access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XGE: COMEX

072 C GOLDMAN 6

092 C DEUTSCHE BANK 185

099 H DEUTSCHE BANK AG 74

104 C MIZUHO SECURITIES US 3

118 C MACQUARIE FUTURES US 20

118 H MACQUARIE FUTURES US 14

132 C SG AMERICAS 7

167 C MAREX 9

190 H BMO CAPITAL MARKETS 38

332 H STANDARD CHARTERED B 640

363 C WELLS FARGO SECURITI 3

363 H WELLS FARGO SECURITI 39

435 H SCOTIA CAPITAL (USA) 207

624 H BOFA SECURITIES 1641

661 C JP MORGAN SECURITIES 11 428

686 C STONEX FINANCIAL INC 1 1

690 C ABN AMRO CLR USA LLC 10

709 C BARCLAYS 9

730 C PTG DIVISION OF SGAS 1

732 H RBC CAP MARKETS 14

880 H CITIGROUP 26

905 C ADM 15

JPMORGAN STOPPED: 428/1701

GOLD: NUMBER OF NOTICES FILED FOR DEC/2025: 1701 CONTRACTs NOTICES FOR 170,100 OZ or 5.2908 TONNES

total notices so far: 26,163 contracts for 2,616,300 OR 81.373 tonnes)

SILVER NOTICES: 565 NOTICE(S) FILED FOR 2.825 MILLION OZ/

total number of notices filed so far this month : 10,092 CONTRACTS (NOTICES) for 50.460 million oz

INITIAL STANDING FOR DEC: 49.33 MILLION OZ FOLLOWED BY TODAY’S STRONG 0.555 MILLION OZ QUEUE JUMP//STANDING ADVANCES TO 54.500 MILLION OZ//

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOV: 9.045 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER HUGE 0.555 MILLION OZ QUEUE JUMP // STANDING ADVANCES TO 54.500 MILLION OZ//

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S HUGE 3.256 TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 0.6524 TONNES//NEW STANDING ADVANCES TO 86.696 TONNES/

NEW STANDING FOR GOLD, DEC CONTRACT AT 86.696 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 27 TONNES//VERY SMALL THIS MONTH.

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 632 CONTRACTS OI TO 150,200 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 30 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 30 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 632 CONTRACTS AND ADD TO THE 30 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 602 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $0,23 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 5.395 MILLION PAPER OZ

OCCURRED DESPITE OUR GAIN IN PRICE.OF $0.23

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS THURSDAY MORNING:

ASIA RESULTS; THURSDAY DEC 4

HANGHAI CLOSED DOWN 2.21 POINTS OR 0.06%

//Hang Seng CLOSED UP 175.17 PTS OR 0.65%

// Nikkei CLOSED UP 1163.74 PTS OR 2.33% //Australia’s all ordinaries CLOSED UP 0.14%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.0717

/ OFFSHORE CLOSED DOWN AT 7.0666/ Oil UP TO 59.29 dollars per barrel for WTI and BRENT UP TO 62.85 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 7.0717 OFFSHORE YUAN TRADING DOWN TO 7.0666:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4905 CONTRACTS TO 423,395 OI WITH OUR GAIN IN PRICE OF $14.25 WITH RESPECT TO WEDNESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2310). WE HAD ZERO T.A.S. LIQUIDATION WEDNESDAY (WITH MONTH END SPREADER LIQUIDATIONS FINISHED ON NOV 30). .. IT SEEMS THAT THE SPECULATORS WENT STRONGLY TO THE LONG SIDE WITH OUR FRBNY PROVIDING THE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE . JUDGING BY THE MASSIVE NOTICES FOR DELIVERY FILED WEDNESDAY NIGHT AT 1701 NOTICES FOR 170,100 OZ (5.2908 TONNES), THE EASTERN CENTRAL BANKERS ARE STANDING FOR CONSIDERABLE AMOUNT OF GOLD FOR DECEMBER DELIVERIES. YOU WILL NOTICE THAT THE COMEX OI HAS STILL A VERY LOW AT 423,948 AND THESE GUYS ARE VERY STICKY AND A LITTLE HIGHER THAN TUESDAY SO THEY PROVIDE A LITTLE FODDER FOR OUR CROOKS TO RAID!!

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 7275 CONTRACTS (OR 22.62 TONNES). THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR 0 OZ OR NIL TONNES OF GOLD.

FIRST LETS DO A REVIEW OF EXCHANGE FOR RISK ISSUANCES THIS PAST YEAR

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD PRIOR MONTHS

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;TOTAL EXCHANGE FOR RISK LAST 6 MONTHS 70.097 TONNES. THE RECIPIENT OF THESE EXCHANGE FOR RISK IS THE BANK OF ENGLAND. THIS CENTRAL BANK LOANED OUT ITS GOLD AND WANTS IT BACK. THEIR TOTAL RESERVES PRIOR TO THE LOANS IS LISTED AT 310 TONNES.

LET US LOOK AT JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

NOW LET US LOOK AT THE MONTH OF AUGUST:

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

NOW LET US LOOK AT SEPT.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FOR 14.553 TONNES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

LET’S SUM UP EXCHANGE FOR RISK FOR THE LAST 11 MONTHS

HISTORY: LAST 11 MONTH’S EXCHANGE FOR RISK//TOTAL CONTRACT ISSUANCES //TONNES OF GOLD

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

NOVEMBER:

NOVEMBER: TWO ISSUANCES:

WHICH NOW BRINGS US TO NOVEMBER WHERE WE RECEIVED NOTICE OF OUR SECOND ISSUANCE OF 1016 CONTRACTS FOR 101,600 OZ OR 3.165 TONNES. WE MUST NOW ADD THIS TO OUR INITIAL ISSUANCE OF 450 NOTICES //45000 OZ OR 1.3996 TONNES. THUS THE NEW TOTAL EXCHANGE FOR RISK FOR NOVEMBER IS 1,466 NOTICES FOR 146,600 OZ OR 4.5598 TONNES OF GOLD.

AND NOW DECEMBER: SO FAR 0 NOTICES ISSUED:

DEC 0

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 10 MONTH TOTALS 134.8646 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES) NO WONDER THE BANK OF ENGLAND THROUGH THE E.E.A. CANNOT SIGN OFF ON THEIR AUDIT

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 54 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES IN AUGUST AND THEN ADDED 24 TONNES IN SEPT. AND THUS THEIR SHORTFALL TO THE BIS IS 54 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 12TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK THIS YEAR !!…..(DEC 24 THROUGH DEC 25//ONLY MISSING JUNE. TOTAL 12 MONTHS ISSUANCE 134.8646 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW DECEMBER COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 7275 CONTRACTS DESPITE OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 3.9% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER. GRASBERG WILL NOT BE READY TO RESUME NORMAL PRODUCTION UNTIL JULY 2026

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH DECEMBER/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A FAIR T.A.S ISSUANCE CONTRACTS AS THE 5 CONSECUTIVE MEGA HUGE ISSUANCES HAS ENDED. THE CME NOTIFIES US THAT THEY HAVE ISSUED 642 T.A.S CONTRACTS. THE 5 CONSECUTIVE MEGA HUGE T.A.S ISSUANCES IN NOVEMBER WERE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK FINISHING OFF WITH A MASSIVE HUGE RAID ON GOLD (AND SILVER) DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS ALWAYS ENDS IN FAILURE AS WE SAW GOLD//SILVER RISE HUGELY ON MONDAY.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S HUGE 3.256 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF .6524 TONNES//STANDING ADVANCES TO 86.696 TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 54+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 54 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 54 TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING. IT LOOKS LIKE THE FRBNY IS QUITE NERVOUS, MAYBE I AM WRONG. WE MUST WAIT TO SEE THE DATA FROM BIS SWAPS FROM ROBERT LAMBOURNE TO SEE IF THEY WILL BEGIN TO COVER!!

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING:

EXCHANGE FOR PHYSICAL ISSUANCE/DEC.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 2370 CONTRACTS.

THAT IS A FAIR SIZED 2370 EFP CONTRACT WAS ISSUED: : /DEC 2370 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2370 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 54 TONNES

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS EARLY IN COMEX SESSION + BUT DID HAVE CONSIDERABLE GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED

T.A.S.SPREADER ISSUANCE//DECEMBER

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT//THURSDAY MORNING WAS A FAIR SIZED 1067 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP WEDNESDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING STRONG GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE..ENOUGH FODDER FOR A RAID//

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 5 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S MASSIVE 3.256 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: .4524 TONNES//NEW STANDING ADVANCES TO 86.696 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

AN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING DECEMBER,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $14.25/ /)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION WEDNESDAY WITH THE PRICE GAIN// COMEX TRADING//.. BUT OUR SPECULATORS REMAIN STOIC//THEY REFUSED TO BE RINSED. OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL TUESDAY NIGHT WHICH EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR DECEMBER. THE COMEX IS ONE BIG MESS!! THIS WEEK,

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

A LITTLE REVIEW OF GOLD STANDING THESE PAST 3 MONTHS:

STANDING FOR GOLD OCT THROUGH TO DECEMBER:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A HUGE 1047 CONTRACT QUEUE JUMP WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: .6524 TONNES///STANDING ADVANCES TO 86.696 TONNES.

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $14.25

WE HAD A FAIR 553 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL. ALL TIME RECORD REMOVAL

INITIAL GOLD COMEX

DEC 4

DEC CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entries i) Out of Brinks 22,393.830oz 0.6984 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entries xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1701 notice(s) 170,100 OZ 5.2908 TONNES OF GOLD |

| No of oz to be served (notices) | 1710 contracts 171,000 OZ 5.368 TONNES |

| Total monthly oz gold served (contracts) so far this month | 26,163 notices 2,616,300 0z 81.378 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

1 entries

i) Out of Malca; 11,960.172 oz

0.3729 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1 all dealer to customer

a) Brinks 4540.545 oz

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF DECEMBER STANDS AT 3411 CONTRACTS FOR A GAIN OF 953 CONTRACTS. WE HAD 94 CONTRACTS FILED ON WEDNESDAY SO WE GAINED A WHOPPING 1047 CONTRACT QUEUE JUMP FOR 104700 OZ OR 3.256 TONNES TO WHICH WE ADD TO OUR PREVIOUS QUEUE JUMPS .THUS STANDING FOR GOLD IN DECEMBER INCREASES HUGELY TO 86.696 TONNES

JANUARY LOST 131 CONTRACTS DOWN TO 2636

FEB LOST 2871 CONTRACTS DOWN TO 319,552 CONTRACTS

We had 1701 contracts filed for today representing 170,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and11 notices issued from their client or customer account. The total of all issuance by all participants equate to 1701 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 482 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2025. contract month, we take the total number of notices filed so far for the month (26,163 ) to which we add the difference between the open interest for the front month of DEC ( 3411 CONTRACTS) minus the number of notices served upon today (1701 x 100 oz per contract) equals 2,787,300 OZ OR 86.696 Tonnes of gold

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (26,163 x 100 oz +we add the difference for front month of DEC (3411 OI} minus the number of notices served upon today (94)x 100 oz) which equals 2,787,300 OR 86.696 TONNES

new total of gold standing in DECEMBER is 86.696 tonnes

TOTAL COMEX GOLD STANDING FOR DEC ..: 86.696 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF DECEMBER

volume WEDNESDAY confirmed 193,893 contracts fair

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,935,391.434 oz 60.19 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,247,560.642 oz

TOTAL REGISTERED GOLD 17,861,818.060or 555.57 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,385,942.602OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 15,926,427oz ((REG GOLD- PLEDGED GOLD)=

495.370 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

DEC 4 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) out of Brinks 600,200.130 ii) Out of Delaware 1964.800 oz iii) Out of JPMorgan 602,120,130 oz iv) //Out of Manfra 88,071,866 oz titak withdrawal 1,292,287.180 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 2 entries i) Into CNT 599,136.731 oz ii) Into HSBC 1,192,309.100 total deposit 1,791,438.820 oz |

| No of oz served today (contracts) | 565 CONTRACT(S) ( 2.825 million OZ |

| No of oz to be served (notices) | 1841 contracts (9.205 MILLION oz) |

| Total monthly oz silver served (contracts) | 10,092 Contracts (50.460 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

please note: lack of any silver coming in or leaving the comex

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

withdrawals: customer side/eligible

4 entries

i) out of Brinks 600,200.130

ii) Out of Delaware 1964.800 oz

iii) Out of JPMorgan 602,120,130 oz

iv) //Out of Manfra 88,071,866

oz

titak withdrawal 1,292,287.180 oz

adjustments: 3//dealer to customer

a) HSBC 251,999.000

b) CNT 538,356.510 oz

c) Loomis: 353,152.500 oz

TOTAL REGISTERED SILVER: 138.328MILLION OZ//.TOTAL REG + ELIGIBLE. 457.220Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC.

silver open interest data:

FRONT MONTH OF DECEMBER /2025 OI: 1373 OPEN INTEREST CONTRACTS FOR A LOSS OF 561 CONTRACTS. WE HAD 672 CONTRACTS FILED ON WEDNESDAY SO WE ACTUALLY HAD ANOTHER HUGE QUEUE JUMP ON DAY 4 OF 111 CONTRACTS OR 0.555 MILLION OZ

JANUARY LOST 22 CONTRACTS DOWN TO 4001 CONTRACTS

FEB GAINED 130 CONTRACTS UP TO 1088 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 565 or 2.825 MILLION oz

CONFIRMED volume; ON TUESDAY 138,328 huge//

AND NOW DECEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 10,092 X5,000 oz = 50,460 MILLION oz

to which we add the difference between the open interest for the front month of DEC (1373) AND the number of notices served upon today (565 )x (5000 oz)

Thus the standings for silver for the DECEMBER 2025 contract month: (10,092) Notices served so far) x 5000 oz + OI for the front month of DEC(1373) minus number of notices served upon today (565)x 5000 oz equals silver standing for the DEC.contract month equating to 54.500 MILLION OZ

New total standing: 54.500million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 138.328. million oz of registered silver

JPMorgan as a percentage of total silver: 197.397/457.220million. 43.10%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

DEC 3/WITH GOLD UP $14.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1048.30 TONNES

DEC 2/WITH GOLD DOWN $53.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.58 TONNES OF GOLD VAPOUR INTO THE GLD// /// ///INVENTORY RESTS AT 1050.01TONNES

DEC 1/WITH GOLD UP $22.75 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43TONNES

NOV 28/WITH GOLD UP $51.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43 TONNES

NOV 26/WITH GOLD UP $25.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT PAPER DEPOSIT OF 4.57 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 25/WITH GOLD UP $46.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 24/WITH GOLD UP $16.95 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.86 TONNES

NOV 21/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.00 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1039.43 TONNES

NOV 20/WITH GOLD DOWN $20.45 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 19/WITH GOLD UP $14.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 18/WITH GOLD DOWN $6.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 17/WITH GOLD DOWN $20.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.93 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1044.000 TONNES

NOV 14/WITH GOLD DOWN $97.55TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1048.93 TONNES

NOV 13/WITH GOLD DOWN $17.80.TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1064.64 TONNES

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT XXX TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

NOV 3 WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 1.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1039,20 TONNES

OCT 31 WITH GOLD DOWN $17.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1040.35 TONNES

OCT 30 WITH GOLD UP $15.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD . /// ///INVENTORY RESTS AT 1036.05 TONNES

OCT 29 WITH GOLD UP $18.60 TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 28 WITH GOLD DOWN $38.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 8.01 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1038.92 TONNES

OCT 27 WITH GOLD DOWN $115.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 5.44 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1046.93 TONNES

OCT 24 WITH GOLD DOWN $7.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A HUGE WITHDRAWAL OF 6.29 TONNES OF GOLD FROM THE GLD./// . /// ///INVENTORY RESTS AT 1052.37TONNES

GLD INVENTORY: 1046.58 TONNES, TONIGHTS TOTAL

SILVER

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

DEC 3/WITH SILVER UP $0.23/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 1.956 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 510.012 MILLION OZ //

DEC 2/WITH SILVER DOWN $0.65 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND FRAUDLUENT PAPER DEPOSIT OF 6.167 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 508.057 MILLION OZ //

DEC 1/WITH SILVER UP $2.21 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 907,000 OZ INTO THE SLV./ :INVENTORY RESTS AT 501.890 MILLION OZ //

NOV28/WITH SILVER UP $3.28 TODAY/NO CHANGES IN SILVER AT THE SLV:/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV26/WITH SILVER UP $1.86 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 2.267 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV25/WITH SILVER UP $0.69 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 8.163 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 498.716 MILLION OZ //THIS IS A FRAUDULENT TRANSACTION

NOV24/WITH SILVER UP $0.43 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 277,000, OZ OUT OF THE SLV/ :INVENTORY RESTS AT 490.553 MILLION OZ MILLION OZ

NOV21/WITH SILVER DOWN $0.53 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 635,000 OZ INTO THE SLV/ :INVENTORY RESTS AT 490.190 MILLION OZ MILLION OZ

NOV20/WITH SILVER DOWN $0.53 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.555 MILLION OZ MILLION OZ

NOV 19/WITH SILVER UP $0.36 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 18/WITH SILVER DOWN $0.13 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489..283 MILLION OZ MILLION OZ

NOV 17/WITH SILVER DOWN $0.07 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.451 MILLION OZ INTO THE SLV:INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 14/WITH SILVER DOWN $2.08 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.722 MILLION OZ INTO THE SLV:

INVENTORY RESTS AT 487.832 MILLION OZ MILLION OZ

NOV 13/WITH SILVER DOWN $0.58 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 4 WITH SILVER DOWN $0.82 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

NOV 3 WITH SILVER $0.12 TODAY/NO CHANGES IN SILVER AT THE SLV: / ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 31 WITH SILVER DOWN $0.35 TODAY/SMALL CHANGES IN SILVER AT THE SLV: ///A WITHDRAWAL OF 636,000 OZ FROM THE SLV// ///INVENTORY RESTS AT 488.363 MILLION OZ

OCT 30 WITH SILVER UP $0.95 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 29 WITH SILVER UP $0.68 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 4.218 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 488.999 MILLION OZ

OCT 28 WITH SILVER UP $0.36 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 493.217 MILLION OZ

OCT 27 WITH SILVER DOWN $1.84 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.588 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 495.758 MILLION OZ

OCT 24 WITH SILVER DOWN $0.25 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.541 MILLION OZ OUT OF THE SLV /// ///INVENTORY RESTS AT 497.346 MILLION OZ

CLOSING INVENTORY 514.365 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

TETHER/GOLD

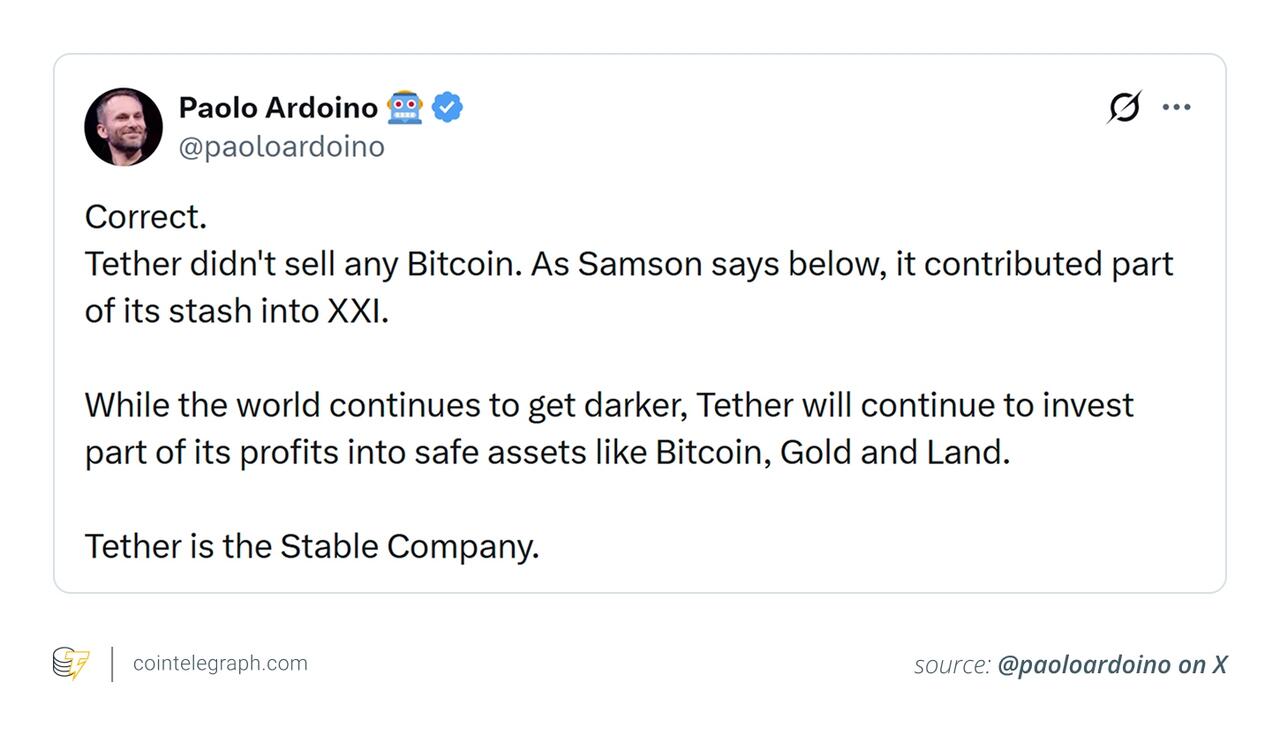

Why Tether Is Buying More Gold Than Many Central Banks, And What It Signals

Thursday, Dec 04, 2025 – 10:30 AM

Authored by Dilip Kumar Patairya via CoinTelegraph.com,

- Tether purchased 26 tons of gold in Q3 2025, a larger quarterly acquisition than any reporting central bank. Its total holdings reached 116 tons, placing it among the world’s top 30 gold holders.

- Stablecoin issuers, sovereign wealth funds, corporations and tech firms are increasingly active in gold markets. This trend marks a structural shift in global demand once dominated by central banks.

- Central banks added 220 tons of gold in Q3 2025, up 28% from Q2. Countries such as Kazakhstan, Brazil, Turkey and Guatemala made notable additions despite record prices.

- While central banks buy gold for national monetary policy, Tether’s purchases come from profits and support diversification, resilience and collateralization for USDT.

The global financial system is witnessing a period when non-state entities are competing with central banks to build gold reserves. Tether, the issuer of Tether USDt – the largest stablecoin in the world – is now one of the largest buyers of gold. In a single quarter, the company purchased more gold than most central banks did in the same period.

This article explores how an enterprise moved ahead of central banks in purchasing gold for its reserves and discusses independent attestations of the purchase. It also examines the rise of non-state gold buyers and what Tether’s gold buying does not indicate.

A private company outpacing central banks in buying gold

During the third quarter of 2025, Tether added 26 metric tons of gold to its holdings. According to analysts at Jefferies, this made Tether the single-largest gold buyer in that quarter, larger than the combined purchases of all reporting central banks.

By the end of September 2025, Tether’s total reported gold holdings stood at about 116 tons. If ranked alongside countries on the International Monetary Fund (IMF) official gold reserves list, this would place Tether among the top 30 holders worldwide, ahead of nations such as Greece, Qatar and Australia.

Per analysis from the investment bank Jefferies, Tether’s 26-ton purchase in Q3 2025 exceeded the official gold purchases of many mid-sized central banks during the same period. This reflects a wider trend.

Large private players, including stablecoin issuers, sovereign wealth funds and multinational corporations, are becoming significant participants in markets once dominated by governments. Research from the World Gold Council has also pointed to rising non-sovereign demand for gold.

Tether CEO Paolo Ardoino said on X, “While the world continues to get darker, Tether will continue to invest part of its profits into safe assets like Bitcoin, Gold and Land.” The company has emphasized that these gold purchases are made from profits, not from customer reserves that back USDT. It holds that diversification into real assets strengthens long-term resilience.

Independent attestations: The verified gold breakdowns

Tether publishes quarterly independent attestations prepared by major accounting firms. These reports provide insight into the company’s reserves:

- As of Sept. 30, 2025, gold and precious metals represent about 7% of Tether’s total consolidated reserves.

- This figure includes both gold-backed USDT and gold allocated to Tether Gold, Tether’s tokenized gold product.

- XAUT has a market value of roughly $1.6 billion, which corresponds to less than 12 tons of gold.

- More than 100 tons of the reported gold is not tied to XAUT and forms part of Tether’s broader corporate reserves and investments.

How Tether compares with central banks

The WGC “Gold Demand Trends – Q3 2025” report shows that central banks globally added a net 220 tons of gold in Q3 2025. For context, this was 28% higher than the Q2 figure and 6% more than the five-year quarterly average.

In 2025, the price of gold rose about 50% year-to-date. Record-high prices likely constrained the scale of initial purchases. However, the renewed increase in central bank demand during the latest quarter indicates that these institutions are continuing to add gold strategically. They are doing so even in the face of significantly higher prices.

To help you compare Tether’s gold purchase in Q3 2025, here is information about similar activity by central banks:

- The National Bank of Kazakhstan was the most significant purchaser in the quarter, boosting its gold reserves by 18 tons to a total of 324 tons.

- The Central Bank of Brazil, making its first gold purchase since July 2021, reported a 15-ton rise in its gold reserves in September 2025, bringing its total gold holdings to 145 tons.

- The Central Bank of Turkey maintained its continuous gold accumulation, with its official central bank and Treasury gold reserves growing by seven tons in Q3 to 641 tons.

- The Bank of Guatemala increased its gold reserves by six tons during the quarter, a substantial 91% jump. The bank now holds a total of 13 tons of gold, accounting for 5% of its total reserves.

While making such comparisons, it is important to remember that central banks have different objectives when purchasing gold.

Central banks acquire gold as part of their national monetary strategy, whereas Tether holds gold as part of its corporate reserves. The acquired gold serves as collateral for its stablecoin and as an asset diversification tactic.

The rise of non-state gold buyers

Before the rise of non-state gold buyers like Tether, demand for gold was driven mainly by central banks, the jewelry sector and commodity investors. In recent years, however, a growing share of gold purchases has come from private institutions, sovereign wealth funds, stablecoin issuers and corporate treasuries.

This shift is being driven by geopolitical uncertainty and fluctuations in currency values. Stablecoin issuers, in particular, have become significant participants. They are acquiring gold in quantities once associated with medium-sized national central banks.

Major technology companies and investment funds are also adding gold to their portfolios as part of broader strategies.

The rapid expansion of non-state gold buyers makes them a noticeable part of overall gold demand. They now form a steadily growing segment that is reshaping the pattern of global gold demand.

What Tether’s gold buying does not indicate

To prevent any misunderstanding, it is important to be clear about what this gold accumulation does not mean:

- It does not indicate liquidity problems or a risk of insolvency. Independent attestations confirm the relationship between assets and liabilities. A private entity buying gold does not, on its own, indicate financial difficulty unless such concerns are disclosed by the entity.

- It does not signal upcoming gold price moves. Gold buying by a non-state actor does not imply any market forecast or directional view.

- It is not a monetary decision in the way central banks operate. Private companies manage their reserves under different objectives and rules, and their gold holdings serve corporate and operational purposes rather than national monetary policy.

This helps place Tether’s gold buying in its proper context and supports a better understanding of what the move represents.

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

Alasdair Macleod….

3.CHRIS POWELL, Secretary/Treasurer//GATA DISPATCHES

Goldman Warns Copper’s Parabolic Breakout Lacks Stability

Thursday, Dec 04, 2025 – 07:45 AM

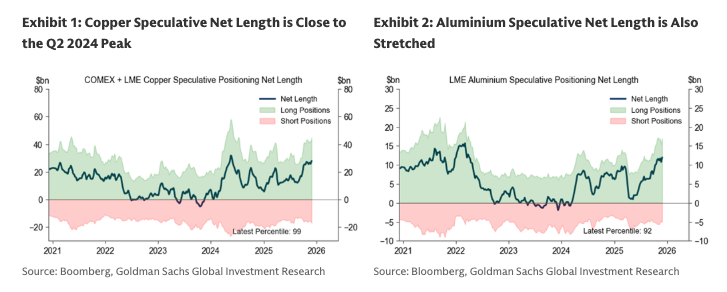

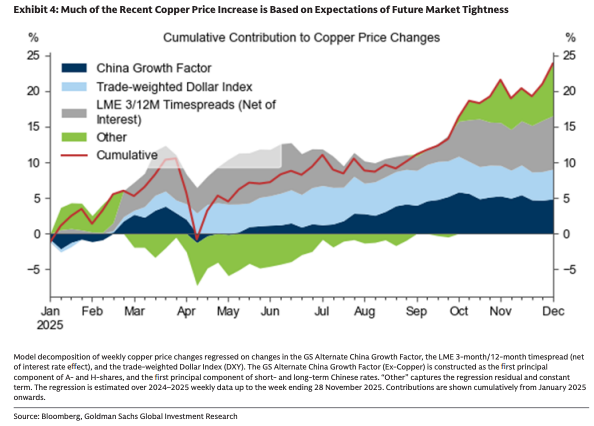

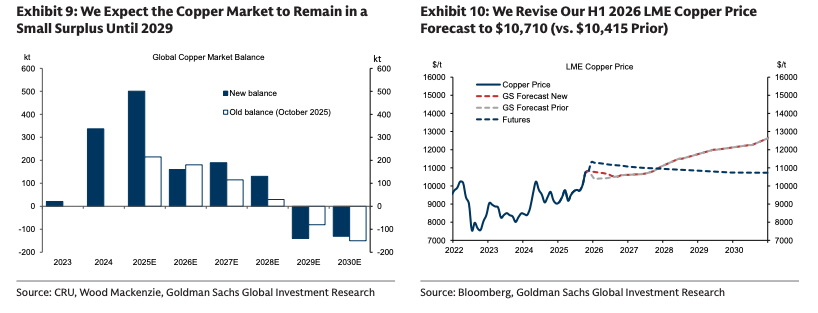

Copper futures on the London Metal Exchange opened the week with a breakout to new record highs (see report). On Wednesday, we highlighted a Goldman note detailing the “circular melt-up” mechanics driving the move higher. By Thursday, a separate Goldman analyst was cautioning clients that the parabolic move above $11,000/ton is unlikely to last.

At 6:30 ET, LME copper futures hit a fresh record at $11,575/ton, driven by a scramble to move metal into the US warehouses ahead of potential Trump-era import tariffs and a burst of demand from Asia. The combination has intensified global tightening fears amid soaring AI data center buildouts and massive power grid upgrades.

The question now is how long this breakout into record territory can last, and whether the momentum will carry into 2026. To address that question, a team of Goldman analysts led by Aurelia Waltham published an overnight note titled “Copper: Our Favourite Industrial Metal.”

“For 2026, we hold a selective outlook for industrial metals. Copper is our ‘favourite’ industrial metal as constrained mine supply growth and structural demand growth from grid & power infrastructure move the market towards balanced in 2026, from oversupplied in 2025,” Waltham told clients.

She continued, “Additionally, higher ex-US premia and conversations with physical traders point to a larger-than-expected reacceleration of copper flows into the US in H1 2026 ahead of a potential tariff, which should further tighten the ex-US market. As a result, we lift our average H1 2026 LME copper price forecast to $10,710 (from $10,415).”

Waltham addressed the ongoing parabolic price surge on the LME this week with a clear note of caution for clients:

That said, we do not expect the market to enter a period of material tightness until the end of the decade. Already-stretched speculative length means that we do not expect the current breakout above $11,000 to be sustained (as was the case in October). Most of the recent price increase has been driven by expectations of future market tightness, rather than current fundamentals (Exhibit 4).

The analyst noted:

While our much smaller 2026 surplus of 160kt moves the market closer to balanced, it means that we do not expect the global copper market to enter a shortage any time soon.

Beyond Waltham’s view, super-bull Kostas Bintas of Mercuria recently told Bloomberg, “If the world keeps going like this we will be left without copper cathodes in the rest of the world.”

Bintas warned, “Just looking at the facts, mathematically… what is going to happen if all of this continues? There’s only one answer: there will be tightness and a higher price.”

Li Xuezhi, head of research at Chaos Ternary Futures, a unit of a commodities hedge fund in Shanghai, said, “The rally has just started, we remain bullish on copper prices.”

The takeaway: LME copper futures look firmly pointed up and to the right for years to come, but the pace of the move is where some analysts’ views sharply diverge.

If you’ve been putting off those copper gutters or pipes for your next home-improvement project, you should lock them in sooner rather than later.

ZeroHedge Pro subs can read the full note in the usual place.

END

SHANGHAI CLOSED DOWN 2.21 POINTS OR 0.06%

//Hang Seng CLOSED UP 175.17 PTS OR 0.65%

// Nikkei CLOSED UP 1163.74 PTS OR 2.33% //Australia’s all ordinaries CLOSED UP 0.14%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.0717

/ OFFSHORE CLOSED DOWN AT 7.0666/ Oil UP TO 59.29 dollars per barrel for WTI and BRENT UP TO 62.85 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 7.0717 OFFSHORE YUAN TRADING DOWN TO 7.0666:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.0717

OFFSHORE YUAN: DOWN TO 7.0666

HANG SENG CLOSED UP 175.17 PTS OR 0.68%

2. Nikkei closed UP 1163.74 PTS OR 2.33%

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX UP TO 98.83 /// EURO RISES TO 1.1668 UP 13 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.941 // UP 5 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.52…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.392 DOWN 3 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN/JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.7550/ Italian 10 Yr bond yield UP to 3.455 SPAIN 10 YR BOND YIELD UP TO 3.228

3i Greek 10 year bond yield UP TO 3.392

3j Gold at $4206.20 Silver at: 57.57 1 am est) SILVER NEXT RESISTANCE LEVEL AT $54.00//AFTER 50.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 59/100 roubles/dollar; ROUBLE AT 77.01

3m oil (WTI) into the 59 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.82 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.941% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.392 DOWN 3 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8003 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9339 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.080 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.741 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.502 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.45 UP 1 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.4300 DOWN 2 PTS

30 YR UK BOND YIELD: 5.172 DOWN 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.226 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.779 DOWN 2 BASIS PTS.

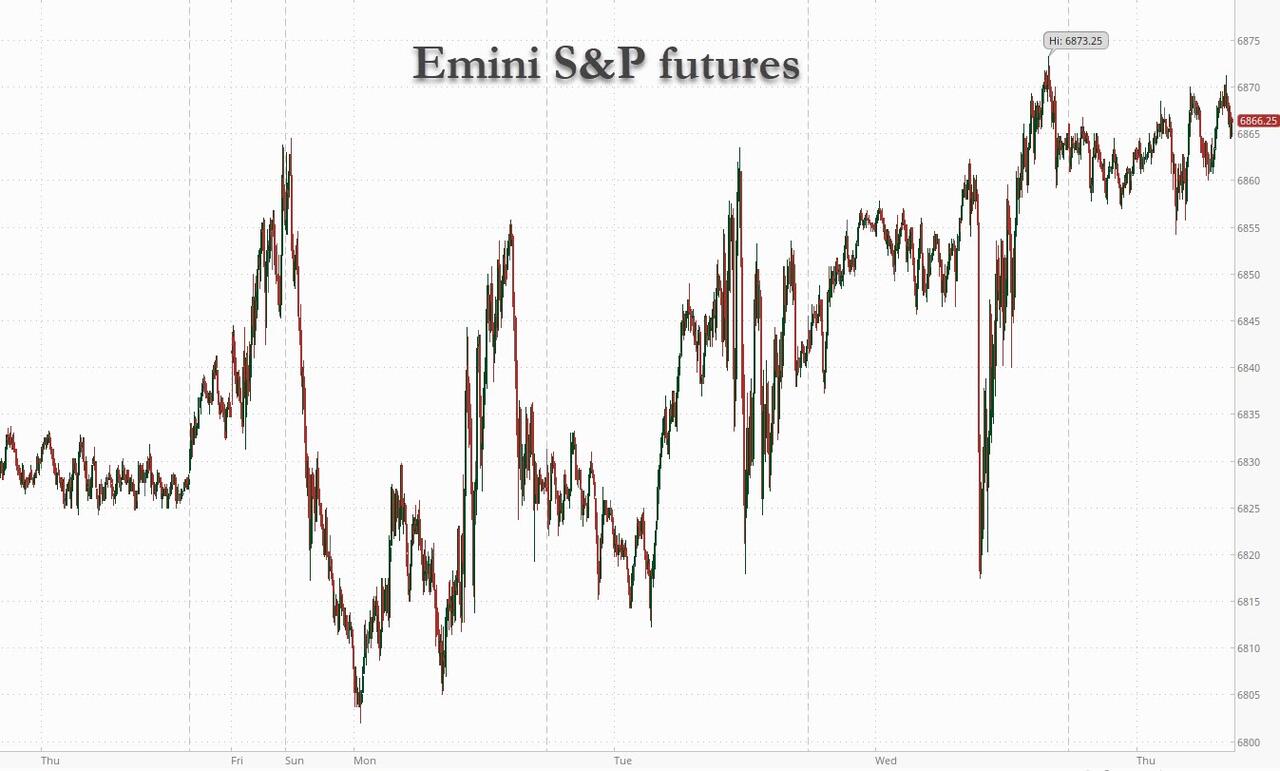

Futures Rise, S&P Set For 8th Gain In 9 Days

Thursday, Dec 04, 2025 – 08:50 AM

US equity futures rise, trading less than a percent away from a new record high amid signs of a leadership rotation with Big Tech not leading the bounce this time. As of 8:00am ET, S&P and Nasdaq 100 contracts are higher by about 0.1% after climbing in seven of the past eight sessions and extend on Wednesday’s gains when bad news was good news as a soft ADP jobs report bolstered expectations for a Fed rate cut next week. Challenger job cuts data for November showed job cuts fell 53% to 71,321 last month from October, but rose 24% from the 57,727 job cuts announced in the same month last year. Pre-market, Mag 7 were up a touch, led by TSLA (+0.9%), META (+0.6%) and NVDA (+0.5%). Salesforce is higher after its forecast beat and it gave a positive view on AI adoption. Bond yields were up modestly, USD unchanged, reversing an earlier drop to a one month low. Commodities are mixed: Oil and base metals are mostly higher; gold/silver are lagging. Bitcoin trades around $93, rebounding almost $10K from its low just days ago. Today’s calendar includes November Challenger jobs cuts (7:30am), weekly jobless claims (8:30am) and September factory orders (10am)

In pre-market trading, tech stocks were broadly steady with all Magnificent Seven megacaps apart from Apple posting modest gains, while Salesforce climbed on signs that customers are embracing its artificial intelligence tools.

- Mag 7 stocks mostly higher (Tesla +0.6%, Nvidia +0.4%, Meta +0.8%, Alphabet +0.6%, Microsoft +0.4%, Amazon +0.1%, Apple -0.04%)

- Axogen (AXGN) rises 5% after the provider of medical and surgical instruments said the FDA approved its biologics license application for its Avance nerve graft to treat peripheral nerve discontinuities.

- Bill Holdings Inc. (BILL) gains 3% after activist investor Barington Capital Group has taken a stake in business payments firm.

- Costco falls (COST) 1.1% after the retailer reported total comparable sales for November that missed the average analyst estimate.

- Dollar General (DG) rises 4% after the company raised its full-year outlook, highlighting value-focused retailers are winning over consumers hunting for deals.

- Guidewire (GWRE) jumps 5% after the software company’s first-quarter results and second-quarter revenue forecast topped analysts’ expectations.

- Hormel (HRL) rises 6% after the protein producer’s 3Q adj. EPS forecast beat the company’s recently lowered guidance, as well as the Street consensus.

- MBX Biosciences (MBX) slips 3% after Goldman Sachs initiated coverage of the drug developer with a sell rating, citing risk to the firm’s data readout in the near term.

- Salesforce Inc. (CRM) is up 1.9% after the software company gave an outlook for revenue in the current period that topped analysts’ estimates, suggesting it is persuading customers to buy its AI tools.

- Snowflake (SNOW) falls 8% after the software company issued a forecast for operating margin in the current quarter that fell short of the average analyst estimate. Analysts noted a deceleration in product revenue growth.

- UiPath (PATH) rises 8% after the software company’s third-quarter results beat expectations. It also gave a forecast.

- UniQure (QURE) falls 13% after saying the FDA indicated that data from its Phase I/II studies of an investigational gene therapy for Huntington’s disease are unlikely to provide primary evidence to support a biologics license application submission.

- ZIM (ZIM) rises 3% after Globes reports that Hapag-Lloyd submitted a bid to purchase the shipping company, without saying where it got the information.

Fed rate-cut expectations have fueled a broad rebound after November’s slump, with investors turning to defensive and other sectors as worries over stretched tech valuations persist. The small-cap Russell 2000 index is now just shy of a record high, while the Nasdaq 100 remains about 2% below its peak.

“We’re expecting a broadening of the rally for sectors that have so far been lagging,” said Amelie Derambure, senior portfolio manager at Amundi SA in Paris. “The Russell is very sensitive to interest rates, so the figures reinforced the market’s idea that the Fed will be able to lower rates, in a non-recessionary context.”

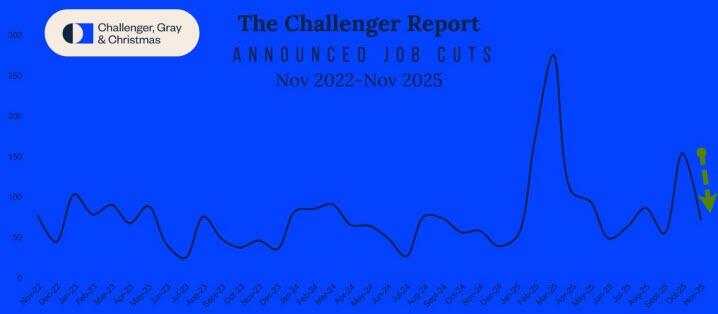

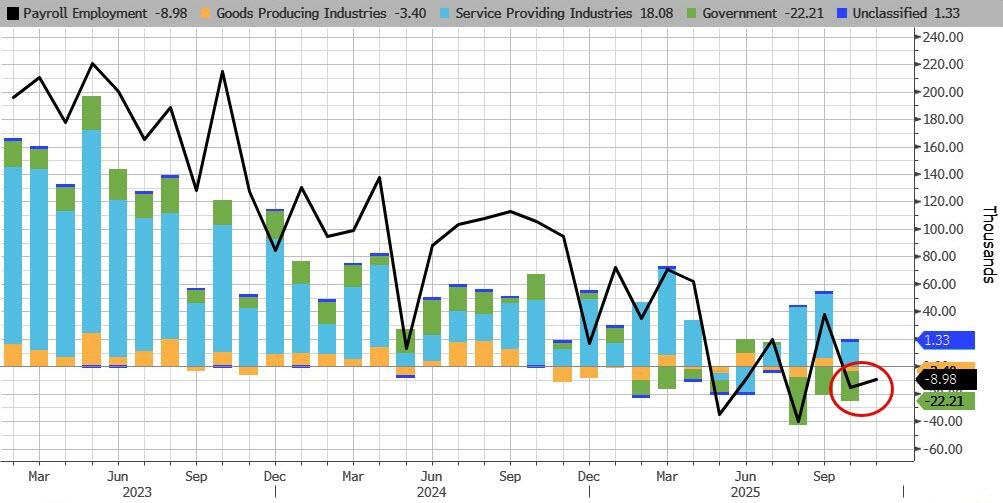

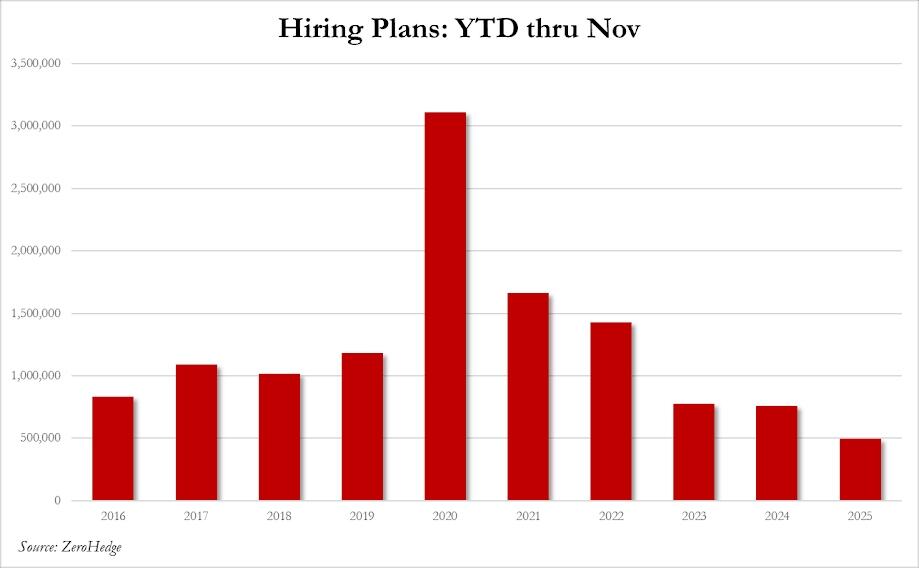

A report on corporate job-cut announcements from Challenger, Gray & Christmas Inc. added to evidence that the US labor market is softening. Announced layoffs fell last month after surging in October, but were still the highest for any November in three years, according to the outplacement firm. Meanwhile, YTD hiring plans are the lowest since 2010.

With official data still delayed, private indicators have increasingly pointed to employment coming under pressure from company belt-tightening and weaker spending. Worries about the jobs market and expectations that President Donald Trump will choose a Fed chair who shares his dovish stance have shifted market pricing toward as many as four rate cuts through 2026. Still, with the broader economy resilient, easier policy should continue to support stocks.

“Retail momentum stocks and crypto are still way below the recent peaks, though both have recovered from the recent lows,” wrote Mohit Kumar, chief economist and strategist for Europe at Jefferies. “We see sentiment remaining positive into year-end.”

Meanwhile, Goldman Sachs is looking past this month’s decision to what it calls a “foggy” Fed rate path in 2026. Risks to its terminal-rate range are skewed to the downside amid labor-market weakness, the bank wrote. They still expect two rate cuts next year. JPMorgan strategists expect the market to be boosted by higher equity demand next year. They project a supply-demand “improvement” of around $700 billion in 2026, which would be the strongest year since 2023.

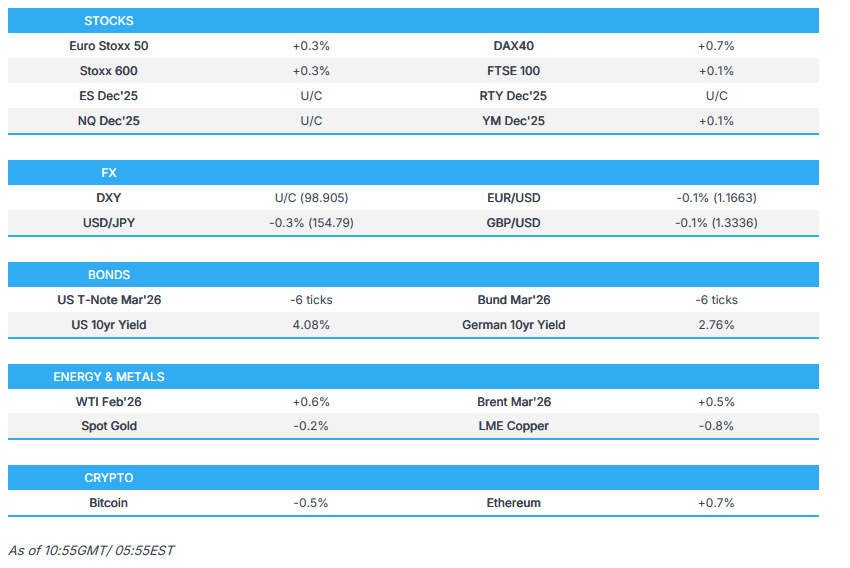

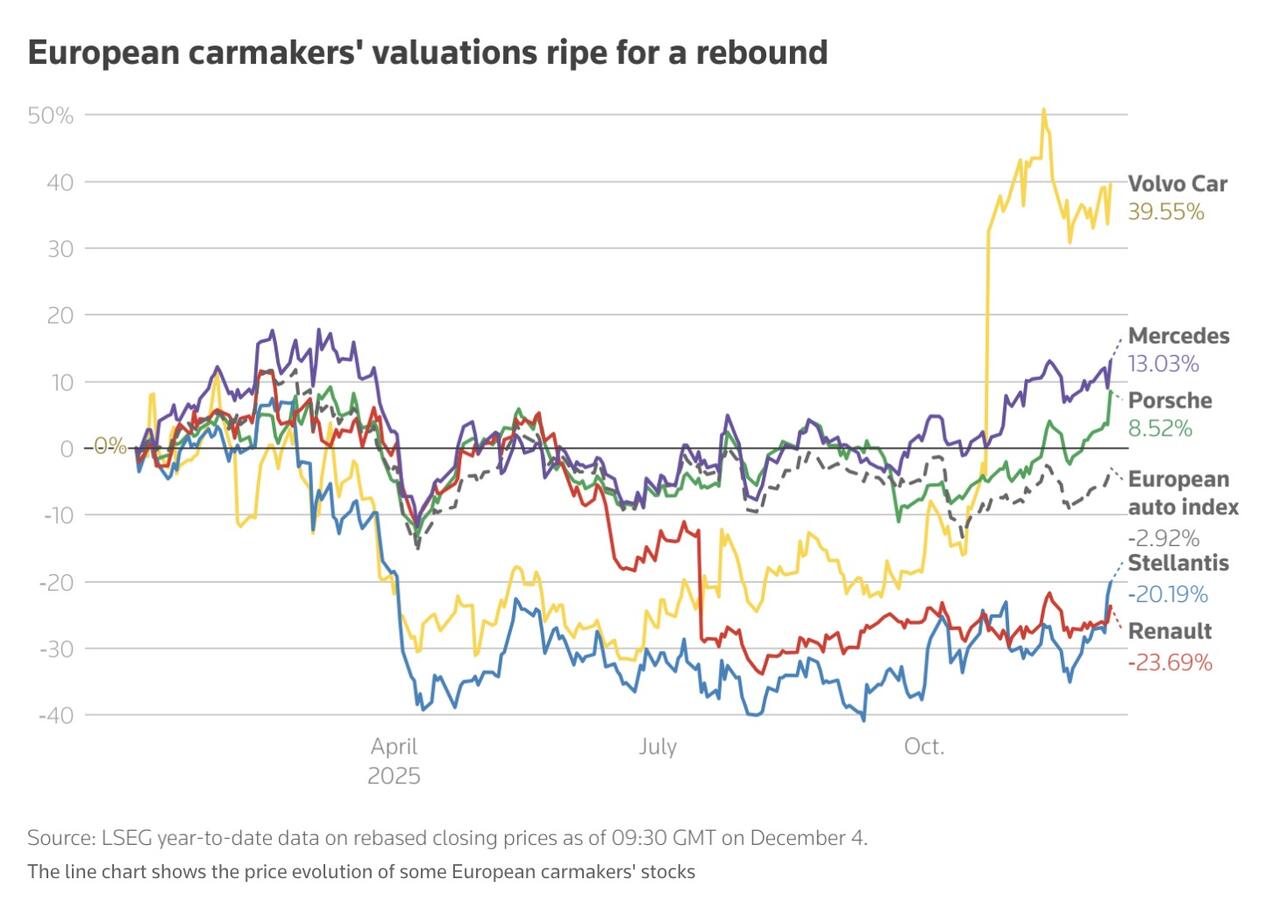

Europe’s Stoxx 600 is 0.3% higher with the DAX outperforming. Autos and industrial stocks are leading the way in Europe while utilities and healthcare dip. Automakers gain as Bank of America upgrades some stocks. Here are some of the biggest movers on Thursday:

- Mercedes, Renault gain as much as 4.4% and 4.8% respectively while holding company Porsche SE rises 5.7%, as Bank of America upgrades the stocks due to a more positive view on the European autos sector.

- Storytel gains as much as 6.5% after SEB initiated coverage of the Swedish audiobook and publishing house with a buy rating, saying the company has improved the quality of its subscriber base and its internal efficiency.

- Cosmo shares rise as much as 5.5%, adding to Wednesday’s 20% jump following positive late-stage trial results for the life science company’s experimental treatment for male hair loss.

- Balfour Beatty shares rise as much as 2.4% after the engineering and construction group said it expects to grow its order book by 20% in 2025 and confirmed more buybacks are on the way in 2026.

- Philips shares drop as much as 8.6% after Citi analysts noted tariff and China challenges for 2026.

- Trustpilot shares fall as much as 21% after Grizzly Research published a report on the consumer-review company.

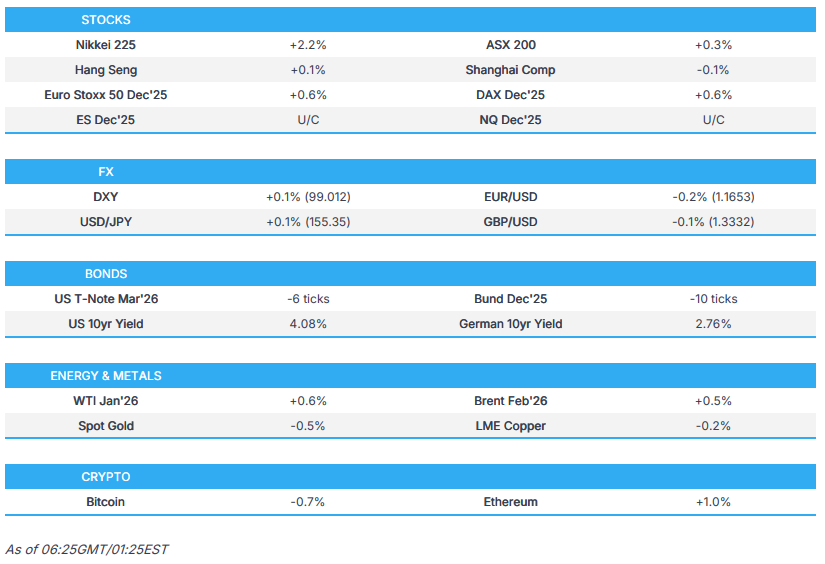

Earlier in the session, Asian stocks rose for a third straight day, led by gains in Japan as regional tech shares tracked their US peers higher. The MSCI Asia Pacific Index advanced as much as 0.9%, with SoftBank Group and Keyence among the biggest contributors. Shares fluctuated in China and Hong Kong, while South Korean stocks slipped. India’s benchmark struggled to hold early gains even as the rupee strengthened against the dollar. Sentiment across the region is improving on rising expectations of a Federal Reserve rate cut this month after the latest US jobs data. Meanwhile, a slightly weaker yen is providing an extra lift to Japanese exporters. Semiconductor shares are showing signs of weakness, with South Korea’s tech-heavy stock index slipping more than 1% as foreign funds take profit. A Microsoft Corp. update is also weighing on sentiment, after a media report that the firm lowered expectations for business customers buying on the cloud unit’s marketplace for artificial intelligence models and agents.

In FX, the dollar gives up earlier gains, Aussie outperforming on bets the central bank may pivot back to rate hikes.

In rates, global bonds weakened, driven by rising yields in Japan. Sentiment shifted as some senior government officials signaled they wouldn’t oppose a Bank of Japan rate hike this month. Treasury yields are rising across the curve. German bonds falling on growing government uncertainty. Gilts are outperforming after very weak construction activity data sparks a small increase in BOE rate-cut bets.

In commodities, oil prices are higher, albeit with some volatility. Brent is trading around $63/barrel. Gold is recovering ground and now trading close to $4,200/oz. Bitcoin, meanwhile, held above $93,000. The dollar was little changed.

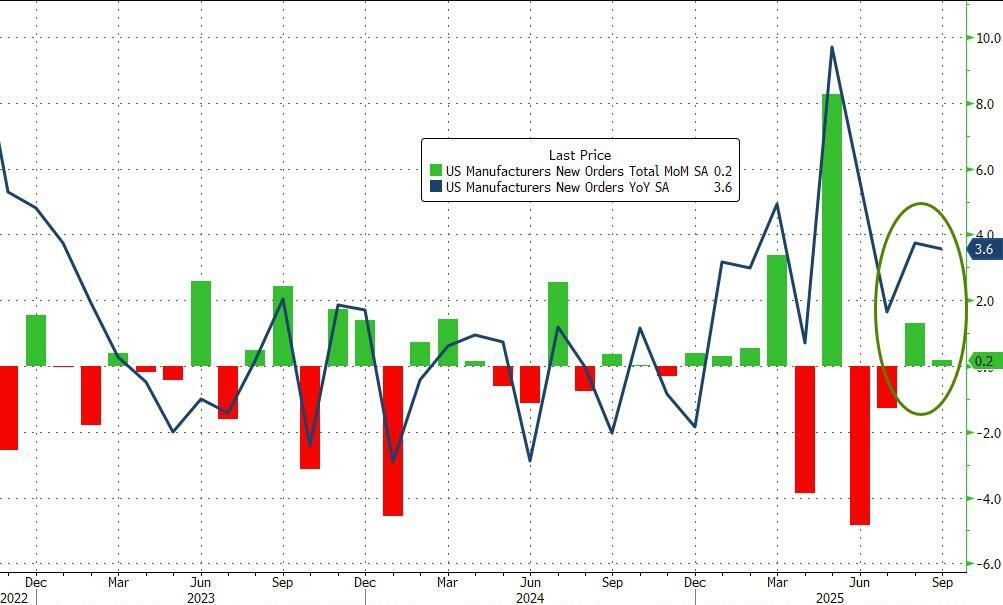

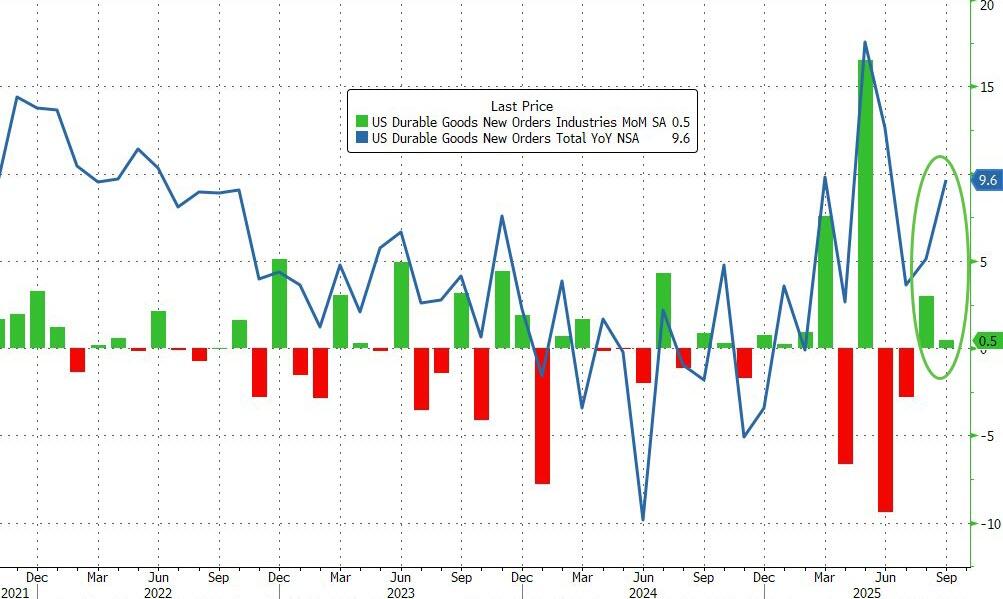

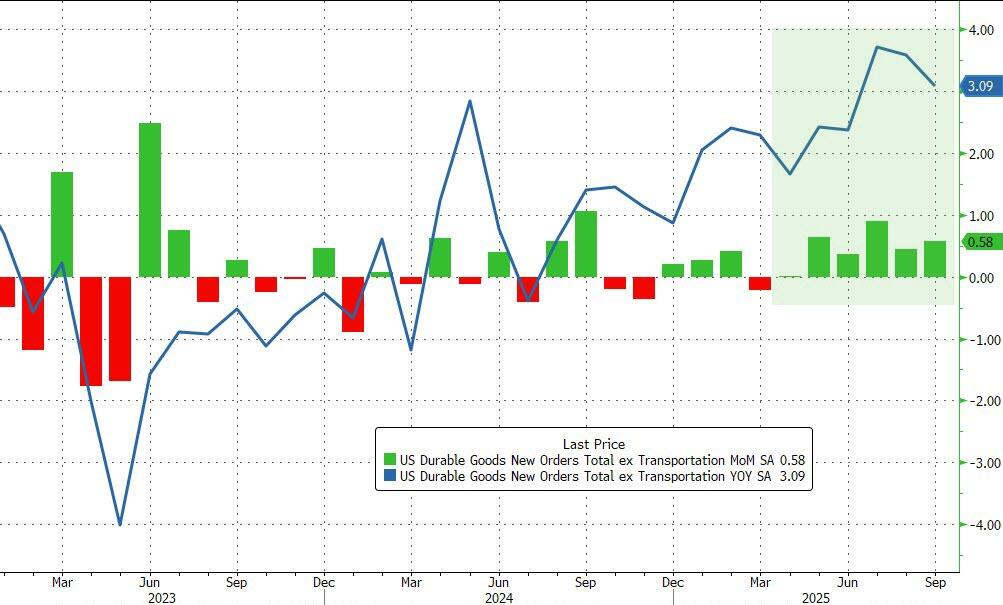

US economic calendar includes November Challenger jobs cuts (7:30am), weekly jobless claims (8:30am) and September factory orders (10am)

Market Snapshot

- S&P 500 mini and Nasdaq 100 mini little-changed

- Russell 2000 mini steady

- Stoxx Europe 600 +0.3%

- DAX +0.8%

- CAC 40 +0.4%

- 10-year Treasury yield +2 basis points at 4.08%

- VIX +0.1 points at 16.17

- Bloomberg Dollar Index little changed at 1212.82

- euro little changed at $1.1668

- WTI crude +0.4% at $59.21/barrel

Top Overnight News

- Donald Trump’s aides are considering having Scott Bessent also head the National Economic Council if Kevin Hassett becomes Fed chair, people familiar said. BBG

- Trump’s administration ordered an enhanced vetting of H-1B visa applicants, with new H-1B visa screening based on any involvement in censorship or free speech, according to the State Department memo.

- Trump said he may work out another trade deal with Canada and Mexico. BBG

- Vladimir Putin said Russia didn’t agree with some points of the US peace proposal for Ukraine, Tass reported, citing his interview with a local media outlet. Earlier, Trump called the meeting between Steve Witkoff and Putin “reasonably good” but next steps remain unclear. BBG