FINALIZED

access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,436.900000000 USD

INTENT DATE: 01/05/2026 DELIVERY DATE: 01/07/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 35

190 H BMO CAPITAL MARKETS 100

332 H STANDARD CHARTERED B 15

363 H WELLS FARGO SECURITI 248

435 H SCOTIA CAPITAL (USA) 49

624 H BOFA SECURITIES 469

661 C JP MORGAN SECURITIES 253

686 C STONEX FINANCIAL INC 2 5

690 C ABN AMRO CLR USA LLC 2

737 C ADVANTAGE FUTURES 2 3

880 H CITIGROUP 35

905 C ADM 3 1

TOTAL: 611 611

MONTH TO DATE: 4,860

JPMORGAN STOPPED 253/611

GOLD: NUMBER OF NOTICES FILED FOR JANUARY/2026: 611 CONTRACTs NOTICES FOR 61,100 OZ or 1.900 TONNES

total notices so far: 4860 contracts for 486,000 OR 15.116 tonnes)

SILVER NOTICES:951 NOTICE(S) FILED FOR 4.755 MILLION OZ OZ/

total number of notices filed so far this month : 4647 CONTRACTS (NOTICES) for 22.755 million oz

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 2.055 MILLION OZ QUEUE JUMP//NEW STANDING ADVANCES TO 25.255 MILLION OZ//

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 8.055 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 2.025 MILLION OZ QUEUE JUMP//STANDING ADVANCES TO 25.255 MILLION OZ//

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1335TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR HUGE QUEUE JUMP OF 1.222 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 3.766 TONNES//NEW TOTAL QUEUE JUMP 4.989 TONNES//NORMAL DELIVERY OF GOLD ADVANCES TO 17.0699 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 3.447 TONNES//NEW STANDING ADVANCES TO 20.5169 TONNES.

NEW STANDING FOR GOLD, JANUARY CONTRACT AT 20.5169 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 16.29 TONNES

SPREADING OPERATION

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE SIZED 1944 CONTRACTS OI TO 152.477 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 700 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 700 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1944 CONTRACTS AND ADD TO THE 700 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 2644 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $5.90 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 15.030 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $5.90

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS JAN 6/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 60.25 PTS OR 1.50%

//Hang Seng CLOSED UP 368.21 PTS OR 1.38%

// Nikkei CLOSED UP 681.20 PTS OR 1.31

//Australia’s all ordinaries CLOSED DOWN 0.57%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9840

/ OFFSHORE CLOSED DOWN AT 6.9797/ Oil UP TO 58.46 dollars per barrel for WTI and BRENT UP TO 62.04 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9840 OFFSHORE YUAN TRADING DOWN TO 6.9797/ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAK//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1871 CONTRACTS TO 480,541 OI DESPITE OUR HUMONGOUS GAIN IN PRICE OF $122.80 WITH RESPECT TO MONDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1589). WE HAD CONSIDERABLE T.A.S. LIQUIDATION MONDAY. IT SEEMS THAT THE SPECULATORS WENT MASSIVELY HUGE TO THE LONG SIDE WITH OUR FRBNY PROVIDING STILL THE MASSIVE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE .

YOU WILL NOTICE THAT THE COMEX OI IS NOW GAINING HUGELY FROM ITS LOW OI OF AROUND 418,000 TO NOW 480,823 AND NOW AMPLE ENOUGH FOR A RAID BY OUR BANKERS LIKE LAST MONDAY. FROM CHINA WE LEARN THAT THE GOLD LEASE RATE IS NOW AROUND ONE TO 2 %

WE THUS HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 561 CONTRACTS (OR 1.744 TONNES). THEN WE WERE NOTIFIED OF ZER0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS AND THEN ONE EARLY JANUARY: 3.446 TONNES)

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 39 TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WILL BE ADDED TO OUR DAILY TOTALS!! (3.447 TONNES)

DETAILS ON OUR NEW JANUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A TINY SIZED LOSS ON OUR TWO EXCHANGES OF 561 CONTRACTS DESPITE OUR HUMONGOUS GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH JANUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A STRONG T.A.S ISSUANCE CONTRACTS. THE CME NOTIFIES US THAT THEY HAVE ISSUED 2592 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE HUGE NUMBER OF T.A.S. ISSUANCES IN DECEMBER.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY 2026: INITIAL GOLD STANDING IS 13.785 TONNES TO WHICH WE ADD OUR NEWEST QUEUE JJUMP OF 1.222 TONNESS WHICH ADDED TO OUR ALL OTHER QUEUE JUMP OF 3.766 TONNES //NEW TOTAL QUEUE JUMP: 4/988 TONNES (NORMAL STANDING ADVANCES TO 17.0699 TONNES) TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 3.447 TONNNES/./NEW STANDING ADVANCES TO 20.5169 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 39+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 39 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. SO IT IS POSSIBLE/PROBABLE THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!!

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 39+ TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/DEC.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1310 CONTRACTS.

THAT IS A FAIR SIZED 1310 EFP CONTRACT WAS ISSUED: : /FEB 1310 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1310 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 39 TONNES

WE HAD :

- CONSIDERABLE LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + AND DID HAVE HUGE GOVERNMENT LIQUIDATION

- ZERO MONTH END SPREADERS LIQUIDATION!!. WILL NOT COMMENCE UNTIL THE END OF JANUARY..

T.A.S.SPREADER ISSUANCE//JANUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A STRONG SIZED 2592 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP MONDAY’S HUGE GAIN IN PRICE IN GOLD WITH A CORRESPONDING FAIR LOSS OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE.. (QUITE STRANGE)

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITIAL GOLD STANDING 13.785 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 1.222 TONNES TO ALLOTHER QUEUE JUMPS OF 3.766 TONNES/NEW TOTAL QUEUE JUMP 4.988/NEW NORMAL STANDING INCREASES TO 17.0699 AND THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 3.447 TONNES//NEW STANDING ADVANCES TO 20.5169 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING JANUARY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $122.80/ /)

WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX// WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL MONDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR JANUARY IN AN OFF MONTH. THE COMEX IS ONE BIG MESS!!

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. NOW JANUARY:

AMOUNT STANDING FOR GOLD INITIALLY 13.7516 TONNES TO WHICH WE ADD OUR NEW QUEUE JUMP OF 1.222 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS POF 3.766 TONNES: NEW QUEUE JUMPING FOR JAN: 4.988 //NEW NORMAL STANDING ADVANCES TO 17.0699 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 3.447 TONNES. NEW STANDING ADVANCES TO 20.5169 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $122.80

WE HAD A SMALL 282 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .

INITIAL GOLD COMEX

JAN 6

JAN 2026 CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 0- ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 611 notice(s) 61100 OZ 1.900 TONNES OF GOLD |

| No of oz to be served (notices) | 628 contracts 62800 OZ 1.953 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4860 notices 486,000 0z 15.116 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

0 ENTRIES

customer withdrawals:

0 ENTRIES

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 0

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF JANUARY STANDS AT 1239 CONTRACTS FOR A GAIN OF 55 CONTRACTS.

WE HAD 338 NOTICES FILED ON MONDAY, SO WE GAINED 393 CONTRACTS OR 39300 OZ (1.222 TONNES) OF A QUEUE JUMP.

FEB LOST 9622 CONTRACTS DOWN TO 321,446 CONTRACTS

MARCH GAINED 170 CONTRACTS UP TO 2802

We had 611 contracts filed for today representing 61,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 611 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 253 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JAN /2026. contract month, we take the total number of notices filed so far for the month (4860 ) to which we add the difference between the open interest for the front month of DEC ( 1239 CONTRACTS) minus the number of notices served upon today (611 x 100 oz per contract) equals 558,800OZ OR 17.0699 Tonnes of gold to which we add our first exchange for risk in January of 3.447 tonnes//new standing advances to 20.5169 tonnes

thus the INITIAL standings for gold for the JAN contract month: No of notices filed so far (4860 x 100 oz +we add the difference for front month of JAN (1229 OI} minus the number of notices served upon today (611)x 100 oz) which equals 558,800 OR 17.0699 TONNES plus our first exchange for risk of 3.447 tonnes//new standing advances to 20.5169 tonnes

new total of gold standing in JANUARY is 20.5169 tonnes

TOTAL COMEX GOLD STANDING FOR JANUARY ..: 20.5169 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume MONDAY confirmed 249,207 good

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,967,592.462 oz 61.20 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,403,451.805. oz

TOTAL REGISTERED GOLD 19,329,396.443 or 601.225 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,074,035.302 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,361.804oz ((REG GOLD- PLEDGED GOLD)=

540.025 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

JAN 6.2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of Brinks: 480,925.05 oz ii) Out of CNT 137,443.905 oz iii) Out of Delaware 1097.500 oz iv) Out of JPMorgan: 1,286.886.400 oz total withdrawal: 1,906,352.100 oz |

| Deposits to the Dealer Inventory | 2 ENTRIES i) Into Asahi: 531,249.600 oz ii) Into CNT 828,107.01 ooz total dealer deposit; 1,359,356.610 oz |

| Deposits to the Customer Inventory | 1 ENTRY i) Into CNT 236,463.930 OZ total deposit: 236,463.930 oz |

| No of oz served today (contracts) | 951 CONTRACT(S) ( 4.755 million OZ |

| No of oz to be served (notices) | 491 contracts (2.455 MILLION oz) |

| Total monthly oz silver served (contracts) | 4547 contracts 22.735 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

2 ENTRIES

i) Into Asahi: 531,249.600 oz

ii) Into CNT 828,107.01 ooz

total dealer deposit; 1,359,356.610 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRY

i) Into CNT 236,463.930 OZ

total deposit: 236,463.930 oz

withdrawals: customer side/eligible

4 entries

i) Out of Brinks: 480,925.05 oz

ii) Out of CNT 137,443.905 oz

iii) Out of Delaware 1097.500 oz

iv) Out of JPMorgan: 1,286.886.400 oz

total withdrawal: 1,906,352.100 oz

adjustments: 5// dealer to customer

i) Asahi 278,766.300 oz

ii) Brinks 171m314.860oz

iii) CNT 245,976,39 oz

iv) JPM: 179,489.460 oz

v) Out of Stonex: 5105.75 oz

total adjusted out of dealer to customer acct: 660,612.679

TOTAL REGISTERED SILVER: 127.186 MILLION OZ//.TOTAL REG + ELIGIBLE. 449.211Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF JANUARY /2026 OI: 1422 OPEN INTEREST CONTRACTS FOR A GAIN OF 255 CONTRACTS. WE HAD 150 NOTICES FILED ON MONDAY SO WE GAINED 405 CONTRACTS OR A STRONG 2.025 MILLION OZ QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND.

FEB GAINED 234 CONTRACTS UP TO 1920 CONTRACTS

MARCH GAINED 463 CONTRACTS UP TO 107,293

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 951 or 0.75 MILLION oz

CONFIRMED volume; ON MONDAY 152,074 huge//

AND NOW JANUARY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 4547 X5,000 oz = 22.735 MILLION oz

to which we add the difference between the open interest for the front month of JANUARY (1442) AND the number of notices served upon today (951 )x (5000 oz)

Thus the standings for silver for the JANUARY 2026 contract month: (4547) Notices served so far) x 5000 oz + OI for the front month of JAN(1442) minus number of notices served upon today (951)x 5000 oz equals silver standing for the JANUARY.contract month equating to 25.255 MILLION OZ

NORMAL STANDING: 25.255 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF JANUARY.

New total standing: 25.255 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 127.186. million oz of registered silver

JPMorgan as a percentage of total silver: 186.317/449.211million. 41.71%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

JAN 6/2026/WITH GOLD UP $47.00 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 19/WITH GOLD UP $22.20 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 18/WITH GOLD DOWN $9.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .85 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 17/WITH GOLD UP $39.45 TODAY/NO CHANGES IN GOLD AT THE GLD:// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 16/WITH GOLD DOWN $3.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 15/WITH GOLD UP $10.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 105.12 TONNES

DEC 12/WITH GOLD UP $14.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.83 TONNES

DEC 11/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 10/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 9/WITH GOLD UP $18.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.14 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1049.11 TONNES

DEC 8/WITH GOLD DOWN $23.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.33 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1050.25 TONNES

DEC 5/WITH GOLD UP $9.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 4.00 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.58 TONNES

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

DEC 3/WITH GOLD UP $14.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.71 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1048.30 TONNES

DEC 2/WITH GOLD DOWN $53.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.58 TONNES OF GOLD VAPOUR INTO THE GLD// /// ///INVENTORY RESTS AT 1050.01TONNES

DEC 1/WITH GOLD UP $22.75 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43TONNES

NOV 28/WITH GOLD UP $51.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1045.43 TONNES

NOV 26/WITH GOLD UP $25.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT PAPER DEPOSIT OF 4.57 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 25/WITH GOLD UP $46.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.57 TONNES

NOV 24/WITH GOLD UP $16.95 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1040.86 TONNES

NOV 21/WITH GOLD UP $18.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.00 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1039.43 TONNES

NOV 20/WITH GOLD DOWN $20.45 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1041.43 TONNES

GLD INVENTORY: 1065.13 TONNES, TONIGHTS TOTAL

SILVER

JAN 6/WITH SILVER UP $4.93 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2,961 MILLION OZ OUT OF THE SLV OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 17/WITH SILVER UP $2.93/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 16/WITH SILVER DOWN $.07/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 56.360 MILLION OZ //

DEC 15/WITH SILVER UP $1.62/SMALL CHANGES IN SILVER AT THE SLV: A SMALL DEPOSIT OF 635,000 INTO THE SLV. ./ :INVENTORY RESTS AT 517.720 MILLION OZ //

DEC 12/WITH SILVER DOWN $2.30/NO CHANGES IN SILVER AT THE SLV: ./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 11/WITH SILVER UP $3.52/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.537 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 9/WITH SILVER UP $2.41/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.179 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 510.828 MILLION OZ //

DEC 8/WITH SILVER DOWN $0.48/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 5.497 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 512.007 MILLION OZ //

DEC 5/WITH SILVER UP 0.39/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.083 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.448 MILLION OZ //

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

DEC 3/WITH SILVER UP $0.23/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 1.956 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 510.012 MILLION OZ //

DEC 2/WITH SILVER DOWN $0.65 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND FRAUDLUENT PAPER DEPOSIT OF 6.167 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 508.057 MILLION OZ //

DEC 1/WITH SILVER UP $2.21 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 907,000 OZ INTO THE SLV./ :INVENTORY RESTS AT 501.890 MILLION OZ //

NOV28/WITH SILVER UP $3.28 TODAY/NO CHANGES IN SILVER AT THE SLV:/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV26/WITH SILVER UP $1.86 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 2.267 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 500.983 MILLION OZ //

NOV25/WITH SILVER UP $0.69 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A MAMMOTH DEPOSIT OF 8.163 MILLION OZ INTO THE SLV/ :INVENTORY RESTS AT 498.716 MILLION OZ //THIS IS A FRAUDULENT TRANSACTION

NOV24/WITH SILVER UP $0.43 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 277,000, OZ OUT OF THE SLV/ :INVENTORY RESTS AT 490.553 MILLION OZ MILLION OZ

NOV21/WITH SILVER DOWN $0.53 TODAY/SMALL CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 635,000 OZ INTO THE SLV/ :INVENTORY RESTS AT 490.190 MILLION OZ MILLION OZ

NOV20/WITH SILVER DOWN $0.53 TODAY/NO CHANGES IN SILVER AT THE SLV: :INVENTORY RESTS AT 489.555 MILLION OZ MILLION OZ

CLOSING INVENTORY 525.730 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD.

3. CHRIS POWELL AND HIS GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 254

5. COMMODITY REPORT//:

COPPER

UBS: “Copper Is The Commodity Everyone Wants To Own”

Tuesday, Jan 06, 2026 – 11:25 AM

Goldman’s “circular melt-up” call and its recent upgrade to the 2026 London Metal Exchange (LME) copper price forecast have so far proven correct, as the industrial metal surged above $13,000 a ton with traders continuing to price in tighter global supply and a broader risk-on mood across metals.

Three-month LME copper futures rose as much as 3.1% to a record $13,387.50, surpassing the previous record high set just a day earlier. The move is driven by the risk that the Trump administration may impose tariffs on refined copper, prompting a multi-month surge in US inventory and draining supplies from major global markets.

“Copper extended its rally on Tuesday, with prices surging to a record $13,187 per ton, fuelled by a rush to ship the metal to the US amid tariff uncertainty and persistent supply disruptions,” UBS analyst Aditi Samajpati wrote in a brief note to clients earlier.

Samajpati continued, “The US premium has driven global inventory imbalances, with US stockpiles rising while the rest of the world faces tightening supplies. Speculative trading intensified as investors bet on further gains, supported by the metal’s critical role in energy transition and ongoing mine setbacks in Chile, Indonesia, and Congo.”

She added, “The rally is also part of a broader upswing in metals, with gold, silver, and platinum hitting new highs.”

In a separate note, UBS analyst Dan Major noted, “Net speculative positioning is elevated, and it is well known that copper is the commodity everyone wants to own.”

The prospect of US import curbs, combined with strong demand due to copper’s role in high-growth sectors such as data center buildouts and power grid upgrades, fueled a wave of optimistic calls late in 2025.

“Inventories used to act as a buffer, but now they’re locked in the US,” Li Xuezhi, head of research at Chaos Ternary Futures Co., recently told Bloomberg. “So the buffer is gone and everyone will have to scramble.”

Latest reporting:

- Goldman: $10,000 Is New Price Floor For Copper

- Copper Hits Record High; Goldman Warns A “Circular Melt-Up” Is Now Driving Global Market

- Goldman Upgrades Copper Price Forecast Weeks After Warning About “Circular Melt-Up”

“The logic behind this rally remains,” said Li. “We need to track the trend and not get fixated on absolute price levels.”

END

5B. COMMODITY REPORT//SILVER/SILVER LEASE RATES:/SILVER

SILVER COMMENTARIES

ASIA RESULTS; TUESDAY JAN 6/2026

SHANGHAI CLOSED UP 60.25 PTS OR 1.50%

//Hang Seng CLOSED UP 368.21 PTS OR 1.38%

// Nikkei CLOSED UP 681.20 PTS OR 1.31

//Australia’s all ordinaries CLOSED DOWN 0.57%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9840

/ OFFSHORE CLOSED DOWN AT 6.9797/ Oil UP TO 58.46 dollars per barrel for WTI and BRENT UP TO 62.04 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9840 OFFSHORE YUAN TRADING DOWN TO 6.9797/ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAK//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

END

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9840

OFFSHORE YUAN: DOWN TO 6.9797

HANG SENG CLOSED UP 363.21 PTS OR 1.38%

2. Nikkei closed UP 681.20 PTS OR 1.31%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 98.11 /// EURO FALLS TO 1.1713 DOWN 1 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.131// UP 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.43… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.497 UP 3 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.8614 Italian 10 Yr bond yield DOWN to 3.517 SPAIN 10 YR BOND YIELD DOWN TO 3.291

3i Greek 10 year bond yield DOWN TO 3.467

3j Gold at $4450.00 Silver at: 77.85 1 am est) SILVER NEXT RESISTANCE LEVEL AT $80.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 5 /100 roubles/dollar; ROUBLE AT 80.81

3m oil (WTI) into the 58 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.43 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.131% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.497 UP 3 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7925 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9827well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.180 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.874 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.467 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.03 UP 1 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.5160 UP 1 PTS

30 YR UK BOND YIELD: 5.258 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.421 DOWN 5 BASIS PTS

5 YR CANADA BOND YIELD: 2.945 DOWN 5 BASIS PTS.

1a New York OPENING REPORT

Global Stock Rally Fizzles, Futures Flat As Market Rotations Accelerate

Tuesday, Jan 06, 2026 – 08:36 AM

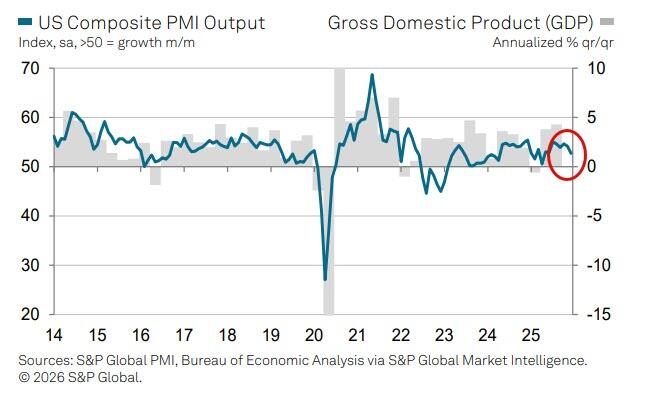

US equity futures are flat with small caps underperforming as geopolitics dominate headlines, including aftershocks from the Maduro seizure and a potential US/EU deal that provides a security guarantee for Ukraine potentially with American soldiers maintaining a presence in Ukraine. As of 8:00am ET, S&P futures are flat as a rotation into regional shares broadened and investors awaited fresh data to gauge the outlook for Federal Reserve interest rates; Nasdaq futures gain 0.2% even as Mag 7 names are weaker premarket ex-NVDA which is leading Semis higher after Jensen Huang’s CES presentation. Futures took a brief spill overnight just around 3am ET when China announced it would launch export controls on Japan, which is negative for heavy machinery; futures then promptly recovered. Defensives are leading Cyclicals ex-Energy. Bond yields are higher by 1-2bp with USD also bid. Major European markets are mixed with UK leading and France lagging. Asian stocks are off to their best start since 2012 with the MXAP up 3% YTD. Today’s US economic calendar includes December final S&P Global US services and composite PMIs at 9:45am. Scheduled Fed speakers include Barkin (8am) and Miran (8:30am)

In premarket trading Mag 7 names are mixed, with Nvidia gaining 0.6% as CEO Jensen Huang said the company’s much-anticipated Rubin data center processors are in production and customers will soon be able to try out the technology.(Alphabet +0.2%, Microsoft is flat, Amazon -0.08%, Meta +0.9%, Apple -0.3%, Tesla -0.6%).

- Aeva (AEVA) jumps 23% after the company announced that its 4D LiDAR technology has been selected for the Nvidia Drive Hyperion autonomous vehicle reference platform.

- Core Scientific (CORZ) climbs 4% as BTIG upgrades to buy as the dust settles following shareholder rejection in October of its acquisition by CoreWeave.

- Frontier Group (ULCC) falls 3% after BofA cut the recommendation on the airline to underperform, expecting cost challenges in 2026 as aircraft rental fees rise.

- Microchip (MCHP) rises 4% after the analog chipmaker’s net sales forecast for the third quarter beat the average analyst estimate. Analysts note that the strong sales numbers highlight broad-based recovery.

- Oculis (OCS) rises 8% after the drug developer said its experimental therapy, Privosegtor, was granted the FDA’s breakthrough therapy designation for the treatment of optic neuritis — inflammation of the eye nerve.

- OneStream Inc. (OS) soars 22% as buyout firm Hg is in advanced talks to acquire the financial software maker, according to people familiar with the matter.

- Vistra Corp. (VST) climbs 4% after agreeing to pay roughly $4 billion for 10 natural gas-fired power plants in the US Northeast and Texas to expand the electricity supplier’s generation capacity in fast-growing energy markets.

- Zeta Global (ZETA) rises 9% after the software company announced that it has entered a strategic collaboration with OpenAI to power conversational intelligence and agentic applications behind Athena by Zeta, its superintelligent agent built for enterprise marketing.

In other corporate news, AB InBev will reacquire a 49.9% stake in US metal plants from a consortium of investors for $3 billion. Electricity supplier Vistra agreed to pay roughly $4 billion for 10 natural gas-fired power plants in the US Northeast and Texas. Software company Zeta Global announced a strategic collaboration with OpenAI.

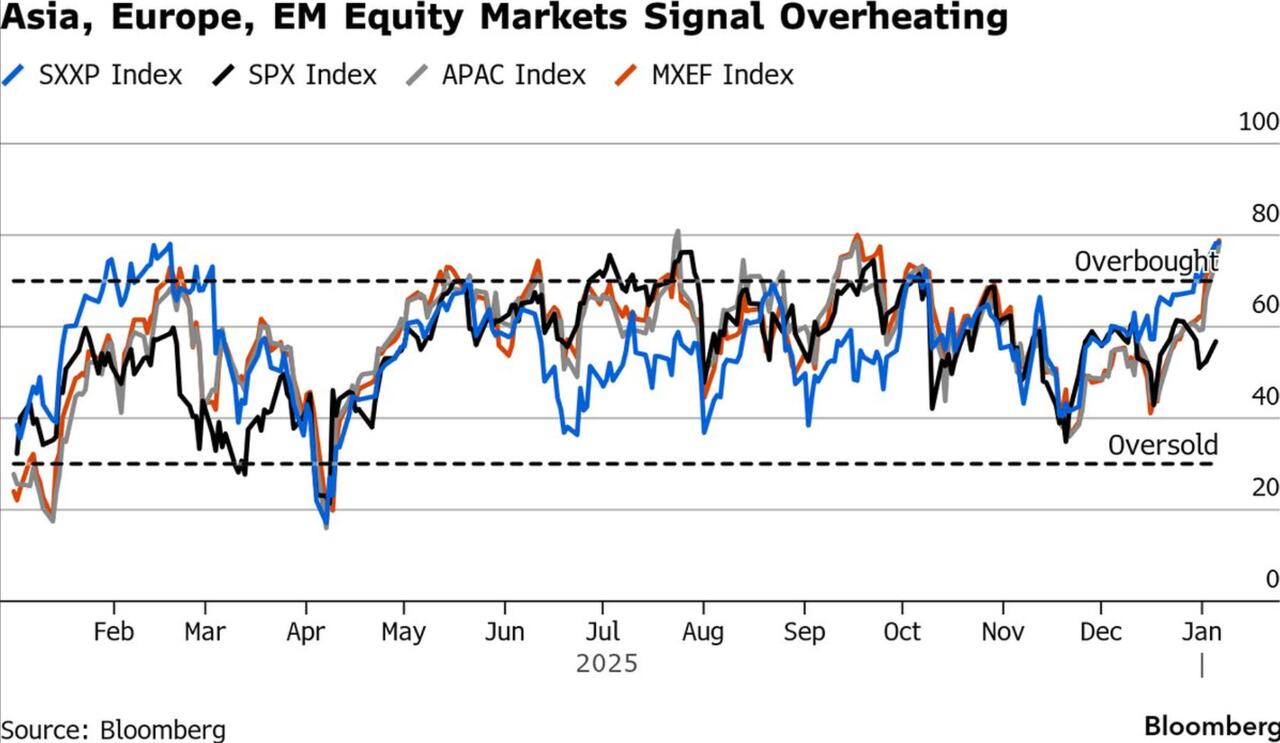

The New Year rally appears to be losing steam, despite renewed appetite for the AI trade and cyclicals over defensives. Some of the biggest action is in commodities, with an index of base metals surging to the highest since March 2022 and copper rising above $13,000 a ton for the first time, which needless to say, is and will be inflationary. At the same time, stocks in Asia surged, but as Bloomberg notes, are now getting dangerously overbought, along with markets in Europe and emerging markets. The S&P 500’s 14-day relative strength index also suggests that US stocks might have further room to run, in contrast with other regions that have surpassed levels typically seen as overbought. Macro and geopolitical risks are numerous, with Venezuela, Greenland and Taiwan all in the headlines today.

Stock investors have so far been largely unfazed by tensions in Venezuela, extending a three-year bull run that’s been fueled by demand for AI–linked shares. The next leg of the rally will depend in part on how quickly the Fed moves to further ease monetary policy, with business activity and jobs market data due this week to help shape rate expectations.

“We are waiting for data,” said Emilie Tetard, a cross-asset strategist at Natixis. “Before this data, as macro uncertainty is probably stronger in the US vs. the rest of the world, it’s a good time to put in place the diversification.”

Meanwhile, US oil producers such as Chevron Corp. and ConocoPhillips extended gains on President Donald Trump’s plans for the reconstruction of Venezuela’s crude industry.

The AI narrative is getting a boost from announcements at CES. AMD unveiled a new chip for corporate data centers, with CEO Lisa Su noting on AI that “we don’t have nearly enough compute for what we could possibly do.” Nvidia CEO Jensen Huang said the company’s highly-anticipated Rubin processors are on track for deployment by customers in the second half. “Demand is really high,” he said. And Intel’s comeback bid is relying on laptops shown at CES that are based on processors with a new design. As Bear Traps report Larry McDonald puts it, “the Pumpmaster is on Stage Again”: Nvidia CEO Huang keynote address confirmed that Vera Rubin is now in full production and is expected to propel Nvidia back into the position of undisputed technical leader. Jensen noted that Vera Rubin contains 6 separate, revolutionary chips, and in years past, each one would have been made by a separate company, but Nvidia does them all itself.

In the geopolitical sphere, Venezuela’s new acting president Delcy Rodríguez is seen as a choice that could stabilize Venezuela’s oil-based economy and facilitate American business. Elsewhere, Trump’s rationale for intervening in Venezuela is fueling concerns among European officials that they could soon face an existential dilemma over Greenland.

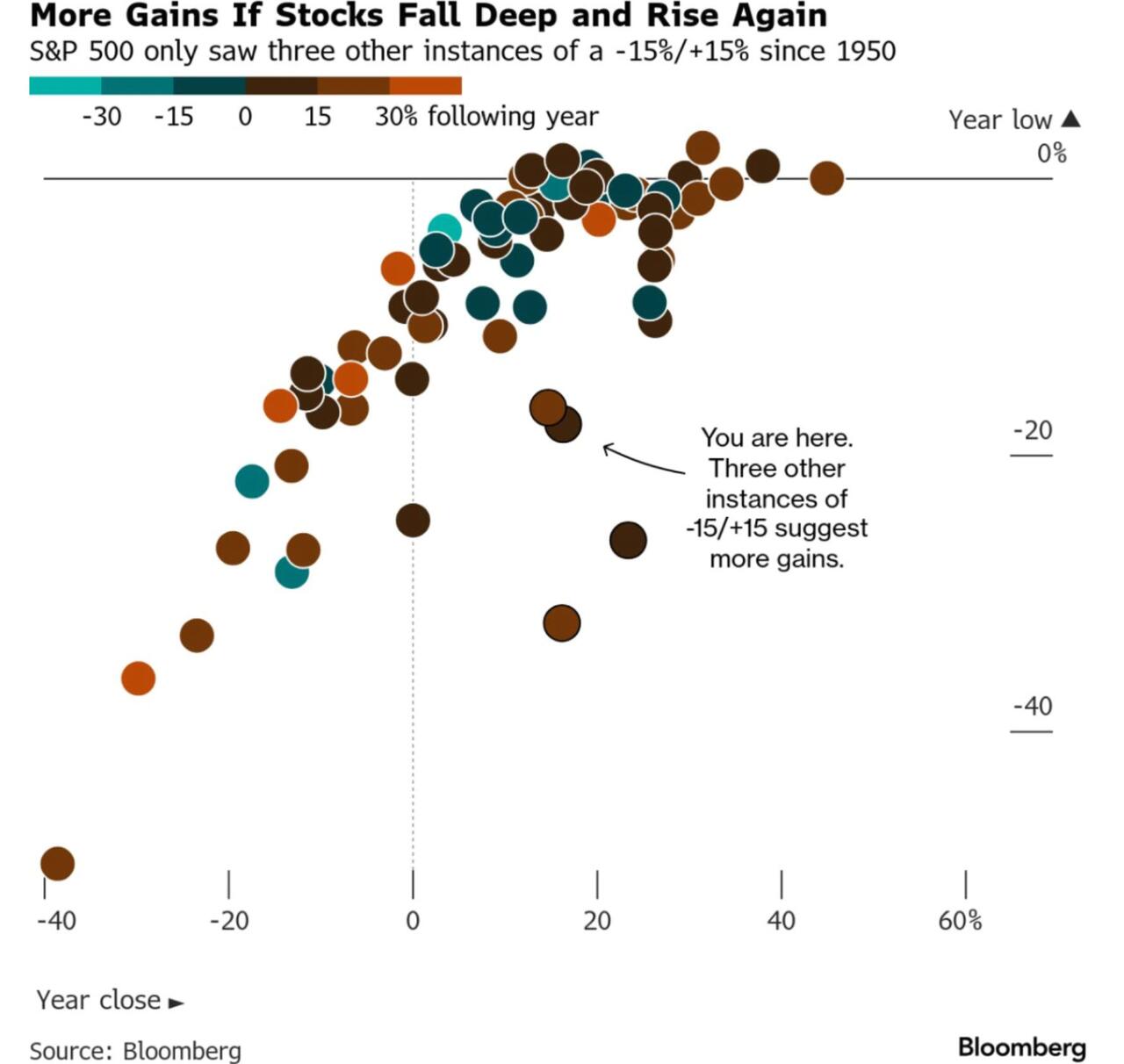

Elsewhere, the data may be on the side of bulls. According to Bloomberg, there have been just four years when the S&P 500 fell at least 15% and and still managed to achieve an annual advance of 15% or more. It happened in 1982, 2009, 2020 — and in 2025. The previous cases have all been followed by strong gains during the next year. Still, Wall Street bulls need a lot to go right if 2026 is going to deliver a fourth straight year of double-digit returns. Read more in today’s Taking Stock.

European stocks are mixed regionally, with the broad Stoxx 600 higher by 0.2%; health care leads, tech lags while miners are lifted after copper surged to a fresh record amid a renewed rush to ship the base metal to the US. Consumer products and services shares lag, with Adidas tailing the sector. Here are some of the biggest movers on Tuesday:

- InPost shares rise as much as 20% after the Polish logistics firm announced it had received an indicative proposal regarding a potential acquisition.

- Next shares climb as much as 3.7%, the most since October, after the fashion retailer reported strong Christmas sales and boosted its profit guidance for the fifth time this financial year.

- Tesco shares climb as much as 3.4% after Worldpanel by Numerator said the British grocer had increased sales and market share in the run-up to Christmas, taking its greatest slice of shoppers’ spend in more than a decade.

- Daimler Truck shares rise as much as 5.6%, hitting the highest level in four months, after the release of positive data for a key measure of North American truck orders.

- SMG Swiss Marketplace Group shares surge as much as a record 17%, after it announced an “amicable” agreement with Switzerland’s Price Supervisor regarding investigations into the Ricardo platform and SMG Real Estate business.

- Infineon shares rise as much as 5.1% after US peer Microchip gave an upbeat forecast and Bank of America lifted its price target, partly due to AI server exposure.

- Adidas shares fall as much as 7.6% after Bank of America downgraded the stock to underperform, predicting a “material stepdown” in growth for the sportswear sector. Retailer JD Sports was cut to neutral, and its shares fall 7.2%.

- DSM-Firmenich shares drop as much as 1.3% after Morgan Stanley downgraded the stock to equal-weight, citing lingering uncertainty around the animal, nutrition and health exit structure and tough mid-term strategic targets for the core business.

- Liontrust Asset Management shares sink as much as 7.7%, the most in six months, as Deutsche Bank analysts cut their recommendation on the firm to sell from hold, and slash the target price by a third.

“It reflects a continuation of a theme that we are in the early innings of, which started last year, i.e. that US exceptionalism has peaked and has started to unwind,” Raymond Sagayam, managing partner at Banque Pictet & Cie SA, told Bloomberg TV.

Asian equities rose to a fresh record high, with a rally in Chinese shares helping fuel stronger risk appetite for the region. The MSCI Asia Pacific Index advanced 1.2%, poised for a fourth straight day of gains in what is poised to be its best-ever start to a year. Tech again remained a focus, with TSMC, SK Hynix and Hitachi among the biggest contributors to the benchmark’s advance. Key gauges in mainland China, Hong Kong as well as Japan rose more than 1%. China’s onshore CSI 300 Index climbed to the highest in four years on enthusiasm for the country’s AI industry and growing signs of an economic recovery. Investors hope for an extension of last year’s gains as Beijing backs key sectors and implements measures to curb excessive competition and revive the ailing property market. A subindex of financial shares also helped boost the Asian benchmark, after US peers climbed overnight. Japanese banks jumped after central bank Governor Ueda said he intends to keep raising rates in line with inflation. The rally in Asian stocks at the start of the year underscores their rising appeal for global investors wary of high tech valuations in the US and the prospect of a weakening dollar. It also points to the room left to run in the region’s tech shares, with Samsung Electronics Co. and Taiwan Semiconductor Manufacturing Co. powering the gains over the past few days.

In FX, German inflation weighed on the euro, lifting the Bloomberg Dollar Index higher by 0.1%. G-10 FX moves are limited.

In rates, treasuries hold small losses in early US session, unwinding a portion of Monday’s gains with oil futures rising further and stock index futures stalled near record highs. European bonds outperform following soft German regional inflation prints. US yields are 1bp-2bp cheaper with curve spreads steeper; 2s10s topped 72bp, approaching 2025 wides; 10-year near 4.17% is about 1bp cheaper on the day, with bunds and gilts in the sector outperforming by about 3bp. German yields are lower by around 2bps across the curve following soft regional inflation metrics. In contrast, US yields are higher with the curve bear-steepening.

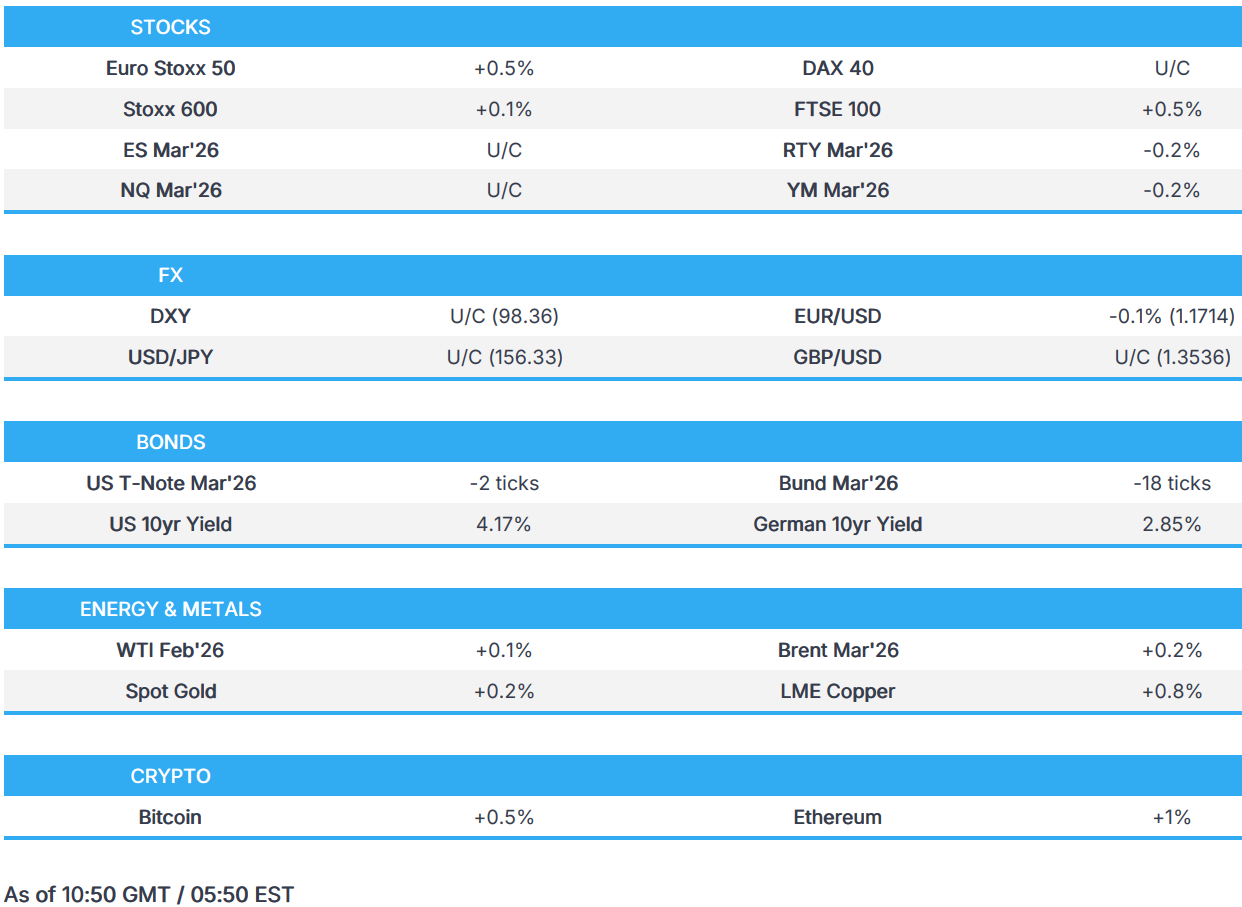

In commodities, WTI crude futures are building on yesterday’s gains, up 0.3%. There’s mixed fortunes for precious metals with spot silver higher by 2.2%. Gold faded initial gains and is now up just 0.2% while LME copper hit further all-time-highs, up 1.3%.Bitcoin has slipped throughout the session, trades lower by 0.4%.

US economic calendar includes December final S&P Global US services and composite PMIs at 9:45am. Scheduled Fed speakers include Barkin (8am) and Miran (8:30am)

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini +0.2%

- Russell 2000 mini -0.3%

- Stoxx Europe 600 little changed

- DAX little changed, CAC 40 -0.6%

- 10-year Treasury yield +1 basis point at 4.17%

- VIX +0.3 points at 15.15

- Bloomberg Dollar Index little changed at 1203.74

- euro little changed at $1.1715

- WTI crude +0.2% at $58.43/barrel

Top Overnight News

- China imposed controls on exports to Japan that could have military use, intensifying a dispute between Asia’s top economies over remarks Japanese PM Sanae Takaichi made last year on Taiwan. BBG

- Trump asked Marco Rubio to oversee an economic and political overhaul of Venezuela, leading a team that includes officials working on energy, finance and military police, White House adviser Stephen Miller said. BBG

- In late night Truth Social post, Trump announced that Danish territory is now an American “protectorate.” Denmark and the broader NATO alliance are extremely concerned the US could imminently seize Greenland and paralyze the NATO alliance. The Atlantic

- Trump said he believes the U.S. oil industry could get expanded operations in Venezuela “up and running” in fewer than 18 months. “A tremendous amount of money will have to be spent, and the oil companies will spend it, and then they’ll get reimbursed by us or through revenue,” he said. NBC

- Nvidia’s Rubin data-center chips are now in production as strong AI demand drives the need for more powerful systems, CEO Jensen Huang said. Rival AMD unveiled a new AI chip for corporate data-center use. BBG

- Nvidia said it has seen strong demand from customers in China for the H200 chip that the Trump administration has said it will consider letting the chipmaker ship to that country. BBG

- The Trump admin is planning to meet with executives from U.S. oil companies later this week to discuss boosting Venezuelan oil production. The meetings are crucial to the administration’s hopes of getting top U.S. oil companies back into the South American nation. RTRS

- MCHP +430 bps in premkt after issuing its second upside preannouncement of the quarter, indicating potential recovery in demand for industrial and automotive chips.

- Trump is scheduled to deliver remarks at a GOP member retreat at 10:00am ET on Tuesday and will participate in a policy meeting at 2:30pm ET.

- Trump posted “Pregnant Women, DON’T USE TYLENOL UNLESS ABSOLUTELY NECESSARY, DON’T GIVE TYLENOL TO YOUR YOUNG CHILD FOR VIRTUALLY ANY REASON, BREAK UP THE MMR SHOT INTO THREE TOTALLY SEPARATE SHOTS”. Full post “Pregnant Women, DON’T USE TYLENOL UNLESS ABSOLUTELY NECESSARY, DON’T GIVE TYLENOL TO YOUR YOUNG CHILD FOR VIRTUALLY ANY REASON, BREAK UP THE MMR SHOT INTO THREE TOTALLY SEPARATE SHOTS (NOT MIXED!), TAKE CHICKEN P SHOT SEPARATELY, TAKE HEPATITAS B SHOT AT 12 YEARS OLD, OR OLDER, AND, IMPORTANTLY, TAKE VACCINE IN 5 SEPARATE MEDICAL VISITS! President DJT”.

Trade/Tariffs

- China Commerce Ministry imposes export controls on dual-use items to Japan, effective immediately

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher following the positive handover from Wall Street, where all major indices gained amid outperformance in energy and a softer yield environment. ASX 200 was the laggard with the index dragged lower by weakness in defensives and the top weighted financial sector, while metal and mining stocks were boosted after the recent climb in underlying commodity prices and reports of an AUD 8.8bln takeover offer for BlueScope Steel. Nikkei 225 rallied at the open to back above the 52,000 level with the advances led by mining and tech-related stocks. Hang Seng and Shanghai Comp conformed to the predominantly upbeat mood, with outperformance in Hong Kong helped by strength in some property names and miners, while aluminium producer China Hongqiao Group led the advances as aluminium prices printed fresh three-year highs.

Top Asian News

- Japan sold JPY 1.96tln 10yr JGB, b/c 3.30x (prev. 3.59x), average yield 2.095% (prev. 1.872%). Lowest accepted price 99.99 vs prev. 98.53. Average accepted price 100.04 vs prev. 98.57. Tail in price 0.05 vs prev. 0.04.

- Japan’s nuclear regulator said no irregularities at Chugoku Electric’s (9504 JT) Shimane nuclear power plant following the earthquake.

- Earthquake with a preliminary magnitude of 6.3 strikes at the Shimane Prefecture in Japan, according to NIED

European bourses (STOXX 600 U/C) opened with very modest gains, but have indices have since slipped a touch off best levels to show a bit more of a mixed picture in Europe. European sectors are mixed, with Health Care, Energy, and Basic Resource leading. Energy is advancing on higher crude prices, despite the absence of a clear catalyst. On a stock-specific basis, the sector is also being supported by gains in heavyweight names such as Shell (+1.6%) and BP (+1.9%). Meanwhile, sentiment in Basic Resources has been underpinned by strength in metal prices.

Top European News

- ‘Coalition of the Willing’ to discuss security guarantees for Ukraine

FX

- DXY resides in a narrow 98.161-98.425 range after recovering from worst levels on the back of some EUR softness (more below), although price action across FX thus far has been muted vs other markets (Equities, Fixed Income, Commodities). The US docket for today only consists of S&P Services and Composite Final PMIs alongside commentary from Fed’s Barkin and Miran. Perhaps more importantly, US President Trump is due to give remarks later today.

- EUR is on a softer footing, with early weakness commencing shortly after the revisions lower to the French PMIs, whilst downward revisions in German Composite and EZ PMIs further weighed on the single currency. Moreover, German State CPIs were more dovish than the Nationwide figure (at 13:00 GMT) implies. EUR/USD resides towards the bottom end of a 1.1708-1.1743.

- GBP/USD trades flat towards the bottom of a 1.3528-1.3568 range with little immediate move seen on the slight revision higher in UK Services and Composite PMIs, with EUR/GBP flat intraday in a narrow 0.8644-0.8660. USD/JPY is also flat in a 156.17-156.80 range and largely trading at the whim of the USD.

- Antipodeans also see little price action but AUD continues to be supported by the recent rally in copper and gold.

Fixed Income

- Benchmarks began the morning on the backfoot, with downside of around five and 20 ticks for USTs and Bunds respectively. Action that came as the benchmarks trimmed into and through the APAC session, with further pressure emanating from weak demand at the Japanese 10yr tap; an auction that sent JGBs lower from 132.23 to a 131.93 session trough, trimming initial gains of around 15 ticks to losses of 16 at worst.

- Since, the complex generally benefited incrementally from a dip in the risk tone as China imposed export-controls on dual-use items to Japan.

- For EGBs, no real move to the French Prelim. HICP metrics, which came in as expected M/M and slightly cooler than expected Y/Y at 0.7% (prev. 0.8%). More pertinently, the German State CPIs ahead of the 13:00GMT nationwide figure, where consensus is for the headline Y/Y to moderate to 2.0% (prev. 2.3%) and the HICP Y/Y to 2.2% (prev. 2.6%); for the respective M/M, at 0.3% (prev. -0.2%) and 0.4% (prev. -0.5%). State CPIs lifted Bunds to a 127.67 high, firmer by 27 ticks at most. A move perhaps driven by the M/M for North Rhine-Westphalia coming in at 0.0% (prev. -0.3%), cooler than the nationwide expectations, as above, for a lift to 0.2% (prev. -0.2%).

- Ahead, USTs look to remarks from Fed’s 2027 voter Barkin, text and Q&A expected, before the region’s own Final PMIs.

- Germany sells EUR 4.4547bln vs exp. EUR 6bln 2.00% 2027 Schatz: b/c 1.93x (prev. 1.7x), average yield 2.11% (prev. 2.05%), retention 24.22% (prev. 20.82%).

Commodities

- Crude benchmarks started the APAC session on the backfoot, paring back some of Monday’s gains before extending higher as the European session gets underway, despite a lack of crude-specific drivers.

- WTI and Brent pulled back to a low of USD 57.85/bbl and USD 61.31/bbl respectively after peaking at USD 58.51/bbl and USD 61.89/bbl in Monday’s session. Benchmarks then bid higher pretty aggressively despite a clear explanation for the move, reaching a session high of USD 58.67/bbl and USD 62.14/bbl before pulling back slightly.

- Spot XAU trades choppy but managing to hold onto modest gains as the yellow metal sits above USD 4450/oz. After dipping to a trough of USD 4428/oz early in the APAC session, XAU extended on Monday’s gains to peak at USD 4476/oz as European traders entered the market. Thus far, the yellow metal is trading in a tight USD 26/oz band above USD 4450/oz.

- 3M LME Copper continued its bid to new ATHs throughout the Asia-Pac session, following the risk-on tone in Asian equities. The red metal opened at USD 13.1k/t and immediately bid higher, peaking at USD 13.39k/t as the European session gets underway. As equities started to pull back, led by Nikkei 225 futures, following the imposition of export controls on dual-use items to Japan by China, 3M LME Copper has started to fall lower and is currently trading at USD 13.24k/t.

- China skips retail gasoline and diesel price adjustment.

- Goldman Sachs said Chinese steel mills face an extended period of depressed margins as efforts to cut capacity in the sector goes slower than expected, while exports remain high.

- ANZ said Venezuela oil output increase is unlikely until the end of the decade as aging infrastructure will require billions of dollars in spending, according to Bloomberg.

- Morgan Stanley expects another period of softness for crude ahead, Brent to fall into the mid-high USD 50/bbl region for the majority of 2026. Expect the market to be in a “significant” surplus before then returning to balance in H2-2027.

Geopolitics

- “Syria: Israeli forces infiltrate the southern countryside of Quneitra”, according to Al Arabiya.