access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XGE: COMEX

132 C SG AMERICAS 1

167 C MAREX 1

323 C HSBC 596

363 H WELLS FARGO SECURITI 84

624 H BOFA SECURITIES 715

661 C JP MORGAN SECURITIES 190

709 C BARCLAYS 200

732 C RBC CAP MARKETS 3

737 C ADVANTAGE FUTURES 4

905 C ADM 42

GOLD: NUMBER OF NOTICES FILED FOR NOV/2025: 918 CONTRACTs NOTICES FOR 91,800 OZ or 2.855 TONNES

total notices so far: 9564 contracts for 956,400 OR 29.788 tonnes)

SILVER NOTICES: 44 NOTICE(S) FILED FOR 220,000 OZ/

total number of notices filed so far this month : 3469 CONTRACTS (NOTICES) for 17.345 million oz

INITIAL STANDING FOR NOV: 11.575 MILLION OZ

PLUS INITIAL 1.245 MILLION OZ QUEUE JUMP

THEN ADD TUESDAY;S 1,93 MILLION OZ QUEUE JUMP

THEN WEDNESDAY;S 0.570 MILLION OZ QUEUE JUMP

THEN 0.080 MILLION OZ

THEN MONDAY’S 425,000 0Z

THEN TUESDAY: 275,000 OZ

THEN WEDNESDAY’S 295,000 OZ

THEN THURSDAY : 10,000 OZ

THEN FRIDAY: 1.245 MILLION OZ

MONDAY: 0.300 MILLION OZ

NOW TUESDAY 0.275 MILLION OZ

EQUALS

17.785 MILLION OZ STANDING FOR SILVER.

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOV: 21.065 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

AND NOW NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY;S QUEUE JUMP OF 1.256 OZ WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 5.255 MILLION OZ//STANDING ADVANCES TO 17.220 MILLION OZ/

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 1.153 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 10.2938 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3996 TONNES//NEW STANDING ADVANCES TO 28.4126 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 74.59 TONNES//VERY SMALL THIS MONTH.

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 5125 CONTRACTS OI TO 151,989 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 75 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 75 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF5051 CONTRACTS AND ADD TO THE 75 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF 5051 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR TINY LOSS OF $0.07 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 25.25 MILLION PAPER OZ

OCCURRED DESPITE OUR LOSS IN PRICE.OF $0.07

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 32.22 POINTS OR 0.81%

//Hang Seng CLOSED CLOSED DOWN 454.25 PTS OR 1.72%

// Nikkei CLOSED : DOWN 1620.93 PTS OR 3.22% //Australia’s all ordinaries CLOSED DOWN 1.94%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1126/ OFFSHORE CLOSED UP AT 7.1139/ Oil DOWN TO 59.66 dollars per barrel for WTI and BRENT DOWN TO 63.93 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP TO 7.1126 OFFSHORE YUAN TRADING UP TO 7.1139:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY FAIR SIZED SIZED 2893 CONTRACTS TO 474,390 OI WITH THE LOSS IN PRICE OF $20.40 WITH RESPECT TO MONDAY’S // TRADING/RAID //COMEX CLOSING TIME:… WE LOST SOME NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1480). WE HAD HUGE T.A.S. LIQUIDATION FRIDAY AND MONDAY.. IT SEEMS THAT THE SPECULATORS WENT TO THE SHORT SIDE AGAIN WITH OUR FRBNY AND OTHER CENTRAL BANKERS ON THE LONG SIDE TAKING IN ALL THE CONTRACTS THAT THEY COULD. JUDGING BY THE NOTICES FOR DELIVERY FILED LAST NIGHT AT 918 NOTICES FOR 91,800 OZ (2.855 TONNES), THEY TOOK EVERYTHING ON OFFER.

WE THUS HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1413 CONTRACTS (OR 41.287 TONNES).THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

FIRST LETS DO A REVIEW OF EXCHANGE FOR RISK ISSUANCES:

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD PRIOR MONTHS

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES. THE RECIPIENT OF THESE EXCHANGE FOR RISK IS THE BANK OF ENGLAND. THIS CENTRAL BANK LOANED OUT ITS GOLD AND WANTS IT BACK. THEIR TOTAL RESERVES PRIOR TO THE LOANS IS LISTED AT 310 TONNES.

LET US LOOK AT JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

NOW LET US LOOK AT THE MONTH OF AUGUST:

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

NOW LET US LOOK AT SEPT.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FOR 14.553 TONNES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

LET’S SUM UP EXCHANGE FOR RISK FOR THE LAST 8 MONTHS

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK//TOTAL CONTRACT ISSUANCES //TONNES OF GOLD

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AND NOW NOVEMBER:

NOVEMBER: SO FAR ONE ISSUANCE:

WHICH NOW BRINGS US TO NOVEMBER WHERE WE RECEIVED NOTICE OF OUR FIRST ISSUANCE OF 450 CONTRACTS FOR 45000 OZ OR 1.3996 TONNES.

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 10 MONTH TOTALS 131.6996 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 54 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES IN AUGUST AND THEN ADDED 24 TONNES IN SEPT. AND THUS THEIR SHORTFALL TO THE BIS IS 54 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 10TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH NOV//ONLY MISSING JUNE. TOTAL 10 MONTHS ISSUANCE 131.6996 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW NOVEMBER COMEX CONTRACT MONTH//

IN TOTAL WE HAD A VERY FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 1413 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 2.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT/ NOVEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS FINALLY A LOWER T.A.S ISSUANCE CONTRACTS AS THE 5 CONSECUTIVE MEGA HUGE ISSUANCES HAS ENDED. THE CME NOTIFIES US THAT THEY HAVE ISSUED 1862 T.A.S CONTRACTS. THESE LAST 5 CONSECUTIVE MEGA HUGE T.A.S ISSUANCES WERE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING THE WEEK FINISHING OFF WITH A MASSIVE HUGE RAID ON GOLD AND SILVER LAST THURSDAY AFTERNOON THROUGH TO MONDAY, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS WE WE WILL PROBABLY SEE GOLD//SILVER RISE HUGELY ON OUR UPCOMING DAYS.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS: SEPT THROUGH NOVEMBER;

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE FINISHING OPTION EXPIRY WEEK, THE CROOKS GOADED OUR SPECULATORS TO CONTINUE ONTO THE SHORT SIDE WITH THE BANKERS ON THE LONG SIDE…THE RAIDS THROUGHT THIS WEEK WERE FREQUENT BUT FAILED TO CAUSE ANY DAMAGE TO THE PRICE WITH OPTIONS EXPIRY FINISHING OCT 31 AS WE NOW ENTER OUR MONTH OF NOVEMBER WITH EARLY MONTH FAILED RAID ATTEMPTS. SO THEY NOW ISSUED THESE MEGA T.A.S. CONTRACTS AND THAT ALWAYS SIGNALS A MAJOR RAID WHICH ARRIVED ON OUR DOORSTEP THURSDAY EARLY AFTERNOON AND CONTINUED RIGHT THROUGH MONDAY AND NOW TODAY.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 8 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. AND NOW NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 3.636TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 11.4468 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES///NEW STANDING ADVANCES TO 32.0496 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 54+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 54 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 54 TONNES REMAIN ON THE BOOKS OF THE BIS.

THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING E.G. NOVEMBER: A HUGE INITIAL 15.651 TONNES STANDING IN AN OFF MONTH!! THIS IS HUGE!!!//WITH QUEUE JUMPS AND EXCHANGE FOR RISK NEW STANDING FOR GOLD NOW AT 32.0496 TONNES

EXCHANGE FOR PHYSICAL ISSUANCE/NOV//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1480 CONTRACTS.

THAT IS A FAIR SIZED 1480 EFP CONTRACT WAS ISSUED: : /DEC 1480 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1480 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 54 TONNES

WE HAD :

- CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY + GOVERNMENT LIQUIDATION AND MASSIVE LIQUIDATION LATE THURSDAY AND FRIDAY/VERY EARLY AFTERNOON CLOSE TO CLOSING TIME

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE OCT 31 WITH OUR ATTEMPTED FAILED RAID, WE WILL SEE THESE MONTHLY MONTH SPREADERS IN ACTION NEXT WEEK DURING OPTIONS EXIRY WEEK.

T.A.S.SPREADER ISSUANCE//NOV

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT// TUESDAY MORNING WAS A MUCH SMALLER SIZED 1862 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP MONDAY’S LOSS IN PRICE IN GOLD YET A CORRESPONDING VERY STRONG GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 5 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S FIRST ISSUANCE FOR 1.36996 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

GOLD STANDING AT THE COMEX FOR GOLD LAST 11 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

AND NOW NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 3.636 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 11.4468 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 1.3966 TONNES.

/STANDING ADVANCES TO 32.0496 TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING NOVEMBER,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $20.40/ /) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME NET SPECULATOR LONGS AS CENTRAL BANKS (FRBNY + OTHER CENTRAL BANKS) TOOK THE LONG SIDE AS WE DID HAVE A FAIR LOSS IN OI FROM TWO EXCHANGES OF 1,413 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION THURSDAY COMEX TRADING THROUGH TO MONDAY.. OTHER CENTRAL BANKS

TENDERED FOR PHYSICAL MONDAY NIGHT. THE COMEX IS ONE BIG MESS!! THIS WEEK, THE BANKERS (FRBNY) WENT TO THE SHORT SIDE AND SPECS AND OTHER CENTRAL BANKERS ON THE LONG SIDE. THE SPECS WILL BE QUITE NICELY RINSED BY THE FRBNY BANKERS IN SHORT ORDER!!

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

STANDING FOR GOLD OCT AND NOVEMBER:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 3.838 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 11.4468 TONNES TO WHICH WE ADD OUR FIRST ISSUANCE OF EXCHANGE FOR RISK OF 1.3966 TONNES..

NEW STANDING ADVANCES TO 32.0496 ONNES OF GOLD.

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $20.40

WE HAD A HUGE 14,687 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

INITIAL GOLD COMEX

NOV 18

NOV CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES i) Out of JPMorgan enhanced: 96,766.100 oz or 242 London good delivery bars of 400 oz each total withdrawal: 96,766.100 oz or 3.00 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 entries i) Into HSBC 2999.99 oz First entry as a deposit in 3 months. xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 918 notice(s) 91,800 OZ 2.855 TONNES OF GOLD |

| No of oz to be served (notices) | 290 contracts 29,000 OZ 0.9020 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9564 notices 956,400 0z 29.788 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 entries

i) Into HSBC 2999.99 oz

First entry as a deposit in 3 mont

customer withdrawals:

1 ENTRIES

i) Out of JPMorgan enhanced:

96,766.100 oz or 242 London good delivery bars

of 400 oz each

total withdrawal: 96,766.100 oz

or 3.00 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 0

volume at the comex: MONDAY: 275,792 oz//

AMOUNT OF GOLD STANDING FOR NOVEMBER:

THE FRONT MONTH OF NOV STANDS AT 1208 CONTRACTS FOR A HUG GAIN OF 760 CONTRACTS.

WE HAD 409 CONTRACTS SERVED ON MONDAY. SO WE GAINED A MEGA HUGE 1169 CONTRACTS FOR 116,900 OZ OF GOLD (3.636 TONNES).

DECEMBER LOST 10,970 CONTRACTS DOWN TO 232,736 CONTRACTS . DECEMBER IS THE NEW FRONT MONTH AND WE ARE GOING TO HAVE A DILLY MONTH STANDING FOR GOLD!!

JANUARY LOST 74 CONTRACTS DOWN TO 1246

We had 918 contracts filed for today representing 91,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 918 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 190 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2025. contract month, we take the total number of notices filed so far for the month (9564 oz ) to which we add the difference between the open interest for the front month of NOV ( 1208 CONTRACTS) minus the number of notices served upon today (918 x 100 oz per contract) equals 985,400 OZ OR 30.6500 Tonnes of gold to which we add our first issuance of exchange for risk for 1.3996 tonnes//new standing advances to 32.0496 tonnes.

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (9564x 100 oz +we add the difference for front month of NOV (1208 OI} minus the number of notices served upon today (918)x 100 oz) which equals 985,400 OZ OR 30.6500 TONNES to which we add our 1.3996 tonnes of exchange for risk//new total of gold standing in November is 32.0496 tonnes

TOTAL COMEX GOLD STANDING FOR NOV..: 32.0496 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE ACTIVE DELIVERY MONTH OF NOVEMBER

volume MONDAY confirmed 381,612 contracts HUGE

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,970,845.069 oz 61.30 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 37,224,744.190 oz

TOTAL REGISTERED GOLD 19,476,351.607 or 605.790 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,748,392.583 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,505,506 oz ((REG GOLD- PLEDGED GOLD)=

544.49 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE NOV. 2025 SILVER CONTRACTS

NOV 18 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of aSAHI 2100,372.990 OZ ii) Out of CNT 597,007.426 oz iii) Out of Delaware 13,807.305 oz iv) Out of JPMorgan: 1,289,142.600 oz total withdrawal: 4,000,330.321 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT DEPOSIT ENTRIES/CUSTOMER ACCOUNT 0 |

| No of oz served today (contracts) | 44 CONTRACT(S) ( 220,000 OZ 0.220 MILLION OZ |

| No of oz to be served (notices) | 89 contracts (0.445MILLION oz) |

| Total monthly oz silver served (contracts) | 3468Contracts (17.345 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 entries

`

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

4 entries

i) Out of aSAHI 2100,372.990 OZ

ii) Out of CNT 597,007.426 oz

iii) Out of Delaware 13,807.305 oz

iv) Out of JPMorgan: 1,289,142.600 oz

total withdrawal: 4,000,330.321 oz

adjustments: 0

comex is in turmoil

TOTAL REGISTERED SILVER: 156.106 MILLION OZ//.TOTAL REG + ELIGIBLE. 465,585 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF NOVEMBER /2025 OI: 133 OPEN INTEREST CONTRACTS FOR A GAIN OF 9 CONTRACTS. WE HAD 45 NOTICES SERVED ON MONDAY SO WE GAINED 54 OR 0.270 MILLION OZ QUEUE JUMP.

DECEMBER LOST 7921 CONTRACTS DOWN TO 62,332. THIS IS THE FRONT MONTH FOR SILVER DELIVERIES AND WE WILL HAVE A STRONG STANDING FOR OUR SILVER METAL.

JANUARY LOST 8 CONTRACTS DOWN TO 2246 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 44 or 0.220 MILLION oz

CONFIRMED volume; ON FRIDAY 90,025 huge//

AND NOW NOVEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 3469 X5,000 oz = 17.345MILLION oz

to which we add the difference between the open interest for the front month of NOV (133) AND the number of notices served upon today (44 )x (5000 oz)

Thus the standings for silver for the NOVEMBER 2025 contract month: (3469) Notices served so far) x 5000 oz + OI for the front month of NOV(133) minus number of notices served upon today (44)x 5000 oz equals silver standing for the NOV.contract month equating to 17.785 MILLION OZ

New total standing: 17.785million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 156.106 million oz of registered silver

JPMorgan as a percentage of total silver: 200,550/465million. 43.02%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

NOV 18/WITH GOLD DOWN $6.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 17/WITH GOLD DOWN $20.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.93 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1044.000 TONNES

NOV 14/WITH GOLD DOWN $97.55TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1048.93 TONNES

NOV 13/WITH GOLD DOWN $17.80.TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1064.64 TONNES

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT XXX TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

NOV 3 WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 1.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1039,20 TONNES

OCT 31 WITH GOLD DOWN $17.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1040.35 TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

OCT 23 WITH GOLD UP $78.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37 TONNES

OCT 22 WITH GOLD DOWN $78.95 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

GLD INVENTORY: 1041.43 TONNES, TONIGHTS TOTAL

SILVER

NOV 18/WITH SILVER DOWN $0.13 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489..283 MILLION OZ MILLION OZ

NOV 17/WITH SILVER DOWN $0.07 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.451 MILLION OZ INTO THE SLV:INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 14/WITH SILVER DOWN $2.08 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.722 MILLION OZ INTO THE SLV:

INVENTORY RESTS AT 487.832 MILLION OZ MILLION OZ

NOV 13/WITH SILVER DOWN $0.58 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 4 WITH SILVER DOWN $0.82 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

NOV 3 WITH SILVER $0.12 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 31 WITH SILVER DOWN $0.35 TODAY/SMALL CHANGES IN SILVER AT THE SLV: ///A WITHDRAWAL OF 636,000 OZ FROM THE SLV// ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

OCT 23 WITH SILVER UP $0.87 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 501.474 MILLION OZ

OCT 22 WITH SILVER DOWN $0.33 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.995 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 504.015 MILLION OZ

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

CLOSING INVENTORY 489.283 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MCLEOD….

CHRIS POWELL, Secretary/Treasurer//GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS /249

SHANGHAI CLOSED DOWN 32.22 POINTS OR 0.81%

//Hang Seng CLOSED CLOSED DOWN 454.25 PTS OR 1.72%

// Nikkei CLOSED : DOWN 1620.93 PTS OR 3.22% //Australia’s all ordinaries CLOSED DOWN 1.94%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1126/ OFFSHORE CLOSED UP AT 7.1139/ Oil DOWN TO 59.66 dollars per barrel for WTI and BRENT DOWN TO 63.93 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP TO 7.1126 OFFSHORE YUAN TRADING UP TO 7.1139:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1139

OFFSHORE YUAN: UP TO 7.1126

HANG SENG CLOSED DOWN 454.24 PTS OR 1,72%

2. Nikkei closed DOWN 1620.93 PTS OR 3.22%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 99.40 – EURO RISES TO 1.1595 UP .0005 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.748//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.09…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.309UP 5 FULL BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP/JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6910/ Italian 10 Yr bond yield DOWN to 3.441 SPAIN 10 YR BOND YIELD DOWN TO 3.196

3i Greek 10 year bond yield DOWN TO 3.335

3j Gold at $4038.25 Silver at: 50.31 1 am est) SILVER NEXT RESISTANCE LEVEL AT $54.00//AFTER 50.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 9/100 roubles/dollar; ROUBLE AT 81.10

3m oil (WTI) into the 59 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.09 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.748% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.305 UP 5 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7958 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9227 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.101 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.723 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.523 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.35 UP 3 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.5190 DOWN 3 PTS

30 YR UK BOND YIELD: 5.3336 DOWN 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.239 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.807 UP 1 BASIS PTS.

a New York OPENING REPORT

Futures, Bitcoin Tumble, Extending Longest Losing Streak Since August

Tuesday, Nov 18, 2025 – 08:27 AM

US equity futures are sharply lower again – but off session lows – after the S&P 500 and Nasdaq closed below their 50-day moving averages for the first time since April; both tech and small caps are lagging as the market tries to find a level as the bond market continues to reduce the probability of a further Fed easing. As of 8:00am. S&P futures are -0.6%, set for the longest losing streak since late August. Nasdaq 100 contracts were also -0.6%. Pre-market, Mag7 names are mostly lower with AAPL/GOOG in the green and Semis are weaker. Cyclicals are poised to lag Defensives as the risk-off tone continues. Bitcoin has also pared its drop to 0.4%, having earlier fallen below $90,000 for the first time since April with traders are betting on even more downside. Rotation trades helped to support the overall market last week, but both the Dow and Russell 2000 underperformed yesterday. Topping the list of worries are AI valuations and whether the Fed will cut rates next month. Fund manager positioning (crowded in stocks and low on cash) is also a possible headwind, according to BofA. Treasuries were the main beneficiaries as investors continued to seek havens, with the 10-year yield falling four basis points to 4.09%. Gold fluctuated above $4,000 an ounce. The dollar was little changed. The macro data focus is old Aug / Sep data being released but ultimately the market awaits NVDA and NFP; the Fed Meeting Minutes may give additional color on the Fed’s reaction function into the Dec meeting.

In premarket trading, most Mag 7 names are lower: Microsoft (MSFT) falls 1.5% and Amazon (AMZN) is down 1.8%, underperforming Magnificent Seven peers after Rothschild & Co Redburn downgraded the stocks for the first time since initiating coverage in June 2022. Alphabet Inc. (GOOGL) is up 0.6% after Loop Capital upgraded the Google parent to buy from hold. Apple (AAPL) +0.4%, Meta Platforms (META) -0.7%, Tesla (TSLA) -0.8%, Nvidia (NVDA) -1.1%

- Barrick Mining (B) is up 2.5% after the Financial Times reported that Elliott Management has built a “large” stake in the gold miner.

- Home Depot (HD) falls 3.5% after the retailer reported comparable sales and adjusted EPS for the third quarter that missed the consensus estimates. They also reduced the annual EPS guidance.

- Honeywell International (HON) falls 2.1% after BofA Global Research cut the recommendation on the industrial giant to underperform from buy, becoming the lone sell-equivalent rating in Bloomberg data. BofA expects shares to lag as elements of its spinoff strategy disappoint investors and the company doesn’t deliver earnings growth next year.

- Medtronic (MDT) is up 3.5% after the medical device maker lifted the bottom end of its range for adjusted profit forecast for the year.

- Molina Healthcare (MOH) is up 3.1% after hedge fund manager Michael Burry touted the health insurer in a X post.

In corporate news, Apple’s iPhone 17 series drove a 37% rise in its monthly smartphone sales in the key China market, according to Counterpoint Research. Akzo Nobel agreed to acquire smaller rival paint maker Axalta Coating Systems in a €7.9 billion ($9.2 billion) deal. Baidu posted its biggest quarterly revenue slide on record, despite major AI spending.

The ongoing global rout underscored continued unease over interest rates and technology earnings, with Nvidia Corp.’s report on Wednesday poised to test investor nerves over lofty valuations in the artificial-intelligence sector. Focus will then turn to the delayed September jobs report due Thursday, a key gauge for the Federal Reserve’s policy outlook. With all the talk of a potential bubble in AI, most recently with comments from JPMorgan Vice Chairman Daniel Pinto, Nvidia earnings on Wednesday are crucial for market direction. The report “will be the ultimate ‘blue or red pill’ moment for the market,” said Stephan Kemper, chief investment strategist at BNP Paribas Wealth Management. Options suggest an earnings-related move of about 6.4%, roughly matching Nvidia’s recent average, according to data compiled by Bloomberg.

“The question is whether the selloff will continue after Nvidia’s results,” said Eric Bleines, a fund manager at SwissLife Gestion Privée in Paris. “This will make the difference between the market just taking a breather or going for a correction.”

Additionally, traders have less conviction about that, with interest-rate swaps now implying a less-than-50% likelihood of a December rate reduction. Several Fed officials have recently cautioned against a cut, although Governor Waller repeated his view in favor of lowering rates.

“A bit of volatility and a pullback into year-end was on Santa’s wish list for a majority of institutional accounts,” wrote Mohit Kumar, chief economist and strategist for Europe at Jefferies. “Apart from retail investors, we do not think there is a lot of pain on the street.”

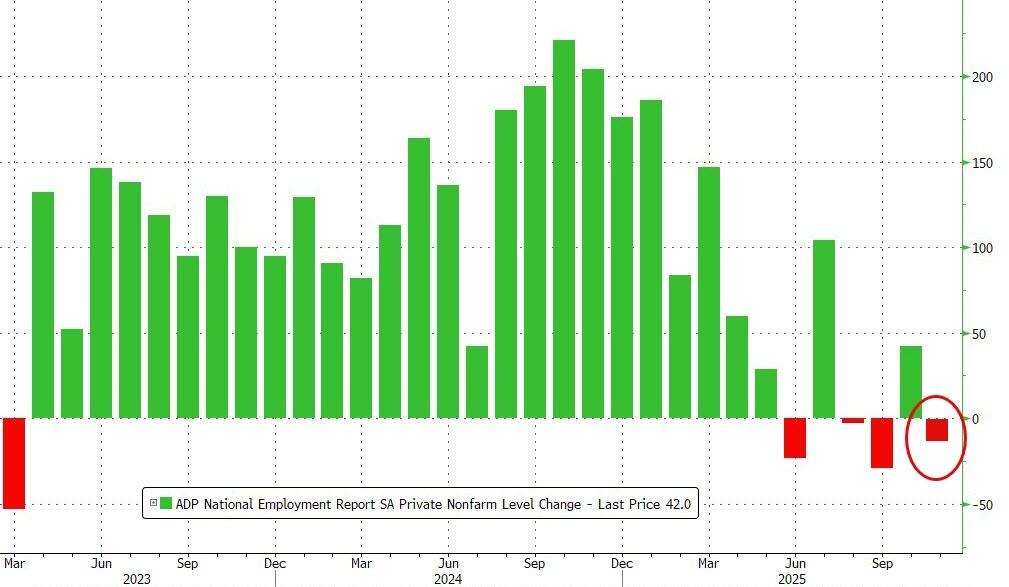

Meanwhile, in a sign that US government agencies were resuming operations after the longest shutdown on record, the Labor Department’s website showed 232,000 initial jobless claims for the week ended Oct. 18. Data for the previous three weeks weren’t available. Weekly employment estimates from ADP Research due later Tuesday will offer more insight into the labor market.

Barclays strategists led by Anshul Gupta said Nvidia’s results and the September payrolls report will shape near-term sentiment. They see potential upside for the chipmaker amid accelerating AI investment and rising demand for computing infrastructure, but note the stock has posted negative one-week returns in four of its last five earnings periods.

European stocks followed their Asian counterparts lower, with the Stoxx 600 down 1.3% and looking at a fourth day of losses, with mining and auto shares leading declines, while health care and personal care equities are the biggest outperformers. Here are the biggest movers Tuesday:

- Roche shares gain as much as 7% after the drugmaker announced its phase 3 study evaluating investigational giredestrant as an adjuvant endocrine treatment for people with ER-positive, HER2-negative, early-stage breast cancer met its primary endpoint at a pre-planned interim analysis

- Rheinmetall shares rise as much as 4.7% after the German maker of tanks and ammunition said it is targeting sales of about €50 billion in 2030, while also providing guidance around margins and cash conversion

- Imperial Brands climbs as much as 3.2% after reporting its full-year results and outlining guidance for 2026. Panmure Liberum says the tobacco company’s results are on “the right side” of in-line

- Greencore Group shares jump as much as 6.7% after the food producer posted earnings ahead of expectations

- Mining shares are the worst performers in Europe on Tuesday, falling as much as 3.2%, as aluminum and copper declined ahead of publication of delayed US economic data

- UK lenders were among the worst-performing banks in Europe on Tuesday amid tax worries ahead of Chancellor of the Exchequer Rachel Reeves’s budget announcement on Nov. 26

- Umicore shares dropped as much as 14% after a vehicle of holder Groupe Bruxelles Lambert sold roughly €300 million worth of shares in the chemicals company in an overnight placing

- ABB shares drop as much as 4.7%, the most in seven months, after the provider of power and automation technologies updated its financial goals ahead of its capital markets day

- Crest Nicholson shares fall as much as 12%, most since August 2024, as the UK housebuilder forecasts full-year profits at the low end of the range analysts expected

Earlier in the session, Asian stocks dropped, poised for a third-straight session of losses, as concerns about an artificial intelligence bubble returned to the fore ahead of Nvidia’s earnings report. The MSCI Asia Pacific Index fell as much as 2.4%, dipping below its 50-day moving average for the first time since April. A sub-gauge of technology shares led a broad decline across all sectors, with chipmakers TSMC and SK Hynix the biggest drags. Most markets in the region were in the red, with gauges in South Korea, Taiwan and Japan down more than 2% each. Concerns of AI overexuberance dominated sentiment as investors awaited Nvidia earnings due Thursday morning in Asia. A filing showed Peter Thiel’s hedge fund sold its entire stake in the chip-maker in the third quarter, adding fuel to market concerns over sector valuations. Tensions between Beijing and Tokyo impacted markets for a second day, with Korean travel shares advancing after China warned its citizens against visiting Japan. Meanwhile, analysts said Philippine stocks could face more headwinds due to political instability as President Ferdinand Marcos reshuffles his cabinet.

In FX, the Bloomberg Dollar Spot Index is little changed with not much movement versus the majors.

In rates, treasuries advance, with US 10-year yields falling 3 bps to 4.10%. UK and German government bonds also rise. Treasury futures hold gains with stock futures lower and technology sector in focus. Focal points of US session include weekly ADP jobs data and three scheduled Fed speakers. Treasury yields are richer by as much as 4bp-5bp in front-end and belly, outperforming long end and steepening the curve; 2s10s spread is about 1bp wider, 5s30s about 2bp; 10-year near 4.10% is about 2bp richer vs German counterpart, about 4bp vs UK. Treasury auctions this week include $16 billion 20-year bonds on Wednesday and $19 billion 10-year TIPS Thursday.

In commodities, spot gold is steady near $4,040/oz. Brent is trading near session highs, around $64.38.

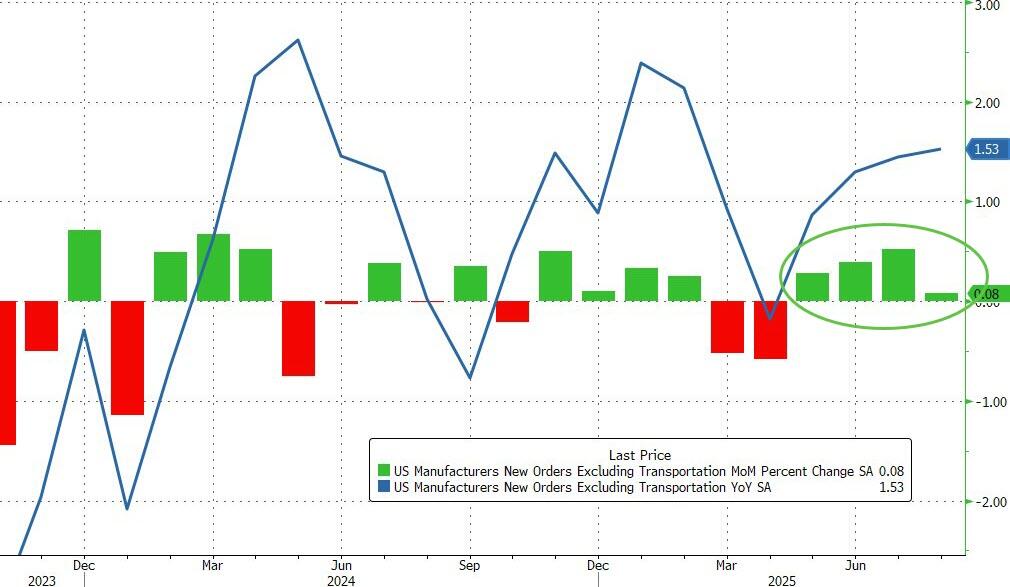

Looking ahead, today’s US economic calendar includes ADP weekly jobs data (8:15am), August factory orders (10am) and September TIC flows (4pm); initial jobless claims in the week ended Oct. 18 numbered 232k in data posted to Labor Department website after being delayed by US government shutdown. Fed speaker slate includes Barr (10:30am), Barkin (11am) and Logan (7:55pm) On the corporate side, Home Depot reports earnings.

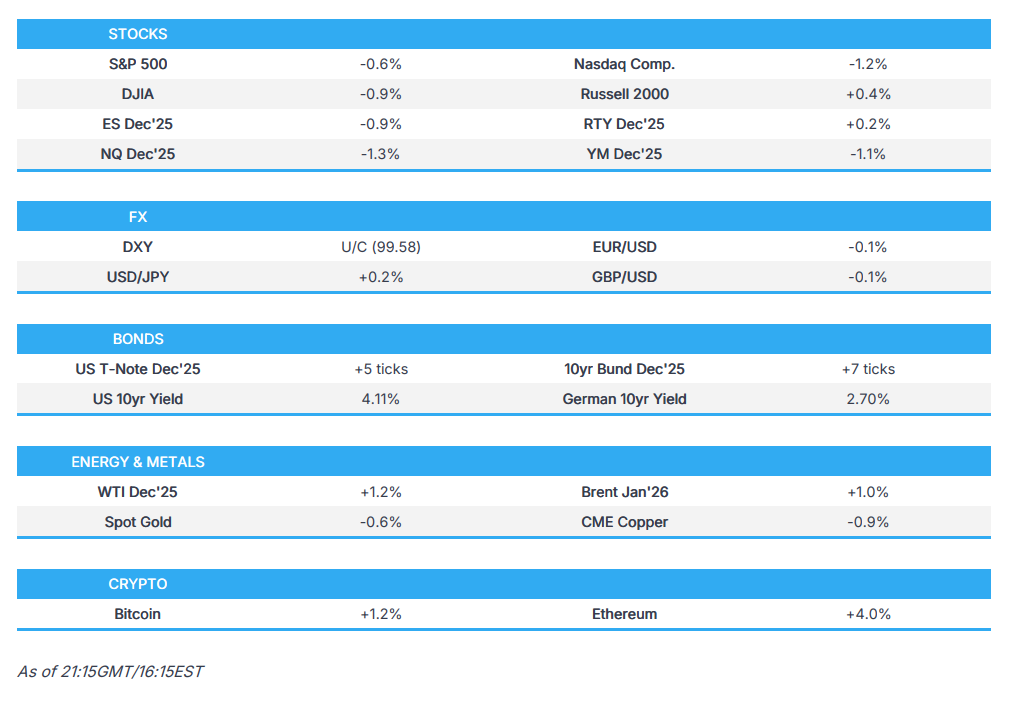

Market Snapshot

- S&P 500 mini -0.6%

- Nasdaq 100 mini -0.6%

- Russell 2000 mini -0.7%

- Stoxx Europe 600 -1.2%

- DAX -1.2%

- CAC 40 -1.2%

- 10-year Treasury yield -3 basis points at 4.1%

- VIX +0.8 points at 23.16

- Bloomberg Dollar Index little changed at 1220.57

- euro little changed at $1.1581

- WTI crude -0.2% at $59.8/barrel

Top Overnight News

- White House officials are insisting that latest tariff relief doesn’t amount to a retreat from the president’s staunch defense of tariffs as economic drivers, as critics say the White House is capitulating on its signature economics policy. NBC

- US initial jobless claims totaled 232,000 in the week ended Oct. 18, according to US Labor Department website showing historical data. The data’s release had been affected the government shutdown. BBG

- Mark Carney won a key budget vote by the slimmest of margins in Canada’s Parliament, ensuring the survival of his government and avoiding an election. BBG

- Hong Kong bankers and regulators are showing signs of growing concern about the city’s deepest real estate downturn since the Asian financial crisis. BBG

- China has bought nearly a million tons of US soybeans, a move that ends a temporary pause and appears to signal commitment to a trade truce agreed late last month. BBG

- Governor Kazuo Ueda told Prime Minister Sanae Takaichi that the Bank of Japan is in the process of slowly dialing back its easing support for the economy, signaling his unshaken intention to carefully raise rates. BBG

- Banking execs in the EU are bracing to be disappointed when officials lay out proposals to cut red tape in the coming weeks, as they predict that the measures will be far behind the deregulation taking place in the US. BBG

- Apple’s iPhone 17 series drove a 37% rise in monthly smartphone sales in China. BBG

- Home Depot (-3% premkt) cut its full-year earnings guidance, warning that some unsteady consumers are hitting the pause button on big-ticket home purchases. A modest miss was expected. Goldman thinks expectations were for a very small cut and it feels like we could say this was slightly worse than expectations.

- This earnings season, the share of firms discussing AI-related productivity on earnings calls has been highest within Communication Services and Financials. This quarter, 74% of Comm Services companies and 66% of Financials companies mentioned AI in the context of efficiency on their conference calls. AI-related productivity mentions were lowest in Utilities, Energy, and Materials. GIR

- JPMorgan COO Pinto says the US economy is not likely to enter a recession. On AI, says, there is likely to be a “correction” in AI valuations at some point. Upside for the S&P from here is relatively limited.

- US President Trump said he wants 1% inflation: BBG

Trade/Tariffs

- EU Trade Commissioner Sefcovic says the EU plans to introduce restrictions on EU exports of aluminium scrap.

- German Finance Minister on rare earths says Germany must do its homework and diversify supply chains.

A more detailed look at global markets courtesy of Newquawk

APAC stocks extended losses throughout the session following a similar lead from Wall Street, which had seen heavy losses on Monday. Overall newsflow in APAC hours was quiet, although tech stocks were among the laggards in the region. ASX 200 showed a clear defensive bias across its sectors, with tech the hardest hit. No obvious reaction was seen to the RBA minutes, which largely emphasised uncertainty and data-dependence. Nikkei 225 edged lower after the open and eventually surrendered the 49,000 level, falling as much as 3% intraday. Several additional factors on top of the global risk aversion could’ve exacerbated losses, including woes surrounding Japan–China relations and the recent JPY and long-end JGB weakness. Several Japanese officials verbally intervened throughout the session but failed to sway the index meaningfully. KOSPI lagged as the index joined the global stock rout, following the prior day’s outperformance. Hang Seng and Shanghai Comp opened in the red and initially conformed to regional losses, with Hong Kong underperforming the Mainland amid its tech exposure.

Top Asian News

- BoJ Governor Ueda says he discussed the economy, inflation and monetary policy with Japanese PM Takaichi. Will decide on monetary policy while scrutinising various data. FX was discussed, won’t comment on details. Desirable for FX to move to reflect fundamentals.

- Japanese Finance Minister Katayama said she is keeping an eye on markets with regard to fiscal policy and would not comment on FX levels, adding she is alarmed over FX moves; she said currencies should move in a stable manner reflecting fundamentals, and that the government will thoroughly monitor for excessive or disorderly forex fluctuations with a high sense of urgency. She noted concern over recent one-sided, rapid FX moves and said that while GDP avoided the worst, negative growth justifies a sizeable package, according to Reuters.

- Japan’s Economy Minister Kiuchi said long-term rate moves are determined by markets and that the government is watching market moves — including long-term rates — closely, according to Reuters.

- RBA November meeting minutes said it is appropriate in the current environment to remain cautious and data-dependent, with members determined they could remain patient while assessing incoming data on the extent of spare capacity. On rates, the minutes noted a mixed picture on whether policy remains restrictive — in contrast with the clearer signals seen in 2024 — and said the cash rate could be held at its current level if demand recovers more strongly than expected, while policy easing is still seen if the labour market weakens materially or growth disappoints; the Board said it is not possible to be confident about which scenario is more likely. The minutes said there may be a little more underlying inflationary pressure than previously assessed, noted the AUD remains close to equilibrium estimates, and said global growth is likely to slow in H2 2025, though the likelihood of a severe downside scenario has diminished, according to Reuters.

European bourses (STOXX 600 -1.3%) opened lower across the board, in a continuation of the downbeat mood seen in Wall St and in APAC trade overnight. Indices found a base in early morning trade, where they have resided throughout the morning so far. European sectors are entirely in the red, and hold a clear defensive bias. Healthcare tops the pile, buoyed by strength in Roche (+5.6%), after a positive trial update related to a breast cancer pill. To the downside, Autos, Tech and Basic Resources are all pressured. US equity futures (ES -0.2%, NQ -0.2%, RTY -0.2%) are modestly lower across the board, albeit not to the extent seen in Europe. Traders count down their clocks till NVIDIA earnings on Wednesday, but before that markets will have some US data (Durable Goods, Weekly ADP Average Estimate) and a couple of Fed speakers. Earlier, a surprise jobless claims release (w/e 18th Oct) had little impact on contracts.

Top European News

- EU Commission says definitive measures imposed consist of country-specific tariff rate quotas per type of ferroalloy, limiting the volume of imports to enter the EU duty free.

FX

- DXY is currently choppy and trades within a busy 99.39 to 99.60 range. Initial action saw the index buoyed by the downbeat risk tone, where the USD was pressured by typical haven currencies such as the JPY & CHF whilst the Antipodeans lagged. Thereafter, the risk tone improved a touch and the Dollar dipped to make a session low – a move which also came amidst a surprise US weekly claims release. Do note that the weekly claims release is a delayed report for the w/e Oct 18th; it printed at 232k, whilst continuing claims printed at 1.957mln. Looking ahead, ADP will release its weekly US jobs gauge; last week, it reported that its average weekly estimate was -11,250. US factory orders are expected to have risen by 1.4% M/M in August (prev. -1.3%); durable goods revisions for August are also due today. NAHB’s housing market index is seen unchanged at 37 in November. Fed’s Barr (voter) and Fed’s Barkin (2027 voter) are set to speak, while Fed’s Logan (2026 voter) will deliver remarks after the close.

- EUR is currently flat/mildly lower and largely moving at the whim of the Dollar given the lack of pertinent European newsflow. Initially flat vs the Dollar, then caught a bid to make a fresh session high above the 1.1600 mark – before once again reversing. Bid seemingly in the moments preceding the US jobless claims figures. Currently towards lows at 1.1583.