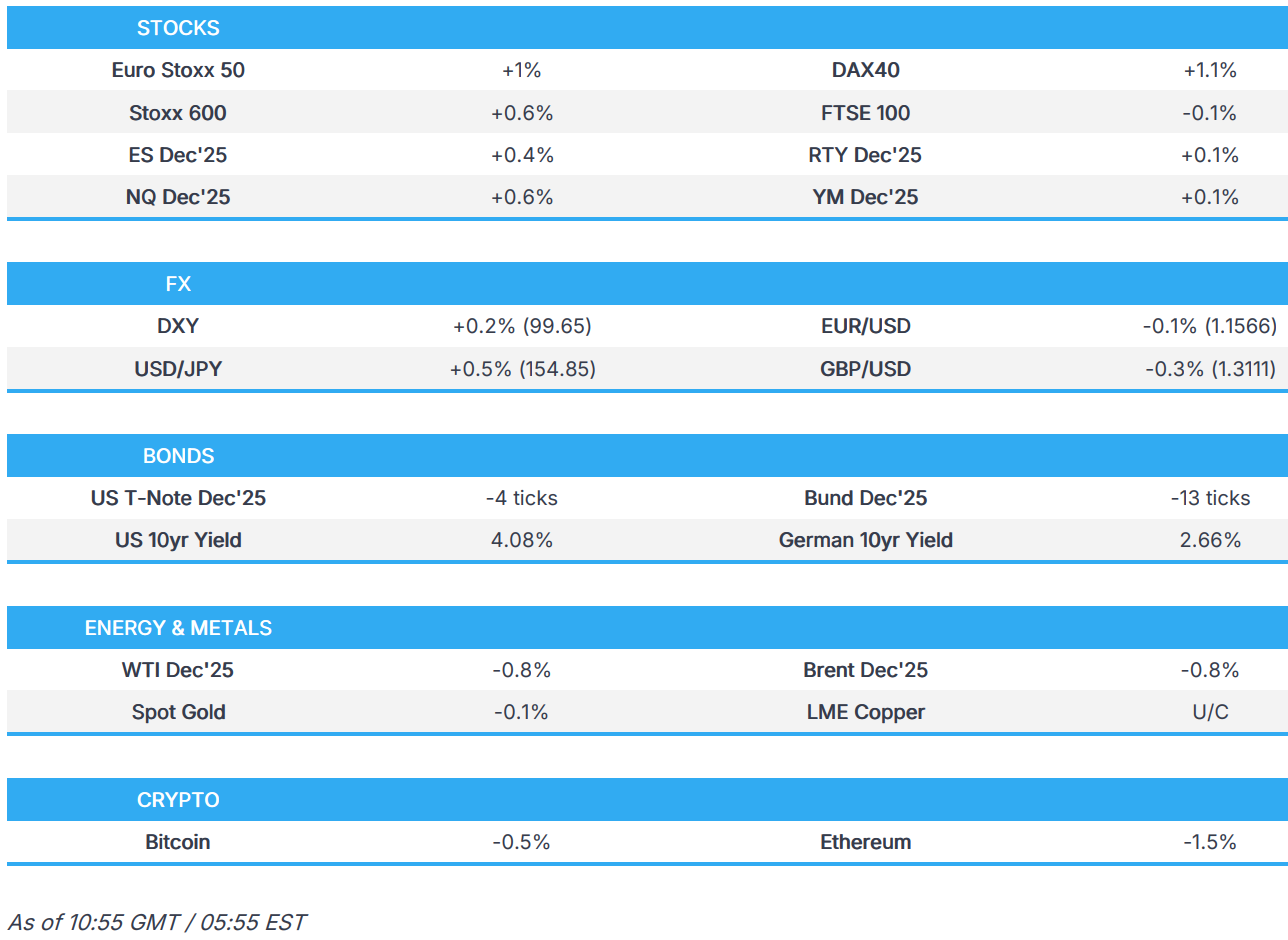

a New York OPENING REPORT

Futures Rise With Government Set To Reopen Within Hours

Wednesday, Nov 12, 2025 – 08:36 AM

US futures are higher as the US takes another step to reopen with a House vote (expected to pass early evening on Wednesday, with Trump’s approval. As of 8:15am, S&P futures are 0.4% higher with the mood buoyed by expectations of an imminent end to the government shutdown and a Fed rate cut next month. Bullish datapoints in the AI story from AMD and FoxConn/Hon Hai Precision are also helping lift Nasdaq futures 0.7% as Nvidia led gains across the Magnificent Seven in premarket trading. Pre-market, Mag7 names are all higher and NVDA (+1.5%) and AVGO (+1.4%) boosting Semis while Nvidia partner Hon Hai Precision Industry Co. and Europe’s Infineon Technologies AG offered rosy forecasts. Cyclicals (ex-Energy) poised to outperform as the yield curve bull steepens with traders buying bonds to match yesterday’s rally in Treasury futures follower weaker than expected jobs data. USD is bid up pre-mkt; commodities are mixed with Energy and Ags weaker with Base higher, gold flat, and silver +1.2%. The macro focus today is on the House vote and mtge applications; XHB has outperformed the SPX by ~1% MTD; IYR and XLRE have outperformed by almost 2% MTD. On the calendar, there is no macro again, Trump is hosting Wall Street execs for dinner tonight. There is a firehose of Fed speaker: Williams (9:20am), Paulson (10am), Waller (10:20am), Bostic (12:15pm), Miran (12:30pm) and Collins (4pm)

In premarket trading, Mag 7 stocks are all higher (Nvidia +1.5%, Alphabet +0.7%, Apple +0.2%, Amazon +0.5%, Tesla +0.4%, Meta +0.3%, Microsoft +0.4%)

- Alcon (ALC) rises 5% after the eye-care company reported core earnings per share for the third quarter that beat the average analyst estimate.

- Advanced Micro Devices (AMD) gains 5% after the semiconductor company projected accelerating sales growth over the next five years.

- Bill Holdings Inc. (BILL) is exploring options including a potential sale, people familiar with the matter said. Shares are up 11%.

- Black Rock Coffee Bar (BRCB) declines 7% after the operator of drive-thru coffee bars announced its first earnings report since going public in September.

- Circle Internet (CRCL) falls 4% after the stablecoin issuer reported third-quarter reserve income hurt by a decline in the reserve return rate.

- Clearwater Analytics Holdings Inc. (CWAN) is considering a potential sale after receiving takeover interest, according to people familiar with the matter. Shares climb 9%.

- GlobalFoundries (GFS) gains 6% after the semiconductor-manufacturing company reported adjusted earnings per share for the third quarter that beat the average analyst estimate.

- Oklo shares (OKLO) rises 4% as analysts see the company’s US Department of Energy Nuclear Safety Design Agreement approval accelerating the licensing process.

- On Holding (ONON) climbs 9% after the Swiss sneaker brand boosted its sales forecast for the year after better-than-expected third-quarter results.

- RLJ Lodging (RLJ) gains 2.9% after Raymond James upgraded to strong buy following the stock’s significant underperformance this year.

In corporate news, Eli Lilly is dropping CVS’s drug benefit plan for its employees after CVS stopped covering its weight-loss drug in favor of a rival medication from Novo Nordisk. Visa is testing the ability for businesses to send stablecoins directly to consumers’ cryptocurrency wallets for global payouts. JPMorgan has started rolling out a deposit token JPM Coin.

Markets are anticipating an end to the 43-day US government shutdown, with House members set to return to Washington to vote on a spending deal. Traders are betting that the resumption of data releases could bolster the case for interest-rate cuts amid lingering uncertainty over policymakers’ next move. Soft ADP jobs data on Tuesday has already prompted traders to price in a higher chance of rate cut. However, it won’t all be smooth sailing, with the Wall Street Journal’s Nick Timiraos warning that the data blackout has fueled Fed divisions.

“What I see is a wind of optimism and momentum in the US,” said Roland Kaloyan, head of European equity strategy at Societe Generale SA. “Markets are currently buying 2026 amid a positive cocktail of resilient growth, AI investments, Fed cuts and a weaker dollar.”

AI remains front and center, with AMD predicting accelerating sales growth over the next five years, driven by strong demand for its data center products, and Nvidia partner Hon Hai Precision giving a rosy outlook. Meanwhile, a senior researcher at AI startup DeepSeek warned that a severe labor market crisis is coming as automation wipes out most jobs, according to the South China Morning Post. And Fed Governor Barr said there need to be clear guardrails to prevent risks as the financial sector looks to adopt AI.

In strategy, Citi’s Beata Manthey said that near-term choppiness won’t stop global equities from realizing modest gains through the middle of 2026. And Goldman strategists expect emerging markets to deliver higher returns than US stocks in the next decade, helped by a weaker dollar and higher growth

Trump said the US needed skilled workers from abroad even as his administration has taken steps to make it harder for businesses to use the H-1B visa system. Trump is also said to be hosting financial industry executives for dinner Wednesday at the White House. The FDA named Richard Pazdur, a 26-year veteran of the agency, as its lead drug regulator.

Looking at earnings, out of the 457 S&P 500 companies that have reported so far in the earnings season, 81% have topped analyst forecasts, while 15% have missed. Alcon is rising in premarket trading after the eye-care company reported core earnings that beat the average analyst estimate. TransDigm, GlobalFoundries and Circle Internet are among companies expected to report results before the market open. Earnings from Cisco, Flutter Entertainment and Tetra Tech follow later in the day.

Europe’s Stoxx 600 is up by 0.6%, with autos and banks outperforming. SSE shares rose to a record high on the electricity supplier’s new investment plan, lifting utilities shares. The autos sector also outperforms, while personal care products lag. Here are some of the biggest movers on Wednesday:

- SSE shares rise as much as 13%, hitting record high, after the utility company outlined its intention to spend £33 billion as part of a new investment plan.