ACCESS MARKET

GOLD $4780.20 3:30 PM)

SILVER: 70.95 3;30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,920.400000000 USD

INTENT DATE: 02/04/2026 DELIVERY DATE: 02/06/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 11

099 H DEUTSCHE BANK AG 641

118 C MACQUARIE FUTURES US 25

190 H BMO CAPITAL MARKETS 689

323 C HSBC 29

363 H WELLS FARGO SECURITI 345

365 C MAREX CAPITAL MARKET 29

435 H SCOTIA CAPITAL (USA) 400

523 C INTERACTIVE BROKERS 1

555 C BNP PARIBAS SEC CORP 8

555 H BNP PARIBAS SEC CORP 96

657 C MORGAN STANLEY 45

661 C JP MORGAN SECURITIES 740

686 C STONEX FINANCIAL INC 1

709 C BARCLAYS 1304 12

880 H CITIGROUP 1000

905 C ADM 8

TOTAL: 2,692 2,692

MONTH TO DATE: 32,004

JPMORGAN STOPPED 740/2642

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 2692 CONTRACTs NOTICES FOR 269,200 OZ or 8.373 TONNES

total notices so far: 32,004 contracts for 3,200,400 OR 99.545 tonnes)

SILVER NOTICES: 608 NOTICE(S) FILED FOR 3,040,000 MILLION OZ /

total number of notices filed so far this month : 3,040,000 CONTRACTS (NOTICES) for 17.815 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S 0.130 MILLION OZ EXCHANGE FOR PHYSICAL TRANSFER//NEW STANDING FOR SILVER AT THE COMEX REDUCES TO 18.945 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ//NEW TOTALS STANDING THUS REDUCES BY A TINY BIT TO 19.070 MILLION OZ//

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 19.870 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL TRANSFER OF 0.1300 MILLION OZ AND THEN ADD BACK 0.125 MILLION EXCHANGE FOR RISK////NEW STANDING REDUCES BY A TINY BIT TO 19.070 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 8.103 TONNES TO OTHER OF 10.5701 TONNES/ NEW QUEUE JUMP TOTAL: 18.6731 TONNES//NEW STANDING ADVANCES TO 112.261 TONNES

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 112.261 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES (WILTONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 59.368 TONNES (WHICH WILL BE ANOTHER STRONG)

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A TINY SIZED 50 CONTRACTS OI TO 143,180 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 660 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 660 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 50 CONTRACTS AND ADD TO THE 660 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 710 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $2.02 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 3.550 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $2.02

2.ASIAN AFFAIRS FEB 5/2025

SHANGHAI CLOSED DOWN 26.29 PTS OR 0.64%

//Hang Seng CLOSED UP 37.92 PTS OR 0.14%

// Nikkei CLOSED DOWN 397.86 PTS OR 0.73%

//Australia’s all ordinaries CLOSED DOWN 0.52%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9414

/ OFFSHORE CLOSED DOWN AT 6.9408 Oil UP TO 64.32 dollars per barrel for WTI and BRENT UP TO 68..48 Stocks in Europe OPENED MOSTLY ALL RED

ONSHORE USA/ YUAN TRADING DOWN TO 6.9414 OFFSHORE YUAN TRADING DOWN TO 6.9408 ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2,051 CONTRACTS TO 407,643 OI DESPITE OUR STRONG GAIN IN PRICE OF $17.20 WITH RESPECT TO WEDNESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4275).

WE HAD NO T.A.S. LIQUIDATION WEDNESDAY. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO LONG WITH OUR FRBNY PROVIDING STILL THE MASSIVE NECESSARY SHORT PAPER. BUT OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE PILING ON AND THEN TENDERING FOR PHYSICAL AT THE END OF THE DAY.

YOU WILL NOTICE THAT THE COMEX OI IS NOW BACK TO A LOWER OI FROM ITS LOW OI OF AROUND 407,000 TO NOW 407,752 AND NOW AMPLE ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE DIFFICULT TO FLEECE. FROM CHINA WE LEARN THAT THE GOLD LEASE RATE IS NOW AROUND 3 %

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 2224 CONTRACTS (OR 6.917TONNES).

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS AND THEN WE HAVE 6 ISSUED IN JANUARY: 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, jAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

FEB EXCHANGE FOR RISK: 0 NOTICES SO FAR!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 56+ TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WAS ADDED TO OUR DAILY TOTALS!! (17.656 TONNES)

FEBRUAY ISSUANCE; ZERO SO FAR!!

DETAILS ON OUR NEW FEBRUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 2224 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH FEBRUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 1479 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS FAILED MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK IN JANUARY WITH ITS 6 ISSUANCES ( IN FEB: 0 ISSUANCES!!)

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0,000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

11.FEB; 0. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 8.103 TONNES ADDING TO ALL OTHER QUEUE JUMPS OF 10.5701 TONNNES//NEW TOTAL QUEUE JUMP: 18.6731// / STANDING ADVANCES TO 112.261 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 56+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 56 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. BUT IT IS IMPOSSIBLE/ THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!!,(LATEST BIS DATA SHOWS AN INCREASE IN GOLD BORROWING BY THE FRBNY// BUT MAY BE THE BUYER IN JANUARY OF 22.315 TONNES TOTAL IN JANUARY/6 ISSUANCES AS WE NOW HAVE THE BIS DATA FOR GOLD SWAPS FOR DECEMBER 2025 AND HERE WE FIND THAT THE FED ACTUALLY INCREASED THEIR GOLD SWAP LOANS WITH THE BIS TO THE 56 TONNES WHICH I NOW RECORD FOR YOU.!!

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOT GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 56+ TONNES REMAIN ON THE BOOKS OF THE BIS

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/JAN//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 4275 CONTRACTS.

THAT IS A STRONG SIZED 4275 EFP CONTRACT WAS ISSUED: : /APRIL 4275 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4275 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 56+ TONNES

WE HAD :

- HUGE LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + AND DID HAVE HUGE GOVERNMENT LIQUIDATION

- HUGE MONTH END SPREADERS LIQUIDATION ENDED FEB 2 AS IT FINALIZED OPERATIONS AS THEY AWAIT THEIR TURN AT THE END OF THIS MONTH OF FEBRUARY.

T.A.S.SPREADER ISSUANCE//FEBRUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A FAIR SIZED 1439 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP WEDNESDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING FAIR SIZED LOSS OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OPTIONS EXPIRY MONTH INCLUDING JANUARY’S OTC/LBMA DRIVE BY SHOOTING!

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 8.103 WHICH IS ADDED TO ALL OTHER QUEUE JUMPS OF 10.5711 TO TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB:: 18.6731 TONNES///STANDING ADVANCES TO 112.261 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING FEBRUARY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $17.20)

WE HAD NO T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL WEDNESDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR FEBRUARY. THE COMEX IS ONE BIG MESS!!

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. NOW JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 8.103 TONNES TO WHICH WE ADD TO ALL OTHER QUEUR JUMPS OF 10.5701 / NEW QUEUE JUMP TOTALS: 18.6731//STANDING ADVANCES TO: 112.261 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $17.20

WE HAD A SMALL 109 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

INITIAL GOLD COMEX

FEB 5

FEB 2026 CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES customer withdrawals: 4 ENTRIES i) Out of HSBC 64,302.000 oz (2000 kilobars) ii) Out of JPMorgan: 128,604.000 oz (4000 kilobars) iii) Out of Manfr: 6817.219 oz total withdrawal: 199,723.219 oz or 6.2122 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entry xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 2692 notice(s) 269,200 OZ 8.373 TONNES TONNES OF GOLD |

| No of oz to be served (notices) | 4088 contracts 408,800 OZ 12.715 TONNES |

| Total monthly oz gold served (contracts) so far this month | 32,004 notices 3,2004,000 oz 99.545 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0

customer withdrawals:

4 ENTRIES

i) Out of HSBC 64,302.000 oz

(2000 kilobars)

ii) Out of JPMorgan: 128,604.000 oz

(4000 kilobars)

iii) Out of Manfr: 6817.219 oz

total withdrawal: 199,723.219 oz or 6.2122 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 4

DEALER TO CUSTOMER:

a) Out of Asahi: 1,603.795 oz

b) Out of Brinks: 6,664.276 oz

c) Out of JPMorgan: 22,939.252 oz

d) Out of Loomis 99,938.382 oz

e) Out of Manfra: 6005.616 oz

t

total adjusted out of dealer (reg) to eligible (customer) = 104,151.7163 oz or 3.239 tonnes

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 6780 CONTRACTS FOR A HUGE GAIN OF 1452 CONTRACTS.

WE HAD 1153 CONTRACTS SERVED ON WEDNESDAY, SO WE GAINED A MONSTER 2605 CONTRACT–

QUEUE JUMP FOR 260,500 OZ OR 8.103 TONNES COMING CLOSE TO THE HIGHEST EVER RECORDED QUEUE JUMP WHICH WAS NORTH OF 9 TONNES.

MARCH SAW A GAIN 282 CONTRACTS UP TO 5101 CONTRACT OI AS MARCH BECOMES THE NEW FRONT MONTH FOR GOLD AND EXPECT TO HAVE A STANDING OF AROUND 13 TONNES FO GOLD

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 3956 CONTRACTS DOWN TO 284,826 CONTRACTS

We had 2692 contracts filed for today representing 269,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 2692 contract(s) of which 740 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (32,004) to which we add the difference between the open interest for the front month of FEB ( 6780 CONTRACTS) minus the number of notices served upon today (2692 x 100 oz per contract) equals 3,609,200 OZ OR (112.261 Tonnes of gold)

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (32,004 x 100 oz +we add the difference for front month of FEB (6780 OI} minus the number of notices served upon today (2692 x 100 oz) which equals 3,609,200 OR 112.261 TONNES//

new total of gold standing in FEB is 112.261 TONNES//

TOTAL COMEX GOLD STANDING FOR FEB 112.261 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume WEDNESDAY confirmed 286,515 fair/

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,834,196.914 oz 57.05 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 35,491,308.180 oz

TOTAL REGISTERED GOLD 18,792,604.787 or 584.528 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,658,408 OZ//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 16,958.408 oz ((REG GOLD- PLEDGED GOLD)=

527.474 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SILVER/COMEX

FEB 3 2026

INITIAL/

FEB 4 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) out of Asahi: 1,291,400.200 oz ii) out of CNT 601,621.972. oz iii) Out of Delaware: 1027.023 oz iv) Out of Manfra 907,455.420 oz total withdrawal: 2,801,526.605 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 1 ENTRY i) stonex: 20,098.150 oz total deposit dealer 20,098.150 oz xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | 0 ENTRIES |

| No of oz served today (contracts) | 608 CONTRACT(S) ( 3.040 million OZ |

| No of oz to be served (notices) | 226 Contracts (1.130 MILLION oz) |

| Total monthly oz silver served (contracts) | 3563 contracts 17.818 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 ENTRY

i) stonex: 20,098.150 oz

total deposit dealer 20,098.150 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

withdrawals: customer side/eligible

4 entries

i) out of Asahi: 1,291,400.200 oz

ii) out of CNT 601,621.972. oz

iii) Out of Delaware: 1027.023 oz

iv) Out of Manfra 907,455.420 oz

total withdrawal: 2,801,526.605 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 6

all dealer to customer:

a) Asahi 119,091.800 oz

b) Brinks: 97,813.780 oz

c) CNT 55,353.280 oz

c) JPMorgan 318,074.700 oz

d) Delaware: 128,692.936 oz

e) HSBC 110,629.570

f) Stonex: 35,473.610 oz

net loss from dealer to customer acc’t : 0.547 million oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 103.531MILLION OZ//.TOTAL REG + ELIGIBLE. 398.009 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 834 OPEN INTEREST CONTRACTS FOR A LOSS OF 216 CONTRACTS.

WE HAD 190 NOTICES FILED ON WEDNESDAY SO WE ACTUALLY LOST 26 CONTRACTS OR 0.130 MILLION OZ UNDERWENT AN EXCHANGE FOR PHYSICAL TRANSFER WHERE THEY WILL TAKE DELIVERY OVER IN LONDON.

MARCH LOST 627 CONTRACTS DOWN TO 85,819. THIS BECOMES THE FRONT MONTH FOR SILVER DELIVERY AND IT LOOKS LIKE WE WILL HAVE A DANDY DELIVERY OF SILVER FOR THIS MONTH.

APRIL GAINED 62 CONTRACTS TO AN OI 408 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 608 or 3.040 MILLION oz

CONFIRMED volume; ON WEDNESDAY 139,548 mammoth//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 3563 X5,000 oz = 17.815 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (834) AND the number of notices served upon today (608)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (3563)Notices served so far) x 5000 oz + OI for the front month of FEB(834) minus number of notices served upon today (608 )x 5000 oz equals silver standing for the JANUARY.contract month equating to 18.945 MILLION OZ. THEN WE MUST ADD OUR FIRST EXCHANGE FOR RISK TOTALS OF 25 CONTRACTS FOR .125 MILLION OZ//THUS NEW STANDING REDUCES BY A TINY BIT TO 19.07 MILLION OZ

NEW STANDING: 19.07 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 19.07 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 103.531 million oz of registered silver

JPMorgan as a percentage of total silver: 168.864/398.009.million: 42.42%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

FEB 5/2026/WITH GOLD DOWN $57.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.95 TONNES

FEB 4/2026/WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1083.38 TONNES

FEB 3/2026/WITH GOLD UP $270.80 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1087.10 TONNES

FEB 2/2026/WITH GOLD DOWN $100.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.10 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1081.95 TONNES, TONIGHTS TOTAL

SILVER

FEB 5 WITH SILVER DOWN $7.87 A HUGE WITHDRAWAL OF 2.175 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 526.309 MILLION OZ

FEB 4 WITH SILVER UP $2.02 A HUGE WITHDRAWAL OF 3.551 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 528.484 MILLION OZ

FEB 3 WITH SILVER UP $6.11 A MASSIVE MASSIVE PAPER AND FRAUUDULENT 32.898 CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 531.985 MILLION OZ

FEB 2 WITH SILVER DOWN $1.32 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 526.309 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

3. CHRIS POWELL AND HIS GATA DISPATCHES:

LIVE FROM THE VAULT YOU TUBE: 257

5. COMMODITY REPORT/BITCOIN//MASSIVE CRASH

WILL THERE BE A FINANCIAL FALL OUT WITH THE PLUNGING BITCOIN?

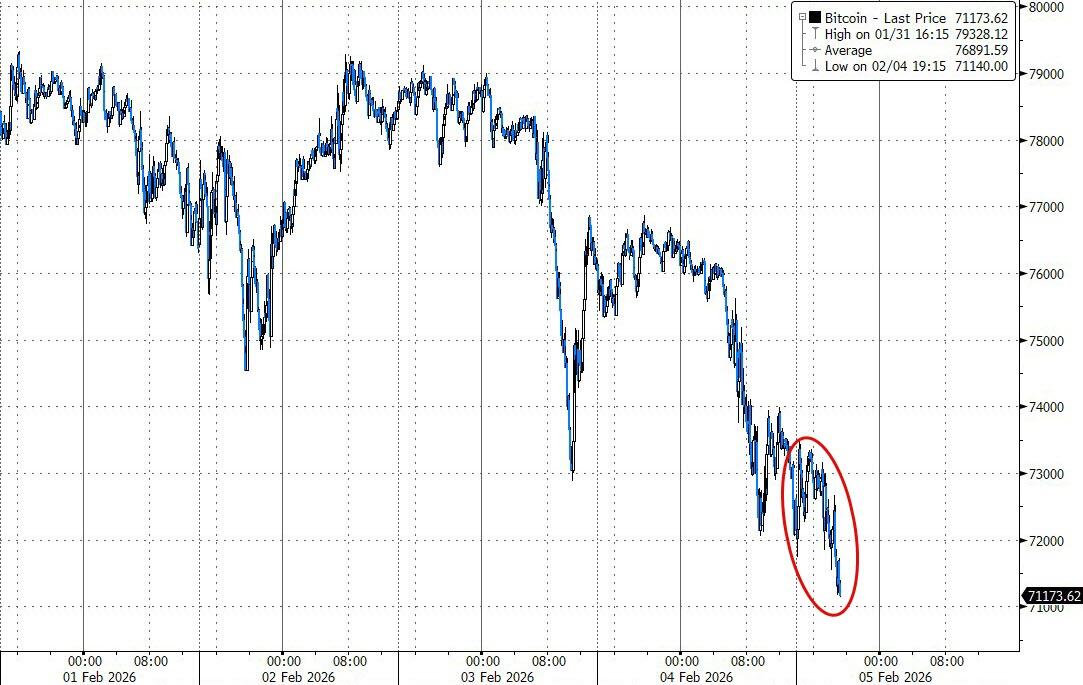

Bitcoin has indeed been plunging sharply throughout early 2026, with its price dropping from a record high of around $126,000 in late 2025 to below $70,000 as of February 5, 2026—a drawdown exceeding 45%.

forex.com This decline has accelerated in recent days, with Bitcoin falling as much as 8.6% on February 4 alone to a low of $66,364 before stabilizing around $67,000, erasing all gains since Donald Trump’s 2024 election win and marking its lowest level since October 2024.

bloomberg.com The broader crypto market has shed over $2 trillion in value since peaking at $4.379 trillion in early October 2025, with nearly $500 billion wiped out in the past week amid cascading liquidations and risk-off sentiment.

reuters.comThis isn’t just a crypto-specific event; it’s already triggering significant financial fallout across multiple sectors, and further effects are likely if the downtrend continues. Here’s a breakdown of the ongoing and potential impacts:1. Massive Liquidations and Trader Losses

- Over $2 billion in leveraged Bitcoin positions (both longs and shorts) have been liquidated since late January 2026, with one single day (January 31) seeing $1 billion in longs wiped out and over $160 billion erased from the total crypto market cap. cnbc.com

- High leverage has created a feedback loop: forced margin calls overwhelm liquidity, amplifying drops and leading to capitulation. Roughly 200,000 trader accounts were liquidated in a recent cascade, with Bitcoin longs alone accounting for $768 million in losses. galaxy.com

- Potential escalation: If prices dip another 10%, expect even larger liquidation events, potentially exceeding $2.5 billion in a single session, as seen in prior flushes.

2. Impact on Corporate Balance Sheets and Stocks

- Companies heavily exposed to Bitcoin, like MicroStrategy (often referred to as “Strategy Inc.” in reports), are facing severe pressure. MicroStrategy’s average cost basis is around $76,037 per Bitcoin, and with prices now well below that, the firm is billions in the red. finance.yahoo.com Michael Burry, known for predicting the 2008 crisis, has warned this could lead to a “death spiral,” where such firms find capital markets closed off, forcing asset sales that further depress prices. finance.yahoo.com

- Bitcoin ETFs are also underwater: As of early February, Bitcoin traded up to 10% below the U.S. ETFs’ average cost basis of $84,000, putting institutional holders at risk of redemptions and outflows. galaxy.com

- Broader stock market ties: The plunge coincides with a tech stock selloff, including AI-exposed names, suggesting correlated risk resets. If Bitcoin falls further, expect amplified declines in crypto-related stocks (e.g., Coinbase, mining firms) and even tangential tech plays.

3. Mining Industry Strain

- Bitcoin miners are on the brink: Sustained prices below $70,000 could push many toward bankruptcy, as operational costs (energy, hardware) outstrip revenues from block rewards and fees. finance.yahoo.com This has historical precedent—similar drops in prior cycles led to mass shutdowns and network hashrate declines.

- Cascade risk: Bankruptcies could flood the market with second-hand mining equipment and force-held Bitcoin sales, adding downward pressure.

4. Broader Economic and Market Ripples

- Crypto’s $2 trillion wipeout represents a wealth destruction event comparable to major stock crashes, potentially denting consumer spending and investor confidence in high-risk assets. reuters.com With 46% of Bitcoin’s supply now underwater (coins acquired at higher prices), long-term holders may start capitulating if support levels like $65,000 break. galaxy.com

- Macro factors fueling the fire: A strengthening U.S. dollar, trade war fears, geopolitical tensions, and rotating capital into safe havens like gold are exacerbating the selloff. aljazeera.com If these persist, the fallout could spill into traditional finance, pressuring leveraged funds and even contributing to a wider risk-off environment in equities.

- Altcoin contagion: Ethereum (down ~5-9% in recent sessions), Solana, and meme coins have suffered double-digit losses, with the total market cap dropping $110-500 billion in short bursts. barrons.com This could lead to project failures and reduced innovation funding in the space.

| Key Metric | Value (as of Feb 5, 2026) | Change from Peak |

|---|---|---|

| Bitcoin Price | ~$67,000 | -47% from $126,000 |

| Crypto Market Cap Loss | $2 trillion | Since Oct 2025 peak |

| Liquidations (Recent Week) | >$2 billion | Longs dominate |

| Drawdown Percentage | 40-45% | From all-time high |

| Underwater Supply | 46% | Coins held at loss |

In summary, the financial fallout is already underway—trillions lost, billions liquidated, and corporate treasuries strained—with cascading effects likely to intensify if Bitcoin breaches $65,000. This looks like a classic bull market reset driven by over-leverage and macro headwinds, but it could evolve into a deeper “crypto winter” if sentiment doesn’t rebound. Long-term Bitcoin structure remains intact for now, but short-term pain is real and substantiated by market data.

END

SILVER/GOLD, PLATINUM

GOLD , SILVER OR PLATINUM LEASE RATES

AROUND 3% FOR GOLD

AROUND 4% FOR SILVER

AND A HUGE 9% FOR PLATINUM….

ROBERT LAMBOURNE…

| Robert Lambourne | 3:30 AM (2 hours ago) | ||

| to me | |||

Harvey,

I had an update last night from AI on metal lease rates in China. There seems to be contradictory information on silver and gold lease rates because of the price volatility, but c3% in gold and c4% in silver seems like the median. So elevated, but not so high that it’s screaming there’s a problem.

In platinum, however, it seems that c9% is a reliable estimate and warehouse inventories are reported to be low.

Regards,

Bob

END

TODAY AI:

DO YOU KNOW THE TWO FIXES SHANGHAI SILVER? DO YOU KNOW LEASE RATES

Searching the web

41 results

Yes, I’m familiar with the current dynamics in the silver market involving Shanghai (via the Shanghai Gold Exchange or SGE, and related futures on SHFE).The “two fixes” you’re likely referring to are the twice-daily benchmark price auctions (also called fixes or benchmark prices) for silver on the Shanghai Gold Exchange (SGE). These are known as the Shanghai Silver Benchmark Price (ticker: SHAG), which is determined through auctions held twice a day:

- Morning session: Around 10:15 a.m. Beijing time

- Afternoon session: Around 2:15 p.m. Beijing time

These auctions involve physical delivery of 15 kg lots of high-purity silver (min. 99.99%) and are designed to reflect real supply/demand balance for physical metal in China. They produce an AM and PM benchmark price each trading day, quoted in yuan per kg (often converted to USD/oz for global comparison). This is similar to how the old London silver fix worked but tied much more closely to physical transactions.This contrasts sharply with Western markets (e.g., COMEX/LBMA), where prices are more influenced by paper/futures trading. In recent weeks/months (as of early 2026), this has led to massive divergences: Shanghai prices often trade at huge premiums (sometimes 20-40% or more) over COMEX/London spot, reflecting tight physical supply and strong demand in China (e.g., industrial use, investment, solar, etc.), while Western prices can be suppressed by futures paper volume.Recent examples from reports show Shanghai fixing at levels equivalent to $100–$130+/oz (or higher in peaks), while COMEX hovered much lower (e.g., $80s–$90s range in volatile periods), with trading halts or limits on SHFE adding to the chaos.Regarding lease rates:Silver lease rates represent the cost to borrow physical silver (typically quoted as an annualized percentage). These are usually derived from the London market (LBMA), where bullion banks lend metal.In the current environment (early 2026), silver lease rates have been elevated (abnormally high compared to historical norms of 0.3–2%):

- Reports mention implied lease rates around 3%, 7–9%, or even spikes higher (e.g., 8–35% in extreme moments during 2025–2026 rallies/crashes).

- High lease rates signal physical scarcity — lenders demand more to part with actual metal because availability is tight (low inventories, high demand, reluctance to lend amid delivery risks).

- This ties directly into the Shanghai premium: When physical is hard to source, borrowing costs soar, and regional markets like Shanghai (more physical-oriented) price much higher than paper-heavy Western ones.

These high rates (especially if sustained) often indicate potential stress or squeezes in the physical market, as seen in backwardation or delivery pressures.The overall picture is one of a bifurcated silver market: “paper” vs. “physical,” with Shanghai’s fixes highlighting real-world tightness in the East. If you’re tracking this for trading or stacking, the persistent Shanghai premium has been a key signal for many in the precious metals community. Let me know if you want more details on current levels or sources!

SILVER EARLY WEDNESDAY EVENING;

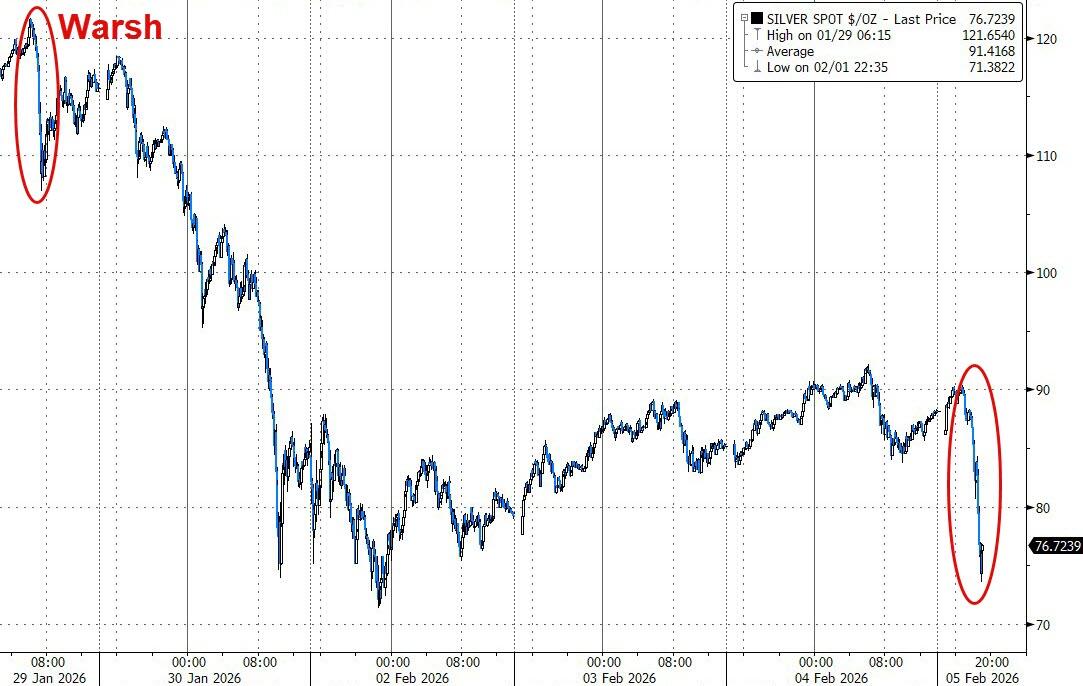

Silver Crashes 20% As China Opens, Gold & Bitcoin Also Plunging

Wednesday, Feb 04, 2026 – 10:25 PM

On the heels of today’s momentum collapse in the US, Silver prices have puked almost 20% in a matter of hours after Asian markets opened…

…erasing the rebound gains of the last three days…

The overall decline from when Trump’s announcement of Warsh’s nomination as the next Fed Chair is now back up to 40%.

“Sentiment seems to have turned soggy across most asset classes, including regional equities and metals,” said Christopher Wong, a strategist at Oversea-Chinese Banking Corp Ltd.

“This underscores fragile sentiment” and has created “a feedback loop amid thin market liquidity,” he said.

Spot Gold prices are also down (around 4-5%), with $5000 seemingly acting as serious resistance…

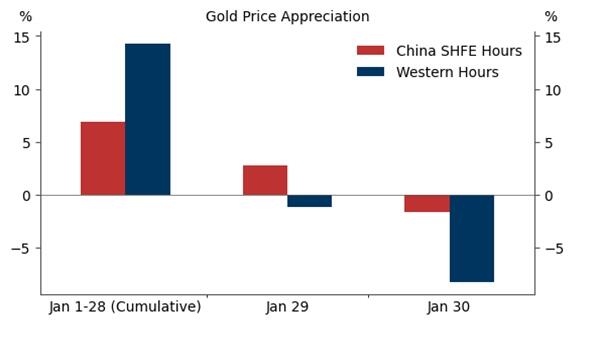

There’s no obvious specific catalysts for the decline in precious metals for now but Goldman Sachs does note that data suggested that Chinese speculators may have played a minor role in the recent volatility (until now).

The timing suggests that Western flows rather than Chinese speculative activity drove late January’s volatility.

Most of the buildup and unwind in gold prices occurred while SHFE–the venue for Chinese speculative futures trading–was closed.

Additionally, China’s strong tradition of physical precious metals ownership and easy access to physical keep it as the dominant form of demand, with the speculative paper market in China — including SHFE futures market and ETF market — being relatively small.

But, given the magnitude and timing of tonight’s collapse, it would appear the speculative Chinese investor has pulled the rug (although gold-backed ETFs are gaining traction in China, their market size remains tiny compared to Western counterparts).

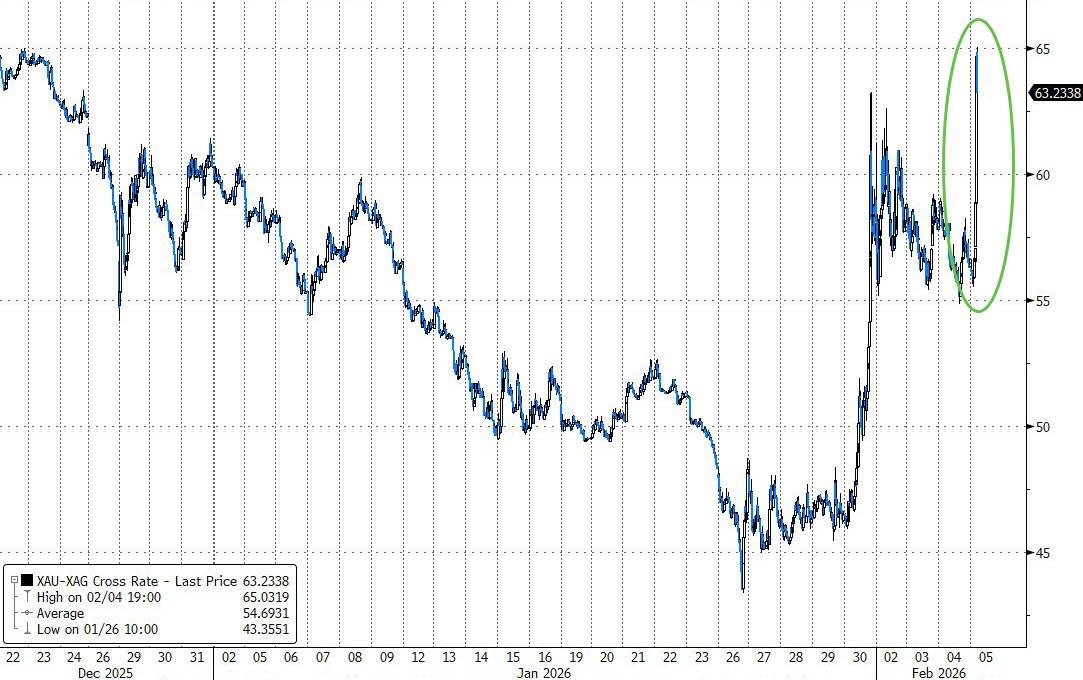

Silver’s relative underperformance has smashed the Gold/Silver ratio back above 65x (6 week highs)…

Bitcoin is also accelerating its losses during the US day session, back below $72,000…

The collapse of these ‘alt’ currencies is coming as the US dollar’s recent gains accelerate…

“Price action is likely to remain volatile until there is greater certainty on the monetary policy outlook,” Standard Chartered Plc analysts including Sudakshina Unnikrishnan said in a note.

Some of this near-term volatility is resulting from investors redeeming their holdings in exchange-traded products, they said, but “structural drivers remain intact and we continue to expect a rebuild to the upside.”

2.ASIAN AFFAIRS FEB 4/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 26.29 PTS OR 0.64%

//Hang Seng CLOSED UP 37.92 PTS OR 0.14%

// Nikkei CLOSED DOWN 397.86 PTS OR 0.73%

//Australia’s all ordinaries CLOSED DOWN 0.52%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9414

/ OFFSHORE CLOSED DOWN AT 6.9408 Oil UP TO 64.32 dollars per barrel for WTI and BRENT UP TO 68..48 Stocks in Europe OPENED MOSTLY ALL RED

ONSHORE USA/ YUAN TRADING DOWN TO 6.9414 OFFSHORE YUAN TRADING DOWN TO 6.9408 ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9414

OFFSHORE YUAN: DOWN TO 6.9408

HANG SENG CLOSED UP 37.92 PTS OR 0.14%

2. Nikkei closed DOWN 397.86 PTS OR 0.73%

WEST TEXAS INTERMEDIATE OIL UP 64.32

BRENT; 68.48

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 97.73 /// EURO FALLS TO 1.1789 DOWN 12 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +2.226/ DOWN 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.25… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.567 DOWN 6 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8769 Italian 10 Yr bond yield UP to 3.504 SPAIN 10 YR BOND YIELD DOWN TO 3.2470

3i Greek 10 year bond yield UP TO 3.488

3j Gold at $4862/00 Silver at: 78.38 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 38/100 roubles/dollar; ROUBLE AT 76.61

3m oil (WTI) into the 64 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.25 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.226% DOWN 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.567 DOWN 6 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7780 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9172 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.272 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.920 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.549 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.54 UP 3 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.5960 UP 6 PTS

30 YR UK BOND YIELD: 5.396 UP 10 BASIS PTS

10 YR CANADA BOND YIELD: 3.445 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.943 DOWN 1 BASIS PTS.

1a New York Opening report

1b European opening report

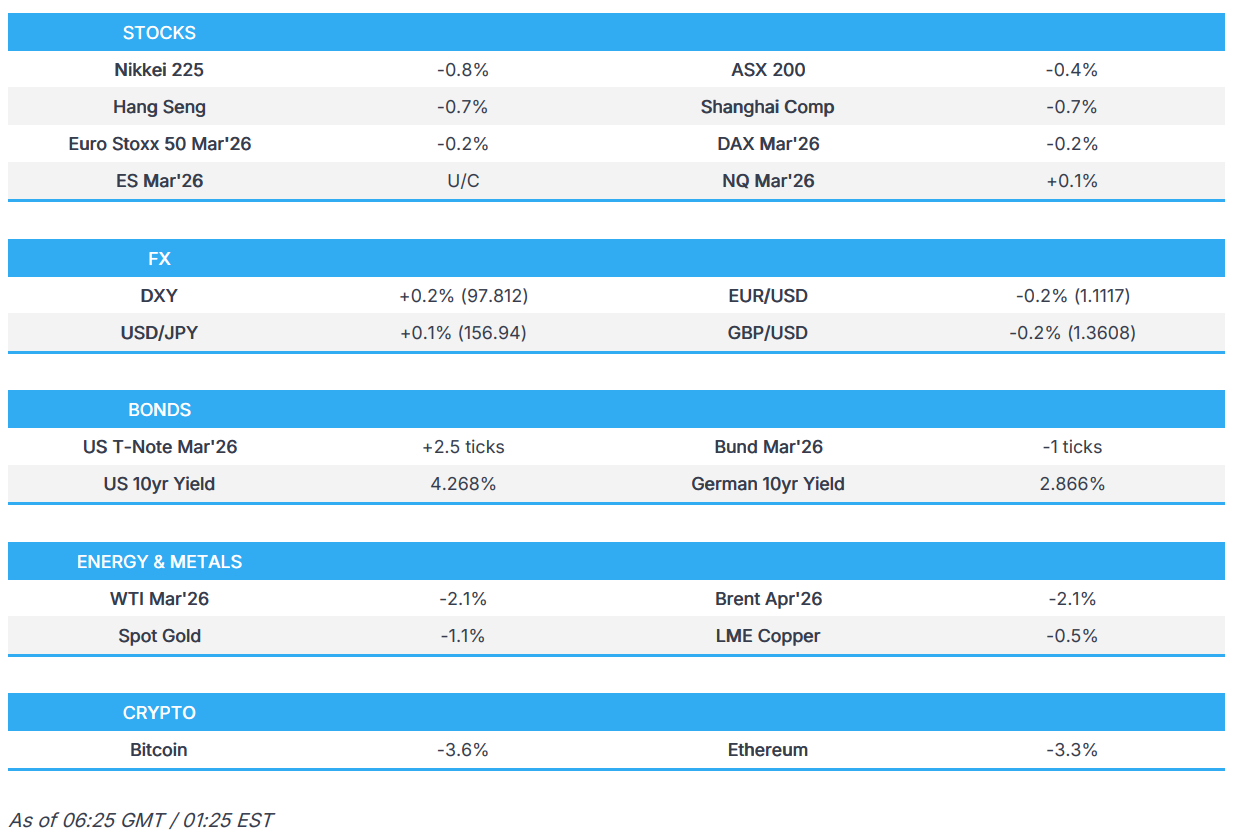

Global equities mixed; markets await ECB and BoE rate announcements – Newsquawk US Market Open

Thursday, Feb 05, 2026 – 06:23 AM

- European bourses are broadly on the backfoot; US equity futures mixed, but the NQ outperforms, as chip names benefit from Alphabet boosting AI spending.

- DXY is mildly firmer, with G10s lower to varying degrees; Aussie hampered by pressure in metals, GBP lags into BoE.

- Fixed income benchmarks are mixed; USTs incrementally firmer, whilst Gilts underperform on political woes.

- Crude benchmarks slip with US-Iran meeting confirmed, Spot gold moves lower, silver -10.5%.

- Looking ahead, highlights include US Challenger (Jan), Weekly/Continuing Jobless Claims, Revelio PLS, ECB Announcement, BoE Announcement & MPR, Banxico Announcement, CNB Announcement. Speakers include BoE’s Bailey, ECB’s Lagarde, Fed’s Bostic, BoC’s Macklem & RBA’s Bullock.

- Earnings from Amazon, Strategy, Roblox, Reddit, Bloom Energy, ConocoPhillips, Bristol Myers Squibb and Barrick Mining.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European equities (STOXX 600 -0.6%) are broadly lower, though the AEX is mildly firmer, boosted by strength in ASML (+1.1%). The chip giant has been boosted after Google noted it would boost AI spending.

- European sectors hold a negative bias. Basic Resources underperforms given the pressure in the metals complex, whilst Shell (-2%, Q4 metrics light) weighs on the Energy sector. Other key movers include Volvo Car (-22%) after poor results and a dire outlook.

- US equity futures (ES U/C, NQ +0.2% RTY +0.2%) are mixed, with very mild outperformance in the tech-heavy NQ. Key names are losing in pre-market trade (Google -2.4%, Arm -6.7%, Qualcomm -10.5%), but focus has been on Google’s decision to double AI spending – a factor which has boosted chip names.

- Alphabet Inc. (GOOGL) Q4 2025 (USD): EPS 2.82 (exp. 2.64), Revenue 113.8bln (exp. 111.29bln) Shares -2.4% pre-market

- ARM (ARM) Q3 2026 (USD): Adj. EPS 0.43 (exp. 0.41), Revenue 1.24bln (exp. 1.23bln) Shares -6.2% pre-market

- QUALCOMM (QCOM) Q1 2026 (USD) Adj. EPS 3.50 (exp. 3.39), Revenue 12.25bln (exp. 12.21bln) Shares -11.1% pre-market

- Maersk (MAERSKB DC) Q4 (USD) EBITDA 1.8bln (exp. 1.84bln), Revenue 13.3bln (exp. 12.9bln).

- Shell (SHEL LN) Q4 (USD): Adj. Profit 3.26bln (exp. 3.51bln), EPS 0.57 (exp. 0.63), Adj. EBITDA 12.79bln (prev. 14.77bln Y/Y), announces USD 3.5bln share buyback programme.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is kept afloat as it continues to claw back losses seen towards the end of January. That being said, the upside is limited following mixed data releases stateside and with plenty of focus on geopolitics amid reports that US-Iran talks scheduled for Friday were off, and on again. DXY has topped resistance seen around the 97.70-97.75 area to reach a current high of 97.83, still some way off the 23rd Jan high at 98.481.

- GBP/USD is among the laggards heading into the BoE, but likely more on political factors at the moment, with UK PM Starmer’s premiership coming under scrutiny for his decision to appoint Peter Mandelson as the US ambassador despite links to Epstein. Back to the BoE, the Bank Rate is expected to be maintained at 3.75%, with some mixed views on the vote split. GBP/USD resides towards the bottom end of a 1.3576-1.3664 range.

- EUR/USD resides in a narrow 1.1783-1.1809 range ahead of the ECB announcement and presser. The ECB is expected to keep its rates on hold, a view held by the likes of Goldman Sachs and Morgan Stanley. Data developments play in favour of keeping rates steady; inflation dipped below the Bank’s target in January, but largely due to base effects. Focus this meeting will be on any commentary surrounding the stronger EUR, trade/geopolitical uncertainty and higher gas prices.

- USD/JPY continues rising amid the firmer USD, with the pair back above 157.00, with yen weakness persisting throughout the week ahead of the snap elections on Sunday. Elsewhere, Antipodeans are softer with AUD the G10 laggard amid headwinds from the subdued risk appetite and selling pressure in commodities.

FIXED INCOME

- USTs are currently firmer by a couple of ticks and trade within a narrow 111-18+ to 111-24 range. Not much driving things for the benchmark this morning, but the focus has been on geopolitics. On Wednesday, it was reported that the US-Iran talks were cancelled, but are now back on and set to happen on Friday. Back to the US, the BLS provided an updated data schedule following the recent partial shutdown. JOLTS is set to be released today; NFP on Feb 11 and CPI on Feb 13. That aside, Jobless Claims is due today, with traders looking to see if the labour market remains in its recent “low hiring – low firing” environment.

- Bunds trade steady and in a narrow 127.88-128.07 range. Really not much driving things for the benchmark this morning aside from EZ Construction PMIs and Retail sales, which had a limited impact on price action. Ahead, the ECB is set to keep its deposit rate at 2.00% and is likely to reiterate that the Bank is in a good place. Focus will be on the recent strength of the EUR and any comments related to potentially undershooting inflation.

- Gilts are underperforming this morning, currently lower by around 40 ticks. Initially gapped lower by around 19 ticks, and then extended lower to make a trough of 90.13. The underperformance in Gilts today can be attributed to the increased pressure that PM Starmer is facing for his decision to appoint Peter Mandelson as the US ambassador, despite knowing about his links to Epstein. As it stands, several MPs are calling for Starmer to resign whilst others are calling for the sacking of Chief of Staff McSweeney; MP Turner said if he does not sack him, then his own back will be “up against the wall… soon” – nonetheless, the did suggest that there is still support for the PM adding that MPs do not want him to go. As it stands, Polymarket odds of Starmer to be out the door by June 30th have risen to 47% (vs 23% yesterday).

- France sold EUR 13.5bln vs exp. EUR 11.5-13.5bln 3.20% 2035, 3.50% 2035, 3.60% 2042 and 3.00% 2049 OAT.

- Spain sold EUR 5.838bln vs exp. EUR 5-6bln 2.35% 2029, 3.00% 2033, 3.20% 2035 Bono and EUR 0.646bln vs exp. EUR 0.25-0.75bln 0.70% 2033 IL.

- Japan sold JPY 525bln 30-yr JGBs; b/c 3.64x (prev. 3.14x), and average yield 3.615% (prev. 3.447%).

COMMODITIES

- Crude benchmarks continued to trade with a lack of clear direction. The pressure seen at the start of the week (following plans of US-Iran talks) was completely reversed in Wednesday’s session over reports that the talks have been cancelled due to Tehran’s demands to change the location and talk format. Late in Wednesday’s session, Iran’s Foreign Minister reconfirmed that talks are back on in Oman for Friday. Prices dropped at the end of the US session. As the European session got underway, benchmarks reversed overnight losses, with Brent returning above USD 68.50/bbl. Today is the expiration day of the New START Treaty. This outcome was expected amid a lack of effort from both sides to renew the agreement.

- Spot gold ended Wednesday’s session below the USD 5,000/oz handle but attempted to regain above the level at the start of the APAC session, but failed to do so. The yellow metal fell to a low of USD 4,790/oz, weighed on by the plunge in silver prices, before slightly paring back losses as European trade gets underway.

- Spot silver wiped out the entirety of the two-day recovery the metal attempted to stage as trade at the Shanghai Metals Exchange got underway. The metal kissed USD 90/oz before slipping to a trough of USD 73.55/oz, with losses seen as much as 16%. Dip-buyers took advantage of the lower prices, with silver prices currently trading around USD 80/oz.

- China gold consumption reportedly fell by 3.6% to 950 tons in 2025 and total gold production rose 3.35% Y/Y to 552 tons.