access market

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

JPMORGAN STOPPED 54/108

GOLD: NUMBER OF NOTICES FILED FOR JANUARY/2026: 1651 CONTRACTs NOTICES FOR 165,100 OZ or 5.135 TONNES

total notices so far: 10,437 contracts for 1,043,700 OR 32.619 tonnes)

SILVER NOTICES: 30 NOTICE(S) FILED FOR 0.150 MILLION OZ OZ/

total number of notices filed so far this month : 8561 CONTRACTS (NOTICES) for 42.825 million oz

NO CHANGES:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 0.810 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 43.195 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 44.105 MILLION OZ!!

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 106/830 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 0.810 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 44.005 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 44.105 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1335TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 5.058 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 21.8302TONNES //NEW TOTAL QUEUE JUMPS 26.888//NORMAL DELIVERY OF GOLD ADVANCES TO 33.086 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 12.997 TONNES//NEW STANDING ADVANCES TO 46/083 TONNES.

NEW STANDING FOR GOLD, JANUARY CONTRACT AT 46.083 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 126/83 TONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE SIZED 1291 CONTRACTS OI TO 153,311 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 375 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 375 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1291 CONTRACTS AND ADD TO THE 375 E.FP. ISSUED

WE OBTAIN A MEGA MEGA HUGE SIZED GAIN OF 1666 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $1.44 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.330MILLION PAPER OZ

OCCURRED DESPITE OUR LOSS IN PRICE.OF $1.44

2.ASIAN AFFAIRS JAN 16/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 5.64 PTS OR 0.14%

//Hang Seng CLOSED UP 44.90 PTS OR 0.17%

// Nikkei CLOSED UP 926/36 PTS OR 1.76%

//Australia’s all ordinaries CLOSED DOWN .21%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9655

/ OFFSHORE CLOSED UP AT 6.9535 Oil DOWN TO 60.08 dollars per barrel for WTI and BRENT UP TO 64.60 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9654 OFFSHORE YUAN TRADING UP TO 6.9535 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4132 CONTRACTS TO 532,136 OI WITH OUR GAIN IN PRICE OF $74.30 WITH RESPECT TO WEDNESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3983). WE HAD ZERO T.A.S. LIQUIDATION TUESDAY. IT SEEMS THAT THE SPECULATORS WENT MASSIVELY HUGE TO THE LONG SIDE WITH OUR FRBNY PROVIDING STILL THE MASSIVE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE .

YOU WILL NOTICE THAT THE COMEX OI IS NOW GAINING HUGELY FROM ITS LOW OI OF AROUND 418,000 TO NOW 532,136 AND NOW AMPLE ENOUGH FOR AN ATTEMPTED RAID BY OUR BANKERS. FROM CHINA WE LEARN THAT THE GOLD LEASE RATE IS NOW AROUND TWO TO 3 %

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 11,847 CONTRACTS (OR 36.833TONNES). THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD. IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS AND THEN WE HAVE THREE ISSUED IN JANUARY: 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES//TOTAL EXCHANGE FOR RISK JANUARY 12.977 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELVERIES.

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 39 TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WILL BE ADDED TO OUR DAILY TOTALS!! (12.997 TONNES)

DETAILS ON OUR NEW JANUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 7115 CONTRACTS WITH OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH JANUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 2777 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE HUGE NUMBER OF T.A.S. ISSUANCES IN DECEMBER AND JANUARY AND THE 3 ISSUANCES OF EXCHANGE FOR RISK!!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR HUGE QUEUE JUMP OF 5.058TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 21.8130 TONNES //NEW TOTAL QUEUE JUMPS 26.888 //NORMAL DELIVERY OF GOLD ADVANCES TO 33.086 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 12.997 TONNES//NEW STANDING ADVANCES TO 46.083 TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 39+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 39 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. SO IT IS POSSIBLE/PROBABLE THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!! AND THEN ANOTHER 12.997 TONNES TOTAL IN JANUARY/3 ISSUANCES:

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 39+ TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/JAN//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 1150 CONTRACTS.

THAT IS A STRONG SIZED 2983 EFP CONTRACT WAS ISSUED: : /FEB 2983 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2983 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 39 TONNES

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + AND DID HAVE HUGE GOVERNMENT LIQUIDATION

- ZERO MONTH END SPREADERS LIQUIDATION!!. WILL NOT COMMENCE UNTIL NEXT WEEK

T.A.S.SPREADER ISSUANCE//JANUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A STRONG SIZED 2777 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP WEDNESDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING HUGE SIZED GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR HUGE QUEUE JUMP OF 5.058 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 21.8302 TONNES //NEW TOTAL QUEUE JUMPS OF 26/888//NORMAL DELIVERY OF GOLD ADVANCES TO 33/086 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 12.997 TONNES//NEW STANDING ADVANCES TO 46/083TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING JANUARY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $74.30)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX// WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL WEDNESDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR JANUARY IN AN OFF MONTH. THE COMEX IS ONE BIG MESS!!

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. NOW JANUARY:

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR HUGE QUEUE JUMP OF 5.058 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 21.8302TONNES //NEW TOTAL QUEUE: 26.888 TONNES //NORMAL DELIVERY OF GOLD ADVANCES TO 33.086 TONNES TO WHICH WE ADD OUR 3 EXCHANGE FOR RISK OF 12.997 TONNES//NEW STANDING ADVANCES TO 46.083TONNES.

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $74.30

WE HAD A HUGE 4727 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

INITIAL GOLD COMEX

JAN 22

JAN 2026 CONTRACT MONTH

GOLD

GOLD

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 1- ENTRIES i) Into Brinks dealer: 1400.000 oz total deposit 1400.000 oz |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER i) Manfra 7846.773 oz total deposit 7846.773 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1651 notice(s) 165100 OZ 5.135 TONNES OF GOLD |

| No of oz to be served (notices) | 150 contracts 15,000 OZ 0.4665 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,487 notices 1,048,700 oz 32.619TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1

i) Into Brinks dealer: 1400.000 oz

total deposit 1400.000 oz

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

i) Manfra 7846.773 oz

total deposit 7846.773 oz

customer withdrawals:

0 ENTRIES

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 2// dealer to customer

i) Brinks 5690.727 oz

ii) JPMorgan; 14.,039,682. oz

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF JANUARY STANDS AT 1801 CONTRACTS FOR A GAIN OF 1518 CONTRACTS.

WE HAD 108 NOTICES FILED ON WEDNESDAY, SO WE GAINED 1626 CONTRACTS OR 162,600 OZ OF A QUEUE JUMP (5.058 TONNES)

FEB LOST 17,878 CONTRACTS DOWN TO 224.850 CONTRACTS AS FEB BECOMES THE FRONT MONTH, WE ARE GOING TO HAVE A WHOPPER OF A DELIVERY MONTH!!! LITTLE ROLLING TO THE NEXT DELIVERY MONTH WE HAVE ONLY 6 MORE READING DAYS BEFORE FIRST DAY NOTICE

MARCH GAINED 114 CONTRACTS UP TO 3347

We had 1651 contracts filed for today representing 165,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 78 notices issued from their client or customer account. The total of all issuance by all participants equate to 1651 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 121 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JAN /2026. contract month, we take the total number of notices filed so far for the month (10,487) to which we add the difference between the open interest for the front month of JAN ( 1801 CONTRACTS) minus the number of notices served upon today (1651 x 100 oz per contract) equals 1,063,700 OZ OR (33.086Tonnes of gold) to which we add our exchange for risk in January of 12.997 tonnes//new standing advances to 46.083 Tonnes

thus the INITIAL standings for gold for the JAN contract month: No of notices filed so far (10,487 x 100 oz +we add the difference for front month of JAN (18001 OI} minus the number of notices served upon today (1651x 100 oz) which equals 1063,700 OR 33.086 TONNES plus our 3 exchange for risk of 12.997 tonnes//new standing advances to 46.083 tonnes

new total of gold standing in JANUARY is 46.083 tonnes

TOTAL COMEX GOLD STANDING FOR JANUARY 46.083 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume WEDNESDAY confirmed 500,520 huge//

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,911,959.820oz 59.46 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,144,279.824 oz

TOTAL REGISTERED GOLD 18,846,066.229 or 586.19 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,298,213.595 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 16,934,107 oz ((REG GOLD- PLEDGED GOLD)=

526.72 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

JAN 22 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of Asahi 604,247.000 oz ii) JPMoorgan 1281,272.600 oz iii) Out of Looms 649,675.810 oz iv0 Out of Manfra 1614,759.250 oz total: 4,151,954.650 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | i) Into Stonex 199,716.902.610 oz total dealer deposit 199,716.610 oz |

| Deposits to the Customer Inventory | 2 ENTRIES i) Into Asahi: 118,125.700 oz ii0 Into HSBC 1032,776.970 oz total deposit: 1,150,902.670 oz |

| No of oz served today (contracts) | 30 CONTRACT(S) ( 0.150 million OZ |

| No of oz to be served (notices) | 108ontracts (0.540MILLION oz) |

| Total monthly oz silver served (contracts) | 8561 contracts 42.805 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 ENTRY

i) Into Stonex 199,716.902.610 oz

total dealer deposit 199,716.610 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

withdrawals: customer side/eligible

4 entries

i) Out of Asahi 604,247.000 oz

ii) JPMoorgan 1281,272.600 oz

iii) Out of Looms 649,675.810 oz

iv0 Out of Manfra 1614,759.250 oz

total: 4,151,954.650 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 8 all dealer to customer

i) Out of Asahi 606,258.650 oz

ii) Out of Brinks 313,390.350 oz

iii) Out of CNT 140,349.289 oz

iv) Out of Delaware 36,812.629 oz

v Out of HSBC: 5299.450 oz

vi) Out of JPMorgan: 534,474.500 oz

vii Out of Loomis 54,405.800 oz

viii) Out of Stonex: 85,201.900 oz

total adjusted out of the dealer: 1.763 million oz

total adjusted out of reg. to eligible: 3.175 million oz

TOTAL REGISTERED SILVER: 114.262MILLION OZ//.TOTAL REG + ELIGIBLE. 418.161 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF JANUARY /2026 OI: 270 OPEN INTEREST CONTRACTS FOR A LOSS OF 81 CONTRACTS. WE HAD 243 NOTICES FILED ON WEDNESDAY SO WE GAINED 162 CONTRACTS OR A STRONG QUEUE JUMP OF 0.810MILLION OZ QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND.

FEB LOST ONLY 36 CONTRACTS DOWN TO 2199 CONTRACTS AS FEB BECOMES THE FRONT MONTH, WE ARE GOING TO HAVE A STRONG DELIVERY MONTH FOR FEBRUARY, (PROBABLY AROUND 10 MILLION OZ)

MARCH GAINED 108 CONTRACTS UP TO 100,935

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 30 or 0.150 MILLION oz

CONFIRMED volume; ON WEDNESDAY 143,091 huge//

AND NOW JANUARY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 8561 X5,000 oz = 42.805 MILLION oz

to which we add the difference between the open interest for the front month of JANUARY (270) AND the number of notices served upon today (30)x (5000 oz)

Thus the standings for silver for the JANUARY 2026 contract month: (8561)Notices served so far) x 5000 oz + OI for the front month of JAN(270) minus number of notices served upon today (30)x 5000 oz equals silver standing for the JANUARY.contract month equating to 44.005MILLION OZ TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR 20 CONTRACTS OR 0.100 MILLION OZ//NEW TOTAL STANDING FOR DELIVERY: 44.105 MILLION OZ.

NEW STANDING: 44.105 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF JANUARY.

New total standing: 44.105 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 114.262 million oz of registered silver

JPMorgan as a percentage of total silver: 174.363/418.161.million: 41.62%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 19/WITH GOLD UP $22.20 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 18/WITH GOLD DOWN $9.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .85 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 17/WITH GOLD UP $39.45 TODAY/NO CHANGES IN GOLD AT THE GLD:// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 16/WITH GOLD DOWN $3.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 15/WITH GOLD UP $10.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 105.12 TONNES

DEC 12/WITH GOLD UP $14.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.83 TONNES

DEC 11/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 10/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 9/WITH GOLD UP $18.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.14 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1049.11 TONNES

DEC 8/WITH GOLD DOWN $23.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.33 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1050.25 TONNES

DEC 5/WITH GOLD UP $9.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 4.00 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.58 TONNES

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

GLD INVENTORY: 1077.66 TONNES, TONIGHTS TOTAL

SILVER

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 17/WITH SILVER UP $2.93/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 16/WITH SILVER DOWN $.07/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 56.360 MILLION OZ //

DEC 15/WITH SILVER UP $1.62/SMALL CHANGES IN SILVER AT THE SLV: A SMALL DEPOSIT OF 635,000 INTO THE SLV. ./ :INVENTORY RESTS AT 517.720 MILLION OZ //

DEC 12/WITH SILVER DOWN $2.30/NO CHANGES IN SILVER AT THE SLV: ./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 11/WITH SILVER UP $3.52/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.537 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 9/WITH SILVER UP $2.41/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.179 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 510.828 MILLION OZ //

DEC 8/WITH SILVER DOWN $0.48/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 5.497 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 512.007 MILLION OZ //

DEC 5/WITH SILVER UP 0.39/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.083 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.448 MILLION OZ //

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

CLOSING INVENTORY 519,752 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

ALASDAIR MACLEOD..

MATHEW PIPENBURG/EGON VON GREYERZ

3.CHRIS POWELL AND HIS GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 255

5. COMMODITY REPORT//:silver

Michael Oliver: T-Bond Nuclear Panic Will Send Silver VIOLENTLY to $300–$500 | Gold to $8,000

![]()

by ITM Trading

Wednesday, Jan 21, 2026 – 13:16

In a rare, no-spin interview with Daniela Cambone, veteran market technician Michael Oliver dropped a warning few are prepared to hear. This is not a bull market—it’s a regime shift. After four decades in the trenches and a prescient call ahead of the 1987 crash, Oliver says the system has crossed a critical threshold. The tell? November’s violent breakout in silver versus gold, snapping a multi-year ceiling. History shows what comes next: vertical repricing lasting quarters, not years. Oliver’s momentum models point to chaos in paper markets—and eye-watering targets ahead: silver at $300–$500, gold at $8,000. Buckle up.

Follow Daniela on X: Daniela Cambone

About ITM Trading: ITM Trading has been a trusted leader in precious metals for over 28 years, helping clients protect and grow their wealth with custom gold and silver strategies designed for economic downturns and currency resets.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

END

GOLD/

HUGE STORY!! WHERE ARE THEY GOING TO GET THIS HUGE AMOUNT OF GOLD!!

Poland to Buy 150 Tons More Gold, Approves up to 36.6% Held

by VBL

Wednesday, Jan 21, 2026 – 9:30

GFN – WARSAW Poland’s central bank has approved a plan to purchase up to 150 tons of gold, reinforcing its position as the world’s largest reported sovereign buyer and accelerating a reserve strategy that could place the country among the top ten gold-holding nations globally.

The National Bank of Poland said Tuesday the new purchases would significantly expand its bullion holdings, which already reached 550 tons at the end of 2025 following a record 100-ton accumulation last year, the largest declared central-bank purchase reported to the International Monetary Fund. At current market prices, the new buying program would be worth nearly $23 billion and exceed the total gold reserves of several large economies, including Brazil and Mexico.

“This will place Poland among the elite 10 countries with the largest gold reserves in the world.” –Bloomberg

Central-bank gold accumulation has been a major driver of the metal’s rally, which has doubled prices over the past 18 months. Buying accelerated sharply in 2022 after Russia’s foreign-exchange reserves were immobilized, highlighting bullion’s role as a reserve asset that cannot be frozen by foreign authorities.

Governor Adam Glapiński said last week that he intends to raise the ceiling for Poland’s gold holdings to 700 tons, up from the current 550-ton level. Until now, the central bank was permitted to allocate up to 30 percent of its total reserve assets to gold. He added that there is no fixed timeline for reaching the new target.

The latest decision confirms Poland’s long-running shift toward bullion as a strategic reserve anchor, positioning the country alongside long-established gold holders in Europe and reinforcing gold’s growing role in sovereign reserve management amid rising geopolitical and financial fragmentation.

Poland currently holds approximately 550 tons of gold within total reserve assets of about $271 billion. At a gold price of $5,000 per ounce, those existing holdings equate to roughly $88 billion in value. If the National Bank of Poland completes its planned 150-ton purchase, total gold holdings would rise to 700 tons, valued near $112.5 billion, lifting Poland’s total reserves to approximately $295 billion on a mark-to-market basis. Under that framework, gold would represent about 38 percent of Poland’s total reserve assets, positioning the country among the most gold-concentrated reserve portfolios in the developed world.

Appendix: Data Box

Using the latest end-December 2025 NBP reserve total ($271.1bn) and the reported end-2025 gold stock (~550 tonnes) worth about $76.5bn :

- Current gold share (end-2025): $76.5bn / $271.1bn ≈ 28.2%

- Implied value per tonne: $76.5bn / 550t ≈ $139.1m per tonne

- Value of +150t (at same implied valuation): 150t × $139.1m ≈ $20.9bn

- New gold value: $76.5bn + $20.9bn ≈ $97.4bn

- New total reserves (no selling of anything else): $271.1bn + $20.9bn ≈ $292.0bn

- Gold as % of total reserves after +150t: $97.4bn / $292.0bn ≈ 33.3%

So under that price assumption, Poland would move from ~28% gold to about 33% gold of total reserves.

At $5,000 gold, with 700 tonnes and no asset sales, Poland’s gold would represent approximately 36.6% of total central-bank reserves.

end

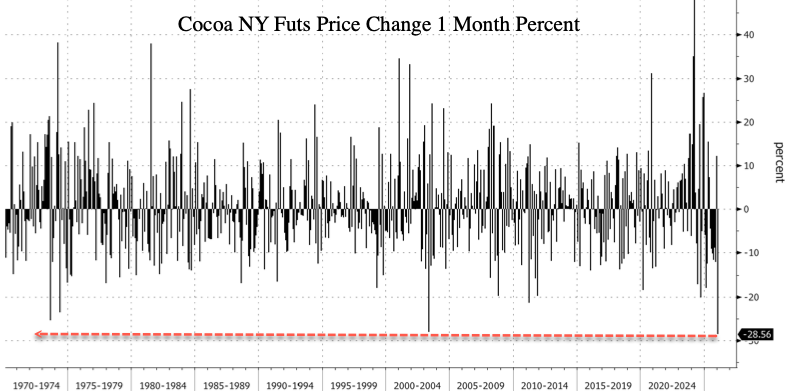

COCOA

Cocoa Prices Set For Worst Monthly Drop On Record As Demand Craters

Thursday, Jan 22, 2026 – 05:45 AM

Cocoa futures in New York tumbled to two-year lows as fresh grinding data confirmed that consumers are balking at high chocolate prices.

Contracts are now down more than 28.5% on the month, and if the decline holds through the end of next week, January would register the largest monthly percentage drop on record, with Bloomberg data going back to 1970.

The great cocoa panic of 2023-24, which sent prices from $2,190 a ton to as high as $13,000 a ton by December 2024, has now retraced nearly the entire bull move to the 76.4% Fibonacci level. This latest downward pressure comes as new grinding data in Europe, cited by Bloomberg, shows clear demand deterioration:

- Demand is deteriorating: European cocoa grindings fell to the lowest quarterly level since 2013, Asia also declined, while North America was roughly flat.

- Reduced grindings have hit processors hard: Barry Callebaut AG reported a 22% drop in cocoa division volumes and nearly 10% lower overall sales volumes.

Goldman analyst Natasha de la Grense provided clients with more color on Barry Callebaut’s earnings, which showed negative market demand for chocolate:

Barry Callebaut – Q1 volumes in line (-9.9%) with a better outcome in Gourmet (-3.6% vs -5.5%) and Food Manufacturers (-7.4% vs -8.0%) offset by worse volumes in Cocoa Products (-22% vs -16.5%). The miss at the latter was impacted by negative market demand notably in AMEA and the prioritisation of volume towards higher return segments. Pricing was +19% YoY (vs +40% last quarter) so sequentially improving and now passed its peak. They say that global chocolate volumes were -6.8%. No change to FY26 outlook but they note lower bean prices are encouraging for chocolate market stabilisation. With this release, a new CEO has been announced which is a bit of a surprise (and Mr Feld is leaving almost immediately). However, the newly appointed Mr Schumacher is former CEO of Unilever and well-liked by investors. On the call, the Chairman suggested there will be no major change in strategy or need for reinvestment under new management. Note that BC also said it is committed to its integrated business model which should pour cold water on speculation around a split.

Barry Callebaut CFO Peter Vanneste told investors on an earnings call, “We believe consumers will adapt and adjust to these new price levels and ultimately continue to buy chocolate given the high engagement of the category.”

We told readers in December that sliding cocoa prices would produce “Tailwinds” for the badly beaten-down Hershey stock …

Read the note here.

5B. COMMODITY REPORT//GOLD OR /SILVER LEASE RATES:/GOLD

GOLD LEASE RATES CLIMB TO AROUND 3.0 TO 4.0%

| Robert Lambourne | 7:56 AM (4 minutes ago) | ||

| to me | |||

Harvey,

Interesting comment for you on gold from Chinese AI. Gold lease rates are ticking up in all markets, c3%/4% and inventories draining. Reportedly demand in Asia is strong, including Japan as confidence in bonds there is probably fraying. Possibly gold is slightly under the radar here because of silver.

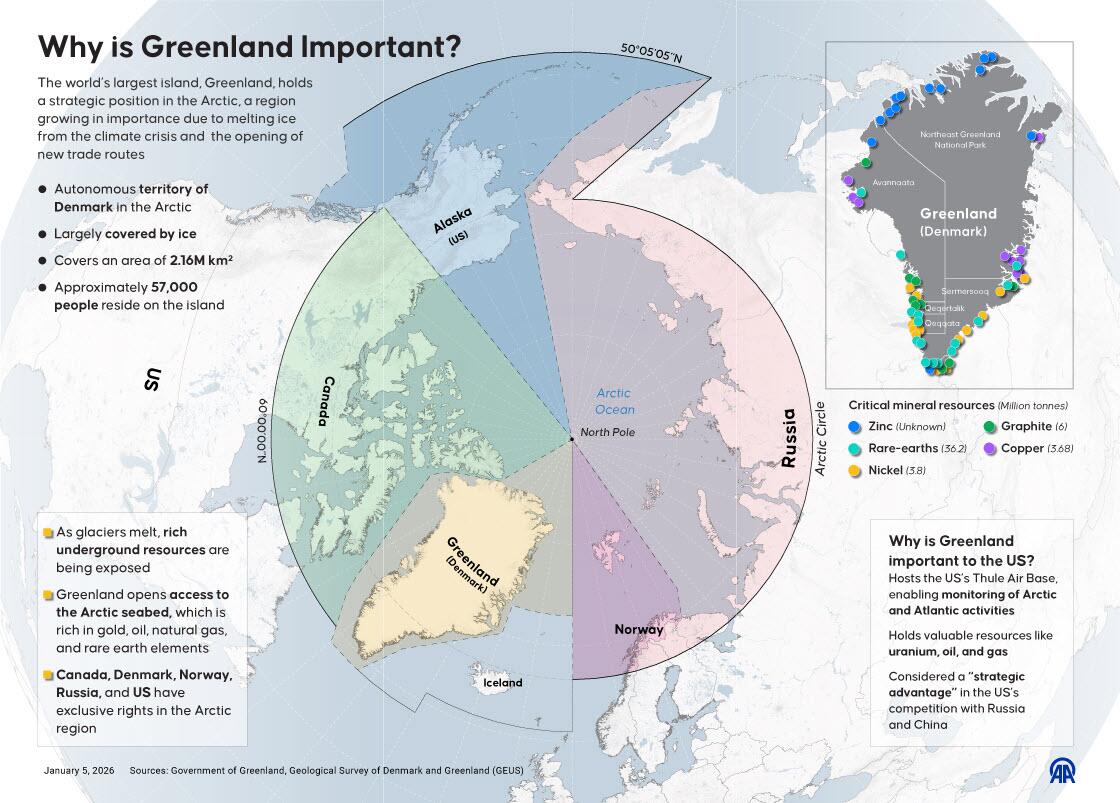

I’ve no idea how Trump will handle his latest tariff threats re Greenland, but the situation seems quite unstable. Gold might well move strongly here.

No December 2025 BIS gold swap data yet. I’ve emailed Chris to suggest it might only appear right at the month end. This is no great surprise, but we can guess plausibly that the BIS will be under some pressure to end the gold swaps. Whatever you think about Jerome Powell, his influence is already reduced and this will also apply to any successor when they attend the BIS meetings.

Regards,

Bob

2.ASIAN AFFAIRS JAN 22/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 5.64 PTS OR 0.14%

//Hang Seng CLOSED UP 44.90 PTS OR 0.17%

// Nikkei CLOSED UP 926/36 PTS OR 1.76%

//Australia’s all ordinaries CLOSED DOWN .21%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9655

/ OFFSHORE CLOSED UP AT 6.9535 Oil DOWN TO 60.08 dollars per barrel for WTI and BRENT UP TO 64.60 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9654 OFFSHORE YUAN TRADING UP TO 6.9535 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9655

OFFSHORE YUAN: UP TO 6.9535

HANG SENG CLOSED UP 44.90PTS OR 0.17%

2. Nikkei closed UP 926.36 PTS OR 1.76%

WEST TEXAS INTERMEDIATE OIL DOWN 60.08

BRENT; 64.60

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 99.56 /// EURO RISES TO 1.1653 UP 21 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +2.250/ DOWN 4 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.93… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.677 DOWN 2 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

6.25 VS 64.79

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8650 Italian 10 Yr bond yield UP to 3.501 SPAIN 10 YR BOND YIELD DOWN TO 3.250

3i Greek 10 year bond yield UP TO 3.464

3j Gold at $4825/00 Silver at: 93.70 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 24/100 roubles/dollar; ROUBLE AT 75.75

3m oil (WTI) into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.93 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.296% DOWN 8 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.722 DOWN 19 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7934 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9277 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.235 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.851 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.591 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.30 DOWN 0 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.422 DOWN 4 PTS

30 YR UK BOND YIELD: 5.161 DOWN 5 BASIS PTS

10 YR CANADA BOND YIELD: 3.416 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.951 UP 1 BASIS PTS.

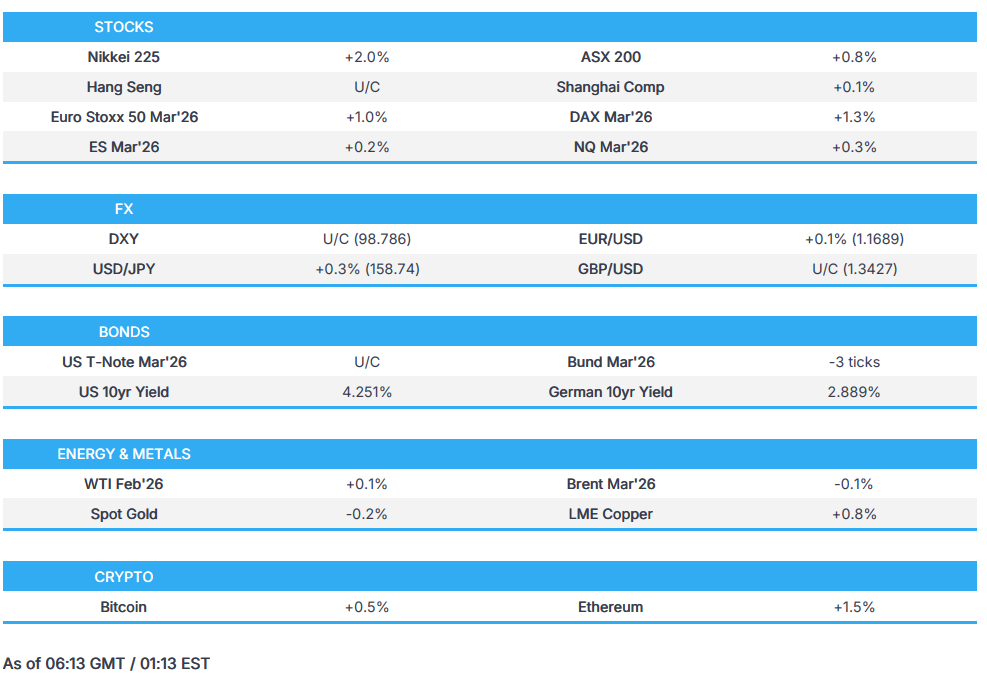

1a New York OPENING REPORT

US Futures, Global Markets Rally After Trump Greenland Pivot

Thursday, Jan 22, 2026 – 08:30 AM

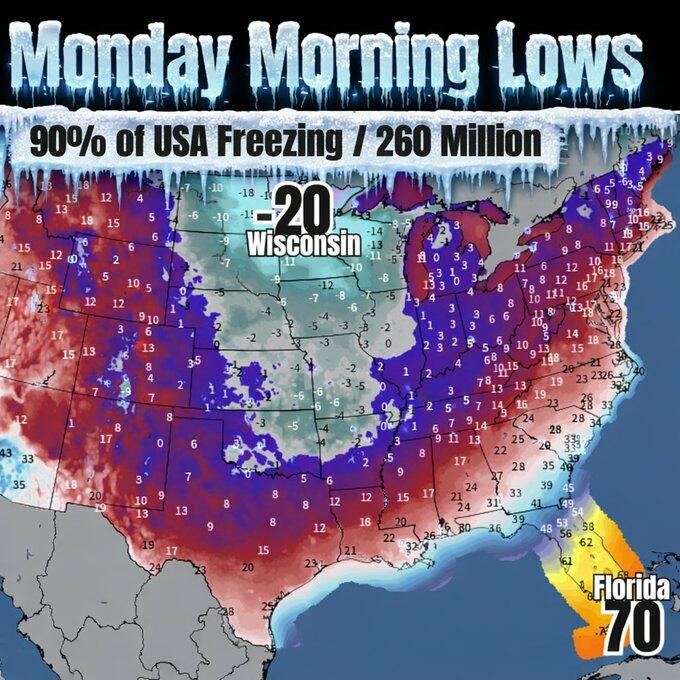

US equity futures and global stocks are sharply higher as the S&P again marches toward a new ATH while the latest vol spike subsides, after Trump’s tariff pivot eased geopolitical fears, though Greenland and other flashpoints mean the optimistic mood is laced with some caution. As of 8:00am ET, S&P 500 futures rose 0.5% after the benchmark’s biggest advance since November as a relief rally over President Donald Trump’s pivot on Greenland continued, with a flurry of activity in the artificial-intelligence space adding support to tech stocks: Nasdaq 100 futures climbed 0.8% as names linked to the build-out of AI-infrastructure outperformed in premarket trading, while all Mag 7 members advanced in premarket trading with Fins/Industrials also standout performers as Staples are mostly lower. The 10-year is flat 4.24%, dollar similar DYX $99 and Bitcoin same place as yesterday $89.8k. Commodities are mixed: nat gas surges for a third day of follow through up 14% prompt to $5.56 – highest level since late 2022 – on bruising cold across the US, while crude, copper, gold all taking a breather this morning as WTI may fall below $60/bbl. Today’s macro data gives an update on Q3 metrics, November spending / PCE, and new jobless claims.

In premarket trading, Mag 7 stocks are rallying alongside index futures (Alphabet +2%, Tesla +1%, Microsoft +0.8%, Amazon +1%, Nvidia +0.9%, Apple +0.5%, Meta +1.9%)

- Venture Global Inc. (VG) is up 10% after the company won a dispute with Spain’s Repsol SA involving the sale of liquefied natural gas shipments from its export plant in Louisiana.

- Abbott (ABT) falls 4% after posting fourth quarter results.

- Axogen (AXGN) is down 7% after the health care firm said it will offer $85 million of shares of its common stock.

- Knight-Swift (KNX) falls 2% after the freight transportation company posted fourth quarter earnings that fell short of expectations.

- Mobileye (MBLY) drops 6% after the maker of software and hardware technology for automobiles provided revenue guidance for 2026 missed the average analyst estimate.

- Procter & Gamble Co. (PG) slips 1.6% as growth in a key sales metric stagnated in the latest quarter while volume slipped, showing that US consumers spent cautiously in the final months of the year.

- Rocket Lab (RKLB) falls 2% after the company said qualification testing of the Stage 1 tank resulted in a rupture during a hydrostatic pressure trial.

- Sphere Entertainment (SPHR) rises 3% as BTIG upgrades the live entertainment and media company to buy, citing multiple catalysts driving the stock’s upside potential.

In corporate news, Lululemon’s founder lashed out over the company’s latest product flop, calling it a “total operational failure” that he blamed on the company’s board of directors. GameStop CEO disclosed the purchase of 500,000 shares of the gaming retailer, sending the stock higher in premarket trading.

The rebound in stocks followed Trump’s announcement of a framework agreement with NATO to end a days-long standoff over Greenland. The rally gained momentum on Thursday as NATO’s chief said the breakthrough didn’t involve discussion of the territory’s sovereignty, easing concerns over a key sticking point, focusing rather on the broader issue of security.

This week’s events have rewarded TACO trade dip buyers, while also serving as a reminder that volatility is never far away. Fundamentals for 2026 still look excellent, according to Tikehau Capital’s Raphael Thuin. There’s “a rare alignment of stars” going on, with double-digit earnings expected, good economic growth and possible rate cuts.

“Despite a very positive market narrative about 2026, geopolitical crisis and US tariffs can fuel volatility spikes at any time,” said Raphael Thuin, head of capital markets strategies at Tikehau Capital in Paris. “The fast-changing AI industry, like last year, also represents both a big upward potential as much as a potential downward risk.”

Sentiment was also lifted after Japanese bonds rebounded for a second straight session.

Small-cap stocks look set to continue their strong run after outperforming the S&P 500 for 13 straight sessions, with contracts on the Russell 2000 broadly tracking those on the S&P 500 on Thursday.

Meanwhile, the AI narrative is back, with Asian chip stocks surging after Wednesday’s bullish comments on AI spending from Nvidia’s Jensen Huang. The theme is getting more juice from news that Anthropic’s revenue run rate is said to have more than doubled since last summer. News that Alibaba Group Holding Ltd. is preparing to list its chipmaking arm added to a series of upbeat moves in tech after bullish comments from Nvidia Corp. Details emerged that Anthropic PBC’s revenue run rate has more than doubled since last summer, while OpenAI was locked in talks about a fresh funding round at a marked-up valuation.

In geopolitics, NATO’s chief said a breakthrough over Greenland was secured without discussing the territory’s sovereignty with Trump, focusing rather on the broader issue of security. Ukraine’s Zelenskiy arrived in Davos to meet with Trump. Speakers at the event today include Elon Musk and Larry Fink. Amid renewed speculation that foreigners may sell US assets, JPMorgan strategists said there’s been little sign of foreign investors shunning US assets amid the Greenland tensions.

In other assets, Goldman raised its December 2026 gold price forecast by more than 10% to $5,400 an ounce, on the assumption that investors who bought gold as a hedge will maintain positions. Global natural gas prices continue to soar amid freezing weather. A sweeping crypto market bill is likely to be delayed by several weeks as key lawmakers shift their focus to potential housing legislation in support of Trump’s affordability push.

Out of the 52 S&P 500 companies that have reported so far in the earnings season, 83% have managed to beat analyst forecasts, while 12% have missed.

PCE data for October and November will likely corroborate evidence that tariff pass-through is fading. That could support the case for rate cuts later in the year. Trump suggested that’s he’s down to just one choice for next Fed chair, and said Rick Rieder and Kevin Warsh are good options.

In Europe, the Stoxx 600 is up 0.9% after four days of declines, with telecoms, construction and auto sectors leading the gains. Here are the biggest movers Thursday:

- Orsted rallied as much as 5.5% after Oddo BHF upgraded to outperform from neutral, citing a “structural change of regime at the Danish offshore wind developer

- Volkswagen shares rise as much as 6.1% after the German carmaker delivered a positive surprise on free cash flow in its automotive division, driven by improvements in working capital and lower investment spend

- AB Foods climbs as much as 1.5% after the conglomerate reported first-quarter constant currency sales which Shore Capital analyst Clive Black (hold) said were “a bit better” than the group guided for earlier this month

- Aryzta shares jump as much as 14%, the most in more than three years, as analysts see the Swiss baker’s 2025 performance and outlook for the coming year as a first step to regain investor trust

- Baltic Classifieds Group shares rise as much as 6.9% after Morgan Stanley initiates the online classifieds company at overweight, citing its regional leadership position across verticals and a favorable macro backdrop

- Basic resources is the worst-performing sector in Europe on Thursday after copper declined to its lowest intraday level in almost two weeks, weighing on miners

- Essity drops as much as 5.3%, with a miss on sales overshadowing an adjusted Ebita beat by the Swedish personal care products producer

- Bankinter shares decline as much as 2.9%, the only lender declining on the Stoxx 600 Banks Index, after the Spanish bank reported earnings in line with analysts expectations

- Wickes shares climb as much as 2.2% after the home improvement products retailer reported “solid” second-half results, with analysts encouraged by evidence of market share gains

Earlier in the session, Asian stocks advanced, poised to snap a three-day losing streak, after US President Donald Trump retreated from his tariff threat on European nations and investors returned to tech stocks. The MSCI Asia Pacific Index gained 0.7%, boosted by tech shares — including TSMC and Samsung Electronics — after Nvidia CEO Jensen Huang’s comment about AI spending fueled optimism for the sector. South Korea’s stock benchmark Kospi briefly crossed the 5,000-level, a threshold targeted by the country’s president during his campaign last year.

In FX we saw muted moves with the dollar little changed. The pound was little changed.

In rates, treasuries are little changed, lagging most European bond markets but outperforming gilts, hit by potential UK leadership challenge to Prime Minister Starmer. Focal points of US session include weekly jobless claims and November personal income and spending data — which embeds PCE price indexes — and $21 billion 10-year TIPS auction. US 10-year yield near 4.24% is within 1bp of Wednesday’s closing level with UK counterpart about 2bp cheaper on the day and Germany’s richer by about 1.5bp. Gilts underperformed European peers after a pathway for a potential leadership challenge against Prime Minister Keir Starmer emerged.

In commodities, gold erases an earlier decline, trading little changed around $4,830/oz. Oil prices falling, with Brent slipping toward $64/barrel and extending after Trump comments on potential talks with Iran. Gas surged 14% to $5.56, its third day of gains, on freezing cold.

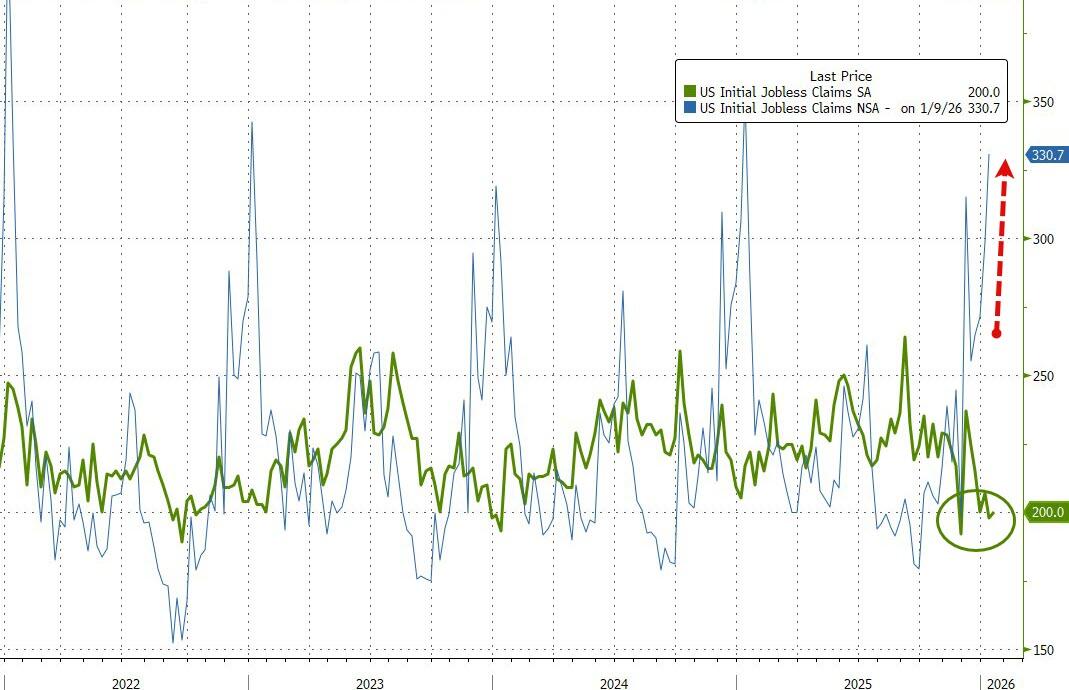

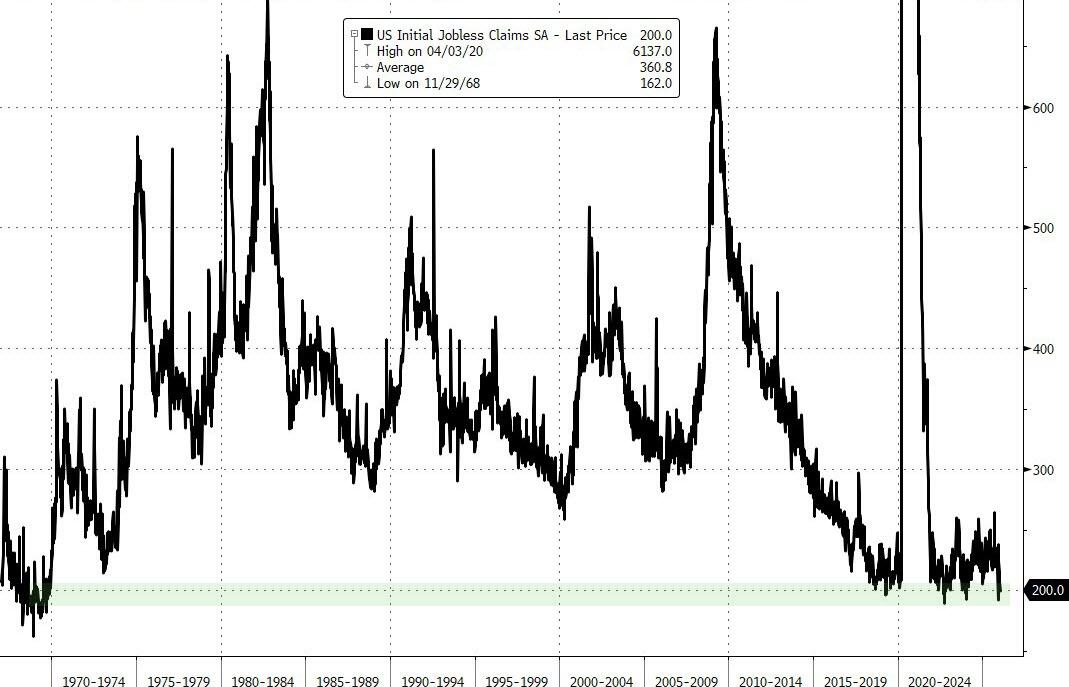

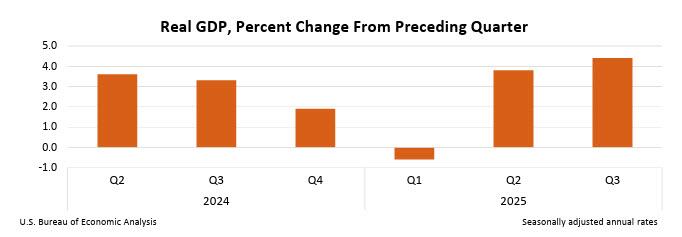

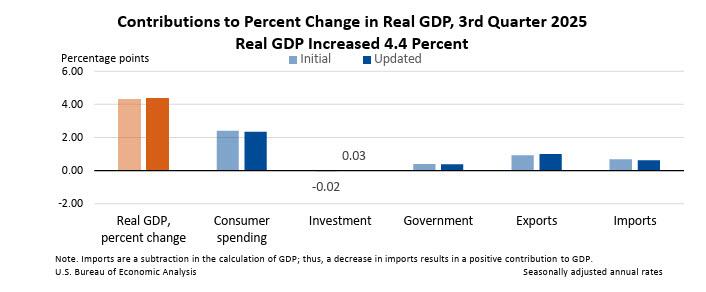

US economic calendar includes third estimate of 3Q GDP and jobless claims (8:30am), November personal income and spending (10am) and January Kansas City Fed manufacturing activity (11am)

Market Wrap

- S&P 500 mini +0.6%

- Nasdaq 100 mini +0.8%

- Russell 2000 mini +0.5%

- Stoxx Europe 600 +1.3%

- DAX +1.4%

- CAC 40 +1.3%

- 10-year Treasury yield little changed at 4.24%

- VIX -0.8 points at 16.07

- Bloomberg Dollar Index little changed at 1205.89

- euro little changed at $1.1687

- WTI crude -1.1% at $59.93/barrel

Top Overnight News

- NATO Secretary General Mark Rutte said Greenland’s sovereignty wasn’t discussed with Trump but that talks centered on Arctic security in a “practical sense.” BBG

- Emboldened by the U.S. ouster of Venezuelan President Nicolás Maduro, the Trump administration is searching for Cuban government insiders who can help cut a deal to push out the Communist regime by the end of the year. WSJ

- US House GOP leaders are struggling to strike a deal with Republican hard-liners tonight that would allow the final government funding package to advance. “The Rules Committee recessed Wednesday evening without a solution. Senior Rs hope to reconvene the panel by 9 pm”: Politico

- Volodymyr Zelenskiy is traveling to Davos to meet with Trump, a person familiar said. US envoys Steve Witkoff and Jared Kushner will go to Russia for talks with Vladimir Putin. BBG

- It took just $280 million of trading to push Japan’s government bond market into meltdown, with a $41 billion wipeout across the Japanese curve. The disconnect between the size of the wipeout and the amount that actually traded shows how Japan’s sometimes illiquid bond market has become a weak spot in the global financial system. BBG

- For the first time since the start of the private-credit boom, large numbers of individual investors are trying to get their money out. Several of the biggest funds eligible to wealthy individuals received requests from about 5% of shareholders to cash out at the end of last year, well above the normal volume, according to SEC filings. WSJ

- South Korea isn’t delaying the first $20 billion tranche of its US investment pledge, Finance Minister Koo Yun Cheol said. Project selection is ongoing, making execution unlikely in the first half. BBG

- Japan’s exports rose a less-than-expected 5.1% in December. South Korea’s economy unexpectedly shrank last quarter. The Malaysian central bank kept its policy rate at 2.75% as expected. BBG

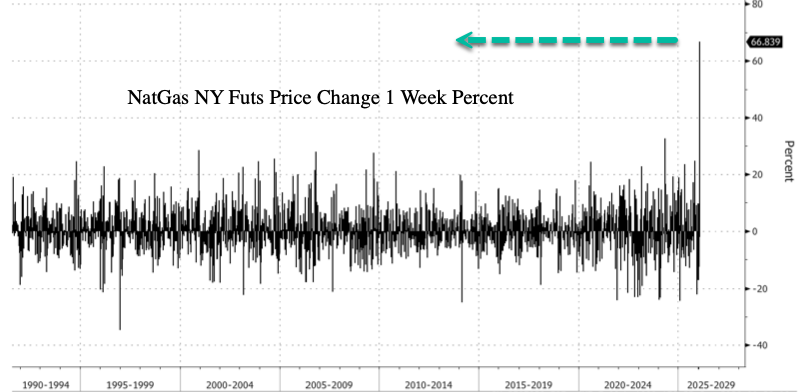

- US natural gas surged to the highest since 2022, jumping more than 70% in three days as brutal cold lifts demand amid short covering. A storm is set to hit starting tomorrow, plunging Texas into a deep freeze that may also disrupt production. BBG

- The Fed will finally get core PCE data for October and November today. Both headline and core inflation are expected to rise year on year, but the monthly figures will probably indicate that tariff pass-through is fading. BBG

Trade/Tariffs

- Switzerland’s Parmelin via X said he had a very constructive talks with USTR Greer.

- UK Business Secretary Kyle said the European customs unions is not currently on the radar of the UK government.

- China’s Commerce Ministry said China is concerned with the EU excluding some of Chinese tech suppliers.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded entirely in the green, tracking the rebound on Wall Street after President Trump withdrew plans for additional tariffs on EU countries. ASX 200 opened around +0.8%, lifted by the improved global tone after US tariff removal, though the index later dipped following a hotter-than-expected Australian jobs report. Nikkei 225 posted firm gains of nearly 2%, snapping a five-day losing streak as chipmakers and financials advanced and JGBs stabilised. Hang Seng and Shanghai Comp the laggards, despite a brief recovery tech and easing trade-tension concerns after the US rollback of tariffs.

Top Asian News

- Australia’s Nationals Leader said coalition can no longer continue.

European equities (STOXX 600 +1.3%) are firmer across the board. Sentiment has tracked tailwinds from APAC and Wall St which traded higher after market sentiment was kept at ease following Trump’s Davos speech where he vowed to not use military action against NATO allies and later withdrew tariff plans on some European countries. European sectors are all in the green. Autos takes the top spot, boosted by gains in Volkswagen (+5%) and Michelin (+3.3%) after providing positive trading updates.

Top European News

- German Chancellor Merz said there needs to be significant defence investment.

FX

- DXY is currently flat and trades within a narrow 98.72 to 98.82 range; the low for the day coincides with its 200 DMA. Some further pressure in the index could see the test of its 100 DMA (98.69).