GOLD CLOSED CLOSED DOWN $143.65 TO $4928.15

ACCESS MARKET

GOLD $4918.02 3:30 PM)

SILVER: 75.00 3;30 PM

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 5,071.600000000 USD

INTENT DATE: 02/11/2026 DELIVERY DATE: 02/13/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 2

099 H DEUTSCHE BANK AG 702

118 C MACQUARIE FUTURES US 2

118 H MACQUARIE FUTURES US 111

190 H BMO CAPITAL MARKETS 724

323 C HSBC 10

332 H STANDARD CHARTERED B 2

363 H WELLS FARGO SECURITI 62

365 C MAREX CAPITAL MARKET 6

435 H SCOTIA CAPITAL (USA) 151

555 C BNP PARIBAS SEC CORP 237

555 H BNP PARIBAS SEC CORP 20

657 C MORGAN STANLEY 9

661 C JP MORGAN SECURITIES 131

685 C RJ OBRIEN 20

686 C STONEX FINANCIAL INC 17

709 C BARCLAYS 525 3

880 H CITIGROUP 213

905 C ADM 7

TOTAL: 1,477 1,477

MONTH TO DATE: 35,436

JPMORGAN STOPPED 131/1477

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 1477 CONTRACTs NOTICES FOR 147,700 OZ or 4.5940 TONNES

total notices so far: 35,436 contracts for 3,643,600 OR 110.220 tonnes)

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000 OZ /

total number of notices filed so far this month : 4,595 CONTRACTS (NOTICES) for 22.975 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S 0.000 MILLION OZ QUEUE JUMP//NEW STANDING FOR SILVER AT THE COMEX REMAINS AT 23.810 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ//

NEW TOTALS FOR SILVER OZ STANDING IS AS FOLLOWS

NORMAL STANDING 23.810 MILLION OZ

PLUS OUR 2 EXCHANGE FOR RISK: 185,000 OZ

EQUALS

23.995 MILLION OZ!! HUGE FOR A FEBRUARY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 37.195 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEU JUMP OF 0.000 MILLION OZ AND THEN ADD OUR 2 EXCHANGE FOR RISK FOR .185 MILLION OZ STANDING ADVANCES TO 23.995 MILLION OZ!!

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 7.7138 TONNES TO OTHER OF 23.9535 TONNES/ NEW QUEUE JUMP TOTAL: XXXX TONNES// AND THEN WE ADD OUR THREE EXCHANGE FOR RISK: 6276 CONTRACTS OR 19.5209 TONNES//NEW STANDING ADVANCES TO 144.3979 TONNES

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 144.3979 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING AND OUR THREE ISSUANCES EXCHANGE FOR RISK!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES (WILTONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 92.35 TONNES (WHICH WILL BE ANOTHER STRONG)

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG SIZED 412 CONTRACTS OI TO 134,056 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 170 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 170 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 412 CONTRACTS AND ADD TO THE 170 E.FP. ISSUED

WE OBTAIN A STRONG SIZED GAIN OF 582 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $3.89

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 2.910 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $3.89

2.ASIAN AFFAIRS FEB 11/2025

SHANGHAI CLOSED UP 2.03 PTS OR 0.05%

//Hang Seng CLOSED DOWN 233.84 PTS OR 0.82%

// Nikkei CLOSED UP 80.46 PTS OR 0.14%

//Australia’s all ordinaries CLOSED UP 0.27%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9011

/ OFFSHORE CLOSED UP AT 6.8982 Oil DOWN TO 64.33 dollars per barrel for WTI and BRENT DOWN TO 69.08 Stocks in Europe OPENED MOSTLY ALL GREEN EXCEPT SPAIN

ONSHORE USA/ YUAN TRADING UP TO 6.9011 OFFSHORE YUAN TRADING UP TO 6.8982 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 3678 CONTRACTS UP TO 408,069 OI WITH OUR HUGE GAIN IN PRICE OF $63.65 WITH RESPECT TO WEDNESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD . AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A SMALL NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (697).

WE HAD ZERO T.A.S. LIQUIDATION YESTERDAY. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO LONG TUESDAY AND WEDNESDAY AFTER A BRIEF PERIOD OF GOING NET SHORT

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS FEBRUARY CONTRACT MONTH!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW BACK TO AN EXTREMELY LOW OI OF AROUND 408,000 TO NOW 408,069 AND NOW AMPLE ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE DIFFICULT TO FLEECE. THE ALL TIME LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 5 %

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 4375 CONTRACTS (OR 13.608TONNES) WITH THE HUGE GAIN IN PRICE.

THEN WE WERE NOTIFIED OF ANOTHER MONSTER 3000 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 300,000 OZ OR 9,331 TONNES OF GOLD. ON TUESDAY WE HAD AN IDENTICAL 3000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE ARE THE HIGHEST EVER IN TONNAGE ISSUED. THUS THE TOTAL ISSUANCE FOR FEB NOW TOTALS THREE.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO FEBRUARY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND NOW FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 3 ISSUANCES: 6276 CONTRACTS FOR 627,600 OZ OR 19.5209 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 56+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WAS ADDED TO OUR DAILY TOTALS!! (17.656 TONNES)

FEBRUAY ISSUANCE 3. FOR; 19.5209 TONNES SO FAR!!

DETAILS ON OUR NEW FEBRUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 4375 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH FEBRUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 2325 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY THROUGH TO FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0,000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

11.FEB; 0. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 7.7138 TONNES ADDING TO ALL OTHER QUEUE JUMPS OF 23.9535 TONNNES//NEW TOTAL QUEUE JUMP: 31.6673/ STANDING ADVANCES TO 117.163 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 19.5209 TONNES/NEW STANDING ROCKETS TO 144.3979 TONNES!!

THE FED IS THE OTHER MAJOR SHORT IN GOLD OF AROUND 56+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 56+ TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. BUT IT IS IMPOSSIBLE/ THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!!,(LATEST BIS DATA SHOWS AN INCREASE IN GOLD BORROWING BY THE FRBNY// BUT MAY BE THE BUYER IN JANUARY OF 22.315 TONNES TOTAL IN JANUARY/6 ISSUANCES AS WE NOW HAVE THE BIS DATA FOR GOLD SWAPS FOR DECEMBER 2025 AND HERE WE FIND THAT THE FED ACTUALLY INCREASED THEIR GOLD SWAP LOANS WITH THE BIS TO THE 56 TONNES WHICH I NOW RECORD FOR YOU.!!THEN MUCH TO OUR ANGER WE RECEIVED NOTICE TODAY OF OUR THIRD EXCHANGE FOR RISK OF 9.3312 TONNES//TOTAL EXCHANGE FOR RISK FEB OF 3 ISSUANCES EQUATES TO 19.5209 TONNES OF GOLD WHICH WE ADD TO OUR NORMAL DELIVERY TOTALS.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/FEB.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1340 CONTRACTS.

THAT IS A SMALL SIZED 647 EFP CONTRACT WAS ISSUED: : /APRIL 647 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 647 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 56+ TONNES

WE HAD :

- NO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE SOME GOVERNMENT LIQUIDATION

- HUGE MONTH END SPREADERS LIQUIDATION ENDED FEB 2 AS IT FINALIZED OPERATIONS AS THEY AWAIT THEIR TURN AT THE END OF THIS MONTH OF FEBRUARY.

T.A.S.SPREADER ISSUANCE//FEBRUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A STRONG SIZED 2325 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP WEDNESDAY’S GAIN IN PRICE IN GOLD YET WITH A CORRESPONDING STRONG SIZED GAIN OF COMEX OI AND A SMALL EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- JANUARY’S 6 ISSUANCE FOR 22.215 TONNES

- AND NOW FEB’S THREE ISSUANCES FOR A MONSTER 19.5209 TONNES.

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 56+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAIDS TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OPTIONS EXPIRY MONTH INCLUDING JANUARY’S OTC/LBMA DRIVE BY SHOOTING! ALONG WITH RAIDS IN EARLY FEBRUARY LIKE YESTERDAY, FEB 10.

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 7.7138 TONNES WHICH IS ADDED TO ALL OTHER QUEUE JUMPS OF 23.9535 TO TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB:: 31.6673 TONNES///STANDING ADVANCES TO 124.877 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 19.5209 TONNES/NEW STANDING ROCKETS TO TO 144.3979 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING FEBRUARY,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $63.65)

WE HAD ZERO T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL WEDNESDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR FEBRUARY. THE COMEX IS ONE BIG MESS!!

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 7.7138 TONNES TO WHICH WE ADD TO ALL OTHER QUEUE JUMPS OF 23.9535 / NEW QUEUE JUMP TOTALS: 31.6673 TONNES//STANDING ADVANCES TO: 124.877 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 6276 CONTRACTS FOR 627,600 OZ OR 19.5209 TONNES/NEW STANDING 144.3979 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $63.65

WE HAD A HUGE 1952 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

INITIAL GOLD COMEX

FEB 12

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 6 ENTRIES customer withdrawals: 6 ENTRIES i) Out of Asahi 35,687.484 oz (1110 kilobars) ii) Out of HSBC 51,684.135 oz iii) Out of Int. Delaware 37,122.550 ooz iv) Out of jPMorgan: 22,939.252 oz v) Out of Loomis 80,377.500 oz (2500 kilobars) vi) Out of Malca 59,202.162 (1842 kilobars) total withdrawal: 287m033.073 oz 8.927 tonnes of gold |

| Deposit to the Dealer Inventory in oz | 0 |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entry xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1477 notice(s) 147,700 OZ 4.5940 TONNES TONNES OF GOLD |

| No of oz to be served (notices) | 4762 contracts 476,200 OZ 14.656 TONNES |

| Total monthly oz gold served (contracts) so far this month | 35,436 notices 3,543,600 oz 110.220 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

i

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0

customer withdrawals:

customer withdrawals:

6 ENTRIES

i) Out of Asahi 35,687.484 oz (1110 kilobars)

ii) Out of HSBC 51,684.135 oz

iii) Out of Int. Delaware 37,122.550 ooz

iv) Out of jPMorgan: 22,939.252 oz

v) Out of Loomis 80,377.500 oz (2500 kilobars)

vi) Out of Malca 59,202.162 (1842 kilobars)

total withdrawal: 287m033.073 oz

8.927 tonnes of gold

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 2

ALL DEALER TO CUSTOMER:

adjustments all dealer to customer account;

i) Brinks: 38,388.293 oz

ii) JPMorgan 10,073.72 oz.

total adjusted out of the dealer (reg) to customer (elig) acct: 48,492.073 oz

or 1.508 tonnes

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 6189 CONTRACTS FOR A GAIN OF 2304 CONTRACTS.

WE HAD 176 CONTRACTS SERVED ON WEDNESDAY, SO WE GAINED A MONSTER 2480 CONTRACT–

QUEUE JUMP FOR 248,000 OZ OR 7.7138 TONNES

MARCH SAW A LOSS OF ONLY 95 CONTRACTS DOWN TO 4857 CONTRACT OI AS MARCH BECOMES THE NEW FRONT MONTH FOR GOLD AND EXPECT TO HAVE A STANDING OF AROUND 15 TONNES FO GOLD

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT GAINED 1065 CONTRACTS UP TO 283,282 CONTRACTS

We had 1477 contracts filed for today representing 147,700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1477 contract(s) of which 131 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (35,436) to which we add the difference between the open interest for the front month of FEB ( 6159 CONTRACTS) minus the number of notices served upon today (1477 x 100 oz per contract) equals 4,014,800 OZ OR (124.877 Tonnes of gold) to which we add February’s 3 exchange for risk of 6276 contracts or 627,600 oz or 19.5209 tonnes//new total gold standing in Feb increases to 144.3979 tonnes.

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (35,436 x 100 oz +we add the difference for front month of FEB (6159 OI} minus the number of notices served upon today (1477 x 100 oz) which equals 4,014,800 OR 124.877 TONNES// to which we add our THREE exchange for risk//627,600 oz or 19.5209 tonnes//new standing advances to 144.3979 tonnes!!!

new total of gold standing in FEB is 144.3979 TONNES//

TOTAL COMEX GOLD STANDING FOR FEB 144.3979 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF FEBRUARY.

confirmed volume WEDNESDAY confirmed 125,161 AWFUL/

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,762,006.462 oz 54.805 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 34,448,412.418 oz (draining huge of gold)

TOTAL REGISTERED GOLD 17,588,988.627. or 547.09 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,859.023.791 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 15,726,982 oz ((REG GOLD- PLEDGED GOLD)=

489.175 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SILVER/COMEX

FEB 12 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 5 entries i) out of Asahi: 431,920.430 oz ii) Out of Delaware 129,734.436 oz iii) Out of JPMorgan 1,126,603.750 oz 1v) Out of Loomis: 50,476.750 oz vi) Out of Manfra: 597,061.864 OZ total withdrawal: 2,335,796.880 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 0 ENTRY 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 0 ENTRIES |

| No of oz served today (contracts) | 3 CONTRACT(S) ( 15,000 OZ |

| No of oz to be served (notices) | 167 Contracts (0.835 MILLION oz) |

| Total monthly oz silver served (contracts) | 4595 contracts 22.975 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

withdrawals: customer side/eligible

5 entries

i) out of Asahi: 431,920.430 oz

ii) Out of Delaware 129,734.436 oz

iii) Out of JPMorgan 1,126,603.750 oz

1v) Out of Loomis: 50,476.750 oz

vi) Out of Manfra: 597,061.864 OZ

total withdrawal: 2,335,796.880 oz

5 entries

i) out of Asahi: 431,920.430 oz

ii) Out of Delaware 129,734.436 oz

iii) Out of JPMorgan 1,126,603.750 oz

1v) Out of Loomis: 50,476.750 oz

vi) Out of Manfra: 597,061.864 OZ

total withdrawal: 2,335,796.880 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 5

all dealer to customer:

a) Brinks 1,440234,813 oz

b) CNT 2,368,902.04 oz

c) Out of Delaware: 413,592.568 oz

d) Out of Int. Delaware 346,959.600 oz

e) Out of Manfra: 538,131.519 oz

total adjusted out of dealer (reg) and into customer (elig) 5,107,820.59 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 93.070MILLION OZ//.TOTAL REG + ELIGIBLE. 379.233 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 170 OPEN INTEREST CONTRACTS FOR A LOSS OF 102 CONTRACTS.

WE HAD 102 NOTICES FILED ON WEDNESDAY SO WE NEITHER GAINED NOR LOST ANY CONTRACTS

MARCH LOST ONLY 2456 CONTRACTS DOWN TO 65,490. THIS BECOMES THE FRONT MONTH FOR SILVER DELIVERY AND WE SHOULD HAVE A DANDY OF A MARCH DELIVERY MONTH!!! WE HAVE 11 MORE READING DAYS BEFORE FIRST DAY NOTICE!

APRIL GAINED 53 CONTRACTS TO AN OI 602 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 or 15,000 oz

CONFIRMED volume; ON WEDNESDAY 94,670 huge+++//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 4595 X5,000 oz = 22.975 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (170) AND the number of notices served upon today (3)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (4595)Notices served so far) x 5000 oz + OI for the front month of FEB(170) minus number of notices served upon today (3 )x 5000 oz equals silver standing for the FEB..contract month equating to 23.810 MILLION OZ. THEN WE MUST ADD OUR FIRST EXCHANGE FOR RISK TOTALS OF 25 CONTRACTS FOR .125 MILLION OZ TO FRIDAY’S 12 CONTRACT ISSUANCE//NEW TOTAL EXCHANGE FOR RISK 37 CONTRACTS FOR .185 MILLION OZ//NEW STANDING ADVANCES TO 23.995 MILLION OZ

NEW STANDING: 23.995 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 23.995 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 93.030 million oz of registered silver

JPMorgan as a percentage of total silver: 162.187/379.233.million: 42.74%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

FEB 12/2026/WITH GOLD DOWN $143.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.000 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.32 TONNES

FEB 11/2026/WITH GOLD UP $63.65 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.34 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.32 TONNES

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

FEB 9/2026/WITH GOLD UP $100,00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.23 TONNES

FEB 6/2026/WITH GOLD UP $86.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1077.95 TONNES

FEB 5/2026/WITH GOLD DOWN $57.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.95 TONNES

FEB 4/2026/WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1083.38 TONNES

FEB 3/2026/WITH GOLD UP $270.80 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1087.10 TONNES

FEB 2/2026/WITH GOLD DOWN $100.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.10 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1081.32 TONNES, TONIGHTS TOTAL

SILVER

FEB 12 WITH SILVER DOWN $8.78 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 635,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 522.005 MILLION OZ

FEB 11 WITH SILVER UP $3.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 815,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 521.370 MILLION OZ

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

FEB 9 WITH SILVER UP $5,24 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

FEB 6 WITH SILVER UP 0.08 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 522.367 MILLION OZ

FEB 5 WITH SILVER DOWN $7.87 A HUGE WITHDRAWAL OF 2.175 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 526.309 MILLION OZ

FEB 4 WITH SILVER UP $2.02 A HUGE WITHDRAWAL OF 3.551 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 528.484 MILLION OZ

FEB 3 WITH SILVER UP $6.11 A MASSIVE MASSIVE PAPER AND FRAUUDULENT 32.898 CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 531.985 MILLION OZ

FEB 2 WITH SILVER DOWN $1.32 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 522.005 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Bloomberg: Russia’s memo and the US dollar

Bloomberg reports that an internal memo in the Kremlin lays out plans for Russia to return to the dollar in “a wide-ranging economic partnership with the Trump administration”.

| Alasdair MacleodFeb 12∙Paid |

Either this is made up in an attempt to knock the stuffing out of China’s increasingly obvious plans to replace the dollar for her trade settlements with the yuan, or it is a Russian ploy to drive US interests apart from those of the Europeans. Part of this so-called plan is for Russia and the US to work together to replace global green energy alternatives with fossil fuels.

On the surface, there’s sense in such a proposal and it obviously appeals to the Trump administration. But even if it exists, it is not the whole story. For a start, Russia is unlikely to entertain such a deal without the stolen $300 billion of her central bank reserves being returned to her. That requires the EU to sanction it, and the EU is committed to spending it on Ukraine.

The fact of the matter is that all energy is priced in and exchanged for dollars anyway. This is hardly a concession by Russia. Furthermore, it does not disrupt the partnership with China, and if this memo has any status other than a blue-sky exercise, we can be sure that it would have been discussed between Xi and Putin before leaking it to Bloomberg.

It is all very fishy. How did Bloomberg get it and why? It reminds us of the Steele dossier, trumped up (pardon the pun) by the Democrats to discredit The Donald. It’s not Putin’s style. If he was contemplating such a move, it would be discussed in back channels.

Of course, we can only speculate, but it looks like disinformation. We know that the dollar is under increasing pressure from China, which has just instructed its private-sector institutions to dump US Treasuries. And obvious moves to secure the yuan’s purchasing power by making it exchangeable for gold threaten to swiftly undermine the dollar’s credibility even further.

Since September, dollar-denominated gold and silver derivatives have been encashed for physical metal, a development that is creating enormous strains in capital markets. It does not escape our notice that gold and silver were marked down heavily on this leak.

Is that the true purpose behind Bloomberg reporting the existence and content of a supposedly internal Russian government memo? If so, it indicates a political attempt by the Americans to rescue a deteriorating situation, and/or someone in the derivatives world is in deep trouble.

Nothing is changed. The US is entirely responsible for the fiat dollar’s problems, not Russia or China. The dollar is in respite care ahead of its certain death. And we should all give thanks for the opportunity to stack even more gold, silver, copper, and everything else to get out of worthless paper.

3. CHRIS POWELL AND HIS GATA DISPATCHES:

LIVE FROM THE VAULT YOU TUBE: 258 AND 257

TODAY CRAIG HEMKE

5. COMMODITY REPORT/GOLD TRADING

Gold & Silver ALERT: Load the Boat at this Level, Crisis Escalating – Soloway

![]()

by ITM Trading

Wednesday, Feb 11, 2026 – 16:51

The hidden technical handwriting is on the wall. Gareth Soloway, a pure chart technician, says the S&P’s decade-long parallel channel — intact since the COVID lows — is now grinding into a brick-wall 7100 ceiling. Every tag of resistance tightens the coil. “The market is telling us there is downside ahead.” His roadmap?

A 12–13% air pocket that wipes out six months of complacent gains. Meanwhile, silver has gone from disciplined accumulation to vertical, emotion-driven euphoria. That spike is the tell. “It has to get taken out.” Soloway’s buy zone: $50–$54 — a cold retest of the scene of the crime.

Follow Daniela on X: Daniela Cambone

About ITM Trading: ITM Trading has been a trusted leader in precious metals for over 28 years, helping clients protect and grow their wealth with custom gold and silver strategies designed for economic downturns and currency resets.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

GOLD , SILVER OR PLATINUM LEASE RATES

ROBERT LAMBOURNE….

I have some implied lease rates for you from yesterday evening based on the Comex. Sorry, but I’m having some issues with my computer equipment so this is an image only. They are really high, even for gold historically.

Regards,

Bob

END

silver inventories from the East:

DeepSeek commentary

Inbox

| Robert Lambourne | 6:35 AM (1 hour ago) | ||

| to me, Chris | |||

Harvey,

Here is an update from DeepSeek on silver inventories in various markets. Generally they are falling, but as DeepSeek itself points out in the second section below this is partly explained in China by the shut down over the New Year holiday.

The second part below covers some of the impacts of the upcoming holiday shut down.

Regards,

Bob

—

AND THEN THIS FROM BOB. L

## SILVER INVENTORIES: CONTINUING FALL?

| Venue | Weekly Change | Direction | Notable |

|—————|—————|—————–|————————————————————–|

| SGE | -5.2% | **Falling** | Accelerated drawdown, highest since 2023 |

| SHFE | -3.1% | **Falling** | |

| COMEX | -0.73% (Moz) | **Falling** | Registered critical low |

| LBMA | -0.28% (Moz) | **Falling** | 11th consecutive week |

| MCX (India) | -1.6% | **Falling** | |

| TOCOM | -3.6% | **Falling** | |

| KRX | Flat | Stable | |

**Conclusion**: Silver inventories are declining **in all major physical hubs** except Korea. The pace has accelerated in Shanghai and London, while COMEX registered inventories now approach levels that typically trigger delivery squeezes.

—

## CHINESE NEW YEAR HOLIDAY EFFECT (holiday starts 16 Feb): Gold premium Shanghai over London: 28 dollars//lease rates a touch higher by 35 basis pts: to 5.35%

– **Price Impact**: SGE benchmark gold premium over London averaged **$28/oz** this week, the widest in four months. Silver premium reached $0.75/oz.

– **Volume Impact**: SGE daily turnover fell 22% w/w; SHFE open interest in silver dropped 15% as speculators squared positions.

– **Leasing Impact**: SGE gold lease rates spiked 35 bps as banks reduced lending ahead of the closure.

– **Restrictions**: SHFE and SGE will be fully closed 16–22 Feb. All physical deliveries scheduled for this period have been advanced to this week, contributing to the inventory drop.

No other major Asian market holidays coincide; however, Indian and Japanese participants have trimmed exposure to China‑linked arbitrage flows.

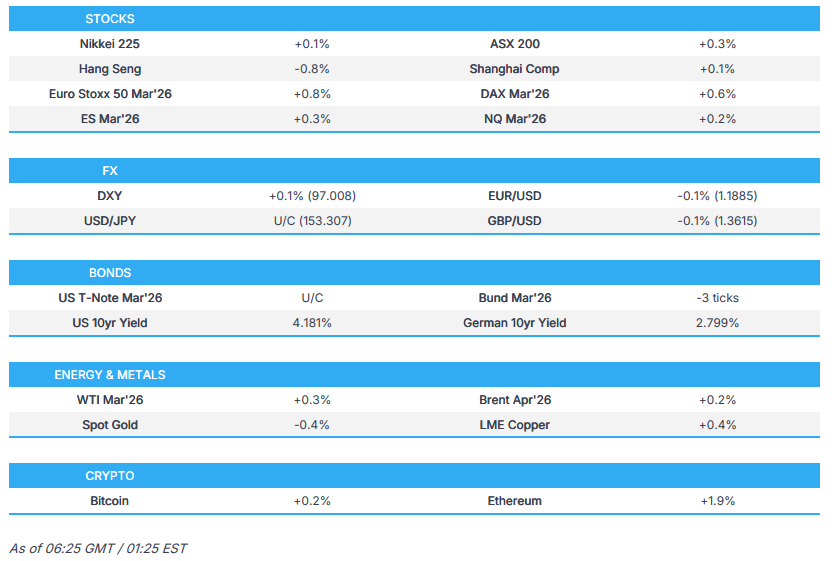

2.ASIAN AFFAIRS FEB 12/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 2.03 PTS OR 0.05%

//Hang Seng CLOSED DOWN 233.84 PTS OR 0.82%

// Nikkei CLOSED UP 80.46 PTS OR 0.14%

//Australia’s all ordinaries CLOSED UP 0.27%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9011

/ OFFSHORE CLOSED UP AT 6.8982 Oil DOWN TO 64.33 dollars per barrel for WTI and BRENT DOWN TO 69.08 Stocks in Europe OPENED MOSTLY ALL GREEN EXCEPT SPAIN

ONSHORE USA/ YUAN TRADING UP TO 6.9011 OFFSHORE YUAN TRADING UP TO 6.8982 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.9011

OFFSHORE YUAN: UP TO 6.8982

HANG SENG CLOSED DOWN 233.84 PTS OR 0.82%

2. Nikkei closed UP 80.46 PTS OR 0.14%

WEST TEXAS INTERMEDIATE OIL DOWN 64.33

BRENT; 69.08

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX UP TO 96.76 /// EURO RISES TO 1.1875 UP 8 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +2.234/ DOWN 1/4 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 153.06… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.430 DOWN 7 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7957 Italian 10 Yr bond yield DOWN to 3.399 SPAIN 10 YR BOND YIELD DOWN TO 3.162

3i Greek 10 year bond yield DOWN TO 3.401

3j Gold at $5059.60 Silver at: 83,26 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 10/100 roubles/dollar; ROUBLE AT 77.19

3m oil (WTI) into the 64 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 153.21 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.234% UP 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.430 DOWN 7 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7683 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9124 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.168 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.798 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.508 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.65 UP 1 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.4770 DOWN 1 PTS

30 YR UK BOND YIELD: 5.275 DOWN 4 BASIS PTS

10 YR CANADA BOND YIELD: 3.338 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.867 DOWN 3 BASIS PTS.

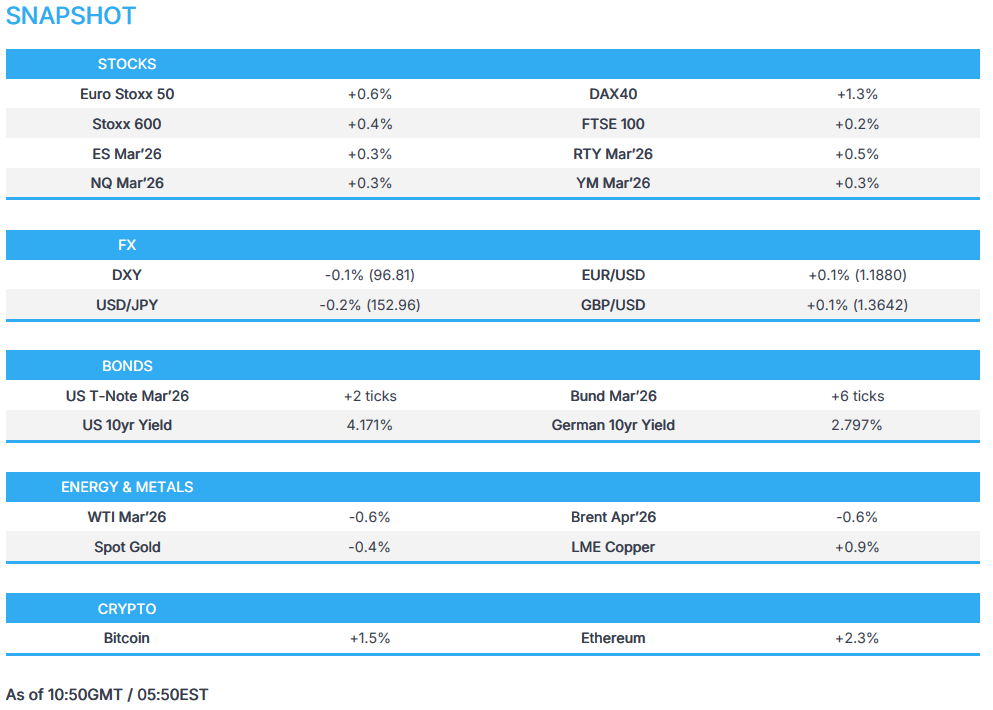

1a New York Opening report

US Futures Rise As European, Asian All Time Highs Spill Over

Thursday, Feb 12, 2026 – 08:29 AM

Futures are higher but there continues to be tangible angst below the surface as traders are aggressively shorting potential AI losers, while US stocks continue to fall behind the rest of the world. “It’s a paradox in that markets are holding, breaking records, yet investors remain cautious,” says Vontobel’s head of equities Jean-Louis Nakamura. As of 8:00am ET, S&P and Nasdaq futures are up 0.3%, with premarket strength in Mag7, Semis and Cyclicals while Energy and Materials underperform. It’s unclear right now which stocks will be hurt by AI, but it’s clear that traders are nervous. “The slightest miss on earnings is brutally penalized and substantial beats are required to boost share prices,” said Nakamura. Bond yield stabilize, flat to down 1bp across the curve with USD also flat. Commodities are mostly lower with Energy and Metals weaker (WTI, Precious down less than 1%) and Ags higher. Today’s macro data focus is on jobless claims and existing home sales. With the stabilization in the bond market and net positive WTD macro data, we may investors push the market higher into tmrw’s CPI where only a materially hawkish print is likely to shift the market narrative.

In premarket trading, Mag 7 stocks are mostly higher (Alphabet +0.5%, Amazon +0.3%, Apple -0.2%, Nvidia +1.2%, Meta Platforms +0.4%, Microsoft +0.4%, Tesla +0.5%),

- Coal stocks are up after the Trump administration ordered the Pentagon to purchase electricity from coal plants and announced funding for upgrades to coal facilities.

- Baxter International (BAX) falls 14% after the medtech company posted fourth quarter results.

- Cisco Systems Inc. (CSCO) drops 7% after the company gave a weaker-than-expected forecast for profitability in the current quarter, spurring concerns that mounting memory-chip prices are taking a toll on the company.

- Cognex (CGNX) is up 23% after the electronics components company forecast revenue for the first quarter that beat the average analyst estimate.

- Equinix (EQIX) rises 9% after the data center operator’s 2026 revenue guidance beat the average analyst estimate. Analysts are positive about the increased bookings and highlight a boost to the company’s forecast from accelerated AI demand.

- Fastly (FSLY) soars 40% after the cloud-platform provider posted fourth-quarter results that beat expectations and management gave a robust full-year forecast.

- ICON (ICLR) sinks 33% after the company said the audit committee launched an internal investigation into its accounting practices.

- Paycom Software (PAYC) falls 9% after the company’s outlook was seen as disappointing and pointing to tepid growth trends.

- Trip.com ADRs (TCOM) fall 5% after China Central Television reported that the city of Beijing had summoned the internet firm along with 11 others over issues related to train ticket sales.

- Viking Therapeutics (VKTX) rises 13% after the biotech said it plans to advance its oral obesity drug to Phase 3 in the third quarter of this year.

- Zoetis (ZTS) climbs 4% after the animal health company gave a forecast for adjusted earnings per share for 2026 that topped Wall Street’s expectations

With US stocks lagging gains in Asia and Latin America this year, the moves underscore how sensitive the market has become to companies’ exposure to the infrastructure behind the AI boom. Memory-chip shortages and pricing are coming up frequently as topics in company earnings reports and conference calls.

“This is a year of the bullish stock market, but a very volatile stock market — and the volatility will be induced by the AI trade, which is evolving,” said Beata Manthey, head of European Equity Strategy at Citigroup Inc. “Right now we are concentrating on losers. But we also need to discover who the new winners are going to be.”

The AI winners and losers trade is playing out across the world, helping Asian markets — with a heavy concentration of AI hardware firms — extend their lead over the US. That’s left the S&P 500 ranking 69th among the 92 stock indexes tracked by Bloomberg, according to Markets Live. Among sectors, jitters over software have given the ‘old economy’ stocks in the Dow Jones Transportation Average a new lease of life.

And in single stocks, the huge memory-chip needs of AI are rippling out. Japanese chipmaker Kioxia surged after its guidance beat estimates, while Cisco shares are lower in premarket trading after saying that mounting memory chip prices are hurting its margins. Elsewhere in the AI space, Anthropic is said to be nearing the completion of a deal to raise more than $20 billion in a funding round with a plethora of big investors. And Softbank announced a near-$20 billion investment gain on OpenAI.

Since Jan. 9, there has been a larger swing for the average S&P 500 stock compared to 99% of the time over the past three decades. The 10.8% move, averaged on an absolute basis in that time, has created a windfall for investors with long dispersion positions, according to data from Nomura. US stocks appear less vulnerable than in recent weeks after hedge funds reduced positioning in January, according to JPMorgan strategists.

Traders are also keeping a close eye on key US economic data. Jobs numbers on Wednesday came in surprisingly strong, and attention now turns to Friday’s inflation report for clues on future policy moves by the Federal Reserve.

In politics, Trump’s tariff policies suffered their strongest political blow yet with the Republican-led US House passing legislation aimed at ending the president’s levies on Canadian imports. The US and Japan are closing in on the first three projects to be funded by Tokyo’s $550 billion investment vehicle, as part of their bilateral trade deal.

Out of the 346 S&P 500 companies that have reported so far in the earnings season, 77% have managed to beat analyst forecasts, while 19% have missed. CBRE, Exelon and Iron Mountain are among companies due to report results before the market open. CBRE earnings come in the face of a real estate services ‘AI scare trade’ which hit the sector on Wednesday. Earnings from Applied Materials, Coinbase and Airbnb follow later.

Europe’s Stoxx 600 rises 0.5% to 624.50, hitting a new record high on Thursday amid a flurry of positive earnings, including from EssilorLuxottica SA and Siemens AG. Financial services outperform, as Nuveen’s deal to buy Schroders Plc sends the UK asset manager soaring. Here are some of the biggest movers on Thursday:

- Schroders shares jump as much as 31%, the most since 2008, after the firm agreed to be bought by US asset manager Nuveen for £9.9 billion ($13.5 billion), a 34% premium to Wednesday’s closing price.

- EssilorLuxottica shares jump as much as 10%, the most since October, after the eyewear maker reported better-than-expected sales for the fourth quarter, riding a boom in demand for AI-powered glasses.

- Siemens gains as much as 6.2%, hitting a record high, after delivering order beats in both Digital Industries and Smart Infrastructure in the first quarter, and boosting its EPS guidance for the full year.

- Autostore shares surge as much as 17%, the most since mid-August, after the Norwegian warehouse automation firm delivered a strong revenue beat in the fourth quarter.

- Hermès gains as much as 3.1% as the French maker of the Birkin bag reported fourth-quarter sales and full-year profits that beat estimates.

- Michelin shares rise as much as 6.2% to the highest since May, after the French tiremaker’s plan to buy back as much as €2 billion worth of shares positively surprised analysts, who also noted improvement in earnings momentum.

- Adyen shares slump as much as 20% after the payments firm gave a revenue growth target that missed estimates, citing “continued macroeconomic uncertainty” weighing on market volume growth.

- Magnum shares fall as much as 16% in Amsterdam after full-year results that Jefferies analysts said will fuel concern over the impact of weight-loss drugs on demand.

- Verisure shares drop as much as 11% to a new record low, after the security services firm missed fourth-quarter adjusted Ebitda estimates, despite strong growth in new installations.

- RELX shares give up early gains as analysts at Morgan Stanley said one set of robust numbers will not settle the broader debate on how artificial intelligence may impact the software and information services sector.

- Sanofi shares drop as much as 5.1%, the most since Dec. 15, after the French drugmaker changed its chief executive following big bets on research spending which didn’t produce quick results, in a move that Jefferies analysts said “will be debated.”

- Mercedes shares fall as much as 5.7% after the German carmaker said margins would remain under pressure in 2026 due to US tariffs and China competition.

Earlier in the session, Asian stocks climbed, poised for a fifth day of gains, on continued investor optimism over benefits for the region’s technology hardware suppliers from the artificial intelligence boom. The MSCI Asia Pacific Index rose as much as 0.9%, on track for its best week since September 2024. South Korea’s Kospi jumped 3.1% to extend its lead as the world’s best-performing market this year, driven by gains in memory makers Samsung Electronics and SK Hynix.