access market

GOLD $4,491.90(3:30 PM)

SILVER: 71.24 3;30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: DECEMBER 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,361.400000000 USD

INTENT DATE: 12/19/2025 DELIVERY DATE: 12/23/2025

FIRM ORG FIRM NAME ISSUED STOPPED

118 H MACQUARIE FUTURES US 2

363 H WELLS FARGO SECURITI 429

435 H SCOTIA CAPITAL (USA) 1

661 C JP MORGAN SECURITIES 726 116

690 C ABN AMRO CLR USA LLC 4

709 C BARCLAYS 170

905 C ADM 2 6

TOTAL: 728 728

MONTH TO DATE: 35,30

EXCHANGE: COMEX

CONTRACT: DECEMBER 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,444.600000000 USD

INTENT DATE: 12/22/2025 DELIVERY DATE: 12/24/2025

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 100

118 C MACQUARIE FUTURES US 1

118 H MACQUARIE FUTURES US 2

132 C SG AMERICAS 1

190 H BMO CAPITAL MARKETS 278

332 H STANDARD CHARTERED B 1

363 H WELLS FARGO SECURITI 248

365 C MAREX CAPITAL MARKET 267

435 H SCOTIA CAPITAL (USA) 1

657 C MORGAN STANLEY 1

661 C JP MORGAN SECURITIES 71 249

690 C ABN AMRO CLR USA LLC 1

709 C BARCLAYS 89

726 C PLUS500US FINANCIAL 1

880 C CITIGROUP 50

905 C ADM 114

991 H CME 87

TOTAL: 781 781

MONTH TO DATE: 36,081

JPMORGAN STOPPED 249/781

GOLD: NUMBER OF NOTICES FILED FOR DEC/2025: 781 CONTRACTs NOTICES FOR 78,100 OZ or 2.429 TONNES

total notices so far: 36,081 contracts for 3,608,100 OR 112.227 tonnes)

SILVER NOTICES:27 NOTICE(S) FILED FOR .135 MILLION OZ/

total number of notices filed so far this month : 12,575 CONTRACTS (NOTICES) for 62.875 million oz

A DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD//

INITIAL STANDING FOR DEC: 49.33 MILLION OZ FOLLOWED BY TODAY’S 305,000 OZ QUEUE JUMP _ PLUS ..850 MILLION OZ EXCHANGE FOR RISK LAST MONDAY AND LAST TUESDAY’S .485 MILLION OZ/ (TOTAL EX. FOR RISK = 1.335 MILLION OZ)///STANDING ADVANCES TO 64.910 MILLION OZ//

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 36.96 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER HUGE 305,000 OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK // STANDING ADVANCES TO 64.910 MILLION OZ//

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.8460 TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 34.5568 TONNES//NEW STANDING ADVANCES TO 112.793 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK FOR DECEMBER OF 2.488 TONNES/NEW STANDING ADVANCES TO 115.281 TONNES

NEW STANDING FOR GOLD, DEC CONTRACT AT 115.281 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 154.74 TONNES//FAIR SIZED THIS MONTH.

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A TINY SIZED 45 CONTRACTS OI TO 156,794 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 500 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 500 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2217 CONTRACTS AND ADD TO THE 500 E.FP. ISSUED

WE OBTAIN A STRONG SIZED GAIN OF 509 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR HUGE GAIN OF $1.28 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 2.545 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $1.28

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ASIA RESULTS; TUESDAY DEC 23

SHANGHAI CLOSED UP 2.61 POINTS OR 0.07%

//Hang Seng CLOSED DOWN 27.63 PTS OR 0.11%

// Nikkei CLOSED UP 28.61 PTS OR 0.06% //Australia’s all ordinaries CLOSED UP 1.15%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.0281

/ OFFSHORE CLOSED UP AT 7.0172/ Oil UP TO 58.01 dollars per barrel for WTI and BRENT UP TO 62.06 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP TO 7.0281 OFFSHORE YUAN TRADING UP TO 7.0172:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY STRONG SIZED 12,149 CONTRACTS TO 501,273 OI WITH OUR HUGE GAIN IN PRICE OF $80.25 WITH RESPECT TO MONDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1775). WE HAD ZERO T.A.S. LIQUIDATION MONDAY (WITH MONTH END SPREADER LIQUIDATIONS CONTINUING MONDAY WITH SMALL REMOVALS). IT SEEMS THAT THE SPECULATORS WENT MASSIVELY HUGE TO THE LONG SIDE WITH OUR FRBNY PROVIDING STILL THE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE .

YOU WILL NOTICE THAT THE COMEX OI IS NOW GAINING HUGELY FROM ITS LOW OI OF AROUND 418,000 TO NOW 499,192 AND NOW AMPLE ENOUGH FOR A RAID BY OUR BANKERS.

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 13,924 CONTRACTS (OR 43.309 TONNES). THEN WE WERE NOTIFIED AGAIN OF A 400 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR 40,000 OZ OR 1.244 TONNES OF GOLD. THIS IS DECEMBER’S SECOND ISSUANCE AS IT COMES LATE IN THE MONTH. WE HAVE 3 CHOICES NOW FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 2.488 TONNES/2 OCCASIONS)

HERE ARE THE CHOICES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 39 TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 2.498 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS..

DETAILS ON OUR NEW DECEMBER COMEX CONTRACT MONTH//

IN TOTAL WE HAD A VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 13,924 CONTRACTS WTH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH DECEMBER/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR T.A.S ISSUANCE CONTRACTS. THE CME NOTIFIES US THAT THEY HAVE ISSUED 1567 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE HUGE NUMBER OF T.A.S. ISSUANCES IN EARLY DECEMBER.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.8406 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 34.5568 TONNES//STANDING ADVANCES TO 112.793 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 2.488 TONNES/NEW STANDING IS THUS: 115.281 TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 39+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 39 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. SO IT IS POSSIBLE THAT THE FED IS THE BUYER OF 1.244 TONNES OF EXCHANGE FOR RISK/DECEMBER!!

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 39 TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/DEC.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1775 CONTRACTS.

THAT IS A FAIR SIZED 1775 EFP CONTRACT WAS ISSUED: : /FEB 1775 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1775 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 39 TONNES

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE CONSIDERABLE GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW COMMENCED!…

T.A.S.SPREADER ISSUANCE//DECEMBER

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT//TUESDAY MORNING WAS A FAIR SIZED 1775 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP MONDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING STRONG GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE..ENOUGH FODDER FOR THE COMMENCEMENT OF A RAID

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.8406 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 34.5568 TONNES//NEW STANDING ADVANCES TO 112.793 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 2.488 TONNES//NEW STANDING THUS INCREASES TO 115.281 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING DECEMBER,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $80.25/ /)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY WITH MINOR MONTH END SPREADER LIQUIDATION// COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX// WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL MONDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR DECEMBER. THE COMEX IS ONE BIG MESS!!

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 3 MONTHS:

STANDING FOR GOLD OCT THROUGH TO DECEMBER:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 272 CONTRACT QUEUE JUMP FOR 27,200 OZ OR 0.8460 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 34.5568 TONNES///STANDING ADVANCES TO 112.793 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 2.488 TONNES/NEW STANDING ADVANCES TO 115.281 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $80.25

WE HAD A HUGE 2061 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .

INITIAL GOLD COMEX

DEC 23

DEC CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES i |

| Deposit to the Dealer Inventory in oz | 0- ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRIES i) Into Manfra 39,174.673 oz total deposit: 39,174.673 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 781 notice(s) 78100 OZ 2.429 TONNES OF GOLD |

| No of oz to be served (notices) | 182 contracts 0.5660 OZ 0.5660 TONNES |

| Total monthly oz gold served (contracts) so far this month | 36,081 notices 3,608,100 0z 112.227TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

1 ENTRIES

1 ENTRIES

i) Into Manfra 39,174.673 oz

total deposit: 39,174.673 oz

customer withdrawals:

0 ENTRIES

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 4//

a) Asahi: 25,270,686.oz (dealer to customer)

b) Brinks: 128,668.302 oz (customer to dealer)

c) JPMorgan: 13,985.629 oz (dealer to customer)

d) Stonex: 25,752.951 oz (customer to dealer)

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF DECEMBER STANDS AT 963 CONTRACTS FOR A LOSS OF 456 CONTRACTS. WE HAD 728 CONTRACTS FILED ON MONDAY SO WE GAINED A STRONG 272 CONTRACTS FOR A QUEUE JUMP OF 27,200 OZ OR 0.8460 TONNES TO WHICH WE ADD TO OUR PREVIOUS QUEUE JUMPS AND THEN ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK FOR 2.488 TONNES .THUS STANDING FOR GOLD IN DECEMBER INCREASES HUGELY TO 115.281 TONNES

JANUARY LOST 22 CONTRACTS DOWN TO 3753 AS JANUARY BECOMES THE FRONT MONTH. WE WILL PROBABLY HAS A GOOD SIZED 8 TO 9 TONNES OF GOLD STANDING.

FEB GAINED 8818 CONTRACTS UP TO 360,434 CONTRACTS

We had 781 contracts filed for today representing 78100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 71 notices issued from their client or customer account. The total of all issuance by all participants equate to 781 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 249 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2025. contract month, we take the total number of notices filed so far for the month (36,081 ) to which we add the difference between the open interest for the front month of DEC ( 963 CONTRACTS) minus the number of notices served upon today (781 x 100 oz per contract) equals 3,626,300 OZ OR 112.793 Tonnes of gold + 2.488 TONNES of exchange for risk issuance: new total standing advances to 115.281 tonnes!!

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (36,081 x 100 oz +we add the difference for front month of DEC (963 OI} minus the number of notices served upon today (781)x 100 oz) which equals 3,626300 OR 112.793 TONNES + 2.488 tonnes exchange for risk//new total standing advances to 115.281 tonnes

new total of gold standing in DECEMBER is 115.281 tonnes

TOTAL COMEX GOLD STANDING FOR DEC ..: 115.281 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF DECEMBER.

volume MONDAY confirmed 228,938 fair to good

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,001,427.554 oz 62.252 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,159,265.143 oz

TOTAL REGISTERED GOLD 19,321,903.563 or 600.995 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,837361.630 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,320,476oz ((REG GOLD- PLEDGED GOLD)=

538.739 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

DEC 23 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) Out of CNT 238,780.230 oz ii) Out of JPMorgan 597,993.380 oz iii) Out of Stonex 24,984.870 oz total withdrawal: 851,758.480 oz |

| Deposits to the Dealer Inventory | 0 ENTRY i total deposit nil |

| Deposits to the Customer Inventory | 3 ENTRIES i) Into Delaware 1004.200 oz ii) Into Loomis 599,388.88 oz iii) Into Manfra 487.944.545 oz total deposit 1088.337.645 oz |

| No of oz served today (contracts) | 27 CONTRACT(S) ( 0.135 million OZ |

| No of oz to be served (notices) | 140 contracts (0.700 MILLION oz) |

| Total monthly oz silver served (contracts) | 12,575 Contracts (62.875 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

3 ENTRIES

i) Into Delaware 1004.200 oz

ii) Into Loomis 599,388.88 oz

iii) Into Manfra 487.944.545 oz

total deposit 1088.337.645 oz

withdrawals: customer side/eligible

3 entries

i) Out of CNT 238,780.230 oz

ii) Out of JPMorgan 597,993.380 oz

iii) Out of Stonex 24,984.870 oz

total withdrawal: 851,758.480 oz

adjustments: 1

dealer to customer: Asahi

1402,453.258 oz

TOTAL REGISTERED SILVER: 127,214 MILLION OZ//.TOTAL REG + ELIGIBLE. 450.880Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC.

silver open interest data:

FRONT MONTH OF DECEMBER /2025 OI: 167 OPEN INTEREST CONTRACTS FOR A GAIN OF 7 CONTRACTS. WE HAD 54 CONTRACTS FILED ON MONDAY SO WE ACTUALLY HAD ANOTHER QUEUE JUMP OF 61 CONTRACTS OR 305,000 OZ

JANUARY LOST 1 CONTRACT DOWN TO 4303 CONTRACTS AS JANUARY NOW BECOMES THE FRONT MONTH. WE MAY HAVE A VERY STRONG JANUARY DELIVERY MONTH FOR AROUND 20 MILLION OZ

FEB GAINED 113 CONTRACTS UP TO 1573 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 27 or 0.135 MILLION oz

CONFIRMED volume; ON MONDAY 109,682 huge//

AND NOW DECEMBER. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 12,575 X5,000 oz = 62.875 MILLION oz

to which we add the difference between the open interest for the front month of DEC (167) AND the number of notices served upon today (27 )x (5000 oz)

Thus the standings for silver for the DECEMBER 2025 contract month: (12,575) Notices served so far) x 5000 oz + OI for the front month of DEC(167) minus number of notices served upon today (27)x 5000 oz equals silver standing for the DEC.contract month equating to 63.575 MILLION OZ + 850 MILLION OZ FOR DEC ‘S FIRST EXCHANGE FOR RISK AND THEN A SECOND EXCHANGE FOR RISK OF .485 MILLION OZ//NEW TOTAL EXCHANGE FOR RISK; 1.335 MILLION OZ: THUS WE HAVE THE FOLLOWING:

NORMAL STANDING: 63.575 MILLION OZ

PLUS 1.335 MILLION OZ EXCHANGE FOR RISK/2 OCCASIONS

New total standing: 64.910 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 127.214. million oz of registered silver

JPMorgan as a percentage of total silver: 188,253/450.880million. 41.94%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 19/WITH GOLD UP $22.20 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 18/WITH GOLD DOWN $9.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .85 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 17/WITH GOLD UP $39.45 TODAY/NO CHANGES IN GOLD AT THE GLD:// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 16/WITH GOLD DOWN $3.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 15/WITH GOLD UP $10.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 105.12 TONNES

DEC 12/WITH GOLD UP $14.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.83 TONNES

DEC 11/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 10/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 9/WITH GOLD UP $18.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.14 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1049.11 TONNES

DEC 8/WITH GOLD DOWN $23.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.33 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1050.25 TONNES

DEC 5/WITH GOLD UP $9.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 4.00 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.58 TONNES

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

DEC 3/WITH GOLD UP $14.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1048.30 TONNES

DEC 2/WITH GOLD DOWN $53.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.58 TONNES OF GOLD VAPOUR INTO THE GLD// /// ///INVENTORY RESTS AT 1050.01TONNES

DEC 1/WITH GOLD UP $22.75 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43TONNES

NOV 28/WITH GOLD UP $51.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43 TONNES

NOV 26/WITH GOLD UP $25.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT PAPER DEPOSIT OF 4.57 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 25/WITH GOLD UP $46.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 24/WITH GOLD UP $16.95 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.86 TONNES

NOV 21/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.00 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1039.43 TONNES

NOV 20/WITH GOLD DOWN $20.45 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 19/WITH GOLD UP $14.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 18/WITH GOLD DOWN $6.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1041.43 TONNES

NOV 17/WITH GOLD DOWN $20.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.93 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1044.000 TONNES

NOV 14/WITH GOLD DOWN $97.55TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1048.93 TONNES

NOV 13/WITH GOLD DOWN $17.80.TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1064.64 TONNES

NOV 12/WITH GOLD UP $97.70.TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.30 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT XXX TONNES

NOV 11/WITH GOLD DOWN $3.80TODAY/NO CHANGES IN GOLD AT THE GLD: . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 10/WITH GOLD UP $114.40TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT 1042.06 TONNES

NOV 7/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD . /// ///INVENTORY RESTS AT1042.06TONNES

NOV 6//WITH GOLD UP $0.30TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 5//WITH GOLD UP $32.50TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL 0F 3.15 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT1038,63TONNES

NOV 4 WITH GOLD DOWN $50.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT 0F 2.58 TONNES OF GOLD OUT OF THE GLD . /// ///INVENTORY RESTS AT 1041.78TONNES

GLD INVENTORY: 1064.66 TONNES, TONIGHTS TOTAL

SILVER

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 17/WITH SILVER UP $2.93/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 16/WITH SILVER DOWN $.07/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 56.360 MILLION OZ //

DEC 15/WITH SILVER UP $1.62/SMALL CHANGES IN SILVER AT THE SLV: A SMALL DEPOSIT OF 635,000 INTO THE SLV. ./ :INVENTORY RESTS AT 517.720 MILLION OZ //

DEC 12/WITH SILVER DOWN $2.30/NO CHANGES IN SILVER AT THE SLV: ./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 11/WITH SILVER UP $3.52/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.537 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 9/WITH SILVER UP $2.41/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.179 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 510.828 MILLION OZ //

DEC 8/WITH SILVER DOWN $0.48/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 5.497 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 512.007 MILLION OZ //

DEC 5/WITH SILVER UP 0.39/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.083 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.448 MILLION OZ //

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

DEC 3/WITH SILVER UP $0.23/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 1.956 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 510.012 MILLION OZ //

DEC 2/WITH SILVER DOWN $0.65 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND FRAUDLUENT PAPER DEPOSIT OF 6.167 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 508.057 MILLION OZ //

DEC 1/WITH SILVER UP $2.21 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 907,000 OZ INTO THE SLV./ :INVENTORY RESTS AT 501.890 MILLION OZ //

NOV28/WITH SILVER UP $3.28 TODAY/NO CHANGES IN SILVER AT THE SLV:/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV26/WITH SILVER UP $1.86 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 2.267 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV25/WITH SILVER UP $0.69 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 8.163 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 498.716 MILLION OZ //THIS IS A FRAUDULENT TRANSACTION

NOV24/WITH SILVER UP $0.43 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 277,000, OZ OUT OF THE SLV/ :INVENTORY RESTS AT 490.553 MILLION OZ MILLION OZ

NOV21/WITH SILVER DOWN $0.53 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 635,000 OZ INTO THE SLV/ :INVENTORY RESTS AT 490.190 MILLION OZ MILLION OZ

NOV20/WITH SILVER DOWN $0.53 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.555 MILLION OZ MILLION OZ

NOV 19/WITH SILVER UP $0.36 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 18/WITH SILVER DOWN $0.13 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489..283 MILLION OZ MILLION OZ

NOV 17/WITH SILVER DOWN $0.07 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.451 MILLION OZ INTO THE SLV:INVENTORY RESTS AT 489.283 MILLION OZ MILLION OZ

NOV 14/WITH SILVER DOWN $2.08 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.722 MILLION OZ INTO THE SLV:

INVENTORY RESTS AT 487.832 MILLION OZ MILLION OZ

NOV 13/WITH SILVER DOWN $0.58 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 12/WITH SILVER UP $2.59 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 11/WITH SILVER UP $0.63 TODAY/NO CHANGES IN SILVER AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 10/WITH SILVER UP $2.05 TODAY/NO CHANGES IN GOLD AT THE SLV: . /// ///INVENTORY RESTS AT 485.110 TONNES

NOV 7 WITH SILVER UP $0.22 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.54 MILLION OZ FROM THE SLV / ///INVENTORY RESTS AT 485.110 MILLION OZ

NOV 6 WITH SILVER DOWN $0.12 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

NOV 5 WITH SILVER UP $0.67TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 713,000 OZ FROM THE SLV / ///INVENTORY RESTS AT 487,650 MILLION OZ

CLOSING INVENTORY 533.678 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD..

3. CHRIS POWELL AND HIS GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 253

OFF UNTIL JANUARY

5. COMMODITY REPORT//SILVER/SILVER LEASE RATES:/URANIUM

ZERO HEDGE/AI

Why The Price Of Uranium Is About To Soar

As of late December 2025, the uranium spot price stands at approximately $80.25 per pound (U₃O₈), reflecting a modest recovery from earlier 2025 lows around $63–$64/lb and highs near $83/lb. Analysts and market reports widely anticipate upward pressure on prices heading into 2026 and beyond, driven by a structural supply-demand imbalance.Surging Demand from Nuclear RenaissanceGlobal nuclear power generation is expanding rapidly as countries pursue clean, reliable baseload energy to meet net-zero goals, energy security needs, and exploding electricity demand from AI data centers. Tech giants like Google, Amazon, and Microsoft have signed deals for nuclear-powered facilities, while governments in the US, China, Japan, the UK, and others commit to new reactor builds and life extensions.The World Nuclear Association forecasts reactor uranium requirements at ~68,900 metric tons in 2025, rising 28% by 2030 and more than doubling to over 150,000 metric tons by 2040 (potentially 204,000+ in high-growth scenarios). This creates a long-term demand pull that outpaces current production.Constrained Supply and Production ChallengesPrimary uranium production struggles to ramp up after a decade of underinvestment post-Fukushima. Major producers face setbacks:

- Kazakhstan’s Kazatomprom (world’s largest, ~40% of supply) → cut 2025–2026 guidance due to sulfuric acid shortages.

- Canada’s Cameco → reduced output targets amid mine delays.

- Other issues include geopolitical risks (e.g., Russian enrichment restrictions, Niger disruptions).

Secondary supplies (e.g., stockpiles, underfeeding) are depleting, with forecasts showing market deficits averaging ~6% through 2030, deepening a cumulative shortfall potentially reaching 32% (1,914 million lbs) from 2025–2045.Geopolitical and Policy SupportBans/restrictions on Russian uranium (supplying ~11–12% of US needs historically) and enriched product exports force Western utilities to secure alternative sources. US policies under recent administrations include expedited reactor approvals, domestic production incentives, and partnerships (e.g., Cameco-Westinghouse). These factors tighten the market further.Market Dynamics and Price IncentivesUtilities have delayed aggressive long-term contracting in 2025 amid volatility, but pent-up demand is building. Long-term contract prices (a better indicator of fundamentals) have held firm around $80–$86/lb, signaling producer discipline. Higher prices—often cited at $90–$100+/lb—are needed to incentivize new mines, which take 10–15+ years to develop.Analyst consensus (e.g., Bank of America, Sprott, Goldman Sachs) points to prices rebounding to $90–$100/lb by mid/end-2025 or into 2026, with upside to $135+ possible if contracting accelerates. While short-term volatility persists (e.g., from trader activity or policy shifts), the multi-year bull case remains intact, positioning uranium as a key commodity in the energy transition.

END

Silver lease rates for Shanghai and London this morning

from Robert Lambourne: London at 8.0% and Shanghai 6.3%

| Robert Lambourne | 9:09 AM (3 minutes ago) | ||

| to me, Chris | |||

Harvey,

Thanks for your report.

Silver lease rates in London remain unchanged at c8% according to the AI report received just now. So rates remain elevated.

Shanghai implied lease rates were also unchanged at c6.3%.

Shanghai is open all over Christmas and only closes on 1 and 2 January although the official calendar is still not published. So things might be quite volatile this holiday season, especially if some of the chatter about the USA declaring war on Venezuela happens. My understanding is that Congress would have to agree before such a declaration could be made, but with the markets already volatile it seems this chatter is bound to affect sentiment.

No wonder prices of gold and silver are firm.

Hope you and your family have a great time and equally so for Chris and his family.

We are definitely living in interesting times.

Best wishes,

Bob

SILVER

AI GENERATED:

ASIA RESULTS; TUESDAY DEC 23

SHANGHAI CLOSED UP 2.61 POINTS OR 0.07%

//Hang Seng CLOSED DOWN 27.63 PTS OR 0.11%

// Nikkei CLOSED UP 28.61 PTS OR 0.06% //Australia’s all ordinaries CLOSED UP 1.15%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.0281

/ OFFSHORE CLOSED UP AT 7.0172/ Oil UP TO 58.01 dollars per barrel for WTI and BRENT UP TO 62.06 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP TO 7.0281 OFFSHORE YUAN TRADING UP TO 7.0172:/ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.0281

OFFSHORE YUAN: UP TO 7.0172

HANG SENG CLOSED DOWN 27.65 PTS OR 0.11%

2. Nikkei closed UP 28.61 PTS OR 0.06%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 97.61 /// EURO RISES TO 1.1788 UP 26 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +2.036 // DOWN 4 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.91…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.438 UP 1/3 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP/JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.875/ Italian 10 Yr bond yield DOWN to 3.522 SPAIN 10 YR BOND YIELD DOWN TO 3.297

3i Greek 10 year bond yield DOWN TO 3.481

3j Gold at $4479.80 Silver at: 69.49 1 am est) SILVER NEXT RESISTANCE LEVEL AT $70.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 38/100 roubles/dollar; ROUBLE AT 79.41

3m oil (WTI) into the 58 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.91 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.034% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.438 UP 1/3 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7874 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9383 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.164 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.814 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.497 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 42.83 UP 1 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.507 DOWN 3 PTS

30 YR UK BOND YIELD: 5.239 DOWN 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.473 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.988 DOWN 1 BASIS PTS.

1a New York OPENING REPORT

Futures Flat Ahead Of Final Macro Data Dump Of 2025

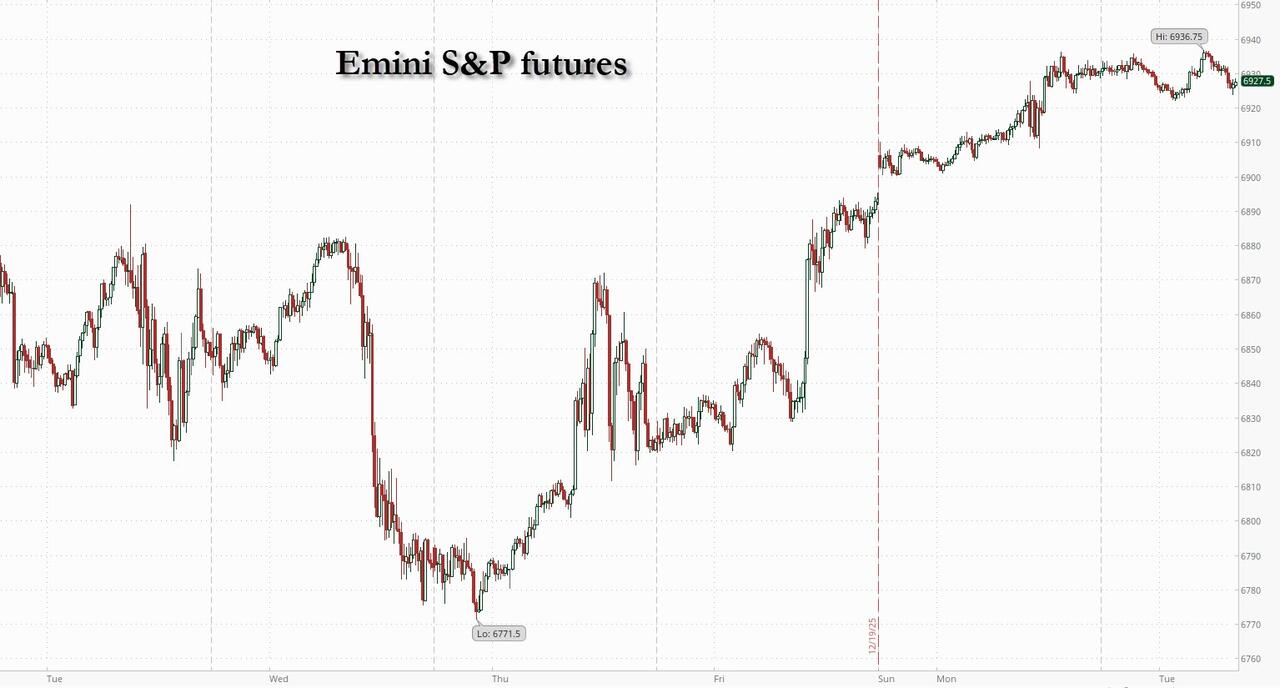

Tuesday, Dec 23, 2025 – 08:29 AM

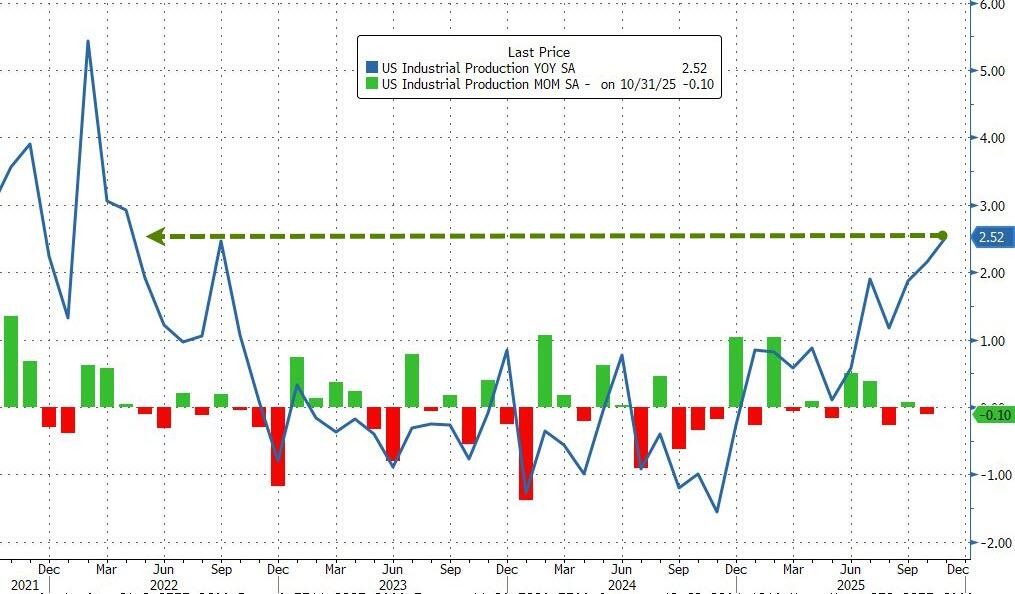

US equity futures are flat, pointing to a muted open off the overnight session highs on the last full trading session before Christmas, as traders await the last remaining data sets of 2025 to see whether they could materially change expectations for Federal Reserve interest-rate cuts. As of 8:0am ET, the S&P 500 is little changed after a three-day rally that has pushed the benchmark within reach of a new all-time high; Nasdaq futures are down 0.1% with Mag 7 names mixed. European stocks are buoyed by a 7% surge in the shares of Novo Nordisk after the Danish firm won US approval to sell a pill version of its obesity drug Wegovy. US Treasuries steadied after days of losses, with the 10-year yield declining two basis points to 4.15%. The dollar fell to the lowest level since October. Gold extended its record-breaking run, setting sights on $4,500 an ounce. Copper rose past $12,000 a ton for the first time. Bitcoin fell again, failing to stage even a modest rebound. The US calendar includes ADP weekly employment change (8:15am), 3Q GDP (8:30am), November industrial production (9:15am), December Richmond Fed manufacturing index, consumer confidence (10am).

In premarket trading, Mag 7 stocks are mixed: (Tesla +0.4%, Alphabet is little changed, Microsoft +0.07%, Apple -0.05%, Amazon -0.1%, Meta is little changed, Nvidia -0.4%)

- Gold, silver and copper mining and royalty stocks climb as the metals continued to hit record highs amid rising geopolitical tensions. Barrick Mining (B) rises 1% while Hudbay Minerals (HBM) gains 1%.

- Invivyd (IVVD) climbs 1% after the FDA granted a fast track designation for the biotech’s investigational vaccine-alternative monoclonal antibody candidate for Covid prevention in individuals with underlying risk factors for severe Covid.

- Sable Offshore Corp. (SOC) soars 25% after the company said that the US Department of Transportation Pipeline and Hazardous Materials Safety Administration approved the firm’s Las Flores pipeline restart plan.

- Zim Integrated Shipping Services (ZIM) climbs 8% after the company said it is evaluating proposals from multiple potential buyers. The review of strategic alternatives is in advanced stages.

In corporate news, department stores group Saks, facing limited options ahead of a more than $100 million debt payment due at the end of this month, is considering Chapter 11 bankruptcy as a last resort, according to people with knowledge of the situation. Johnson & Johnson was ordered to pay about $1.56 billion to a Maryland woman who blamed the company’s talc-based baby powder for causing her asbestos-linked cancer, the largest such jury verdict for an individual in 15 years of litigation. And Nvidia’s biggest Southeast Asian chip customer is facing a smuggling investigation.

The latest three-day rally pushed US stocks fractionally into positive territory for the month after a turbulent start to December. Preserving those gains until the end of December would extend this winning streak to an eighth month, the longest such run since 2018.

Meanwhile, volatility is collapsing. With the VIX index at 14.11, implied volatility for US equities over the coming 30 days is near the lowest in more than a year. That reflects enduring investor optimism around strong earnings growth, slowing inflation and a soft landing for the economy.

“Volatility is sitting at the lows of the year, while credit spreads are among the most compressed we’ve seen in decades,” said Alberto Tocchio, portfolio manager at Kairos Partners. “That dynamic is helping sustain the current market bonanza, especially in an environment where trading volumes are falling sharply and many discretionary players are already on the sidelines.”

The VIX may be snoozing around a 12-month low, but investors added new short bets across US stock futures last week, leaving net positioning near neutral levels, according to Citigroup strategists. Exposure to the Russell 2000 index of small caps is now bearish.

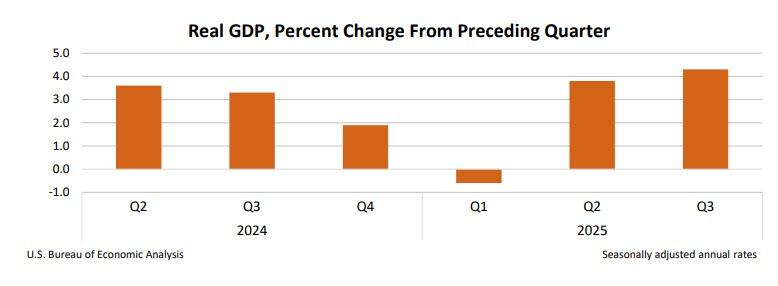

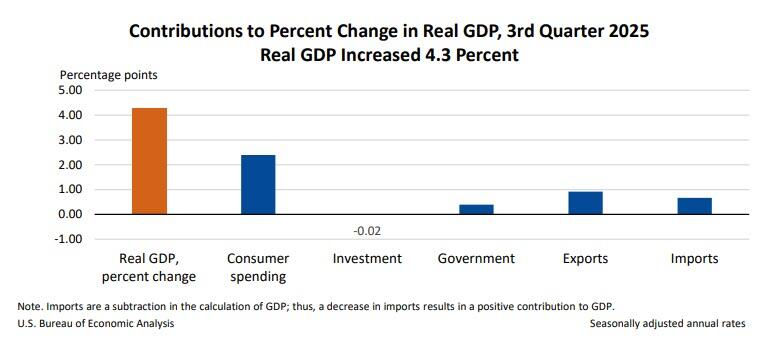

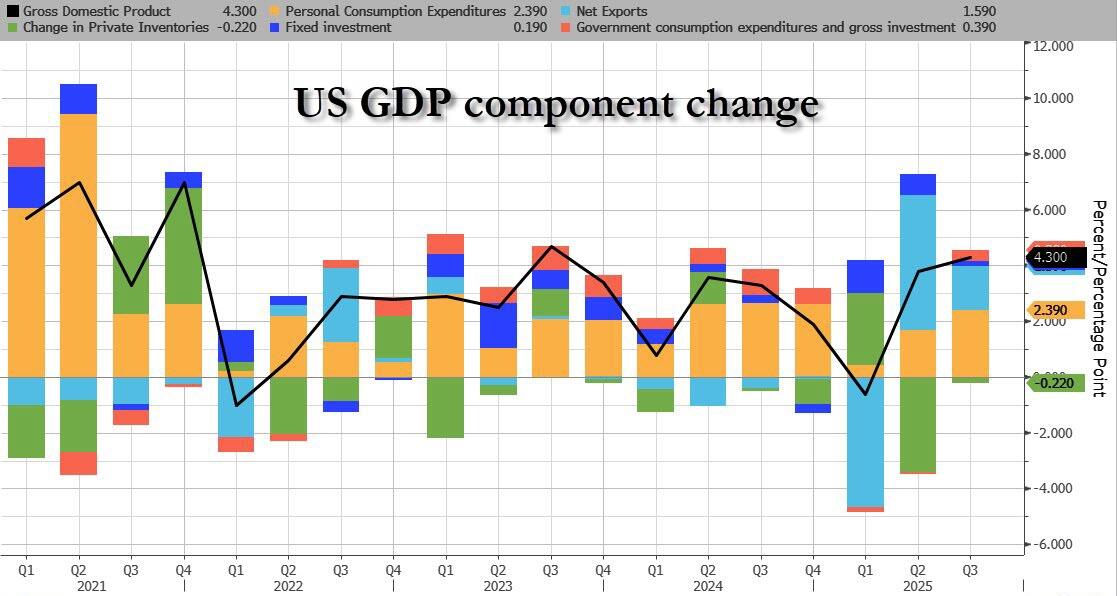

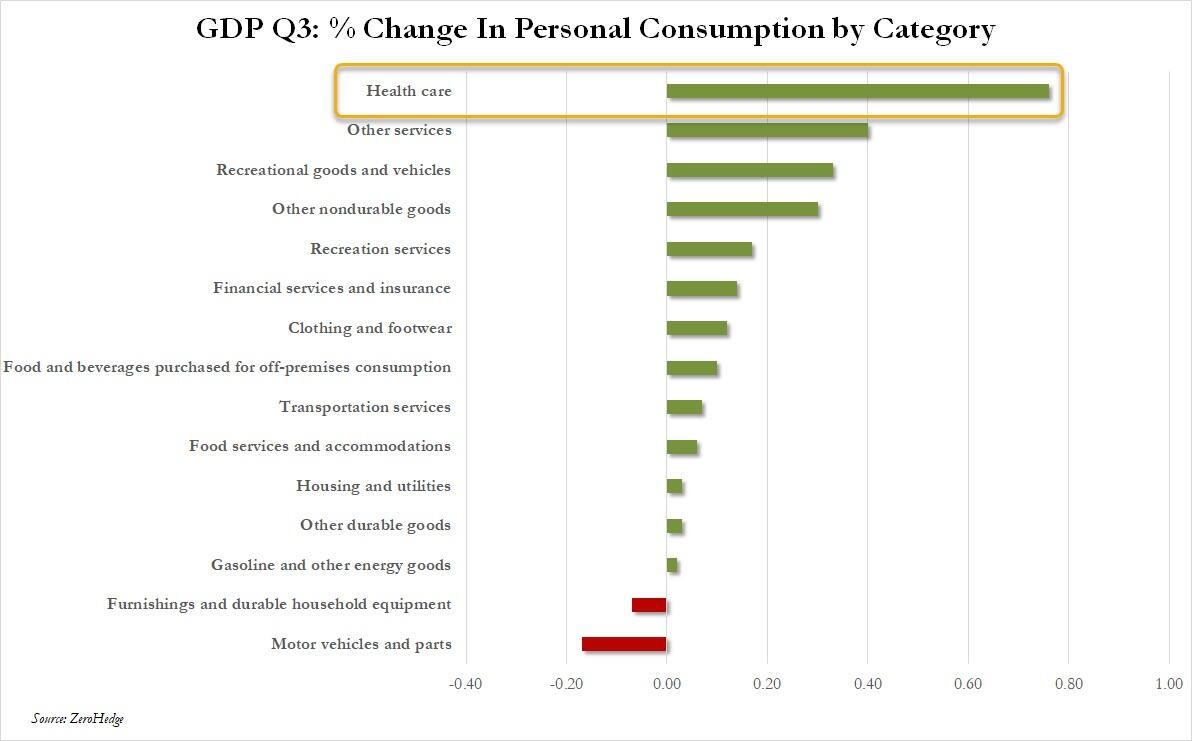

While Tuesday’s delayed third-quarter US gross domestic product print will likely be too dated to offer a clear read on current conditions, traders will also focus on consumer data after November showed a sharp slump in confidence.

In Europe, the Stoxx 600 edges up 0.2% to touch a new all time high with the health care sector leading gains. Novo Nordisk shares rally after the Danish drugmaker won approval to sell a pill version of its blockbuster obesity shot Wegovy in the US. Meanwhile, banks underperform. Here are some of the biggest movers on Tuesday:

- Novo Nordisk shares rise as much as 7.9%, the most since August, after the Danish drugmaker won approval to sell a pill version of its blockbuster obesity shot Wegovy in the US.

- SIG Group shares gain as much as 6.8%, the most in over a month, after the Swiss food packaging maker disclosed that Swedish activist investor Cevian Capital acquired a 3.1% stake.

Asian stocks were on course to advance for a third day, helped by gains in Japan amid expectations for further interest rate hikes. The MSCI Asia Pacific Index rose as much as 0.7%, with TSMC and Sony Group among the major contributors to the climb. Equities gained in Vietnam, Taiwan and Australia, while those in Indonesia fell. Speculation that the Bank of Japan may raise borrowing costs even more buoyed Japan’s financial stocks. Analysts said the yen’s continued weakness remains a tailwind for equities, even though the currency gained slightly overnight following comments by the finance minister. The onshore benchmark CSI 300 Index climbed 0.2%, despite a downgrade by Citi on Chinese equities to neutral from overweight on less favorable earnings revisions and a lackluster macro outlook.

In FX, the Bloomberg Dollar Spot Index is down 0.4%, falling for a second day and trading at the lowest since early October. The kiwi has overtaken the yen as the G-10 outperformer, rising 0.8% against the greenback. The yen is up 0.7%, dragging USD/JPY back below 156 after another round of jawboning from Japan’s Finance Minister. The Hungarian forint falls 0.2% after Economy Minister Nagy renewed his calls for lower interest rates.

Those moves came as the dollar headed for its weakest annual performance in eight years, with the options market signaling that traders are bracing for further losses. The currency is down 8.3% this year, on track for its biggest slide since 2017. Another modest dip would mark its worst year in at least two decades. Options pricing has also turned more negative, with so-called risk reversals, which track positioning and sentiment, showing options traders are the most bearish in three months.

“The structural drivers of US dollar weakness remain intact,” wrote Patrick Brenner, chief investment officer of multi-asset at Schroders Plc. “Institutional credibility continues to erode, fiscal deficits are widening, and global reserve managers remain steady buyers of gold rather than US dollar assets.”

In rates, treasuries advance, pushing US 10-year yields down 2 bps to 4.14%. European government bonds outperform.US yields richer by 1bp to 3bp across the curve in a bull flattening move, tightening 2s10s and 5s30s spreads by 1bp and 1.2bp on the day. Treasury 10-year yields trade around 4.14%, richer by 2.5bp on the day with bunds and gilts outperforming by an additional 1.5bp and 2bp in the sector. The Treasury is selling $70 billion 5-year notes at 1pm New York, with this week’s issuance concluding with $44 billion 7-year notes Wednesday. Ahead of today’s sale, the WI 5-year yield is about 3.705% which is ~14bp cheaper than the November stop-out

In commodities, gold and silver rise 0.9% each, having notched fresh record highs earlier. Copper also hits a record above $12,000 a ton. Brent was near $62 a barrel after rising about 5% over the previous four sessions as the US continued its blockade of crude shipments from Venezuela.Bitcoin falls 0.5%.

Today’s economic calendar includes ADP weekly employment change (8:15am), 3Q GDP (8:30am), November industrial production (9:15am), December Richmond Fed manufacturing index, consumer confidence (10am

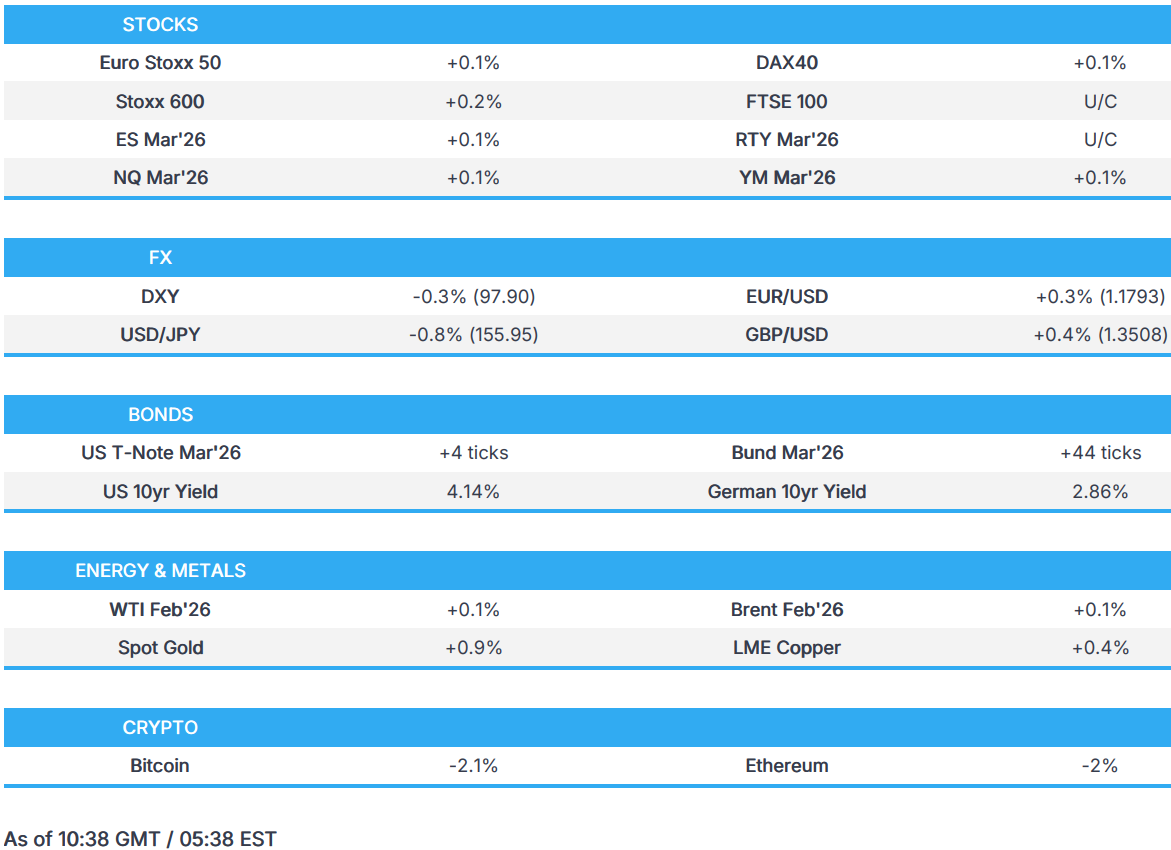

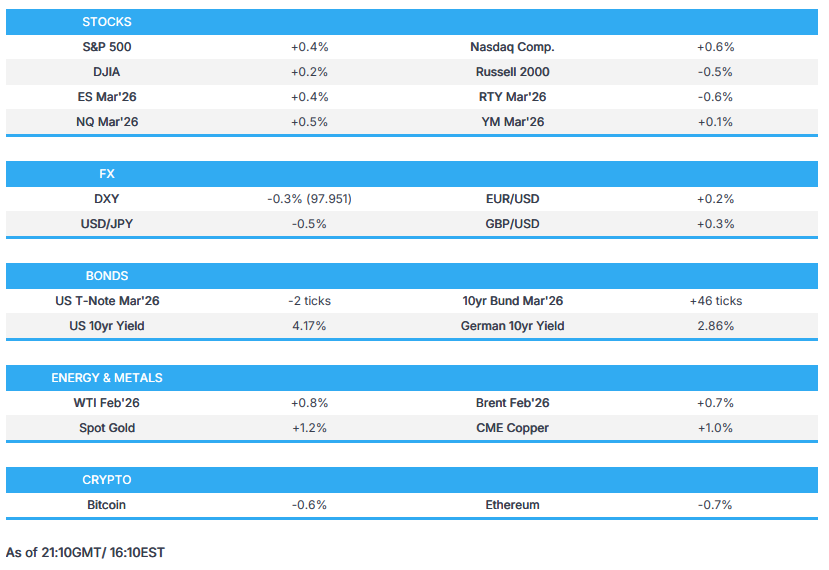

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini little changed

- Russell 2000 mini little changed

- Stoxx Europe 600 +0.2%

- DAX +0.2%

- CAC 40 -0.1%

- 10-year Treasury yield -2 basis points at 4.15%

- VIX little changed at 14.04

- Bloomberg Dollar Index -0.4% at 1201.58

- euro +0.3% at $1.1796

- WTI crude little changed at $58.03/barrel

Top Overnight News

- Pill Version of Wegovy Is Approved for Use in the US: WSJ

- Japan issues sternest intervention warning, says yen deviating from fundamentals: RTRS

- China’s Sprint for Tech Dominance Can’t Hide an Economy Full of Holes: WSJ

- Car Payments Now Average More Than $750 a Month. Enter the 100-Month Loan: WSJ

- Copper Hits $12,000 for First Time as Tariff Trade Upends Market: BBG

- Silver rises above $70/oz for the first time ever, gold rises to record $4500

- Russian air attack on Ukraine kills three and sparks sweeping outages: RTRS

- Ukraine’s Zelenskiy says several draft documents ready after Miami talks: RTRS

- South Africans dragged into Russia’s war in Ukraine dig trenches, dodge bullets: RTRS

- Russian Oil Stuck at Sea Booms as Tanker Logjams in Asia Expand: BBG

- Trump is mulling giving 775 acres of federal wildlife refuge to SpaceX: NYT.

- DOJ Releases Fresh Tranche of Epstein Files as Pressure Mounts: BBG

- A Small Nebraska Town Is Reeling From the Exit of Meatpacking Giant Tyson: WSJ

- Retail investors to have more sway over Wall Street after record year: RTRS

- The AI Boom Is Making Real-Estate Investors Rich—and Exposing Them to Risk: WSJ

- Trump’s First-Term Trust Buster Is Now Working to Get Paramount Its Deal: WSJ

A more detailed look at global markets courtesy of Newsquawk

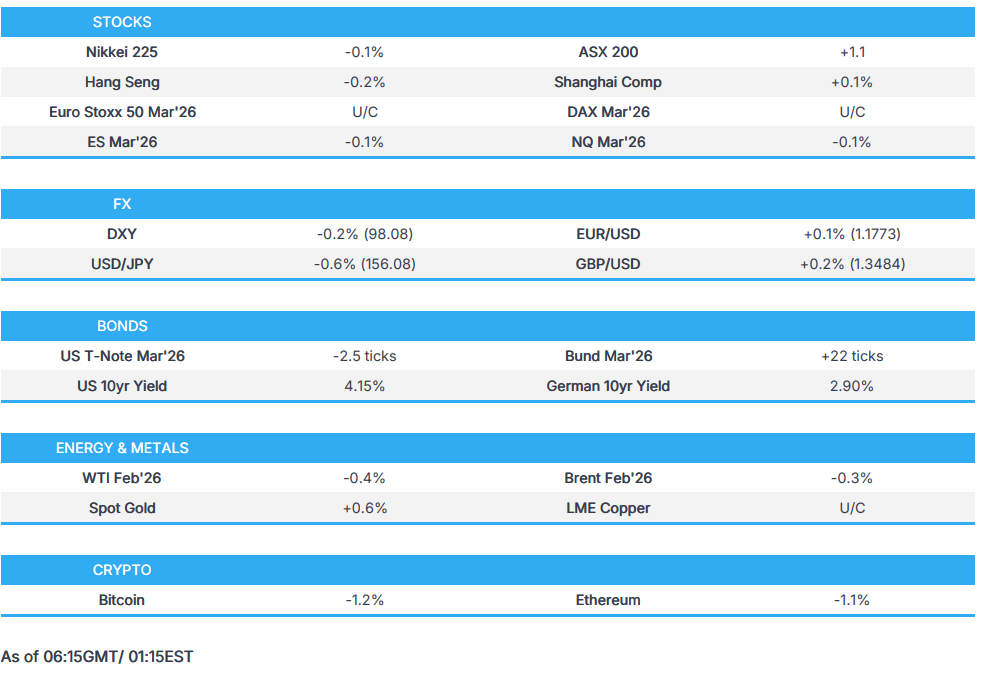

APAC stocks eventually traded mixed after initially taking their cue from Wall Street, although volumes and news flow remained subdued as markets wound down for the holiday period. ASX 200 was underpinned by strength in gold miners after the yellow metal printed a fresh all-time high near USD 4,500/oz, supported by a softer USD and ongoing geopolitical tensions. Nikkei 225 initially saw shallower gains than peers as a firmer yen, following official jawboning, capped upside for the index, whilst further gains in the JPY later took the index into the red. KOSPI extended its tech-led rally, with Samsung Electronics shares pushing toward near all-time highs. Hang Seng and Shanghai Comp initially tracked the broader risk tone, while fresh region-specific catalysts remained scarce. Hang Seng later gave up earlier gains.

Top Asian News

- Japanese Finance Minister Katayama declines to comment on forex levels or interest rates, and said Japan will take appropriate action and reiterates they have a “free hand” to respond to excessive moves in the JPY. FX moves after the BoJ press conference are speculative and not reflecting fundamentals. The market has stabilised somewhat since yesterday.

European bourses are mixed, with macro newsflow light. On the micro side, Novo Nordisk (+6.7%) said its oral Wegovy pill has been approved in the US for weight management after showing 16.6% weight loss in the OASIS 4 trial, and it plans a US launch in January 2026. European sectors have opened mixed with a slight positive bias. Health Care (+1.1%), to no surprise, leads due to gains in Novo Nordisk (+6.7%) after US approval of its weight-management drug. Utilities (+0.4%) and Food, Beverage and Tobacco (+0.4%) are also near the top, however, this is likely a rebound from yesterday’s underperformance. Banks (-0.3%), Consumer Products & Services (-0.3%) and Construction (-0.2%) lag, with little fresh newsflow driving moves.

Top European News

- EU is preparing checks on imported plastics and other measures to shore up its recycling industry, according to FT.

- European Car Sales +2.4% to 1.08mln vehicles in November, according to Bloomberg citing ACEA.

- Novo Nordisk (NOVOB DC) said Wegovy pill is approved in the US as the first oral GLP-1 treatment for weight management after showing 16.6% weight loss in the Oasis 4 trial, and said it plans to launch the drug in the US in January 2026. US-listed NOVO shares +5% after market. Eli Lilly -1.2% after market.

- US President Trump said he told French President Macron that France has to raise its drug prices.

Central Banks

- RBA Minutes: Board discussed whether a rate increase might be needed at some point in 2026; holding the cash rate steady for some time could be sufficient to keep the economy in balance. October CPI suggested a risk that Q4 inflation could also be higher than forecast. The board discussed whether a rate increase might be needed at some point in 2026. Recent data suggested risks to inflation had lifted to the upside. The board judged it was too early to know whether the rise in inflation would prove persistent. The board said it would take a little longer to assess the persistence of inflation. Holding the cash rate steady for some time could be sufficient to keep the economy in balance. Policy would be assessed at future meetings, with Q4 inflation data available before the February meeting. Some board members felt conditions were no longer restrictive, while others felt they were a little restrictive. The impact of the recent rise in bond yields on financial conditions needed to be assessed. The economy was operating with excess demand and it was not clear if financial conditions were tight enough. The labour market was judged to still be a little tight, with the output gap positive. The full impact of policy easing earlier in the year was yet to be felt. Measures of capacity utilisation pointed to supply constraints. Little immediate action in AUD or ASX 200.

FX

- DXY is lower and trades at the bottom end of a 97.88 to 98.23 range; really not much driving things for the USD recently, with newsflow exceptionally light, but perhaps facilitated by a strong JPY (see below). Nonetheless, traders will keep a keen eye out for Q3 GDP Advance/PCE, as well as Durable Goods (Oct), due at the same time.

- JPY is amongst the outperformers, with the strength seemingly a continuation of the price action seen following fresh jawboning from Finance Minister Katayama; as a reminder, she said that they have a “free hand” to take bold action in the FX market if needed. USD/JPY drifted lower from an overnight high of 157.07, down below the 156.00 mark, where the pair currently resides.

- Antipodeans also gained throughout overnight trade and into the European session, boosted by ongoing strength in metals prices (XAU now eyeing USD 4.5k/oz to the upside). Earlier, the Aussie showed little reaction to the RBA minutes, which indicated the Board debated whether a rate increase might be required at some point in 2026. Elsewhere, for the Kiwi specifically, NZD/USD breached 0.58 to the upside, which allowed the pair extend beyond the level, which can explain some of the outperformance this morning.

- The GBP and EUR are steady vs the broadly weaker USD. Really not much driving things for either at the moment; the single currency really only has geopolitical updates to digest heading into the Christmas holidays. For Cable, the pair extended beyond the 1.3500 mark to make a peak of 1.3518; the next level to the upside includes the October 1 high at 1.3527.

Fixed Income

- 10yr JGB futures outperformed, firmer by over 40 ticks at best, while the yen simultaneously reversed its early-week weakness following verbal jawboning from Japanese Finance Minister Katayama. JGB futures then rose further after Japanese PM Takaichi said Japan’s national debt is still high, and rejected any “irresponsible bond issuance or tax cuts”, via a Nikkei interview.

- USTs follow JGBs higher, with a lack of domestic newsflow helping things for the benchmark. Currently trading higher by a handful of ticks, and towards the upper end of a 112-11+ to 112-15+ range. Ahead, focus turns to some key US data points, which include US GDP Advance/PCE (Q3) and Durable Goods.

- Bunds, Gilts and OATs also follow suit. For the latter, OATs remain in focus after yesterday’s cabinet meeting made the use of Article 49.3 more likely. For the near-term fiscal needs, the Assembly and Senate are set to finish debating and then adopt text to allow the government to continue financing basic public services into early-2026, despite the absence of a 2026 budget deal. A point that has contributed to OAT strength, as the benchmark marginally outmuscles Bunds, causing the OAT-Bund 10yr yield spread to probe 70bps to the downside.

- China’s Finance Ministry expects aggregate government bond issuance to remain “elevated” in 2026, according to Reuters citing sources.

Commodities

- WTI and Brent chop around USD 58/bbl and USD 62/bbl, respectively, in tight ranges as crude benchmarks consolidate following Monday’s bid higher. Geopolitics has resurfaced in recent sessions as the near-term driver for crude prices, with tensions between the US and Venezuela rising and a potential escalation between Israel and Iran. However, a lack of updates throughout the APAC session has led to a muted start to Tuesday’s session.

- Spot XAU has followed on from Monday’s trend, peaking just shy of USD 4500/oz as the European morning gets underway, with rising geopolitical tensions acting as a new driver for the yellow metal. The recent US-Venezuela developments, specifically the blockaded oil tankers, have urged investors to look for safer places to place their investments.

- 3M LME Copper traded muted in a tight c. USD 60/t band throughout APAC trade, seemingly not benefiting from the further extension in gold and silver prices. As the European session gets underway, the red metal lifted as the positive risk tone in equities fed through into copper. Thus far, 3M LME Copper trades just shy of the ATH formed in Monday’s session, currently at USD 11.98k/t.

- China crude steel output in November 69.6mln tonnes, -10.9% Y/Y; global crude steel output in November 140.1mln tonnes, -4.6% Y/Y, via WorldSteel.

- Thai Central Bank Chief said there will be a set maximum trading volumes per major gold trader.

- Thailand’s Finance Minister is looking to implement a tax on gold trading online.

Geopolitics

- Russia’s Ryabkov said Russia and US held new round of talks on ‘Irritants’; main issues remain unresolved, via IFX. New round of contacts may take place in early spring.

- Polish Armed Forces said they have scrambled jets following Russian strikes on Ukraine.

- Russia is again attacking Ukraine’s energy infrastructure, according to Ukraine’s energy ministry.

- Russia conducts airstrikes on Ukrainian capital Kyiv, according to Ukraine’s military.

- Ukrainian President Zelensky said “Negotiations to end the war are “close to achieving a result”, according to Sky News Arabia.

- Russia’s Kremlin states Ukraine peace talks over the weekend did not achieve breakthrough.

- Russia needs to understand to what extent the US work with Ukraine and Europe on peace plan corresponds to spirit of earlier Putin-Trump Alaska summit, via TASS.

- Odesa regional governor said Russian forces launch new evening drone attack on Ukraine’s Odesa, damaging port facilities and civilian ship.

- “Israel’s Channel 12: Israel fears miscalculation with Iran, assures Washington that it will not take risks”, via Sky News Arabia.

US Event Calendar

- 8:30 am: US Oct. Durable Goods Orders, est. -1.5%, prior 0.5%

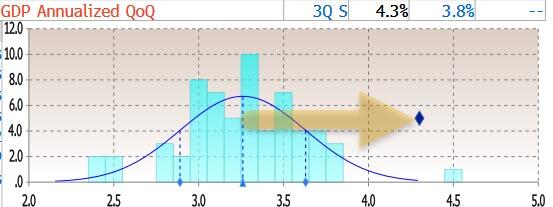

- 8:30 am: US 3Q GDP Annualized QoQ, est. 3.2%, prior 3.8%

- 8:30: US 3Q GDP Price Index, est. 2.7%, prior 2.1%

- 8:30 am: US 3Q Personal Consumption, est. 2.7%, prior 2.5%

- 10 am: US Dec. Richmond Fed Index, est. -10, prior -1

DB’s Jim Reid concludes the overnight wrap

This is the last EMR of 2025, before we resume normal service again on January 2. Many thanks for reading and for your interactions this year and wishing you all a Merry Christmas and a Happy New Year.