ACCESS MARKET

GOLD $4949.60 3:30 PM)

SILVER: 77.52 3;30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,861.400000000 USD

INTENT DATE: 02/05/2026 DELIVERY DATE: 02/09/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 2

099 H DEUTSCHE BANK AG 39

118 C MACQUARIE FUTURES US 4

190 H BMO CAPITAL MARKETS 141

323 C HSBC 8

363 H WELLS FARGO SECURITI 7

365 C MAREX CAPITAL MARKET 4

555 C BNP PARIBAS SEC CORP 1

555 H BNP PARIBAS SEC CORP 17

657 C MORGAN STANLEY 7

661 C JP MORGAN SECURITIES 172 140

685 C RJ OBRIEN 10

709 C BARCLAYS 270 2

880 H CITIGROUP 169

905 C ADM 3

TOTAL: 498 498

MONTH TO DATE: 32,502

JPMORGAN STOPPED 140/498

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 498 CONTRACTs NOTICES FOR 49,800 OZ or 1.5489 TONNES

total notices so far: 32,502 contracts for 3,250,200 OR 101.094 tonnes)

SILVER NOTICES: 181 NOTICE(S) FILED FOR 0.905 MILLION OZ /

total number of notices filed so far this month : 3,744 CONTRACTS (NOTICES) for 18.720 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S 1,510 MILLION OZ QUEUE JUMP//NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 20.655 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OOZ//

NEW TOTALS FOR SILVER OZ STANDING IS AS FOLLOWS

NORMAL STANDING 20.840 MILLION OZ

PLUS OUR 2 EXCHANGE FOR RISK: 185,000 OZ

EQUALS

20.840 MILLION OZ!! HUGE FOR A FEBRUARY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 27.525 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEU JUMP OF 1.510 MILLION OZ F AND THEN ADD OUR 2 EXCHANGE FOR RISK FOR .185 MILLION OZ STANDING ADVANCES TO 20.540 MILLION OZ!!

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 1.138 TONNES TO OTHER OF 18.6731 TONNES/ NEW QUEUE JUMP TOTAL: 19.8111 TONNES// AND THEN WE ADD OUR FIRST EXCHANGE FOR RISK: 276 CONTRACTS OR .858 TONNES//NEW STANDING ADVANCES TO 114.258 TONNES

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 114.258 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING AND OUR FIRST EXCHANGE FOR RISK!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES (WILTONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 66.883 TONNES (WHICH WILL BE ANOTHER STRONG)

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 5880 CONTRACTS OI TO 137,327 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1531 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1531 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 5903 CONTRACTS AND ADD TO THE 1531 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 4362 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $7.97

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 21.745 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $7.87

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES customer withdrawals: 2 ENTRIES i) out of Asahi: 24,949,705 oz (776 kilobars) ii) Out of HSBC 916 453.000 oz (3000 kilobars) total withdrawal: 121,402,705 oz or 3.772 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entry xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 498 notice(s) 49,800 OZ 1.5489 TONNES TONNES OF GOLD |

| No of oz to be served (notices) | 3956 contracts 395,600 OZ 12.304 TONNES |

| Total monthly oz gold served (contracts) so far this month | 32,502 notices 3,250,200 oz 101.094 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0

customer withdrawals:

2 ENTRIES

2 ENTRIES

i) out of Asahi: 24,949,705 oz (776 kilobars)

ii) Out of HSBC 916 453.000 oz (3000 kilobars)

total withdrawal: 121,402,705 oz or 3.772 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 7

ALL DEALER TO CUSTOMER:

a) Out of Asahi: 91,456.322 OZ oz

b) Out of Brinks: 42,996.063 oz

c) Out of HSBC 214,668.297

d) Out of JPMorgan: 38,631.131 oz

e) Out of Loomis 7,562.056 oz

e) Out of Malca: 385.812 oz

f) Manfra 26,689.738 oz

total adjusted out of dealer (reg) to eligible (customer) = 422,388.429 oz or 13.13 tonnes

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 4454 CONTRACTS FOR A LOSS OF 2326 CONTRACTS.

WE HAD 2692 CONTRACTS SERVED ON THURSDAY, SO WE GAINED A HUGE 336 CONTRACT–

QUEUE JUMP FOR 33,600 OZ OR 1.138 TONNES

MARCH SAW A LOSS OF 213 CONTRACTS DOWN TO 4888 CONTRACT OI AS MARCH BECOMES THE NEW FRONT MONTH FOR GOLD AND EXPECT TO HAVE A STANDING OF AROUND 13 TONNES FO GOLD

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 4054 CONTRACTS DOWN TO 280,772 CONTRACTS

We had 498 contracts filed for today representing 49,800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 132 notices issued from their client or customer account. The total of all issuance by all participants equate to 498 contract(s) of which 140 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (32,502) to which we add the difference between the open interest for the front month of FEB ( 4454 CONTRACTS) minus the number of notices served upon today (498 x 100 oz per contract) equals 3,645,800 OZ OR (113.399 Tonnes of gold) to which we add February’s first exchange for risk of 276 contracts or 27600 oz or .858 tonnes//new total gold standing in Feb increases to 114.258 tonnes.

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (32,502 x 100 oz +we add the difference for front month of FEB (4454 OI} minus the number of notices served upon today (498 x 100 oz) which equals 3,645,800 OR 113.399 TONNES// to which we add our first exchange for risk//27600 oz or .858 tonnes//new standing advances to 114.258 tonnes!!!

new total of gold standing in FEB is 114.258 TONNES//

TOTAL COMEX GOLD STANDING FOR FEB 114.258 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume THURSDAY confirmed 267,752 fair/

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,834,196.914 oz 57.05 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 35,370,216.368 oz oz

TOTAL REGISTERED GOLD 18,370,216.368 or 571.39 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,990,889.111//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 16,536,020 oz ((REG GOLD- PLEDGED GOLD)=

514.339 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SILVER/COMEX

FEB 6 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 5 entries i) out of Asahi: 1,244,595.280 oz ii) out of CNT 771,964.556. oz iii) Out of HSBC 452,652.977 iv) Out of Manfra 1,507,865.720 oz v) Out of Stonex: 122,989.730 oz total withdrawal: 4,099,665.263 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 1 ENTRY nil entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | 1 ENTRIES i) Into Brinks : 601,621.972 oz total deposit: 601,621.972 oz |

| No of oz served today (contracts) | 181 CONTRACT(S) ( 0.905 million OZ |

| No of oz to be served (notices) | 387 Contracts (1.935 MILLION oz) |

| Total monthly oz silver served (contracts) | 3744 contracts 18.720 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into Brinks : 601,621.972 oz

total deposit: 601,621.972 oz

withdrawals: customer side/eligible

5 entries

i) out of Asahi: 1,244,595.280 oz

ii) out of CNT 771,964.556. oz

iii) Out of HSBC 452,652.977

iv) Out of Manfra 1,507,865.720 oz

v) Out of Stonex: 122,989.730 oz

total withdrawal: 4,099,665.263 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 3

all dealer to customer:

a) Asahi 458,859.400 oz

b) Stonex: 141,469.560 oz

c) CNT 383,865.024 oz

net loss from dealer to customer acc’t : 0.984 million oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 102.547MILLION OZ//.TOTAL REG + ELIGIBLE. 394.511 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 568 OPEN INTEREST CONTRACTS FOR A LOSS OF 266 CONTRACTS.

WE HAD 608 NOTICES FILED ON THURSDAY SO WE GAINED 302 CONTRACTS OR A HUGE 302 CONTRACT QUEUE JUMP FOR 1.510 MILLION OZ

MARCH LOST 5317 CONTRACTS DOWN TO 80,502. THIS BECOMES THE FRONT MONTH FOR SILVER DELIVERY

APRIL GAINED 25 CONTRACTS TO AN OI 433 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 181 or 0.905 MILLION oz

CONFIRMED volume; ON THURSDAY 208,656 mammoth+++//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 3744 X5,000 oz = 18.720 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (568) AND the number of notices served upon today (181)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (3744)Notices served so far) x 5000 oz + OI for the front month of FEB(568) minus number of notices served upon today (181 )x 5000 oz equals silver standing for the FEB..contract month equating to 20.635 MILLION OZ. THEN WE MUST ADD OUR FIRST EXCHANGE FOR RISK TOTALS OF 25 CONTRACTS FOR .125 MILLION OZ TO TODAY’S 12 CONTRACT ISSUANCE//NEW TOTAL EXCHANGE FOR RISK 37 CONTRACTS FOR .185 MILLION OZ//NEW STANDING ADVANCES TO 20,84 MILLION OZ

NEW STANDING: 20.84 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 20.84 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 102.547 million oz of registered silver

JPMorgan as a percentage of total silver: 168.864/394.511.million: 42.69%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

FEB 6/2026/WITH GOLD UP $86.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1077.95 TONNES

FEB 5/2026/WITH GOLD DOWN $57.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.95 TONNES

FEB 4/2026/WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1083.38 TONNES

FEB 3/2026/WITH GOLD UP $270.80 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1087.10 TONNES

FEB 2/2026/WITH GOLD DOWN $100.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.10 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1077.95 TONNES, TONIGHTS TOTAL

SILVER

FEB 6 WITH SILVER UP 0.08 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 522.367 MILLION OZ

FEB 5 WITH SILVER DOWN $7.87 A HUGE WITHDRAWAL OF 2.175 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 526.309 MILLION OZ

FEB 4 WITH SILVER UP $2.02 A HUGE WITHDRAWAL OF 3.551 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 528.484 MILLION OZ

FEB 3 WITH SILVER UP $6.11 A MASSIVE MASSIVE PAPER AND FRAUUDULENT 32.898 CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 531.985 MILLION OZ

FEB 2 WITH SILVER DOWN $1.32 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 522.367 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Stackers smiling, traders trounced

The disconnection between physical reality and derivative volatility became obvious in gold and silver pricing this week. No silver? No matter. Futures carry on regardless.

| Alasdair MacleodFeb 6∙Paid |

This week has seen price instability in gold and particularly silver. This morning in European trade gold was $4875, up $210 from last Friday’s close and silver at $73.80 is down $11.60 having been as high as $92 on Wednesday.

Contrary to most commentary, speculative interest in both metals Comex contracts is very low, in gold’s case the lowest it has been this decade:

So, what is happening?

The fundamental reasons for stacking gold still apply. Furthermore, most of the big US banks are forecasting higher gold prices over 2026 with their investment funds seriously underweight. And reliable anecdotal evidence is that larger investors are taking the opportunity to buy more physical gold (and silver if they can get it) and are not put off by current developments. This is important, because it isolates the cause of price volatility as a function purely of derivatives.

In the absence of speculative buying interest from hedge funds, we can’t rule out speculative shorting. This is not reflected in Comex open interest, because it allows the swaps (market makers and bullion bank traders who normally take the short side) to close their shorts rather than create new contracts.

We await tonight’s Commitment of Traders report to assess the extent of these shifts. But if so, then the swaps have got a temporary get-out-of-jail card. But hedge funds are likely to be squeezed badly as well when the current hiatus subsides. This squeeze generated by physical demand on derivatives was first noticed in London’s silver forward market in early-October but could now be shifting to Comex.

This morning, the March silver contract stands at 80,479 on preliminary estimates, which compares with only 20,706 contracts equivalent registered in Comex vaults for delivery. In a normal market, we would expect this contract to be either closed or rolled into May which is the next active contract. But speculative interest, which is what normally gets rolled or closed, is extremely low, reflected in our next chart:

It’s about as low as it gets. But if it’s not speculative interest, then a good portion of those 80,479 contracts will stand for delivery, in which case there’s a significant possibility of contract failure. This might not happen because large bullion banks such as JPMorgan will probably find some silver from somewhere to augment registered stocks. But that is borrowing from Peter to pay Paul, adding to all the other leased and swapped obligations to be unwound. It is extremely unlikely that silver prices will remain this low with this deferred buying of physical overhanging the market.

Therefore, the squeeze on London and Comex continues, and is probably made significantly worse by a near-halving of the silver price entirely due to derivative instability.

Meanwhile, gold, which has suffered similarly from derivative shenanigans, has held up better than silver and as its chart plotted logarithmically illustrates it is not too far from trend:

Its price consolidation comes ahead of Japan’s snap general election on Sunday. Prime Minister Sanae Takaichi is strong favourite to win a clear mandate and will go ahead with her reflationary plans. She promises to use the funds to suppress price inflation, the idea being to take pressure off the Bank of Japan to raise rates. But printing money to curb inflation only leads to higher inflation, higher bond yields, and ultimately higher interest rates.

As the world’s principal supplier of capital, Japanese insurance companies and pension funds will be less receptive to buying US, EU, and UK debt as their bond yields resume their rise post-election. Therefore, it could become a different financial environment from next week onwards, including a deteriorating outlook for US debt financing.

Macro-economic figures released this week suggest a stalling US economy, which shows sign of destabilising the tech bubble and more particularly the associated super bubble which is bitcoin. Neo-Keynesian investment and hedge-fund managers take it all as a signal that the Fed can reduce interest rates earlier, reflected in US treasury bond yields easing slightly.

That is a mistake born out of a misunderstanding that bond yields ease in a recession. Instead, dollar bond yields are set to rise reflecting increasing supply of debt without the tax income to fund it.

We’ll see what the foreign holders of $44 trillion and underlying financial assets make of that, in the context of the US dollar debt trap being slammed firmly shut!

end

3. CHRIS POWELL AND HIS GATA DISPATCHES:

LIVE FROM THE VAULT YOU TUBE: 258 AND 257

TODAY CRAIG HEMKE

5. COMMODITY REPORT/COFFEE

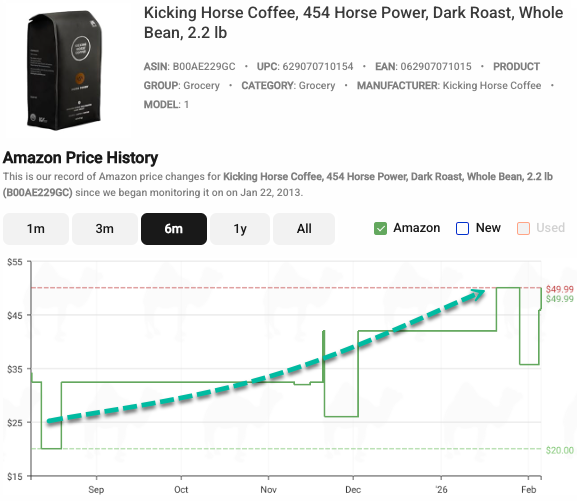

Six-Month Low In Coffee Futs Signals Potential Relief After Beans On Amazon Surge

Thursday, Feb 05, 2026 – 05:20 PM

Tracking a single brand of dark-roast arabica beans on Amazon via the price-tracking website CamelCamelCamel shows that a 2.2-pound bag has nearly doubled in price since August.

For American consumers, paying roughly twice as much for the same bag of coffee beans in just six months is a price shock, even if it is still cheaper than visiting Starbucks daily.

There may finally be some relief in sight. Arabica coffee futures have fallen to a six-month low, raising some hopes that bean prices may have topped out for now.

The most-active New York contract slid to a six-month low on Thursday, falling as much as 2.3% to about $3.10 a pound.

Bloomberg reports this decline was driven by a sharp rebound in exchange inventories, with coffee deliveries doubling over the past two weeks. That restocking has eased fears over near-term supply tightness that previously sent prices surging to nearly $4.5 a pound in 2025.

There is more good news: Favorable weather in Brazil, the world’s top coffee exporter, suggests more supply is near for the next harvest season.

Analysts at investment bank Itaú BBA told clients that traders are closely monitoring weather conditions in Brazil, where forecasts for continued, crop-friendly rains could further improve supply outlooks. If those rains materialize, speculative traders may further unwind bullish positions, adding to the downward pressure on coffee futures.

END

SILVER MICHAEL OLIVER;

WIDELY WATCHED MICHAEL OLIVER:

Michael Oliver Bombshell: Silver’s “Rebirth” After Smackdown – $500 Silver by Summer, $8,000 Gold

![]()

by ITM Trading

Friday, Feb 06, 2026 – 12:07

Michael Oliver isn’t mincing words. The U.S. sovereign debt market, he warns, is sitting on a trapdoor, with dynamics increasingly resembling Japan’s long grind into bond-market dysfunction. What many traders dismissed as a “jiggle in the middle” in gold and silver wasn’t a top—it was a forced shakeout before liftoff.

As paper assets fracture, capital is rotating hard. The dollar is breaking down, commodities are breaking out, and global bond markets are flashing crisis signals simultaneously. In this environment, Oliver says legacy indicators are useless. Silver isn’t “overbought”—it’s being repriced. His call: $300 to $500 silver by summer. Not a bubble. A reset.

Follow Daniela on X: Daniela Cambone

About ITM Trading: ITM Trading has been a trusted leader in precious metals for over 28 years, helping clients protect and grow their wealth with custom gold and silver strategies designed for economic downturns and currency resets.

END

SILVER/GOLD, PLATINUM

GOLD , SILVER OR PLATINUM LEASE RATES

HUGE INCREASE

| Robert Lambourne | 7:32 AM (48 minutes ago) | ||

| to me | |||

Harvey,

Thanks for your efforts. We are living in really interesting times.

Here is a collection of material which will hopefully be of interest.

1. Chinese AI gave what I feel is an informative reply to a question on how long historically large premiums in silver have lasted in Shanghai. It’s been rather longer than I had realised. So maybe, we will have what appears to be an unsustainable difference for some time.

Historical playbook: how long can a premium last?

• Apr–Jul 2020: 8–12 % Shanghai premium lasted 97 days while China maintained COVID-era export curbs; spread collapsed only after Beijing released 2 000 t from state stockpile and restored air-cargo lanes.

• Oct 2022: Russia–Ukraine logistics shock → +6 % premium for 46 days; closed when Indian refiners re-routed metal via Dubai and Chinese solar wafer makers cut orders during power rationing.

Today’s export-quota regime is structural, not event-driven, so the half-life is longer unless:

(a) MOFCOM doubles quota (needs State Council sign-off), or

(b) COMEX price falls another ≥ 20 % so that landed cost in China < domestic price.

2. There are reports that the fall in silver prices on 5 February on SHFE has been blamed on a coordinated short squeeze and that the exchange authorities took action against the parties involved.

Here is a link to a piece about this on Substack.

3. I have some implied lease rates for you from yesterday evening based on the Comex. Sorry, but I’m having some issues with my computer equipment so this is an image only. They are really high, even for gold historically.

Regards,

Bob

THEN

Higher margins after today

Inbox

| Robert Lambourne | 7:56 AM (26 minutes ago) | ||

| to me, Chris | |||

The authorities seem desperate to keep prices suppressed. There also appears to have been an effort to suppress prices yesterday in Shanghai as per my earlier email.

This is the classic playbook from the Hunt brothers time.

CME Group hikes gold, silver margins again as volatility grips markets –

END

2.ASIAN AFFAIRS FEB 6/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 10.33 PTS OR 0.25%

//Hang Seng CLOSED DOWN 325.29 PTS OR 1.25%

// Nikkei CLOSED UP 476,86 PTS OR 0.87%

//Australia’s all ordinaries CLOSED DOWN 1.43%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9369

/ OFFSHORE CLOSED UP AT 6.9375 Oil DOWN TO 64.09 dollars per barrel for WTI and BRENT DOWN TO 68.06 Stocks in Europe OPENED MOSTLY ALL RED

ONSHORE USA/ YUAN TRADING UP TO 6.9389 OFFSHORE YUAN TRADING UP TO 6.9375 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.9389

OFFSHORE YUAN: DOWN TO 6.9376

HANG SENG CLOSED DOWN 325.29 PTS OR 1.21%

2. Nikkei closed UP 476.96 PTS OR 0.87%

WEST TEXAS INTERMEDIATE OIL DOWN 64.09

BRENT; 68.06

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 97.73 /// EURO FALLS TO 1.1789 DOWN 12 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.229/ UP 1/3 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.03… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.567 DOWN 6 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8257 Italian 10 Yr bond yield DOWN to 3.458 SPAIN 10 YR BOND YIELD DOWN TO 3.205

3i Greek 10 year bond yield DOWN TO 3.441

3j Gold at $4862/30 Silver at: 73.69 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 15/100 roubles/dollar; ROUBLE AT 76.91

3m oil (WTI) into the 64 dollar handle for WTI and 68 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.25 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.229% UP 1/3 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.564 DOWN 1/4 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7779 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9173 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.191 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.850 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.477 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.61 UP 7 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.5390 DOWN 2 PTS

30 YR UK BOND YIELD: 5.360 DOWN 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.404 DOWN 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.910 DOWN 3 BASIS PTS.

1a New York Opening report

Futures Rebound To Session High As Software, Gold And Bitcoin All Jump

Friday, Feb 06, 2026 – 08:50 AM

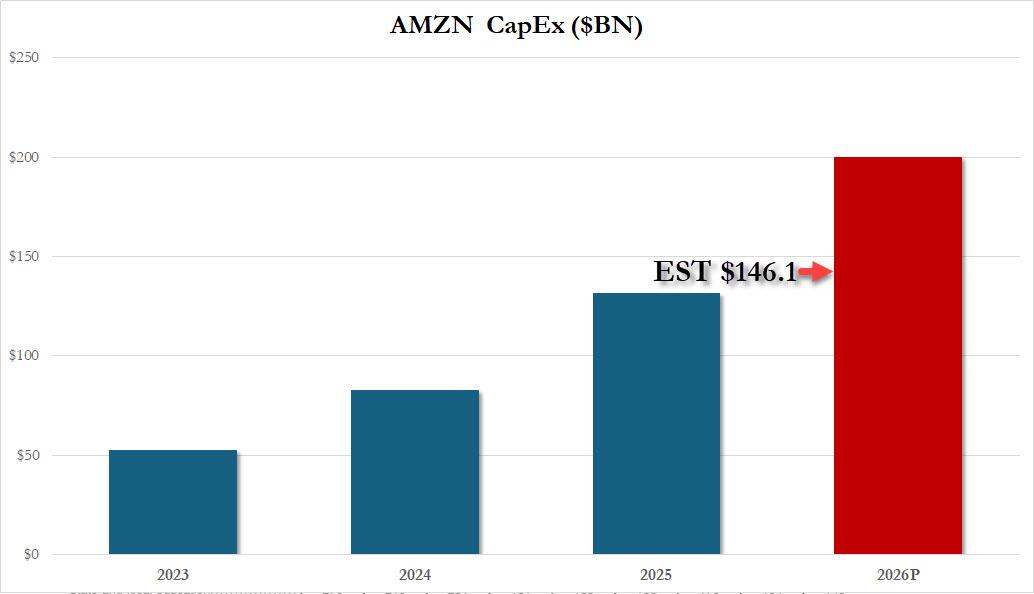

US equity futures are poised to open higher with Software companies finally bouncing (as previewed here), even though Amazon continues to be deep in the red after its eye-watering capex outlook. US stocks will cap a bruising week in which a rush to unwind crowded trades – from AI shares to precious metals and crypto – triggered margin calls and amplified the market’s slide. With the S&P 500 on track for its worst week this year, S&P futures are 0.6% higher at 8:15a.m. ET while contracts on the Nasdaq 100, which just suffered its ugliest three days since Trump’s trade war sent markets into a tailspin in April, were up 0.8% after erasing an earlier decline while precious metals and cryptocurrencies climb after falling sharply on Thursday. In premarket trading, Mag 7 are mostly higher except for AMZN which is down -7% post-earnings on a staggering capex guidance ($200BN, vs $146BN est); NVDA +2.7%, MSFT +1.6%. Yields are 1-3bp higher led by the front-end overnight while the USD is at session lows. Commodities are mixed: base metals are lagging, while gold and silver added 2.0% and 4.4%, respectively; oil added 0.4% overnight. Oil trades near session lows as US-Iran nuclear talks take place. Bitcoin has bounced more than 10% from its session lows just above $60K as dip buying makes a tentative comeback.

In premarket trading, Mag 7 stocks are mostly higher with one exception: Amazon is down 7% after the company announced plans to spend $200 billion this year on data centers, chips and other equipment, worrying investors that its colossal bet on artificial intelligence may not pay off in the long run. AI infrastructure stocks rally after Amazon’s massive capex forecast. Gainers include AMD (AMD) +2%. Other Magnificent Seven stocks: Tesla +0.6%, Alphabet -1%, Microsoft +1.3%, Apple -0.4%, Meta Platforms +0.08%

- Cryptocurrency-linked stocks rally as Bitcoin rebounded after a selloff that briefly dragged the token to a more than 50% retreat from its October peak.

- Bill Holdings (BILL) rises 12% after the payments-automation company raised its full-year forecast.

- Bloom Energy (BE) rises 13% after the manufacturer of solid-oxide fuel cells gave a forecast for 2026 revenue that beat the average analyst estimate.

- Hims & Hers Health (HIMS) falls 8% after FDA Commissioner Marty Makary said his agency will take “swift action against companies mass-marketing illegal copycat drugs, claiming they are similar to FDA-approved products.”

- Impinj (PI) falls 27% after the semiconductor device company gave an outlook that is much weaker than expected, given an inventory overbuild. The results prompted a downgrade

- Molina (MOH) tumbles 25% after the health insurer forecast 2026 profit that was less than half of Wall Street’s expectations.

- Reddit (RDDT) climbs 8% after the social-media company’s fourth-quarter results beat expectations across key metrics. It also gave an outlook that is seen as strong.

- Roblox (RBLX) jumps 8% after the video-game company reported fourth-quarter results that beat expectations on key metrics. It also gave an outlook that is seen as positive.

- Stellantis (STLA) plunges 27% after the carmaker said a business reset resulted in charges of around €22.2 billion for the second half of 2025. Akros says the charges were about double what they expected.

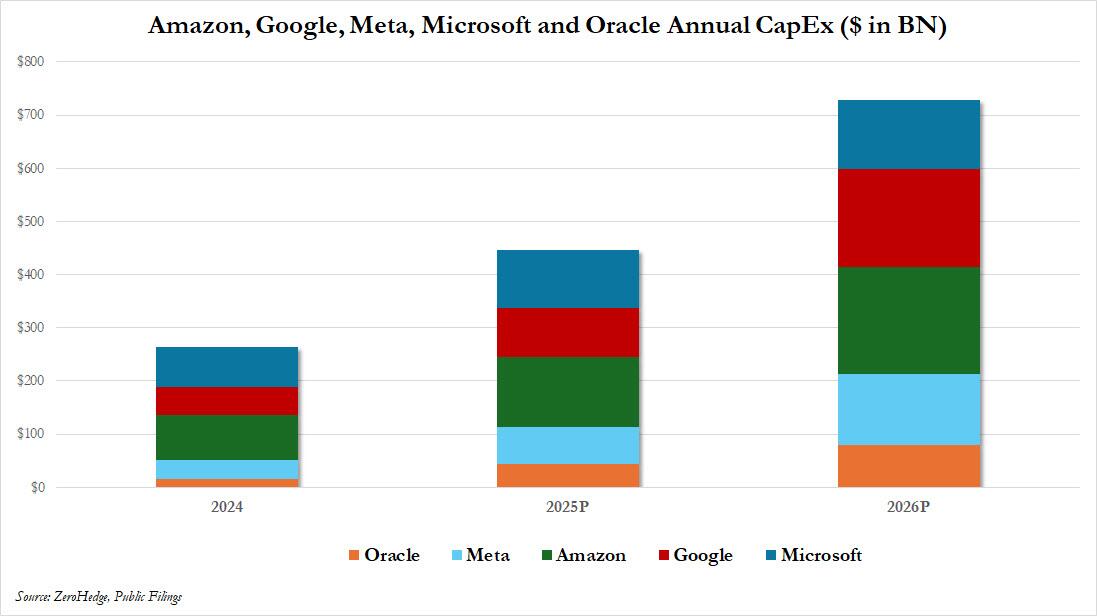

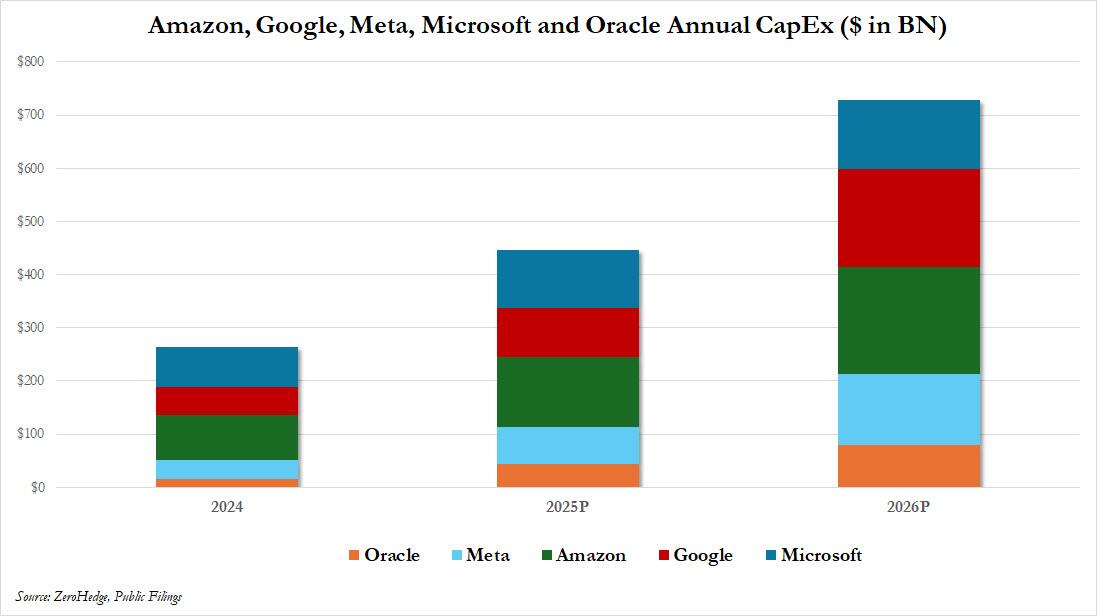

Investors have been spooked by developments on two fronts: the rollout of models from AI startup Anthropic that threaten to render large swaths of software services redundant, alongside the eye-watering spending plans of tech companies. Four of the biggest tech firms plan to invest around $650 billion this year in data centers and the equipment required to run them.

Amazon, almost 8% lower in pre-market trading, is the latest Mag7 member to spook investors about ballooning AI spending, projecting $200 billion for capex this year, far more than the $146 billion Wall Street had penciled in. Taken together with plans from Meta, Google and Microsoft, capital spending by the Big Four AI “hyperscalers” is set to hit about $650 billion this year — up from $356 billion in 2025 and under $100 billion in 2020. On current trajectories, that suggests the quartet’s capex could top $1 trillion in 2027, a scale of investment that’s giving investors pause in what has long been a disinflationary tech industry.

Some investors still appear willing to open their wallets. Oracle’s record-setting bond deal on Monday is an encouraging signal for other big tech firms seeking to raise hundreds of billions of dollars for data-center infrastructure, according to Goldman Sachs’ syndicate desk. Yet if the mounting cost of building AI is rattling markets, so too is the disruption the technology threatens to unleash on other industries. Anthropic is rolling out a new model, Claude Opus 4.6, tailored for financial research – just days after its move into legal services jolted legacy software providers. Meanwhile, Blackstone-backed Liftoff Mobile postponed its IPO this week as a selloff in tech shares compounded investor concerns about AI’s impact.

Still, the week’s retreat is allowing traders to separate stocks facing genuine risk or overvaluation from those caught up in the broader risk-off rout, as the AI rally of the past three years continues to broaden beyond the largest names.

“This is an opportunity for us as active investors to take the baby that has been thrown out with the bath water, because there’s still names out there that we believe will come out very well,” said Fabiana Fedeli, chief investment officer for equities, multi-asset and sustainability at M&G Investments.

For Rory Sandilands, a fixed-income portfolio manager at Aegon Ltd., uncertainty over the disruptive nature of AI may linger as it remains too early to tell how effective the new tools are, or how quickly other software may become obsolete.

“What we’re seeing in the marketplace is fear, because nobody understands really who the winners and losers will be,” Sandilands said. “There’s not enough cushion in credit spreads in aggregate to really to help soften that blow.”

Bitcoin, another canary in the coal mine for risk appetite, touched a new 15-month low of $60,033 on Friday morning, before rallying more than 10%. The original cryptocurrency suffered its biggest daily drop since 2022 on Thursday. Bitcoin’s plunge is intensifying the crisis rocking the digital-asset complex. Few companies are more exposed than Strategy, which confirmed in earnings announcement on Thursday a net loss of $12.4 billion for the fourth quarter, driven by the mark-to-market decline in its vast holdings. Retail investors who piled into the Trump administration’s promised crypto paradise via Wall Street-approved funds are also learning an expensive lesson in market gravity. Crypto funds had their biggest outflows since November in the week ended Feb. 4, Bank of America says, citing EPFR Global data. Money market funds attracted the most inflows, along with stocks. That said, today crypto may finally be due for a rebound: tracking the Software basket, bitcoin is more than 10% above the overnight lows of $60K, trading near session highs of $67K.

Silver has managed a modest rally from Thursday’s 17% leg lower, but remains nearly 39% down from its peak barely a week ago.

Also recall: it may be the first Friday of the month, but there are no non-farms payrolls. Earlier this week, the Bureau of Labor Statistics said the January jobs report would be delayed to next Wednesday because of the partial government shutdown.

Turning to earnings, companies representing nearly 70% of the S&P 500’s market value have now reported in this earnings season. Of the 289 S&P 500 companies to have reported so far, more than 78% have beaten analysts’ forecasts, while 17% have missed. Next week, the calendar is much lighter, with another 8% of the S&P’s market cap reporting. Philip Morris International and Biogen are among those companies expected to report results before the market opens on Friday. PMI investors will be looking for continued strength in its smoke-free portfolio, which includes heated tobacco products and nicotine pouches, to support high-single digit sales growth in the fourth-quarter. For Biogen, all eyes will be on the performance of Leqembi, the drugmaker’s treatment for early Alzheimer’s disease.

European stocks also advance, with construction, utility and bank shares leading gains. Autos underperform as Stellantis shares tumble. Consumer products and chemicals also lag, while construction shares outperform, as French group Vinci announced strong 2025 earnings. Here are some of the biggest movers on Friday:

- Bayer rises as much as 3.2% after the German company said its experimental drug — called asundexian — cut the risk of secondary strokes by 26% in a late-stage trial.

- Kongsberg shares soar as much as 17% after the Norwegian defense firm posted results that Morgan Stanley says delivered a strong end to the year, with all divisions recording double-digit growth in the fourth quarter.

- Vontobel shares rise as much as 6.1% after the investment management firm reported a significant trading-driven earnings beat, according to analysts at Citi.

- Renk Group shares rise as much as 10% after BNP Paribas raises its recommendation on the German defense company to outperform from neutral, citing a reassuring message from the CEO over the upcoming earnings report and the outlook for 2026.

- Stellantis shares fall as much as 24%, the steepest drop on record, after the carmaker said a business reset resulted in charges of around €22.2 billion for the second half of 2025. Akros says the charges were about double what they expected.

- SocGen shares dropped as much as 4.1% following a strong rally after the French lender reported what an RBC analyst says are mixed results as Bloomberg Intelligence notes trading revenue missed estimated and fell short of peers.

- Kering shares fall as much as 5.5% after Morgan Stanley trimmed its price target on the French luxury group ahead of next week’s earnings, saying recent channel checks point to a more difficult start to 2026 than anticipated.

- Coloplast shares drop as much as 9.6% after the Danish medical products-maker reported weaker-than-expected sales and earnings for the first quarter, hurt by its Kerecis skin substitutes business.

- Anglo American shares fall as much as 3.1% after BofA analysts cut the miner’s rating to neutral from buy, citing risks to completing its Teck Resources acquisition and uncertainty over the value of non-core businesses.

- European software and IT services stocks are coming under renewed pressure, tracking declines in Asian and US peers, after Anthropic unveiled a new version of its most powerful artificial intelligence model designed to carry out financial research.

Earlier in the session, Asian stocks pared their initial declines on Friday but still headed for a weekly slide, dragged by concerns over artificial intelligence shares and panic selling in precious metals. The MSCI Asia Pacific Index dropped as much as 1.3% before trading little changed in Friday’s session, with South Korea and Taiwan’s tech-sensitive markets overcame declines. Stocks in Hong Kong dropped and mainland China extended its retreat, while Japan’s market rebounded after opening at a loss. On the week, the regional gauge slid as much as 2.5%, set to snap its streak of advances that started in mid-December. Thailand will also be heading to the polls for a general election, with spending plans and measures to support growth among investors’ top priorities. Shares in India were steady after the central bank kept its benchmark interest rate unchanged, signaling an end to its easing cycle.

“Asian markets have fallen this week as volatility in precious metals prompted investors to reassess stretched valuations more broadly,” said Fabien Yip, market analyst at IG International. A spillover from the US tech selloff has added more pressure, although the region’s decline has been more moderate than global peers, she added.

In FX, the Bloomberg Dollar Spot Index is down 0.2% while the Norwegian krone and Australian dollar are the best performing G-10 currency, rising 0.8% each against the greenback. USD/JPY is little changed ahead of the Japanese election on Sunday.

In rates, treasuries edge lower, pushing US 10-year yields up 2 bp to 4.20%. Gilts lead a rally in European government bonds, with UK 10-year yields falling 3 bps to 4.53%. A combination of the Trump administration’s focus on affordability and a weakening employment picture could open the door to further rate cuts, said Mohit Kumar, chief strategist for Europe at Jefferies.

“Our view remains that we could get a scenario where growth is robust and yet employment is weakening due to the impact of AI,” Kumar wrote. “A Warsh-led Fed could end up being more dovish than what the market currently expects.”

Money market funds attracted the most inflows in the week ended Feb. 4 along with stocks, Bank of America Corp. said, citing EPFR Global data. Crypto funds had their biggest outflows since November, while gold funds saw their first weekly outflow since November.

In commodities, WTI crude futures are steady near $63.30 a barrel as traders eyed the outcome of talks between Iran and the US. Spot silver rises over 5% while Bitcoin rallies back above $66,000 after dropping more than 50% from its October peak.

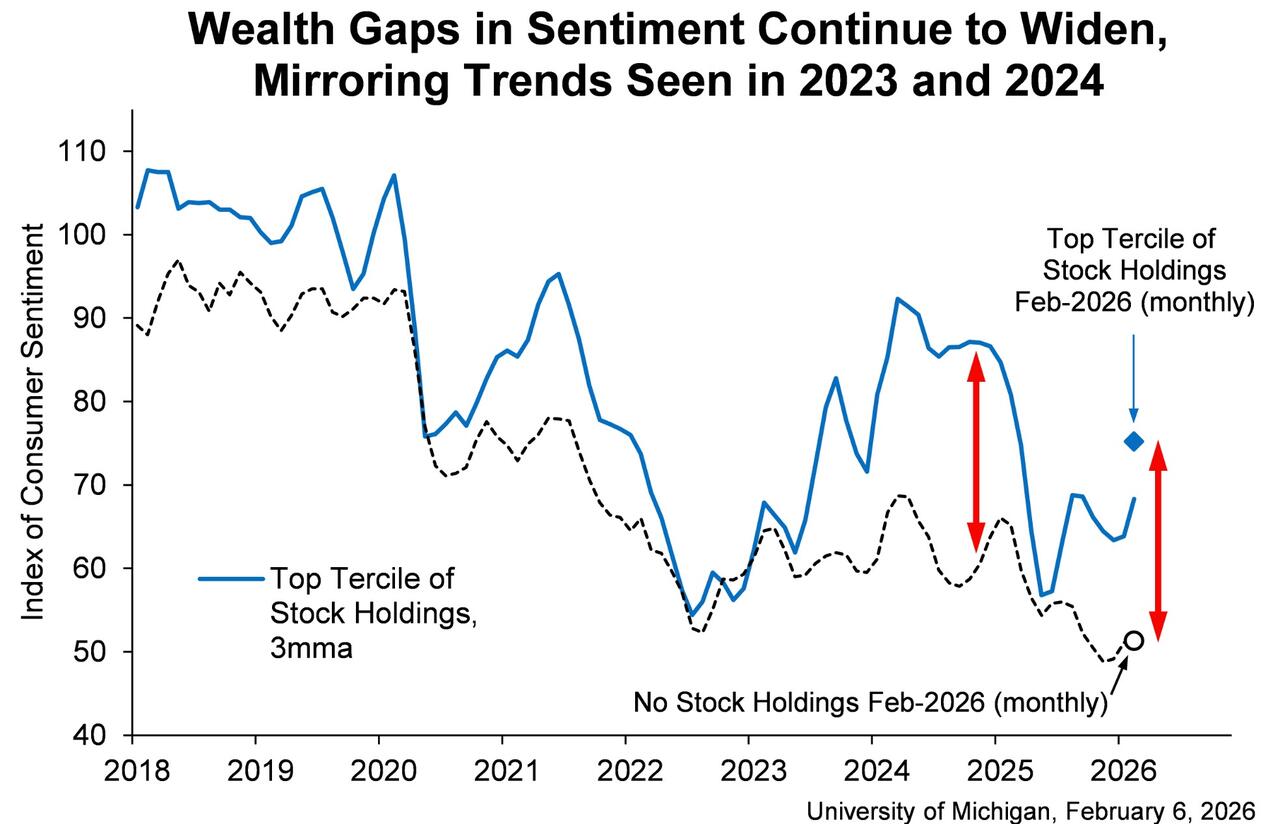

Looking at today’s calendar, the University of Michigan’s provisional reading of consumer sentiment in February is due at 10 a.m. ET however.

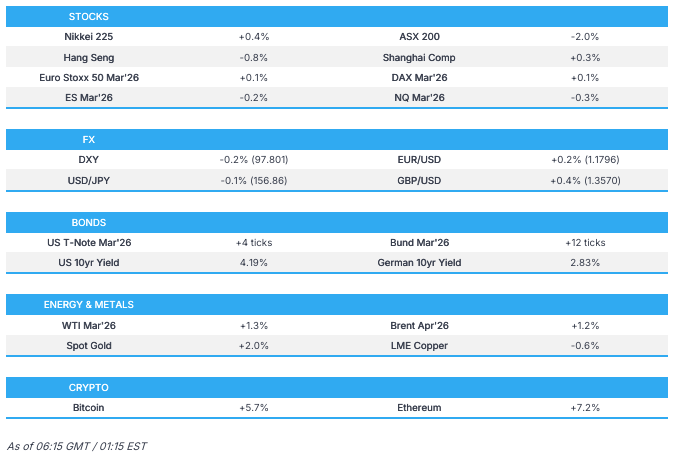

Market Snapshot

- S&P 500 mini +0.4%

- Nasdaq 100 mini +0.5%

- Russell 2000 mini +0.8%

- Stoxx Europe 600 little changed

- DAX +0.1%

- CAC 40 -0.2%

- 10-year Treasury yield +1 basis point at 4.19%

- VIX -1.3 points at 20.51

- Bloomberg Dollar Index -0.1% at 1193.65

- euro +0.1% at $1.1794

- WTI crude +0.7% at $63.73/barrel

Top Overnight News

- Oil dropped US-Iran talks got underway in Oman, with Tehran indicating that a quick deal is unlikely. BBG

- The U.S. Virtual Embassy in Iran issued a security alert early Friday urging American citizens to “leave Iran now.” The notice came as American and Iranian officials were scheduled for a new round of negotiations in Oman on Friday. CNBC

- Bitcoin is bouncing this morning (currently +525bps), rising after a selloff that briefly dragged the token to more than 50% below its October peak. BBG

- US consumer sentiment probably edged lower at the start of February on concerns about a cooling labor market and elevated prices. BBG

- BOJ board member Kazuyuki Masu highlighted the need for a higher benchmark interest rate. BBG

- Indonesia’s assets slid after Moody’s cut the country’s credit outlook to negative. The cost of insuring sovereign debt rose to around 80 bps, the biggest increase among Asian sovereigns. BBG

- Intel and AMD have notified Chinese customers of supply shortages for server central processing units (CPUs), with Intel warning of delivery lead times of up to six months. The supply constraints have driven up prices for Intel’s server products in China by more than 10% generally, although pricing varies by customer contract. RTRS

- Big Tech stocks sold off heavily after the companies unveiled plans to spend $660bn this year on AI, as investors fret that the “breathtaking” capital expenditures are outpacing the eranigns potential of the new technology. Amazon, Google and Microsoft are set to lose a combined $900bn in mkt value since filing their quarterly earnings over the past week. FT

- Sweden’s core inflation slowed more rapidly than expected last month, suggesting a March rate cut may be in play. The CPIF rate excluding energy fell to 1.7% from 2.3% in December. BBG

- South Korean official said US is taking necessary steps regarding the issue of South Korea being on sensitive country lists: Yonhap.

Trade/Tariffs

- Japan and US 1st round of investment to include gas power, ports and artificial diamond, totalling JPY 6-7tln, Nikkei reported.

- Chinese Commerce Ministry said they will lead policy measures to promote travel service exports and boost inbound consumption.

- French President Macron to visit Japan at the end of March, via Nikkei.

- South Africa Trade Minister said they signed a framework economic partnership with China, while the agreement will be followed by an early harvest agreement by end of March 2026, which will then see China provide duty-free access to South African exports.

- South Korea Foreign Minister said South Korea is not intentionally delaying US investment.

- Venezuela and Qatar review bilateral agenda to strengthen cooperation.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were ultimately mixed after the global market rout rolled over into the region following the continued tech woes stateside and weak US labour market data. Nonetheless, most of the regional benchmark indices are well off their worst levels, as the early sell-off gradually stabilised. ASX 200 was among the underperformers with the index dragged lower by heavy tech losses, and with sentiment also not helped by M&A-related disappointment after the proposed Rio Tinto-Glencore merger fell through, while there were comments from RBA Governor Bullock, who noted the RBA board is not happy with inflation and the prospects of getting it down. Nikkei 225 initially declined amid the broad risk-off mood and disappointing Household Spending data, but then recovered as sentiment improved and with participants awaiting the snap election on Sunday, where the ruling bloc is widely anticipated to achieve a landslide victory. Hang Seng and Shanghai Comp were mixed amid a lack of fresh pertinent catalysts and with the mainland clawing back all of its early losses following another two-pronged liquidity operation by the PBoC utilising both 7-day and 14-day reverse repos.

Top Asian News

- Indonesian President said they signed a security treaty with Australia.

- Former Bank of China (3988 HK) Vice President was expelled from the China Communist Party for serious violations of discipline and law.

- China’s Ministry of Agriculture issues implementation plan to advance rural revitalisation and agricultural modernisation.

- Japan ruling parties expected to win over 300 seats out of the 465 seats in the lower house election, according to Nikkei.

European bourses (STOXX 600 +0.1%) broadly opened on the backfoot but have gradually moved higher as the morning progressed. European sectors opened with a clear negative bias but are now mixed. Construction leads, boosted by upside in Vinci (+6.5%). To the downside, Autos has been hit by significant pressure in Stellantis (-22.3%). The Co. noted it is to take a EUR 22bln charge as it resets its business and scales back on its recent EV push.

Top European News

- Russian Ambassador said the UK and France should participate if there is a serious talk multilateral nuclear disarmament.

- UK and China working group will work towards an MOU between the PBoC and BoE.

- ECB’s Escriva said there is always room for changes in monetary policy; inflation is at target and expectations are anchored.

FX

- DXY marginally pulled back since the start of the APAC session after gaining against its peers yesterday amid haven appeal and as the buck continued to nurse some of its YTD weakness, with momentum following the Warsh Fed Chair nomination remaining intact yesterday, despite the slew of weaker-than-expected labour market metrics. The European morning has seen trade within tight parameters as traders look ahead to the University of Michigan prelim survey and comments from Fed’s Jefferson. DXY resides in a 97.75-97.97 range after finding support near 98.00 once again after printing a 97.60-97.98 parameter yesterday.

- EUR/USD ekes mild gains and retested the 1.1800 level, albeit with price action contained following the uneventful ECB policy announcement yesterday, with several ECB speakers offering commentary today, albeit with no obvious impact on EUR assets. Further, the ECB Survey of Professional Forecasters suggested headline and core HICP inflation expectations unchanged across all horizons, while Real GDP growth expectations unchanged except for a slight upward revision for 2026. EUR/USD currently trades within a 1.1765-1.1801, versus Thursday’s 1.1775-1.1822 range.

- GBP/USD regained some composure after the prior day’s underperformance, which was caused by the BoE’s dovish vote split and UK political woes and calls grow for UK PM Starmer to resign. GBP/USD trades between 1.3508-1.3581 compared to yesterday’s wide 1.3518-1.3654 parameter.

- USD/JPY declined overnight but trimmed losses to trade flat at the time of writing, but with price action choppy ahead of the election on Sunday and following disappointing Household Spending data from Japan, while BoJ’s Masu reiterated that the central bank will raise rates if the economy and prices are in line with the BoJ’s outlook.

- Antipodeans outperform across the G10 space, rebounding from a weekly trough as the early sell-off in metals and stocks gradually stabilised and then reversed.

Fixed Income

- USTs are firmer by a handful of ticks, remaining at the elevated levels seen in the prior session. As a reminder, the strength seen on Thursday was attributed to: a) risk-off sentiment, b) poor US jobs data, c) a dovish hold at the BoE. Newsflow is lacking this morning, aside from the recommencement of US-Iran talks in Oman – the key risk is that talks break down, leading to a potential US strike on Iran. Geopols aside, focus will be on the US data slate, which includes the UoM survey. Currently within a 112-06+ to 112-16+ range.

- Bunds are also firmer this morning, following peers; currently firmer by around 15 ticks and trading within a 128.31-128.58 range. Earlier, German Exports rose more than expected with Imports also topping expectations – promising data from the region, though more focus was on the Industrial Production. The metric fell sharply in December, which highlights the uncertain nature of Germany’s recovery. Following this data, Bunds rose from 128.37 to a high of 128.46, before scaling back to just under the 128.40 mark where the benchmark currently resides. Several ECB speakers have appeared throughout the day, Kazaks highlighted risks of the stronger EUR, whilst Rehn suggested that there’s a real risk of lower-than-expected inflation.

- Australia sold AUD 800mln 1.00% December 2030 bonds, b/c 4.14, avg. yield 4.3641%.

Commodities

- WTI and Brent briefly dipped below USD 63/bbl and USD 67/bbl, respectively at the start of the Asia-Pac session, before steadily bidding higher as European trade gets underway. The key event traders will be looking out for today is any reporting following the US-Iran nuclear talks in Oman. As of writing, the meeting has gotten underway but there have been reports that a convoy carrying US officials has left the site where the talks have been taking place.

- Spot gold is trading stronger today and currently at the upper end of a USD 4,655.23-4,903.40/oz range, and just above its 21 DMA (USD 4,848/oz). Focus remains on geopolitical updates out of Oman as the US and Iran remain in meetings.

- Base metals hold a negative bias this morning but have gradually picked up off worst levels as the risk tone improves. 3M LME Copper currently trades in a USD 12,540-12,896.78/t range.

- China’s National Gold Group to constrain precious metals repurchase business from the 7th of February.

- China’s Shanghai Gold Exchange to increase margin ratios, price limits for some gold and silver contracts from the 9th of February closing settlement.

- Weekly SHFE warehouse stocks change (W/W): Copper +6.8%, Aluminium +13.1%, Zinc +8.5%, Lead +56.4%.

- Iraq’s SOMO Director said they are planning to boost oil export from the south by 120k BPD.

- Thailand’s TFEX announces the temporary trading halt of silver online futures.

- Mexico reportedly evaluating how to send fuel to Cuba while avoiding US tariffs.

Central Banks

- BoJ’s Masu said he does not think the BoJ is behind the curve and need to monitor the impact of FX on inflation. Timing of rate hikes to neutral is not predetermined. Not suggesting food price moves need immediate action. Watching food inflation beyond rice prices. Policy should be carefully guided to keep underlying inflation around 2%. True that Japan’s negative real interest rate is likely behind rises in property prices. Past pace of rate hikes will not be any guide to the future pace of hikes.

- BoJ’s Masu said the central bank is closely watching FX market moves and their impact on the economy and prices, also noted that appropriate and timely rate hike is needed. said:. BoJ will raise rates if the economy and prices are in line with the BoJ’s outlook. Cause of inflation also warrants close attention, in terms of whether inflation is truly caused by supply-side factors alone or by a combination of both demand- and supply-side factors. Real interest rate remains at a significantly negative level in Japan. Convinced that continuing with further policy interest rate hikes will be needed to complete the normalisation of monetary policy in Japan.

- BofA expects ECB to hold rates in 2026 (prev. 25bp cut in March), sees 25bps cuts in March and June 2027.

- ECB Survey of Professional Forecasters: Headline and core HICP inflation expectations unchanged across all horizons; Real GDP growth expectations unchanged except for a slight upward revision for 2026. Unemployment rate expectations unchanged for 2026 and 2027 but slightly lower thereafter.

- ECB’s Muller said December’s outlook still good for basic decision making.

- ECB’s Rehn on their next meeting in March said they will be receiving new data and updates for ECB’s forecast, allowing them to refine their assessment of the Euro area’s growth momentum and inflation dynamic. Any changes in the key interest rates in the future, if justified and not executed. Highlights that there’s a real risk of lower than expected inflation.

- ECB’s Kazaks said that rapid EUR strengthening may trigger a response from the ECB.

- ECB’s Villeroy said downside risks are probably more significant; the ECB has no FX target.

- ECB’s Stournaras said “we are monitoring exchange rates”; have strong confidence in the economic outlook. ECB is monitoring the FX rate, but euro increase has not been dramatic. FX rate levels are not a primary focus. January inflation data should be viewed in context. Meeting-by-meeting approach has been good practice. Judges that risks are balanced. Do not think we have to take any action now.

- RBA Governor Bullock said RBA board is not happy with inflation and the prospects of getting it down.

- RBA Governor Bullock said much of the recent increase in inflation is judged to be temporary, but some of it seems to be persistent, adds Board will be monitoring closely the extent to which the strong inflation we have observed is persistent or temporary. said:Labour market is still doing very well, calling it good news.

- RBI maintains Repurchase Rate at 5.25%, as expected, via unanimous decision and maintains neutral policy stance.

Geopolitics: Russia-Ukraine

- Russian Ambassador said the UK and France should participate if there is a serious talk multilateral nuclear disarmament.

- Russia’s Kremlin said Abu Dhabi talks will continue; on nuclear talks, said Russia and the US realise the need to begin talks soon.

- Deputy Head of Russian Military intelligence shot in Moscow, sources report.

Geopolitics: Middle-East

- Iranian media reported that the second round of Muscat talks does not signify the start of negotiations, and these initial sessions have been held for each party to coordinate with the Omani mediator.

- Second round of nuclear negotiations between the US and Iran have gotten underway.

- An Iranian diplomatic person said the presence of CENTCOM or any military officials can jeopardise indirect nuclear talks between the US and Iran.

- A convoy reportedly carrying American officials leaves the site of the US-Iran talks in Oman, the AP reported; details light.

- US envoy Kushner is also attending US-Iran talks, according to Iranian state TV.

- Iran and US commence nuclear talks in Oman, Iranian media reported.

- Iran’s Foreign Minister said they are fully prepared to defend Iran’s sovereignty and security against any transgressions.

- US-Iran talks are reportedly delayed by a few hours.

- Israeli media reported that Israeli PM Netanyahu said in closed sessions of the Knesset that political, military and economic factors brought Iran closer to a critical point, although he did not consider the fall of the government to be certain. He warned that any Iranian attack would be met with a “strong response”.

- US President Trump posted “Rather than extend “NEW START” (A badly negotiated deal by the United States that, aside from everything else, is being grossly violated), we should have our Nuclear Experts work on a new, improved, and modernized Treaty”. Full post: “The United States is the most powerful Country in the World. I completely rebuilt its Military in my First Term, including new and many refurbished nuclear weapons. I also added Space Force and now, continue to rebuild our Military at levels never seen before. We are even adding Battleships, which are 100 times more powerful than the ones that roamed the Seas during World War II — The Iowa, Missouri, Alabama, and others. I have stopped Nuclear Wars from breaking out across the World between Pakistan and India, Iran and Israel, and Russia and Ukraine. Rather than extend “NEW START” (A badly negotiated deal by the United States that, aside from everything else, is being grossly violated), we should have our Nuclear Experts work on a new, improved, and modernized Treaty that can last long into the future. Thank you for your attention to this matter! PRESIDENT DONALD J. TRUMP”.

Geopolitics: Others

- US to resume aid to North Korea whilst outreach stalls, via the WSJ. According to a US official, the decision isn’t an act of gesture but rather as a de facto block on aid to North Korea.

- Senior South Korea official said expects progress in a few days regarding the North Korea issue, according to Yonhap.

US Event Calendar

- 10:00 am: United States Feb P U. of Mich. Sentiment, est. 55, prior 56.4

- 12:00 pm: United States Fed’s Jefferson Speaks on the Economy

DB’s Jim Reid concludes the overnight wrap

Risk assets came under mounting pressure over the last 24 hours, as concerns around AI and a weak batch of US data led to growing questions about the near-term outlook. Once again, software led the sell-off, with the S&P 500’s software component (-5.01%) posting a 7th consecutive fall, whilst the broader S&P 500 (-1.23%) fell for a 3rd session running. But there were clear signs of stress more widely, with the VIX index (+3.13pts) reaching a new 2026 high of 21.77pts, whilst Bitcoin (-13.14%) saw its worst daily decline since November 2022, closing at a 15-month low of $63,083 and down almost 50% from its October peak. Overnight, it even surpassed that 50% threshold, falling to just $60,033 after midnight in London, but it’s since bounced back to $65,366 again. Meanwhile, the risk-off mood drove a sharp rally in Treasuries, with 2yr yields (-10.3bps) posting their biggest decline in six months. And there’s no sign of the sell-off finding a floor just yet, as disappointing results from Amazon after the US close have meant that futures on the S&P 500 are down another -0.50% this morning.

That latest software decline now leaves its S&P 500 component down -29.9% from its October peak. And if you’d just known that US software would be in bear market territory back then, you’d be forgiven for thinking markets would have seen a huge correction by now. However, what we’ve actually seen is a significant rotation, which Jim looked at in yesterday’s chart of the day (link here). So other sectors have taken up the baton from tech, such as energy, materials and consumer staples, meaning that the overall S&P 500 still only closed -2.6% beneath its record high from last month.

Interestingly, that pattern echoes what we saw in 2000 as the dot-com bubble started to burst. Equities started to fall from the March 2000 as tech stocks saw significant declines. However, consumer staples, utilities and healthcare rallied significantly over the months ahead, and in September the S&P 500 actually came within a percentage point of its record high from six months earlier. So it shows that a market can absorb a prolonged rotation without obvious index-level stress for some time. But the longer and deeper the sell-off in a dominant sector becomes, the harder it is for the broader index to withstand the drag, and the continued losses for tech in 2000 ultimately meant the S&P 500 ended that year over -10% lower.

This latest sell-off has shown no sign of easing yet, and it got further momentum as Amazon reported after the close last night. Its net sales guidance was largely in line with expectations but this was accompanied by a sharp rise in planned capex spending, which is expected to reach $200bn this year, well above expectations. That spending also weighed on the operating income guidance ($16.5-21.5bn in the current quarter vs $22.2bn estimated) and pushed Amazon’s shares down by more than -10% in after-hours trading.