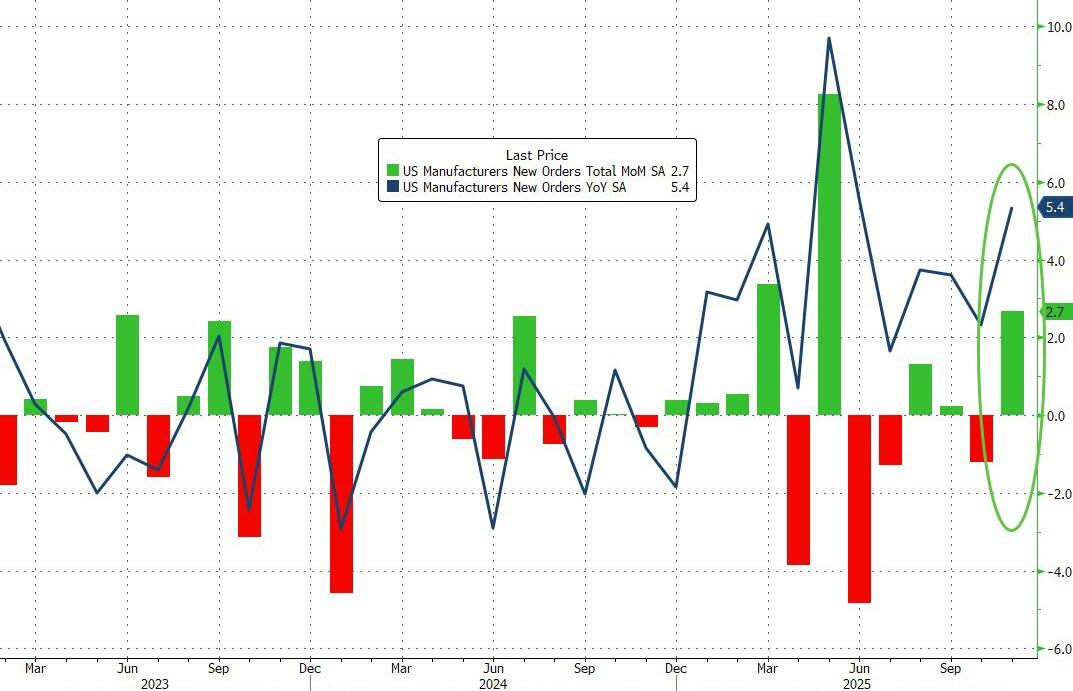

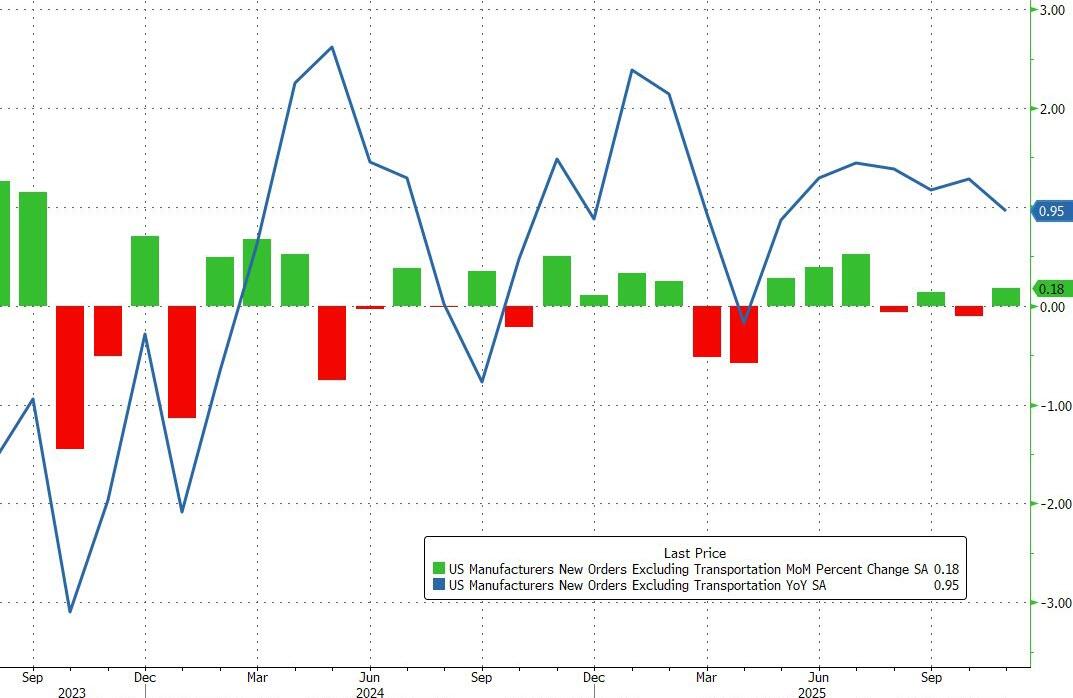

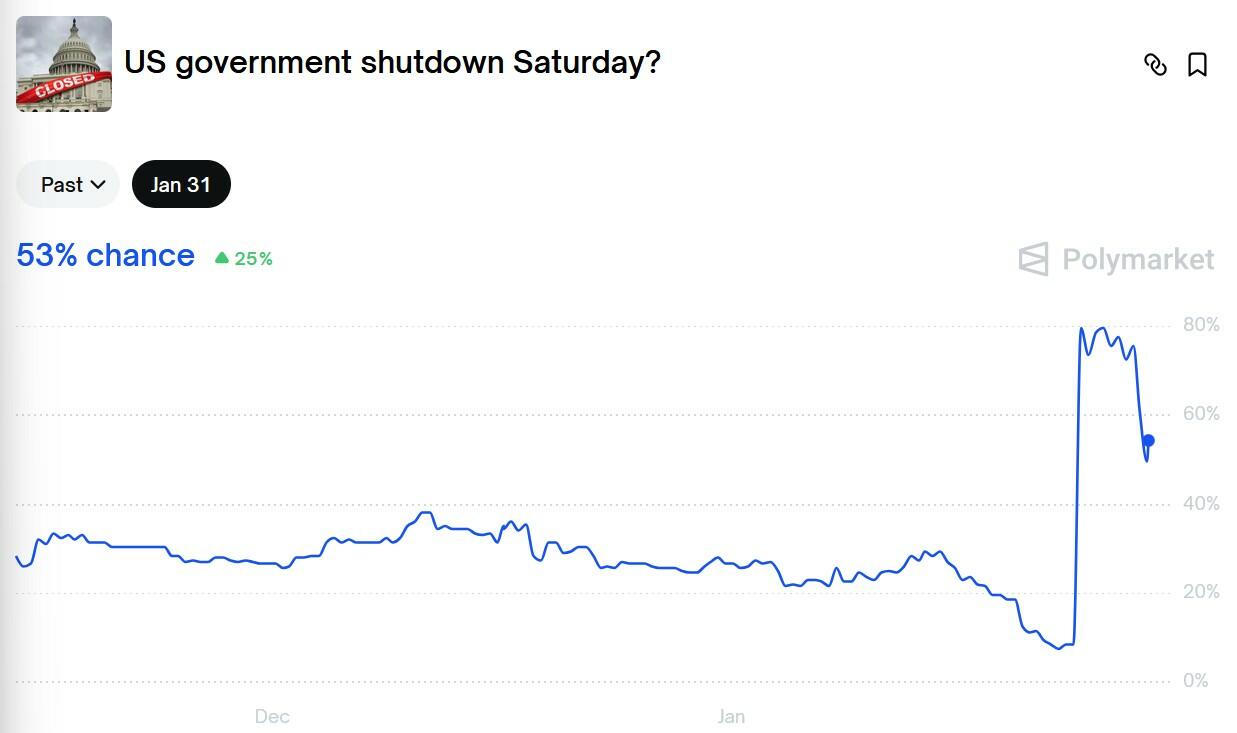

JAN 29//ATTEMPTED RAID ENDS IN FAILURE; GOLD CLOSED UP $23.65 TO $5329.75 WTH SILVER UP $2.80 TO $115.50//PLATINUM HOWEVER FELL BY $207.65 TO $2613.80 WHILE PALLADIUM ALSO SUFFERED A LOSS OF $124.05 TO $2013.65//SILVER INVENTORY AT THE COMEX CONTINUES TO DECLINE WITH REGISTERED SILVER AT 108 MILLION OZ//GOLD COMMENTARY TONIGHT COURTESY OF ALASDAIR MACLEOD//WAR DRUMS BEATING HARD AND A THREAT OF THE CLOSING OF THE STRAIT OF HORMUZ CAUSES OIL TO BREAK OUT WITH BRENT OIL CLIMBING ABOVE $70.00//IRAN VS USA UPDATES//ISRAEL VS HAMAS UPDATES//USA DATA RELEASE: HUGE INCREASE IN FACTORY ORDERS//USA STARTS TALKS WITH DENMARK ON THE SECURITY ARRANGEMENT IN THE ARCTIC//LOOKS LIKE THE USA IS GOING TO HAVE ANOTHER SHUTDOWN//SWAMP STORIES FOR YOU TONIGHT//

*CANADIAN GOLD: $7229.70 DOWN 69.50 CDN dollars per oz( * NEW ALL TIME HIGH $7290.00CDN DOLLARS PER OZ//JAN 28/2026)

*BRITISH GOLD: 3880.00 DOWN $110.00 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING//3999.00 BRITISH POUNDS/OZ) JAN 28.2027/2025

*EURO GOLD: 4477.75 DOWN 24.00 Euros per oz //* (ALL TIME CLOSING HIGH: 4501.00 EUROS PER OZ/ JAN 28//2026)

Bitcoin morning price:$88,001 DOWN 1266 DOLLARS (MANY SWITCHING TO PHYSICAL GOLD)

Bitcoin: afternoon price: $83,933 down 5334 DOLLARS (a massive drop in value)

Platinum price closing UP $48.60 TO $2,821.45

Palladium price; UP $109.25 TO $2137.10

END

EXCHANGE: COMEX

NIL

JPMORGAN STOPPED 2/25

JANUARY

GOLD: NUMBER OF NOTICES FILED FOR JANUARY/2026: 0 CONTRACTs NOTICES FOR 0 OZ or 0.000 TONNES

total notices so far: 11,851 contracts for 1,185,100 OR 36.861 tonnes)

FOR JANUARY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 246 NOTICE(S) FILED FOR 1.230 MILLION OZ OZ/

total number of notices filed so far this month : 9854 CONTRACTS (NOTICES) for 49.270 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $23,65 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 1089.96TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $2.80 AT THE SLV: HUGE CHANGES AT THE SLV: A FRAUDULENT WITHDRAWAL OF 6.798 MILLION OZ FROM THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 502.712 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 135 CONTRACTS TO 156,772 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS MEGA SMALL SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE $5.60 GAIN IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S // TRADING.

THE LONG SPECULATORS ARE STILL QUITE RELENTLESS AS THEY POUR INTO THE OPEN INTEREST AT THE COMEX AS YOU WILL WITNESS WITH TODAY’S TRADING. THE FRBNY CONTINUES TO SUPPLY THE NECESSARY PAPER AS THEY TRY TO DRIVE THE PRICE SOUTHBOUND WITH THE HELP OF HIGH FREQUENCY TRADERS , T.A.S. SPREADERS AND NOW MONTH END SPREADERS.

WE HAVE REVERTED BACK TO NORMAL WITH THE SPECS NOW GOING ON THE LONG SIDE AND THE BANKER (FRBNY) ON THE SHORT SIDE AND PROVIDING THE NECESSARY SHORT PAPER.

IT IS OUR SILVER SPECULATORS THAT WERE PILING INTO THE SILVER COMEX. WE FINALLY ARE MOVING TO A MUCH HIGHER BASE SURPASSING THE $34.40 SILVER PRICE BARRIER TO A HIGH DEGREE, AND NOW SURPASSING OUR LAST MAJOR HURDLE OF $100.00 SILVER.

WE HAVE A HUGE SIZED GAIN OF 961 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE SIZED 826 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY TRADING WITH OUR HUGE GAIN IN PRICE ALONG WITH COMMENCEMENT OF SPREADER LIQUIDATION /// THEY DESPERATELY AGAIN TODAY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON WEDNESDAY WITH SILVER’S HUGE GAIN IN PRICE AS THE SPECS PILED INTO THE SILVER ARENA. .

THE PRICE FINISHED STILL HUGELY ABOVE THE MAGIC NUMBER OF $50.00 SILVER SPOT PRICE CLOSING AT $112.70 UP $5.60 WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS AT A MAMMOTH SIZED 5708 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING AGAIN THE 100.00 DOLLAR MARK!!.MAMMOTH SIZE T.A.S ISSUANCE IS BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A HUGE SIZED 826 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUMONGOUS SIZED 5708 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//RAID AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HAD A HUGE SIZED GAIN OF 961 CONTRACTS ON OUR TWO EXCHANGES WITH OUR HUGE GAIN IN PRICE OF $5.60 WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION AND NO DOUBT REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE SPECULATOR LONGS STILL REMAIN STOIC EVEN ON OUR HUGE PRICE FALLS. EASTERN CENTRAL BANKER WENT TO THE LONG SIDE. THEY WILL TENDER FOR THE BADLY NEEDED PHYSICAL SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT//THURSDAY MORNING: A MAMMOTH SIZED 5708 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

WE HAD:

/ SMALL COMEX OI GAIN+// A HUMONGOUS SIZED 826 EFP ISSUANCE CONTRACTS (/ VI) A MAMMOTH NUMBER OF T.A.S. CONTRACT ISSUANCE 5708 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A MASSIVE 500 SILVER CONTRACTS!!!!!

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN.. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN.

TOTAL CONTRACTS for 19 DAY(S), total 25,953contracts: OR 129.765 MILLION OZ (1365 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 129.765 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 129.765 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 135 CONTRACTS WITH OUR GAIN IN PRICE OF $5.60 IN SILVER PRICING AT THE COMEX// WEDNESDAY,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED CONTRACT EFP ISSUANCE: 826 CONTRACTS ISSUED FOR MARCH, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 10 MONTHS OF SILVER DELIVERIES:

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (5708) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!!

WE HAD 246 NOTICE(S) FILED TODAY FOR 1.230 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON A MASSIVE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A MEGA MEGA HUGE SIZED 23,340 OI CONTRACTS DOWN TO 465,123 OI AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE STILL A RELATIVELY LOWISH OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE AND CRIMINAL 2954 CONTRACTS // MEGA HUGE GOVERNMENT REMOVALS//

WE HAD A MEGA MEGA SIZED LOSS IN COMEX OI (23M340 ONTRACTS) . THIS OCCURRED DESPITE OUR HUGE GAIN OF $218.00 IN PRICE// WEDNESDAY///.

LAST 9 MONTHS OF GOLD DELIVERIES: (MAY THROUGH TO /DECEMBER 25 AND NOW JAN 26)

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

E.F.P. ISSUANCE/FOR OPENING JANUARY GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3201 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 465,123 AND WE NOW WITNESSING A NOW BIGGER COMEX OI BUT WITH AN EXTREMELY HIGH PRICE OF GOLD.//NOW EASIER TO FLEECE SPECS.

SILVER ALSO HAS A FAIR SIZED COMEX OI OF 156,772 CONTRACTS//

IN ESSENCE WE HAVE A MEGA HUGE SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 20,179 CONTRACTS WITH 23,340 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3201 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 20,179 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED BUT CRIMINAL 2618 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON.

GOLD PRICE ON WEDNESDAY ROSE BY $218.00

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(3201) ACCOMPANYING THE STRONG LOSS IN COMEX OI OF 23,340 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 20,179 CONTRACTS..

WE HAVE 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND NEWBIE SPECULATORS GOING TO THE LONG SIDE AND POURING IT ON WITH RECKLASS ABANDON!! . ,2.) STRONG INITIAL STANDING FOR GOLD FOR JAN AT 13.285 PLUS OUR NEXT QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117 NEW TOTAL QUEUE JUMP OF 30.7117 TONNES//NEW NORMAL DELIVERY ADVANCES TO 36.8958 TONNES FOLLOWED BY OUR 6 EXCHANGE FOR RISK OF 22.315 TONNNES//NEW STANDING A HUGE TO 59.2108 TONNES

NEW STANDING ADVANCES TO 59.2108 TONNES.

NEW STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

3) HUGE T.A.S. LIQUIDATION (AND CONSIDERABLE GOVT LIQUIDATION AND HUGE MONTHLY SPREADER LIQUIDATION // AND A HUGE GAIN OF EQUITY SHARES/JAN 27 AS WE HAD 1)A $218.00 COMEX PRICE GAIN AND WE HAD 2) NEWBIE SPEC SHORTS GETTING LIQUIFIED AND ON A NET BASIS, THE SPECS LOST HUGELY IN NUMBERS + EASTERN CENTRAL BANKERS WERE PILING INTO THE LONG SIDE AS WE HAD A MEGA HUGE SIZED LOSS OF 20,128 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A HUGE AMOUNT OF GOLD WILL STAND FOR DELIVERY IN JAN. (59.2108TONNES). //, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL WITH THE HUGE GAIN IN PRICE WEDNESDAY

4)A MEGA HUGE COMEX OI LOSS 5) V) HUGE SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (3201) AND A STRONG T.A.S. ISSUANCE (2618) FOR RAID PURPOSES

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

TOTAL EFP CONTRACTS ISSUED: 57,407 CONTRACTS OR 5,740,700 OZ OR 178.55 TONNES IN 19 TRADING DAY(S) AND THUS AVERAGING: 3021 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN19 TRADING DAY(S) IN TONNES: 178.55 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 178.55 TONNES DIVIDED BY 3550 x 100% TONNES = 5.02% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 178.55 TONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

SPREADING OPERATION

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A SMALL SIZED 135 CONTRACTS OI TO 156,772 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 826 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 826 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 635 CONTRACTS AND ADD TO THE 826 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 961 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $5.60 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.805 MILLION PAPER OZ

OCCURRED DESPITE OUR GAIN IN PRICE.OF $5.60

2.ASIAN AFFAIRS JAN 28/2025

SHANGHAI CLOSED UP 6.75 PTS OR 0.16%

//Hang Seng CLOSED UP 141.19 PTS OR 0.51%

// Nikkei CLOSED UP 65.79 PTS OR 0.12%

//Australia’s all ordinaries CLOSED DOWN 0.36%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9468

/ OFFSHORE CLOSED DOWN AT 6.9451 Oil UP TO 64.61 dollars per barrel for WTI and BRENT UP TO 69.51 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9451 OFFSHORE YUAN TRADING DOWN TO 6.9445 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A HUMONGOUS SIZED 23,390 CONTRACTS TO 465,123 OI DESPITE OUR HUGE GAIN IN PRICE OF $218.00 WITH RESPECT TO WEDNESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3201).

WE HAD HUGE T.A.S. LIQUIDATION WEDNESDAY ALONG WITH THE COMMENCEMENT OF MONTHLY SPREADERS. IT SEEMS THAT THE SPECULATORS WENT MASSIVELY HUGE TO THE LONG SIDE WITH OUR FRBNY PROVIDING STILL THE MASSIVE NECESSARY PAPER AND OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE .

YOU WILL NOTICE THAT THE COMEX OI IS NOW GAINING HUGELY FROM ITS LOW OI OF AROUND 418,000 TO NOW 465,123 AND NOW AMPLE ENOUGH FOR AN ATTEMPTED RAID BY OUR BANKERS. FROM CHINA WE LEARN THAT THE GOLD LEASE RATE IS NOW AROUND 3 TO 4 %

WE THUS HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 20,179 CONTRACTS (OR 53.48TONNES).

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS AND THEN WE HAVE 6 ISSUED IN JANUARY: 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, jAN 27: 3.160 AND FINALLY YESTERDAY’S 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELVERIES.

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 39+ TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WILL BE ADDED TO OUR DAILY TOTALS!! (17.656 TONNES)

DETAILS ON OUR NEW JANUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A MEGA HUMONGOUS SIZED LOSS ON OUR TWO EXCHANGES OF 17,195 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH JANUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 2618 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER AND JANUARY AND THE 6 ISSUANCES OF EXCHANGE FOR RISK!!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117 TONNES //NEW TOTAL QUEUE JUMPS XXXX //NORMAL DELIVERY OF GOLD ADVANCES TO 36.8988 TONNES TO WHICH WE ADD OUR 6 EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

THE FED IS THE OTHER MAJOR SHORT OF AROUND 39+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 39 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. SO IT IS POSSIBLE/PROBABLE THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!! AND THEN ANOTHER 22.315 TONNES TOTAL IN JANUARY/6 ISSUANCES:

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOW GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 39+ TONNES REMAIN ON THE BOOKS OF THE BIS AND THE END OF THE YEAR IS APPROACHING.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/JAN//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 3201 CONTRACTS.

THAT IS A FAIR SIZED 3201 EFP CONTRACT WAS ISSUED: : /APRIL 3201 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3201 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 39+ TONNES

WE HAD :

HUGE LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + AND DID HAVE HUGE GOVERNMENT LIQUIDATION

HUGE MONTH END SPREADERS LIQUIDATION!! AS IT COMMENCED OPERATIONS YESTERDAY!!

T.A.S.SPREADER ISSUANCE//JANUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A STRONG SIZED 2618 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP WEDNESDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING HUGE SIZED LOSS OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OTHER DAY LAST WEEK

GOLD STANDING AT THE COMEX FOR GOLD LAST 12 MONTHS OF 2025

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117 TONNES //NEW TOTAL QUEUE JUMPS OF 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8988 TONNES TO WHICH WE ADD OUR 6 EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING JANUARY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $2.55)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX// WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL MONDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR JANUARY IN AN OFF MONTH. THE COMEX IS ONE BIG MESS!!

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. NOW JANUARY:

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE: 30.7117 TONNES //NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR 6 EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2104TONNES.

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $218.00

WE HAD A HUGE XXXX CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES : 17,195 CONTRACTS OR 1,719,500 OZ OR 53.48 TONNES

Total monthly oz gold served (contracts) so far this month

11,851 notices 1,185100 oz 36.861 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

customer withdrawals:

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 3

DEALER TO CUSTOMER:

a) Brinks 38,408.877 oz

b) JPMorgan: 10,034.715 oz

CUSTOMER TO DEALER

C) Delaware 697.500 oz

chaos inside the comex

AMOUNT OF GOLD STANDING FOR DECEMBER

THE FRONT MONTH OF JANUARY STANDS AT 11 CONTRACTS FOR A LOSS OF 25 CONTRACTS.

WE HAD 25 NOTICES FILED ON WEDNESDAY, SO WE LOST 0 CONTRACTS OR 0 OZ QUEUE JUMP

FEB LOST A HUGE 33,872 CONTRACTS DOWN TO 38,672 CONTRACTS AS FEB BECOMES THE FRONT MONTH, WE ARE STILL GOING TO HAVE A WHOPPER OF A DELIVERY MONTH!!! BUT LESS STANDING TO WHAT I EXPECTED. WE HAVE ONLY 1 MORE READING DAY BEFORE FIRST DAY NOTICE. YESTERDAY CONCLUDES OPTIONS EXPIRY AT THE COMEX AND FRIDAY OTC/LBMA OPTIONS

MARCH GAINED 408 CONTRACTS UP TO 4246

We had 0 contracts filed for today representing 0 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and0 notices issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JAN /2026. contract month, we take the total number of notices filed so far for the month (11,851) to which we add the difference between the open interest for the front month of JAN ( 11 CONTRACTS) minus the number of notices served upon today (0 x 100 oz per contract) equals 1,186,200 OZ OR (36.8988Tonnes of gold) to which we add our 6 exchange for risk in January of 22.315 tonnes//new standing advances to 59.2108 Tonnes

thus the INITIAL standings for gold for the JAN contract month: No of notices filed so far (11,851 x 100 oz +we add the difference for front month of JAN (11 OI} minus the number of notices served upon today (0 x 100 oz) which equals 1,186,200 OR 36.8988 TONNES plus our 6 exchange for risk of 22.315 tonnes//new standing advances to 59.2108 tonnes

new total of gold standing in JANUARY is 59.2108 tonnes

TOTAL COMEX GOLD STANDING FOR JANUARY 59.2108 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume WEDNESDAY confirmed 566m429 mega mega mammoth/

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,578,834.981 oz 49.10 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 35,877,200.324 oz

TOTAL REGISTERED GOLD 18,785,246.160 or 584,300 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,091.954.164 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON 17,206,412 oz ((REG GOLD- PLEDGED GOLD)=

535.191 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

THE JANUARY. 2025 SILVER CONTRACTS

JAN 29 2026

INITIAL/

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

5 entries

i) out of Asahi: 1,137,083.800 oz ii) out of CNT 684,336.789 oz iii) Out of Delaware 3913.840 oz iv) Out of JPMorgan: 1,306,391.400 oz v) Out of Loomis; 299,569.490 oz

total withdrawn 3,431,295.319 oz

the comex is being drained of silver

Deposits to the Dealer Inventory

0 ENTRY

Deposits to the Customer Inventory

0 ENTRIES

No of oz served today (contracts)

79 CONTRACT(S) ( 0.395 million OZ

No of oz to be served (notices)

35 Contracts (0.175 MILLION oz)

Total monthly oz silver served (contracts)

9608 contracts 48.040 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

withdrawals: customer side/eligible

5 entries

i) out of Asahi: 1,137,083.800 oz ii) out of CNT 684,336.789 oz iii) Out of Delaware 3913.840 oz iv) Out of JPMorgan: 1,306,391.400 oz v) Out of Loomis; 299,569.490 oz

total withdrawn 3,431,295.319 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 5

first 4: dealer to customer:

a) Asahi: 98,747.600 oz

b) Brinks 289,781.660 oz

c) CNT 122m493,749 oz

d) JPMorgan 248,319.300 oz

last one: customer to dealer Loomis

e) Loomis: 1044,642.620 oz

net positive to the dealer (registered) 482,000 oz

TOTAL REGISTERED SILVER: 108.157MILLION OZ//.TOTAL REG + ELIGIBLE. 408,253 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF JANUARY /2026 OI: 281 OPEN INTEREST CONTRACTS FOR A GAIN OF 158 CONTRACTS. WE HAD 79 NOTICES FILED ON WEDNESDAY SO WE GAINED 237 CONTRACTS OR A STRONG QUEUE JUMP OF 1.185 MILLION OZ QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND.

FEB GAINED 262 CONTRACTS UP TO 2572 CONTRACTS AS FEB BECOMES THE FRONT MONTH, WE ARE GOING TO HAVE A STRONG DELIVERY MONTH FOR FEBRUARY, (PROBABLY AROUND 13 MILLION OZ)

MARCH LOST 256 CONTRACTS DOWN TO 99,920

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 246 or 1.230 MILLION oz

CONFIRMED volume; ON WEDNESDAY 205,675 mammoth//

AND NOW JANUARY. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 9854 X5,000 oz = 49.270 MILLION oz

to which we add the difference between the open interest for the front month of JANUARY (281) AND the number of notices served upon today (246)x (5000 oz)

Thus the standings for silver for the JANUARY 2026 contract month: (9854)Notices served so far) x 5000 oz + OI for the front month of JAN(281) minus number of notices served upon today (246 )x 5000 oz equals silver standing for the JANUARY.contract month equating to 49.445 MILLION OZ TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR 20 CONTRACTS OR 0.100 MILLION OZ//NEW TOTAL STANDING FOR DELIVERY: 49.545 MILLION OZ.

NEW STANDING: 49.545 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF JANUARY.

New total standing: 49.545 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 108.253 million oz of registered silver

JPMorgan as a percentage of total silver: 171.559/408.253.million: 41.91%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 19/WITH GOLD UP $22.20 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 18/WITH GOLD DOWN $9.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .85 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1052.54 TONNES

DEC 17/WITH GOLD UP $39.45 TODAY/NO CHANGES IN GOLD AT THE GLD:// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 16/WITH GOLD DOWN $3.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1051.69 TONNES

DEC 15/WITH GOLD UP $10.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 105.12 TONNES

DEC 12/WITH GOLD UP $14.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.83 TONNES

DEC 11/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 10/WITH GOLD UP $85.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.82 TONNES

DEC 9/WITH GOLD UP $18.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.14 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1049.11 TONNES

DEC 8/WITH GOLD DOWN $23.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.33 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1050.25 TONNES

DEC 5/WITH GOLD UP $9.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 4.00 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1050.58 TONNES

DEC 4/WITH GOLD UP $9.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1046.58 TONNES

GLD INVENTORY: 1089.96 TONNES, TONIGHTS TOTAL

SILVER

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 17/WITH SILVER UP $2.93/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 16/WITH SILVER DOWN $.07/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.36 MILLION OZ FROM THE SLV. ./ :INVENTORY RESTS AT 56.360 MILLION OZ //

DEC 15/WITH SILVER UP $1.62/SMALL CHANGES IN SILVER AT THE SLV: A SMALL DEPOSIT OF 635,000 INTO THE SLV. ./ :INVENTORY RESTS AT 517.720 MILLION OZ //

DEC 12/WITH SILVER DOWN $2.30/NO CHANGES IN SILVER AT THE SLV: ./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 11/WITH SILVER UP $3.52/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.537 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.085 MILLION OZ //

DEC 9/WITH SILVER UP $2.41/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 1.179 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 510.828 MILLION OZ //

DEC 8/WITH SILVER DOWN $0.48/HUGE CHANGES IN SILVER AT THE SLV: A HUGE WITHDRAWAL OF 5.497 MILLION OZ OUT THE SLV./ :INVENTORY RESTS AT 512.007 MILLION OZ //

DEC 5/WITH SILVER UP 0.39/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 3.083 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 517.448 MILLION OZ //

DEC 4/WITH SILVER DOWN $1.12/HUGE CHANGES IN SILVER AT THE SLV: A HUGE DEPOSIT OF 4383 MILLION OZ INTO THE SLV./ :INVENTORY RESTS AT 514.365 MILLION OZ //

Gold confirms our thesis, that the purchasing power of the dollar faces a collapse. More conventionally, this will be reported as soaring price inflation and almost no one expects it.

Do not be surprised to see consumer price inflation rise strongly later this year. And we are not talking just 5 or 10 percent. It will be far higher, driven by the US Government’s attempts to avoid a financial crisis from rising bond yields, shore up the stock market, and rescue the financial system.

It will reflect a collapse in the dollar, which is set to accelerate rapidly as it approaches the end of its life as a fiat currency.

We have had a fiat dollar for so long now, that very few people understand that it is only credit whose value depends partly on changes in its quantity, but most importantly the faith its holders and users have in it. But in both common law and accounting, a paper currency’s value depends entirely on the holder’s faith in the issuer’s obligation to discharge its debt in gold.

The US Treasury reneged on this obligation in 1933 when US citizens were ordered by President Roosevelt to hand in their gold for currency. America’s long default started from that action. Within months the following year he then devalued the dollar by 40% against the gold which citizens were still not allowed to possess. And in 1944, the Bretton Woods Agreement further limited the right to encash dollars for gold to sovereign nations. US citizens were still denied their right to exchange dollars for real money. Even that was abandoned in August 1971 and for over 54 years no one, not even foreign governments, has had the right to cash in dollars for gold.

In effect, a currency which is meant to represent an obligation to pay in gold is effectively worthless. It is a national default. The only reason dollars retain any value is that they circulate as a medium of exchange which US citizens must acquire in order to pay their taxes. It persists in this state so long as you can find suckers to take them in exchange for something of value.

Meanwhile, the price of gold measured in these defaulted dollars has risen to over $5,500. That represents a loss of value since the original 1933 default of 99.6%. As the introductory chart shows, since the year 2000, the dollar’s value has declined by 95% to date at a rate which is now accelerating.

While we can dream up reasons for this, it remains a fact which we have to accept. The onus is on the US Treasury and the Fed as issuer of dollars to take steps to prevent their value deteriorating even more. Fat chance of that. The dollar is even sliding against other fiat currencies which refer their own value back to the dollar:

Chartists will confirm that the dollar’s trade weighted index looks terrible.

Declining value means rising prices

So far, no one seems to be taking this seriously. But when a currency loses purchasing power, which is what’s happening, it is reflected in higher wholesale and consumer prices. The apparent rise in the gold price is actually a decline in the currency, which tells us that when people wake up to the consequences it will be because prices start rising strongly.

We can only guess how consumer price inflation will evolve under these conditions, but it will certainly surprise on the upside. By the end of this year, do not be surprised to see consumer prices rise by well over 20%. Even 50% or more cannot be ruled out.

For readers who might think statements of this sort are outlandish, ponder on the chart below, which compares gold priced in 1920s reichsmarks with modern-day dollars:

The time scales are different and so are the y-axes. But the message is clear: dollars are on a value path similar to the reichsmark’s. It is rapidly approaching its demise as a fiat currency, just as every fiat currency has done in the long history of money.

This raises the question as to what happens to bond yields. They should rise to reflect the accelerating decline in the dollar’s purchasing power. But when that happens, the authorities are bound to suppress interest rates and bond yields in an attempt to stop banks, over-indebted business, and indebted consumers going bust. Equities will crash as well.

These attempts to avoid reality will simply crush whatever value is left in factually worthless dollars even more rapidly. That is what the death of fiat currencies is all about, and that is what gold priced in defaulted dollars is now telling us.

3.CHRIS POWELL AND HIS GATA DISPATCHES

nd

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 256

PETER KRAUTH

LIVE FROM THE VAULT YOU TUBE: 256

Episode 256

Posted 23rd January 2026

Could Silver Climb Even Higher? Feat. Peter Krauth

In this week’s Live from the Vault, Andrew Maguire welcomes back Peter Krauth to explain why silver surges past key caps, climbing relentlessly since February 2024 as long-term supply-demand fundamentals suggest a possible upward trend.

5. COMMODITY REPORT//:silver

Inbox

Robert Lambourne

2:57 PM (2 minutes ago)

to me, Chris

I got this from Chinese AI just now.

New trading controls announced today

• CME Group (effective 28 Jan, after the close): ◦ Initial margin hiked another 15 % → $18 975 per full-size contract (second increase in a week). ◦ Spec position limit cut to 3 000 lots (from 5 000) in the front two months; hedgers must file daily inventory affidavits above 1 500 lots.

• SHFE (after intra-day limit-up breach): ◦ Daily price band widened to ±18 % but exchange signalled it will halt new long opening orders if limit-up is hit before 14:30 Shanghai time.

END

EARLY TUESDAY MORNING

Robert Lambourne

Mon, Jan 26, 2:57 PM (11 hours ago)

I got this from Chinese AI just now. New trading controls announced today • CME Group (effective 28 Jan, after the close): ◦ Initial margin hiked another 15 % →

Chris Powell

Mon, Jan 26, 7:18 PM (7 hours ago)

Thanks, Bob. Sounds like they see the risk of things getting out of control. cp

Robert Lambourne

2:41 AM (13 minutes ago)

to Chris, me

Chris,

In the same note, it was reported that solar panel production in China had been stopped for two weeks in at least one manufacturing facility because of no silver. If correct, and normally it’s accurate, that reinforces the likelihood of limited silver exports from China.

Hence I think you’re right that officials in China and in the West must be really concerned.

Bob

END

LONGI Ditches Silver for Base Metals as Solar Industry Faces Price Crunch

Inbox

Robert Lambourne

7:30 AM (3 hours ago)

to me, Chris

Chris and Harvey,

This article provides an explanation of the silver price increase impact on the economics of solar panel production. It also covers some of the process changes being made to reduce silver consumption including copper being used as a substitute.

One major producer in China, LONGI, is seeking to replace silver with a mainly copper based alloy of base metals in Q2 of 2026.

The note quotes the cost impact at a silver price of $84 per Troy ounce which it claims has risen to 17% of the per watt cost of the solar panel from 3% in 2023. It’s reported that in Q4 of 2025 alone the silver cost increased to 17% from 12%.

Current silver prices of over $100 will have reinforced this push to reduce silver usage.

The article explains that such substitution of silver might not be repeatable in alternative technologies such as TOPCon used by many of LONGI’s competitors. But the need to contain product costs is clear given the scale of silver’s recent price increases.

5B. COMMODITY REPORT//GOLD OR /SILVER LEASE RATES:/GOLD

GOLD LEASE RATES CLIMB TO AROUND 3.0 TO 4.0%

Robert Lambourne

7:56 AM (4 minutes ago)

to me

Harvey,

Interesting comment for you on gold from Chinese AI. Gold lease rates are ticking up in all markets, c3%/4% and inventories draining. Reportedly demand in Asia is strong, including Japan as confidence in bonds there is probably fraying. Possibly gold is slightly under the radar here because of silver.

I’ve no idea how Trump will handle his latest tariff threats re Greenland, but the situation seems quite unstable. Gold might well move strongly here.

No December 2025 BIS gold swap data yet. I’ve emailed Chris to suggest it might only appear right at the month end. This is no great surprise, but we can guess plausibly that the BIS will be under some pressure to end the gold swaps. Whatever you think about Jerome Powell, his influence is already reduced and this will also apply to any successor when they attend the BIS meetings.

Regards,

Bob

end

ROBERT LAMBOURNE//TODAY

Summary of new restrictions on precious metals futures trading announced this week

Inbox

Robert Lambourne

10:35 AM (1 hour ago)

to me, Chris

Harvey and Chris,

I got this today from DeepSeek initially and then checked by Kimi – both Chinese AI. I was a bit surprised that CME had not changed their gold margin, but had changed both silver and platinum.

The language used to describe the CME silver and platinum increase is Orwellian and consequently really amusing – a routine volatility review. Even the AI picked it up.

Bob

AI sourced:

Below is a same-day (28 Jan 2026) summary of new margin hikes, position limits or other trading restrictions that have actually been announced this week for the key precious-metals futures on the world’s principal exchanges.