access market

GOLD $4,979.80 3:30 PM)

SILVER: 102.14 3

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JANUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,908.800000000 USD

INTENT DATE: 01/22/2026 DELIVERY DATE: 01/26/2026

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 25

332 H STANDARD CHARTERED B 4

363 H WELLS FARGO SECURITI 11

435 H SCOTIA CAPITAL (USA) 1005

624 H BOFA SECURITIES 988

661 C JP MORGAN SECURITIES 48 83

737 C ADVANTAGE FUTURES 7 4

905 C ADM 5

TOTAL: 1,090 1,090

MONTH TO DATE: 11,577

JPMORGAN STOPPED 54/108

GOLD: NUMBER OF NOTICES FILED FOR JANUARY/2026: 1090 CONTRACTs NOTICES FOR 109,000 OZ or 3.3903 TONNES

total notices so far: 11,577 contracts for 1,157,700 OR 36.009 tonnes)

SILVER NOTICES: 265 NOTICE(S) FILED FOR 1.375 MILLION OZ OZ/

total number of notices filed so far this month : 8826 CONTRACTS (NOTICES) for 44.140 million oz

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.265 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 45.270 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 45.370 MILLION OZ!!

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 109.275 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.265 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 45.270 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 45.370 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1335TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 3.250 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 26.871TONNES //NEW TOTAL QUEUE JUMPS 30.121//NORMAL DELIVERY OF GOLD ADVANCES TO 36.33 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 12.997 TONNES//NEW STANDING ADVANCES TO 49.327 TONNES.

NEW STANDING FOR GOLD, JANUARY CONTRACT AT 49.327 TONNES OF GOLD

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 130.74 TONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 2253 CONTRACTS OI TO 158,995 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 489 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 489 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5684 CONTRACTS AND ADD TO THE 489 E.FP. ISSUED

WE OBTAIN A MEGA MEGA HUGE SIZED GAIN OF 2742 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $3.20 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 13,710 MILLION PAPER OZ

OCCURRED DESPITE OUR GAIN IN PRICE.OF $3.20

2.ASIAN AFFAIRS JAN 16/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 13.59 PTS OR 0.33%

//Hang Seng CLOSED UP 119.55 PTS OR 0.45%

// Nikkei CLOSED UP 185.61 PTS OR 0.35%

//Australia’s all ordinaries CLOSED UP 0..07%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9655

/ OFFSHORE CLOSED UP AT 6.9520 Oil UP TO 60.15 dollars per barrel for WTI and BRENT UP TO 64.81 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP TO 6.9655 OFFSHORE YUAN TRADING UP TO 6.9520 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 8897 CONTRACTS TO 541,033 OI WITH OUR GAIN IN PRICE OF $76.20 WITH RESPECT TO THURSDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1295).

WE HAD ZERO T.A.S. LIQUIDATION THURSDAY. IT SEEMS THAT THE SPECULATORS WENT MASSIVELY HUGE TO THE LONG SIDE WITH OUR FRBNY PROVIDING STILL THE MASSIVE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE .

YOU WILL NOTICE THAT THE COMEX OI IS NOW GAINING HUGELY FROM ITS LOW OI OF AROUND 418,000 TO NOW 541,033 AND NOW AMPLE ENOUGH FOR AN ATTEMPTED RAID BY OUR BANKERS. FROM CHINA WE LEARN THAT THE GOLD LEASE RATE IS NOW AROUND TWO TO 3 %

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 10,172 CONTRACTS (OR 31.576TONNES).

THEN WE WERE NOTIFIED OF A 0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD. IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS AND THEN WE HAVE THREE ISSUED IN JANUARY: 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES//TOTAL EXCHANGE FOR RISK JANUARY 12.977 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELVERIES.

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 39 TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WILL BE ADDED TO OUR DAILY TOTALS!! (12.997 TONNES)

DETAILS ON OUR NEW JANUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 10,152 CONTRACTS WITH OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH JANUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A HUGE SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 5178 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE HUGE NUMBER OF T.A.S. ISSUANCES IN DECEMBER AND JANUARY AND THE 3 ISSUANCES OF EXCHANGE FOR RISK!!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR HUGE QUEUE JUMP OF 3.250 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 26.871 TONNES //NEW TOTAL QUEUE JUMPS 30.121 //NORMAL DELIVERY OF GOLD ADVANCES TO 33.086 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 12.997 TONNES//NEW STANDING ADVANCES TO 49.327 TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 39+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 39 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. SO IT IS POSSIBLE/PROBABLE THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!! AND THEN ANOTHER 12.997 TONNES TOTAL IN JANUARY/3 ISSUANCES:

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 39+ TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/JAN//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1255 CONTRACTS.

THAT IS A FAIR SIZED 1255 EFP CONTRACT WAS ISSUED: : /FEB 1255 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1255 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 39 TONNES

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + AND DID HAVE HUGE GOVERNMENT LIQUIDATION

- ZERO MONTH END SPREADERS LIQUIDATION!!. WILL NOT COMMENCE UNTIL NEXT WEEK

T.A.S.SPREADER ISSUANCE//JANUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A FAIR SIZED 1255 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP THURSDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING HUGE SIZED GAIN OF COMEX OI AND A FAIR EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR HUGE QUEUE JUMP OF 3.250 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 26.871 TONNES //NEW TOTAL QUEUE JUMPS OF 30.371//NORMAL DELIVERY OF GOLD ADVANCES TO 36.33 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 12.997 TONNES//NEW STANDING ADVANCES TO 49.327TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING JANUARY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $75.20)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX// WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL WEDNESDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR JANUARY IN AN OFF MONTH. THE COMEX IS ONE BIG MESS!!

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. NOW JANUARY:

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR HUGE QUEUE JUMP OF 3.250 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 26.871TONNES //NEW TOTAL QUEUE: 30.121 TONNES //NORMAL DELIVERY OF GOLD ADVANCES TO 36.33 TONNES TO WHICH WE ADD OUR 3 EXCHANGE FOR RISK OF 12.997 TONNES//NEW STANDING ADVANCES TO 49.327TONNES.

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $75.20

WE HAD A HUGE 4727 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

INITIAL GOLD COMEX

JAN 23

JAN 2026 CONTRACT MONTH

GOLD

GOLD

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER NIL xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1090 notice(s) 109000 OZ 3.3903 TONNES OF GOLD |

| No of oz to be served (notices) | 105 contracts 10,500 OZ 0.326 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,577 notices 1,157,700 oz 36.009TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

customer withdrawals:

0 ENTRIES

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1// dealer to customer

i) Brinks 383.812 OZ oz

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF JANUARY STANDS AT 1195 CONTRACTS FOR A LOSS OF 606 CONTRACTS.

WE HAD 1651 NOTICES FILED ON THURSDAY, SO WE GAINED 1045 CONTRACTS OR 104,500 OZ OF A QUEUE JUMP (3.290 TONNES)

FEB LOST ONLY 11,183 CONTRACTS DOWN TO 213,667 CONTRACTS AS FEB BECOMES THE FRONT MONTH, WE ARE GOING TO HAVE A WHOPPER OF A DELIVERY MONTH!!! LITTLE ROLLING TO THE NEXT DELIVERY MONTH WE HAVE ONLY 5 MORE READING DAYS BEFORE FIRST DAY NOTICE

MARCH GAINED 76 CONTRACTS UP TO 3423

We had 1090 contracts filed for today representing 109000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 48 notices issued from their client or customer account. The total of all issuance by all participants equate to 1090 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 83 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JAN /2026. contract month, we take the total number of notices filed so far for the month (11,577) to which we add the difference between the open interest for the front month of JAN ( 1195 CONTRACTS) minus the number of notices served upon today (1090 x 100 oz per contract) equals 1,168,200 OZ OR (36.33Tonnes of gold) to which we add our exchange for risk in January of 12.997 tonnes//new standing advances to 49.329 Tonnes

thus the INITIAL standings for gold for the JAN contract month: No of notices filed so far (11,577 x 100 oz +we add the difference for front month of JAN (1195 OI} minus the number of notices served upon today (1090x 100 oz) which equals 1,168,200 OR 36.33 TONNES plus our 3 exchange for risk of 12.997 tonnes//new standing advances to 49.327 tonnes

new total of gold standing in JANUARY is 49.327 tonnes

TOTAL COMEX GOLD STANDING FOR JANUARY 49.327 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume THURSDAY confirmed 357,149 huge//

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,911,959.820oz 59.46 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 36,144,279.824 oz

TOTAL REGISTERED GOLD 18,846,066.229 or 586.19 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,298,213.595 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 16,934,107 oz ((REG GOLD- PLEDGED GOLD)=

526.72 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

JAN 23 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of CNT 571,636.203 oz ii) Out of Delaware 10,114.019 oz iii) Out of Looms 647,816.050 oz iv) Out of Manfra 170,061.100 oz v) Out of HSBC 654,458.100 oz total withdrawn 2,054,085.422 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1 ENTRIES i) Into Loomis 317,245.050 oz total deposit 317,245.05 oz |

| No of oz served today (contracts) | 265 CONTRACT(S) ( 1.325 million OZ |

| No of oz to be served (notices) | 228ontracts (1.140MILLION oz) |

| Total monthly oz silver served (contracts) | 8826 contracts 44.130 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into Loomis 317,245.050 oz

total deposit 317,245.05 oz

withdrawals: customer side/eligible

4 entries

i) Out of CNT 571,636.203 oz

ii) Out of Delaware 10,114.019 oz

iii) Out of Looms 647,816.050 oz

iv) Out of Manfra 170,061.100 oz

v) Out of HSBC 654,458.100 oz

total withdrawn 2,054,085.422 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 0

TOTAL REGISTERED SILVER: 114.262MILLION OZ//.TOTAL REG + ELIGIBLE. 416.424 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF JANUARY /2026 OI: 493 OPEN INTEREST CONTRACTS FOR A GAIN OF 223 CONTRACTS. WE HAD 30 NOTICES FILED ON THURSDAY SO WE GAINED 253 CONTRACTS OR A STRONG QUEUE JUMP OF 1.265 MILLION OZ QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND.

FEB GAINED 17 CONTRACTS UP TO 2216 CONTRACTS AS FEB BECOMES THE FRONT MONTH, WE ARE GOING TO HAVE A STRONG DELIVERY MONTH FOR FEBRUARY, (PROBABLY AROUND 10 MILLION OZ)

MARCH GAINED 1990 CONTRACTS UP TO 102,025

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 265 or 1.325 MILLION oz

CONFIRMED volume; ON THURSDAY 123,755 huge//

AND NOW JANUARY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 8826 X5,000 oz = 44.130 MILLION oz

to which we add the difference between the open interest for the front month of JANUARY (493) AND the number of notices served upon today (265)x (5000 oz)

Thus the standings for silver for the JANUARY 2026 contract month: (8826)Notices served so far) x 5000 oz + OI for the front month of JAN(493) minus number of notices served upon today (265 )x 5000 oz equals silver standing for the JANUARY.contract month equating to 45.270MILLION OZ TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR 20 CONTRACTS OR 0.100 MILLION OZ//NEW TOTAL STANDING FOR DELIVERY: 45.370 MILLION OZ.

NEW STANDING: 45.370 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF JANUARY.

New total standing: 45.370 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 114.262 million oz of registered silver

JPMorgan as a percentage of total silver: 174.363/416.474.million: 41.82%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 19/WITH GOLD UP $22.20 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 18/WITH GOLD DOWN $9.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .85 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 17/WITH GOLD UP $39.45 TODAY/NO CHANGES IN GOLD AT THE GLD:// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 16/WITH GOLD DOWN $3.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 15/WITH GOLD UP $10.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 105.12 TONNES

DEC 12/WITH GOLD UP $14.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.83 TONNES

DEC 11/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 10/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 9/WITH GOLD UP $18.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.14 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1049.11 TONNES

DEC 8/WITH GOLD DOWN $23.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.33 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1050.25 TONNES

DEC 5/WITH GOLD UP $9.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 4.00 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.58 TONNES

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

GLD INVENTORY: 1079.66 TONNES, TONIGHTS TOTAL

SILVER

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 17/WITH SILVER UP $2.93/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 16/WITH SILVER DOWN $.07/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 56.360 MILLION OZ //

DEC 15/WITH SILVER UP $1.62/SMALL CHANGES IN SILVER AT THE SLV: A SMALL DEPOSIT OF 635,000 INTO THE SLV. ./ :INVENTORY RESTS AT 517.720 MILLION OZ //

DEC 12/WITH SILVER DOWN $2.30/NO CHANGES IN SILVER AT THE SLV: ./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 11/WITH SILVER UP $3.52/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.537 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 9/WITH SILVER UP $2.41/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.179 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 510.828 MILLION OZ //

DEC 8/WITH SILVER DOWN $0.48/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 5.497 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 512.007 MILLION OZ //

DEC 5/WITH SILVER UP 0.39/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.083 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.448 MILLION OZ //

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

CLOSING INVENTORY 517.758 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

ALASDAIR MACLEOD..

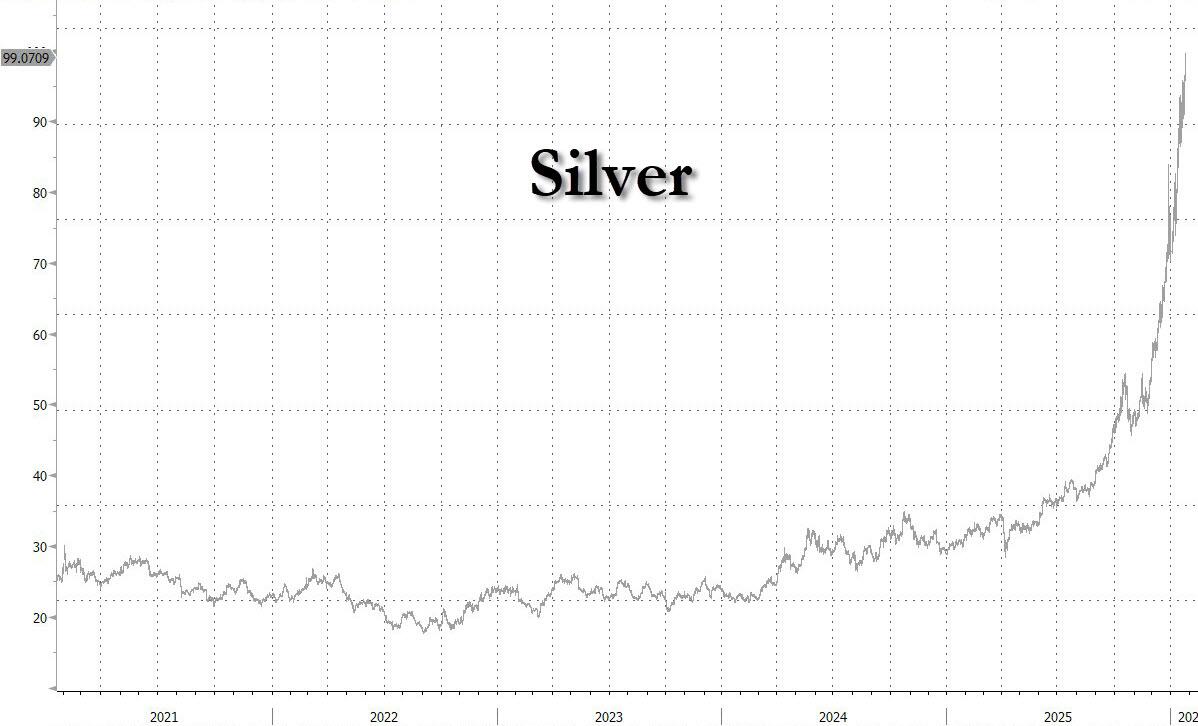

Gold and silver surge ahead

Amid signs of an intensifying derivative crisis in silver, gold is probably beginning to discount disruption in paper markets. Western speculators are sidelined.

| Alasdair MacleodJan 23∙Paid |

Looking into the guts of COT reports, we see that the increase in Comex open interest in gold does not much reflect managed money buying into momentum. It rather reflects Globex trade, predominantly Asian in origin buying futures presumably with a view to taking delivery.

Is this why Comex stopped reporting stand-for-deliveries from 15th January in both contracts? Is it a warning sign of derivative problems?

Gold and silver continued to rise this week, both establishing new record prices in all currencies. In early morning European trade, gold closed out the week at $4915, up $308, and silver at $98.20 is up $8.10. Overnight, they hit $4967 and $99.30 respectively.

On Comex, volumes in both contracts were high, but declining somewhat in silver as the price rose, evidence of an intensifying squeeze on paper shorts.

Why is it that hedge funds are not playing the silver game? It is reasonable to suggest that they should be making hay out of this short squeeze, but they appear not to. Instead, they seem scared by silver’s sheer volatility.The next chart continues to illustrate this fact:

To this evidence we can add the managed money longs from the CFTC’s Commitment of Traders numbers. They are approaching the lowest levels seen in the last 20 years:

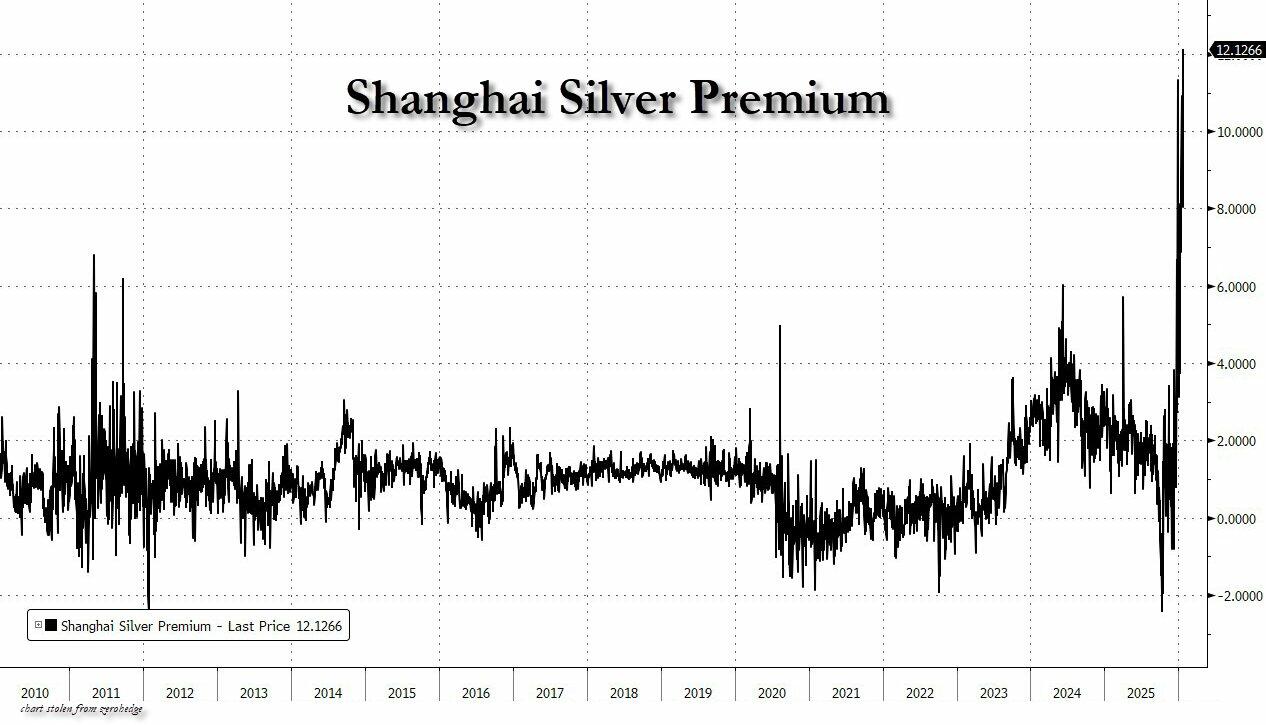

Furthermore, the smart money leading the charge is in China where silver prices are a good 10% higher than in seemingly reluctant London and Comex.

We cannot say for certain that China is setting out to destroy Western capital markets, but there is supporting evidence that they are being unfriendly toward our financial system. They have established a non-dollar payment system which is increasingly being used in what appears to be an alternative for the global south to the fiat dollar for trade settlement balances. And they are starving the West of rare earths, presumably extended to silver policy. It means the dollar is becoming sidelined and sold down, a process that may be accelerating.

Further evidence that the West is frozen out of the action is seen in gold. The next chart shows US managed money longs on Comex:

While there has been an uptick in the net position since end-October, as an overbought/oversold indicator it is level with the long-term average. The position of the other and non-reported categories confirms that most of the long interest is there:

It is these categories that contain non-US and most of non-European interest including central banks, national wealth funds, and Asian family-offices.

So far, we have assumed that bullion banks and market makers in the swaps category are covered long in London forwards, though their short position on Comex is now positively scary:

Being long in London and short on Comex depends on the integrity of both markets being maintained, which in turn relies on counterparty risk not escalating. We can only guess how Comex feels about its potential liability in the event of counterparty failure and whether it will be prepared to destroy its own credibility by declaring force majeure, which it can do within its own rules. The LBMA and the Bank of England must be monitoring London’s forward markets with some concern as well.

In the end-game of the fiat currency era, these market disruptions are an interim event in the overall decline. However, the spread of counterparty risk throughout the entire derivative system would hasten the demise of credit, including the value of fiat currencies. We have yet to see investment managers take on board this risk and respond by the only way they can, which is to attempt to acquire physical gold and silver.

This panic of some $300 trillion in global investment portfolios desperately increasing their less than 1/2% exposure is yet to come. And when it does, it will be epic.

MATHEW PIPENBURG/EGON VON GREYERZ

3.CHRIS POWELL AND HIS GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 255 AND 256

pETER KRAUTH

LIVE FROM THE VAULT YOU TUBE: 256

Episode 256

Posted 23rd January 2026

Could Silver Climb Even Higher? Feat. Peter Krauth

In this week’s Live from the Vault, Andrew Maguire welcomes back Peter Krauth to explain why silver surges past key caps, climbing relentlessly since February 2024 as long-term supply-demand fundamentals suggest a possible upward trend.

Peter highlights key drivers including AI, solar, and data centre demand, alongside limited supply and underperforming mining stocks, pointing to a bullish environment that could support higher silver prices and opportunities for investors.

5. COMMODITY REPORT//:silver

THIS HURTS:

Silver Museum Emptied in Massive Heist

by VBL

Thursday, Jan 22, 2026 – 11:49

**Silver Museum Emptied in Massive Overnight Heist

Massive Silver Burglary in Netherlands

GFN – DOESBURG (Netherlands) – In the early hours of Wednesday, 21 January 2026, the Zilvermuseum Doesburg, a small museum housed inside the historic Martinikerk in the Gelderland town of Doesburg, was completely robbed of its antique silver collection in what authorities are treating as a major burglary. The theft — involving more than 300 precious silver objects representing centuries of craftsmanship from around the world — has left museum officials, local authorities, and heritage advocates stunned.

GoldFix is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

At approximately 4:30 a.m., two unknown individuals forced their way into the church through a tower entrance, used a crowbar to breach the museum’s doors, and smashed all 14 display vitrines before departing with the entire silver collection, police and museum statements confirm.

“The entire collection of antique silver has been stolen.”

— Museum press release, Zilvermuseum Doesburg (translated)

A Cultural Loss Beyond Its Weight in Silver

The collection, assembled over decades and sourced from more than 20 countries, featured objects ranging from ornate silver mustard pots and spoons to intricate cruet sets tied to the butter, vinegar, and tobacco trades. Among the stolen pieces was a unique silver mustard pot and spoon specially designed for the museum by silversmith Marcel Blok, symbolizing the meandering IJssel River and bearing the city coat of arms of Doesburg — an item that “does not exist anywhere else in the world.”

“This is not just a theft of silver, but of stories, craftsmanship, and history.”

— Martin de Kleijn, Founder of Zilvermuseum Doesburg

Museum chairman Ernst Boesveld told local media that only some ceramics on temporary display were left undisturbed by the thieves, and that the museum is now closed indefinitely as investigators work the scene. He emphasized that while financial loss from the theft — estimated in the tens of thousands of euros — is significant, the emotional and historical damage is far greater.

Crime Scene, Investigation, and Security Gaps

Police were called soon after the burglary and have begun combing through the surrounding area for video surveillance footage that could help identify suspects. A spokesperson told Dutch broadcasters that the thieves briefly appeared in footage before disabling the cameras. No arrests have been reported as of the latest updates, and investigators have not yet determined if the burglary was precisely planned by insiders or opportunistic.

Authorities are appealing to witnesses who may have been near the Martinikerk around the time of the burglary to come forward with information, including any sightings of suspicious individuals or recently offered silver items for sale.

Historical and Material Context

The Zilvermuseum, though modest in scale, occupies a floating glass structure within the 13th-century Martinikerk and had become a cherished locus for cultural tourists and local residents alike. Its exhibits offered rare insight into the evolution of silver craft, both utilitarian and ceremonial, from the 18th through early 20th centuries.

Silver’s recent surge in price — spurred by investor demand amid geopolitical uncertainty — complicates the aftermath of the theft. While the museum stressed that the cultural and historical value cannot be quantified in monetary terms, a higher bullion price inherently increases the financial damage and may tempt thieves to sell or melt objects rather than attempt resale through legitimate channels.

Reactions and Heritage Significance

Local cultural advocates voiced deep regret that centuries-old artifacts documenting craftsmanship and social history were lost in a matter of minutes. Some commentators note that museum security, while adequate for daily visitors, was insufficient to deter determined intruders with tools and foreknowledge. Comparisons to other high-profile European museum heists — where thieves specifically target small collections for metallurgical resale value — are already emerging in Dutch cultural discourse.

“They have made a very substantial haul,” a police spokeswoman told RTL Nieuws, reflecting on the breadth of the stolen works but stopping short of suggesting motive or sophistication.

Heritage professionals warn that silver items stripped of provenance and melted down are among the hardest to recover, underscoring the urgency of public reporting and international cooperation in art crime investigations..

More here

END

SILVER

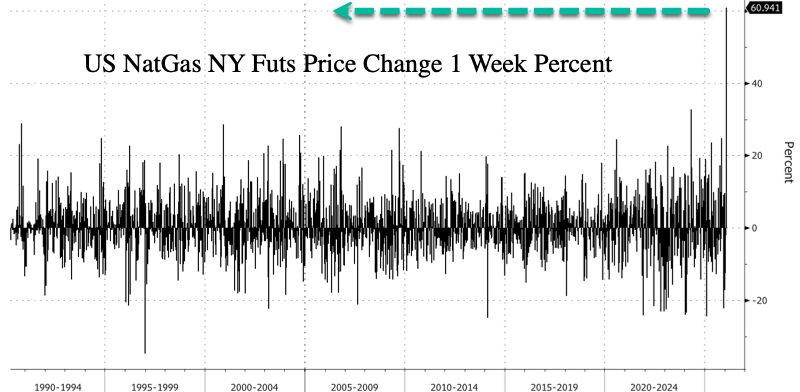

Silver Tops $100 As Chinese Demand Is Literally ‘Off The Charts’

despite record highs prices, Goldman’s commodity trading desk notes that spec positioning in New York and Shanghai remains close to the lows.

5B. COMMODITY REPORT//GOLD OR /SILVER LEASE RATES:/GOLD

GOLD LEASE RATES CLIMB TO AROUND 3.0 TO 4.0%

| Robert Lambourne | 7:56 AM (4 minutes ago) | ||

| to me | |||

Harvey,

Interesting comment for you on gold from Chinese AI. Gold lease rates are ticking up in all markets, c3%/4% and inventories draining. Reportedly demand in Asia is strong, including Japan as confidence in bonds there is probably fraying. Possibly gold is slightly under the radar here because of silver.

I’ve no idea how Trump will handle his latest tariff threats re Greenland, but the situation seems quite unstable. Gold might well move strongly here.

No December 2025 BIS gold swap data yet. I’ve emailed Chris to suggest it might only appear right at the month end. This is no great surprise, but we can guess plausibly that the BIS will be under some pressure to end the gold swaps. Whatever you think about Jerome Powell, his influence is already reduced and this will also apply to any successor when they attend the BIS meetings.

Regards,

Bob

2.ASIAN AFFAIRS JAN 23/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 13.59 PTS OR 0.33%

//Hang Seng CLOSED UP 119.55 PTS OR 0.45%

// Nikkei CLOSED UP 185.61 PTS OR 0.35%

//Australia’s all ordinaries CLOSED UP 0..07%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9655

/ OFFSHORE CLOSED UP AT 6.9520 Oil UP TO 60.15 dollars per barrel for WTI and BRENT UP TO 64.81 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING UP TO 6.9655 OFFSHORE YUAN TRADING UP TO 6.9520 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.9655

OFFSHORE YUAN: UP TO 6.9520

HANG SENG CLOSED UP 119.55 PTS OR 0.45%

2. Nikkei closed UP 185.61 PTS OR 0.35%

WEST TEXAS INTERMEDIATE OIL UP 60.15

BRENT; 64.81

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 98.18 /// EURO FALLS TO 1.1771 DOWN 23 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.256/ UP 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.10… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.677 DOWN 2 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8998 Italian 10 Yr bond yield UP to 3.5141 SPAIN 10 YR BOND YIELD UP TO 3.278

3i Greek 10 year bond yield UP TO 3.408

3j Gold at $4829.95 Silver at: 98.45 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 13/100 roubles/dollar; ROUBLE AT 75.86

3m oil (WTI) into the 60 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.10 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.256% DOWN 8 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.647 DOWN 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7912 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9282 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.239 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.826 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.613 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.27 DOWN 0 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.490 UP 2 PTS

30 YR UK BOND YIELD: 5.231 UP 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.411 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.939 DOWN 1 BASIS PTS.

1a New York OPENING REPORT

Futures Drop As Intel Plunges, Silver Just Under $100

Friday, Jan 23, 2026 – 08:38 AM

US stock futures are lower with tech stocks lagging as Intel plunged 14% after the chipmaker warned it was struggling with manufacturing problems leading to poor Q1 guidance. As of 8:00am ET, S&P and Nasdaq futures are down 0.1% but off session lows (and well off session highs), paring losses as Nvidia shares gained after Bloomberg reported Chinese officials have told the country’s largest tech firms they can prepare orders for Nvidia’s H200 AI chips. Mag 7 are mixed with NVDA leading gains after Chinese officials were said to have told the country’s largest tech firms, including Alibaba Group Holding Ltd., they can prepare orders for Nvidia Corp.’s H200 AI chips. Bond yields are mostly unchanged; USD is flat. Japan’s top currency official declined to comment on whether the government stepped into the market after USD/JPY plunged over 150 pips in just a few minutes. The pair swiftly bounced and is now around 158.30 having topped 159 during the Bank of Japan press conference after Governor Ueda didn’t offer any clear signal that an early rate hike was possible. The pound sits atop the G-10 FX pile, rising 0.2% against the greenback after PMI topped estimates and hawkish remarks from BOE’s. Commodities are mostly higher led by Oil (+1.5%); both base metals and precious metals are higher with silver trading just under $100/oz. The key macro focus today were global PMIs.

In premarket trading, Magnificent Seven stock are mixed: Nvidia gains 1.5% after Chinese officials were said to have told the country’s largest tech firms, including Alibaba Group Holding Ltd., they can prepare orders for Nvidia Corp.’s H200 AI chips (Tesla -0.1%, Microsoft +0.04%, Amazon +0.1%, Alphabet +0.01%, Apple -0.08%, Meta -0.5%)

- Solar stocks are extending gains after Elon Musk commented on solar-powered satellites in his Davos talk on Thursday. Array Technologies (ARRY) +2%, First Solar (FSLR) +1.4%.

- Booz Allen (BAH) rises 5% after the defense contractor boosted its adjusted earnings per share guidance for the full year, with the new outlook beating the average analyst estimate.

- Capital One Financial Corp. (COF) falls 2% after the bank reported adjusted earnings per share for the fourth quarter that missed the average analyst estimate, driven by higher-than-expected costs. The firm also said it agreed to acquire Brex.

- CSX Corp. (CSX) gains 2% after the freight transportation company provided some guidance for 2026, including low single-digit revenue growth.

- Intel (INTC) plunges 13% after Chief Executive Officer Lip-Bu Tan gave a lackluster forecast and warned that the chipmaker was struggling with manufacturing problems. The stock closed Thursday at the highest level since 2022.

- Intuitive Surgical (ISRG) gains 1.5% after the medical equipment firm reported adjusted earnings per share for the fourth quarter that surpassed estimates. Analysts note that the results were largely in line with the company’s pre-announcement.

In corporate news, Amazon.com is gearing up to ax thousands more corporate employees, ratcheting up efforts to streamline bureaucracy. Apple accused the European Commission of using “political delay tactics” to postpone new app policies as a pretense to investigate and fine the iPhone maker. TikTok and its Chinese parent ByteDance have closed a long-awaited deal to transfer parts of their US operations to American investors, securing the popular video app’s future in the US and avoiding a nationwide ban.

Even with the S&P just shy of all time highs, investors have been quietly trying to sidestep bouts of volatility driven by US policies, highlighted this week by Trump’s push to assert greater control over Greenland. While the outlook for US stocks remains strong, traders are also looking elsewhere for pockets of calm and opportunity.

“I hope that the geopolitical situation starts to ease so that the market can focus on substance versus noise,” said Andrea Gabellone, head of global equities at KBC Global Services. “Full-year 2026 guidances are, in my view, the most crucial piece of data the market has been waiting for quite some time, given valuations and growth expectations.”

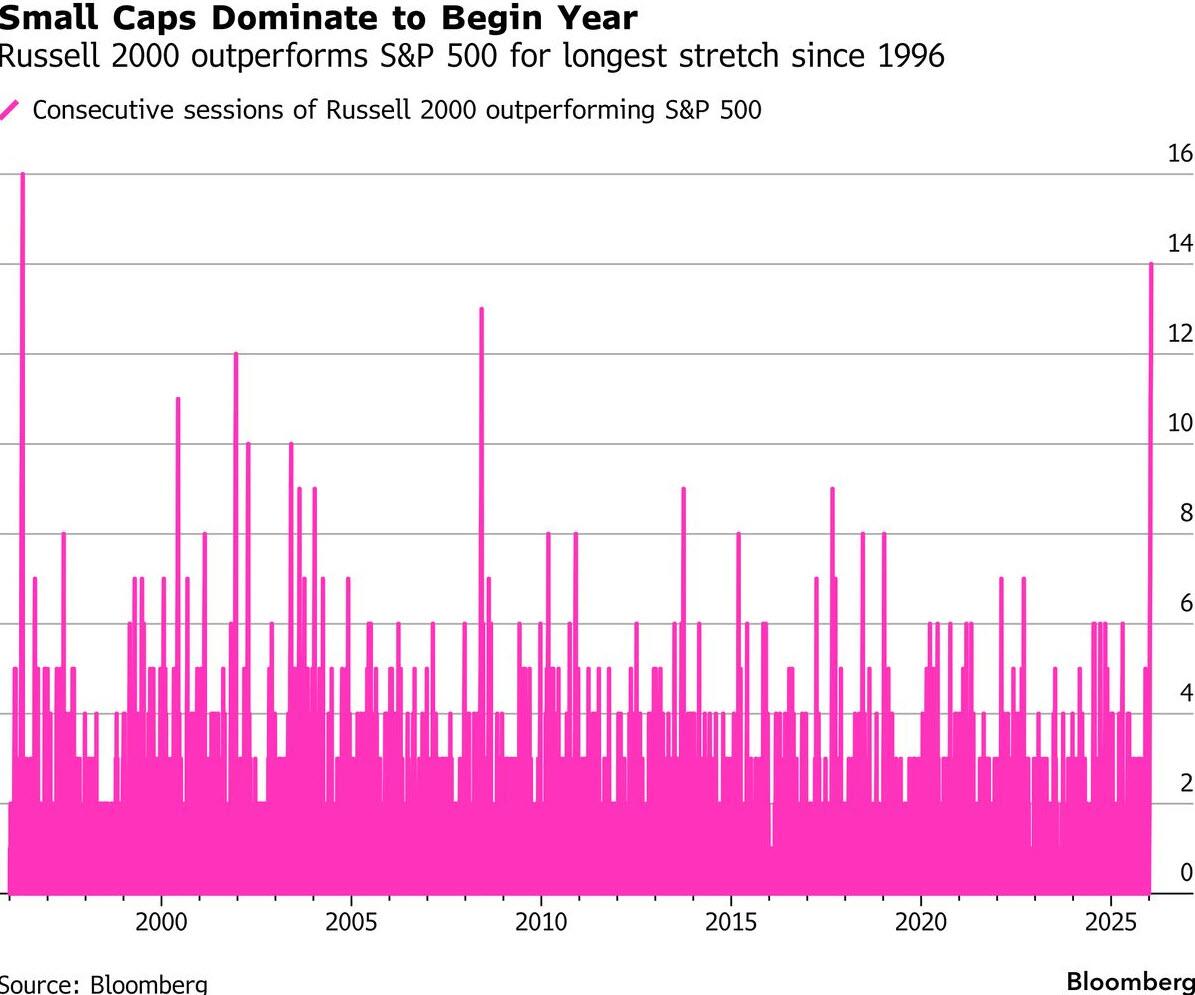

Small caps extended a winning streak over large-cap cohorts amid concern about a possible AI bubble and bets that an economic recovery will filter to broader swathes of the economy. The Russell 2000’s outperformance of the S&P 500 in 2026 is the longest such streak in 30 years.

“Typically, safe bonds and Treasuries have been a source of diversification during times of uncertainty, but particularly Treasuries haven’t provided any cushion over the past days,” said Philipp Lisibach, head of strategy and research at LGT Private Banking. “That’s also why gold continues to rally.”

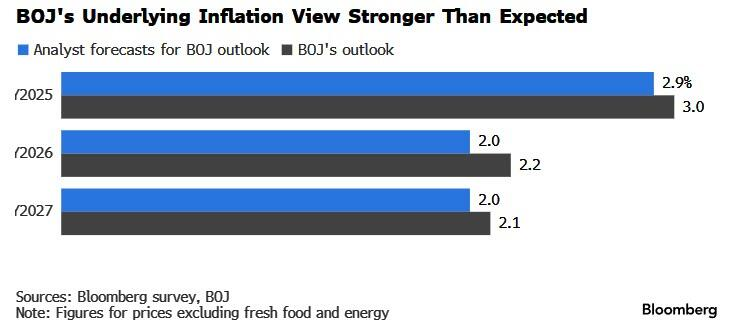

In Asia, the Bank of Japan maintained its benchmark rate and issued higher inflation forecasts. While Governor Kazuo Ueda suggested that inflation will weaken below 2% soon, he also left open the possibility of an early rate hike. “The challenge is balancing rate hikes to support the yen without slowing growth,” wrote Min Joo Kang, senior economist at ING Bank. “Timing is uncertain, but we now see a June hike as the base case.”

Elsewhere, the US wants to rewrite its defense agreement with Denmark to remove any limits on its military presence in Greenland, people familiar with the matter said. And the Kremlin said the “territorial issue” remains unresolved after Putin held late-night talks with US envoys Steve Witkoff and Jared Kushner about the latest plan to end Russia’s war on Ukraine. Talks continue between US, Russian and Ukrainian representatives in the United Arab Emirates on Friday and Saturday.

Trump said he has finished interviewing candidates to serve as the next Fed chair and reiterated that he has someone in mind for the job. His shortlist includes National Economic Council Director Kevin Hassett, BlackRock executive Rick Rieder, current Fed Governor Christopher Waller and a former governor, Kevin Warsh.

The Stoxx 600 falls 0.1%. Telecoms and energy sectors outperform, while travel and consumer product shares lag. The focus fell on the Amsterdam debut of armored vehicle and munitions maker CSG NV. The stock opened 28% higher after the largest-ever initial public offering globally for a pure-play defense firm, highlighting growing appetite for the sector. Here are the biggest movers Friday:

- Ericsson shares surge as much as 12% after the telecom equipment maker reported stronger-than-expected sales in the core networks division, driven by mission-critical projects

- Siemens Energy gains as much as 2.6% to a record high after UBS raised its recommendation to buy from sell and lifted its PT to €175 from €38

- SFS Group shares gain as much as 7.4%, hitting their highest level since May, after analysts said the Swiss tool and component supplier delivered stronger growth than expected in a challenging market

- SSP shares climb as much as 4.1%, the most in a month, after the travel food and beverage outlet operator reported first-quarter results which showed continued positive trading momentum and reassured analysts

- Watches of Switzerland shares rise as much as 6.4% to the highest level since February 2025 after the luxury watch seller acquired Deutsch & Deutsch, a retailer with four showrooms and Rolex distribution in Texas

- Castellum gains as much as 2.6% after Goldman Sachs upgraded its view on the Swedish property firm to buy from neutral in a review of the European real estate sector, where it also upgrades Colonial to neutral from sell

- Babcock International shares drop as much as 3.8% after the support services company said CEO David Lockwood is retiring and will be succeeded by the head of its Nuclear division, Harry Holt

- Edenred shares fall as much as 3.2%, while Pluxee declines as much as 4.7% as UBS downgrades both French-listed meal-voucher stocks, saying the regulatory “tide is turning” against the sector

- C&C Group shares plunge as much as 18%, briefly slumping to their lowest level since 2009, after the alcoholic beverage maker said trading has been worse than expected

Earlier, Asian stocks gained for a second consecutive session, erasing their losses for the week, as fears over tariffs and Greenland faded.

The MSCI Asia Pacific Index gained 0.4% on Friday, with Alibaba, MediaTek and TSMC among the biggest boosts. Korea’s Kospi advanced to a fresh record near the 5,000 level. Stocks also gained in Taiwan, Japan and Hong Kong. The regional gauge is on track to end the week steady after rising for four straight weeks. Investors are shifting focus back to earnings and the outlook for the artificial intelligence trade after US President Donald Trump backed off from putting tariffs on European nations due to tensions over Greenland. Meanwhile, most central banks in the region are cutting rates and economic growth is expected to improve. Equities rose in Tokyo as the yen weakened after the Bank of Japan held interest rates steady as expected. The Straits Times Index rose to a record as Singapore started handing out some of the S$5 billion it plans to invest in local stocks to selected fund managers.

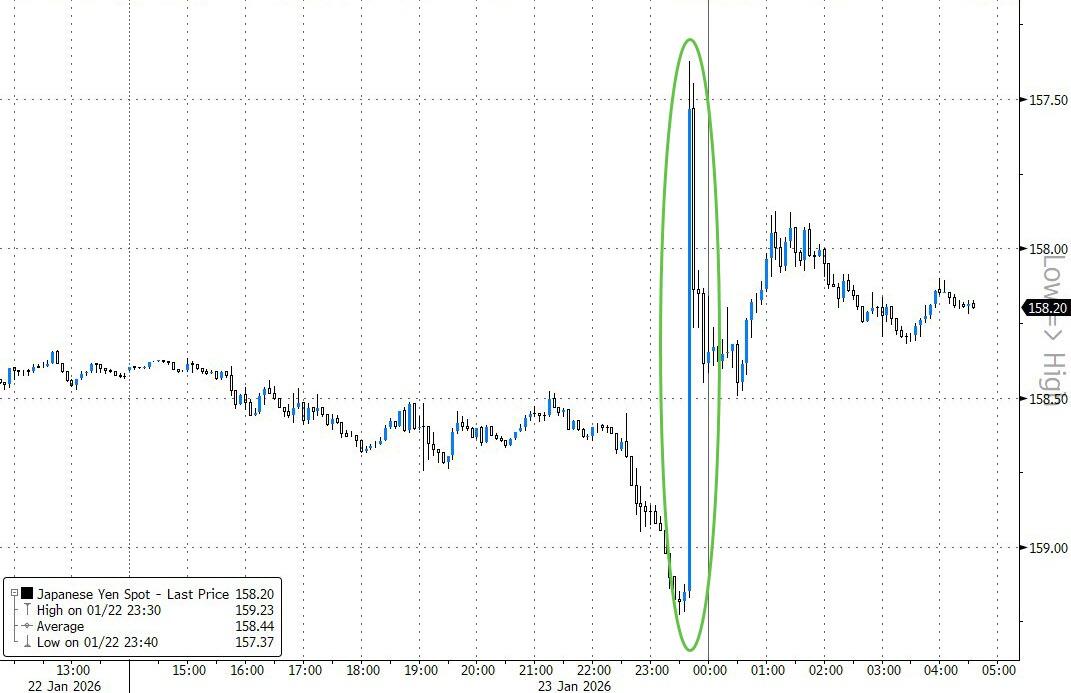

In FX, Japan’s top currency official declined to comment on whether the government stepped into the market after USD/JPY plunged over 150 pips in just a few minutes. The pair swiftly bounced and is now around 158.30 having topped 159 during the Bank of Japan press conference after Governor Ueda didn’t offer any clear signal that an early rate hike was possible. The pound sits atop the G-10 FX pile, rising 0.2% against the greenback after PMI topped estimates and hawkish remarks from BOE’s Greene that also weighed on shorter-dated gilts.

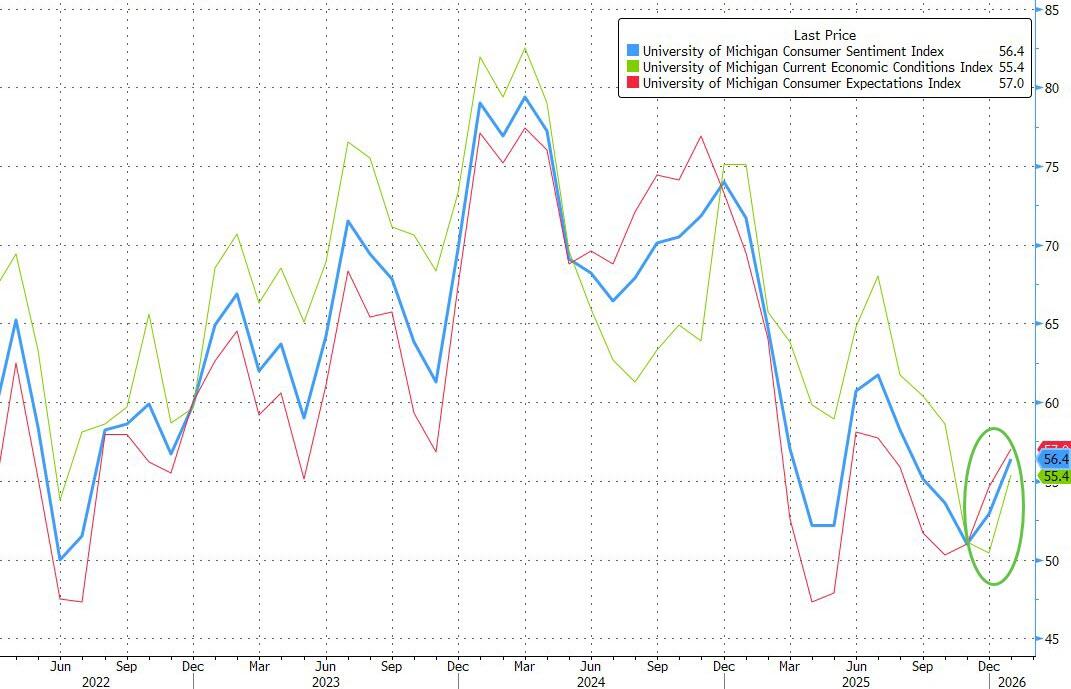

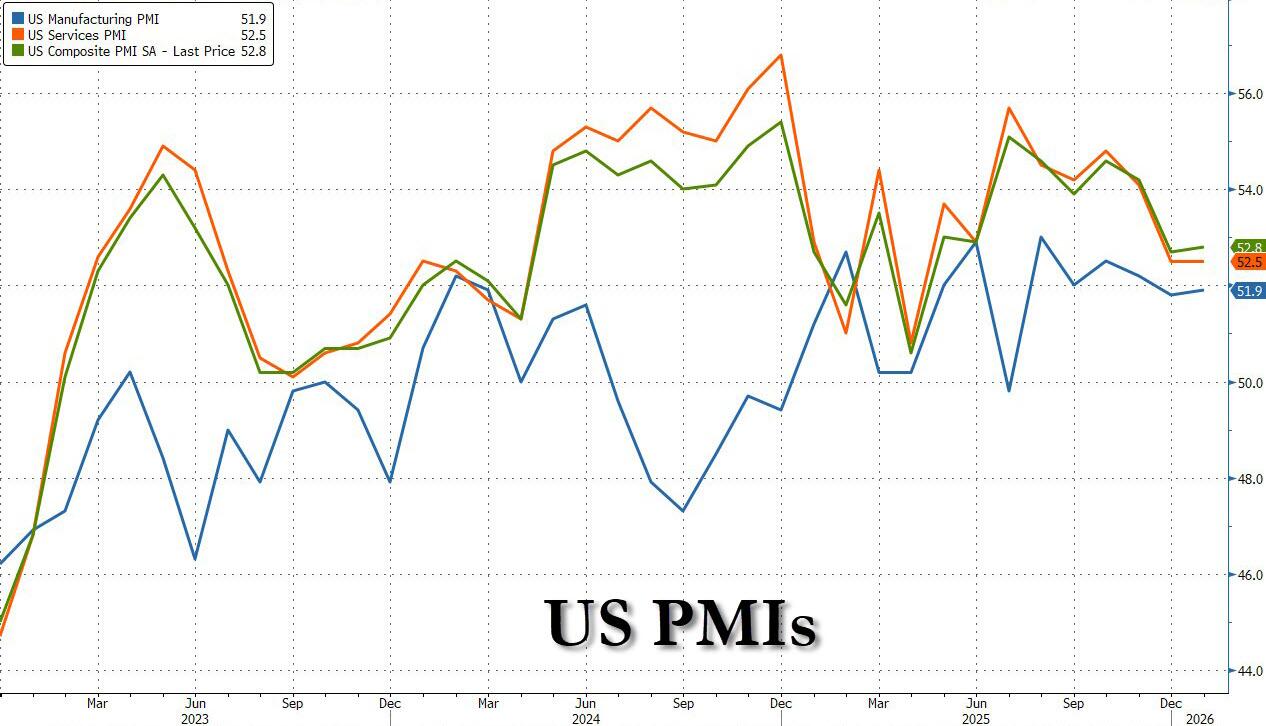

In rates, the yield on 10-year US Treasuries hovered near the highest since September, holding small gains with long-end yields about 2bp richer on the day, flattening the curve. European bonds underperform following UK retail sales and European PMI gauges. US stock futures little changed while crude oil is up nearly 2%.US yields are 1bp-2bp richer across the curve with 2s10s and 5s30s spreads flatter by about 1bp; 10-year near 4.23% is 1.7bp lower on the day with German counterpart little changed and UK cheaper by about 1bp. Focal points of US session include S&P Global US PMIs and University of Michigan sentiment gauge, as well as next week’s supply — both corporate and Treasury coupon auctions scheduled to start Monday.

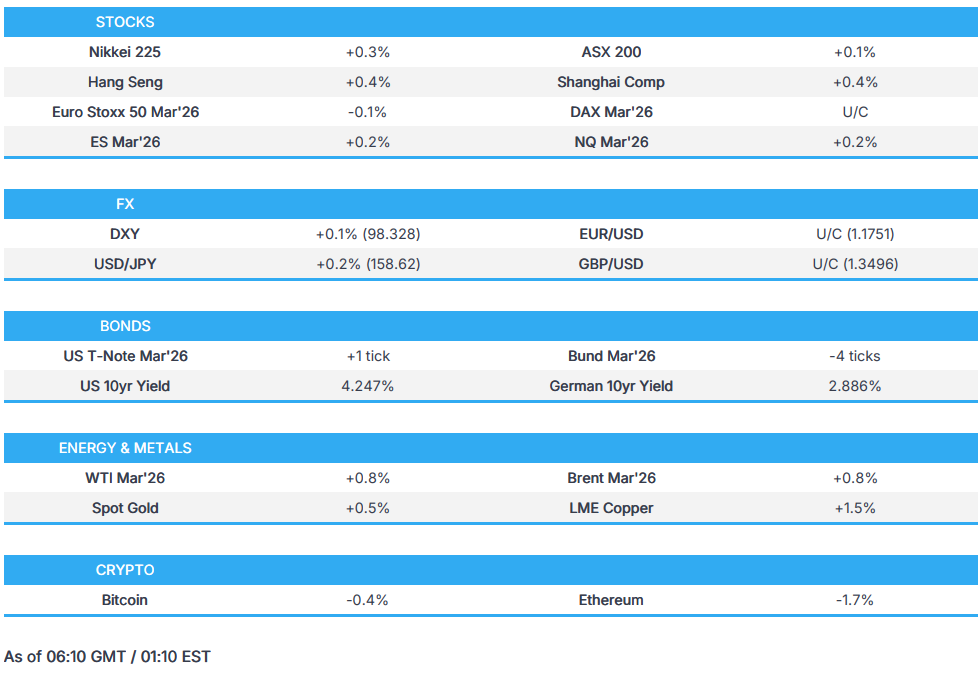

In commodities, spot silver rises 2.5% while gold erased an earlier gain to trade lower. Silver rose just shy of $100 and will likely surpass the key level today…

… as the Shanghai silver premium jumped 50% overnight to a record 12.

Precious metals are expected to remain in demand should investors continue to diversify away from US assets in response to erratic US policy and heightened geopolitical risk.Renewed concern about the possibility of US military action against Iran is spurring oil prices. WTI crude futures rise 1.7% to near $60.40; and Brent is at $65 in New York.

Today’s economic calendar includes January preliminary S&P Global US PMIs (9:45am), November Leading Index, January final University of Michigan sentiment (10am) and Kansas City Fed services activity (11am). Friday is slower for company earnings, with SLB slated to report before the market opens. Capital One’s fourth-quarter revenues came in slightly higher than expected, but EPS missed, and the bank agreed to buy Brex, a fintech company focused on corporate expense management and accounting, for $5.15 billion.Next week is the busiest of this earnings season, when companies speaking for more than a third of the S&P 500’s total market value will report.

Market Snapshot

- S&P 500 mini -0.1%

- Nasdaq 100 mini -0.1%

- Russell 2000 mini -0.2%

- Stoxx Europe 600 -0.3%

- DAX -0.2%

- CAC 40 -0.5%

- 10-year Treasury yield -1 basis point at 4.24%

- VIX +0.5 points at 16.16

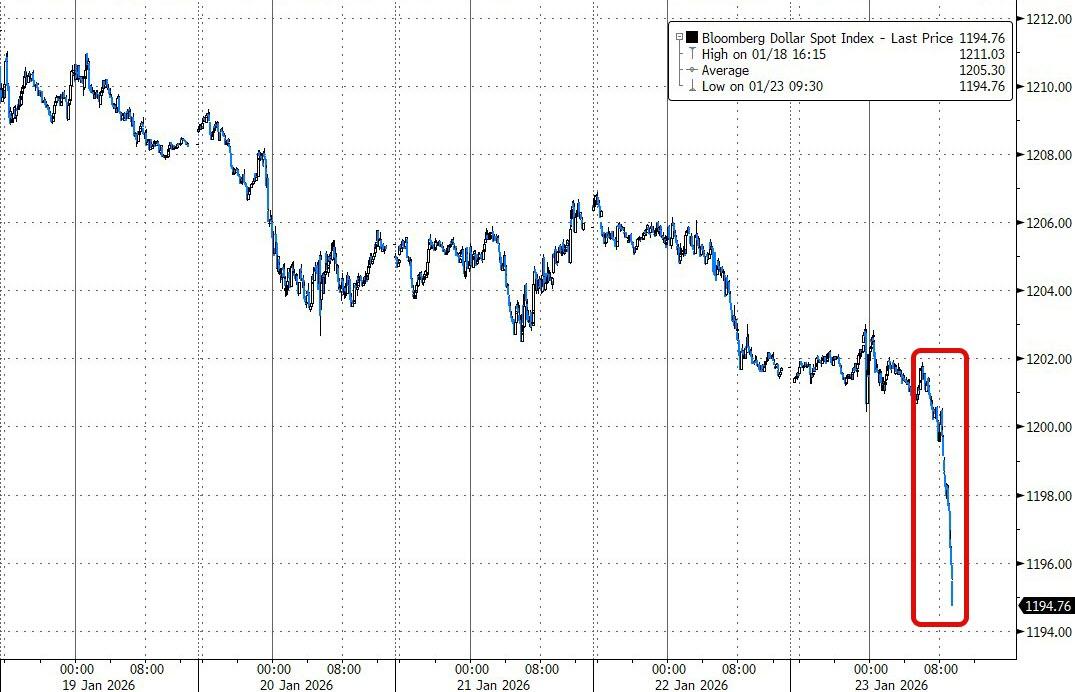

- Bloomberg Dollar Index little changed at 1201.56, euro -0.2% at $1.1735

- WTI crude +1.4% at $60.2/barrel

Top Overnight News

- Russia said it will hold security talks with the U.S. and Ukraine in Abu Dhabi on Friday, but warned after a late-night meeting between President Vladimir Putin and three U.S. envoys that a durable peace would not be possible unless territorial issues were resolved. RTRS

- The US wants to rewrite its defense agreement with Denmark to remove any limits on its military presence in Greenland, people familiar said. It currently says the US must “consult with and inform” the two. Donald Trump also mused on social media about invoking NATO’s collective defense clause to protect the US’s southern border. BBG