access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: DECEMBER 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,361.400000000 USD

INTENT DATE: 12/19/2025 DELIVERY DATE: 12/23/2025

FIRM ORG FIRM NAME ISSUED STOPPED

118 H MACQUARIE FUTURES US 2

363 H WELLS FARGO SECURITI 429

435 H SCOTIA CAPITAL (USA) 1

661 C JP MORGAN SECURITIES 726 116

690 C ABN AMRO CLR USA LLC 4

709 C BARCLAYS 170

905 C ADM 2 6

TOTAL: 728 728

MONTH TO DATE: 35,30

JPMORGAN STOPPED 116/728

GOLD: NUMBER OF NOTICES FILED FOR DEC/2025: 728 CONTRACTs NOTICES FOR 72,800 OZ or 2.264 TONNES

total notices so far: 35,300 contracts for 3,530,000 OR 109.797 tonnes)

SILVER NOTICES:54 NOTICE(S) FILED FOR 0.270 MILLION OZ/

total number of notices filed so far this month : 12,548 CONTRACTS (NOTICES) for 62.740 million oz

INITIAL STANDING FOR DEC: 49.33 MILLION OZ FOLLOWED BY TODAY’S 355,000 OZ QUEUE JUMP _ PLUS ..850 MILLION OZ EXCHANGE FOR RISK MONDAY AND TUESDAY’S .485 MILLION OZ/ (TOTAL EX. FOR RISK = 1.335 MILLION OZ)///STANDING ADVANCES TO 64.605 MILLION OZ//

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 34.190 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER HUGE 375,000 OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + YESTERDAY’S 495,000 OZ EXCHANGE FOR RISK // STANDING ADVANCES TO 64.605 MILLION OZ//

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 2.889 TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 31.6678 TONNES//NEW STANDING ADVANCES TO 111.947 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR DECEMBER OF 1.244 TONNES/NEW STANDING ADVANCES TO 113.191 TONNES

NEW STANDING FOR GOLD, DEC CONTRACT AT 113.191 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 149.219 TONNES//FAIR SIZED THIS MONTH.

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 2217 CONTRACTS OI TO 158,126 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 424 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 424 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2217 CONTRACTS AND ADD TO THE 424 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF 2641 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE GAIN OF $2.06 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 13.205 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $2.06

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ASIA RESULTS; MONDAY DEC 22

SHANGHAI CLOSED UP 26.92 POINTS OR 0.69%

//Hang Seng CLOSED UP 111.24 PTS OR 0.43%

// Nikkei CLOSED UP 895.18 PTS OR 1.81% //Australia’s all ordinaries CLOSED UP 0.02%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.0328

/ OFFSHORE CLOSED UP AT 7.0318/ Oil UP TO 57.57 dollars per barrel for WTI and BRENT UP TO 61.58 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP TO 7.0328 OFFSHORE YUAN TRADING UP TO 7.0318:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 6,450 CONTRACTS TO 491,060 OI WITH OUR GAIN IN PRICE OF $22.20 WITH RESPECT TO FRIDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1372). WE HAD ZERO T.A.S. LIQUIDATION FRIDAY (WITH MONTH END SPREADER LIQUIDATIONS COMMENCING FRIDAY WITH SMALL REMOVALS). IT SEEMS THAT THE SPECULATORS WENT MASSIVELY HUGE TO THE LONG SIDE WITH OUR FRBNY PROVIDING STILL THE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE .

YOU WILL NOTICE THAT THE COMEX OI IS NOW GAINING FROM ITS LOW OI OF AROUND 418,000 TO NOW 491.060 AND NOW AMPLE ENOUGH FOR A RAID BY OUR BANKERS.

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 7822 CONTRACTS (OR 24.329 TONNES). THEN WE WERE NOTIFIED OF A 400 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR 40,000 OZ OR 1.244 TONNES OF GOLD. THIS IS DECEMBER’S FIRST ISSUANCE AND IT CAME LATE IN THE MONTH. WE HAVE 3 CHOICES NOW FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY.

HERE ARE THE CHOICES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 39 TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 1.249 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS..

DETAILS ON OUR NEW DECEMBER COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 7,822 CONTRACTS WTH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH DECEMBER/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR T.A.S ISSUANCE CONTRACTS. THE CME NOTIFIES US THAT THEY HAVE ISSUED 1118 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE HUGE NUMBER OF T.A.S. ISSUANCES IN EARLY DECEMBER.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 0.0 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 2.889 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 31.6678 TONNES//STANDING ADVANCES TO 111.947 TONNES TO WHICH WE ADD OUR FIRST ISSUANCE OF EXCHANGE FOR RISK OF 1.244 TONNES/NEW STANDING IS THUS: 113.191 TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 39+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 39 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. SO IT IS POSSIBLE THAT THE FED IS THE BUYER OF 1.244 TONNES OF EXCHANGE FOR RISK/DECEMBER!!

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 39 TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/DEC.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1372 CONTRACTS.

THAT IS A FAIR SIZED 1372 EFP CONTRACT WAS ISSUED: : /FEB 1372 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1372 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 39 TONNES

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE CONSIDERABLE GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW COMMENCED!…

T.A.S.SPREADER ISSUANCE//DECEMBER

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT//FRIDAY MORNING WAS A FAIR SIZED 1118 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP FRIDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING STRONG GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE..ENOUGH FODDER FOR THE COMMENCEMENT OF A RAID

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 2.889 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 31.6678 TONNES//NEW STANDING ADVANCES TO 111.947 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.244 TONNES//NEW STANDING THUS INCREASES TO 113.191 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING DECEMBER,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $22.20/ /)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION FRIDAY WITH MINOR MONTH END SPREADER LIQUIDATION// COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX// WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL THURSDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR DECEMBER. THE COMEX IS ONE BIG MESS!!

FRIDAY NIGHT//SATURDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL FRIDAY EVENING/ SATURDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 3 MONTHS:

STANDING FOR GOLD OCT THROUGH TO DECEMBER:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 929 CONTRACT QUEUE JUMP FOR 92,900 OZ OR 2.889 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 31.6678 TONNES///STANDING ADVANCES TO 111.947 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.244 TONNES/NEW STANDING ADVANCES TO 113.191 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $22.20

WE HAD A HUGE XXXX CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .

INITIAL GOLD COMEX

DEC 22

DEC CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 3 ENTRIES i) Out of HSBC 61,086.900oz (1900 kilobars) ii) Out of Loomis: 22,328.350 oz iii) Out of Manfra: 25,752.751 oz (801 kilobars) total withdrawal: 114,168.201 oz or 3.56 tonnes |

| Deposit to the Dealer Inventory in oz | 0- ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 728 notice(s) 72,800 OZ 2.264 TONNES OF GOLD |

| No of oz to be served (notices) | 691 contracts 69,100 OZ 2.1493 TONNES |

| Total monthly oz gold served (contracts) so far this month | 35,300 notices 3,530,000 0z 109.797TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

0 ENTRIES

customer withdrawals:

3 ENTRIES

i) Out of HSBC 61,086.900oz

(1900 kilobars)

ii) Out of Loomis: 22,328.350 oz

iii) Out of Manfra: 25,752.751 oz

(801 kilobars)

total withdrawal: 114,168.201 oz or 3.56 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 2// dealer to customer

a) Brinks: 32,118.849 oz (999 KILOBARS)

b) HSBC 59,704.407 oz (1858 kilobars)

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF DECEMBER STANDS AT 1419 CONTRACTS FOR A GAIN OF 12 CONTRACTS. WE HAD 917 CONTRACTS FILED ON FRIDAY SO WE GAINED A WHOPPING 929 CONTRACTS FOR A QUEUE JUMP OF 92,900 OZ OR 2.889 TONNES TO WHICH WE ADD TO OUR PREVIOUS QUEUE JUMPS AND THEN ADD OUR FIRST ISSUANCE OF EXCHANGE FOR RISK FOR 1.244 TONNES .THUS STANDING FOR GOLD IN DECEMBER INCREASES HUGELY TO 113.191 TONNES

JANUARY GAINED 146 CONTRACTS UP TO 3775 AS JANUARY BECOMES THE FRONT MONTH. WE WILL PROBABLY HAS A GOOD SIZED 8 TO 9 TONNES OF GOLD STANDING.

FEB GAINED 2643 CONTRACTS UP TO 353,735 CONTRACTS

We had 728 contracts filed for today representing 72,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 726 notices issued from their client or customer account. The total of all issuance by all participants equate to 728 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 116 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2025. contract month, we take the total number of notices filed so far for the month (35,300 ) to which we add the difference between the open interest for the front month of DEC ( 1419 CONTRACTS) minus the number of notices served upon today (728 x 100 oz per contract) equals 3,599,100 OZ OR 111.947 Tonnes of gold + 1.244 TONNES of exchange for risk issuance: new total standing advances to 113.191 tonnes!!

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (35,300 x 100 oz +we add the difference for front month of DEC (1419 OI} minus the number of notices served upon today (728)x 100 oz) which equals 3,599,100 OR 111.947 TONNES + 2.44 tonnes exchange for risk//new total standing advances to 113.947 tonnes

new total of gold standing in DECEMBER is 113.191 tonnes

TOTAL COMEX GOLD STANDING FOR DEC ..: 113.191 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF DECEMBER.

volume FRIDAY confirmed 181,095 fair

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,015,413.233 oz 62.687 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,120,090.560 oz

TOTAL REGISTERED GOLD 19,206,738.675 or 597.410 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,913,351.885 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,191,325oz ((REG GOLD- PLEDGED GOLD)=

537.57 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

DEC 22 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 0 entries total withdrawal: nil oz |

| Deposits to the Dealer Inventory | 0 ENTRY i total deposit nil |

| Deposits to the Customer Inventory | 5 ENTRIES i) Out of Asahi 589,064.400 oz ii) Out of CNT 600,000.250 oz iii) Out of Delaware 10,981.400 oz iv) Out of JPMorgan: 1,282,399.50 oz v) Out of Loomis: 600,963.200 oz total: 3083,409.750 oz |

| No of oz served today (contracts) | 54 CONTRACT(S) ( 0.270 million OZ |

| No of oz to be served (notices) | 106 contracts (0.530 MILLION oz) |

| Total monthly oz silver served (contracts) | 12,548 Contracts (62.740 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRY

withdrawals: customer side/eligible

5 ENTRIES

i) Out of Asahi 589,064.400 oz

ii) Out of CNT 600,000.250 oz

iii) Out of Delaware 10,981.400 oz

iv) Out of JPMorgan: 1,282,399.50 oz

v) Out of Loomis: 600,963.200 oz

total: 3083,409.750 oz

adjustments: 0

TOTAL REGISTERED SILVER: 128,616 MILLION OZ//.TOTAL REG + ELIGIBLE. 450.643Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC.

silver open interest data:

FRONT MONTH OF DECEMBER /2025 OI: 160 OPEN INTEREST CONTRACTS FOR A LOSS OF 49 CONTRACTS. WE HAD 120 CONTRACTS FILED ON FRIDAY SO WE ACTUALLY HAD ANOTHER QUEUE JUMP OF 71 CONTRACTS OR 355,000 OZ

JANUARY GAINED 55 CONTRACTS UP TO 4304 CONTRACTS AS JANUARY NOW BECOMES THE FRONT MONTH. WE MAY HAVE A VERY STRONG JANUARY DELIVERY MONTH FOR 20 MILLION OZ

FEB GAINED 62 CONTRACTS UP TO 1461 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 54 or 0.270 MILLION oz

CONFIRMED volume; ON FRIDAY 104,662 huge//

AND NOW DECEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 12,548 X5,000 oz = 62.740 MILLION oz

to which we add the difference between the open interest for the front month of DEC (160) AND the number of notices served upon today (54 )x (5000 oz)

Thus the standings for silver for the DECEMBER 2025 contract month: (12,548) Notices served so far) x 5000 oz + OI for the front month of DEC(160) minus number of notices served upon today (54)x 5000 oz equals silver standing for the DEC.contract month equating to 63.350 MILLION OZ + 850 MILLION OZ FOR DEC ‘S FIRST EXCHANGE FOR RISK AND THEN TODAY’S SECOND EXCHANGE FOR RISK OF .485 MILLION OZ//NEW TOTAL EXCHANGE FOR RISK; 1.335 MILLION OZ: THUS WE HAVE THE FOLLOWING:

NORMAL STANDING: 63.270 MILLION OZ

PLUS 1.335 MILLION OZ EXCHANGE FOR RISK/2 OCCASIONS

New total standing: 64.605 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 128.616. million oz of registered silver

JPMorgan as a percentage of total silver: 188,851/450.643million. 41.94%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 19/WITH GOLD UP $22.20 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 18/WITH GOLD DOWN $9.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .85 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 17/WITH GOLD UP $39.45 TODAY/NO CHANGES IN GOLD AT THE GLD:// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 16/WITH GOLD DOWN $3.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 15/WITH GOLD UP $10.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 105.12 TONNES

DEC 12/WITH GOLD UP $14.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.83 TONNES

DEC 11/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 10/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 9/WITH GOLD UP $18.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.14 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1049.11 TONNES

DEC 8/WITH GOLD DOWN $23.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.33 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1050.25 TONNES

DEC 5/WITH GOLD UP $9.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 4.00 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.58 TONNES

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

DEC 3/WITH GOLD UP $14.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1048.30 TONNES

DEC 2/WITH GOLD DOWN $53.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.58 TONNES OF GOLD VAPOUR INTO THE GLD// /// ///INVENTORY RESTS AT 1050.01TONNES

DEC 1/WITH GOLD UP $22.75 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43TONNES

NOV 28/WITH GOLD UP $51.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43 TONNES

NOV 26/WITH GOLD UP $25.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT PAPER DEPOSIT OF 4.57 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 25/WITH GOLD UP $46.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 24/WITH GOLD UP $16.95 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.86 TONNES

NOV 21/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.00 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1039.43 TONNES

NOV 20/WITH GOLD DOWN $20.45 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 19/WITH GOLD UP $14.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 18/WITH GOLD DOWN $6.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 17/WITH GOLD DOWN $20.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.93 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1044.000 TONNES

NOV 14/WITH GOLD DOWN $97.55TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1048.93 TONNES

NOV 13/WITH GOLD DOWN $17.80.TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1064.64 TONNES

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT XXX TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

GLD INVENTORY: 1052.54 TONNES, TONIGHTS TOTAL

SILVER

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 17/WITH SILVER UP $2.93/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 16/WITH SILVER DOWN $.07/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 56.360 MILLION OZ //

DEC 15/WITH SILVER UP $1.62/SMALL CHANGES IN SILVER AT THE SLV: A SMALL DEPOSIT OF 635,000 INTO THE SLV. ./ :INVENTORY RESTS AT 517.720 MILLION OZ //

DEC 12/WITH SILVER DOWN $2.30/NO CHANGES IN SILVER AT THE SLV: ./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 11/WITH SILVER UP $3.52/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.537 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 9/WITH SILVER UP $2.41/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.179 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 510.828 MILLION OZ //

DEC 8/WITH SILVER DOWN $0.48/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 5.497 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 512.007 MILLION OZ //

DEC 5/WITH SILVER UP 0.39/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.083 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.448 MILLION OZ //

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

DEC 3/WITH SILVER UP $0.23/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 1.956 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 510.012 MILLION OZ //

DEC 2/WITH SILVER DOWN $0.65 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND FRAUDLUENT PAPER DEPOSIT OF 6.167 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 508.057 MILLION OZ //

DEC 1/WITH SILVER UP $2.21 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 907,000 OZ INTO THE SLV./ :INVENTORY RESTS AT 501.890 MILLION OZ //

NOV28/WITH SILVER UP $3.28 TODAY/NO CHANGES IN SILVER AT THE SLV:/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV26/WITH SILVER UP $1.86 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 2.267 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV25/WITH SILVER UP $0.69 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 8.163 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 498.716 MILLION OZ //THIS IS A FRAUDULENT TRANSACTION

NOV24/WITH SILVER UP $0.43 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 277,000, OZ OUT OF THE SLV/ :INVENTORY RESTS AT 490.553 MILLION OZ MILLION OZ

NOV21/WITH SILVER DOWN $0.53 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 635,000 OZ INTO THE SLV/ :INVENTORY RESTS AT 490.190 MILLION OZ MILLION OZ

NOV20/WITH SILVER DOWN $0.53 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.555 MILLION OZ MILLION OZ

NOV 19/WITH SILVER UP $0.36 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 18/WITH SILVER DOWN $0.13 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489..283 MILLION OZ MILLION OZ

NOV 17/WITH SILVER DOWN $0.07 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.451 MILLION OZ INTO THE SLV:INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 14/WITH SILVER DOWN $2.08 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.722 MILLION OZ INTO THE SLV:

INVENTORY RESTS AT 487.832 MILLION OZ MILLION OZ

NOV 13/WITH SILVER DOWN $0.58 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

CLOSING INVENTORY 516.541 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

Silver Just Called The COMEX’s Bluff

Monday, Dec 22, 2025 – 12:45 PM

Authored by Matthew Piepenburg via VonGreyerz.gold,

December means many things: A year coming to an end, a time for reflection, a time for looking ahead. A time for family and friends, and of course, a time for holiday belly-expansion.

However, what many may have missed this December is that it was the month the paper markets in silver had yet another near-death experience.

Hiding in Plain Site

As usual, this critical turning point in metals, as well as its neon-flashing signal of a globally debt-sick financial and currency system, went largely unnoticed.

In financial markets, the daily buzz remained forever focused on the usual suspects, from BTC’s massive falls, MicroStrategy’s losing gambit (-59% YTD) and an over-stretched stock market to crude oil’s annual loss or the never-ending deflation/inflation or strong vs. weak DXY debates.

These are, of course, important debates and topics. Most investors understand them, and thus most investors, bull or bear, have an opinion about them. That is why they fill headlines.

Hiding in Intentional Complexity

But often, in fact nearly always, the real and more nuanced signals, as well as market warnings, are deliberately omitted from the Zeitgeist.

This is not only because such signals are a threat to the so-called “experts” behind these failing and corrupted systems, but because, as such, they are made deliberately too complex for Joe Sixpack to see and hence critique.

I’ve written about such intentional obfuscation through intentional complexity before.

And nowhere is this tactic put to better use than in trying to hide the legalized price-fixing masquerading as “hedging” at that oh-so complex beast otherwise known as the COMEX exchange.

For this reason, I’ve tried (as well as warned) for years to make simple sense out of the otherwise senseless COMEX mechanizations used to manipulate the paper price of gold and silver.

If needed, these “simplifications” of the “complex” can be chronologically revisited here, here and here for a re-fresher course.

Making the Complex Simple

For now, however, let’s continue to derive the simple from the complex.

Toward this end, the core theme is very simple and worth repeating: Sovereign nations guilty of unprecedented debt addiction—and hence the currency debasement needed to monetize that addiction—are absolutely terrified of rising gold and silver prices.

This is because rising precious metals are an open middle finger to governments who have grossly and negligently mismanaged the national currencies by which most citizens measure their wealth.

Precious metals naturally rise when paper money, inflated to reduce debt burdens, unnaturally falls in purchasing power.

And when a currency loses its purchasing power, the natives get restless, and the government, fully to blame for the same, gets both nervous and dishonest.

Making the COMEX Simple

That is why the COMEX, in 1974, added futures contracts to allow massive levels of leverage in the hands of a small cabal of bullion banks to conduct equally massive shorts on the gold and silver price each and every day since. This keeps the prices forced down.

The COMEX, in short, was designed for no other reason than to manipulate gold and silver, for gold and silver, promised by the U.S. Constitution as real money, had been taken away from the people in August of 1971.

The cabal responsible for this crime didn’t want this stolen “real money” to outshine the fake paper money that replaced it.

Since 1971, the fall of fiat money’s purchasing power when measured against gold has been greater than 99%.

That was embarrassing, of course, but it was a slow frog boil which the media and even most citizens ignored for decades.

By December of 2025, however, the narrative of a robust USD had lost its credibility for so many reasons detailed elsewhere, but made most obvious by an astronomical, 2025 gold and silver price appreciation driven by global demand which openly preferred real money over the USD and USTs as the new strategic reserve asset.

Today, global central banks hold more physical gold than USTs.

In short, the world has caught on that precious metals preserve their purchasing power infinitely better than credit-based and openly melting paper dollars.

The Greenback, since it was weaponized in 2022, has simply lost its prior hegemony.

Or stated even more simply: Uncle Sam was losing, and hence the COMEX was desperate to save face and buy time for his discredited dollar by attempting to kneecap the precious metals.

But as we’ve warned all year, the COMEX was running out of the needed gold and silver to continue its legalized charades.

A COMEX NDE

Which brings us, at last, to December 12, 2025 and the COMEX’ Near Death Experience (NDE)…

Unnoticed by nearly everyone, a desperate CME board raised the margin requirement (i.e., cost of leverage) for silver futures contracts by 10%, in what could be the first of more to come.

This may sound wonky, perhaps even boring, but its mechanizations and ramifications are very important.

What this crafty, 2:00 AM pre-weekend hike in margins by a so-called “neutral exchange” boiled down to was a deliberate and desperate attempt to force a massive liquidation (i.e., sell-off) in silver.

Thanks to an overnight hike in “buy-in” on that legalized and fixed casino otherwise known as the COMEX, the shadow-banking speculators going long silver at massive turns of leverage were immediately and electronically forced to cover the fee gap or have their positions sold automatically.

Needless to say, at 2:00 AM, covering was nearly impossible, so the sell-off was effectively forced.

Running Out of Control

If this seems crazy, it was. But sadly, the desperate tactic was nothing new. In 1980, a similar and overnight re-pricing of levered contracts took 50% off the silver price due to a massive sell-off in PAPER silver.

By May of 2011, the same tactic successfully crushed the metal when five consecutive margin hikes sent the silver price down in a matter of days from $49 to $33. Thereafter, PAPER silver stayed low for years to come. The COMEX had won.

Since then, similar margin hikes of 10% occurred in February of 2010, followed by an 11% hike in October. In both instances, silver dipped by 1.8% to 3.3% and then rose by 9% and 18% respectively, within 30 days. We saw similar patterns in August of 2020.

The COMEX had lost. Classic shakeouts were followed by major moves to the upside.

On December 12 of this year, unnoticed by most headlines and investors, the same trick failed yet again just as the metal closed at $62.50.

The 10% margin hike this month didn’t shake silver. 67 million ounces of paper silver sold off in minutes, only to be absorbed by purchasers of the physical metal. Less than a week later, silver was at new highs above $66.00.

The reasons why silver (which has seen a >100% upside for the year) prevailed speaks volumes not only about precious metals, but the state of the broken financial system in which we are all trying to navigate.

What Went Wrong in New York?

So why had the COMEX lost more steam in December of 2025?

Despite the exchange’s complex plumbing, the answer is simple, and boils down to this: The demand for physical silver is stronger than the COMEX’s once unstoppable paper market shorts.

In 1980 and 2011, for example, the COMEX vaults still had enough of the actual metals—i.e. a “silver float”—to lever the same.

But as we’ve argued since November of 2024, the metals have been exiting the COMEX at historical levels because, in a world of dying paper currencies, counterparties (i.e., sovereign nations) now want to own the physical metal.

In addition, the industrial bid for a tightly-supplied basket of genuine, physical silver at places as diverse as Samsung or Tesla is much stronger than the paper games played in New York.

These industrial buyers of silver need the metal for circuit boards, photovoltaic panels, e-vehicles and even nuclear reactors.

When they saw last weekend’s attempt by the COMEX to manipulate the price down, rather than get spooked out of the trade (like hedge funds and other speculators), they had standing orders to buy rather than sell the artificial dip.

Industrial bidders also knew that once this physical silver is bought, it is melted into use and never coming back, which means that the silver price (based on tight supply and rising demand) will move higher over time—and thus all the more reason to rejoice rather than panic whenever a CME dip is manufactured in New York.

Rock Now Beats Paper

Tying this altogether, the failed December attempt to create a massive silver sell-off was nothing more than a clearing of the PAPER speculators from the space and major buy signal for the physical metal buyers who now have more power, patience and leverage than an increasingly tapped-out COMEX exchange.

As warned for years, the COMEX is slowly dying because demand for physical metals is outpacing their empty vaults and increasingly impotent paper games.

Or as I stated months ago: “Rock now beats paper.”

The Long Game Wins

Of course, the foregoing but largely ignored trick in the COMEX has larger ramifications for investors playing the long game in physical rather than paper silver.

Those mocked for years as “stackers” will be getting the last laugh over time. Like industrial bidders or sovereign wealth funds who want real rather than paper silver for actual use as well as superior monetary value, physical silver owners don’t have to worry about the paper version of the metal.

They have always known that paper silver is not silver, it’s merely a levered and largely impotent “claim” on silver.

More importantly, the ability of exchanges like the COMEX to beat down physical silver via paper contracts is getting weaker and weaker, which means free price discovery is returning to the metals after decades of legalized COMEX fraud.

Or stated even more simply, COMEX was always about managing (manipulating) the paper price of silver, but the real-world demand for the physical metal represents a massive and now more powerful wall of money.

In a 2025 backdrop of culminating distrust for debt-soaked bonds, currencies and policies, global demand for physical silver—and, of course, physical gold—has outpaced the power and tricks of that COMEX paper tiger in New York.

This, of course, is yet another critical signal in the historically familiar cycles of dying fiat money and rising precious metals.

Keeping It Real

But this does not mean silver or gold will only go up in straight lines from here. Not at all.

Bull markets in metals have seen retracements, even large ones, in the middle of their rising cycles. A Tanking stock market, which is equally inevitable, can also cause temporary pullbacks in precious metals, which no one can time or predict. No one.

But owners of precious metals know this much: Gold and silver store their value better than paper currencies over time. And time is on their side.

A Couple Tricks Left

Nor is the increasingly desperate and openly gasping COMEX out of tricks. It still has a couple up its tattered sleeves.

For example, its next move could be position-limits whereby it will limit the number of silver contracts held by ETFs or family offices who still confuse paper metal with actual metal. Such position limits would induce sell-offs and southern price moves.

But as occurred this month, any such “discount” made in New York would later be bought rather than sold.

The final move we could expect from the COMEX is the most desperate. That is, it could go into liquidation mode, a “nuclear option” by which parties to the COMEX could only be sellers rather than buyers of silver.

In such an extreme scenario, the paper price of silver would, of course, sink.

Silver buyers in such a scenario would likely move to other metals desks in Shanghai or London for fairer pricing, a move which would only make the COMEX even less relevant.

Back to Simple

Ultimately, all these signals and sounds from the once all-powerful COMEX are the signals and sounds of a dying system in not only paper contracts, but so-called “paper money.”

The global financial system, after decades of buying time and unprecedented debt levels with mouse-clicked currencies, is finally hitting its inflection point (or Waterloo Moment) as physical silver and gold rise steadily above the rubble of a broken monetary system led by the home (and central bank) of the world’s weaponized reserve currency.

Silver was simply calling the bluff on a failed system in general and a discredited COMEX in particular.

ALASDAIR MACLEOD..

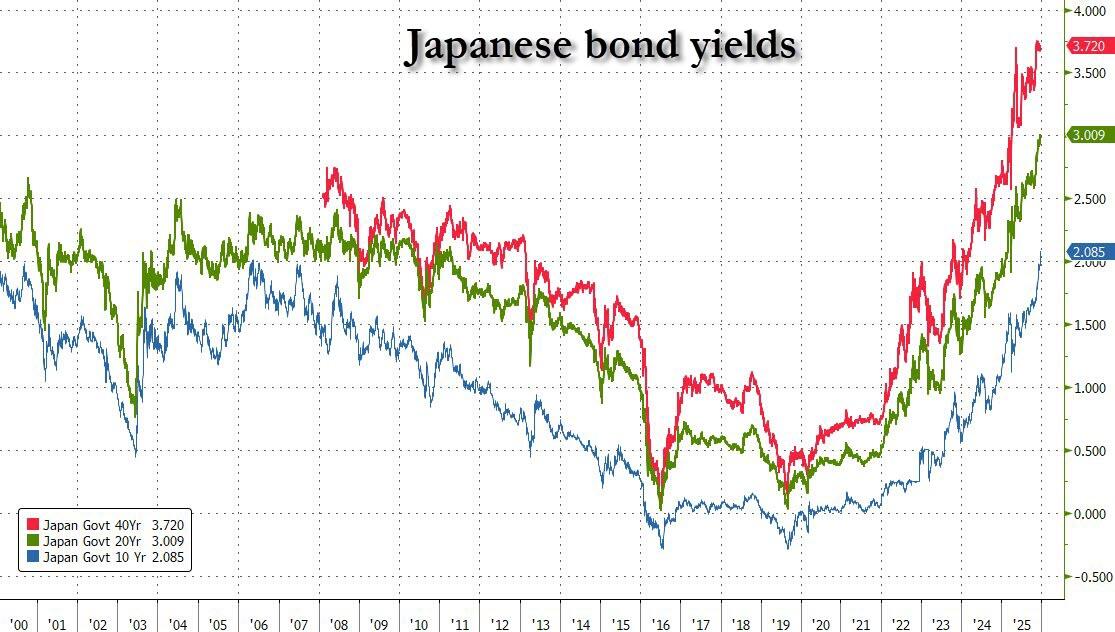

G7 bond yields are breaking higher into 2026

In this article we demonstrate the consequences of a bond bear market while equities are in in a bubble. Something will have to give and it will be equities.

| Alasdair MacleodDec 21∙Paid |

Introduction

Bond markets of three G7 nations are on the verge of crashing. The USA, UK, and Canada are not far behind, and the jury is out for Italy. But with Japan and two Eurozone nations facing a debt crisis, they are almost certain to take down the other G7s as well.

The most important of the crash candidates is Japan, because low yields for JGBs have encouraged Japanese pension funds and insurance companies to invest in US Treasuries instead. Furthermore, the Bank of Japan’s interest rate suppression has given Japanese institutions an additional benefit from a weakening yen to the dollar, moving from ¥103 in late-December 2020 to ¥158 currently, a profitable decline of 35%.

Japanese institutions now account for $1.2 trillion of US Treasuries. Mostly by way of a yen-based carry trade, US captive insurance companies and offshore hedge funds based in the Cayman Islands account for an additional $418.5 billion.

Additionally, special purpose vehicles operating out of Luxembourg account for most of an additional $419 billion, and London-based carry traders funding in cheap euros probably represent the bulk of an additional $878 billion. Belgium, where Euroclear is based accounts for an additional $468 billion of US Treasuries.

That is a total of $3,383.5 billion of US Treasuries mostly owned by speculative foreign-based “shadow banks” basing their ownership on yield differentials between the US and Japan and the Eurozone. It is locking in US Treasury yields to those of sovereign bonds in the euro and yen. Where they go, so will US Treasuries.

The charts below are of 10-year bond yields for Japan, Germany, and France. Japan’s yield is already in runaway mode, soaring over 2% — the highest level since 1997. German and French 10-year bond yields are just breaking into new high ground.

Canada and Italy have similar consolidation patterns but are not yet challenging breakout levels. The US 10-year Treasury note is crawling along the lower trend line of a similar pattern to that of the 10-year gilt (not shown):

While the US Treasury yield is not yet threatening to break out above an 18-month consolidation, the global trend is clear. And Canada’s is breaking above its flag, but has about 60 basis points to go before making new high ground:

Confirmation of these yield trends is likely to come very soon, though Japan is already leading the way. But it is worth noting that longer-dated bond yields in Japan, Germany, and France are already hitting new highs. And in all the G7 the longer the maturity, the greater the yield.

The reasons driving higher yields

An investor will want a return on his investment, comprised of his estimate of the following three considerations: the loss of use of capital which might be deployed elsewhere, counterparty risk, and the risk associated with the currency. When it comes to investing in readily marketable government bonds in its own currency, it is currency risk which predominates — the risk that at the end of a period, perhaps a year for reference, the currency’s purchasing power might decline.

Therefore, key G7 yields threatening to rise further tell us that the balance of probabilities is for an increasing risk of currencies facing a decline in purchasing power. This is confirmed by a rising gold price.

The relationship between bonds and equities

Experience guides us of the relationship between equities and bonds. In the first phase of a bull market after the preceding bear, bond yields will have stabilised. But the economy is depressed and the bankruptcy rate remains high. Seasoned entrepreneurs and company doctors will seek out opportunities to restructure businesses, perhaps merging them with others. They will work with banks to recover their loans. Gradually, investment and commercial banks will extend finance to facilitate mergers and takeovers. Share prices begin an initial recovery process on the back of this corporate activity, but the investing public remains sellers on balance while observing that the economy is still in recession.

Because the expansion of bank credit is limited to financing takeovers, mergers, and other restructuring activities, there is likely to be a pause in the bull market while uncertainty persists, before the second bull phase gets under way.

As increasing signs that the recession is getting no worse and some economic stability is returning, a second bull phase starts. Banks gradually become more confident in their lending, perhaps competing for low-risk loan quality by reducing their lending margins. Professional investors are early buyers of equities in this second phase, and economic recovery encourages both credit demand and investment. Towards the end of the second phase demand begins to drive bank credit expansion, wholesale and consumer prices begin to rise, and interest rates and bond yields begin to rise as well.

In the third and final bull market phase, the wider public reckons buying stocks is a good thing. They have forgotten their losses in the last bear market, are always late to the party, and chase fashionable sectors. Increasingly, value takes a back seat and momentum investing emerges. Greed for profit replaces fear of loss. Meanwhile, demand for credit increases, not only to finance unexpected rises in business input costs and excess consumption, but also stockmarket speculation. Consequently, interest rates and bond yields rise, due to excessive credit demand in conditions of economic overheating.

This description of the three phases of a bull market separated by two periods of consolidation is an idealised model, shorn of most government meddling. But it is important to appreciate that equities can tolerate an initial rise in bond yields — after all they are an alternative investment and their initial decline chases funds into equities. But it is the second rise in bond yields which marks the end of the entire bullish cycle.

That is why the charts of government bond yields in the first part of this article are so important. While global bond yields have been in a consolidation phase for the last eighteen months, equity markets in the G7 nations rose strongly, as the investing public have come to believe that equities will continue to rise and rise. Obviously, the surprise of higher bond yields will shatter that dream.

Equity valuations have become massively overstretched

Our last chart shows something else. While we can understand an idealised equity relationship to bonds over one whole cycle, there is a tendency for an even larger cycle to evolve, driven by governments and their central banks preventing the full malinvestment liquidation phase of bear markets. Instead of Schumpeter’s creative destruction when accumulated economic distortions are washed out of the system, it becomes only a partial flush, with industrial and financial businesses which should have ceased trading subsidised by governments to continue.

The chart above bears close examination. It is constructed by basing the S&P and the long bond yield at 100 in 1985, and plotting both to logarithmic scales. While the S&P’s y-axis on the left increases positively, the bond yield’s y-axis on the right is inverted. The chart therefore shows the close negative correlation between the two: in other words, a falling bond yield generally correlates with rising equities and vice-versa.

There have been instances when optimism in equities has driven them too high in relation to the bond yield. The buildup in the late 1990s to the dot-com bubble is clearly demonstrated. A secondary equity overvaluation ahead of the Lehman crisis, corrected by a bear market taking the S&P down to a low point in February 2009 is also visible.

Following that crisis, the Fed suppressed interest rates and therefore bond yields making equities appear cheap relative to bonds, evidenced by the blue line being consistently above the red line on the chart. This reached a maximum distortion during covid, when accelerated QE by the Fed drove down bond yields to their lowest level ever. That kick-started a new bull phase for the S&P which took it from under 2,500 to 6,834 currently, a rise of 173%.

At the same time bond yields began to recover sharply, reflecting the inflationary consequences of the Fed’s unprecedented QE. But so ingrained was end-of-cycle investor optimism that the equity bull has continued to the point where the valuation gap is the largest recorded in history, indicated by the double-headed arrow on the right of the chart.

It is evidence of the end of a super-cycle. Over repeated boom-and-bust cycles, government intervention has prevented bust phases from occurring. Unaddressed economic distortions have accumulated into a mountain of unproductive debt, as governments have bailed and subsidised economic activities since the 1980s. Otherwise, they would have gone to the wall. These distortions have fostered an assumption that if things go wrong, the government will always bail everyone out.

Confidence and wealth generation in the stock market are an essential component of economic policy. It leads to the conclusion that not just banks and industries will never be allowed to fail, but that the entire financial system including investors will be bailed out as well. After all, that was the clear message from the Fed’s handling of the 2007—2009 financial crisis.

Now that bond yields are beginning to rise again with signs of debt traps and doom loops being sprung on governments, the moment when the equity bubble bursts will shortly be upon us. Valuations are now so extreme that the collapse in equity values should be greater than anything seen since the 1929—1932 bear market on Wall Street, when 10,000 banks failed.

This time, the economic imperative is to prevent such an outcome. Ninety-five years ago, the dollar was on a gold standard: this time it is pure fiat and there is no such restraint. We can be certain that the US Treasury and the Fed will use that freedom to expand QE as much as required to secure the entire financial system and prevent a wealth-destroying 90% equity market crash.

They might succeed, but the cost will be the debasement of the dollar. It is an outcome already telegraphed by rising gold and metals prices. The surprise to all will be sharply rising prices for commodities, goods, and services perhaps from mid-2026 onwards. It won’t be prices rising, but the dollar’s purchasing power collapsing.

The signs are that the crisis is at hand. Multi-year suppression of commodity prices is backfiring, with silver and platinum threatening to destabilise derivative markets. And importantly, the rise in global bond yields is just beginning, threatening to burst the equity bubble. And the rise in the gold price is discounting the consequences for all the major currencies in 2026—2027.

3. CHRIS POWELL AND HIS GATA DISPATCHES:

Mining entrepreneur Eric Sprott reviews a great year for the monetary metals

Submitted by admin on Fri, 2025-12-19 21:11 Section: Daily Dispatches

9:11p ET Friday, December 19, 2025

Dear Friend of GATA and Gold (and Silver):

On behalf of Sprott Money, Craig Hemke today interviewed Canadian mining entrepreneur Eric Sprott for their 2025 yearly review and they celebrated what seems like the imminent triumph of the monetary metals.

Sprott notes that the usual price smashes in the New York futures market now are often reversed within an hour and that physical prices are now being set in Shanghai.

Even so, Sprott says, the prices of gold and silver mining company shares are not yet keeping up with metal prices as they should, though the industrial fundamentals in favor of silver particularly have become overwhelming, far beyond what current mining production can cover.

Sprott expects that 2026 will be another great year for the monetary metals and the companies that mine them.

Hemke also induces Sprott to discuss some mining companies he is most enthusiastic about.

The discussion is 47 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ivory Coast miners start paying higher royalties after failed resistance, sources tell Reuters

Submitted by admin on Tue, 2025-12-16 17:08 Section: Daily Dispatches

By Maxwell Akalaare Adombila

Reuters

Tuesday, December 16, 2025

Gold mining companies in Ivory Coast have begun paying a new 8% royalty on revenue, backdated to January, after months of disputing the legality of the levy, three industry sources told Reuters.

Reuters previously reported that the top cocoa producer, which is seeking to diversify its economy, replaced the previous 3% to 6% range linked to contract terms with the flat 8% rate.

Miners initially refused to pay, arguing that the move was unlawful because their contracts shielded them from fiscal changes and entered negotiations with the government to have the new royalty scrapped.

However, companies have since started paying after the government refused to change its position, said the three people familiar with the matter, who declined to be named because they were not authorised to speak to the media. …

… For the remainder of the report:

END

China is quietly destroying the dollar … and that’ll cost you

Submitted by admin on Tue, 2025-12-16 16:45 Section: Daily Dispatches

By Charlie Garcia

MarketWatch, New York

Tuesday, December 16, 2025

China controls the rare earths. China controls the cobalt. China, through its Belt and Road spending spree, now controls most of the mines in Africa that produce the stuff inside your phone, your car, and your refrigerator.

And now China has figured out how to price and settle all of it without using a single U.S. dollar.

South African banking giant Standard Bank Group, Africa’s largest lender, has quietly integrated with China’s Cross-Border Interbank Payment System (CIPS). In June, Standard Bank secured its CIPS license; in September the new rail went live, and by November Africa’s first direct yuan, or renminbi, channel was open, a seemingly dry banking milestone that in reality shifted a crucial line on the hidden map of global power.

The financial press buried it under Federal Reserve noise and earnings reports. Everyone kept scrolling. But the dollar’s monopoly is cracking.

It matters to you. Not because you trade cobalt futures, but because when the U.S. dollar loses its monopoly on pricing critical resources, your purchasing power shrinks. That shows up at the grocery store, at the gas pump, and in every aisle of every store. You just won’t know why.

Here’s what happened: A payment that used to take three to five days now takes seven seconds. Costs dropped 98%. A cobalt shipment from Congo to Shanghai now settles in Chinese yuan, without touching New York and without anyone in Washington getting a vote.

The dollar just got cut out of the transaction entirely.

This isn’t about banking plumbing. It’s about power. Who sets commodity prices. Who controls sanctions. Who gets to define the term “risk-free.” For 50 years, that’s been the U.S. Not anymore. …

… For the remainder of the analysis:

* * *

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 253

OFF UNTIL JANUARY

5. COMMODITY REPORT//SILVER/SILVER LEASE RATES:/SILVER

Silver lease rates

Inbox

| Robert Lambourne | 1:28 PM (2 hours ago) | ||

| to me | |||

Harvey,

I checked earlier and silver lease rates for one month leases in Shanghai are reported as c6% and c7.5%/8% for one month leases in London as of Friday.

By the way gold lease rates are also slightly higher than normal at c3%/3.5% for one month.

So in silver lease rates are still elevated and so far there is no real indication that they are about to fall as inventories are reported to be tight with industrial demand strong in Asia.

I shall forward a couple of video links to Chris and you shortly. One of them is highlighted by one of the Chinese AI programs and possibly throws some more light on the rumoured large JP Morgan lease of silver from China.

We are certainly living in interesting times.

Bob

…end

PLATINUM//

PRICE RISES ABOVE $2,000 WITH ITS LEASE RATE AT 14%

FROM ROBERT LAMBOURNE:

lPlatinum hits 17-year high as tight supply doubles price in 2025 – FashionNetwork United Kingdom

Harvey,