SORRY FOR BEING LATE: WAS AT MY DENTIST FOR QUITE A WHILE

access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XGE: COMEX

323 C HSBC 171

363 H WELLS FARGO SECURITI 492

661 C JP MORGAN SECURITIES 701

709 C BARCLAYS 380

737 C ADVANTAGE FUTURES 4

905 C ADM 4

JPMORGAN STOPPED: 701/876

GOLD: NUMBER OF NOTICES FILED FOR NOV/2025: 876 CONTRACTs NOTICES FOR 87,600 OZ or 2.725 TONNES

total notices so far: 10,440 contracts for 1,044,000 OR 32.472 tonnes)

SILVER NOTICES: 333 NOTICE(S) FILED FOR 1.680 MILLION OZ/

total number of notices filed so far this month : 3802 CONTRACTS (NOTICES) for 18.010 million oz

INITIAL STANDING FOR NOV: 11.575 MILLION OZ

WEDNESDAY: 1.475 MILLION OZ

THEN ALL PREVIOUS QUEUE JUMPS OF 6.68 MILLION OZ

EQUALS

19.205 MILLION OZ STANDING FOR SILVER.

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOV: 22.815 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

AND NOW NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY;S QUEUE JUMP OF 1.475 OZ WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 6.68 MILLION OZ//STANDING ADVANCES TO 19.265 MILLION OZ/

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 4.024 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 15.0533 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3996 TONNES//NEW STANDING ADVANCES TO 36.0736 TONNES OF GOLD.

NEW STANDING FOR GOLD, NOV CONTRACT AT 36.0736 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 82.441 TONNES//VERY SMALL THIS MONTH.

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE SIZED 1306 CONTRACTS OI TO 153,295 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 350 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1306 CONTRACTS AND ADD TO THE 350 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 1656 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $0.13 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.28 MILLION PAPER OZ

OCCURRED DESPITE OUR LOSS IN PRICE.OF $0.13

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 6.93 POINTS OR 0.18%

//Hang Seng CLOSED CLOSED DOWN 99.38 PTS OR 0.38%

// Nikkei CLOSED : DOWN 165.28 PTS OR 0.34% //Australia’s all ordinaries CLOSED DOWN 0.24%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1125/ OFFSHORE CLOSED UP AT 7.1139/ Oil UP TO 60.38 dollars per barrel for WTI and BRENT UP TO 64.40 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.1125 OFFSHORE YUAN TRADING UP TO 7.1139:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY FAIR SIZED SIZED 2437 CONTRACTS TO 471,953 OI WITH THE LOSS IN PRICE OF $6.30 WITH RESPECT TO TUESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, DESPITE THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2522). WE HAD ZERO T.A.S. LIQUIDATION TUESDAY.. IT SEEMS THAT THE SPECULATORS WENT TO THE SHORT SIDE AGAIN WITH OUR FRBNY AND OTHER CENTRAL BANKERS ON THE LONG SIDE TAKING IN ALL THE CONTRACTS THAT THEY COULD. JUDGING BY THE NOTICES FOR DELIVERY FILED LAST NIGHT AT 876 NOTICES FOR 87,600 OZ (2.725 TONNES), THEY TOOK EVERYTHING ON OFFER.

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 86 CONTRACTS (OR 0.2646 TONNES).THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

FIRST LETS DO A REVIEW OF EXCHANGE FOR RISK ISSUANCES:

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD PRIOR MONTHS

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES. THE RECIPIENT OF THESE EXCHANGE FOR RISK IS THE BANK OF ENGLAND. THIS CENTRAL BANK LOANED OUT ITS GOLD AND WANTS IT BACK. THEIR TOTAL RESERVES PRIOR TO THE LOANS IS LISTED AT 310 TONNES.

LET US LOOK AT JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

NOW LET US LOOK AT THE MONTH OF AUGUST:

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

NOW LET US LOOK AT SEPT.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FOR 14.553 TONNES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

LET’S SUM UP EXCHANGE FOR RISK FOR THE LAST 8 MONTHS

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK//TOTAL CONTRACT ISSUANCES //TONNES OF GOLD

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AND NOW NOVEMBER:

NOVEMBER: SO FAR ONE ISSUANCE:

WHICH NOW BRINGS US TO NOVEMBER WHERE WE RECEIVED NOTICE OF OUR FIRST ISSUANCE OF 450 CONTRACTS FOR 45000 OZ OR 1.3996 TONNES.

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 10 MONTH TOTALS 131.6996 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 54 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES IN AUGUST AND THEN ADDED 24 TONNES IN SEPT. AND THUS THEIR SHORTFALL TO THE BIS IS 54 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 10TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH NOV//ONLY MISSING JUNE. TOTAL 10 MONTHS ISSUANCE 131.6996 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW NOVEMBER COMEX CONTRACT MONTH//

IN TOTAL WE HAD A TINY SIZED GAIN ON OUR TWO EXCHANGES OF 86 CONTRACTS WITH OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 2.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT/ NOVEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS FINALLY A LOWER T.A.S ISSUANCE CONTRACTS AS THE 5 CONSECUTIVE MEGA HUGE ISSUANCES HAS ENDED. THE CME NOTIFIES US THAT THEY HAVE ISSUED 1229 T.A.S CONTRACTS. THESE LAST 5 CONSECUTIVE MEGA HUGE T.A.S ISSUANCES WERE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING THE WEEK FINISHING OFF WITH A MASSIVE HUGE RAID ON GOLD AND SILVER LAST THURSDAY AFTERNOON THROUGH TO MONDAY, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS ALWAYS ENDS IN FAILURE AS WE WE WILL NOW SEE GOLD//SILVER RISE HUGELY ON OUR UPCOMING DAYS.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS: SEPT THROUGH NOVEMBER;

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE FINISHING OPTION EXPIRY WEEK, THE CROOKS GOADED OUR SPECULATORS TO CONTINUE ONTO THE SHORT SIDE WITH THE BANKERS ON THE LONG SIDE…THE RAIDS THROUGHT THIS WEEK WERE FREQUENT BUT FAILED TO CAUSE ANY DAMAGE TO THE PRICE WITH OPTIONS EXPIRY FINISHING OCT 31 AS WE NOW ENTER OUR MONTH OF NOVEMBER WITH EARLY MONTH FAILED RAID ATTEMPTS. SO THEY NOW ISSUED THESE MEGA T.A.S. CONTRACTS AND THAT ALWAYS SIGNALS A MAJOR RAID WHICH ARRIVED ON OUR DOORSTEP THURSDAY EARLY AFTERNOON AND CONTINUED RIGHT THROUGH MONDAY AND NOW TODAY.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 8 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. AND NOW NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 4.024 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 15.0828 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES///NEW STANDING ADVANCES TO 36.0736 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 54+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 54 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 54 TONNES REMAIN ON THE BOOKS OF THE BIS.

THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING E.G. NOVEMBER: A HUGE INITIAL 15.651 TONNES STANDING IN AN OFF MONTH!! THIS IS HUGE!!!//WITH QUEUE JUMPS AND EXCHANGE FOR RISK NEW STANDING FOR GOLD NOW AT 32.0496 TONNES

EXCHANGE FOR PHYSICAL ISSUANCE/NOV//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 2523 CONTRACTS.

THAT IS A STRONG SIZED 2523 EFP CONTRACT WAS ISSUED: : /DEC 2523 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2523 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 54 TONNES

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY + GOVERNMENT LIQUIDATION AND MASSIVE LIQUIDATION LATE THURSDAY AND FRIDAY/VERY EARLY AFTERNOON CLOSE TO CLOSING TIME

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE OCT 31 WITH OUR ATTEMPTED FAILED RAID, WE WILL SEE THESE MONTHLY MONTH SPREADERS IN ACTION NEXT WEEK DURING OPTIONS EXIRY WEEK.

T.A.S.SPREADER ISSUANCE//NOV

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT// WEDNESDAY MORNING WAS A MUCH SMALLER SIZED 1229 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE THIS MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP TUESDAY’S LOSS IN PRICE IN GOLD YET A CORRESPONDING VERY FAIR LOSS OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 5 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S FIRST ISSUANCE FOR 1.36996 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

GOLD STANDING AT THE COMEX FOR GOLD LAST 11 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

AND NOW NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 4.024 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 15.0829 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 1.3966 TONNES.

/STANDING ADVANCES TO 36.0736 TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING NOVEMBER,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $6.30/ /) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS CENTRAL BANKS (FRBNY + OTHER CENTRAL BANKS) TOOK THE LONG SIDE AS WE DID HAVE A VERY STRONG GAIN IN OI FROM TWO EXCHANGES OF 16,121 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION TUESDAY// COMEX TRADING//.. OTHER CENTRAL BANKS TENDERED FOR PHYSICAL TUESDAY NIGHT WHICH EXPLAINS THE HUGE NUMBER OF NOTICES FILED!!. THE COMEX IS ONE BIG MESS!! THIS WEEK, THE BANKER (FRBNY) WENT TO THE SHORT SIDE AND SPECS AND OTHER CENTRAL BANKERS ON THE LONG SIDE. THE SPECS WILL BE QUITE NICELY RINSED BY THE FRBNY BANKERS IN A TIMELY FASHION!!

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

STANDING FOR GOLD OCT AND NOVEMBER:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 4.024 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 15.0826 TONNES TO WHICH WE ADD OUR FIRST ISSUANCE OF EXCHANGE FOR RISK OF 1.3966 TONNES..

NEW STANDING ADVANCES TO 36.0736 ONNES OF GOLD.

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $6.30

WE HAD A HUGE 14,687 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

INITIAL GOLD COMEX

NOV 19

NOV CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES i) Out of Brinks 255,568.299 oz (7549 kilobars) 7.549 tonnes of gold |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 876 notice(s) 87,600 OZ 2.725 TONNES OF GOLD |

| No of oz to be served (notices) | 708 contracts 70,800 OZ 2.202 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,440 notices 1,044,000 0z 32.472 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

1 ENTRIES

i) Out of Brinks 255,568.299 oz

(7549 kilobars)

7.549 tonnes of gold

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs \2 both dealer to customer

a) Brinks 15,914.745 oz

b) Manfra: 6,403.437 oz

AMOUNT OF GOLD STANDING FOR NOVEMBER:

THE FRONT MONTH OF NOV STANDS AT 1584 CONTRACTS FOR A HUGE GAIN OF 376 CONTRACTS.

WE HAD 918 CONTRACTS SERVED ON TUESDAY. SO WE GAINED A MEGA HUGE 1294 CONTRACTS FOR 129,400 OZ OF GOLD (4.024 TONNES).

DECEMBER LOST 11876 CONTRACTS DOWN TO 220,860 CONTRACTS . DECEMBER IS THE NEW FRONT MONTH AND WE ARE GOING TO HAVE A DILLY MONTH STANDING FOR DELIVERY FOR GOLD!!

JANUARY GAINED 96 CONTRACTS UP TO 1343

We had 876 contracts filed for today representing 91,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 918 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 190 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2025. contract month, we take the total number of notices filed so far for the month (10,440 oz ) to which we add the difference between the open interest for the front month of NOV ( 1584 CONTRACTS) minus the number of notices served upon today (876 x 100 oz per contract) equals 1,114,800 OZ OR 34.674 Tonnes of gold to which we add our first issuance of exchange for risk for 1.3996 tonnes//new standing advances to 36.0736 tonnes.

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (10,440x 100 oz +we add the difference for front month of NOV (1684 OI} minus the number of notices served upon today (876)x 100 oz) which equals 1,114,800 OZ OR 34.674 TONNES to which we add our 1.3996 tonnes of exchange for risk//new total of gold standing in November is 36.0736 tonnes

TOTAL COMEX GOLD STANDING FOR NOV..: 36.0736 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE ACTIVE DELIVERY MONTH OF NOVEMBER

volume TUESDAY confirmed 245,142 contracts GOOD

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,970,845.069 oz 61.30 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,969,175.891 oz

TOTAL REGISTERED GOLD 19,454,033.425 or 605.10 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,515,142.466 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,505,506 oz ((REG GOLD- PLEDGED GOLD)=

544.49 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE NOV. 2025 SILVER CONTRACTS

NOV 19 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of ASAHI 1,8932,870.600 OZ ii) Out of CNT 45,057.669 oz iii) Out of hsbc 300,807.35 oz iv) Out of JPMorgan 825,477.300 oz total withdrawal: 3,104,314.910 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 1 entries I) Into Delaware 9987.208 oz total deposit 9987.208 oz |

| No of oz served today (contracts) | 333 CONTRACT(S) ( 1,680,000 OZ 1.680 MILLION OZ |

| No of oz to be served (notices) | 51 contracts (0.255MILLION oz) |

| Total monthly oz silver served (contracts) | 3802 Contracts (18.010 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 entries

I) Into Delaware 9987.208 oz

total deposit 9987.208 oz

`

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

4 entries

i) Out of ASAHI 1,8932,870.600 OZ

ii) Out of CNT 45,057.669 oz

iii) Out of hsbc 300,807.35 oz

iv) Out of JPMorgan 825,477.300 oz

total withdrawal: 3,104,314.910 oz

adjustments: 2 dealer to customer

a) JPmorgan: 2,311612.625 oz

b) Manfra: 1,245,023.393 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 152.547 MILLION OZ//.TOTAL REG + ELIGIBLE. 462.520 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF NOVEMBER /2025 OI: 384 OPEN INTEREST CONTRACTS FOR A GAIN OF 251 CONTRACTS. WE HAD 44 NOTICES SERVED ON TUESDAY SO WE GAINED 295 CONTRACTS FOR A 1.475 MILLION OZ QUEUE JUMP.

DECEMBER LOST 2902 CONTRACTS DOWN TO 59,430. THIS IS THE FRONT MONTH FOR SILVER DELIVERIES AND WE WILL HAVE A STRONG STANDING FOR OUR SILVER METAL.

JANUARY GAINED 35 CONTRACTS UP TO 2281 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 333 or 1.680 MILLION oz

CONFIRMED volume; ON TUESDAY 95,322 huge//

AND NOW NOVEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 3802 X5,000 oz = 18.010MILLION oz

to which we add the difference between the open interest for the front month of NOV (384) AND the number of notices served upon today (333 )x (5000 oz)

Thus the standings for silver for the NOVEMBER 2025 contract month: (3802) Notices served so far) x 5000 oz + OI for the front month of NOV(384) minus number of notices served upon today (333)x 5000 oz equals silver standing for the NOV.contract month equating to 19.265 MILLION OZ

New total standing: 19.265million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 152.547 million oz of registered silver

JPMorgan as a percentage of total silver: 199.675/462.530million. 43.29%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

NOV 19/WITH GOLD UP $14.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 18/WITH GOLD DOWN $6.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 17/WITH GOLD DOWN $20.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.93 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1044.000 TONNES

NOV 14/WITH GOLD DOWN $97.55TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1048.93 TONNES

NOV 13/WITH GOLD DOWN $17.80.TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1064.64 TONNES

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT XXX TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

NOV 3 WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 1.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1039,20 TONNES

OCT 31 WITH GOLD DOWN $17.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1040.35 TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

OCT 23 WITH GOLD UP $78.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37 TONNES

OCT 22 WITH GOLD DOWN $78.95 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

GLD INVENTORY: 1041.43 TONNES, TONIGHTS TOTAL

SILVER

NOV 19/WITH SILVER UP $0.36 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 18/WITH SILVER DOWN $0.13 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489..283 MILLION OZ MILLION OZ

NOV 17/WITH SILVER DOWN $0.07 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.451 MILLION OZ INTO THE SLV:INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 14/WITH SILVER DOWN $2.08 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.722 MILLION OZ INTO THE SLV:

INVENTORY RESTS AT 487.832 MILLION OZ MILLION OZ

NOV 13/WITH SILVER DOWN $0.58 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 4 WITH SILVER DOWN $0.82 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

NOV 3 WITH SILVER $0.12 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 31 WITH SILVER DOWN $0.35 TODAY/SMALL CHANGES IN SILVER AT THE SLV: ///A WITHDRAWAL OF 636,000 OZ FROM THE SLV// ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

OCT 23 WITH SILVER UP $0.87 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 501.474 MILLION OZ

OCT 22 WITH SILVER DOWN $0.33 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.995 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 504.015 MILLION OZ

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

CLOSING INVENTORY 489.283 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

THIS IS IMPORTANT;

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MCLEOD….

3.CHRIS POWELL, Secretary/Treasurer//GATA DISPATCHES

Italian lawmakers seek to revive state claim on central bank’s $300 billion gold reserves

Submitted by admin on Wed, 2025-11-19 08:54 Section: Daily Dispatches

By Giuseppe Fonte and Giselda Vagnoni

Reuters

Tuesday, November 18, 2025

ROME — Italian lawmakers have revived attempts to establish that the central bank’s $300 billion in gold reserves belong to the state, presenting a proposal to parliament.

All five lawmakers who signed the proposal, which was tabled as an amendment to next year’s budget, are senators from Prime Minister Giorgia Meloni’s Brothers of Italy party.

The Bank of Italy sits on the world’s third-largest national gold stockpile, behind only the United States and Germany. Its 2,452 metric tons of gold are equivalent to around 13% of national output.

Unlike Britain or Spain, Italy has refused to sell off gold during financial downturns, retaining its reserves even through the 2008 debt crisis. Central banks generally accumulate gold to hedge against adverse scenarios and preserve confidence in the financial system.

Around 1,100 tons of the Bank of Italy’s gold are stored in a vault beneath its headquarters at Palazzo Koch in Rome. A similar portion is held in the United States, while smaller amounts are kept in Britain and Switzerland.

Politicians of all parties have called in the past 20 years to clarify ownership of the gold and then sell it to cut Italy’s public debt, which totals more than 3 trillion euros ($3.48 trillion) and is predicted by the Italian Treasury to peak at 137.4% of GDP next year. …

… For the remainder of the report:

end

Craig Hemke: What’s next for silver prices?

Submitted by admin on Tue, 2025-11-18 20:00 Section: Daily Dispatches

By Craig Hemke

Sprott Money, Toronto

Tuesday, November 18, 2025

After making new all-time intraday highs last week, there are all sorts of prognostications regarding what’s next for the silver price. Let’s discuss the most likely scenario.

First and foremost, we need to establish that this time is different. The situation economically, monetarily, and physically is entirely different from 1980 and 2011. If you don’t understand what I mean, please check out this post from two weeks ago:

https://www.sprottmoney.com/blog/silver-prices-test-your-senses-spot-price-analysis

In that post, you were reminded that in late 1979 and early 1980, the silver price moved from $10 to $48 in four months and then fell back to $10 in two months. In 2010 and 2011, the price moved from $18 to $48 in eight months and then fell back to $26 a few months later.

Is the current attempt to break through $48/ounce any different?

On the chart below, note that price first reached $48 on October 3 and here we are, more than six weeks later, and price is still trading above $50/ounce. That’s a big difference from 1980 and 2011. …

…Dispatch continues below …

https://www.sprottmoney.com/blog/whats-next-silver-prices-2025-breakout-analysis

end

Elliot going for gold; He is building his stake in Barrick/.wrong company. Should be Agnico eagle

(London Financial Times)

Elliott builds stake in Barrick amid speculation company might be broken up

Submitted by admin on Tue, 2025-11-18 10:03 Section: Daily Dispatches

By Leslie Hook, Oliver Barnes, and Arash Massoudi

Financial Times, London

Tuesday, November 18, 2025

Activist hedge fund Elliott Management has built a large stake in Barrick Mining, according to people familiar with the matter, after the world’s second-largest gold producer struggled to capitalise on a blistering bullion rally.

Elliott’s investment comes as the Toronto-based miner has pledged to refocus on its lucrative North American business after the sudden departure of its chief executive Mark Bristow in September, adding to speculation that the company could be planning a break-up or asset sales.

Elliott’s stake puts it among Barrick’s 10 largest investors, the people said. That would mean the hedge fund’s holding is worth at least $700 million (C$1 billion).

As bullion has soared to record highs in recent months, boosting gold miners’ valuations, Barrick’s share price performance has lagged rivals and the company has faced a series of setbacks, including losing control of a key mine in Mali.

However, the people said Elliott was encouraged by the idea that Barrick could split into two companies, separating its higher-growth North American operations from its mines in riskier regions across Asia and Africa. …

… For the remainder of the report:

end

Interesting!

Indonesia plans taxes of up to 15% on gold exports next year

Submitted by admin on Mon, 2025-11-17 08:29 Section: Daily Dispatches

By Gayatri Suroyo

Reuters

Monday, November 17, 2025

JAKARTA — Indonesia will charge taxes on exports of gold of between 7.5% and 15% in a plan that will be implemented some time next year, a senior finance ministry official said today.

The tax policy, currently being finalised, is being designed so that lower rates are applied to processed goods to help encourage domestic processing, Febrio Kacaribu, the ministry’s director general of fiscal strategy, told a parliamentary hearing.

For example, a higher rate for gold dore — bars or ingots with impurities — and a lower rate for minted bars would be charged, he said.

Global gold prices will also be a factor in determining the taxes, he said, noting that higher rates are likely to be applied when prices are at or above $3,200 per troy ounce to capture miners’ windfall profits. …

… For the remainder of the report:

end

Chris Powell

important to listen to him!!

GATA secretary discusses many gold topics in interview with Soar Financially

Submitted by admin on Sun, 2025-11-16 19:01 Section: Daily Dispatches

7:05p ET Sunday, November 16, 2025

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed at the New Orleans Investment Conference by Soar Financially’s Kai Hoffman, discussing the continuing intervention against gold by central banks in the London and New York markets, the steady transfer of physical gold from West to East, and the realization by many governments and central banks that gold remains the ultimate money and that the United States no longer can be trusted as the custodian of foreign assets.

lso discussed were deception in official gold data maintained by the International Monetary Fund, the sudden disappearance of President Trump’s desire to audit the U.S. gold reserve at Fort Knox, China’s realization that gold is its most powerful weapon against U.S. influence around the world, and the possibility of an official revaluation of gold.

Gold, your secretary/treasurer says, is both the playground and battlefield of central banks and gold reserves are held primarily for currency market intervention.

The discussion is 22 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS /249

SHANGHAI CLOSED UP 6.93 POINTS OR 0.18%

//Hang Seng CLOSED CLOSED DOWN 99.38 PTS OR 0.38%

// Nikkei CLOSED : DOWN 165.28 PTS OR 0.34% //Australia’s all ordinaries CLOSED DOWN 0.24%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1125/ OFFSHORE CLOSED UP AT 7.1139/ Oil UP TO 60.38 dollars per barrel for WTI and BRENT UP TO 64.40 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.1125 OFFSHORE YUAN TRADING UP TO 7.1139:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1105

OFFSHORE YUAN: UP TO 7.1139

HANG SENG CLOSED DOWN 99.38 PTS OR 0.38%

2. Nikkei closed DOWN 165.28 PTS OR 0.34%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 99.65 – EURO FALLSS TO 1.1568 DOWN 12 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.772//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.98…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA/NEW PRIME MINSTER TAKAICHI. JAPAN 30 YR BOND YIELD: 3.3444 UP 4 FULL BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP/JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7962/ Italian 10 Yr bond yield UP to 3.450 SPAIN 10 YR BOND YIELD UP TO 3.206

3i Greek 10 year bond yield DOWN TO 3.348

3j Gold at $4112.60 Silver at: 52.28 1 am est) SILVER NEXT RESISTANCE LEVEL AT $54.00//AFTER 50.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 9/100 roubles/dollar; ROUBLE AT 80.76

3m oil (WTI) into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.98 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.772% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.344 UP 4 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8021 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9279 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.126 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.743 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.579 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.36 UP 3 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.5520 DOWN 1 PTS

30 YR UK BOND YIELD: 5.3850 DOWN 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.257 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.819 UP 1 BASIS PTS.

a New York OPENING REPORT

Futures Rebound After 4 Day Slide With Nvidia Earnings On Deck

by Tyler Durden

Wednesday, Nov 19, 2025 – 08:43 AM

After 4 days of steep declines, futures are finally higher ahead of Nvidia earnings, with AI bulls hoping for strong numbers to provide respite from the market selloff. As of 8:00am ET, S&P futures are 0.3% higher and Nasdaq futs gains 0.4%, both bracing for big moves later: NVDA alone has accounted for almost 20% of S&P 500 gains this year. FOMC minutes and a batch of retailer earnings are also due. Pre-mkt, Mag 7 names are mostly higher: NVDA (+1.4%) leads gains while AAPL (-0.1bp) is dragging the other end; semis are higher, too as the AI theme is seeing a pre-mkt bid. Cyclicals are flat versus Defensives with Fins/Materials and HC leading their respective factors higher. The dollar edges higher, with Aussie and kiwi at the bottom of G-10 scoreboard; USDJPY spiked above 156 as the yen is flooded with devaluation fears again. Treasury 10-year yield dips 2bps to 4.11% even as the yield curve bear steepens. In other assets, Bitcoin’s slide is continuing. According to JPM, the market setup appears to be poised for an ‘Everything Rally’ as the market receives new macro data (Fed Mins and Mtge Apps) and old data (Trade) before the NVDA print. Today’s US economic calendar includes the August trade balance (8:30am); the Fed speaker slate includes Miran (10am), Barkin (12:45pm) and Williams (2pm). Minutes of FOMC’s Oct. 28-29 meeting are due at 2pm

In premarket trading, Mag 7 stock are mostly higher (Alphabet +1.6%, Tesla +0.9%, Nvidia +1.4%, Amazon +0.4%, Meta +0.05%, Microsoft -0.09%, Apple -0.1%).

- Agios Pharmaceuticals (AGIO) tumbles 37% after the company’s Phase 3 trial of mitapivat in patients 16 and older with sickle-cell disease met one primary endpoint but missed another.

- Constellation Energy Corp. (CEG) is up 2% as its plan to restart its shuttered Three Mile Island nuclear plant is getting $1 billion in backing from the US government as the Trump administration pushes to add more atomic power on the electric grid.

- DoorDash (DASH) rises 2% after Jefferies upgraded the stock to buy from hold, with the analyst noting that the food delivery company’s annual forecast helped lower expectations, providing flexibility for both long-term investments and upside to estimates.

- Dycom Industries (DY) gains 6% after saying it will acquire Power Solutions, one of the Mid-Atlantic’s largest electrical contractors serving data centers.

- La-Z-Boy (LZB) shares are up 11% after the home furniture retailer reported both sales and adjusted earnings per share for the second quarter that beat Wall Street’s expectations.

- Lowe’s (LOW) rises 6% as adjusted EPS and gross margin for the third quarter topped expectations, and comparative sales, while short of the consensus estimate, were better than feared after Home Depot’s report on Tuesday.

- Plug Power Inc. (PLUG) sinks 19% on the green hydrogen company’s plans for a private offering of $375 million in convertible senior notes due 2033.

- SEMrush Holdings (SEMR) soars 69% after the WSJ reported that Adobe is nearing a $1.9 billion deal to acquire the company.

- Unity Software (U) gains 8% after the company announced it is working with Epic Games to bring Unity games into Fortnite.

In corporate news, South Korean antitrust regulators were said to have visited the Seoul offices of Arm Holdings this week as part of an inquiry into its licensing practices, following a complaint by Qualcomm. The US government is providing $1 billion in backing to Constellation Energy’s plan to restart its Three Mile Island nuclear plant in Pennsylvania.

The S&P 500 has lost more than 3% this month as the tech giants that powered much of 2025’s gains came under pressure. Nvidia’s results, due after the close, are seen as a bellwether for whether lofty valuations and massive capital spending in artificial intelligence remain justified.

For Benoit Peloille, chief investment officer at Natixis Wealth Management, the recent retreat “could easily morph into a 10% to 15% correction” for the S&P 500. “I’m not sure that even very good results from Nvidia would be enough to prevent that,” he said.

Comments at the Bloomberg New Economy Forum in Singapore are largely cautious, with Goldman Sachs President John Waldron saying the market could pull back further, Atlas Merchant Capital’s Bob Diamond talking about a “healthy correction” and Algebris Investments’ CEO Davide Serra warning of a “significant correction” for big AI stocks.

Others are staying positive. Fidelity International fund manager Joseph Zhang sees AI spending and usage as “still in the early stage of the party.” As for Nvidia numbers, analysts are estimating more than 50% growth for both net income and sales for the quarter (more in our full preview to follow). And despite all the talk of stretched tech valuations, the stock is now trading at about 29x forward earnings, far below the 10-year average of 35x.

The big question is how the market will interpret the numbers. JPMorgan strategists see room for Nvidia to zoom higher on a beat-and-raise and recommend buying call spreads. Barclays strategists, meanwhile, note the stock has posted negative one-week returns following four of the last five earnings releases. The options markets implies a 7% swing in either direction post-earnings.

Microsoft, Amazon.com, Alphabet and Meta — which account for more than 40% of Nvidia’s sales — are projected to boost combined AI spending 34% to $440 billion over the next year, according to data compiled by Bloomberg. The risk is that such projections could falter if major AI players, including OpenAI, scale back their commitments. Options suggest an earnings-related move of about 7%, signaling the big potential impact on the market if the results deviate.

The recent slide has made the stock more attractive, said Louis Puga, a fund manager at Societe de Gestion Prevoir and holder of Nvidia shares. “Paying 26 times for Nvidia’s next-year profits, sorry but I don’t see a bubble there,” Puga said. “We are like at the start of a gold rush: Nvidia is supplying the shovels and it doesn’t matter who finds the gold.”

Elsewhere, Elon Musk returned to the White House on Tuesday evening in a sign that tensions between Trump and the world’s richest man have thawed. Trump also gave Saudi Arabia’s crown prince a lavish reception in Washington. Trump said he thinks he’s identified his choice to be the next chair of the Fed, while asserting people are holding him back from firing Powell.

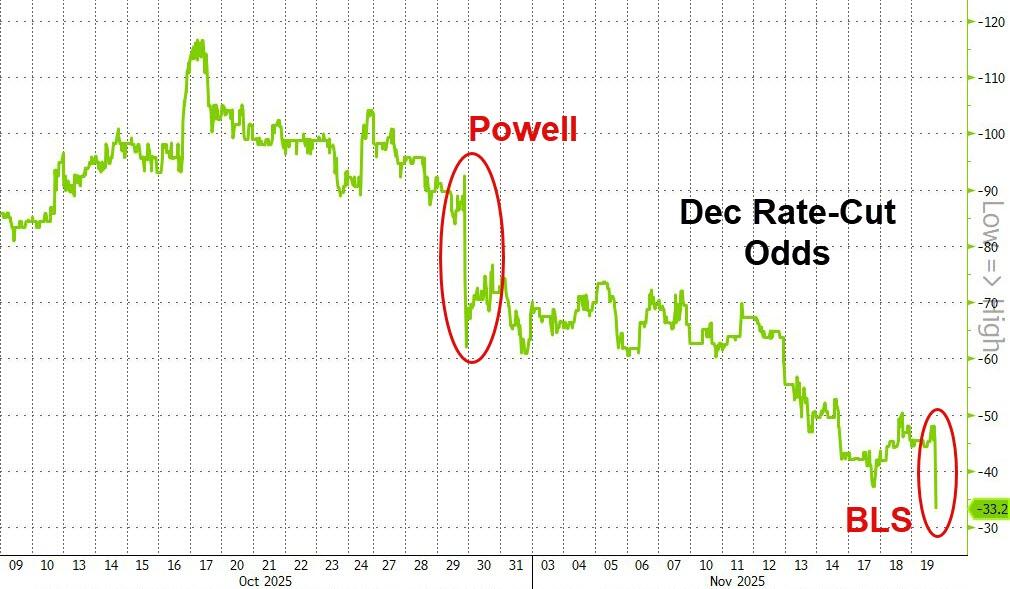

Investors will also be watching the release of minutes from the Federal Reserve’s meeting last month. The unwinding of expectations for a December interest-rate cut has added to the market malaise, with traders now seeing less than a 50% chance of a quarter-point reduction.

“We expect the minutes to show a deeply divided Fed with concerns over a weaker employment picture, but sticky inflation,” wrote Mohit Kumar, chief economist and strategist for Europe at Jefferies.

European equities edged higher on Wednesday with media and mining stocks leading gains, while the biggest laggards are utilities and real estate shares. Stoxx 600 gain 0.1% to 562.58 with 222 members down, 370 up, and 8 little changed. Here are the biggest movers Wednesday:

- Rotork shares gain as much as 5.2%, the most since early August, after the valve manufacturer announced a new £50m share buyback and delivered a “very healthy performance” in the four months to the end of October, according to Jefferies

- NKT shares jump as much as 12%, the most since April and to a fresh record high, after the Danish cable manufacturer reported its latest earnings and presented new 2030 targets

- WH Smith shares rise as much as 4.7%, reversing an initial slide, as analysts find some positives amid the publication of an independent review by Deloitte that led to the resignation of CEO Carl Cowling

- SMA Solar surges as much as 13%, hitting the highest since June 2024, as Jefferies upgrades the renewable energy equipment firm to buy, saying it has “weathered the worst”

- European defense companies slipped in Wednesday lunchtime trading as Politico reported that the White House is on the brink of unveiling a major new peace agreement with Russia that officials say will bring war with Ukraine to an end

- Enel shares drop as much as 2.4% while Endesa falls as much as 3.1% after the pair were cut to underperform from sector perform at RBC, with expectations “looking too optimistic” and valuations too high

- Kering shares drop as much as 4%, most in nearly two weeks, after Chief Executive Officer Luca de Meo said the company must reduce its reliance on its flagship Gucci brand

- Vivendi slumped on Wednesday after Le Monde reported that billionaire Vincent Bolloré’s eponymous holding company could escape having to pay anything to compensate minority shareholders over the recent split of the group

- Interparfums shares fall as much as 11% to the lowest level since October 2020, after the French maker of personal care products didn’t provide a sales forecast for next year on the back of the current economic and geopolitical backdrop

Earlier in the session, Asian stocks fell, heading for a four-day losing streak as investors stayed cautious ahead of Nvidia’s earnings and lingering doubts over the durability of the AI-driven rally. The MSCI Asia Pacific Index declined 0.2%, with Samsung, Xiaomi and TSMC among the biggest drags. Losses in South Korea and Australia offset gains in China. Hang Seng Tech Index falls about 1% and Kospi drifts lower. Japanese and mainland China indexes are broadly steady.

In FX, the dollar edges marginally firmer, with Aussie and kiwi at the bottom of G-10 scoreboard.

In rates, treasury 10-year yield hovers little changed around 4.11% ahead of Wednesday’s 20-year bond auction and FOMC meeting minutes release; German gilts are about 2bps richer on the day; gilt curve pivots steeper around little-changed 10-year sector. Australian yields ease 1-2 bps across the curve. JGB futures pare losses after 20-year auction draws demand in line with 12-month average. UK front-end outperforms as more easing by Bank of England is priced in after October UK services inflation slowed more than forecast; UK 2-year yields down around 2.5bp. Treasury auctions resume with $16 billion 20-year bond sale at 1pm, with $19 billion 10-year TIPS ahead Thursday. WI 20-year yield near 4.705% is ~20bp cheaper than last month’s, which stopped through by 1.2bp

In commodities, Brent crude futures are near $64.70; gold rises to near $4,090 an ounce. Bitcoin slides below $91k as investors pulled more than half a billion dollars from BlackRock’s iShares Bitcoin Trust on Tuesday, the largest single-day outflow since the fund’s debut. Bitcoin has fallen almost 30% from a record high set in October, entering oversold territory on a technical RSI measure.

The US economic calendar includes August trade balance (8:30am). Fed speaker slate includes Miran (10am), Barkin (12:45pm) and Williams (2pm). Minutes of FOMC’s Oct. 28-29 meeting are due at 2pm

Market Snapshot

- S&P 500 mini +0.3%

- Nasdaq 100 mini +0.4%

- Russell 2000 mini +0.4%

- Stoxx Europe 600 little changed

- DAX little changed

- CAC 40 -0.2%

- 10-year Treasury yield +1 basis point at 4.13%

- VIX -0.8 points at 23.9

- Bloomberg Dollar Index +0.2% at 1221.39

- euro -0.1% at $1.1569

- WTI crude -0.6% at $60.39/barrel

Top Overnight News

- Trump said he would formally designate Saudi Arabia as a major non-NATO ally after meeting with Mohammed bin Salman. The countries signed several agreements and made progress on a long-sought nuclear technology-sharing deal. BBG

- The Trump administration has been secretly working in consultation with Russia to draft a new plan to end the war in Ukraine, report US and Russian officials. Axios