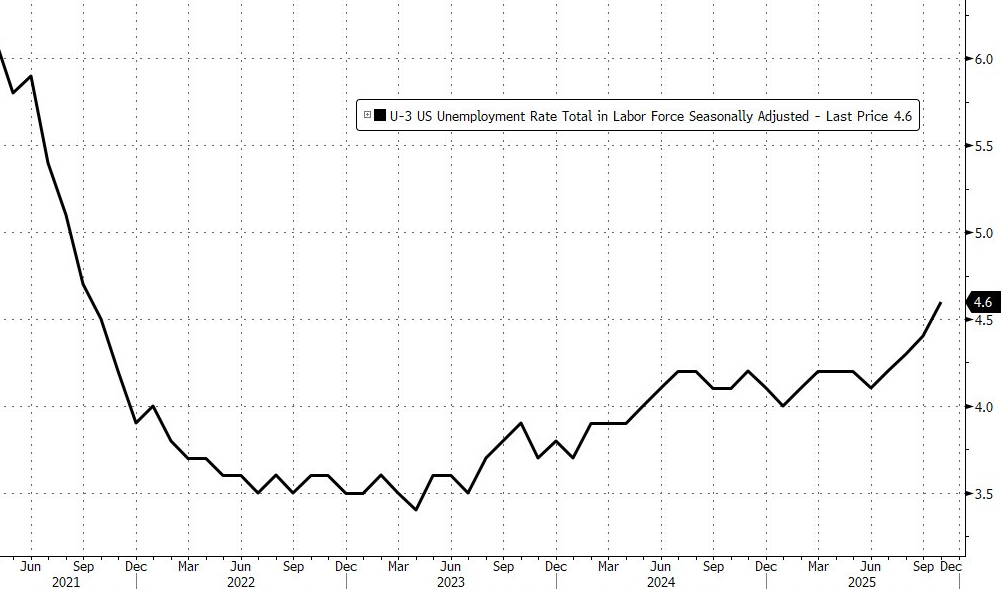

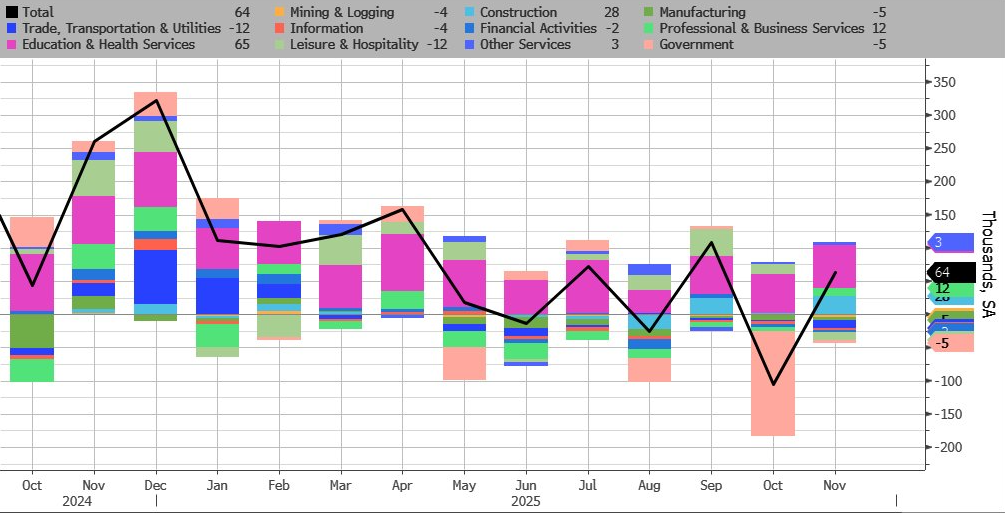

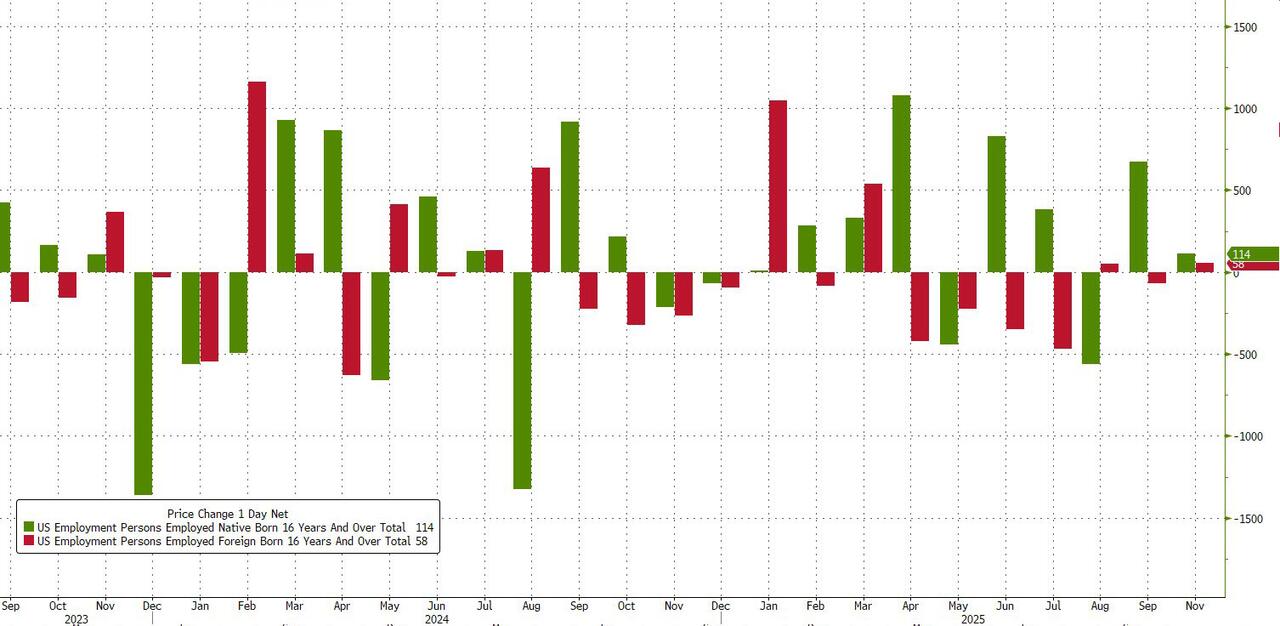

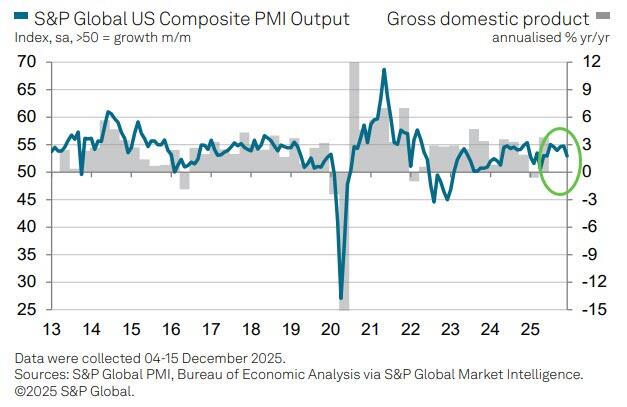

DEC 16/GOLD CLOSED DOWN $3.95 TO $4301.80/SILVER ALSO CLOSED DOWN BY $0.07 TO $63.46 DESPITE THE FACT THAT SILVER IS BACKWARD MARCH TO DECEMBER AND ITS LEASE RATE FOR BORROWING SILVER FOR ONE TO 3 MONTHS IS 7%//PLATINUM CONTINUES TO SKYROCKET UP ANOTHER $54.30 TO $1843.40 WHILE PALLADIUM CLOSED UP $32.70 TO $1605.40//COMMODITY REPORT TONIGHT ON SILVER AND PLATINUM//GREAT COMMENTARY ON CHINA’S STRENGTH IN THE RARE EARTH FIELD//JIMMY LAI CONVICTED IN HONG KONG AS FREE SPEECH HAS ENDED IN THAT COLONY// ITALY IS NOW AGAINST THE USE OF FROZEN RUSSIAN ASSETS: A GREAT COMMENTARY ON THAT//ISRAEL VS HAMAS UPDATES/TBN ISRAEL LAST 24 HRS//MANY UPDATES ON RUSSIA VS UKRAINE/COVID UPDATES//OIL UPDATES//USA DATA RELEASES: FAIR GAIN IN JOBS YET UNEMPLOYMENT RISES//POOR PMI REPORTS/SWAMP STORIES FOR YOU TONIGHT///

072 C GOLDMAN 27 092 C DEUTSCHE BANK 2 118 C MACQUARIE FUTURES US 143 118 H MACQUARIE FUTURES US 134 332 H STANDARD CHARTERED B 133 363 H WELLS FARGO SECURITI 88 435 H SCOTIA CAPITAL (USA) 7 661 C JP MORGAN SECURITIES 529 123 686 C STONEX FINANCIAL INC 1 690 C ABN AMRO CLR USA LLC 4 709 C BARCLAYS 140 905 C ADM 13

TOTAL: 672 672 MONTH TO DATE: 29,109

JPMORGAN STOPPED 123/672

DECEMBER

GOLD: NUMBER OF NOTICES FILED FOR DEC/2025: 672 CONTRACTs NOTICES FOR 67,200 OZ or 2.0902 TONNES

total notices so far: 29,108 contracts for 2,910,800 OR 90.538 tonnes)

FOR DEC

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 84 NOTICE(S) FILED FOR 0.420 MILLION OZ/

total number of notices filed so far this month : 11,663 CONTRACTS (NOTICES) for 58.315 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $3.95 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD//

INVENTORY RESTS AT 1051.69 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.07 AT THE SLV:

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:/ // A WITHDRAWAL OF 1.36 MILLION OZ

OUT OF THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 516.360. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 196 CONTRACTS TO 154,451 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITEH OUR HUGE $1.62 GAIN IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S // TRADING. THE LONG SPECULATORS ARE STILL QUITE RELENTLESS AS THEY POUR INTO THE OPEN INTEREST AT THE COMEX. THE FRBNY CONTINUES TO SUPPLY THE NECESSARY PAPER AS THEY TRY TO DRIVE THE PRICE SOUTHBOUND WITH THE HELP OF HIGH FREQUENCY TRADERS AND T.A.S. SPREADERS BUT WITH A NO SUCCESS ON MONDAY. THEN EARLY MONDAY MORNING WE RECEIVED NOTICE OF A HUGE 170 CONTRACT EXCHANGE FOR RISK AND NO DOUBT THE RECIPIENT OF THIS IS THE CENTRAL BANK OF INDIA. THE TOTAL IN OZ FOR THIS EXCHANGE FOR RISK IS .850 MILLION OZ AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE TO GIVE US THE EXACT AMOUNT OF SILVER STANDING FOR DECEMBER.

WE HAVE REVERTED BACK TO NORMAL WITH THE SPECS NOW GOING ON THE LONG SIDE AND THE BANKER (FRBNY) ON THE SHORT SIDE AND PROVIDING THE NECESSARY SHORT PAPER. IT IS OUR SILVER SPECULATORS THAT WERE PILING INTO THE SILVER COMEX. WE FINALLY ARE MOVING TO A MUCH HIGHER BASE SURPASSING THE $34.40 SILVER PRICE BARRIER TO A HIGH DEGREE, AND NOW SURPASSING SURPASS OUR LAST MAJOR HURDLE OF $50.00 SILVER AGAIN. WE HAD A FAIR SIZED GAIN OF 328 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL SIZED 132 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO MONDAY TRADING WITH OUR HUGE GAIN IN PRICE /// THEY DESPERATELY AGAIN TODAY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $50.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED AGAIN ON THURSDAY WITH SILVER’S GAIN IN PRICE AS THE SPECS PILED INTO THE SILVER ARENA. . THE PRICE FINISHED HUGELY ABOVE THE MAGIC NUMBER OF $50.00 SILVER SPOT PRICE CLOSING AT $63.44 UP $1.62 . WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS AT A HUGE SIZED 1242 T.A.S. CONTRACTS (BUT STILL DOWN FROM THE MEGA MEGA HUGE SIZED 5,000 PLUS CONTRACT ISSUANCE DURING NOVEMBER)!!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING AGAIN THE 50.00 DOLLAR MARK!!. THERE IS NO NEXT LINE IN THE SAND ONCE THE 50.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A SMALL SIZED 132 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 1242 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//RAID AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE HAD A FAIR SIZED GAIN OF 328 CONTRACTS ON OUR TWO EXCHANGES WITH OUR HUGE GAIN IN PRICE OF $1.62. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION AND NO DOUBT REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE SPECULATOR LONGS REMAIN STOIC EVEN ON PRICE FALLS. EASTERN CENTRAL BANKER WENT TO THE LONG SIDE. THEY WILL TENDER FOR THE BADLY NEEDED PHYSICAL SILVER. THUS ON A NET BASIS WE LOST NO SPECULATORS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT//TUESDAY MORNING: A HUGE SIZED 1242 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR DEC: 49.33 MILLION OZ FOLLOWED BY TODAY’S STRONG 1.470 MILLION OZ QUEUE JUMP _ PLUS ..850 MILLION OZ EXCHANGE FOR RISK////STANDING ADVANCES TO 62.425 MILLION OZ//

WE HAD:

/ SMALL SIZED COMEX OI GAIN+// A SMALL 196 EFP ISSUANCE CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 1242 CONTRACTS)/VII: DECEMBER ISSUED ITS FIRST EXCHANGE FOR RISK OF 0.850 MILLION OZ//

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED ANOTHER 157 CONTRACTS!!!!! THAT IS WE HAVE ADDED 7 OUT OF THE LAST 9 DAYS CONTRACTS TO THE SILVER OI TOTAL

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC.. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC.

TOTAL CONTRACTS for 13 DAY(S), total 5874 contracts: OR 29.370 MILLION OZ (451 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 29.370 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 29.370 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 843 CONTRACTS WITH OUR GAIN IN PRICE OF $1.62 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A HUGE SIZED CONTRACT EFP ISSUANCE : 735 ISSUED FOR MARCH, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 9 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER HUGE 1.470 MILLION OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ // STANDING ADVANCES TO 62.425 MILLION OZ//

THE NEW TAS ISSUANCE MONDAY NIGHT (1242) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!!

WE HAD 84 NOTICE(S) FILED TODAY FOR 0.420 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON A MASSIVE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE\

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 6897 OI CONTRACTS UP TO 467,088 OI AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A RELATIVELY LOWISH OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE AND CRIMINAL 2391 CONTRACTS // MEGA HUGE GOVERNMENT REMOVALS//

WE HAD A STRONG GAIN IN COMEX OI (6897 CONTRACTS) . THIS OCCURRED WITH OUR GAIN OF $10.15 IN PRICE// MONDAY///.

LAST 8 MONTHS OF GOLD DELIVERIES: (MAY THROUGH TO NOVEMBER/DECEMBER)

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 2.684 TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 17.005 TONNES//NEW STANDING ADVANCES TO 97.402 TONNES/

E.F.P. ISSUANCE/FOR OPENING DECEMBER GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 4454 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 467,088 AND WE NOW WITNESSING A NOW BIGGER COMEX OI BUT WITH AN EXTREMELY HIGH PRICE OF GOLD.//NOW EASIER TO FLEECE SPECS.

SILVER ALSO HAS A SMALL SIZED COMEX OI OF 154,451 CONTRACTS//BUT STILL DIFFICULT TO FLEECE SPEC LONGS.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,351 CONTRACTS WITH 6897 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4454 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 11,351 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1509 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON LIKE TODAY.

GOLD PRICE ON MONDAY ROSE BY $10.15

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(4454) ACCOMPANYING THE STRONG GAIN IN COMEX OI OF 6897 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 11,351 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND NEWBIE SPECULATORS GOING TO THE LONG SIDE AND POURING IT ON WITH RECKLASS ABANDON!! . ,2.) STRONG INITIAL STANDING FOR GOLD FOR DEC AT 83.813 TONNES OF NORMAL DELIVERY FOLLOWED BY OUR 2.684 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPING OF 17.005 TONNES//NEW STANDING ADVANCES TO 97.402 TONNES

NEW STANDING ADVANCES TO 97.402 TONNES.

NEW STANDING FOR GOLD, DEC CONTRACT AT 97.402 TONNES OF GOLD

3) ZERO T.A.S. LIQUIDATION (BUT CONSIDERABLE GOVT LIQUIDATION // AND STRONG LOSS OF EQUITY SHARES/DEC 16) AS WE HAD 1)A $10.15 COMEX PRICE FALL AND WE HAD 2) NEWBIE SPEC SHORTS GETTING LIQUIFIED AND ON A NET BASIS, THE SPECS GAINED HUGELY IN NUMBERS + EASTERN CENTRAL BANKERS WERE PILING INTO THE LONG SIDE AS WE HAD A HUGE SIZED GAIN OF 11,351 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A HUGE AMOUNT OF GOLD WILL STAND FOR DELIVERY IN DECEMBER (97.402 TONNES). //, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL WITH THE RISE IN PRICE YESTERDAY

4) STRONG SIZED COMEX OI GAIN/ 5) V) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (4454) AND A FAIR T.A.S. ISSUANCE 1509 FOR RAID PURPOSES WHICH STARTED TODAY.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

TOTAL EFP CONTRACTS ISSUED: 33,650 CONTRACTS OR 3,365,000 OZ OR 104.665 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 2588 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN13 TRADING DAY(S) IN TONNES: 14.665 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 104.665 TONNES DIVIDED BY 3550 x 100% TONNES = 2.95% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 104.665 TONNES//VERY SMALL THIS MONTH.

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A SMALL SIZED 230 CONTRACTS OI TO 154,485 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 132 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 132 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 196 CONTRACTS AND ADD TO THE 132 E.FP. ISSUED

WE OBTAIN A FAIR SIZED GAIN OF 362 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR HUGE GAIN OF $1.62 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 1.810 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ASIA RESULTS; TUESDAY DEC 16

SHANGHAI CLOSED DOWN 43.11 POINTS OR 1.11%

//Hang Seng CLOSED DOWN 393.47 PTS OR 1.54%

// Nikkei CLOSED DOWN 726.11 PTS OR 1.45% //Australia’s all ordinaries CLOSED DOWN 0.14%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.0422

/ OFFSHORE CLOSED UP AT 7.0392/ Oil DOWN TO 55.99 dollars per barrel for WTI and BRENT DOWN TO 59.84 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.0423 OFFSHORE YUAN TRADING UP TO 7.0372:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 5882 CONTRACTS TO 466,073 OI WITH OUR GAIN IN PRICE OF $10.15 WITH RESPECT TO MONDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4454). WE HAD ZERO T.A.S. LIQUIDATION MONDAY (WITH MONTH END SPREADER LIQUIDATIONS FINISHED ON NOV 30). . IT SEEMS THAT THE SPECULATORS WENT MASSIVELY HUGE TO THE LONG SIDE WITH OUR FRBNY PROVIDING STILL THE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE .

YOU WILL NOTICE THAT THE COMEX OI IS NOW GAINING FROM ITS LOW TO NOW 466,073 AND NOW SOME OF THESE GUYS ARE NOT VERY STICKY AND THUS VULNERABLE TO A RAID.

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 10,336 CONTRACTS (OR 32.149 TONNES). THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR 0 OZ OR NIL TONNES OF GOLD.

FIRST LETS DO A REVIEW OF EXCHANGE FOR RISK ISSUANCES THIS PAST YEAR

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD PRIOR MONTHS

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;TOTAL EXCHANGE FOR RISK LAST 6 MONTHS 70.097 TONNES. THE RECIPIENT OF THESE EXCHANGE FOR RISK IS THE BANK OF ENGLAND. THIS CENTRAL BANK LOANED OUT ITS GOLD AND WANTS IT BACK. THEIR TOTAL RESERVES PRIOR TO THE LOANS IS LISTED AT 310 TONNES.

LET US LOOK AT JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

NOW LET US LOOK AT THE MONTH OF AUGUST:

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

NOW LET US LOOK AT SEPT.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES//FOR 14.553 TONNES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

LET’S SUM UP EXCHANGE FOR RISK FOR THE LAST 11 MONTHS

HISTORY: LAST 11 MONTH’S EXCHANGE FOR RISK//TOTAL CONTRACT ISSUANCES //TONNES OF GOLD

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

NOVEMBER:

NOVEMBER: TWO ISSUANCES:

WHICH NOW BRINGS US TO NOVEMBER WHERE WE RECEIVED NOTICE OF OUR SECOND ISSUANCE OF 1016 CONTRACTS FOR 101,600 OZ OR 3.165 TONNES. WE MUST NOW ADD THIS TO OUR INITIAL ISSUANCE OF 450 NOTICES //45000 OZ OR 1.3996 TONNES. THUS THE NEW TOTAL EXCHANGE FOR RISK FOR NOVEMBER IS 1,466 NOTICES FOR 146,600 OZ OR 4.5598 TONNES OF GOLD.

AND NOW DECEMBER: SO FAR 0 NOTICES ISSUED:

DEC 0

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 10 MONTH TOTALS 134.8646 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES) NO WONDER THE BANK OF ENGLAND THROUGH THE E.E.A. CANNOT SIGN OFF ON THEIR AUDIT

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 39 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES IN AUGUST AND THEN ADDED 24 TONNES IN SEPT AND FINALLY LAST MONTH COVERED 15 TONNES TO CREATE A SHORTFALL OF 39 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 12TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK THIS YEAR !!…..(DEC 24 THROUGH DEC 25//ONLY MISSING JUNE. TOTAL 12 MONTHS ISSUANCE 134.8646 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S E.E.A. AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OUR NEW DECEMBER COMEX CONTRACT MONTH//

IN TOTAL WE HAD A HUGE SIZED GAIN ON OUR TWO EXCHANGES OF 10,336 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 3.9% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER. GRASBERG WILL NOT BE READY TO RESUME NORMAL PRODUCTION UNTIL JULY 2026

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH DECEMBER/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR T.A.S ISSUANCE CONTRACTS. THE CME NOTIFIES US THAT THEY HAVE ISSUED 1,509 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE HUGE NUMBER OF T.A.S. ISSUANCE AND THUS A FORTHCOMING RAIDS THIS WEEK.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 0.0 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 2.684 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 17.005 TONNES//STANDING ADVANCES TO 97.402 TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 39+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 39 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 39 TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING:

EXCHANGE FOR PHYSICAL ISSUANCE/DEC.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED EXCHANGE FOR PHYSICAL OF 4464 CONTRACTS.

THAT IS A HUGE SIZED 4464 EFP CONTRACT WAS ISSUED: : /FEB 4464 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4464 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 39 TONNES

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE CONSIDERABLE GOVERNMENT LIQUIDATION

MONTH END SPREADERS HAVE NOW FINISHED

T.A.S.SPREADER ISSUANCE//DECEMBER

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT//TUESDAY MORNING WAS A FAIR SIZED 1509 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP MONDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING GAIN OF COMEX OI AND A HUGE EXCHANGE FOR PHYSICAL ISSUANCE..ENOUGH FODDER FOR THE COMMENCEMENT OF A RAID WHICH COMMENCED AROUND 10 PM LAST NIGHT

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

GOLD STANDING AT THE COMEX FOR GOLD LAST 12 MONTHS OF 2025

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 2.684 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 17.005 TONNES//NEW STANDING ADVANCES TO 97.402 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING DECEMBER,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $14.20/ /)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION WITH OUR STRONG PRICE GAIN////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX// WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL FRIDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR DECEMBER. THE COMEX IS ONE BIG MESS!! THIS WEEK,

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

A LITTLE REVIEW OF GOLD STANDING THESE PAST 3 MONTHS:

STANDING FOR GOLD OCT THROUGH TO DECEMBER:

ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 863 CONTRACT QUEUE JUMP FOR 86,300 OZ OR 2.684 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 17.005 TONNES///STANDING ADVANCES TO 97.402 TONNES.

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $10.15

WE HAD A HUGE XXXX CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .

NET GAIN ON THE TWO EXCHANGES : 10,336 CONTRACTS OR 1,033,600 OZ OR 32.149 TONNES

Total monthly oz gold served (contracts) so far this month

29,108 notices 2,910,800 0z 90.538TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

i) 1 ENTRIES

i) Into Manfra: 24,113.250 oz (750 kilobars)

customer withdrawals:

0 ENTRIES

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1// CUSTOMER ACCOUNT TO DEALER

a) Brinks 133,450.952 oz (4152 kilobars)

4.152 tonnes

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF DECEMBER STANDS AT 2878 CONTRACTS FOR A GAIN OF 857 CONTRACTS. WE HAD 6 CONTRACTS FILED ON MONDAY SO WE GAINED A WHOPPING 863 CONTRACTS FOR A QUEUE JUMP OF 86,300 OZ OR 2.684 TONNES TO WHICH WE ADD TO OUR PREVIOUS QUEUE JUMPS .THUS STANDING FOR GOLD IN DECEMBER INCREASES HUGELY TO 97.402 TONNES

JANUARY LOST 30 CONTRACTS DOWN TO 3050

FEB GAINED 3969 CONTRACTS UP TO 339,237 CONTRACTS

We had 672 contracts filed for today representing 67,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 528 notices issued from their client or customer account. The total of all issuance by all participants equate to 672 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 123 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2025. contract month, we take the total number of notices filed so far for the month (29,108 ) to which we add the difference between the open interest for the front month of DEC ( 2872 CONTRACTS) minus the number of notices served upon today (672 x 100 oz per contract) equals 3,131,500 OZ OR 97.402 Tonnes of gold

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (29,108 x 100 oz +we add the difference for front month of DEC (2872 OI} minus the number of notices served upon today (672)x 100 oz) which equals 3,131,500 OR 97.402 TONNES

new total of gold standing in DECEMBER is 97.402 tonnes

TOTAL COMEX GOLD STANDING FOR DEC ..: 97.402 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF DECEMBER

volume MONDAY confirmed 223,993 fair

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,991,242.509 oz 61.99 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 35,991,344.896 oz

TOTAL REGISTERED GOLD 19,191,884.913 or 595.948 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,799,659.983 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,200,642oz ((REG GOLD- PLEDGED GOLD)=

535.012 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

THE DEC. 2025 SILVER CONTRACTS

DEC 16 2025

INITIAL/

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

2 entries

i) Out of HSBC 600,134.800 oz ii) Out of JPMorgan: 1,286,159.900 oz

total withdrawal: 1,886,294.700 oz

Deposits to the Dealer Inventory

1 ENTRY

i) Into Stonex; 353,152.500 oz

total deposit 353,152.500 oz

Deposits to the Customer Inventory

2 entries

i) Into CNT 5811.000 oz ii) Into HSBC 813,092.240 oz\

total deposit; 818,903.240 oz

No of oz served today (contracts)

84 CONTRACT(S) ( 0.420 million OZ

No of oz to be served (notices)

442 contracts (2.210 MILLION oz)

Total monthly oz silver served (contracts)

11,663 Contracts (58.315 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

please note: lack of any silver coming in or leaving the comex

DEPOSITS INTO DEALER ACCOUNTS

1 ENTRY

1 ENTRY

I) Inro Stonex: 353,152.500 oz

total dealer deposit 353,152.500 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 entries

i) Into CNT 5811.000 oz ii) Into HSBC 813,092.240 oz\

total deposit; 818,903.240 oz

withdrawals: customer side/eligible

2 entries

i) Out of HSBC 600,134.800 oz ii) Out of JPMorgan: 1,286,159.900 oz

total withdrawal: 1,886,294.700 oz

adjustments: 1// all dealer to customer

a) CNT 60,636.230 oz

TOTAL REGISTERED SILVER: 130.147MILLION OZ//.TOTAL REG + ELIGIBLE. 453.846Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC.

silver open interest data:

FRONT MONTH OF DECEMBER /2025 OI: 736 OPEN INTEREST CONTRACTS FOR A LOSS OF 154 CONTRACTS. WE HAD 448 CONTRACTS FILED ON MONDAY SO WE ACTUALLY HAD ANOTHER HUGE QUEUE JUMP OF 294 CONTRACTS OR 1.470 MILLION OZ

JANUARY GAINED 83 CONTRACTS UP TO 4201 CONTRACTS

FEB GAINED 21` CONTRACTS UP TO 1433 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 84 or 0.420 MILLION oz

CONFIRMED volume; ON MONDAY 125,079 huge//

AND NOW DECEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 11,663 X5,000 oz = 58.315 MILLION oz

to which we add the difference between the open interest for the front month of DEC (736) AND the number of notices served upon today (84 )x (5000 oz)

Thus the standings for silver for the DECEMBER 2025 contract month: (11,663) Notices served so far) x 5000 oz + OI for the front month of DEC(736) minus number of notices served upon today (84)x 5000 oz equals silver standing for the DEC.contract month equating to 61.575 MILLION OZ + 850 MILLION OZ FOR DEC ‘S FIRST EXCHANGE FOR RISK: NEW TOTALS STANDING 62.425 MILLION OZ!!!

New total standing: 62.425 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 130.647. million oz of registered silver

JPMorgan as a percentage of total silver: 193.723/453.846million. 42.68%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

DEC 16/WITH GOLD DOWN $3.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 15/WITH GOLD UP $10.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 105.12 TONNES

DEC 12/WITH GOLD UP $14.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.83 TONNES

DEC 11/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 10/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 9/WITH GOLD UP $18.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.14 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1049.11 TONNES

DEC 8/WITH GOLD DOWN $23.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.33 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1050.25 TONNES

DEC 5/WITH GOLD UP $9.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 4.00 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.58 TONNES

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

DEC 3/WITH GOLD UP $14.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1048.30 TONNES

DEC 2/WITH GOLD DOWN $53.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.58 TONNES OF GOLD VAPOUR INTO THE GLD// /// ///INVENTORY RESTS AT 1050.01TONNES

DEC 1/WITH GOLD UP $22.75 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43TONNES

NOV 28/WITH GOLD UP $51.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43 TONNES

NOV 26/WITH GOLD UP $25.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT PAPER DEPOSIT OF 4.57 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 25/WITH GOLD UP $46.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 24/WITH GOLD UP $16.95 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.86 TONNES

NOV 21/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.00 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1039.43 TONNES

NOV 20/WITH GOLD DOWN $20.45 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 19/WITH GOLD UP $14.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 18/WITH GOLD DOWN $6.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 17/WITH GOLD DOWN $20.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.93 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1044.000 TONNES

NOV 14/WITH GOLD DOWN $97.55TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1048.93 TONNES

NOV 13/WITH GOLD DOWN $17.80.TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1064.64 TONNES

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT XXX TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

GLD INVENTORY: 1051.69 TONNES, TONIGHTS TOTAL

SILVER

DEC 16/WITH SILVER DOWN $.07/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 56.360 MILLION OZ //

DEC 15/WITH SILVER UP $1.62/SMALL CHANGES IN SILVER AT THE SLV: A SMALL DEPOSIT OF 635,000 INTO THE SLV. ./ :INVENTORY RESTS AT 517.720 MILLION OZ //

DEC 12/WITH SILVER DOWN $2.30/NO CHANGES IN SILVER AT THE SLV: ./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 11/WITH SILVER UP $3.52/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.537 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 9/WITH SILVER UP $2.41/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.179 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 510.828 MILLION OZ //

DEC 8/WITH SILVER DOWN $0.48/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 5.497 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 512.007 MILLION OZ //

DEC 5/WITH SILVER UP 0.39/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.083 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.448 MILLION OZ //

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

DEC 3/WITH SILVER UP $0.23/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 1.956 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 510.012 MILLION OZ //

DEC 2/WITH SILVER DOWN $0.65 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND FRAUDLUENT PAPER DEPOSIT OF 6.167 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 508.057 MILLION OZ //

DEC 1/WITH SILVER UP $2.21 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 907,000 OZ INTO THE SLV./ :INVENTORY RESTS AT 501.890 MILLION OZ //

NOV28/WITH SILVER UP $3.28 TODAY/NO CHANGES IN SILVER AT THE SLV:/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV26/WITH SILVER UP $1.86 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 2.267 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV25/WITH SILVER UP $0.69 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 8.163 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 498.716 MILLION OZ //THIS IS A FRAUDULENT TRANSACTION

NOV24/WITH SILVER UP $0.43 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 277,000, OZ OUT OF THE SLV/ :INVENTORY RESTS AT 490.553 MILLION OZ MILLION OZ

NOV21/WITH SILVER DOWN $0.53 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 635,000 OZ INTO THE SLV/ :INVENTORY RESTS AT 490.190 MILLION OZ MILLION OZ

NOV20/WITH SILVER DOWN $0.53 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.555 MILLION OZ MILLION OZ

NOV 19/WITH SILVER UP $0.36 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 18/WITH SILVER DOWN $0.13 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489..283 MILLION OZ MILLION OZ

NOV 17/WITH SILVER DOWN $0.07 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.451 MILLION OZ INTO THE SLV:INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 14/WITH SILVER DOWN $2.08 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.722 MILLION OZ INTO THE SLV:

INVENTORY RESTS AT 487.832 MILLION OZ MILLION OZ

NOV 13/WITH SILVER DOWN $0.58 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

CLOSING INVENTORY 516.360

MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD….

3. CHRIS POWELL AND HIS GATA DISPATCHES:

CHINA buying evering in sight: this is major. They need the gold for their currency

Submitted by admin on Mon, 2025-12-15 20:41 Section: Daily Dispatches

From Bloomberg News Sunday, December 14, 2025

CMOC Group, one of China’s biggest miners, extended its push into precious metals with a $1 billion deal to buy the Brazilian operations of Equinox Gold Corp.

It will take full ownership of two Equinox entities — Leagold LatAm Holdings BV and Luna Gold Corp. — that control several mines or deposits in the South American nation. Equinox will receive $900 million in cash, plus a contingent payment of as much $115 million one year after the deal closes, CMOC said in an exchange filing

The Chinese firm is one of the fastest-growing miners, passing Glencore Plc as the biggest cobalt producer in 2023 and having major copper operations. It has been posting strong profits off the back of high prices for the industrial metal and said earlier this year it would focus on M&A in copper, gold, and minor metals. …

But the more important point isn’t the price level—it’s where we are in the metals liquidity stack.

Gold ran first. Silver followed. And historically, when capital starts chasing precious metals with momentum, it doesn’t stop at the deepest, most liquid markets.

It moves down the ladder.

The liquidity problem (and opportunity)

Gold and silver are enormous markets. They can absorb a lot of capital before price action becomes disorderly.

Platinum cannot.

It’s thinner, less liquid, and far more prone to gap-style moves when demand shows up in size. That’s not a bug—it’s the feature.

As David Janello, PhD, CFA put it in a piece we referenced back in October:

“What happens when the same demand hits markets with 1% of the liquidity of Silver and less than 1/10,000th the liquidity of Gold?”

His answer was blunt: the move can be violent.

Most traders have spent their careers in orderly markets, where price moves in steps. Thin markets don’t behave that way. They reprice, sometimes all at once.

Why this matters now

The backdrop today looks eerily familiar to prior precious-metal inflection points:

A macro bid under the metals complex

Breadth widening beyond just gold

Growing attention on assets that don’t require much incremental capital to move sharply

Once attention rotates into thinner markets, price doesn’t politely climb—it jumps.

That’s why, back in October, we explicitly framed precious metals exposure as tail-risk by design, not as a conservative allocation.

How we think about expressing this theme

When markets like platinum start to move, timing matters—but structure matters more.

Our approach (which we laid out previously) follows a simple philosophy:

Uncapped upside for the tail

Defined downside so we can afford to wait

Pre-wired exits so we’re not forced to babysit positions

In thin markets, you don’t want to be perfectly right and structurally wrong. You want a setup that can survive noise while keeping the upside open if things get disorderly.

That’s why our precious-metals playbook has emphasized:

Leaving the top open

Financing that exposure with a small, defined risk floor

Avoiding structures that cap gains just as things get interesting

We’re not trying to predict the exact path—only to be positioned if the move accelerates.

The setup is changing

Platinum at a 14-year high isn’t the end of the story. Historically, it’s often been the beginning of attention.

If capital keeps migrating down the liquidity ladder, this is exactly the kind of market where moves can happen faster—and more violently—than most participants expect.

Gold showed what happens when demand overwhelms supply. Silver reminded traders what leverage to liquidity looks like.

Platinum may be next. Subscribers can see exactly how we’re positioned for platinum exploding higher here.

A bullish options trade on a much less liquid precious metal that might go parabolic.

If you’d like a heads up when we place our next precious metals trade, you can subscribe to The Portfolio Armor Substack below.

END

SILVER:

LEASE RATES FOR SILVER: REMAIN ELEVATED AT 6.5% TO 7//AI

this is huge!! lease rates are generally for 3 months and used by the bankers to supply silver

to the longs for delivery purposes. Rarely do you see lease rates remain elevated for longer than a month because the lessor is still short this silver and must pay it back. This creates massive stress in the silver market.

Robert Lambourne

5:54 AM (2 hours ago)

to me

Thanks Harvey.

I’ve just seen something that says silver lease rates in London have shot up since last week and are supposedly remaining high – 3 month rates are >200 basis points over USD rates at c6.5%/7% annualised.

Presumably that is a sign of tight physical supply. So it seems a tough ask to push prices down unless more physical appears.

Thanks as ever for your commentary.

Bob

END

SPECIAL THANKS TO ROBERT LAMBOURNE TO GOT THIS FOR US;

SILVER

Silver Price Forecast: Top Trends for Silver in 2026

The silver price reached heights not seen in more than 40 years in 2025, posting new all-time highs in the fourth quarter amid a supply deficit, expanding industrial use and rising safe-haven demand.

The white metal reached its highest point for the year in mid-December, breaking through US$64 per ounce following an interest rate cut from the US Federal Reserve. With investors looking for non-interest bearing assets in which to store and grow their wealth, the world’s metals exchanges are having a hard time keeping their silver inventories stocked.

What will 2026 hold for silver? As the new year approaches, investors are closely watching how changes in monetary policy and global uncertainty could impact the precious metal, along with supply and demand trends in the space.

Here’s what experts see coming for silver in 2026.

Silver’s persistent structural supply deficit

Silver’s “relentless” move from under US$30 in January to over US$60 by December of this year speaks to the tightness in the market, Peter Krauth of Silver Stock Investor and Silver Advisor told the Investing News Network (INN) in a December interview. He expects that key thread to continue running through the silver story into 2026.

In its “2025/2026 Precious Metals Investment” report, Metal Focus forecasts a fifth straight year of a silver supply deficit for 2025, coming in at 63.4 million ounces. And while that figure is expected to retract to 30.5 million ounces in 2026, the firm is confident that the deficit will continue to be a factor for silver this coming year.

Essentially, silver is in an entrenched structural deficit tied to a multi-year mine supply shortfall that can’t keep up with both rising industrial use and strong investment demand. Aboveground silver stocks are running dry, with silver mine production has decreased over the past decade, especially in the silver-mining hubs of Central and South America.

Even with silver at never-seen-before prices, it could be years before any sort of balance returns to the market.

Krauth told INN that higher silver prices are not enough of a motivation for miners to increase production, because about 75 percent of silver is mined as a by-product of other metals such as gold, copper, lead and zinc.

“If the silver that you produce is a small portion of your stream of revenues, you’re not that motivated to try to produce more silver,” he explained. In fact, Krauth said a higher silver price could result in less silver coming to market as miners switch to processing lower-grade material that was once uneconomical and might even contain less silver.

On the exploration side, it takes 10 to 15 years to bring a silver deposit through discovery and into production.

“The reaction time to higher prices is actually really, really slow. I think we’re going to see these shortages and tightness persist,” Krauth added.

Industrial demand for silver from cleantech and AI

Industrial demand was another major catalyst for higher silver prices in 2025, and is expected to remain a strong tailwind for the silver market next year and beyond.

In a December report titled “Silver, the Next Generation Metal,” the Silver Institute explains that heavy demand for silver through 2030 is coming from the cleantech sector — mainly from the solar and electric vehicle (EV) segments — and emerging technologies such as artificial intelligence (AI) and data centers. Silver’s critical role in these economically important industries led the US government to include silver on its list of critical minerals this year.