GOLD CLOSED CLOSED UP $94.30 TO $5022.45

ACCESS MARKET

GOLD $5027.60 3:30 PM)

SILVER: 76.78 3;30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,923.700000000 USD

INTENT DATE: 02/12/2026 DELIVERY DATE: 02/17/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 265

118 H MACQUARIE FUTURES US 30

132 C SG AMERICAS 4

190 H BMO CAPITAL MARKETS 192

323 C HSBC 2

363 H WELLS FARGO SECURITI 23

365 C MAREX CAPITAL MARKET 1

555 C BNP PARIBAS SEC CORP 63

555 H BNP PARIBAS SEC CORP 6

657 C MORGAN STANLEY 2

661 C JP MORGAN SECURITIES 145 35

880 H CITIGROUP 57

905 C ADM 3

TOTAL: 414 414

MONTH TO DATE: 35,850

JPMORGAN STOPPED 35/414

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 414 CONTRACTs NOTICES FOR 41,400 OZ or 1.2877 TONNES

total notices so far: 35,850 contracts for 3,585,000 OR 111.508 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ /

total number of notices filed so far this month : 4,595 CONTRACTS (NOTICES) for 22.975 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S 0.255 MILLION OZ QUEUE JUMP//NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 24.065 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ//

NEW TOTALS FOR SILVER OZ STANDING IS AS FOLLOWS

NORMAL STANDING 24.065 MILLION OZ

PLUS OUR 2 EXCHANGE FOR RISK: 185,000 OZ

EQUALS

24.250 MILLION OZ!! HUGE FOR A FEBRUARY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 38.845 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEU JUMP OF 0.255 MILLION OZ AND THEN ADD OUR 2 EXCHANGE FOR RISK FOR .185 MILLION OZ STANDING ADVANCES TO 24.250 MILLION OZ!!

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.8055 TONNES TO OTHER OF 39.3811 TONNES/ NEW QUEUE JUMP TOTAL: 40.1866 TONNES// AND THEN WE ADD OUR THREE EXCHANGE FOR RISK: 6276 CONTRACTS OR 19.5209 TONNES//NEW STANDING ADVANCES TO 145.2029 TONNES

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 145.2029 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING AND OUR THREE ISSUANCES EXCHANGE FOR RISK!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES (WILTONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 99.754 TONNES (WHICH WILL BE ANOTHER STRONG)

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 1599 CONTRACTS OI TO 132,454 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 330 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 330 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1599 CONTRACTS AND ADD TO THE 330 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF 1269 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $8.78

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 6.345 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $8.78

2.ASIAN AFFAIRS FEB 11/2025

SHANGHAI CLOSED DOWN 51.95 PTS OR 1.26%

//Hang Seng CLOSED DOWN 465.42 PTS OR 1.72%

// Nikkei CLOSED DOWN 712.84 PTS OR 1.24%

//Australia’s all ordinaries CLOSED DOWN 0.73%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9113

/ OFFSHORE CLOSED DOWN AT 6.9095 Oil DOWN TO 62.62 dollars per barrel for WTI and BRENT DOWN TO 67.55 Stocks in Europe OPENED MOSTLY ALL RED EXCEPT SPAIN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9113 OFFSHORE YUAN TRADING DOWN TO 6.9025 ONSHORE YUAN TRADING BELOW OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1661 CONTRACTS UP TO 406,408 OI DESPITE OUR HUGE LOSS IN PRICE OF $143.65 WITH RESPECT TO THURSDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST SOME NET LONGS, WITH THAT PRICE LOSS FOR GOLD . AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2380).

WE HAD SOME T.A.S. LIQUIDATION YESTERDAY. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO LONG THIS WEEK AFTER A BRIEF PERIOD OF GOING NET SHORT. HOWEVER THE LONG SPECULATORS WERE ANNHILATED AGAIN ON A MASSIVE RAID ORCHESTRATED BY THE CROOKS AFTER 11 AM ONCE LONDON WAS PUT TO BED.

CENTRAL BANKS TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS FEBRUARY CONTRACT MONTH!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW BACK TO AN EXTREMELY LOW OI OF AROUND 411,000 TO NOW 411,794 AND NOW AMPLE ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE DIFFICULT TO FLEECE. THE ALL TIME LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 5 %

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 719 CONTRACTS (OR 2.23TONNES) DESPITE THE HUGE LOSS IN PRICE.

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. THIS PAST WE WE HAVE HAD TWO IDENTICAL MONSTER 3000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE ARE THE HIGHEST EVER IN TONNAGE ISSUED. THUS THE TOTAL ISSUANCE THUS FAR FOR FEB NOW TOTALS THREE.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO FEBRUARY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND NOW FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 3 ISSUANCES: 6276 CONTRACTS FOR 627,600 OZ OR 19.5209 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 56+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WAS ADDED TO OUR DAILY TOTALS!! (17.656 TONNES)

FEBRUAY ISSUANCE 3. FOR; 19.5209 TONNES SO FAR!!

DETAILS ON OUR NEW FEBRUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A SMALL SIZED GAIN ON OUR TWO EXCHANGES OF 719 CONTRACTS DESPITE OUR STRONG LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH FEBRUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A HUGE SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 3965 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY THROUGH TO FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0,000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

11.FEB; 0. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.8055 TONNES ADDING TO ALL OTHER QUEUE JUMPS OF 39.3811 TONNNES//NEW TOTAL QUEUE JUMP: 40.1866/ STANDING ADVANCES TO 125.682 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 19.5209 TONNES/NEW STANDING ROCKETS TO 145.2029 TONNES!!

THE FED IS THE OTHER MAJOR SHORT IN GOLD OF AROUND 56+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 56+ TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. BUT IT IS IMPOSSIBLE/ THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!!,(LATEST BIS DATA SHOWS AN INCREASE IN GOLD BORROWING BY THE FRBNY// BUT MAY BE THE BUYER IN JANUARY OF 22.315 TONNES TOTAL IN JANUARY/6 ISSUANCES AS WE NOW HAVE THE BIS DATA FOR GOLD SWAPS FOR DECEMBER 2025 AND HERE WE FIND THAT THE FED ACTUALLY INCREASED THEIR GOLD SWAP LOANS WITH THE BIS TO THE 56 TONNES WHICH I NOW RECORD FOR YOU.!!THEN MUCH TO OUR ANGER WE RECEIVED NOTICE TODAY OF OUR THIRD EXCHANGE FOR RISK OF 9.3312 TONNES//TOTAL EXCHANGE FOR RISK FEB OF 3 ISSUANCES EQUATES TO 19.5209 TONNES OF GOLD WHICH WE ADD TO OUR NORMAL DELIVERY TOTALS.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/FEB.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1340 CONTRACTS.

THAT IS A STRONG SIZED 2380 EFP CONTRACT WAS ISSUED: : /APRIL 2380 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2380 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 56+ TONNES

WE HAD :

- NO LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE SOME GOVERNMENT LIQUIDATION

- HUGE MONTH END SPREADERS LIQUIDATION ENDED FEB 2 AS IT FINALIZED OPERATIONS AS THEY AWAIT THEIR TURN AT THE END OF THIS MONTH OF FEBRUARY.

T.A.S.SPREADER ISSUANCE//FEBRUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A HUGE SIZED 3965 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP THURSDAY’S LOSS IN PRICE IN GOLD YET WITH A CORRESPONDING STRONG SIZED GAIN OF COMEX OI AND A SMALL EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- JANUARY’S 6 ISSUANCE FOR 22.215 TONNES

- AND NOW FEB’S THREE ISSUANCES FOR A MONSTER 19.5209 TONNES.

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 56+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAIDS TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OPTIONS EXPIRY MONTH INCLUDING JANUARY’S OTC/LBMA DRIVE BY SHOOTING! ALONG WITH RAIDS IN EARLY FEBRUARY LIKE YESTERDAY, FEB 10.

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.8055 TONNES WHICH IS ADDED TO ALL OTHER QUEUE JUMPS OF 39,3811 TO TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB:: 40.1866 TONNES///STANDING ADVANCES TO 125.682 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 19.5209 TONNES/NEW STANDING ROCKETS TO TO 145.2029 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING FEBRUARY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $143.65 )

WE HAD ZERO T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// WITH OUR LOSS IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL THURSDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR FEBRUARY. THE COMEX IS ONE BIG MESS!!

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.8055 TONNES TO WHICH WE ADD TO ALL OTHER QUEUE JUMPS OF 39.3811 / NEW QUEUE JUMP TOTALS: 40.1866 TONNES//STANDING ADVANCES TO: 125.682 TONNES TO WHICH WE ADD OUR THREE EXCHANGE FOR RISK OF 6276 CONTRACTS FOR 627,600 OZ OR 19.5209 TONNES/NEW STANDING 145.2029 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $143.65

WE HAD A HUGE 5386 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

INITIAL GOLD COMEX

FEB 13

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 6 ENTRIES customer withdrawals: 1 ENTRIES i) Out of Brinks: 32,151.000 ooz (1000 kilobars) total withdrawal 32,151.000 oz |

| Deposit to the Dealer Inventory in oz | 0 |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entry xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 414 notice(s) 41400 OZ 1.2877 TONNES TONNES OF GOLD |

| No of oz to be served (notices) | 4557 contracts 455,700 OZ 14.174 TONNES |

| Total monthly oz gold served (contracts) so far this month | 35,850 notices 3,585,000 oz 111.508 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0

customer withdrawals:

customer withdrawals:

1 ENTRIES

i) Out of Brinks: 32,151.000 ooz

(1000 kilobars)

total withdrawal 32,151.000 oz

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 4

ALL DEALER TO CUSTOMER:

adjustments all dealer to customer account;

i) Brinks: 8605.439 oz

ii) JPMorgan 964.530

iii) Loomis 868.077 oz

iv) Manfra: 2025.513 oz

total adjusted out of the dealer (reg) to customer (elig) acct: 12,463.559 oz

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 4971 CONTRACTS FOR A LOSS OF 1218 CONTRACTS.

WE HAD 1477 CONTRACTS SERVED ON THURSDAY, SO WE GAINED A STRONG 259 CONTRACT–

QUEUE JUMP FOR 25,900 OZ OR 0.8055 TONNES

MARCH SAW A GAIN OF 134 CONTRACTS UP TO 4991 CONTRACT OI AS MARCH BECOMES THE NEW FRONT MONTH FOR GOLD AND EXPECT TO HAVE A STANDING OF AROUND 15 TONNES FO GOLD

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 3504 CONTRACTS DOWN TO 279,778 CONTRACTS

We had 414 contracts filed for today representing 41,400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 145 notices issued from their client or customer account. The total of all issuance by all participants equate to 414 contract(s) of which 35 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (35,850) to which we add the difference between the open interest for the front month of FEB ( 4971 CONTRACTS) minus the number of notices served upon today (414 x 100 oz per contract) equals 4,040,700 OZ OR (125.682 Tonnes of gold) to which we add February’s 3 exchange for risk of 6276 contracts or 627,600 oz or 19.5209 tonnes//new total gold standing in Feb increases to 145.2029 tonnes.

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (35,850 x 100 oz +we add the difference for front month of FEB (4971 OI} minus the number of notices served upon today (414 x 100 oz) which equals 4,040,700 OR 125.682 TONNES// to which we add our THREE exchange for risk//627,600 oz or 19.5209 tonnes//new standing rockets to 145.2029 tonnes!!!

new total of gold standing in FEB is 145.2029 TONNES//

TOTAL COMEX GOLD STANDING FOR FEB 145.2029 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF FEBRUARY.

confirmed volume THURSDAY confirmed 188,691 poor/

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,762,006.462 oz 54.805 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 34,448,415,861.418 oz (draining huge of gold)

TOTAL REGISTERED GOLD 17,576,525.068. or 546.703 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,837,336.350 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 15,814.519 oz ((REG GOLD- PLEDGED GOLD)=

401.89 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SILVER/COMEX

FEB 13 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) Out of CNT 363,108.525 ii) Out of Delaware: 11,667.394 oz iii) Out of JPMorgan; 2,441,186.700 oz total withdrawal: 2,805,962.619 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 0 ENTRY 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 0 ENTRIES |

| No of oz served today (contracts) | 0 CONTRACT(S) ( NIL OZ |

| No of oz to be served (notices) | 218 Contracts (1.090 MILLION oz) |

| Total monthly oz silver served (contracts) | 4595 contracts 22.975 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

withdrawals: customer side/eligible

3 entries

i) Out of CNT 363,108.525

ii) Out of Delaware: 11,667.394 oz

iii) Out of JPMorgan; 2,441,186.700 oz

total withdrawal: 2,805,962.619 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 1

all dealer to customer:

a) Manfra 130,217.900 oz

total adjusted out of dealer (reg) and into customer (elig) 130,217.900 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 92.899MILLION OZ//.TOTAL REG + ELIGIBLE. 376.874 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 218 OPEN INTEREST CONTRACTS FOR A GAIN OF 48 CONTRACTS.

WE HAD 3 NOTICES FILED ON THURSDAY SO WE GAINED 51 CONTRACTS OR WE HAD A STRONG QUEUE JUMP

OF 255,000 OZ.

MARCH LOST 6,091 CONTRACTS DOWN TO 59,399. THIS BECOMES THE FRONT MONTH FOR SILVER DELIVERY AND WE SHOULD HAVE A DANDY OF A MARCH DELIVERY MONTH!!! WE HAVE 9 MORE READING DAYS BEFORE FIRST DAY NOTICE!

APRIL GAINED 6 CONTRACTS TO AN OI 608 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 or NIL oz

CONFIRMED volume; ON THURSDAY 129,292 huge+++//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 4595 X5,000 oz = 22.975 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (218) AND the number of notices served upon today (0)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (4595)Notices served so far) x 5000 oz + OI for the front month of FEB(218) minus number of notices served upon today (0 )x 5000 oz equals silver standing for the FEB..contract month equating to 24.065 MILLION OZ. THEN WE MUST ADD OUR FIRST EXCHANGE FOR RISK TOTALS OF 25 CONTRACTS FOR .125 MILLION OZ TO FRIDAY’S 12 CONTRACT ISSUANCE//NEW TOTAL EXCHANGE FOR RISK 37 CONTRACTS FOR .185 MILLION OZ//NEW STANDING ADVANCES TO 24.250 MILLION OZ

NEW STANDING: 24.250 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 24.250 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 92.899 million oz of registered silver

JPMorgan as a percentage of total silver: 159.446/376.474.million: 42.28%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

FEB 13/2026/WITH GOLD UP $94.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.140 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.18 TONNES

FEB 12/2026/WITH GOLD DOWN $143.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.000 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.32 TONNES

FEB 11/2026/WITH GOLD UP $63.65 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.34 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.32 TONNES

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

FEB 9/2026/WITH GOLD UP $100,00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.23 TONNES

FEB 6/2026/WITH GOLD UP $86.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1077.95 TONNES

FEB 5/2026/WITH GOLD DOWN $57.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.95 TONNES

FEB 4/2026/WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1083.38 TONNES

FEB 3/2026/WITH GOLD UP $270.80 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1087.10 TONNES

FEB 2/2026/WITH GOLD DOWN $100.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.10 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1076.18 TONNES, TONIGHTS TOTAL

SILVER

FEB 13 WITH SILVER UP $2.35 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.994 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 520.011 MILLION OZ

FEB 12 WITH SILVER DOWN $8.78 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 635,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 522.005 MILLION OZ

FEB 11 WITH SILVER UP $3.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 815,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 521.370 MILLION OZ

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

FEB 9 WITH SILVER UP $5,24 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

FEB 6 WITH SILVER UP 0.08 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 522.367 MILLION OZ

FEB 5 WITH SILVER DOWN $7.87 A HUGE WITHDRAWAL OF 2.175 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 526.309 MILLION OZ

FEB 4 WITH SILVER UP $2.02 A HUGE WITHDRAWAL OF 3.551 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 528.484 MILLION OZ

FEB 3 WITH SILVER UP $6.11 A MASSIVE MASSIVE PAPER AND FRAUUDULENT 32.898 CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 531.985 MILLION OZ

FEB 2 WITH SILVER DOWN $1.32 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 520.011 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Silver slammed in thin trade

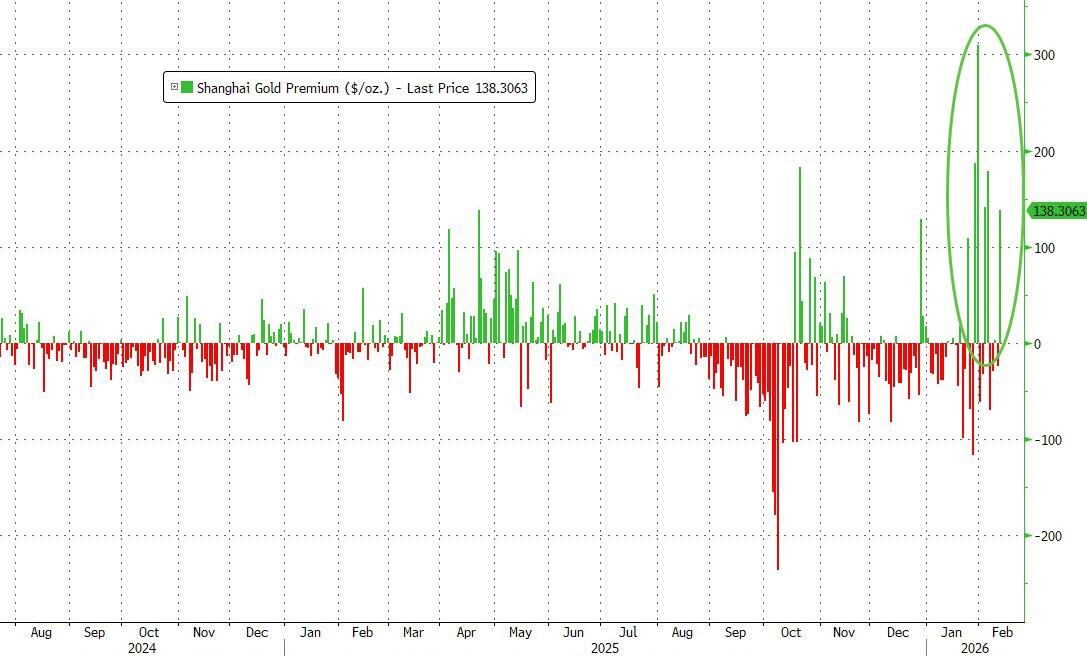

Evidence is mounting that the silver shorts on Comex and London are desperate to close their positions. Will they use the Chinese New Year holiday to this end?

| Alasdair MacleodFeb 13∙Paid |

In this report, we focus on silver, illustrating how silver derivatives on Comex and London are becoming irrelevant. This is because price discovery has moved to Shanghai, whose premiums are leading to physical metal being drained out of Comex and London vaults. But next week, with Shanghai closed for business, expect even greater price distortions in the days ahead. Indeed, Shanghai is closed as of now.

Following a solid recovery from recent unprecedented falls in gold and silver prices, yesterday they were hit again, with silver down over 10% at one stage. Prices opened a little higher this morning. In European morning trade, gold was $4950, down $20 from last Friday’s close. And silver at $77.00 was down 85 cents on balance.

Trade volumes on Comex were very low, even below those in holiday seasons, illustrated in the snapshot below:

Ahead of yesterday’s price smash, on Tuesday silver’s volume fell to 78,296 contracts, less than half that of 31 December and one third less than on 2 January.

Speculative interest is extremely low, shown in the next silver chart, but a similar pattern can be seen in gold:

Additionally, Comex futures stand at a substantial discount to Shanghai. The next illustration shows last night’s Shanghai close:

While gold is trading in line with Comex on the Shanghai Futures Exchange, at $89.17 the silver contract was at a premium of over 13% to Comex at SHFE’s close.

Putting all this evidence together, it is clear that not only is the market being set in Shanghai and not Comex nor by implication London, but the price of silver on Comex is false. It is the price of disconnected paper bearing diminishing relavence to physical metal. But so long as this distortion continues, there will be attempts to acquire physical silver and gold by buying futures and forwards at discounted prices with a view to taking delivery.

We can see the consequences in the decline in stocks in today’s Comex silver vault statistics:

5,107,820 ounces have been moved from registered as available for delivery to Eligible, which is not available for delivery. It is a noticeable trend recently. Furthermore, 2,335,797 ounces have been withdrawn from Comex vaults altogether, reducing stocks at pace This is also a continuing drain as we can see in the next chart:

Comex vaults have lost 30% of total silver stocks from early-October when London had a delivery panic driving lease rates to nearly 40%. Physical liquidity can only be restored if Comex futures trade above Shanghai prices. Until then, they will continue to be drained.

On Comex, the theoretical total available for delivery today is the equivalent of only 18,606 contracts. Meanwhile, open interest in the March future is 59,418 contracts, whose first position (when longs are allocated deliveries for which they must have the funds up front) is 26 February, a week on Thursday.

Obviously, we should expect March’s open interest to reduce ahead of that event to less than the silver available. But it is an event to be watched, following which silver available for delivery could be a serious problem.

While all this looks immensely bullish, Shanghai will be closed next week for the Chinese New Year holidays. As the true pricing centre for silver and ahead of 26 February’s first position, bullion bank traders seeking to close their Comex shorts might work together to drive paper prices lower. It might be their last chance to do so.

This is not something which we can forecast, but it is as well to be wary. While dealers in derivatives will do anything to reduce their silver losses, their risk is that vault stocks will deplete even more rapidly. It is a good example of a situation which stackers should ignore while traders get whipsawed. We appear to be seeing silver derivatives in the West becoming less and less relevant.

ZEROHEDGE…

China’s Central Bank Keeps Buying Gold… And Dumping US Debt

by Tyler Durden

Thursday, Feb 12, 2026 – 05:40 PM

Authored by Andrew Moran via The Epoch Times,

China’s ferocious appetite for gold is influencing the global metals market, and that demand is what will keep driving up metal prices, according to Michael Howell, founder of CrossBorder Capital.

The People’s Bank of China’s gold holdings totaled 74.19 million fine troy ounces by the end of January, up from 74.15 million in the previous month, according to recent central bank data.

Beijing’s value of gold reserves also surged to $369.58 billion, from $319.45 billion in December 2025.

Gold accounts for almost 9 percent of China’s total reserves, the World Gold Council estimates.

The metals market has been on a roller coaster ride over the past few months.

Gold prices are currently trading at about $5,000 per ounce—up by 17 percent this year—on the COMEX division of the New York Mercantile Exchange.

Silver, the sister commodity to gold, is hovering at about $80 per ounce. The white metal has fallen sharply since reaching an all-time high of $121.

The commodities boom will continue, with a focus on oil and gold, Howell said in a recent interview with Siyamak Khorrami, host of EpochTV’s “California Insider.”

Global financial markets are experiencing a commodities boom, particularly in industrials, which coincides with the buildout of artificial intelligence infrastructure. At the same time, Howell said, energy is also witnessing a dramatic increase.

“Stronger economic activity worldwide will elevate oil prices from their current subdued levels,” he said. “Gold has had a tremendous rally over the last 18 months. It’s defied most predictions, but it continues to go up.”

China is playing an outsized role in its meteoric ascent.

Although retail traders are fueling sizable inflows into gold investments, China has been on a gold-buying spree for years as part of the country’s de-dollarization efforts.

For more than a decade, Beijing has been diversifying its foreign exchange reserves to reduce its exposure to the U.S. dollar and American assets, particularly Treasury securities.

In October, China’s holdings of U.S. debt fell to $688.7 billion, down by nearly 10 percent from the previous year, according to Treasury Department data.

Reports have surfaced that Chinese regulators have advised banks to trim their holdings of U.S. government bonds because of market volatility. Whether this shows up in the data over the coming months could further cement China’s long-term plans to ditch the dollar and remain in gold.

Influential Force in Gold Markets

As China remains one of the world’s largest buyers, it will also maintain an immense influence in global gold markets, according to Howell.

“The reason gold is going up is because of what’s happening in China,” he said.

It is no secret that China has largely shaped the global metals market through physical demand, whether through industrial consumption or retail use.

But recent activity on the Shanghai Futures Exchange indicates that Beijing is also influencing prices, said Ewa Manthey, commodities strategist at ING.

“Rising turnover and open interest signal a greater role for speculative positioning in driving momentum, and notably, key price breaks in gold and silver have increasingly occurred during Asian hours, with Europe and the US following rather than leading,” Manthey said in a Feb. 6 research note.

Domestic investors are increasingly turning to commodity futures to express macro views and hedge risks, as property markets are weak, equities are uneven, and capital outflows face tighter controls, according to Manthey.

In this environment of economic and geopolitical uncertainty, metals—across the base and precious spectrum—have become a more prominent alternative investment channel.

Gold trading at a premium in China sends various signals to global markets, mainly the sign that domestic stockpiling is underway. This, Manthey said, sends the message that supplies are tightening and worldwide availability could be tightening.

Although fundamentals trump short-term speculative forces in precious metals, influential noise can trigger greater volatility and abrupt, sharper price corrections.

The Great Debasement

One long-term factor supporting the bullish case for gold is money printing.

Over the years, China has frequently engaged in monetary debasement through aggressive stimulus programs.

Howell estimates that officials have injected more than $1 trillion in liquidity into the financial system to prop up the world’s second-largest economy amid diminished household demand, trade strife, and slowing factory activity. At the same time, China is grappling with enormous debt.

“China’s probably got the biggest problem of the lot, because it’s still sitting on that huge real estate debt which has been saddling the economy,” Howell said.

Although Evergrande and Country Garden have not captured international attention lately, the fallout of China’s real estate bubble burst persists, featuring a mountain of red ink.

Today, China’s general government debt accounts for more than 100 percent of gross domestic product, reflecting the years-long dependence on credit-fueled growth.

The only solution for the authorities to prevent a debt-fueled crisis is to print money, according to Howell. Although defaults are one strategy, they would inevitably destroy the credit system.

“So what happens is central banks come in, and they print money, and that is the solution to every financial crisis you can think of going backwards, and that will be the solution to future financial crises,” Howell said.

“Given the fact that the debt levels are rising remorselessly year after year after year, politicians are kicking the can down the road,” he said. “They’ve got no appetite to control spending, and they just think the easy way out is either take on more debt or print money.”

At a time when assets have become the go-to investment for institutional investors and armchair traders, one of the most important strategies is to refrain from selling gold.

“You don’t want to be selling gold right now,” he said. “Strategically, you’ve got to hold gold.”

Good as Gold

In 10 years, gold could reach $10,000 per ounce, according to Howell—and he is not the only one presenting a bullish prognostication.

Yardeni Research forecasts $10,000 by the end of the decade.

“This is all happening because rising geopolitical tensions are driving a military arms race, and defense companies need metals to increase their output,” Yardeni Research said in a Jan. 25 research note.

“Also boosting metals prices is the geopolitical AI arms race, which is escalating capital spending on technology.”

Meanwhile, “deep currents” are supporting gold’s rally, such as U.S. deficit spending and central bank buying, said David Miller, senior portfolio manager at Catalyst Funds.

“These are very powerful forces and will likely drive gold significantly higher over the next three, five, or even [10] years,” Miller said in a note emailed to The Epoch Times.

3. CHRIS POWELL AND HIS GATA DISPATCHES:

LIVE FROM THE VAULT YOU TUBE: 259 AND 258

LAST WEEK CRAIG HEMKE

5. COMMODITY REPORT/AGNICO EAGLE/EARNINGS RESULTS

- HUGE INCREASE IN RESERVES BY 2% HUGE

- EARNINGS $3.04 PER SHARE IN THIS QUARTER

- INCREASE IN INDICATED 10% AND INFERRED 15%

AgnicoEagle – AGNICO EAGLE PROVIDES AN UPDATE ON 2025 EXPLORATION RESULTS AND 2026 EXPLORATION PLANS – YEAR OVER YEAR MINERAL RESERVES INCREASE 2% TO 55.4 MOZ; INDICATED MINERAL RESOURCES INCREASE 10% TO 47.1 MOZ AND INFERRED MINERAL RESOURCES INCREASE 15% TO 41.8 MOZ

Highlights from 2025 include:

- Gold mineral reserves increase to record level – Year-end 2025 gold mineral reserves increased by 2.1% to 55.4 million ounces of gold (1,330 million tonnes grading 1.30 grams per tonne (“g/t”) gold). The year-over-year increase in mineral reserves is due to a combination of mineral reserve replacement from operating mines and the initial declaration of mineral reserves at the Marban deposit in Malartic. At year-end 2025, measured and indicated mineral resources were up 9.6% to 47.1 million ounces (1,200 million tonnes grading 1.22 g/t gold) and inferred mineral resources were up 15.5% to 41.8 million ounces (522 million tonnes grading 2.49 g/t gold)

- Detour Lake – The Company’s exploration program continued to de-risk the Detour Lake underground project in the western plunge of the main orebody hosting the producing open pits. Conversion drilling further increased underground indicated mineral resources below the resources open pit to 3.47 million ounces of gold (52.9 million tonnes grading 2.04 g/t gold) at year-end while exploration drilling below and to the west of the open pit increased underground inferred mineral resources to 3.88 million ounces of gold (59.6 million tonnes grading 2.03 g/t gold) at year-end

- Odyssey – Inferred mineral resources increased by 62% (2.8 million ounces of gold) year over year at the East Gouldie deposit to 7.4 million ounces of gold (94.3 million tonnes grading 2.43 g/t gold), including the Eclipse zone. The Odyssey mine now hosts a total of 6.03 million ounces of gold in proven and probable mineral reserves (59.7 million tonnes grading 3.14 g/t gold), 3.4 million ounces of gold in measured and indicated mineral resources (57.8 million tonnes grading 1.85 g/t gold) and 12.7 million ounces of gold in inferred mineral resources (177.7 million tonnes grading 2.21 g/t gold)

- Marban – As part of the “fill-the-mill” strategy at Canadian Malartic, a technical evaluation was completed at the Marban deposit during the fourth quarter of 2025 that updated the probable mineral reserves to 1.58 million ounces of gold (51.6 million tonnes grading 0.95 g/t gold) at December 31, 2025. This is the first declaration of mineral reserves by the Company at Marban since the acquisition of O3 Mining Inc., which includes the Marban deposit, in March 2025

- Hope Bay – Exploration drilling in 2025 totalled 131,208 metres and focused mainly on mineral resource expansion of the Madrid deposit following the exploration success at the Patch 7 zone during 2024 and 2025. The Patch 7 zone now hosts 1.0 million ounces of gold in indicated mineral resources (4.5 million tonnes grading 6.77 g/t gold) while inferred mineral resources have increased by 123% to 1.7 million ounces of gold (8.0 million tonnes grading 6.57 g/t gold)

- Exploration guidance – In 2026, the Company’s total exploration expenditures and project expenses are expected to be between $565 million and $635 million, with a mid-point of $600 million. This includes approximately $384 million for capitalized and expensed exploration, and approximately $216 million for advanced exploration project expenses, studies, and other corporate development activities. The Company’s exploration focus remains on extending mine life at existing operations, testing near-mine opportunities and advancing key value driver projects. Priorities for 2026 include continued drilling of the Detour Lake underground project, assessing the full potential of the Canadian Malartic property, supporting regional synergies in Abitibi and exploring Hope Bay

GOLD MINERAL RESERVES

As at December 31, 2025, the Company’s proven and probable mineral reserve estimate totalled 55.4 million ounces of gold (1,330 million tonnes grading 1.30 g/t gold). This represents a 2.1% (1.16 million ounce) increase in contained ounces of gold compared to the proven and probable mineral reserve estimate of 54.3 million ounces of gold (1,277 million tonnes grading 1.32 g/t gold) at year-end 2024 (see the Company’s news release dated February 13, 2025 for details regarding the Company’s December 31, 2024 proven and probable mineral reserve estimate).

The increase in mineral reserves at December 31, 2025 is the result of the replacement of 3.0 million ounces of gold mined from operating assets, including Odyssey, Meliadine, LaRonde, Goldex, Fosterville and Macassa, combined with the acquisition of the Marban project, where initial mineral reserves were declared at year-end 2025.

A technical evaluation of the Marban deposit completed during the fourth quarter of 2025 resulted in new probable mineral reserves of 1.58 million ounces of gold (51.6 million tonnes grading 0.95 g/t gold) at December 31, 2025. The progress in mineral reserve development at Marban is the result of efforts by the Company to leverage regional synergies following the recent transactions to consolidate the Malartic camp at Canadian Malartic and advance the “fill-the-mill” strategy.

Mineral reserves were calculated using a gold price of $1,600 per ounce for most operating assets, with exceptions that include Detour Lake open pit using $1,500 per ounce; Amaruq and Pinos Altos using $2,000 per ounce; and variable assumptions for some other pipeline projects, including Marban and Wasamac using $1,650 per ounce. For detailed mineral reserves and mineral resources (“MRMR”) data, including the economic parameters used to estimate the mineral reserves and mineral resources and by-product silver, copper and zinc at mines and advanced projects, see “Detailed Mineral Reserves and Mineral Resources Data (as at December 31, 2025)” and “Assumptions used for the December 31, 2025 mineral reserve and mineral resource estimates reported by the Company” below.

The ore extracted from the Company’s mines in 2025 contained 3.74 million ounces of in-situ gold (65.5 million tonnes grading 1.78 g/t gold).

The Company’s gold mineral reserves as at December 31, 2025 are set out in the table below, and are compared with the gold mineral reserves as at December 31, 2024. Data in this table and certain other data in this news release have been rounded to the nearest thousand and discrepancies in total amounts are due to rounding.

| Proven & ProbableGold Mineral Reserve (000s oz) | Average Mineral ReserveGold Grade (g/t) | ||||||||

| Operation / Project | 2025 | 2024* | Change | 2025 | 2024* | Change | |||

| LaRonde mine | 1,959 | 2,081 | -122 | 5.73 | 6.03 | -0.30 | |||

| LaRonde Zone 5 | 889 | 659 | 230 | 2.09 | 2.21 | -0.12 | |||

| LaRonde Total | 2,848 | 2,740 | -108 | 3.72 | 4.26 | -0.54 | |||

| Canadian Malartic mine | 1,449 | 1,944 | -495 | 0.77 | 0.81 | -0.04 | |||

| Marban deposit | 1,577 | n/a | n/a | 0.95 | n/a | n/a | |||

| Odyssey deposit | 327 | 317 | 10 | 2.12 | 2.27 | -0.14 | |||

| East Gouldie | 5,699 | 5,236 | 463 | 3.23 | 3.37 | -0.15 | |||

| Canadian Malartic Total | 9,052 | 7,497 | 1,555 | 1.66 | 1.83 | -0.17 | |||

| Goldex | 786 | 789 | -2 | 1.60 | 1.57 | 0.02 | |||

| Akasaba West | 112 | 138 | -26 | 0.92 | 0.90 | 0.03 | |||

| Wasamac | 1,377 | 1,377 | — | 2.90 | 2.90 | — | |||

| Detour Lake(at or above 0.5 g/t) | 14,954 | 15,636 | -682 | 0.93 | 0.93 | — | |||

| Detour Lake (below 0.5 g/t) | 3,621 | 3,415 | 206 | 0.38 | 0.39 | (0.01) | |||

| Detour Lake Total | 18,575 | 19,051 | -476 | 0.72 | 0.75 | -0.02 | |||

| Macassa | 1,883 | 1,829 | 54 | 8.84 | 10.50 | -1.66 | |||

| Macassa Near Surface | 10 | 12 | -1 | 3.84 | 5.31 | -1.47 | |||

| AK deposit | 306 | 233 | 73 | 4.53 | 4.71 | -0.19 | |||

| Macassa Total | 2,200 | 2,074 | 125 | 7.77 | 9.18 | -1.42 | |||

| Upper Beaver | 2,768 | 2,768 | — | 3.71 | 3.71 | — | |||

| Hammond Reef | 3,323 | 3,323 | — | 0.84 | 0.84 | — | |||

| Amaruq | 1,454 | 1,609 | -155 | 2.55 | 3.36 | -0.81 | |||

| Meadowbank Total | 1,454 | 1,609 | -155 | 2.55 | 3.36 | -0.81 | |||

| Meliadine | 3,622 | 3,365 | 257 | 5.10 | 5.29 | -0.19 | |||

| Hope Bay | 3,396 | 3,398 | -2 | 6.53 | 6.52 | 0.01 | |||

| Fosterville | 1,670 | 1,650 | 20 | 4.99 | 5.37 | -0.38 | |||

| Kittila | 3,319 | 3,400 | -81 | 4.17 | 4.16 | 0.01 | |||

| Pinos Altos | 269 | 433 | -164 | 1.80 | 1.94 | -0.14 | |||

| San Nicolás (50%)** | 672 | 672 | — | 0.40 | 0.40 | — | |||

| Total Mineral Reserves | 55,442 | 54,284 | 1,158 | 1.30 | 1.32 | -0.03 | |||

2025 Exploration Highlights

At Detour Lake in 2025, exploration drilling totalled 214,668 metres for the full year. The program continued to expand and infill the mineralization below and to the west of the mineral resource pit.

In 2025, Domain 53 was tested through a high intensity drilling program from surface. It validated the continuity of the mineralization and improved the accuracy of the geological model. The investigation of Domain 54 is continuing with drilling from surface while the exploration ramp development is being advanced.