ACCESS MARKET

GOLD $4946.00 3:30 PM)

SILVER: 87.50 3;30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,903.700000000 USD

INTENT DATE: 02/03/2026 DELIVERY DATE: 02/05/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 9

099 H DEUTSCHE BANK AG 4

118 C MACQUARIE FUTURES US 20

190 H BMO CAPITAL MARKETS 197

323 C HSBC 2

363 C WELLS FARGO SECURITI 82

363 H WELLS FARGO SECURITI 60

555 H BNP PARIBAS SEC CORP 69

657 C MORGAN STANLEY 32

661 C JP MORGAN SECURITIES 443

690 C ABN AMRO CLR USA LLC 14

709 C BARCLAYS 127 14

730 C PTG DIVISION OF SGAS 870

880 H CITIGROUP 358

905 C ADM 5

TOTAL: 1,153 1,153

MONTH TO DATE: 29,312

JPMORGAN STOPPED 443/1153

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 1153 CONTRACTs NOTICES FOR 115,300 OZ or 3.5863 TONNES

total notices so far: 29,312 contracts for 2,951,200 OR 91.172 tonnes)

SILVER NOTICES: 190 NOTICE(S) FILED FOR 0.950 MILLION OZ OZ/

total number of notices filed so far this month : 2955 CONTRACTS (NOTICES) for 14.775 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S 2.680 MILLION OZ QUEUE JUMP//NEW STANDING FOR SILVER AT THE COMEXADVANCES TO 19.080 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 16.570 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 2.680 MILLION OZ//NEW STANDING ADVANCES TO 19.080 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.7651 TONNES TO OTHER OF 9.805 TONNES/ NEW QUEUE JUMP TOTAL: 10.5701 TONNES//NEW STANDING ADVANCES TO 104.762 TONNES

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 104.162 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 46.342 TONNES (WHICH WILL BE ANOTHER STRONG)

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 812 CONTRACTS OI TO 143,180 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 585 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 585 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 813 CONTRACTS AND ADD TO THE 585 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1397 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $6.11 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 6.985 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $6.11

2.ASIAN AFFAIRS FEB 4/2025

SHANGHAI CLOSED UP 34.46 PTS OR 0.85%

//Hang Seng CLOSED UP 12.55 PTS OR 0.05%

// Nikkei CLOSED DOWN 427.30 PTS OR 0.78%

//Australia’s all ordinaries CLOSED UP 1.67%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9413

/ OFFSHORE CLOSED DOWN AT 6.9401 Oil DOWN TO 6.335 dollars per barrel for WTI and BRENT UP TO 67.43 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9413 OFFSHORE YUAN TRADING DOWN TO 6.9401 ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5,082 CONTRACTS TO 409,694 OI DESPITE OUR HUGE GAIN IN PRICE OF $270.50 WITH RESPECT TO TUESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4980).

WE HAD NO T.A.S. LIQUIDATION TUESDAY. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO LONG WITH OUR FRBNY PROVIDING STILL THE MASSIVE NECESSARY SHORT PAPER. BUT OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE PILING ON AND THEN TENDERING FOR PHYSICAL AT THE END OF THE DAY.

YOU WILL NOTICE THAT THE COMEX OI IS NOW BACK TO A LOWER OI FROM ITS LOW OI OF AROUND 411,000 TO NOW 409,694 AND NOW AMPLE ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE DIFFICULT TO FLEECE. FROM CHINA WE LEARN THAT THE GOLD LEASE RATE IS NOW AROUND 3 %

WE THUS HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 102 CONTRACTS (OR 0.317TONNES).

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS AND THEN WE HAVE 6 ISSUED IN JANUARY: 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, jAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

FEB EXCHANGE FOR RISK: 0 NOTICES SO FAR!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 56+ TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WAS ADDED TO OUR DAILY TOTALS!! (17.656 TONNES)

FEBRUAY ISSUANCE; ZERO SO FAR!!

DETAILS ON OUR NEW FEBRUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A SMALL SIZED LOSS ON OUR TWO EXCHANGES OF 102 CONTRACTS WITH OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH JANUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 2247 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND HUGE NUMBER OF EXCHANGE FOR RISK IN JANUARY WITH ITS 6 ISSUANCES ( IN FEB: 0 ISSUANCES!!)

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0,000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

11.FEB; 0. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.7651 TONNES ADDING TO ALL OTHER QUEUE JUMPS OF 9.805 TONNNES//NEW TOTAL QUEUE JUMP: 10.5701// / STANDING ADVANCES TO 104.162 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 56+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 56 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. BUT IT IS IMPOSSIBLE/ THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!!,(LATEST BIS DATA SHOWS AN INCREASE IN GOLD BORROWING BY THE FRBNY// BUT MAY BE THE BUYER IN JANUARY OF 22.315 TONNES TOTAL IN JANUARY/6 ISSUANCES AS WE NOW HAVE THE BIS DATA FOR GOLD SWAPS FOR DECEMBER 2025 AND HERE WE FIND THAT THE FED ACTUALLY INCREASED THEIR GOLD SWAP LOANS WITH THE BIS TO THE 56 TONNES WHICH I NOW RECORD FOR YOU.!!

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOT GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 56+ TONNES REMAIN ON THE BOOKS OF THE BIS

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/JAN//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 4980 CONTRACTS.

THAT IS A STRONG SIZED 4980 EFP CONTRACT WAS ISSUED: : /APRIL 4980 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4980 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 56+ TONNES

WE HAD :

- HUGE LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + AND DID HAVE HUGE GOVERNMENT LIQUIDATION

- HUGE MONTH END SPREADERS LIQUIDATION ENDED FEB 2 AS IT FINALIZED OPERATIONS !!

T.A.S.SPREADER ISSUANCE//FEBRUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A STRONG SIZED 2247 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP TUESDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING GOOD SIZED LOSS OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OPTIONS EXPIRY MONTH INCLUDING JANUARY’S OTC/LBMA DRIVE BY SHOOTING!

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.7651 WHICH IS ADDED TO ALL OTHER QUEUE JUMPS OF 9.805 TO TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB:: 10.5711 TONNES///STANDING ADVANCES TO 104.162 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING FEBRUARY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $270.50)

WE HAD NO T.A.S. SPREADER LIQUIDATION TUESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL TUESDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR FEBRUARY. THE COMEX IS ONE BIG MESS!!

TUESDAY NIGHT//WEDNESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. NOW JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.7651 TO WHICH WE ADD TO ALL OTHER QUEUR JUMPS OF 9.805 / NEW QUEUE JUMP TOTALS: 10.5701//STANDING ADVANCES TO: 104.162 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $270.50

WE HAD A HUGE 1317 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

INITIAL GOLD COMEX

FEB 4

FEB 2026 CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES customer withdrawals: ONE ENTRY i) Out of JPMorgan: 64,302.000 oz (2000 kilobars) |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entry xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1153 notice(s) 115,300 OZ 3.5863 TONNES TONNES OF GOLD |

| No of oz to be served (notices) | 4176 contracts 417,600 OZ 12.989 TONNES |

| Total monthly oz gold served (contracts) so far this month | 29,312 notices 2,93,1200 oz 91.172 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0

customer withdrawals:

ONE ENTRY

i) Out of JPMorgan: 64,302.000 oz

(2000 kilobars)

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 4

DEALER TO CUSTOMER:

a) Brinks: 42,535.657 oz

b) HSBC 11,388.779 oz

c) Loomis: 4919.103 oz

d) Manfra: 6751.917 oz

total adjusted out of dealer (reg) to eligible (customer) = 65,595.456 oz or 2.040 tonnes

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 5328 CONTRACTS FOR A LOSS OF 393 CONTRACTS.

WE HAD 639 CONTRACTS SERVED ON TUESDAY, SO WE GAINED A STRONG 246 CONTRACT–

QUEUE JUMP FOR 24,600 OZ OR 0.7651 TONNES!!

MARCH SAW A LOSS OF ONLY 147 CONTRACTS DOWN TO 4819 CONTRACT OI AS MARCH BECOMES THE NEW FRONT MONTH FOR GOLD.

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 4467 CONTRACTS DOWN TO 288,782 CONTRACTS

We had 1153 contracts filed for today representing 115,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1153 contract(s) of which 443 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (29,312) to which we add the difference between the open interest for the front month of FEB ( 5328 CONTRACTS) minus the number of notices served upon today (1153 x 100 oz per contract) equals 3,348,800 OZ OR (104.162 Tonnes of gold)

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (29,312 x 100 oz +we add the difference for front month of FEB (5328 OI} minus the number of notices served upon today (1153 x 100 oz) which equals 3,348,800 OR 104.162 TONNES//

new total of gold standing in FEB is 104.162 TONNES//

TOTAL COMEX GOLD STANDING FOR FEB 104.162 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume TUESDAY confirmed 409,694 mega mega mammoth/

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,841,387.935 oz 57.27 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 35,691,231.403 oz

TOTAL REGISTERED GOLD 18,896,756.103 or 587.768 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,794,475.300 OZ//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 17,055,369 oz ((REG GOLD- PLEDGED GOLD)=

530.49 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SILVER/COMEX

FEB 3 2026

INITIAL/

FEB 4 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) out of Asahi: 1,891,937.860 oz ii) out of HSBC 902,102.976 oz iii) out of JPMorgan 282,596.460 oz total withdrawal: 3,066,617.296 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 0 ENTRIES |

| No of oz served today (contracts) | 190 CONTRACT(S) ( 0.95000 million OZ |

| No of oz to be served (notices) | 861 Contracts (4.305 MILLION oz) |

| Total monthly oz silver served (contracts) | 2955 contracts 14.776 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

withdrawals: customer side/eligible

3 entries

i) out of Asahi: 1,891,937.860 oz

ii) out of HSBC 902,102.976 oz

iii) out of JPMorgan 282,596.460 oz

total withdrawal: 3,066,617.296 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 4

first 3: dealer to customer:

a) Asahi 610,906.300 oz

b) Brinks: 632,174.500

c) JPMorgan 318,074.700 oz

and the 4th/customer to dealer Loomis

d) 2,548,721.080 oz

net gain to dealer 987.765 million oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 104.058MILLION OZ//.TOTAL REG + ELIGIBLE. 400,790 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 1051 OPEN INTEREST CONTRACTS FOR A GAIN OF 285 CONTRACTS.

WE HAD 251 NOTICES FILED ON TUESDAY SO WE GAINED A HUGE 536 CONTRACTS OR 2.680 MILLION OZ UNDERWENT A MONSTER QUEUE JUMP WHERE THEY WILL STAND ON THIS SIDE OF THE POND!!

MARCH GAINED 6 CONTRACTS UP TO 86,446. THIS BECOMES THE FRONT MONTH FOR SILVER DELIVERY AND IT LOOKS LIKE WE WILL HAVE A DANDY DELIVERY OF SILVER FOR THIS MONTH.

APRIL LOST 0 CONTRACTS TO AN OI 346 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 251 or 1.255 MILLION oz

CONFIRMED volume; ON TUESDAY 150,234 mammoth//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 2955 X5,000 oz = 14.775 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (1051) AND the number of notices served upon today (190)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (2955)Notices served so far) x 5000 oz + OI for the front month of FEB(1051) minus number of notices served upon today (190 )x 5000 oz equals silver standing for the JANUARY.contract month equating to 19.080 MILLION OZ

NEW STANDING: 19.080 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 19.070 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 104.058 million oz of registered silver

JPMorgan as a percentage of total silver: 168.864/400.790.million: 42.12%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

FEB 4/2026/WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1083.38 TONNES

FEB 3/2026/WITH GOLD UP $270.80 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1087.10 TONNES

FEB 2/2026/WITH GOLD DOWN $100.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.10 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1083.38 TONNES, TONIGHTS TOTAL

SILVER

FEB 4 WITH SILVER UP $2.02 A HUGE WITHDRAWAL OF 3.551 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 528.484 MILLION OZ

FEB 3 WITH SILVER UP $6.11 A MASSIVE MASSIVE PAPER AND FRAUUDULENT 32.898 CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 531.985 MILLION OZ

FEB 2 WITH SILVER DOWN $1.32 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 528.484 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Watch out for Japan’s election on Sunday

Japan is the world’s exporter of capital, which could be disrupted by its election this weekend with consequences for the dollar. But first we look at gold and silver.

| Alasdair MacleodFeb 4∙Paid |

We can see from open interest on Comex that speculator interest in both contracts is now extremely low. When prices collapsed on Friday, it was because there were no buyers. There was a vacuum under prices. The correction was a washout.

That is now behind us, and buyers are returning. Prices will continue to be driven by China’s and India’s demand for physical gold and silver. In the case of silver, while the price in Shanghai did drop, it has maintained a significant premium over paper values in London and New York. Paper gold is still in touch with Shanghai physical and the demand for it seems more general and Western bullion banks have balanced their books.

Silver’s chart is interesting, particularly in the context of a log scale for price. Intraday on Friday and Monday, it found support between $71.55 and $74.60, which is where the 55-day moving average sits at $73.20:

The same is true of gold, which fell to a low of $4408 on Monday, which compares with the 55-day MA at $4466:

The point about log scales is they properly represent incremental price progress. And in both cases, we see the underlying trends more clearly. In the case of the gold/silver ratio, the effect is dramatic:

Intraday, the bounce hit 62, which is the 55-day MA level.

These three charts show that technical support was found where it would be expected, and the question then arises as to whether the bullish trends in both metals require a pull-back to the longer-term average. For guidance, we look at the dollar itself. And it’s trade weighted index is indeed grim:

While it briefly broke below the 97 level before rallying above it, the plunging moving averages tell us that any further recovery looks extremely limited. As George W. Bush might have put it, this sucker is going down.

The outcome of Japan’s snap election this coming Sunday is likely to have an effect on the dollar/yen exchange rate, which is a significant component of the dollar’s TWI. Polymarket, the betting odds site predicts a resounding win for Sanae Takaichi’s LDP, endorsing her reflationary plans aimed primarily at subsidising prices to synthetically reduce consumer price inflation.

Almost certainly, the consequence will be to drive Japanese government bond yields higher and the Bank of Japan’s interest rates as well. This should strengthen the yen and throw doubt on investments in US treasuries by Japan’s pension funds and insurance companies. This could exacerbate a funding crisis in US treasuries as the world’s provider of capital withdraws from the market.

A look at the chart indicates that US bond yields are likely to break higher, probably much higher which would be the case if Japan stops buying:

The detail tells us that if the yield goes above 4.75% it will have broken out on the upside. And at that time, both moving averages will move upwards towards a golden cross. This can be seen in the next chart which is more detailed:

In conclusion, Japan’s election this weekend could prove to be a defining moment for markets, with dollar down, and bond yields up. Gold and silver are rising on physical demand mostly from China and India. Why? The Asians see the dollar destabilising sooner or later. And now it could be sooner. With the dollar down there is only one way for them to go and that’s up!

3. CHRIS POWELL AND HIS GATA DISPATCHES:

LIVE FROM THE VAULT YOU TUBE: 257

5. COMMODITY REPORT/

GOLD , SILVER OR PLATINUM LEASE RATES

AROUND 3% FOR GOLD

AROUND 4% FOR SILVER

AND A HUGE 9% FOR PLATINUM….

ROBERT LAMBOURNE…

| Robert Lambourne | 3:30 AM (2 hours ago) | ||

| to me | |||

Harvey,

I had an update last night from AI on metal lease rates in China. There seems to be contradictory information on silver and gold lease rates because of the price volatility, but c3% in gold and c4% in silver seems like the median. So elevated, but not so high that it’s screaming there’s a problem.

In platinum, however, it seems that c9% is a reliable estimate and warehouse inventories are reported to be low.

Regards,

Bob

2.ASIAN AFFAIRS FEB 4/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 34.46 PTS OR 0.85%

//Hang Seng CLOSED UP 12.55 PTS OR 0.05%

// Nikkei CLOSED DOWN 427.30 PTS OR 0.78%

//Australia’s all ordinaries CLOSED UP 1.67%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9413

/ OFFSHORE CLOSED DOWN AT 6.9401 Oil DOWN TO 6.335 dollars per barrel for WTI and BRENT UP TO 67.43 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9413 OFFSHORE YUAN TRADING DOWN TO 6.9401 ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9413

OFFSHORE YUAN: DOWN TO 6.9401

HANG SENG CLOSED UP 12.55 PTS OR 0.05%

2. Nikkei closed DOWN 427,30 PTS OR 0.78%

WEST TEXAS INTERMEDIATE OIL UP 63.35

BRENT; 67.43

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 97.39 /// EURO FALLS TO 1.1810 DOWN 5 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.250/ DOWN 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.78… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.636 DOWN 1 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8699 Italian 10 Yr bond yield DOWN to 3.475 SPAIN 10 YR BOND YIELD DOWN TO 3.238

3i Greek 10 year bond yield UP TO 3.368

3j Gold at $5023.80 Silver at: 89.36 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 38/100 roubles/dollar; ROUBLE AT 76.61

3m oil (WTI) into the 63 dollar handle for WTI and 67 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.65 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.250% DOWN 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.636 DOWN 1 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7765 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9171 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.281 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.912 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.584 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.51 UP 2 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.5260 UP 1 PTS

30 YR UK BOND YIELD: 5.297 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.446 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.960 UP 1 BASIS PTS.

1a New York Opening report

Futures Rise Despite Software, AMD Rout Ahead Of Google Earnings

Wednesday, Feb 04, 2026 – 08:29 AM

US stock futures are up small with Tech lagging on rotation fears, though major indices are off their overnight lows. The AI narrative has been flipped upside down, with traders focused on perceived losers, most of which are in the Software sector, where “there’s no floor” according to one investment manager. As of 8:00am ET, S&P futures are up 0.2%, well off session lows; Nasdaq futures rise 0.2%, pressured by weakness in AMD which tumbled 8% after projections which disappointed Wall Street; Alphabet is set to report after the close. Pre-market, Mag7 are mixed with AAPL, AMZN, and GOOG higher with Semis under pressure (AMD -7%, AVGO -0.8%, NVDA -0.1%). Both Cyclicals and Defensives are mixed without a clear leader. The USD is bid as bond yields are higher by 1-2bps.Commodities are stronger led by Energy and Metals, with gold blasting off back over $5k, and silver rising above $90. Today’s macro data focus is on ISM Services where an in line / stronger print may create a renewed bid for stocks.

In premarket trading, Mag 7 stocks are mostly higher: Alphabet +1% ahead of earnings due after the market close (Microsoft +0.1%, Amazon +0.3%, Apple +0.3%, Nvidia +0.3%, Meta little changed, Tesla -0.06%)

- AMD (AMD) slides 9% after the chipmaker’s sales forecast underwhelmed investors, a sign that it’s not making the AI inroads that some on Wall Street anticipated.

- Boston Scientific (BSX) falls 9% after the maker of medical devices gave a profit and sales growth forecast for 2026 that fell short of Wall Street’s expectations.

- Chipotle (CMG) falls 5% after the restaurant chain operator’s underwhelming annual comparable sales forecast.

- Eli Lilly & Co. (LLY) rises 7% after providing an upbeat sales forecast for the year as strong demand for its weight loss drug cemented its position at the top of the obesity market.

- Emerson Electric (EMR) rises 4% after the automation technology provider reported 9% growth in underlying orders in its first quarter. Citi said orders and other results show a “largely healthy demand environment.”

- Johnson Controls (JCI) rises 8% after the HVAC company boosted its adjusted earnings per share forecast for the full year to a figure above what analysts expected.

- Lumen Technologies (LUMN) falls 4% after the wireline telecommunications company’s results and outlook prompted a downgrade from Raymond James.

- Lumentum (LITE) rises 10% after the maker of optical and photonic products posted stronger-than-expected second-quarter results and gave a robust forecast.

- Match Group (MTCH) jumps 7% after the dating service provider reported revenue for the fourth quarter that beat the average analyst estimate.

- Silicon Laboratories (SLAB) jumps 53% after agreeing to be acquired by Texas Instruments for $231 per share in cash.

- Sonos (SONO) rises 12% after the speaker company’s first-quarter results beat expectations on key metrics.

- Take-Two Interactive (TTWO) rises 5% after the video game publisher raised its fourth-quarter bookings forecast. Analysts are positive about the company reiterating the launch date of its highly anticipated Grand Theft Auto VI.

- Uber Technologies Inc. (UBER) falls 6% after giving a weak profit outlook and promoted an outspoken driverless-vehicle bull to be its new chief financial officer, signaling further investment in a closely watched area of the ride-hailing company’s business.

Economically sensitive shares were Wednesday’s biggest gainers, with futures for the Russell 2000 index of small caps advancing 0.4%, while tech treaded water after a historic rout for SaaS/Software names. The rotation into cyclical stocks persisted as renewed fears over AI-driven disruption weighed on markets. Tuesday’s selloff was sparked by a new automation tool from Anthropic PBC, with losses spilling into financial services and asset managers. Caution lingered on Wednesday, with a European basket of stocks seen at risk from AI disruption falling another 1.1%.

“I don’t think the market has fully resolved whether this move was based on fear or fundamentals. What’s clear is that we’ve had a confidence break, really, at the category level,” said Stephanie Niven, portfolio manager at Ninety One. “Before convictions can be rebuilt at that really important company level, we are seeing this kind of indiscriminate selling.”

Disruption fears have added a new layer of complexity in distinguishing winners from losers in AI. With valuations stretched and earnings season under way, investors have already punished companies that failed to live up to elevated expectations. The mood among investors about software stocks and other sectors deemed at risk of AI advances is grim, according to JPMorgan Chase & Co. analyst Toby Ogg. Ogg met more than 50 investors across Europe and the US over two weeks and said he found that they had significantly reduced software holdings over the past 12 to 18 months. Even after the latest pullback, “the general appetite to step in remains generally low,” he said in a client note.

No one is interested in buying the dip, according to JPMorgan analyst Toby Ogg, and even good earnings won’t be enough, since AI disruption is a long-term issue. “We are now in an environment where the sector isn’t just guilty until proven innocent but is now being sentenced before trial,” he said.

“There’s clearly indiscriminate selling across the entire software cluster,” said Karen Kharmandarian, senior equity investment manager at Mirova in Paris. “There’s no floor, the downward momentum is too strong. It looks a bit like capitulation, which could offer opportunities selectively once things stabilize”.

The pain isn’t just in equities, with banks unable to sell a software loan deal. In options, the implied volatility of software stocks is blowing out versus the S&P 500 ETF.

Another test looms for the AI trade when Alphabet reports after the close. The stock has been the top performer among the Magnificent Seven megacaps since the beginning of 2025. Peers Microsoft Corp. and Meta Platforms Inc. saw divergent reactions to their results last week, reflecting views over whether heavy AI spending is paying off.

“The biggest risk regarding tonight’s publication is the fact that there is a decoupling between Google’s long-term stature as an AI winner, thanks to its vertically integrated approach, and short terms trends in search and monetization, which might prove more erratic,” said Jacques-Aurélien Marcireau, co-head of equities at Edmond de Rothschild Asset Management.

European stocks reverse an earlier decline as an initial extension of the Anthropic-sparked software selloff eases. Stoxx 600 now up by 0.3% as gains in telecoms and chemicals offset mixed results from the financials sector and a large drop for drugmaker Novo Nordisk, which sank 16% after a disappointing sales outlook. Here are some of the biggest movers on Wednesday:

- Handelsbanken gains as much as 4.4% after posting a top-line beat in its full-year report.

- DNB Bank shares rise as much as 3.5% after the Norwegian bank reported net profit ahead of expectations, driven by beats in net interest income and fees.

- Mediobanca shares rise as much as 7.8% after MF daily reported that the board of the Banca Monte Paschi di Siena is begining to tilt toward a delisting of the taken over bank.

- Wendel shares rise as much as 7% after Germany’s Henkel agreed to buy Stahl Parent from Stahl Group, which is majority-owned by the French investment firm. BASF and Clariant also have stakes.

- AMS Osram shares rise as much as 13% after agreeing to offload its sensor business to Infineon for €570m in cash.

- Novo Nordisk shares plunge as much as 20% in Copenhagen after the drugmaker forecast a steep decline in sales this year that was also wider than analyst expectations.

- Software, IT, data services, ad agencies and exchanges are among the equity sectors leading losses in the European session on Wednesday, as they extend a selloff following persistent investor concerns over potential disruption from AI tools.

- UBS shares dropped as much as 5.5% despite a beat on 4Q earnings as it announced a below-expected $3 billion buyback program for 2026 that could increase during the year and maintained its financial targets for 2028.

- Santander shares drop as much as 5% after the Spanish lender announced the acquisition of Webster Financial in a $12 billion deal.

- Watches of Switzerland tumbles as much as 5.1% after the watch retailer cut the midpoint of its margin goal, countering the improved outlook for sales growth.

- DSV falls as much as 4.5% after the Danish shipping and logistics group guidance for 2026 disappointed, overshadowing decent 4Q figures.

- Novartis shares drop as much as 3.1% after the Swiss drugmaker reported net sales for the fourth quarter that missed expectations, while its 2026 Ebit forecast was also below estimates.

- Atalaya Mining Copper shares fall as much as 8.9% to 937 pence, slipping below the offering price after holder Trafigura Group sold 14 million shares at 945 pence per share.

Earlier in the session, Asian stocks slipped in another session dominated by technology concerns, after a broad selloff in the US on fears of disruption from artificial intelligence. The MSCI Asia Pacific Index fell as much as 0.6%, with software makers among the biggest decliners after Anthropic’s launch of a new automation tool. Hong Kong led losses and Japan’s Nikkei 225 also dropped, while stocks rose in South Korea, Australia and Thailand.

Eli Lilly, Uber and Yum! Brands are among companies expected to report before the market open. Lilly investors will be looking for guidance on how the company sees the obesity market expanding following a deal with the Trump administration to widen access for some patients with Medicare. Rival Novo Nordisk’s guidance fell well short.

In FX, the dollar is stronger and the yen extended losses for a 4th session as traders anticipated a victory for Prime Minister Sanae Takaichi’s Liberal Democratic Party in this weekend’s poll.

In rates,treasuries are slightly cheaper across the curve, with yields around 1bp higher vs Tuesday’s close and lagging European bonds, which are higher after euro-area January inflation data and services PMIs. US session includes ISM services gauge, following Treasury quarterly refunding announcement at 8:30am. US 10-year yield near 4.28% is more than 1bp cheaper on the day while German counterpart is richer by about 2bp; UK 10-year is higher by less than 1bp European bonds rising and outperforming gilts and Treasuries. Euro-zone inflation cooled to the lowest level in more than a year.

In commodities, gold moves back above $5,000/oz and silver up to around $89/oz. Oil prices up, Brent above $67/barrel. Bitcoin hovered near $76,000.

The dollar and Treasuries were little changed.

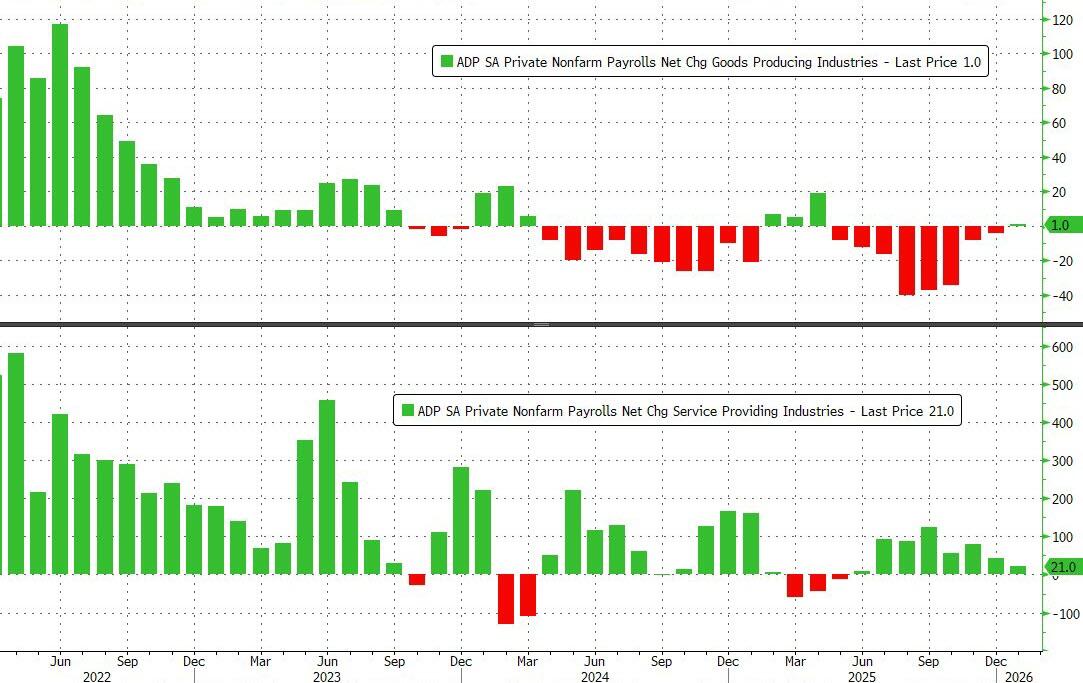

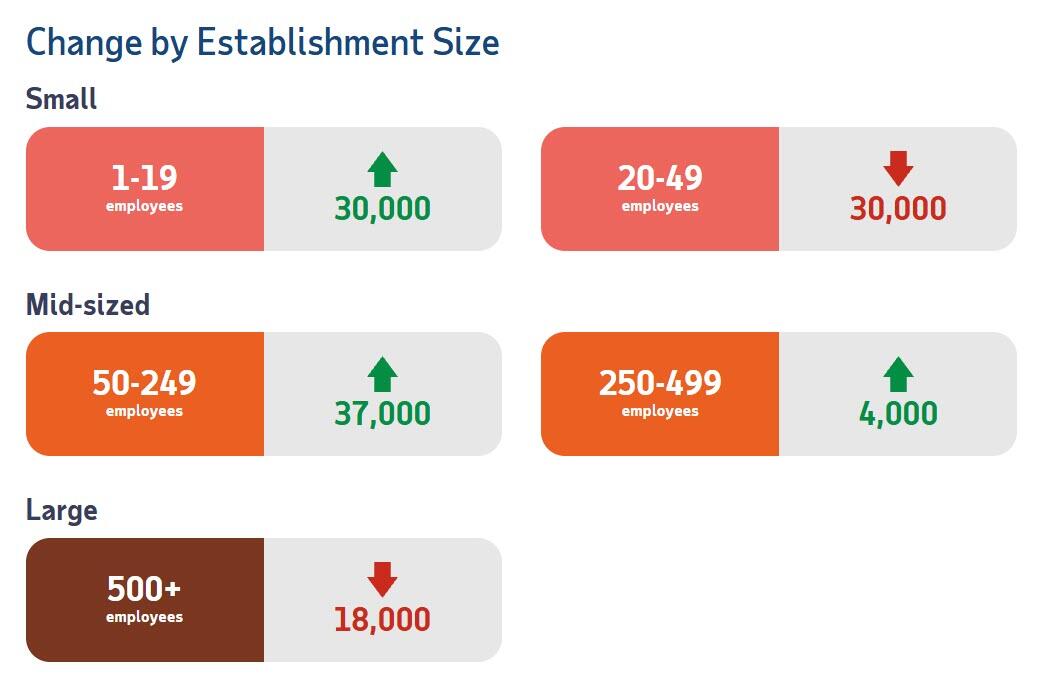

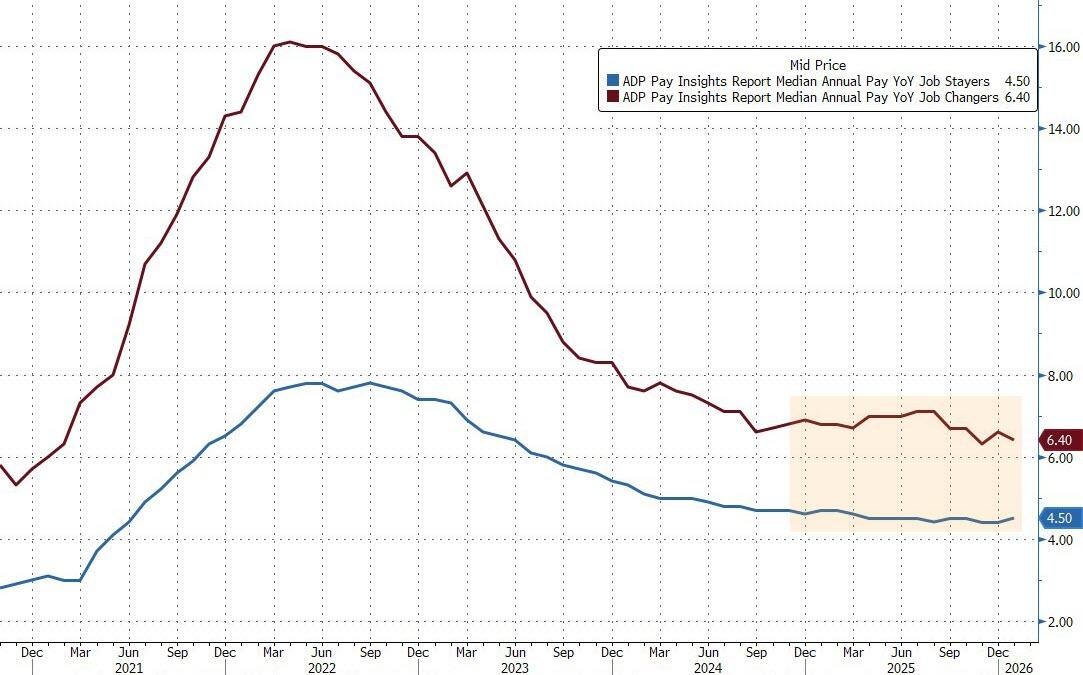

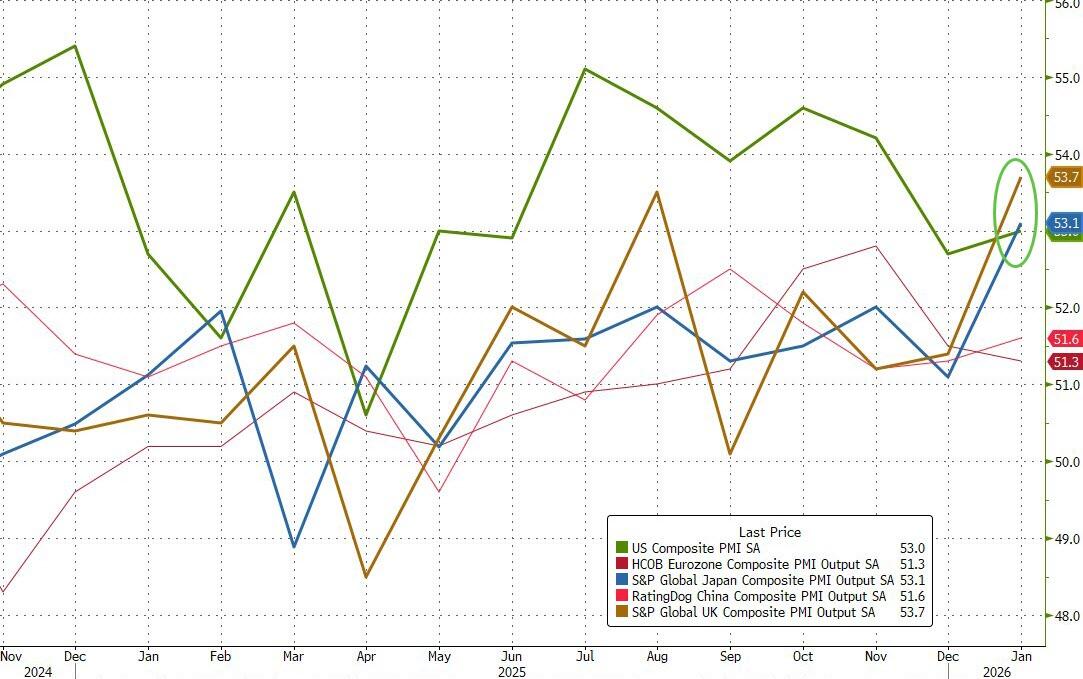

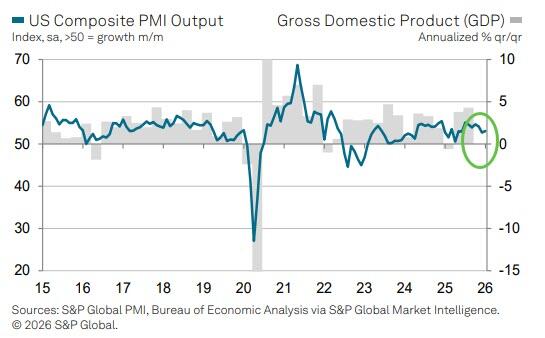

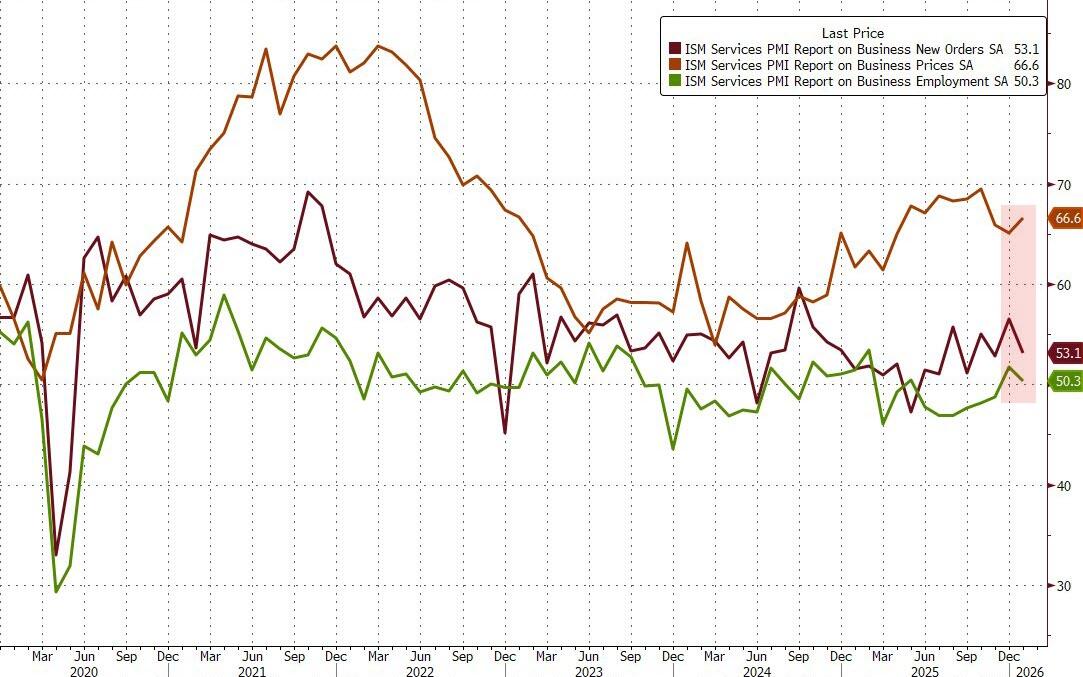

US economic calendar includes January ADP employment change (8:30am), January final S&P Global US services PMI (9:45am) and January ISM services index (10am).Fed speaker slate includes Governor Cook on monetary policy and the economic outlook at the Economic Club of Miami (6:30pm)

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini little changed

- Russell 2000 mini +0.3%

- Stoxx Europe 600 little changed

- DAX -0.1%, CAC 40 +0.7%

- 10-year Treasury yield +1 basis point at 4.28%

- VIX -0.1 points at 17.94

- Bloomberg Dollar Index +0.2% at 1189.69

- euro little changed at $1.1814

- WTI crude +0.7% at $63.66/barrel

Top Overnight News

- Donald Trump reiterated that the US and Iran are maintaining diplomatic talks, even after an American warplane shot down an Iranian drone in the Arabian Sea. BBG

- Trump’s Federal Reserve chair nominee Kevin Warsh faces a battle in the Senate after lawmakers threatened to hold up his confirmation until the DoJ halts its probes into Jay Powell and Lisa Cook. FT

- Nvidia is nearing a deal to invest $20 billion in OpenAI as part of its latest funding round, people familiar said. BBG

- Prime Minister Sanae Takaichi should not count on the Bank of Japan’s help in taming sharp bond yield rises given the huge cost of intervention, including the significant risk of igniting unwelcome yen falls, sources say. RTRS

- Hedge funds are using leverage to reap 28% returns from the safest of bonds. A key ingredient is their use of borrowed cash to juice returns, in some cases amplifying positions up to 15 times their initial investment. BBG

- Investors are ramping up bets on higher long dated Treasury yields and a steeper yield curve as incoming Federal Reserve Chair Kevin Warsh is expected to press for interest rate cuts while shrinking the U.S. central bank’s balance sheet. Warsh’s preference for a materially smaller Fed balance sheet, currently around $6.59 trillion, implies a withdrawal of meaningful government demand for Treasuries, a move which tightens financial conditions because the central bank is not providing liquidity to the market. RTRS

- Euro-area inflation slowed to 1.7% in January, the weakest reading in more than a year and further below the ECB’s 2% target. BBG

- Novo shares plunged after the drugmaker forecast sales decline of up to 13% in 2026, amid price pressure in obesity drugs. But Eli Lilly LLY is now +8% in the pre on Strong 4Q GLP-1 Momentum + Guidance Ahead of Street Quelling Last Minute Fear from NVO Guide. BBG, GS Trading

- NVDA CEO Jensen Huang dismissed fears that artificial intelligence will replace software and related tools, calling the idea “illogical”, after a significant selloff in global software stocks on Tuesday. RTRS

- Department of Labor said all agencies will fully resume to normal operations from the 4th of February 2026.

Trade/Tariffs

- US Senators push for USD 70bln funding deal to support US President Trump’s critical minerals agenda, FT reported.

- Indian Trade Minister said the US trade deal will offer a competitive advantage to Indian exporters and our priority is to energy security for our citizens. Need to bolster capabilities in many sectors including nuclear energy and data centres. India will raise trade with the US.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were ultimately mixed as the region partially shrugged off the downbeat handover from Wall Street, where sentiment was mired by renewed tech-selling, while participants in the region also reflected on the latest Chinese PMI data and the end of the partial US government shutdown. ASX 200 climbed higher with the upside led by outperformance in miners as metal prices continued their recovery, but with gains in the index capped by heavy losses in the tech sector. Nikkei 225 slumped at the open but is off worst levels, while risk appetite was pressured following recent earnings, including disappointing results from Nintendo, which saw its shares suffer a double-digit percentage drop. Hang Seng and Shanghai Comp saw two-way price action as participants digested stronger-than-expected Chinese RatingDog Services PMI data, and after the PBoC drained liquidity, while it was also reported that NVIDIA AI chip sales to China are stalled by a US security review and that Chinese customers are meanwhile not placing H200 chip orders with the company.

Top Asian News

- China’s market regulator unconditionally approves CATL (3750 HK), Chery (9973 HK) and others joint venture formation.

- China’s Vice Finance Minister said China is facing persistent headwinds and policy uncertainty.

- New Zealand ANZ Commodity Price Index MM (Jan) +2.0% (Prev. -2.1%).

European bourses (+0.1%) are broadly firmer across the board, though the DAX 40 (-0.1%) has been pressured by post-earnings losses in Infineon (-2.3%). European sectors hold a positive bias. Telecoms and Chemicals leads whilst Healthcare is the clear laggard, hampered by post-earning losses in Novo Nordisk (-17.6%) and Novartis (-1%). The former reported strong headline metrics, though its 2026 guidance disappointed.

Top European News

- Germany sold EUR 3.197bln vs exp. EUR 4.0bln 2.50% 2032 Bund: b/c 1.51x (prev. 1.2x), average yield 2.60% (prev. 2.33%), retention 20.1 (prev. 23.87%).

- Germany’s VDA announces that 2025 EV production comes out at 1.67mln vehicles, +23% Y/Y.

- Europe’s safest corporate bond spreads drop to its lowest level since 2007.

Central Banks

- Fed Governor Miran resigned on Tuesday from his position as Chair of Council of Economic Advisers, Barron’s reported citing a White House official.

- BoJ won’t come to the rescue of a Takaichi-driven bond rout, with sources stating that Japanese PM Takaichi should not count on the BoJ’s help in taming sharp yield rises given the high cost of intervention including risk of igniting unwanted yen declines.

- PBoC announces plan to build a multi-level financial service system to support domestic demand, tech innovation and SMEs. To continue to support debt risk resolutions for financing platforms, back local government in market oriented reforms and guide financial institutions to provide services based on marker and legal principles.

- Riksbank Minutes: President Thedeen said “at present I assess that monetary policy is following a stable and reasonable course, and we can tolerate minor deviations in data outcomes without immediately needing to adjust the course we have set.

FX