FEB 10//GOLD CLOSED DOWN $46.80 TO $5008.15 WHILE SILVER WAS ALSO DOWN $2.21 TO $80.51/PLATINUM WAS DOWN $36,20 TO $2087.20 WHILE PALLADIUM WAS DOWN $14.60 TO $1713.15//CIBC GIVES A COMPELLING CASE WHY AGNICO GOLD MINES IS THE BEST MINING OPERATION ON THE PLANET//FALLOUT FROM THE CONVICTION OF MEDIA MOGUL JIMMIE LAI IN HONG KONG//FROM EUROPE: GERMANY’S ECONOMY CONTINUES TO FALTER//GOOD COMMENTARY ON THE STUPIDITY OF FRANCE//ISRAEL AND IRAN UPDATES/AS WELL AS RUSSIA VS UKRAINE/USA//THE FEUD BETWEEN TRUMP AND CARNEY ESCALATE: TRUMP IS THREATENING TO HALT TRAFFIC FROM THE AMBASSADOR BRIDGE CONNECTING WINDSOR AND DETROIT: THIS WOULD BE CATASTOPHIC FOR BOTH COUNTRIES//USA DATA RELEASES//SWAMP STORIES FOR YOU TONIGHT//

072 C GOLDMAN 1 099 H DEUTSCHE BANK AG 144 118 C MACQUARIE FUTURES US 1 132 C SG AMERICAS 14 190 H BMO CAPITAL MARKETS 49 323 C HSBC 2 365 C MAREX CAPITAL MARKET 1 555 C BNP PARIBAS SEC CORP 28 555 H BNP PARIBAS SEC CORP 4 657 C MORGAN STANLEY 2 661 C JP MORGAN SECURITIES 4 36 709 C BARCLAYS 5 880 H CITIGROUP 42 905 C ADM 1

TOTAL: 167 167 MONTH TO DATE: 33,783

MONTH TO DATE: 32,502

JPMORGAN STOPPED 248/1114

February

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 167 CONTRACTs NOTICES FOR 16,700 OZ or 0.5189 TONNES

total notices so far: 33,783 contracts for 3,378,300 OR 105.079 tonnes)

FOR FEB.

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 429 NOTICE(S) FILED FOR 2.145 MILLION OZ /

total number of notices filed so far this month : 4,490 CONTRACTS (NOTICES) for 22.950 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $46.80 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.43 TONNES OF GOLD INOT THE GLD/

INVENTORY RESTS AT 1079.66 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $2.21 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV/

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 520.555 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 862 CONTRACTS TO 136,120 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE $5.24 GAIN IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S // TRADING.

NOW ON A NET BASIS OUR SPECULATORS HAVE REVERTED BACK TO GOING LONG. THE FRBNY ON A NET BASIS IS PROVIDING THE NECESSARY PAPER TO OUR LONGS AND THEN THE LONGS TENDER FOR PHYSICAL AT 4 PM. BECAUSE OF THE HUGE SHORTFALL IN PHYSICAL SILVER THERE IS A LOTTERY TO SEE WHO GETS ANY OF THE PHYSICAL SILVER THAT IS PRESENT. IF NOBODY GETS ANY THEY COME BACK THE NEXT DAY AND SO ON. THIS IS IN LONDON, THE HOME OF PHYSICAL SILVER!!

WE HAVE REVERTED TO SPECS NOW GOING BACK TO THE LONG SIDE AND THE BANKER (FRBNY) ON THE SHORT SIDE

IT IS OUR SILVER SPECULATORS THAT WERE BRUTALLY BEATEN UP AT THE SILVER COMEX AND GOT RINSED OUT BADLY WITH FRIDAY GAIN. WE FINALLY ARE MOVING TO A MUCH HIGHER BASE SURPASSING THE $34.40 SILVER PRICE BARRIER TO A HIGH DEGREE, AND NOW READY TO ATTACK AGAIN, OUR LAST MAJOR HURDLE OF $100.00 SILVER.

WE HAVE A HUGE SIZED GAIN OF 1707 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE SIZED 845 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO MONDAY TRADING WITH OUR GAIN IN PRICE ALONG WITH ANOTHER MASSIVE 9981 T.A.S. ISSUANCE!! /// THEY DESPERATELY AGAIN TODAY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON MONDAY WITH SILVER’S HUGE GAIN IN PRICE AS THE SPECS PILED INTO THE SILVER ARENA.

THE PRICE FINISHED STILL ABOVE THE MAGIC NUMBER OF $50.00 SILVER SPOT PRICE BUT BELOW THE $100.00 MARK CLOSING AT $82.72 UP $5.24 WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS AT AN ULTRA MAMMOTH SIZED 9984 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING ABOVE THE 100.00 DOLLAR MARK!!.MAMMOTH SIZE T.A.S ISSUANCE IS BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A HUGE SIZED 845 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR MAMMOTH SIZED 9984 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//RAID AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HAD A MEGA HUGE SIZED GAIN OF 1721 CONTRACTS ON OUR TWO EXCHANGES WITH OUR HUGE GAIN IN PRICE OF $5.24 WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION AND NO DOUBT REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE STICKY SPECULATOR LONGS STILL REMAIN STOIC EVEN ON OUR HUGE PRICE FALLS. THE NON STICKY SPECULATORS ARE BEING WIPED OUT. EASTERN CENTRAL BANKERS (LIKE CENTRAL BANK OF INDIA) AND LARGE INDUSTRIAL USERS CONTINUE ON THE LONG SIDE AS THEY WILL TENDER FOR THE BADLY NEEDED PHYSICAL SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT//TUESDAY MORNING: AN ULTRA MAMMOTH SIZED 9984 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS AS ONE UNIT, BUT SELL THE SHORT SIDE FIRST AND THEN LIQUIDATE THE LONG SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S 2.155 MILLION OZ QUEUE JUMP//NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 23.280 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ//

NEW TOTALS FOR SILVER OZ STANDING IS AS FOLLOWS

NORMAL STANDING 23.280 MILLION OZ

PLUS OUR 2 EXCHANGE FOR RISK: 185,000 OZ

EQUALS

23.465 MILLION OZ!! HUGE FOR A FEBRUARY

WE HAD:

/ HUGE COMEX OI GAIN+// A HUGE SIZED 845 EFP ISSUANCE CONTRACTS (/ VI) A MEGA MEGA HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 9984 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 11 SILVER CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN.. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FRB.

TOTAL CONTRACTS for 7 DAY(S), total 6800 contracts: OR 34.0000 MILLION OZ (971 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 34.0000 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 34.000 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 862 CONTRACTS WITH OUR HUGE GAIN IN PRICE OF $5.24 IN SILVER PRICING AT THE COMEX// MONDAY,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED CONTRACT EFP ISSUANCE:845 CONTRACTS ISSUED FOR MARCH, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS.W HAD A HUGE 2.135 MILLION OZ QUEUE JUMP// THEN WE MUST ADD OUR FIRST EXCHANGE FOR RISK: 25 CONTRACTS FOR 125,000 OZ TO OUR SECOND EXCHANGE FOR RISK OF 12 CONTRACTS OR 0.060 MILLION OZ//NEW TOTALS NOW JUMPS UP TO 23.465 MILLION OZ!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

LAST 10 MONTHS OF SILVER DELIVERIES

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEU JUMP OF 2.135 MILLION OZ F AND THEN ADD OUR 2 EXCHANGE FOR RISK FOR .185 MILLION OZ STANDING ADVANCES TO 23.465 MILLION OZ!!

THE NEW TAS ISSUANCE MONDAY NIGHT (9984) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!!

WE HAD 429 NOTICE(S) FILED TODAY FOR 2.145 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON A MASSIVE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2837 OI CONTRACTS UP TO 404,446 OI AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE ARE NOW AT ITS NADIR OI IN COMEX BUT WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE CRIMINAL 1738 CONTRACTS // MEGA HUGE GOVERNMENT REMOVALS//

WE HAD A FAIR SIZED GAIN IN COMEX OI (2837 ONTRACTS) . THIS OCCURRED WITH OUR HUGE GAIN OF $100.00 IN PRICE// MONDAY///.

LAST 10 MONTHS OF GOLD DELIVERIES: (MAY THROUGH TO /FEB)

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.3701 TONNES TO OTHER OF 23.204 TONNES/ NEW QUEUE JUMP TOTAL: 23.5741 TONNES// AND THEN WE ADD OUR TWO EXCHANGE FOR RISK: 3276 CONTRACTS OR 10.189 TONNES//NEW STANDING ADVANCES TO 127.342 TONNES

E.F.P. ISSUANCE/FOR OPENING FEB. GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2655 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 404,446 AND WE NOW WITNESSING A LOWER COMEX OI BUT WITH AN EXTREMELY HIGH PRICE OF GOLD.//NOW ALMOST IMPOSSIBLE TO FLEECE.

SILVER ALSO HAS A FAIR SIZED COMEX OI OF 136,120 CONTRACTS//

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5492 CONTRACTS WITH 2837 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 2655 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5492 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED BUT CRIMINAL 3343 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON

GOLD PRICE ON MONDAY ROSE BY $100.00

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(2655) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI OF 2837 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5492 CONTRACTS..

WE HAVE 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND NEWBIE SPECULATORS GOING TO THE LONG SIDE// . ,2.) STRONG INITIAL STANDING FOR GOLD FOR FEBRUARY:

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.3701 TONNES TO ALL OTHER QUEUE JUMP OF 23.204 TONNES//NEW QUEUE JUMP TOTALS: 23.5741 TONNES// /// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR 276 CONTRACTS OR 2760 OZ OR .858 TONNES//NEW STANDING ADVANCES TO 127.342 TONNES

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 127.342 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING AND OUR TWO ISSUANCES EXCHANGE FOR RISK!!

3) ZERO T.A.S. LIQUIDATION (AND CONSIDERABLE GOVT LIQUIDATION // AND A STRONG GAIN OF EQUITY SHARES/FEB 5 AS WE HAD 1)A $100.00 COMEX PRICE GAIN AND WE HAD 2) NEWBIE SPEC SHORTS GOING LONG AGAIN ON A NET BASIS, + EASTERN CENTRAL BANKERS WERE PILING INTO THE LONG SIDE AS WE HAD A STRONG SIZED GAIN OF 5492 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A HUGE AMOUNT OF GOLD WILL STAND FOR DELIVERY IN FEB. (127.342 TONNES). //, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4)A STRONG SIZED COMEX OI GAIN 5) V) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (3496) AND A STRONG T.A.S. ISSUANCE (3343) FOR RAID PURPOSES

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

TOTAL EFP CONTRACTS ISSUED: 27,654 CONTRACTS OR 2,765,400 OZ OR 86.01 TONNES IN 7 TRADING DAY(S) AND THUS AVERAGING: 3950 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN7 TRADING DAY(S) IN TONNES: 86.01 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2025, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 86.01TONNES DIVIDED BY 3550 x 100% TONNES = 2.42% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES (WILTONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 86.01 TONNES (WHICH WILL BE ANOTHER STRONG)

SPREADING OPERATION

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 862 CONTRACTS OI TO 136,120 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 845 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 876 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 862 CONTRACTS AND ADD TO THE 845 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1707 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $5.24

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.535 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $5.24

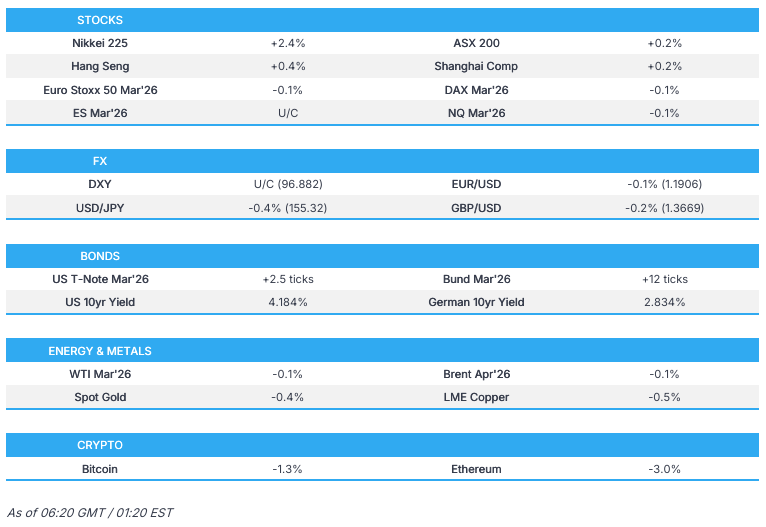

2.ASIAN AFFAIRS FEB 10/2025

SHANGHAI CLOSED UP 5.28 PTS OR 0.13%

//Hang Seng CLOSED UP 155.99 PTS OR 0.58%

// Nikkei CLOSED UP 1238.56 PTS OR 2.20%

//Australia’s all ordinaries CLOSED UP 0.69%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9130

/ OFFSHORE CLOSED UP AT 6.9102 Oil UP TO 64.35 dollars per barrel for WTI and BRENT UP TO 69.29 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING UP TO 6.9130 OFFSHORE YUAN TRADING UP TO 6.9101 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2,837 CONTRACTS UP TO 404,446 OI WITH OUR STRONG GAIN IN PRICE OF $100.00 WITH RESPECT TO MONDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD BUT OUR SHORT SPECS GOT CLOBBERED. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3496).

WE HAD ZERO T.A.S. LIQUIDATION MONDAY. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO LONG MONDAY AFTER A BRIEF PERIOD OF GOING NET SHORT, AS WERE HIT BADLY ON FRIDAY, WITH OUR FRBNY GOING NET LONG AND THE SPECS PROVIDING THE SHORT PAPER. CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY WITH MEGA SHOCK FROM THE SHORT SPECS AS THEY NEEDED TO PROVIDE THE PHYSICAL!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW BACK TO AN EXTREMELY LOW OI OF AROUND 404,000 TO NOW 404,446 AND NOW AMPLE ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE DIFFICULT TO FLEECE. THE ALL TIME LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 5 %

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 7230 CONTRACTS (OR 22.488TONNES).

THEN WE WERE NOTIFIED OF A MONSTER 3000 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 300,000 OZ OR 9.3312 TONNES OF GOLD ONE OF THE HIGHEST EVER ISSUED AND THUS THE TOTAL ISSUANCE FOR FEB NOW TOTALS TWO.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO FEBRUARY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

THEN WE HAVE 6 ISSUED IN JANUARY: 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, jAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

FEB EXCHANGE FOR RISK: NOW 2 ISSUANCES: 3276 CONTRACTS FOR 327,600 OZ OR 10.189 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 56+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WAS ADDED TO OUR DAILY TOTALS!! (17.656 TONNES)

FEBRUAY ISSUANCE 1. FOR; 0.858 TONNES SO FAR!!

DETAILS ON OUR NEW FEBRUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 5492 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH FEBRUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 3343 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY THROUGH TO FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING TODAY’S MONSTER 9..3312 TONNE ISSUANCE. OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0,000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

11.FEB; 0. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.3701 TONNES ADDING TO ALL OTHER QUEUE JUMPS OF 23.204 TONNNES//NEW TOTAL QUEUE JUMP: 23.5741/ / STANDING ADVANCES TO XXXXX TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK OF 10.189 TONNES/NEW STANDING ROCKETS TO 127.349 TONNES!!

THE FED IS THE OTHER MAJOR SHORT IN GOLD OF AROUND 56+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 56+ TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. BUT IT IS IMPOSSIBLE/ THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!!,(LATEST BIS DATA SHOWS AN INCREASE IN GOLD BORROWING BY THE FRBNY// BUT MAY BE THE BUYER IN JANUARY OF 22.315 TONNES TOTAL IN JANUARY/6 ISSUANCES AS WE NOW HAVE THE BIS DATA FOR GOLD SWAPS FOR DECEMBER 2025 AND HERE WE FIND THAT THE FED ACTUALLY INCREASED THEIR GOLD SWAP LOANS WITH THE BIS TO THE 56 TONNES WHICH I NOW RECORD FOR YOU.!!THEN MUCH TO OUR ANGER WE RECEIVE NOTICE OF OUR SECOND EXCHANGE FOR RISK OF 9.3312 TONNES//TOTAL EXCHANGE FOR RISK FEB WITH 2 ISSUANCES EQUATES TO 10.189 TONNES OF GOLD.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/FEB.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 2655 CONTRACTS.

THAT IS A STRONG SIZED 2655 EFP CONTRACT WAS ISSUED: : /APRIL 2655 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2655 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 56+ TONNES

WE HAD :

NO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE HUGE GOVERNMENT LIQUIDATION

HUGE MONTH END SPREADERS LIQUIDATION ENDED FEB 2 AS IT FINALIZED OPERATIONS AS THEY AWAIT THEIR TURN AT THE END OF THIS MONTH OF FEBRUARY.

T.A.S.SPREADER ISSUANCE//FEBRUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A STRONG SIZED 3342 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP MONDAY’S GAIN IN PRICE IN GOLD WITH A CORRESPONDING STRONG SIZED GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

JANUARY’S 6 ISSUANCE FOR 22.215 TONNES

AND NOW FEB’S TWO ISSUANCES FOR A MONSTER 10.189 TONNES.

THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 56+ TONNES OF GOLD.

MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAIDS TO BE!

MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OPTIONS EXPIRY MONTH INCLUDING JANUARY’S OTC/LBMA DRIVE BY SHOOTING! ALONG WITH RAIDS IN EARLY FEBRUARY

GOLD STANDING AT THE COMEX FOR GOLD LAST 13 MONTHS OF 2025

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.3701 TONNES WHICH IS ADDED TO ALL OTHER QUEUE JUMPS OF 23.204 TO TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB:: 23.5741 TONNES///STANDING ADVANCES TO 117.163 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK OF 10.189 TONNES/NEW STANDING ROCKETS TO TO 127.349 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING FEBRUARY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $100.00)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL MONDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR FEBRUARY. THE COMEX IS ONE BIG MESS!!

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.3701 TONNES TO WHICH WE ADD TO ALL OTHER QUEUE JUMPS OF 23.204 / NEW QUEUE JUMP TOTALS: 23.5741 TONNES//STANDING ADVANCES TO: 117.163 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK OF 3276 CONTRACTS FOR 327,600 OZ OR 10.189 TONNES/NEW STANDING 127.849 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $100.00

WE HAD A HUGE 1738 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES : 5492 CONTRACTS OR 549,200 OZ OR 17.08 TONNES

Total monthly oz gold served (contracts) so far this month

33,733 notices 3,373,300 oz 105.079 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0

customer withdrawals:

1 ENTRIES

1 ENTRIES

i) Out of hsbc 64,302.000 OZ

(2000 KILOBARS)

total withdrawal: 64,302.000 or 2.0 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 6

ALL DEALER TO CUSTOMER:

a) Out of Brinks: 167,738.861 oz

b) out of HSBC: 85,650.941 oz

c) Out of Loomis: 3375.855 oz

d) out of JPMorgan: 117,576.207 oz

e) Out of Malca 79,187.913 oz

f) Out of Manfra: 6,269.445 oz

total adjusted out of dealer and landing into customer acct: 439,829.222 oz

or 13.650 tonnes

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 4052 CONTRACTS FOR A LOSS OF 995 CONTRACTS.

WE HAD 1114 CONTRACTS SERVED ON MONDAY, SO WE GAINED A STRONG 119 CONTRACT–

QUEUE JUMP FOR 11,900 OZ OR 0.3701 TONNES

MARCH SAW A GAIN OF 164 CONTRACTS UP TO 5070 CONTRACT OI AS MARCH BECOMES THE NEW FRONT MONTH FOR GOLD AND EXPECT TO HAVE A STANDING OF AROUND 15 TONNES FO GOLD

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT GAINED 3115 CONTRACTS UP TO 283,182 CONTRACTS

We had 167 contracts filed for today representing 16,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 4 notices issued from their client or customer account. The total of all issuance by all participants equate to 167 contract(s) of which 36 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (33,783) to which we add the difference between the open interest for the front month of FEB ( 4052 CONTRACTS) minus the number of notices served upon today (167 x 100 oz per contract) equals 3,766800 OZ OR (117.163 Tonnes of gold) to which we add February’s two exchange for risk of 3276 contracts or 327,600 oz or 10.189 tonnes//new total gold standing in Feb increases to 127.349 tonnes.

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (33,783 x 100 oz +we add the difference for front month of FEB (4052 OI} minus the number of notices served upon today (167 x 100 oz) which equals 3,766,800 OR 117.163 TONNES// to which we add our TWO exchange for risk//327,600 oz or 10.189 tonnes//new standing advances to 127.349 tonnes!!!

new total of gold standing in FEB is 127.349 TONNES//

TOTAL COMEX GOLD STANDING FOR FEB 127.349 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF FEBRUARY.

confirmed volume MONDAY confirmed 153,802 fair/

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,828,313,281 oz 56.86 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 35,229,810.642 oz

TOTAL REGISTERED GOLD 17,799,159.769 or 553.63 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,430,650.823 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 15,970,846 oz ((REG GOLD- PLEDGED GOLD)=

496.760 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SILVER/COMEX

THE FEB 2026 SILVER CONTRACTS

FEB 10 2026

INITIAL/

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

5 entries

i) out of Asahi: 628,704.400 oz ii) out of CNT 678,372.665 oz iii) Out of Delaware 19,167.272 oz

iv) Out of JPMorgan 2,135,547.800 oz v) Out of Loomis: 900,673.370 oz

total withdrawal: 4,362,465.507 oz

the comex is being drained of silver

Deposits to the Dealer Inventory

1 ENTRY

0 entries

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Deposits to the Customer Inventory

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into Delaware: 169,483.949 oz

No of oz served today (contracts)

429 CONTRACT(S) ( 2.145 million OZ

No of oz to be served (notices)

166 Contracts (0.830 MILLION oz)

Total monthly oz silver served (contracts)

4490 contracts 22.450 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

2 ENTRIES

2 entries

i) Into CNT 291,987.700 oz ii) Into Stonex: 19,763.180 oz

total deposit into dealer; 311,750.850 OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into Delaware: 169,483.949 oz

withdrawals: customer side/eligible

5 entries

i) out of Asahi: 628,704.400 oz ii) out of CNT 678,372.665 oz iii) Out of Delaware 19,167.272 oz

iv) Out of JPMorgan 2,135,547.800 oz v) Out of Loomis: 900,673.370 oz

total withdrawal: 4,362,465.507 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 4

dealer to customer:

a) JPMorgan: 372,167.520 oz

b) Loomis: 106,868.472 oz

c) Malca: 191,129.600 oz

d) Manfera: 191,574.800

net loss from dealer to customer acc’t : 0.861 million oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 101.394MILLION OZ//.TOTAL REG + ELIGIBLE. 386.273 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 595 OPEN INTEREST CONTRACTS FOR A GAIN OF 110 CONTRACTS.

WE HAD 317 NOTICES FILED ON MONDAY SO WE GAINED 427 CONTRACTS OR A HUGE 427 CONTRACT QUEUE JUMP FOR 2.135 MILLION OZ

MARCH LOST 2937 CONTRACTS DOWN TO 73,128. THIS BECOMES THE FRONT MONTH FOR SILVER DELIVERY AND WE SHOULD HAVE A DANDY OF A MARCH DELIVERY MONTH!!!

APRIL GAINED 22 CONTRACTS TO AN OI 466 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 429 or 2.145 MILLION oz

CONFIRMED volume; ON MONDAY 106,530 mammoth+++//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 4490 X5,000 oz = 22.450 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (595) AND the number of notices served upon today (429)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (4490)Notices served so far) x 5000 oz + OI for the front month of FEB(595) minus number of notices served upon today (429 )x 5000 oz equals silver standing for the FEB..contract month equating to 23.280 MILLION OZ. THEN WE MUST ADD OUR FIRST EXCHANGE FOR RISK TOTALS OF 25 CONTRACTS FOR .125 MILLION OZ TO FRIDAY’S 12 CONTRACT ISSUANCE//NEW TOTAL EXCHANGE FOR RISK 37 CONTRACTS FOR .185 MILLION OZ//NEW STANDING ADVANCES TO 23.465 MILLION OZ

NEW STANDING: 23.465 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 23.465 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 101/394 million oz of registered silver

JPMorgan as a percentage of total silver: 165.879/386.273.million: 40.43%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

FEB 9/2026/WITH GOLD UP $100,00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.23 TONNES

FEB 6/2026/WITH GOLD UP $86.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1077.95 TONNES

FEB 5/2026/WITH GOLD DOWN $57.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.95 TONNES

FEB 4/2026/WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1083.38 TONNES

FEB 3/2026/WITH GOLD UP $270.80 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1087.10 TONNES

FEB 2/2026/WITH GOLD DOWN $100.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.10 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1079.66 TONNES, TONIGHTS TOTAL

SILVER

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

FEB 9 WITH SILVER UP $5,24 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

FEB 6 WITH SILVER UP 0.08 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 522.367 MILLION OZ

FEB 5 WITH SILVER DOWN $7.87 A HUGE WITHDRAWAL OF 2.175 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 526.309 MILLION OZ

FEB 4 WITH SILVER UP $2.02 A HUGE WITHDRAWAL OF 3.551 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 528.484 MILLION OZ

FEB 3 WITH SILVER UP $6.11 A MASSIVE MASSIVE PAPER AND FRAUUDULENT 32.898 CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 531.985 MILLION OZ

FEB 2 WITH SILVER DOWN $1.32 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 520.555 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

3. CHRIS POWELL AND HIS GATA DISPATCHES:

LIVE FROM THE VAULT YOU TUBE: 258 AND 257

TODAY CRAIG HEMKE

5. COMMODITY REPORT/GOLD AND SILVER/BILL HOLTER

END

AND HERE IS A REPORT ON THE WORLD’;S NUMBER ONE GOLD MINER AGNICO EAGLE:

COURTESY OF CIBC

Assessing Agnico Eagle Mines (AEM) Valuation After CIBC’s Higher Gold Price Outlook

Scroll back up to restore default view.

Agnico Eagle Mines (AEM) is back in focus after CIBC raised its gold price forecasts and reaffirmed a positive view on the miner, highlighting the company’s solid production, cash generation, and mine footprint.

The recent CIBC upgrade and higher gold price forecasts come on top of a strong run, with Agnico Eagle Mines posting a 21.8% 90 day share price return and a very large 3 year total shareholder return, suggesting momentum has been building rather than fading.

If this move in gold has your attention, it could be a good moment to look beyond a single miner and scan 21 elite gold producer stocks for other potential opportunities in the sector.

With AEM up strongly over the past year and trading at a discount to the average analyst price target, the key question is whether the stock still offers value or if the market is already pricing in future growth.

Most Popular Narrative: 11.3% Undervalued

At a last close of $196.60 versus a narrative fair value of $221.67, the most followed view sees more upside still baked into Agnico Eagle Mines.

Exploration success and rapid reserve expansion near key long-life assets (notably Detour Lake, Canadian Malartic, and Hope Bay) position Agnico Eagle for significant organic production growth; this supports a long runway of high-quality, low-risk volume expansion that can drive top-line revenue growth and production leverage.

Curious what earnings power that kind of reserve story is meant to support? The narrative leans on measured revenue growth, firm margins and a premium future earnings multiple. The exact mix of those inputs is where the valuation story gets interesting.

However, this upbeat narrative still depends on gold prices remaining supportive, and on major projects avoiding delays or cost overruns that could reduce future earnings power.

The narrative model sees Agnico Eagle Mines as 11.3% undervalued, but the simple P/E check tells a tighter story. AEM trades on 28.6x earnings, above both the US Metals and Mining industry at 26.8x and its own fair ratio of 26.3x, which points to a valuation that leans expensive rather than cheap. For you, that raises a simple question: is this premium paying for quality or just for recent momentum?

I have some implied lease rates for you from yesterday evening based on the Comex. Sorry, but I’m having some issues with my computer equipment so this is an image only. They are really high, even for gold historically.

Regards,

Bob

THEN

Higher margins after today

Inbox

Robert Lambourne

7:56 AM (26 minutes ago)

to me, Chris

The authorities seem desperate to keep prices suppressed. There also appears to have been an effort to suppress prices yesterday in Shanghai as per my earlier email.

This is the classic playbook from the Hunt brothers time.

CME Group hikes gold, silver margins again as volatility grips markets –

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 5.28 PTS OR 0.13%

//Hang Seng CLOSED UP 155.99 PTS OR 0.58%

// Nikkei CLOSED UP 1238.56 PTS OR 2.20%

//Australia’s all ordinaries CLOSED UP 0.69%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9130

/ OFFSHORE CLOSED UP AT 6.9102 Oil UP TO 64.35 dollars per barrel for WTI and BRENT UP TO 69.29 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING UP TO 6.9130 OFFSHORE YUAN TRADING UP TO 6.9101 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.9130

OFFSHORE YUAN: UP TO 6.9101

HANG SENG CLOSED UP 155.99 PTS OR 0.58%

2. Nikkei closed UP 2110.21 PTS OR 1.76%

WEST TEXAS INTERMEDIATE OIL UP 64.55

BRENT; 69.29

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX UP TO 96.78 /// EURO RISES TO 1.1910 UP 9 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +2.228/ DOWN 6 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.53… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.495 DOWN 7 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.8268 Italian 10 Yr bond yield DOWN to 3.440 SPAIN 10 YR BOND YIELD DOWN TO 3.198

3i Greek 10 year bond yield DOWN TO 3.438

3j Gold at $5049.00 Silver at: 82.55 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 11/100 roubles/dollar; ROUBLE AT 77.11

3m oil (WTI) into the 64 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/