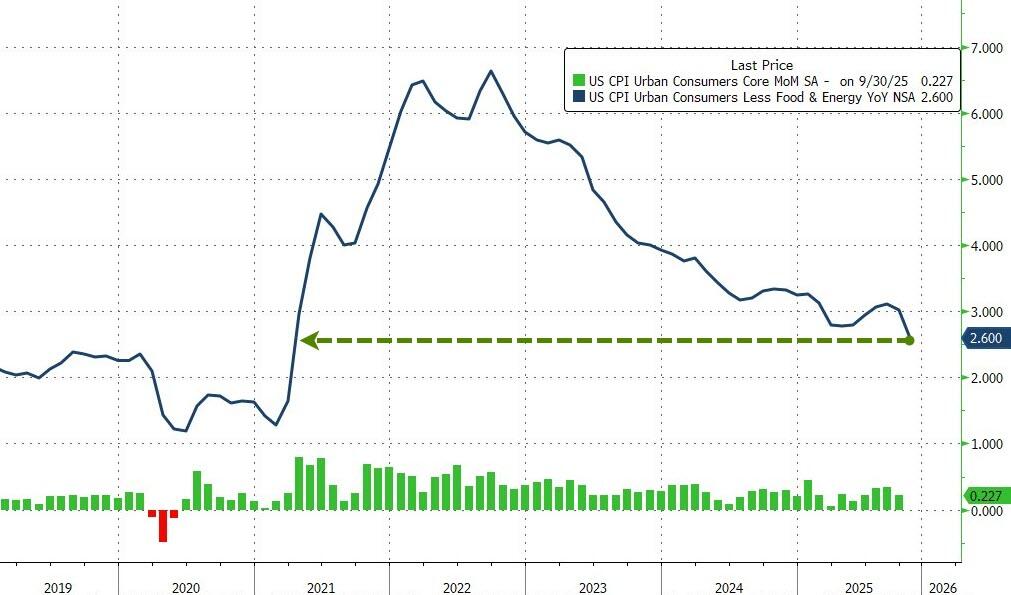

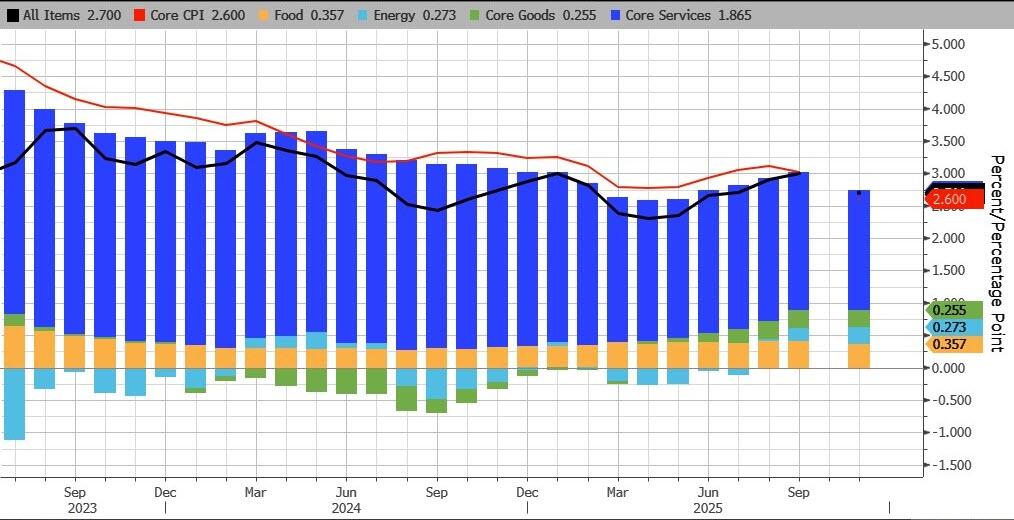

DEC 18/GOLD CLOSED DOWN $9.05 TO $4341.25 WHILE SILVER ALSO FELL BY $1.13 DOWN TO $65.26/PLATINUM WAS UP $25.35 TO $1921.95 AT A 15 YR HIGH// PALLADIUM CONTINUES ON A TEAR RISING $60.95 TO $1700.85 A TWO YEAR HIGH////GOLD COMMENTARY TONIGHT COURTESY OF ALASDAIR MACLEOD//COMMODITY COMMENTARY TONIGHT ON SILVER AND COPPER//IN DEPTH LOOK AT SPAIN AND HOW THE MIGRANTS DECIMATED THEIR ECONOMY//ISRAEL VS HAMAS UPDATES/ISRAEL TBN// MORE FALLOUT FROM THE BONDI/AUSTRALIA MASSACRE//COVID INJURY REPORT: MARK CRISPIN MILLER/DR PAUL ALEXANDER//VENEZUELA UPDATES/USA DATA RELEASES; JOBLESS CLAIMS AND THE CPI WHICH CAME IN QUITE TAME//SWAMP STORIES FOR YOU TONIGHT//

099 H DEUTSCHE BANK AG 1 118 C MACQUARIE FUTURES US 80 118 H MACQUARIE FUTURES US 116 132 C SG AMERICAS 7 332 H STANDARD CHARTERED B 31 435 H SCOTIA CAPITAL (USA) 18 657 C MORGAN STANLEY 50 46 657 H MORGAN STANLEY 533 661 C JP MORGAN SECURITIES 87 1107 709 C BARCLAYS 580 880 C CITIGROUP 70 880 H CITIGROUP 1000 905 C ADM 72

TOTAL: 1,899 1,899 MONTH TO DATE: 33,655

JPMORGAN STOPPED 590/1899

DECEMBER

GOLD: NUMBER OF NOTICES FILED FOR DEC/2025: 1899 CONTRACTs NOTICES FOR 189,900 OZ or 5.9066 TONNES

total notices so far: 33,655 contracts for 3,365,500 OR 104.682 tonnes)

FOR DEC

XXXXXXXXXXXXXXXXXX

SILVER NOTICES:254 NOTICE(S) FILED FOR 1.220 MILLION OZ/

total number of notices filed so far this month : 12,374 CONTRACTS (NOTICES) for 61.870 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $9.05 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .850 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 1052.54 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $1.13 AT THE SLV:

NO CHANGES IN SILVER INVENTORY AT THE SLV:/ //

OUT OF THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 515.000. MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 1567 CONTRACTS TO 154,478 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR MAMMOTH $2.93 GAIN IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S // TRADING. I BELIEVE THAT THIS GAIN OF $2.93 IS THE HIGHEST GAIN IN COMEX HISTORY. THE LONG SPECULATORS ARE STILL QUITE RELENTLESS AS THEY POUR INTO THE OPEN INTEREST AT THE COMEX AS YOU WILL WITNESS WITH TODAY’S TRADING. THE FRBNY CONTINUES TO SUPPLY THE NECESSARY PAPER AS THEY TRY TO DRIVE THE PRICE SOUTHBOUND WITH THE HELP OF HIGH FREQUENCY TRADERS AND T.A.S. SPREADERS BUT WITH A NO SUCCESS ON WEDNESDAY. THEN EARLY MONDAY MORNING WE RECEIVED NOTICE OF OUR FIRST HUGE 170 CONTRACT EXCHANGE FOR RISK AND THEN TO TOP OFF YESTERDAY’S DATA WE RECEIVED NOTICE OF A SECOND EXCHANGE FOR RISK OF 97 CONTRACTS FOR .485 MILLION OZ AND NOW I HAVE A LITTLE DOUBT OF THE RECIPIENT OF THIS ISSUANCE. THE CENTRAL BANK OF INDIA IS THE LOGICAL CHOICE BUT COULD IT BE THE CENTRAL BANK OF CHINA? THE TOTAL IN OZ FOR THIS EXCHANGE FOR RISK ON TWO OCCASIONS IS 1.335 MILLION OZ AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE TO GIVE US THE EXACT AMOUNT OF SILVER STANDING FOR DECEMBER.

WE HAVE REVERTED BACK TO NORMAL WITH THE SPECS NOW GOING ON THE LONG SIDE AND THE BANKER (FRBNY) ON THE SHORT SIDE AND PROVIDING THE NECESSARY SHORT PAPER. IT IS OUR SILVER SPECULATORS THAT WERE PILING INTO THE SILVER COMEX. WE FINALLY ARE MOVING TO A MUCH HIGHER BASE SURPASSING THE $34.40 SILVER PRICE BARRIER TO A HIGH DEGREE, AND NOW SURPASSING SURPASS OUR LAST MAJOR HURDLE OF $50.00 SILVER AGAIN. WE HAD A HUMONGOUS SIZED GAIN OF 1647 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL SIZED 110 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY TRADING WITH OUR HUGE GAIN IN PRICE /// THEY DESPERATELY AGAIN TODAY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $50.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON WEDNESDAY WITH SILVER’S GAIN IN PRICE AS THE SPECS PILED INTO THE SILVER ARENA. . THE PRICE FINISHED HUGELY ABOVE THE MAGIC NUMBER OF $50.00 SILVER SPOT PRICE CLOSING AT $66.39 UP $2.93 . WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS AT A STRONG SIZED 1603 T.A.S. CONTRACTS (BUT STILL DOWN FROM THE MEGA MEGA HUGE SIZED 5,000 PLUS CONTRACT ISSUANCE DURING NOVEMBER)!!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING AGAIN THE 50.00 DOLLAR MARK!!. THERE IS NO NEXT LINE IN THE SAND ONCE THE 50.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A SMALL SIZED 110 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUMONGOUS SIZED 1603 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//RAID AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE HAD A HUMONGOUS SIZED GAIN OF 1647 CONTRACTS ON OUR TWO EXCHANGES WITH OUR HUGE GAIN IN PRICE OF $2.93. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION AND NO DOUBT REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE SPECULATOR LONGS REMAIN STOIC EVEN ON PRICE FALLS. EASTERN CENTRAL BANKER WENT TO THE LONG SIDE. THEY WILL TENDER FOR THE BADLY NEEDED PHYSICAL SILVER. THUS ON A NET BASIS WE LOST NO SPECULATORS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT//THURSDAY MORNING: A HUMONGOUS SIZED 1603 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR DEC: 49.33 MILLION OZ FOLLOWED BY TODAY’S 795,000 OZ QUEUE JUMP _ PLUS ..850 MILLION OZ EXCHANGE FOR RISK MONDAY AND TUESDAY’S .485 MILLION OZ/ (TOTAL EX. FOR RISK = 1.335 MILLION OZ)///STANDING ADVANCES TO 63.790 MILLION OZ//

WE HAD:

/ HUMONGOUS SIZED COMEX OI GAIN+// A SMALL 110 EFP ISSUANCE CONTRACTS (/ VI) A HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE 1603 CONTRACTS)/VII: DECEMBER ISSUED ITS FIRST EXCHANGE FOR RISK OF 0.850 MILLION OZ MONDAY AND TUESDAY ANOTHER ONE WAS ISSUED FOR 97 CONTRACTS OR .485 MILLION OZ!! TOTAL EXCHANGE FOR RISK DEC: 1.335 MILLION OZ

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 835 CONTRACTS!!!!! T

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC.. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC.

TOTAL CONTRACTS for 15 DAY(S), total 6414 contracts: OR 32.070 MILLION OZ (427 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 32.070 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 32.070 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1567 CONTRACTS WITH OUR HUGE GAIN IN PRICE OF $2.93 IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. . THE CME NOTIFIED US THAT WE HAD A SMALL SIZED CONTRACT EFP ISSUANCE : 110 ISSUED FOR MARCH, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 9 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER HUGE 795,000 OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + YESTERDAY’S 495,000 OZ EXCHANGE FOR RISK // STANDING ADVANCES TO 63.790 MILLION OZ//

THE NEW TAS ISSUANCE TUESDAY NIGHT (1603) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!!

WE HAD 254 NOTICE(S) FILED TODAY FOR 1.220 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON A MASSIVE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 7095 OI CONTRACTS UP TO 478,188 OI AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A RELATIVELY LOWISH OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE AND CRIMINAL 1356 CONTRACTS // MEGA HUGE GOVERNMENT REMOVALS//

WE HAD A STRONG GAIN IN COMEX OI (7095 CONTRACTS) . THIS OCCURRED DESPITE OUR GAIN OF $39.45 IN PRICE// WEDNESDAY///.

LAST 8 MONTHS OF GOLD DELIVERIES: (MAY THROUGH TO NOVEMBER/DECEMBER)

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 6.3608 TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 23.322 TONNES//NEW STANDING ADVANCES TO 107.073 TONNES/

E.F.P. ISSUANCE/FOR OPENING DECEMBER GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 4592 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 478,188 AND WE NOW WITNESSING A NOW BIGGER COMEX OI BUT WITH AN EXTREMELY HIGH PRICE OF GOLD.//NOW EASIER TO FLEECE SPECS.

SILVER ALSO HAS A SMALL SIZED COMEX OI OF 154,313 CONTRACTS//BUT STILL DIFFICULT TO FLEECE SPEC LONGS. AND YET THIS SMALLISH OI IN COMEX IS ACCOMPANIED BY A HUGE GAIN IN PRICE IN SILVER!!

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,687 CONTRACTS WITH 8451 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4592 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 11,687 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1392 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON.

GOLD PRICE ON TUESDAY ROSE BY $39.45

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(4592) ACCOMPANYING THE STRONG GAIN IN COMEX OI OF 7095 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 11,687 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND NEWBIE SPECULATORS GOING TO THE LONG SIDE AND POURING IT ON WITH RECKLASS ABANDON!! . ,2.) STRONG INITIAL STANDING FOR GOLD FOR DEC AT 83.813 TONNES OF NORMAL DELIVERY FOLLOWED BY OUR 6.3608 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPING OF 23.325 TONNES//NEW STANDING ADVANCES TO 107.073 TONNES

NEW STANDING ADVANCES TO 107.073 TONNES.

NEW STANDING FOR GOLD, DEC CONTRACT AT 107.073 TONNES OF GOLD

3) ZERO T.A.S. LIQUIDATION (BUT CONSIDERABLE GOVT LIQUIDATION // AND SMALL GAIN OF EQUITY SHARES/DEC 17) AS WE HAD 1)A $39.45 COMEX PRICE GAIN AND WE HAD 2) NEWBIE SPEC SHORTS GETTING LIQUIFIED AND ON A NET BASIS, THE SPECS GAINED HUGELY IN NUMBERS + EASTERN CENTRAL BANKERS WERE PILING INTO THE LONG SIDE AS WE HAD A HUGE SIZED GAIN OF 13,043 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A HUGE AMOUNT OF GOLD WILL STAND FOR DELIVERY IN DECEMBER (107.073 TONNES). //, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL WITH THE RISE IN PRICE YESTERDAY

4) STRONG SIZED COMEX OI GAIN/ 5) V) HUGE SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (4300) AND A FAIR T.A.S. ISSUANCE 1392 FOR RAID PURPOSES

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

TOTAL EFP CONTRACTS ISSUED: 42,542 CONTRACTS OR 4,254,200 OZ OR 132.32 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 2836 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN15 TRADING DAY(S) IN TONNES: 132.32 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 132.32 TONNES DIVIDED BY 3550 x 100% TONNES = 3.74% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 132.32 TONNES//VERY SMALL THIS MONTH.

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 1557 CONTRACTS OI TO 154,478 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 110 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 110 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1557 CONTRACTS AND ADD TO THE 110 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF 1647 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE GAIN OF $2.93 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.335 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ASIA RESULTS; THURSDAY DEC 17

SHANGHAI CLOSED UP 6.09 POINTS OR 0.16%

//Hang Seng CLOSED UP 5.72 PTS OR 0.02%

// Nikkei CLOSED DOWN 433.28 PTS OR 0.88% //Australia’s all ordinaries CLOSED UP 0.33%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.0417

/ OFFSHORE CLOSED UP AT 7.0358/ Oil UP TO 56.28 dollars per barrel for WTI and BRENT UP TO 60.10 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.0417 OFFSHORE YUAN TRADING UP TO 7.0358:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7095 CONTRACTS TO 478.188 OI WITH OUR GAIN IN PRICE OF $39.45 WITH RESPECT TO WEDNESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4592). WE HAD ZERO T.A.S. LIQUIDATION WEDNESDAY (WITH MONTH END SPREADER LIQUIDATIONS FINISHED ON NOV 30). . IT SEEMS THAT THE SPECULATORS WENT MASSIVELY HUGE TO THE LONG SIDE WITH OUR FRBNY PROVIDING STILL THE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE .

YOU WILL NOTICE THAT THE COMEX OI IS NOW GAINING FROM ITS LOW OI OF AROUND 418,000 TO NOW 478,188 AND NOW SOME OF THESE GUYS ARE NOT VERY STICKY AND THUS VULNERABLE TO A RAID.

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 11,687 CONTRACTS (OR 36.35 TONNES). THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR 0 OZ OR NIL TONNES OF GOLD. IF YOU NEED A HISTORY OF ALL EXCHANGE FOR RISK FOR GOLD, I HAVE ARCHIVED ALL MY COMMENTARIES AND YOU CAN VIEW IT AT ANY TIME.

DETAILS ON OUR NEW DECEMBER COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 11,687 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH DECEMBER/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR T.A.S ISSUANCE CONTRACTS. THE CME NOTIFIES US THAT THEY HAVE ISSUED 1392 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE HUGE NUMBER OF T.A.S. ISSUANCES IN EARLY DECEMBER.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 0.0 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 6.3608 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 23.325 TONNES//STANDING ADVANCES TO 107.073 TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 39+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 39 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 39 TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/DEC.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED EXCHANGE FOR PHYSICAL OF 4592 CONTRACTS.

THAT IS A HUGE SIZED 4592 EFP CONTRACT WAS ISSUED: : /FEB 4592 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4592 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 39 TONNES

WE HAD :

ZERO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE CONSIDERABLE GOVERNMENT LIQUIDATION

MONTH END SPREADERS HAVE NOW FINISHED

T.A.S.SPREADER ISSUANCE//DECEMBER

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT//THURSDAY MORNING WAS A FAIR SIZED 1392 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP WEDNESDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING GAIN OF COMEX OI AND A HUGE EXCHANGE FOR PHYSICAL ISSUANCE..ENOUGH FODDER FOR THE COMMENCEMENT OF A RAID WHICH WILL NOT HAPPEN TODAY AS SILVER ROSE HUGELY PULLING UP GOLD.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

GOLD STANDING AT THE COMEX FOR GOLD LAST 12 MONTHS OF 2025

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 6.3608 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 23.325 TONNES//NEW STANDING ADVANCES TO 107.073 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

AN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING DECEMBER,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $39.45/ /)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX// WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL TUESDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR DECEMBER. THE COMEX IS ONE BIG MESS!! THIS WEEK,

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 3 MONTHS:

STANDING FOR GOLD OCT THROUGH TO DECEMBER:

ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 2045 CONTRACT QUEUE JUMP FOR 204,500 OZ OR 6.3608 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 23.325 TONNES///STANDING ADVANCES TO 107.073 TONNES.

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $39.45

WE HAD A HUGE 1356 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .

NET GAIN ON THE TWO EXCHANGES : 11,687 CONTRACTS OR 1,168,700 OZ OR 36.35 TONNES

i))Into Brinks 4932.151 oz ii) Into Manfra: 22,473.549 oz (699 kilobars)

total deposit 27,405.700 oz

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

1899 notice(s) 189,900 OZ

5.9066 TONNES OF GOLD

No of oz to be served (notices)

769 contracts 76,900 OZ 2.3919 TONNES

Total monthly oz gold served (contracts) so far this month

33,655 notices 3,365,500 0z 104.682TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 1

i) Into the dealer Brinks 51,409.449 oz

(1599 kilobars)

total deposit: 51,409.449 oz

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

2 ENTRIES

i)Into Brinks 4932.151 oz

ii) Into Manfra: 22,473.549 oz (699 KILOBARS)

total deposit 27,405.700 oz

customer withdrawals:

0 ENTRIES

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 0//

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF DECEMBER STANDS AT 2668 CONTRACTS FOR A LOSS OF 602 CONTRACTS. WE HAD 2647 CONTRACTS FILED ON WEDNESDAY SO WE GAINED A WHOPPING 2045 CONTRACTS FOR A QUEUE JUMP OF 204,500 OZ OR 6.3608 TONNES TO WHICH WE ADD TO OUR PREVIOUS QUEUE JUMPS .THUS STANDING FOR GOLD IN DECEMBER INCREASES HUGELY TO 107.073 TONNES

JANUARY GAINED 187 CONTRACTS UP TO 3703

FEB GAINED 6132 CONTRACTS UP TO 346,701 CONTRACTS

We had 1899 contracts filed for today representing 189,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1899 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 580 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2025. contract month, we take the total number of notices filed so far for the month (33,655 ) to which we add the difference between the open interest for the front month of DEC ( 2668 CONTRACTS) minus the number of notices served upon today (1899 x 100 oz per contract) equals 3,442,400 OZ OR 107.073 Tonnes of gold

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (33,655 x 100 oz +we add the difference for front month of DEC (2668 OI} minus the number of notices served upon today (1899)x 100 oz) which equals 3,442,400 OR 108.073 TONNES

new total of gold standing in DECEMBER is 107.073 tonnes

TOTAL COMEX GOLD STANDING FOR DEC ..: 107.073 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF DECEMBER.

volume WEDNESDAY confirmed 232,327 fair

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,969,701.020 oz 61.26 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,070,160.045 oz

TOTAL REGISTERED GOLD 19,276,088.382 or 599.56 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,794,071.663 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,306387oz ((REG GOLD- PLEDGED GOLD)=

538.30 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

THE DEC. 2025 SILVER CONTRACTS

DEC 18 2025

INITIAL/

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1 entries

i) Out of JPMorgan: 987,379.380 oz totally removed from customer acct.

total withdrawal: 987,379.380 oz

Deposits to the Dealer Inventory

1 ENTRY

i) Into Stonex; 717,539.940 oz

total deposit 717,539.940 oz

Deposits to the Customer Inventory

1 entries

i) Into CNT 495,269.350 oz

total deposit: 495,269.350 oz

No of oz served today (contracts)

254 CONTRACT(S) ( 1.220 million OZ

No of oz to be served (notices)

117 contracts (0.585 MILLION oz)

Total monthly oz silver served (contracts)

12,374 Contracts (61.870 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

1 ENTRY

1 ENTRY

i) Into Stonex; 717,539.940 oz

total deposit 717,539.940 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

i) Into CNT 495,269.350 oz

total deposit: 495,269.350 oz

withdrawals: customer side/eligible

1 entries

1 entries

i) Out of JPMorgan: 987,379.380 oz totally removed from customer acct.

total withdrawal: 987,379.380 oz

adjustments: 4

i) dealer to customer acct Asahi 928,030.370 oz

ii) dealer to customer acct Stonex: 352,349.000 oz

iiiP customer to dealer Brinks 9783.400 oz

iv) customer to dealer CNT 332,349.00 oz

TOTAL REGISTERED SILVER: 130.324MILLION OZ//.TOTAL REG + ELIGIBLE. 453,176Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC.

silver open interest data:

FRONT MONTH OF DECEMBER /2025 OI: 371 OPEN INTEREST CONTRACTS FOR A LOSS OF 299 CONTRACTS. WE HAD 458 CONTRACTS FILED ON WEDNESDAY SO WE ACTUALLY HAD ANOTHER QUEUE JUMP OF 159 CONTRACTS OR 795,000 OZ

JANUARY GAINED 141 CONTRACTS UP TO 4167 CONTRACTS AS JANUARY BECOMES THE FRONT MONTH

FEB LOST 19 CONTRACTS DOWN TO 1353 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 254 or 1.220 MILLION oz

CONFIRMED volume; ON WEDNESDAY 161,536 huge//

AND NOW DECEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 12,374 X5,000 oz = 61.870 MILLION oz

to which we add the difference between the open interest for the front month of DEC (371) AND the number of notices served upon today (384 )x (5000 oz)

Thus the standings for silver for the DECEMBER 2025 contract month: (12,374) Notices served so far) x 5000 oz + OI for the front month of DEC(371) minus number of notices served upon today (254)x 5000 oz equals silver standing for the DEC.contract month equating to 62.455 MILLION OZ + 850 MILLION OZ FOR DEC ‘S FIRST EXCHANGE FOR RISK AND THEN TODAY’S SECOND EXCHANGE FOR RISK OF .485 MILLION OZ//NEW TOTAL EXCHANGE FOR RISK; 1.335 MILLION OZ: THUS WE HAVE THE FOLLOWING:

NORMAL STANDING: 62.455 MILLION OZ

PLUS 1.335 MILLION OZ EXCHANGE FOR RISK/2 OCCASIONS

New total standing: 63.790 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 130.324. million oz of registered silver

JPMorgan as a percentage of total silver: 190.780/453.176million. 42.10%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

DEC 18/WITH GOLD DOWN $9.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .85 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 17/WITH GOLD UP $39.45 TODAY/NO CHANGES IN GOLD AT THE GLD:// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 16/WITH GOLD DOWN $3.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 15/WITH GOLD UP $10.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 105.12 TONNES

DEC 12/WITH GOLD UP $14.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.83 TONNES

DEC 11/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 10/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 9/WITH GOLD UP $18.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.14 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1049.11 TONNES

DEC 8/WITH GOLD DOWN $23.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.33 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1050.25 TONNES

DEC 5/WITH GOLD UP $9.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 4.00 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.58 TONNES

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

DEC 3/WITH GOLD UP $14.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1048.30 TONNES

DEC 2/WITH GOLD DOWN $53.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.58 TONNES OF GOLD VAPOUR INTO THE GLD// /// ///INVENTORY RESTS AT 1050.01TONNES

DEC 1/WITH GOLD UP $22.75 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43TONNES

NOV 28/WITH GOLD UP $51.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43 TONNES

NOV 26/WITH GOLD UP $25.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT PAPER DEPOSIT OF 4.57 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 25/WITH GOLD UP $46.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 24/WITH GOLD UP $16.95 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.86 TONNES

NOV 21/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.00 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1039.43 TONNES

NOV 20/WITH GOLD DOWN $20.45 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 19/WITH GOLD UP $14.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 18/WITH GOLD DOWN $6.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 17/WITH GOLD DOWN $20.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.93 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1044.000 TONNES

NOV 14/WITH GOLD DOWN $97.55TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1048.93 TONNES

NOV 13/WITH GOLD DOWN $17.80.TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1064.64 TONNES

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT XXX TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

GLD INVENTORY: 1052.50 TONNES, TONIGHTS TOTAL

SILVER

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 17/WITH SILVER UP $2.93/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 16/WITH SILVER DOWN $.07/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 56.360 MILLION OZ //

DEC 15/WITH SILVER UP $1.62/SMALL CHANGES IN SILVER AT THE SLV: A SMALL DEPOSIT OF 635,000 INTO THE SLV. ./ :INVENTORY RESTS AT 517.720 MILLION OZ //

DEC 12/WITH SILVER DOWN $2.30/NO CHANGES IN SILVER AT THE SLV: ./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 11/WITH SILVER UP $3.52/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.537 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 9/WITH SILVER UP $2.41/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.179 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 510.828 MILLION OZ //

DEC 8/WITH SILVER DOWN $0.48/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 5.497 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 512.007 MILLION OZ //

DEC 5/WITH SILVER UP 0.39/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.083 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.448 MILLION OZ //

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

DEC 3/WITH SILVER UP $0.23/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 1.956 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 510.012 MILLION OZ //

DEC 2/WITH SILVER DOWN $0.65 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND FRAUDLUENT PAPER DEPOSIT OF 6.167 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 508.057 MILLION OZ //

DEC 1/WITH SILVER UP $2.21 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 907,000 OZ INTO THE SLV./ :INVENTORY RESTS AT 501.890 MILLION OZ //

NOV28/WITH SILVER UP $3.28 TODAY/NO CHANGES IN SILVER AT THE SLV:/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV26/WITH SILVER UP $1.86 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 2.267 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV25/WITH SILVER UP $0.69 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 8.163 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 498.716 MILLION OZ //THIS IS A FRAUDULENT TRANSACTION

NOV24/WITH SILVER UP $0.43 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 277,000, OZ OUT OF THE SLV/ :INVENTORY RESTS AT 490.553 MILLION OZ MILLION OZ

NOV21/WITH SILVER DOWN $0.53 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 635,000 OZ INTO THE SLV/ :INVENTORY RESTS AT 490.190 MILLION OZ MILLION OZ

NOV20/WITH SILVER DOWN $0.53 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.555 MILLION OZ MILLION OZ

NOV 19/WITH SILVER UP $0.36 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 18/WITH SILVER DOWN $0.13 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489..283 MILLION OZ MILLION OZ

NOV 17/WITH SILVER DOWN $0.07 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.451 MILLION OZ INTO THE SLV:INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 14/WITH SILVER DOWN $2.08 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.722 MILLION OZ INTO THE SLV:

INVENTORY RESTS AT 487.832 MILLION OZ MILLION OZ

NOV 13/WITH SILVER DOWN $0.58 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

The Romans created the system of money and credit upon which our laws today are based. This article charts the history of gold in common law and why it is still relevant.

It is a mistake to underestimate modern disinformation and ignorance on the topics of money and credit. It will seem extraordinary to those not versed in finance that even economists of the various schools of thought with their PhDs are utterly clueless on this vital topic, an ignorance which extends even into staff economists at central banks. Few of them understand the role of commercial banks in creating bank credit, assuming that either they are simply agents deploying deposits into loans, or that they operate on a fractional reserve system. Neither is true.

This article is not here to debate modern banking, but to describe the evolution of money and credit throughout history, and how they came to be defined in every nation’s common law. It started with the Romans. The first system of Roman law was the Twelve Tables of 448 BC, which established methodical habits of business.

The legal distinctions of money and credit

What interests us in this topic is the system of recording transactions, which following the Twelve Tables were divided into two classes, res mancipi, and res nec mancipi. The former refered to a small list of physical property transferred by a formal ceremony of mancipation, or transfer: bronze-copper ingots (the physical form of money at that time), lands and houses on Roman soil, beasts of burden, slaves, agricultural rights, and other rights over land were res mancipi. By this definition only a bronze-copper ingot weighing a Roman pound, the aes, was corporeal money and the final payment for discharging debt obligations. It was conveyed formally in the presence of five witnesses of full age and the aes would be weighed on scales in front of the witnesses and handed to the seller in payment.

Everything else were termed res nec mancipi, including incorporeal debt obligations, which were always entered in to be finally settled in aes in due course. The relationship between money and credit, always the other side of a debt obligation being the future final payment, was thereby defined in Roman law.

At the time of the Twelve Tables very few Romans were literate, agriculture dominated, and settlement practices reflected this. The strict formalities of a property transfer in res mancipi were abolished by Emperor Leo in 469AD, reflecting the economic and social advances in the eight centuries since the Twelve Tables. Other forms of money, principally the silver denarius and gold aureus coins entered into use during that time, replacing the earlier aes. The distinction between items confined to res mancipi and res nec mancipi was finally abolished in Justinian’s Pandects in 520AD. But reflecting the rulings of jurors Ulpian and Paulus in the second and third centuries AD the relationship between money and credit was crystalised in their original relationship.

Out of the Roman Empire evolved the colonising nations whose common laws were based on Justinian’s Pandects and the later Basilica translation of them in Greek (AD892). Following the fifteenth and sixteenth centurys’ global discoveries by Spain and Portugal, their colonies and those of the colonising nations that followed them all adopted Justinian’s legal distinction between money and credit in their common laws. Spain’s discoveries in the New World brought gold and silver into greater circulation, as did Britain’s guinea from West African gold introduced in 1663.

Following independence, the USA adopted UK common law through Blackstone’s Commentaries on the Laws of England, including the inherited relationship between money and credit crystalised in Justinian’s Pandects. And when in evidence to Congress in 1912, John Pierpont Morgan the greatest banker at that time said that “Credit is evidence of banking but it is not the money itself. Money is gold, and nothing else”, he was stating correctly the legal position defined in common law from Roman times.

Credit today

As well as defining the difference between money and credit in law, the Romans invented banking. Sweden invented central banking, which was closely followed by the establishment of the Bank of England. Central banks have the mandate to act for their governments and to issue currency. Currency is a debt of its issuer to discharge that obligation for money on demand and is clearly credit. And so long as that promise is adhered to, a currency as well as deposits held at the issuing bank have their value tied to that of gold.

This is why to this day banknotes issued by the Bank of England bear the legend, “I promise to pay the bearer on demand the sum of [the face value of the note]” signed by the chief cashier. It requires the issuer to maintain sufficient stocks of gold in the form of coin or bullion to meet public demand for redemptions of currency and deposits. To suspend conversion of currency and deposits into gold is fraudulent in common law.

In the twentieth century, governments began to bend the law, starting with European combatants suspending convertibility of currencies into gold at the outbreak of the First World War. In 1933, America’s President Roosevelt transgressed common law by executive order commanding citizens to submit their gold and gold notes in return for dollars, which he then devalued by 40% the following year. The selective return to international convertibility under the Bretton Woods Agreement was in 1944, which was finally suspended in 1971. Since then, the US Treasury and its central bank embarked on a propaganda campaign to describe dollars as money in place of gold and for all other currencies to regard it as such for international settlements.

But the dollar is never money in common law. It is a broken promise to pay the bearer his right to final settlement in legal money.

For fifty-four years, the dollar has been a fiat currency, fiat meaning it owes its status to the laws of the country and not to a common law right for final settlement in gold. The consequence is that the dollar has lost purchasing power against gold so that its value in real money has declined since Bretton Woods was “suspended” to only 0.8% of one cent — so far.

Fiat currencies never survive

Fiat currencies come into existence because states require funds beyond what they can raise from their citizens through taxation. For a while, currency debasement succeeds without creating undue alarm in the public. But prices of goods begin to rise reflecting its dilution of value, usually wrongly attributed to other factors. Consequently, the state has to accelerate the rate of debasement to cover rising costs as their future liabilities come due. This is reflected in the widening gulf between money, which is gold, and its value expressed in depreciating currency. The chart below illustrates this:

Since the year 2000, the dollar has lost 93.4% of its value measured in gold (since the suspension of Bretton Woods that loss has been over 99% as noted above). Alarmingly, the rate of the dollar’s depreciation is accelerating, indicating that the end of its existence as a fiat currency is approaching. Yet, there appears to be very little recognition of this fact in the Federal Government, its central bank, and worryingly among all those economics PhDs in state institutions and universities.

It is already too late to stop the end of the fiat dollar, which can only be achieved by taking the necessary steps to halt its debasement and reinstate the promise to tie all credit to final settlement in gold. But the monetary establishment is so committed to not tying the value of the dollar to gold and so ignorant of the universal common law setting out the relationship between money and credit that the implementation of the necessary stabilisation policies is inconceivable.

Unless, in the highly unlikely event that there is a Damascene conversion in the political class which can be sold to the electorate, we must assume that the dollar will never be a gold substitute and is doomed to lose all its purchasing power — and probably soon at that.

end

3. CHRIS POWELL AND HIS GATA DISPATCHES:

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 253

5. COMMODITY REPORT//SILVER

end

COPPER

Goldman Upgrades Copper Price Forecast Weeks After Warning About “Circular Melt-Up”

Goldman Sachs recently upgraded its 2026 copper price forecast just weeks after cautioning about a speculative “circular melt-up” in the market.In early December 2025, Goldman analysts described the rapid copper price surge as a “circular melt-up,” driven by self-reinforcing dynamics: tightening LME inventories and backwardation encouraging US stockpiling ahead of potential tariffs, which further squeezes ex-US supply and pushes prices higher in a feedback loop.However, on December 15, 2025, Goldman raised its average 2026 copper price forecast to $11,400 per metric ton (from $10,650 previously). This upgrade reflects lowered odds of near-term US refined copper tariffs in the first half of 2026, due to concerns over affordability and inflation. A delayed tariff (likely announced in H1 2026 but implemented in 2027) would prolong US hoarding, exacerbating supply tightness outside the US and supporting higher prices in 2026.Goldman kept its 2027 forecast unchanged at $10,750 per ton, expecting prices to retreat once tariffs take effect and global markets rebalance into surplus.As of mid-December 2025, copper prices have pulled back slightly from record highs above $11,950/ton but remain elevated around $11,700/ton (or roughly $5.30–$5.35/lb on COMEX), up over 33% year-to-date. The rally has been fueled by mine disruptions, AI/green energy demand optimism, and tariff-related trade flow distortions—despite Goldman viewing much of the move as speculative rather than fundamentally driven in the short term.Longer-term, Goldman remains structurally bullish, projecting prices rising toward $15,000/ton by 2035 (in nominal terms) due to electrification and infrastructure demand.

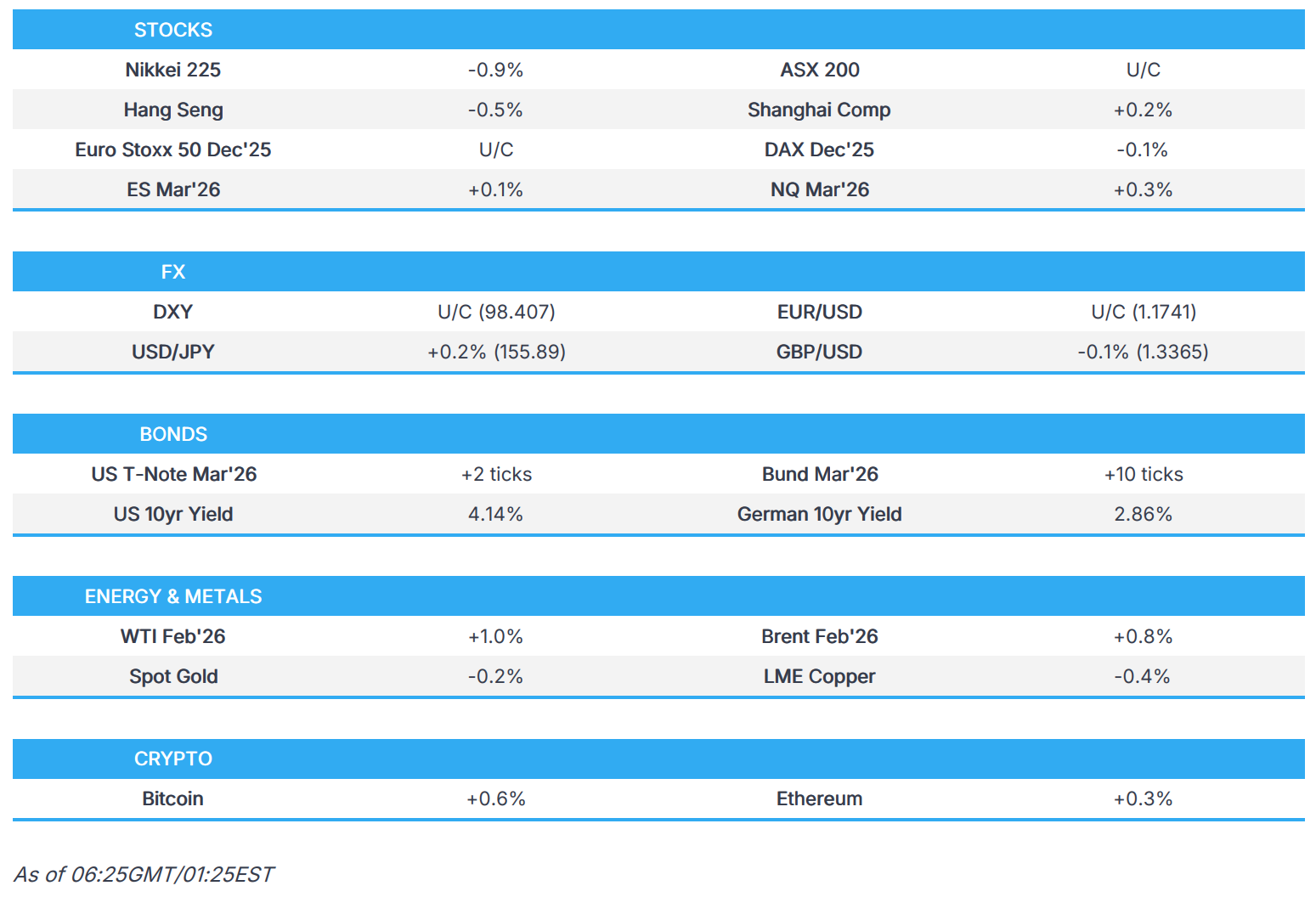

ASIA RESULTS; THURSDAY DEC 18

SHANGHAI CLOSED UP 6.09 POINTS OR 0.16%

//Hang Seng CLOSED UP 5.72 PTS OR 0.02%

// Nikkei CLOSED DOWN 433.28 PTS OR 0.88% //Australia’s all ordinaries CLOSED UP 0.33%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.0417

/ OFFSHORE CLOSED UP AT 7.0358/ Oil UP TO 56.28 dollars per barrel for WTI and BRENT UP TO 60.10 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.0417 OFFSHORE YUAN TRADING UP TO 7.0358:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.0417

OFFSHORE YUAN: UP TO 7.0358

HANG SENG CLOSED UP 5.72 PTS OR 0.02%

2. Nikkei closed DOWN 433.28 PTS OR 0.88%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 98.10 /// EURO FALLS TO 1.1730 DOWN 11 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.962 // DOWN 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.82…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.381 UP 3 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN/JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8457/ Italian 10 Yr bond yield DOWN to 3.502 SPAIN 10 YR BOND YIELD DOWN TO 3.275

3i Greek 10 year bond yield UP TO 3.451

3j Gold at $4327.50 Silver at: 66.04 1 am est) SILVER NEXT RESISTANCE LEVEL AT $54.00//AFTER 50.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 33/100 roubles/dollar; ROUBLE AT 80.38

3m oil (WTI) into the 56 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.50 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.982% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.351 UP 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7955 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9331 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.133 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.819 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.466 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.74 UP 2 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.4610 DOWN 1 PTS

30 YR UK BOND YIELD: 5.209 DOWN 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.436DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2,985 DOWN 0 BASIS PTS.

1a New York OPENING REPORT

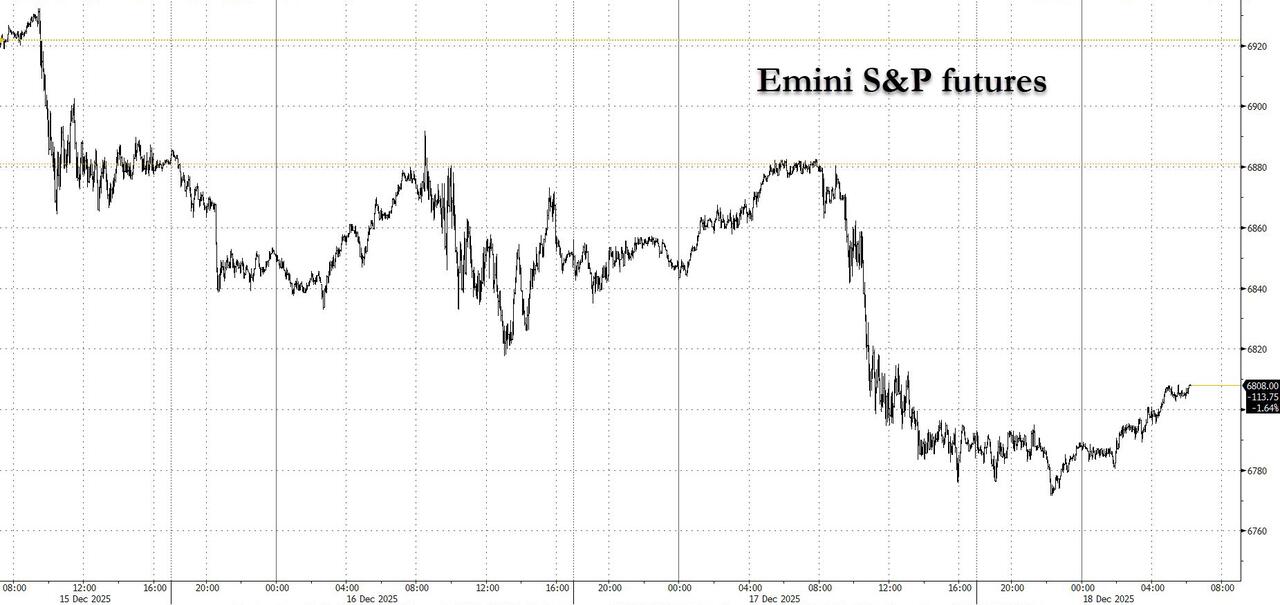

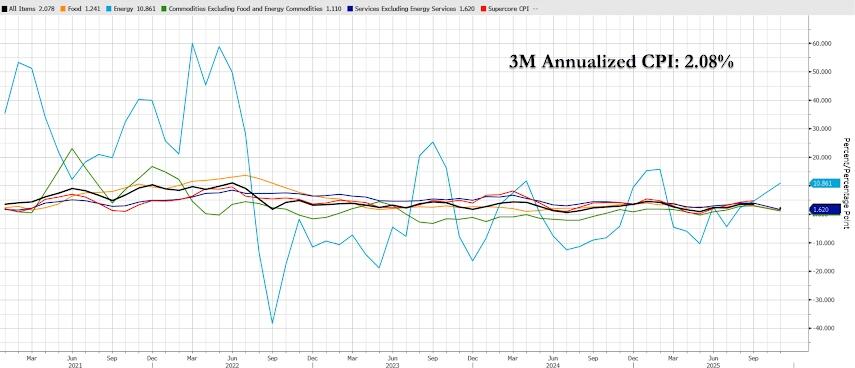

Futures Rise After 4-Days Of Declines Ahead Of CPI, Central Bank Bonanza

Thursday, Dec 18, 2025 – 06:58 AM

Stocks rebounded from Wednesday’s tech-led rout after an upbeat forecast from Micron helped put the brakes on a tech-driven selloff on a busy day for data and central bank meetings. As of 7:15am ET, S&P and Nasdaq futures rose 0.6% following four down days. In premarket trading, Micron shares soared 11% after reporting blowout earnings. Europe’s Stoxx 600 index rose 0.2%, while Asian shares slid. The tech slide, combined with dovish comments from a Federal Reserve official, helped boost Treasuries. The yield on the 10-year was down two basis points at 4.13% even as the BBG dollar index recovered from an earlier loss to trade 0.05% higher. Oil rose modestly to trade +0.4% at $56.18/barrel. Among key events for financial markets Thursday are the release of US inflation data for November, along with monetary policy decisions from the European Central Bank and Bank of England.

In premarket trading Mag 7 stocks are mostly higher (Tesla +1.4%, Nvidia +1.4%, Alphabet +1.1%, Amazon +0.8%, Meta +0.7%, Microsoft +0.7%, Apple -0.2%).

Insmed (INSM) falls 20% after the biotech said its Phase 2b BiRCh study of brensocatib in patients with chronic rhinosinusitis without nasal polyps failed to meet primary or secondary efficacy goals, prompting immediate discontinuation of the CRSsNP program.