access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XGE: COMEX

323 C HSBC 66

363 H WELLS FARGO SECURITI 33

624 H BOFA SECURITIES 807

661 C JP MORGAN SECURITIES 724

709 C BARCLAYS 11

905 C ADM 5

JPMORGAN STOPPED: 724/823

GOLD: NUMBER OF NOTICES FILED FOR NOV/2025: 823 CONTRACTs NOTICES FOR 82,300 OZ or 2.559 TONNES

total notices so far: 11,916 contracts for 1,191.600 OR 37.063 tonnes)

SILVER NOTICES: 31 NOTICE(S) FILED FOR 0.155 MILLION OZ/

total number of notices filed so far this month : 3897 CONTRACTS (NOTICES) for 19.485 million oz

INITIAL STANDING FOR NOV: 11.575 MILLION OZ

WEDNESDAY: 1.475 MILLION OZ

THURSDAY: 0.250 MILLION OZ

FRIDAY: AN EFP TRANSFER OF 20,000 OZ AND THIS WILL BE SUBTRACTED FROM OUR PREVIOUS TOTAL

MONDAY: ZERO GAIN.

TUESDAY: A SMALL 10,000 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON

THEN ALL PREVIOUS QUEUE JUMPS OF 8.155 MILLION OZ- 0.03 MILLION EFP TRANSFER.

EQUALS

19.485 MILLION OZ STANDING FOR SILVER.

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOV: 30.705 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

AND NOW NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ EXCHANGE FOR PHYSICAL TRANSFER WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING REDUCES TO 19.485 MILLION OZ/

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 1.723 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 19.8317 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3996 TONNES//NEW STANDING ADVANCES TO 38.5186 TONNES OF GOLD.

NEW STANDING FOR GOLD, NOV CONTRACT AT 38.5186 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 118.60 TONNES//VERY SMALL THIS MONTH.

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 5294 CONTRACTS OI TO 148,942 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 200 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF5294 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 5094 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $0.43 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 25.470 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.43

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 33.04 POINTS OR 0.87%

//Hang Seng CLOSED UP 178.05 PTS OR 0.69%

// Nikkei CLOSED UP 33.04 PTS OR 0.07% //Australia’s all ordinaries CLOSED UP 0.27%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.0856/ OFFSHORE CLOSED UP AT 7.0846/ Oil UP TO 58.63 dollars per barrel for WTI and BRENT UP TO 63.10 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.0856 OFFSHORE YUAN TRADING UP TO 7.0846:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

SHANGHAI CLOSED UP 1.87 POINTS OR 0.05%

//Hang Seng CLOSED UP 496.48 PTS OR 1.97%

// Nikkei CLOSED HOLIDAY //Australia’s all ordinaries CLOSED UP 1.34%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1071/ OFFSHORE CLOSED UP AT 7.1079/ Oil UP TO 57.71 dollars per barrel for WTI and BRENT DOWN TO 62.21 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.1071 OFFSHORE YUAN TRADING UP TO 7.1079:/ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A MEGA MEGA HUGE SIZED SIZED 28,079 CONTRACTS TO 442,270 OI DESPITE OUR GAIN IN PRICE OF $18.55 WITH RESPECT TO MONDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2400). WE HAD ZERO T.A.S. LIQUIDATION MONDAY.. IT SEEMS THAT THE SPECULATORS WERE WIPED OUT FROM THE LONG SIDE WITH OUR FRBNY MOVING TO THE LONG SIDE AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE . JUDGING BY THE NOTICES FOR DELIVERY FILED LAST NIGHT AT 823 NOTICES FOR 82,300 OZ (2.559 TONNES), THE EASTERN CENTRAL BANKERS TOOK EVERYTHING THEY COULD ON OFFER. THE FRBY HAS NOW ENGINEERED ANOTHER SMALL RAID EARLY TUESDAY AS THE SPECS WENT TO THE SHORT SIDE AND THEY WILL BE RINSED IN SHORT ORDER!!

WE THUS HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 25,679 CONTRACTS (OR 79L87 TONNES). THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

FIRST LETS DO A REVIEW OF EXCHANGE FOR RISK ISSUANCES:

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD PRIOR MONTHS

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES. THE RECIPIENT OF THESE EXCHANGE FOR RISK IS THE BANK OF ENGLAND. THIS CENTRAL BANK LOANED OUT ITS GOLD AND WANTS IT BACK. THEIR TOTAL RESERVES PRIOR TO THE LOANS IS LISTED AT 310 TONNES.

LET US LOOK AT JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

NOW LET US LOOK AT THE MONTH OF AUGUST:

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

NOW LET US LOOK AT SEPT.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FOR 14.553 TONNES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

LET’S SUM UP EXCHANGE FOR RISK FOR THE LAST 8 MONTHS

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK//TOTAL CONTRACT ISSUANCES //TONNES OF GOLD

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AND NOW NOVEMBER:

NOVEMBER: SO FAR ONE ISSUANCE:

WHICH NOW BRINGS US TO NOVEMBER WHERE WE RECEIVED NOTICE OF OUR FIRST ISSUANCE OF 450 CONTRACTS FOR 45000 OZ OR 1.3996 TONNES.

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 10 MONTH TOTALS 131.6996 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 54 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES IN AUGUST AND THEN ADDED 24 TONNES IN SEPT. AND THUS THEIR SHORTFALL TO THE BIS IS 54 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 10TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH NOV//ONLY MISSING JUNE. TOTAL 10 MONTHS ISSUANCE 131.6996 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW NOVEMBER COMEX CONTRACT MONTH//

IN TOTAL WE HAD A MEGA HUGE SIZED LOSS ON OUR TWO EXCHANGES OF 25,679 CONTRACTS DESPITE OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 2.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT/ NOVEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG T.A.S ISSUANCE CONTRACTS AS THE 5 CONSECUTIVE MEGA HUGE ISSUANCES HAS ENDED. THE CME NOTIFIES US THAT THEY HAVE ISSUED 4036 T.A.S CONTRACTS. THE 5 CONSECUTIVE MEGA HUGE T.A.S ISSUANCES IN NOVEMBER WERE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK FINISHING OFF WITH A MASSIVE HUGE RAID ON GOLD (AND SILVER) DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS ALWAYS ENDS IN FAILURE AS WE WE WILL NOW SAW GOLD//SILVER RISE HUGELY YESTERDAY.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS: SEPT THROUGH NOVEMBER;

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE FINISHING OPTION EXPIRY WEEK, THE CROOKS GOADED OUR SPECULATORS TO CONTINUE ONTO THE SHORT SIDE WITH THE BANKERS ON THE LONG SIDE…THE RAIDS THROUGHT THIS WEEK WERE FREQUENT BUT FAILED TO CAUSE ANY DAMAGE TO THE PRICE WITH OPTIONS EXPIRY FINISHING OCT 31 AS WE NOW ENTER OUR MONTH OF NOVEMBER WITH EARLY MONTH FAILED RAID ATTEMPTS. SO THEY NOW ISSUED THESE MEGA T.A.S. CONTRACTS AND THAT ALWAYS SIGNALS MAJOR RAIDS WHICH ARRIVED ON OUR DOORSTEP EARLY NOV. MONTH AND CARRIED ON IN FULL FORCE TO THIS DAY.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 8 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. AND NOW NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 1.723 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 19.6545 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES///NEW STANDING ADVANCES TO 38.5186 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 54+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 54 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 54 TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING. IT LOOKS LIKE THE FRBNY IS QUITE NERVOUS, MAYBE I AM WRONG. WE MUST WAIT TO SEE THE DATA FROM BIS SWAPS FROM ROBERT LAMBOURNE TO SEE IF THEY WILL BEGIN TO COVER!!

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING:

E.G. NOVEMBER: A HUGE INITIAL 15.651 TONNES STANDING IN AN OFF MONTH!! THIS IS HUGE!!!//WITH QUEUE JUMPS AND EXCHANGE FOR RISK NEW STANDING FOR GOLD NOW AT 38.5186 TONNES

EXCHANGE FOR PHYSICAL ISSUANCE/NOV//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 2400 CONTRACTS.

THAT IS A STRONG SIZED 2400 EFP CONTRACT WAS ISSUED: : /DEC 2400 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2400 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 54 TONNES

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY + GOVERNMENT LIQUIDATION AND MASSIVE LIQUIDATION LATE THURSDAY /EARLY FRIDAY/

- MONTH END SPREADERS HAVE NOW BEGUN AS IT IS IN FULL FORCE THESE PAST TWO DAYS:COMEX OPTIONS EXPIRY WAS YESTERDAY, //LONDON OTC// LBMA// OPTION EXPIRES NOV 28!!

T.A.S.SPREADER ISSUANCE//NOV

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT// TUESDAY MORNING WAS A MUCH LARGER SIZED THAN NORMAL 4036 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP MONDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING STRONG GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 5 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S FIRST ISSUANCE FOR 1.36996 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY!

GOLD STANDING AT THE COMEX FOR GOLD LAST 11 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

AND NOW NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 1.723 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 19.8317 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 1.3966 TONNES.

/STANDING ADVANCES TO 38.5186 TONNES OF GOLD.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

AN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING NOVEMBER,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $18.55/ /) AND WERE QUITE SUCCESSFUL IN KNOCKING OFF HUGE NUMBERS OF SPECULATOR SHORTS WHO TRIED TO COVER WITH THE PRICE RISE AS CENTRAL BANKS (FRBNY + OTHER CENTRAL BANKS) TOOK THE LONG SIDE. WE DID HAVE A STRONG LOSS IN OI FROM TWO EXCHANGES OF 11,079 CONTRACTS WITH THE SPECULATOR SHORT LIQUIDATION.. BUT AS EXPLAINED ABOVE WE HAD SOME T.A.S. SPREADER LIQUIDATION MONDAY AND WE DID HAVE CONTINUATION OF MONTH END SPREADER LIQUIDATION// COMEX TRADING//.. OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL MONDAY NIGHT WHICH EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR DECEMBER. THE COMEX IS ONE BIG MESS!! THIS WEEK, THE BANKER (FRBNY) WENT TO THE LONG SIDE ALONG WITH OTHER EASTERN CENTRAL BANKERS AND SPECS LIQUIDATED ON THE SHORT SIDE SIDE. THE SPECS WERE QUITE NICELY RINSED BY THE FRBNY.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

STANDING FOR GOLD OCT AND NOVEMBER:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 1.713 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 19.8317 TONNES TO WHICH WE ADD OUR FIRST ISSUANCE OF EXCHANGE FOR RISK OF 1.3966 TONNES..

NEW STANDING ADVANCES TO 38.5186 ONNES OF GOLD.

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $18.55

WE HAD A HUGE 14,600 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL. ALL TIME RECORD REMOVAL

INITIAL GOLD COMEX

NOV 25

NOV CONTRACT MONTH

CME DID NOT PROVIDE INVENTORY CHANGES TONIGHT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entry i) One entry: out of Malca: 2515.157 oz total withdrawal 2515.157 or 0.07 tonnnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 823 notice(s) 82,300 OZ 2.558 TONNES OF GOLD |

| No of oz to be served (notices) | 18 contracts 1800 OZ 0.0559 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,916 notices 1,191,600 0z 37.063 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

1 ENTRIES

1 entry

i) One entry:

out of Malca: 2515.157 oz

total withdrawal 2515.157

or 0.07 tonnnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 3 all dealer to customer

a) Asahi: 97.800 oz

b) Brinks 864.689 oz

c) Manfra 288.867 oz

AMOUNT OF GOLD STANDING FOR NOVEMBER:

THE FRONT MONTH OF NOV STANDS AT 841 CONTRACTS FOR A GAIN OF 379 CONTRACTS.

WE HAD 175 CONTRACTS SERVED ON MONDAY. SO WE GAINED A HUGE SIZED 554 CONTRACTS FOR 55400 OZ OF GOLD (1.723 TONNES).

DECEMBER AGAIN LOST A MUCH SMALLER THAN EXPECTED CONTRACTS TOTALLING 62,401 TO 91,638 CONTRACTS . DECEMBER IS THE NEW FRONT MONTH AND WE ARE GOING TO HAVE A MEGA MEGA DILLY MONTH STANDING FOR DELIVERY FOR GOLD!! WE HAVE 2 MORE READING DAYS BEFORE FIRST DAY NOTICE: WEDNESDAY AND THEN FIRST DAY NOTICE FRIDAY NOV 28.

JANUARY GAINED 403 CONTRACTS UP TO 2161

We had 823 contracts filed for today representing 82,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 823 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 714 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2025. contract month, we take the total number of notices filed so far for the month (11,915 oz ) to which we add the difference between the open interest for the front month of NOV ( 841 CONTRACTS) minus the number of notices served upon today (823 x 100 oz per contract) equals 1,193,400 OZ OR 37.119 Tonnes of gold to which we add our first issuance of exchange for risk for 1.3996 tonnes//new standing advances to 38.5180 tonnes.

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (11,916x 100 oz +we add the difference for front month of NOV (841 OI} minus the number of notices served upon today (823)x 100 oz) which equals 1,193,400OZ OR 37.119 TONNES to which we add our 1.3996 tonnes of exchange for risk//new total of gold standing in November is 38.5186 tonnes

TOTAL COMEX GOLD STANDING FOR NOV..: 38.5186 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL NON ACTIVE ACTIVE DELIVERY MONTH OF NOVEMBER

volume MONDAY confirmed 348,958 contracts EXCELLENT

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,957,622.110 oz 60.89 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,571,142.558 oz

TOTAL REGISTERED GOLD 19,274,299.950 or 598.50 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,296,842.608 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,316,677 oz ((REG GOLD- PLEDGED GOLD)=

538.62 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

THE NOV. 2025 SILVER CONTRACTS

NOV 25 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of ASAHI 593.289.900 OZ ii) Out of Delaware 20,243.969 oz iii) Out of Brinks 597,914.440 oz iv) Out of JPMorgan: 593,903.00000 oz ??? total withdrawal 1,805,350.909 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | one entry i) Into HSBC: 604,099.630 oz total deposit 604,099.630 oz |

| No of oz served today (contracts) | 31 CONTRACT(S) ( 155,000 OZ 0.070 MILLION OZ |

| No of oz to be served (notices) | 0 contracts (0.0MILLION oz) |

| Total monthly oz silver served (contracts) | 3897 Contracts (19.485 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1entries

one entry

i) Into HSBC: 604,099.630 oz

total deposit 604,099.630 oz

withdrawals: customer side/eligible

4 entries

i) Out of ASAHI 593.289.900 OZ

ii) Out of Delaware 20,243.969 oz

iii) Out of Brinks 597,914.440 oz

iv) Out of JPMorgan: 593,903.00000 oz ???

total withdrawal 1,805,350.909 oz

adjustments: 2 dealer to customer

a) Asahi: 491,081.01

Delaware 1,017,135.07 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 150.238 MILLION OZ//.TOTAL REG + ELIGIBLE. 459.237 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF NOVEMBER /2025 OI: 31 OPEN INTEREST CONTRACTS FOR A LOSS OF 16 CONTRACTS. WE HAD 14 NOTICES SERVED ON MONDAY SO WE LOST 2 CONTRACTS OR 10,000 OZ AS THEY EXERCISED AN EXP CONTRACT AND TOO DELIVERY OVER IN LONDON

DECEMBER LOST 14,101 CONTRACTS DOWN TO 28,643. THIS IS THE FRONT MONTH FOR SILVER DELIVERIES AND WE WILL HAVE A STRONG STANDING FOR OUR SILVER METAL PROBABLY CLOSE TO 60 MILLION OZ!!

JANUARY GAINED 457 CONTRACTS UP TO 3152 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 31 or 0.155 MILLION oz

CONFIRMED volume; ON MONDAY 95,293 huge//

AND NOW NOVEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in NOV. we take the total number of notices filed for the month so far at 3893 X5,000 oz = 19.485MILLION oz

to which we add the difference between the open interest for the front month of NOV (31) AND the number of notices served upon today (31 )x (5000 oz)

Thus the standings for silver for the NOVEMBER 2025 contract month: (3897) Notices served so far) x 5000 oz + OI for the front month of NOV(31) minus number of notices served upon today (31)x 5000 oz equals silver standing for the NOV.contract month equating to 19.485 MILLION OZ

New total standing: 19.485million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 151.627 million oz of registered silver

JPMorgan as a percentage of total silver: 199.031/459.031million. 43.35%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

NOV 25/WITH GOLD UP $46.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 24/WITH GOLD UP $16.95 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.86 TONNES

NOV 21/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.00 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1039.43 TONNES

NOV 20/WITH GOLD DOWN $20.45 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 19/WITH GOLD UP $14.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 18/WITH GOLD DOWN $6.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 17/WITH GOLD DOWN $20.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.93 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1044.000 TONNES

NOV 14/WITH GOLD DOWN $97.55TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1048.93 TONNES

NOV 13/WITH GOLD DOWN $17.80.TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1064.64 TONNES

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT XXX TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

NOV 3 WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 1.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1039,20 TONNES

OCT 31 WITH GOLD DOWN $17.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1040.35 TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

OCT 23 WITH GOLD UP $78.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37 TONNES

OCT 22 WITH GOLD DOWN $78.95 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

GLD INVENTORY: 1040.86 TONNES, TONIGHTS TOTAL

SILVER

NOV25/WITH SILVER UP $0.69 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 8.163 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 498.716 MILLION OZ //THIS IS A FRAUDULENT TRANSACTION

NOV24/WITH SILVER UP $0.43 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 277,000, OZ OUT OF THE SLV/ :INVENTORY RESTS AT 490.553 MILLION OZ MILLION OZ

NOV21/WITH SILVER DOWN $0.53 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 635,000 OZ INTO THE SLV/ :INVENTORY RESTS AT 490.190 MILLION OZ MILLION OZ

NOV20/WITH SILVER DOWN $0.53 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.555 MILLION OZ MILLION OZ

NOV 19/WITH SILVER UP $0.36 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 18/WITH SILVER DOWN $0.13 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489..283 MILLION OZ MILLION OZ

NOV 17/WITH SILVER DOWN $0.07 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.451 MILLION OZ INTO THE SLV:INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 14/WITH SILVER DOWN $2.08 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.722 MILLION OZ INTO THE SLV:

INVENTORY RESTS AT 487.832 MILLION OZ MILLION OZ

NOV 13/WITH SILVER DOWN $0.58 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 4 WITH SILVER DOWN $0.82 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

NOV 3 WITH SILVER $0.12 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 31 WITH SILVER DOWN $0.35 TODAY/SMALL CHANGES IN SILVER AT THE SLV: ///A WITHDRAWAL OF 636,000 OZ FROM THE SLV// ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

OCT 23 WITH SILVER UP $0.87 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 501.474 MILLION OZ

OCT 22 WITH SILVER DOWN $0.33 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.995 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 504.015 MILLION OZ

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43//HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

CLOSING INVENTORY 498.716 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

Peter Schiff: Bubbles Pop Everywhere

Tuesday, Nov 25, 2025 – 02:45 PM

On Wednesday’s episode of the Peter Schiff Show, Peter returns to his show to walk listeners through what he sees as multiple asset bubbles and why those bubbles matter beyond headline market moves. He calls out the AI stock mania, a fragile housing market propped up by policy, and the crypto circus — all potential bubbles inflated by easy money.

He opens by framing the broader problem: we don’t just have one overheating market, we have many, and policy choices make their unwinding more dangerous:

The bigger question is not just whether or not this is a precursor for other bubbles to pop because there are a lot of bubbles. We have a bubble in AI stocks and I’ll talk about that too. On this podcast, we got Nvidia earnings out after the close today, but we have the AI bubble. There’s a bubble in housing, which, you know, the government is really trying to prevent from deflating, which of course they need to allow it to deflate, but they’re afraid of what might happen.

Peter is careful to separate hype from technological promise — he believes AI could genuinely reshape productivity and living standards — but warns that enthusiasm is fueling speculative excess rather than sober investment:

When I talk about an AI bubble, I am not saying that there isn’t potential in artificial intelligence. In fact, I think there’s tremendous potential. I think there’s probably more potential there than in anything I’ve seen, which would include the internet, which had a lot of potential. I think that AI could be the most transformative invention as far as lifting the standard of living of all of humanity.

Shifting from tech to crypto, Peter points to recent price action as evidence that much of the Bitcoin story is built on air — a sharp drawdown is “a pretty big bear market in nothing,” and he prefers measuring crypto’s value relative to gold rather than dollars:

Earlier this afternoon, Bitcoin traded below 88,500. Now, of course, that’s still a ridiculously high price to pay for nothing, but it’s about 30% below what you had to pay for nothing a couple of months ago. All right. So that is a pretty big bear market in nothing; Bitcoin down 30%. In terms of gold, which again is a better way to measure the price of Bitcoin, because after all Bitcoin is marketed as being digital gold, as being an alternative to gold that is going to replace gold because it’s better than gold.

Ironically, Peter says, the one real constructive outcome from the crypto craze could be greater utility for actual money: tokenized gold. If blockchain tech makes gold more liquid and transferable, that can strengthen gold’s role rather than replace it — because tokens are only as meaningful as the asset backing them:

Ironically, the one thing that might come out of the whole crypto bubble is tokenized gold. Gold may be the only real winner. Rather than killing gold, blockchain may have just given it a new lease on life by making gold even more efficient than it’s ever been as a means of exchange, making it more liquid, making it more divisible, making it more portable. All the characteristics that people think Bitcoin has that are better than gold are worthless without the underlying value of gold.

Finally, Peter reads the Fed’s recent comments as dangerously complacent. He notes that members of the FOMC (Federal Open Market Committee) appeared to downplay inflation risks tied to tariffs, suggesting any price increases from trade barriers may be temporary — even as tariff policy changes are being used politically to try to cool prices:

I thought what was significant, and it should have produced a bigger reaction, but it did not, was that the FOMC members seem to believe that the inflation threat that they thought may have come from tariffs isn’t there. And to the extent that prices are higher, that it’s not, you know, a permanent thing, that it’s like a one and done situation. And of course, Trump has been rolling back more tariffs recently, a lot of items.

END

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

Ignored Red Repo Signals = More Obvious Golden Tailwinds

Monday, Nov 24, 2025 – 03:45 PM

Authored by Matthew Piepenburg via VonGreyerz.gold,

Markets are many things, but in simplest terms, they are a paradox.

From the Complex…

By this, I mean they are incredibly and intentionally complex, which makes them a kind of exclusive environment managed, allegedly at least, by cadres of well-versed experts (?) trained in, and comfortable with, complexity.

The extraordinarily complex mechanics, for example, of layered derivative trades or currency and rate swaps, the hedging of futures contracts on the New York COMEX or the maze-like liquidity and collateral movements in repo and reverse repo facilities are indeed settings of just mind-numbing complexity.

…To the Simple

But herein lies the paradox, for despite such deliberate and gated complexity, these markets—from the most basic ETF purchase to the most confusing asset-backed securities—operate upon one extraordinarily simple force, namely: Liquidity.

Or stated even more simply, everything hinges upon one question: Is there enough cash to keep these systems afloat?

And even if you have never had the time to study every market correction from the first Persian trading huts or Roman currency collapses to the great crashes of 18th-century France, 19th-century America or even the more recent ghosts of 2008, the key takeaway is equally simple: Every market crisis is at heart a liquidity crisis.

In short: Liquidity matters.

Engines Need Oil, Markets Need Cash

Liquidity—or cash flows—are like the oil levels in a basic engine, and anyone who has ever owned or driven a car knows it’s never a good thing when the dashboard signals a glowing, red low-oil warning.

Unless more oil is added soon, the warning phase progresses quickly to a stalled car phase.

What many investors may not realize is that these otherwise immortal risk asset markets are riddled with “low-oil warnings” which few are discussing, but which gold is recognizing.

Warning Lights in the Repo Market: Boring but Important

Take the current “Standard Repo Facility”—a topic so boring and complex that it’s easy to both ignore and misunderstand.

In simplest terms, the repo market is where big banks (“primary dealers”) go to get overnight loans (i.e., “liquidity”) from each other to keep their bank engines humming along.

It is here where they execute what are called “repurchase agreements”—i.e. where Party A asks for cash from Party B by offering Party B overnight collateral in the form of “safe” USTs.

The next day, Party A pays back the loan and buys back its collateral at a slightly higher price/rate than the Fed Funds Rate set by the FED (the FFR), otherwise known as the “repo rate.”

Such repo transactions keep the wheels of banking, money market yields and even hedge fund leverage tools comfortably “greased” and chugging along smoothly so long as the FFR and repo rates are aligned, affordable and hence: “Liquid.”

But when the repo rates begin to climb noticeably above the allegedly calming Fed Funds Rate, this is a dashboard warning that trust among the counterparties’ collateral is falling and that future liquidity is stalling.

Or, and stated more simply: Rising repo rates signal tightening liquidity, which for bankers is like the appearance of a rising shark fin for a weekend ocean swimmer.

Nervous “Experts” …

Recently, a bunch of market “swimmers” (i.e. primary dealers and their representatives) met at the home of the New York Fed in a very nervous mood and behind closed doors.

Why?

Because they are seeing shark fins circling and low-oil signals flashing from their dashboards.

The repo rates are decoupling from (rising above) the FFR, which means the cost of borrowing between insiders is getting painful.

This also means liquidity is drying and the engine of US and global markets (as literally everything and every asset is impacted by expensive liquidity) is slowly beginning to smoke, rattle and choke.

If repo rates go from rising to dangerously spiking, as they did in September of 2019, the engine stalls altogether, and the repair bill (i.e., Fed-injected liquidity) becomes extraordinary.

Prepare the Firehose

In other words, this means rapidly expanding liquidity measures from the Fed’s “emergency funding” source (aka: “reverse repo facility”), which is nothing more than QE (money printing) by another false title.

What’s equally creepy, and equally off the radar of most investors and coopted financial media sources, is that even before these nervous bankers met in New York, the Fed had already injected $125B of short-term funding operations to keep these repo rates “controlled,” but with little success.

Why?

Because after 3 years of Powell desperately trying to reduce the Fed’s embarrassingly fat balance sheet via QT while its commercial banking nieces and nephews on Wall Street were simultaneously reducing their own balance sheets to meet regulatory measures, liquidity was already quietly drying up even before the engine warning lights finally went red in the repo market.

The Past is Prologue

So, what does this mean going forward for markets in general or gold in particular?

By now, it should be no surprise to any that the Fed, which is a private bank owned by other commercial banks as part of a legalized cabal that is little more than a dishonest, unelected and insider trade, will do “whatever it takes” to keep themselves alive and “liquid.”

This means the Fed will inevitably, and once again, face an inflection point in which more bazooka/firehose money will flow into this “system.”

In short, “liquidity,” ultimately created from thin air, will save a now entrenched and parasitic system at the expense of the inherent purchasing power of the USD in general and the paper wealth of its citizens in particular, in this hidden backdrop of serfs and lords otherwise masquerading as free market capitalism.

The Future is Simple

As for gold, it may not be as human as our central bankers and primary dealers, but it is a heck of a lot more honest.

Its price moves today (which are increasingly less inhibited by the tapped-out COMEX and LBMA banks who lack the free-float to legally price fix precious metals) are telling us what our leadership and banks cannot, namely: Paper money is being debased at alarming levels to keep liquidity flowing into a debt-draped and broken system.

Throughout history, gold has always been nature’s honest monetary reaction to fiat currencies’ “human, all too human” debasement sins.

The market knows that more QE and QE-like liquidity is coming, which means a USD, which has already lost more than 99% of its purchasing power when measured against gold, will continue to lose its “punch” in the same way a glass of wine loses its flavor when buckets of added water dilute its vintage.

Gold, whose bull market is just beginning in such a backdrop, will continue its secular and historical rise, because fiat currencies will continue their secular, political, human and oh-so historically familiar fall.

In short, and despite pages, centuries and layers of complexity, the case for gold is ultimately as simple as that.

END

ALASDAIR MCLEOD

The bitcoin crisis

Bitcoin’s problems could be just starting. Having rapidly fallen 30% from its highs, leveraged bulls could become forced sellers, with wider implications for markets and gold.

| Alasdair MacleodNov 25∙Paid |

Introduction

The concept behind bitcoin was that its quantity would become progressively harder to mine as it approached its hard stop of 21,000,000. It was promoted as a future private sector money compared with the endless expansion of government currency. Valued in continually debasing government currency, bitcoin’s value would increase and increase.

It succeeded in alerting generally complacent investors to the issue of currency debasement. And here was a new technology which allowed individuals to hedge against it. It seemed to hold greater promise than gold, which already had significant aboveground stocks and was frankly old hat not going anywhere at the time and whose supply would always expand. Surely, the argument went that a new technocratic solution could do better.

Enthusiasts promoted the idea that as a world currency you could compare bitcoin with the global fiat money supply. It offered the prospects of soaring towards infinity — and from time to time it appeared to be on its way. But in the last month the dream has become severely tested, with its dollar value crashing up to 30%.

But as the chart above shows, in real terms as opposed to arithmetic it appears to have lost momentum in successive bullish phases and appears likely to be heading for further declines, potentially testing a six-year uptrend currently below $50,000. Given that there are significant leveraged positions in bitcoin, a decline to this level could be swift as some major holders are foreclosed on by their lenders.

Chief among these is Michael Saylor’s Strategy Inc. (MSTR), whose further buying into the bitcoin crash was to no effect. According to Coinbase, MSTR appears to have now stopped buying, suggesting that it has run out of firepower.

Furthermore, MSTR is likely to be removed from major benchmarks leading to automated selling by tracker funds. Coinbase estimates that this could lead to further automated sales of $2.8bn when Morgan Stanley Capital International (a major compiler of international indices) issues its ruling on 15 January, and a further $8.8bn if other index compilers follow suit.

As a leveraged play on bitcoin MSTR’s shares have already declined by 70% from their peak. The question arises as to whether the market disruption faced by MSTR and similar leveraged vehicles can be contained without undermining bitcoin itself. It seems highly unlikely.

Currently, bitcoin is capitalised at about $1.5 trillion, and its destabilisation is bound to have an impact elsewhere. In recent years it has correlated neatly with NASDAQ, as the chart below indicates — until now:

The point behind this correlation is that holders of bitcoin are technology investors generally. And if bitcoin collapses as speculative leverage is unwound, then tech stocks will be undermined as well.

Could this be chaos theory’s butterfly in the jungle whose flapping wings become magnified by a domino effect into a financial hurricane on Wall Street? We know that there’s a massive financial credit bubble waiting to implode and that momentum stocks such as the Magnificent 7 are vulnerable.

What’s particularly striking is that bitcoin’s negative performance comes at a time when previously unfashionable gold is now outperforming bitcoin. To put it in perspective, global portfolio exposure to gold is estimated by the World Gold Council at only $500 billion, one-third of bitcoin’s capitalisation. Bitcoin’s collapse will undoubtedly leave investors without the protection from debasing fiat currencies that they originally sought.

As stackers in gold might muse, it’s an ill wind that brings benefits. Bulls of bitcoin hiding from currency debasement will have lost it and can only turn to tried and tested protection, which is gold.

3.CHRIS POWELL, Secretary/Treasurer//GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS /249 AND TODAY;S 250

DAVE KRANZLER

ASIA RESULTS; TUESDAY NOV 25

SHANGHAI CLOSED UP 33.04 POINTS OR 0.87%

//Hang Seng CLOSED UP 178.05 PTS OR 0.69%

// Nikkei CLOSED UP 33.04 PTS OR 0.07% //Australia’s all ordinaries CLOSED UP 0.27%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.0856/ OFFSHORE CLOSED UP AT 7.0846/ Oil UP TO 58.63 dollars per barrel for WTI and BRENT UP TO 63.10 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.0856 OFFSHORE YUAN TRADING UP TO 7.0846:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.0856

OFFSHORE YUAN: UP TO 7.0846

HANG SENG CLOSED UP 178.05 PTS OR 0.69%

2. Nikkei closed HOLIDAY

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 99.98 – EURO RISES TO 1.1577 UP 17 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.806 // UP 2 FULL BASIS PTS//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.27…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.335 UP 2 FULL BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN/JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP this morning

3h European bond buying continues to push yields LOWERER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6882/ Italian 10 Yr bond yield DOWN to 3.440 SPAIN 10 YR BOND YIELD DOWN TO 3.194

3i Greek 10 year bond yield DOWN TO 3.3188

3j Gold at $4133.00 Silver at: 51.18 1 am est) SILVER NEXT RESISTANCE LEVEL AT $54.00//AFTER 50.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 33/100 roubles/dollar; ROUBLE AT 78.76

3m oil (WTI) into the 58 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.27 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.806% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.360 UP 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8090 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9347 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.026 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.674 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.485 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.44 DOWN 0 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.520 DOWN 3 PTS

30 YR UK BOND YIELD: 5.334 DOWN 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.1743 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.749 DOWN 3 BASIS PTS.

a New York OPENING REPORT

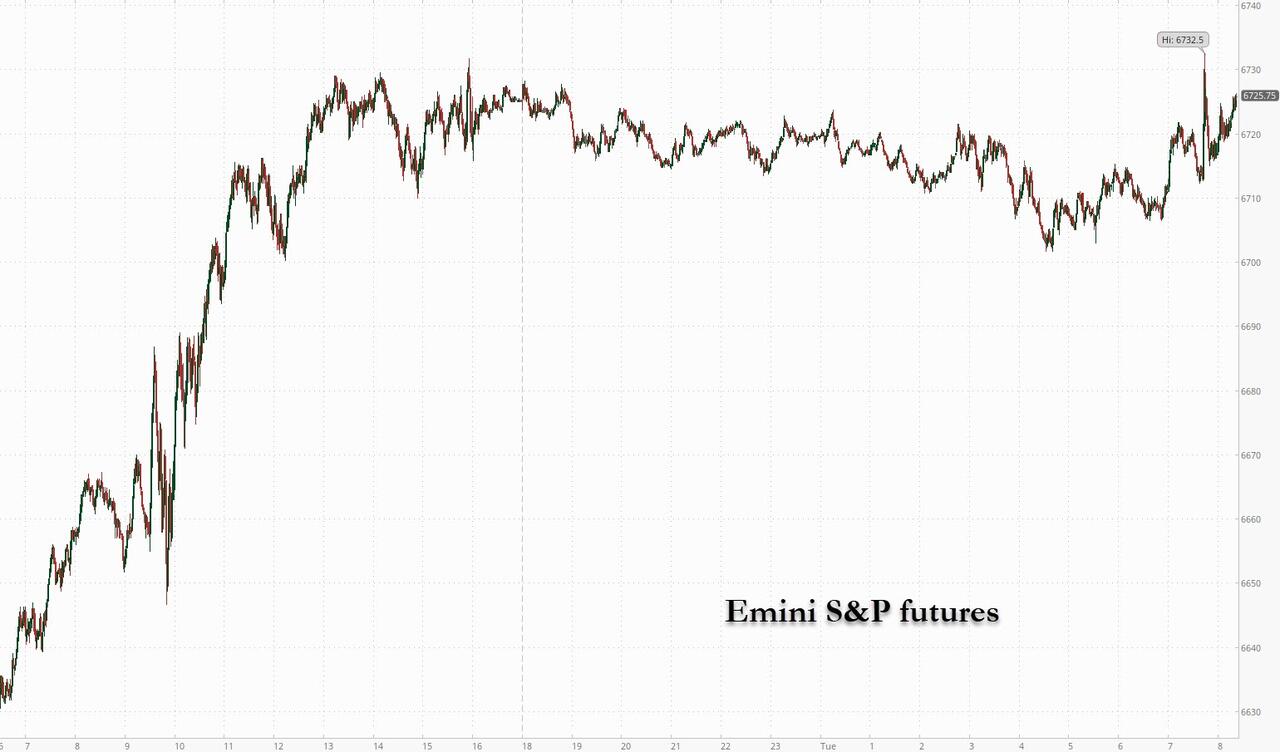

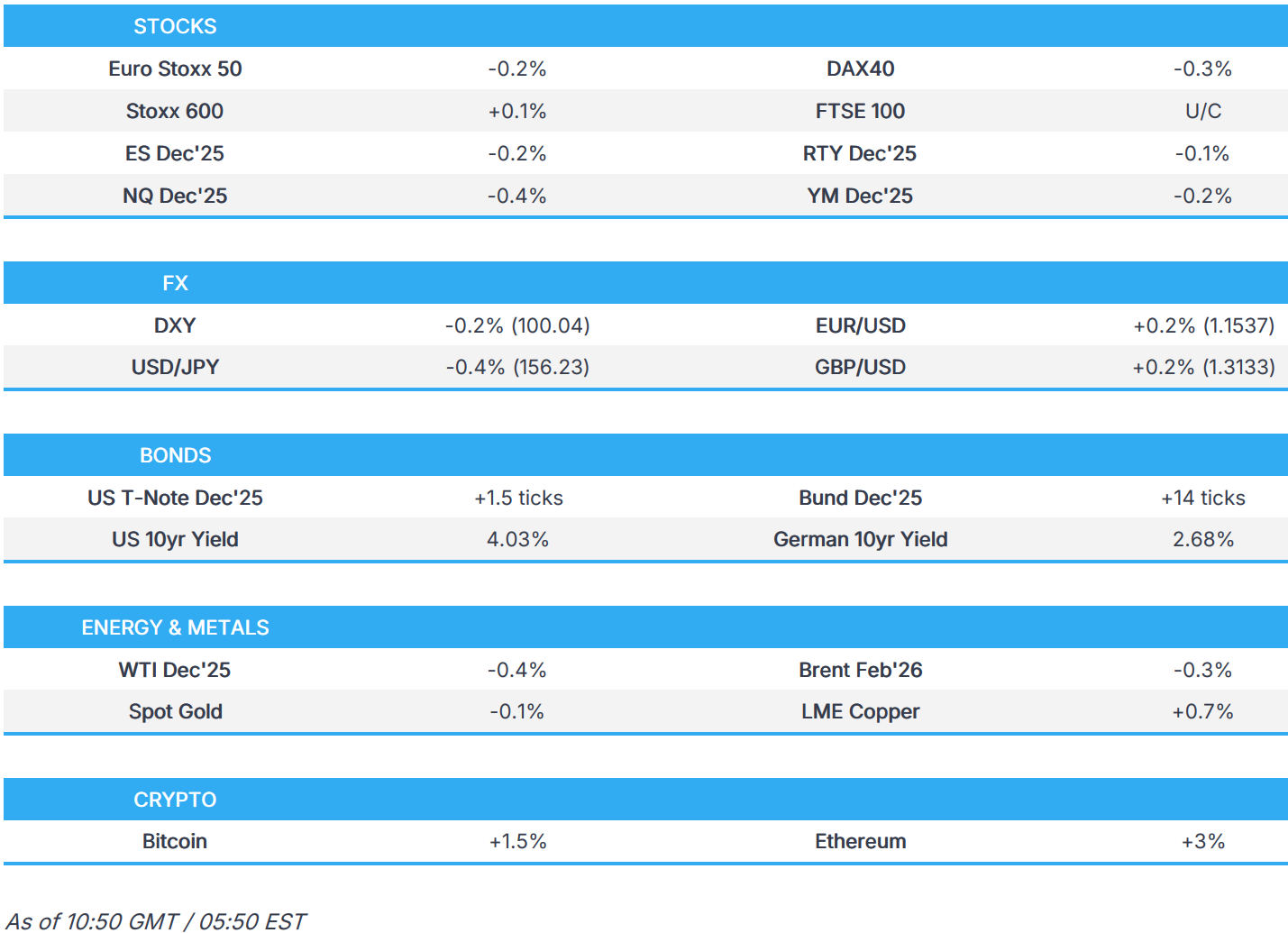

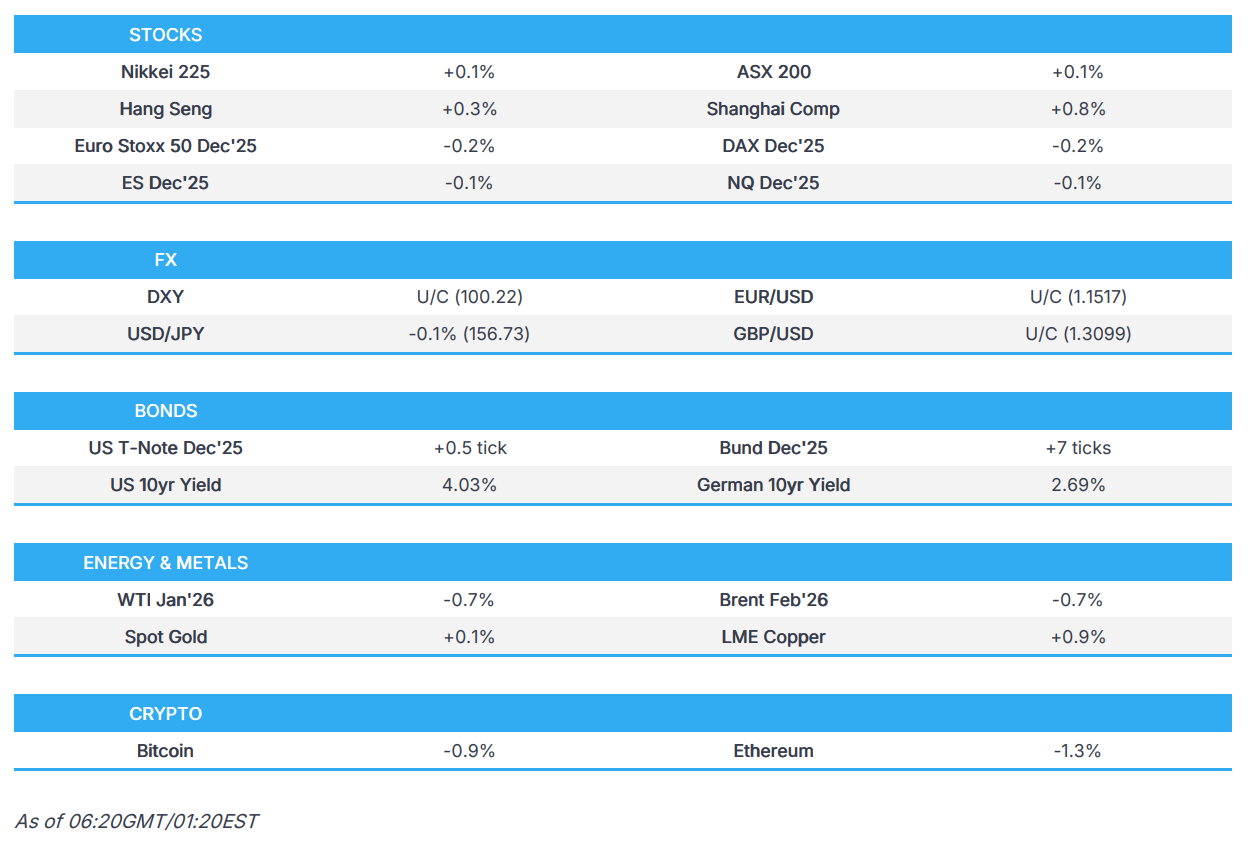

Stock Rally Falters As Nvidia-Google AI Rivalry Intensifies

Tuesday, Nov 25, 2025 – 08:55 AM