GOLD CLOSED CLOSED UP $79.85 TO $5058.25

ACCESS MARKET

GOLD $5086.00 3:30 PM)

SILVER: 84.41 3;30 PM)

HUMOUR OF THE DAY:

Oakland Mayor, Who Supported ‘Defund The Police’ Has Her Car Stolen

Friday, Feb 20, 2026 – 01:20 PM

Authored by Luis Cornelio via Headline USA,

An alleged thief stole Oakland Mayor Barbara Lee’s city-owned vehicle after breaking into her office just two days earlier, according to the California edition of the New York Post.

The Oakland Police Department recovered the vehicle within hours, two days after somebody tampered with her office’s door.

“The Oakland Police Department is investigating the theft of a city-owned vehicle. On February 17, 2026, OPD was notified that the vehicle was stolen from Oakland City Hall,” the OPD said through a spokesperson.

“The vehicle was recovered within hours. OPD is following up on potential leads.”

Lee took office in May 2025 after serving more than two decades in Congress.

She previously expressed support for efforts to “restructure” and “overhaul” policing during the 2020 protests, language widely associated with the “defund the police” movement.

In 2020, she told Politico she was “really proud” of the Minneapolis City Council’s pledge to defund the local police.

In December 2020, she also said, “We have to restructure our funding priorities in terms of how we make our communities safe.”

“We have seen video after video over the last few weeks of peaceful protestors being met with extreme violence from police,” Lee said during the 2020 protest in favor of George Floyd.

“We can’t wait. It’s time to overhaul our policing system.”

According to the New York Post, police already had an arrest warrant for the alleged suspect.

In a statement, Lee claimed her administration takes crimes seriously:

“As with criminal cases such as this, the Oakland Police Department is actively investigating, and we cannot comment further at this time. No one in Oakland should have to worry about their car being stolen, whether they’re a resident, a city worker, or the Mayor. Public safety is a priority across our entire city.”

The theft comes amid a broader problem for Oakland as the city reported 9,914 motor vehicle thefts in 2024, one of the highest rates in the country.

END

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,975.900000000 USD

INTENT DATE: 02/19/2026 DELIVERY DATE: 02/23/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 8

190 H BMO CAPITAL MARKETS 5

555 C BNP PARIBAS SEC CORP 2

661 C JP MORGAN SECURITIES 1

880 H CITIGROUP 2

TOTAL: 9 9

MONTH TO DATE: 36,578

JPMORGAN STOPPED 0/9

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 9 CONTRACTs NOTICES FOR 900 OZ or 0.0279 TONNES

total notices so far: 36,578 contracts for 3,657,800 OR 113.773 tonnes)

SILVER NOTICES: 50 NOTICE(S) FILED FOR 250,000 OZ /

total number of notices filed so far this month : 4,689 CONTRACTS (NOTICES) for 23.425 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S 0.235 MILLION OZ QEFP TRANSFER TO LONDON/ : NEW STANDING FOR SILVER AT THE COMEX REDUCES TO 24.145 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ//

NEW TOTALS FOR SILVER OZ STANDING IS AS FOLLOWS

NORMAL STANDING 24.145 MILLION OZ

PLUS OUR 2 EXCHANGE FOR RISK: 185,000 OZ

EQUALS

24.330 MILLION OZ!! HUGE FOR A FEBRUARY

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 50.930 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE SUBTRACT OUR EXCHANGE FOR PHYSICAL JUMP TO LONDONOF 0.235 MILLION OZ AND THEN ADD OUR 2 EXCHANGE FOR RISK FOR .185 MILLION OZ STANDING REDUCES TO 24.330 MILLION OZ!!

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0186 TONNES TO OTHER OF 41.92 TONNES/ NEW QUEUE JUMP TOTAL:41.9386 TONNES// AND THEN WE ADD OUR FIVE EXCHANGE FOR RISK: 9596 CONTRACTS OR 29.746 TONNES//NEW STANDING ADVANCES TO 157.186 TONNES

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 157.186 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING AND OUR FIVE ISSUANCES EXCHANGE FOR RISK!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 124.292 TONNES (WHICH WILL BE SMALLER THAN OTHER MONTHS)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A STRONG SIZED 518 CONTRACTS OI TO 130,490 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 610 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 666 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 592 CONTRACTS AND ADD TO THE 610 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF 92 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $0.23

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.460 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $0.23

2.ASIAN AFFAIRS FEB 20/2025

SHANGHAI CLOSED

HANG SENG CLOSED

Nikkei CLOSED DOWN 292.59 PTS OR 1.10%

//Australia’s all ordinaries CLOSED UP 0.28%

//Chinese yuan (ONSHORE) CLOSED XXXX

/ OFFSHORE CLOSED DOWN AT 6.9023 Oil UP TO 66.62 dollars per barrel for WTI and BRENT UP TO 71.28 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING XXXX OFFSHORE YUAN TRADING DOWN TO 6.9023 ONSHORE YUAN TRADING BELOW OFF SHORE AND XXX ON THE DOLLAR// / AND THUS XXXXX//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 592 CONTRACTS UP TO 409.585 OI WITH OUR LOSS IN PRICE OF $9.00 WITH RESPECT TO THURSDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST LITTLE NET LONGS, WITH THAT PRICE LOSS FOR GOLD . AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2495).

WE HAD LITTLE T.A.S. LIQUIDATION DURING THURSDAY’S TRADING. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO LONG THIS WEEK AFTER A BRIEF PERIOD OF GOING NET SHORT. HOWEVER SOME OF THOSE LONG SPECULATORS WERE ANNHILATED DURING THE TUESDAY RAID AND OTHERS WAITED UNTIL THE CONCLUSION OF TRADING AND TENDERED FOR BADLY NEEDED PHYSICAL TUESDAY AND WEDNESDAY

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS FEBRUARY CONTRACT MONTH!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW BACK TO AN EXTREMELY LOW OI OF AROUND 409000 TO NOW 409,585 AND NOW AMPLE ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE DIFFICULT TO FLEECE. THE ALL TIME LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 5 %

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1903 CONTRACTS (OR 5.919TONNES) DESPITE THE LOSS IN PRICE, WEDNESDAY.

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. THIS PAST WEEK WE HAVE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE ARE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE THUS FAR FOR FEB NOW REMAINS AT FIVE.(29.746 TONNES)

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO FEBRUARY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND NOW FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 5 ISSUANCES: 9596 CONTRACTS FOR 959,600 OZ OR 29.746 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY TOTALS!!

FEBRUAY ISSUANCES 5 FOR; 29.746 TONNES SO FAR!!

DETAILS ON OUR NEW FEBRUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1903 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH FEBRUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS (1439 CONTRACTS).THE CME NOTIFIES US THAT THEY HAVE ISSUED 773 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 5 EXCHANGE FOR RISK INCLUDING TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 29.746 TONNES!! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0,000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

11.FEB; 0. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.0186 TONNES ADDING TO ALL OTHER QUEUE JUMPS OF 41.920 TONNNES//NEW TOTAL QUEUE JUMP: 41.9386/ STANDING ADVANCES TO 127.234 TONNES TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK OF 29.746 TONNES/NEW STANDING ROCKETS TO 157.186 TONNES!!

THE FED IS THE OTHER MAJOR SHORT IN GOLD OF AROUND 106+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED ALL BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THE 106 TONNES IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD TO KEEP THE GOLD SUPPRESSION GAME ALIVE!! .. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. A MUCH HIGHER GOLD PRICE BLOWS UP THE DERIVATIVE APPARATUS OF THE BULLION BANKS.

BUT IT WAS IMPOSSIBLE/ THAT THE FED WAS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER,(LATEST BIS DATA SHOWS AN INCREASE IN GOLD BORROWING BY THE FRBNY// AND IT WAS NOT THE BUYER IN JANUARY OF 22.315 TONNES TOTAL IN JANUARY/6 EXCHANGE FOR RISK ISSUANCES AS WE NOW HAVE THE BIS DATA FOR GOLD SWAPS FOR JANUARY 2025 AND HERE WE FIND THAT THE FED ACTUALLY INCREASED THEIR GOLD SWAP LOANS WITH THE BIS TO THE 106 TONNES WHICH I NOW RECORD FOR YOU.!!THEN MUCH TO OUR ANGER WE RECEIVED NOTICE ON FRIDAY OF OUR 5TH EXCHANGE FOR RISK OF 6.871 TONNES//TOTAL EXCHANGE FOR RISK FEB OF 5 ISSUANCES EQUATES TO 29.746 TONNES OF GOLD WHICH WE ADD TO OUR NORMAL DELIVERY TOTALS.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/FEB.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 2495 CONTRACTS.

THAT IS A STRONG SIZED 2495 EFP CONTRACT WAS ISSUED: : /APRIL 2495 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2495 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 106+ TONNES

WE HAD :

- LITTLE LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE SOME GOVERNMENT LIQUIDATION

- SOME MONTH END SPREADERS LIQUIDATION AS THEY HAVE COMMENCED THEIR OPERATION

T.A.S.SPREADER ISSUANCE//FEBRUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A SMALL SIZED 773 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP THURSDAY’S LOSS IN PRICE IN GOLD YET WITH A CORRESPONDING STRONG SIZED GAIN OF OI ON OUR TWO EXCHANGES..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- JANUARY’S 6 ISSUANCE FOR 22.215 TONNES

- AND NOW FEB’S FIVE ISSUANCES FOR A MONSTER 29.746 TONNES.

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 30 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 106+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAIDS TO BE!GENERALLY HAPPENS ONCE EVERY TWO MONTHS

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OPTIONS EXPIRY MONTH INCLUDING JANUARY’S OTC/LBMA DRIVE BY SHOOTING! ALONG WITH RAIDS IN EARLY FEBRUARY LIKE WE EXPERIENCED FEB 10 ANDNOW TODAY

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.0186 TONNES WHICH IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.920 TO TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB:: 41.9386 TONNES///STANDING ADVANCES TO 127.440 TONNES TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK OF 29.746 TONNES/NEW STANDING ROCKETS TO TO 157.186 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING FEBRUARY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $9.00 )

WE HAD LITTLE T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// DESPITE OUR LOSS IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL WEDNESDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR FEBRUARY. THE COMEX IS ONE BIG MESS!!

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR NEXT QUEUE JUMP OF 0.0186 TONNES TO WHICH WE ADD TO ALL OTHER QUEUE JUMPS OF 41.920 / NEW QUEUE JUMP TOTALS: 41.9386 TONNES//STANDING ADVANCES TO: 127.234 TONNES TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK OF 9596 CONTRACTS FOR 959,600 OZ OR 29.746 TONNES/NEW STANDING 157.186 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $9.00

WE HAD A HUGE 5215 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

INITIAL GOLD COMEX

FEB 20

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRY i) Out of HSBC: 174,706.217 oz total withdrawal: 174,706.217 oz or 5.73 tonnes |

| Deposit to the Dealer Inventory in oz | 0 |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entry xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 9 notice(s) 900 OZ 0.0279 TONNES TONNES OF GOLD |

| No of oz to be served (notices) | 4394 contracts 439,400 OZ 13.672 TONNES |

| Total monthly oz gold served (contracts) so far this month | 36,578 notices 3,657,800 oz 113.773 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRY

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entry

customer withdrawals:

customer withdrawals:

1 ENTRY

i) Out of HSBC: 174,706.217 oz

total withdrawal: 174,706.217 oz or 5.73 tonnes

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 2

ALL DEALER TO CUSTOMER:

adjustments all dealer to customer account;

i) HSBC: 23,438.079 oz

ii) Loomis 289.359 oz

total adjusted out of dealer (reg) to customer (elig) = 23,727.438 oz

or 0.73 tonnes tonnes

leaving registered acct and landing in eligible accts.

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 4403 CONTRACTS FOR A LOSS OF 375 CONTRACTS.

WE HAD 381 CONTRACTS SERVED ON THURSDAY, SO WE GAINED A TINY 6 CONTRACT–

QUEUE JUMP FOR 600 OZ OR 0.016 TONNES

MARCH SAW A LOSS OF 192 CONTRACTS DOWN TO 5048 CONTRACT OI AS MARCH BECOMES THE NEW FRONT MONTH FOR GOLD AND EXPECT TO HAVE A HUGE STANDING OF AROUND 15+ TONNES FO GOLD. MARCH IS AN OFF MONTH FOR GOLD. SIXTEEN TONNES IS ABNORMALLY HIGH FOR MARCH!!

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 228 CONTRACTS UP TO 280,856 CONTRACTS

We had 9 contracts filed for today representing 900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 11 notices issued from their client or customer account. The total of all issuance by all participants equate to 9 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (36,578) to which we add the difference between the open interest for the front month of FEB (4403 CONTRACTS) minus the number of notices served upon today (9 x 100 oz per contract) equals 4,097,200 OZ OR (127.440 Tonnes of gold) to which we add February’s 5 exchange for risk of 9596 contracts or 95,9600 oz or 29.746 tonnes//new total gold standing in Feb skyrockets to 157.186 tonnes.

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (36,578 x 100 oz +we add the difference for front month of FEB (4403 OI} minus the number of notices served upon today (9 x 100 oz) which equals 4,097,200 OR 127.440 TONNES// to which we add our FIVE exchange for risk//959600 oz or 29.746 tonnes//new standing rockets to 157.186 tonnes!!!

new total of gold standing in FEB is 157.186 TONNES//

TOTAL COMEX GOLD STANDING FOR FEB 157.186 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF FEBRUARY.

confirmed volume THURSDAY confirmed 113,624 poor/

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,746,165.988 oz 54.31 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 33,920,234.713 oz (draining huge of gold)

TOTAL REGISTERED GOLD 17,176,865.725. or 534.27 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,743,,368..988 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 15,430,700 oz ((REG GOLD- PLEDGED GOLD)=

479.95 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SILVER/COMEX

FEB 20 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of Delaware 4000.800 oz ii) Out of HSBC 625,953.500 oz iii0 Out in Int.Delaware 346,959.600 oz iv) Out of Manfra: 192,635.400 oz total withdrawal: 1,169,549.300 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 0 ENTRY 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT ENTRIES: 1 i) Into Delaware: tiny 7,183.275 oz total deposit; 7183.275 oz |

| No of oz served today (contracts) | 50 CONTRACT(S) ( 250,000 OZ |

| No of oz to be served (notices) | 140 Contracts (0.700 MILLION oz) |

| Total monthly oz silver served (contracts) | 4689 contracts 23.425 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

withdrawals: customer side/eligible

i) Out of Delaware 4000.800 oz

ii) Out of HSBC 625,953.500 oz

iii0 Out in Int.Delaware 346,959.600 oz

iv) Out of Manfra: 192,635.400 oz

total withdrawal: 1,169,549.300 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 0

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 88.191MILLION OZ//.TOTAL REG + ELIGIBLE. 366.287 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 190 OPEN INTEREST CONTRACTS FOR A LOSS OF 62 CONTRACTS.

WE HAD 15 NOTICES FILED ON THURSDAY SO WE LOST 47 CONTRACTS OR WE HAD A STRONG

EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OF 235,000 OZ WHERE THESE BOYS WILL TAKE DELIVERY OVER IN LONDON. SILVER IS VERY SCARCE ON THIS SIDE OF THE POND.

MARCH LOST ONLY 5844 CONTRACTS DOWN TO 47,847. THIS BECOMES THE FRONT MONTH FOR SILVER DELIVERY AND WE SHOULD HAVE A DANDY OF A MARCH DELIVERY MONTH!!! WE HAVE 5 MORE READING DAYS BEFORE FIRST DAY NOTICE FEB 27. THE ROLLOVERS TO FUTURE MONTHS HAVE BEEN ON THE LOW SIDE AS IT SEEMS MANY WILL STAND FOR DELIVERY AND MAY EVEN BREAK THE BANK!!

APRIL GAINED 89 CONTRACTS TO AN OI 861 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 50 or 250,000 oz

CONFIRMED volume; ON WEDNESDAY 60,572 strong+++//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 4689 X5,000 oz = 23.425 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (190) AND the number of notices served upon today (50)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (4689)Notices served so far) x 5000 oz + OI for the front month of FEB(190) minus number of notices served upon today (50 )x 5000 oz equals silver standing for the FEB..contract month equating to 24.145 MILLION OZ. THEN WE MUST ADD OUR FIRST EXCHANGE FOR RISK TOTALS OF 25 CONTRACTS FOR .125 MILLION OZ TO FRIDAY’S 12 CONTRACT ISSUANCE//NEW TOTAL EXCHANGE FOR RISK 37 CONTRACTS FOR .185 MILLION OZ//NEW STANDING REDUCES TO 24.330 MILLION OZ

NEW STANDING: 24.330 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 24.330 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 88.191 million oz of registered silver

JPMorgan as a percentage of total silver: 155.854/366.257.million: 42.53%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

FEB 20/2026/WITH GOLD UP $79.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 19/2026/WITH GOLD DOWN $9.00 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 18/2026/WITH GOLD UP $102.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 17/2026/WITH GOLD DOWN $136.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ /// ///INVENTORY RESTS AT 1077..04 TONNES

FEB 13/2026/WITH GOLD UP $94.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.140 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.18 TONNES

FEB 12/2026/WITH GOLD DOWN $143.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.000 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.32 TONNES

FEB 11/2026/WITH GOLD UP $63.65 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.34 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.32 TONNES

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

FEB 9/2026/WITH GOLD UP $100,00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.23 TONNES

FEB 6/2026/WITH GOLD UP $86.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1077.95 TONNES

FEB 5/2026/WITH GOLD DOWN $57.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.95 TONNES

FEB 4/2026/WITH GOLD UP $17.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.72 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1083.38 TONNES

FEB 3/2026/WITH GOLD UP $270.80 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1087.10 TONNES

FEB 2/2026/WITH GOLD DOWN $100.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.10 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1075.61 TONNES, TONIGHTS TOTAL

SILVER

FEB 20 WITH SILVER UP $4.85 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.035 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.853 MILLION OZ

FEB 19 WITH SILVER DOWN $0.23 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 5.798 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 502.888 MILLION OZ

FEB 18 WITH SILVER UP $4.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 11.325 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508.686 MILLION OZ

FEB 17 WITH SILVER DOWN $4.39 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 4.253 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 515.753 MILLION OZ

FEB 13 WITH SILVER UP $2.35 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.994 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 520.011 MILLION OZ

FEB 12 WITH SILVER DOWN $8.78 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 635,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 522.005 MILLION OZ

FEB 11 WITH SILVER UP $3.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 815,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 521.370 MILLION OZ

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

FEB 9 WITH SILVER UP $5,24 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

FEB 6 WITH SILVER UP 0.08 A HUGE WITHDRAWAL OF 3.942 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 522.367 MILLION OZ

FEB 5 WITH SILVER DOWN $7.87 A HUGE WITHDRAWAL OF 2.175 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 526.309 MILLION OZ

FEB 4 WITH SILVER UP $2.02 A HUGE WITHDRAWAL OF 3.551 MILLION OZ FROM THE SLV://. ./ :INVENTORY RESTS AT 528.484 MILLION OZ

FEB 3 WITH SILVER UP $6.11 A MASSIVE MASSIVE PAPER AND FRAUUDULENT 32.898 CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 531.985 MILLION OZ

FEB 2 WITH SILVER DOWN $1.32 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 499.853 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Gold and silver recovering

In very low turnover on Comex, gold and silver begin to recover as geopolitical tensions rise. Evidence is increasing of a possible attack by the US on Iran in the coming days.

| Alasdair MacleodFeb 20∙Paid |

Gold and silver rallied this week in a firmer tone suggesting a gradual climb higher is in prospect. In Europe this morning, gold traded at $5025, up $105 from last Friday’s close, while silver at $80.50 was up $5.30 over the same timeframe. US markets were closed on Monday for Washington’s birthday, which may have contributed to pitifully low volumes on Comex, arrowed on the charts below:

These turnover numbers are exceptionally low, even for holiday periods and reflect a futures market dying on its feet. Open interest in both contracts is also very low, but gold’s is showing some signs of recovery, illustrated next:

Clearly, speculative interest is virtually absent in both contracts, which is likely to be reflected in London’s forward market. If the point behind the recent shakeout was to rinse out flaky longs, then that process is completed.

There has been some uncertainty over price trends during China’s new year holiday, with Shanghai markets being closed for the entire week, reopening on Monday. The evidence is that this is where prices are being determined, particularly for silver with London and New York playing a secondary role. Therefore, the few speculators on the short side would be sensible to close their bears ahead of the weekend, which explains the feel of a firmer underlying tone for both metals from mid-week onwards.

Additionally, there is mounting speculation by informed sources that the US is preparing to mount an attack on Iran in the next few days. If so, then it could take place this weekend. It follows Bibi’s visit to Washington with his list of demands to be satisfied in current US-Iran negotiations, which are clearly unacceptable to the Iranians.

The UK is reported to have refused to allow the US to use the RAF’s Fairford airbase in Gloucestershire in an attack on Iran. If the report in Wednesday’s The Times is true, US plans to attack Iran are well advanced and are being frustrated by the UK’s interpretation of international law over the use of its airbases.

We can guess that the UK government will give way. But Iran has made it clear that if she is attacked, she will respond aggressively against US bases in the region and use her recently obtained Russian hypersonic missiles against Tel Aviv. Additionally, she will close the Straits of Hormuz, which Goldman Sachs believes could spike oil to $300. Furthermore, the 2026 comprehensive strategic pact between Iran, China, and Russia comes into the picture, potentially escalating a US-Iran conflict into a wider conflict which would almost certainly backfire badly on the US.

All this points to a US attack in the coming days being unlikely, with US tactics primarily intended to maximise pressure on Iran’s negotiators. They surely suspect this, expecting to force the US to back down, though tensions are likely to continue to exist.

In other news which might be distantly related to ongoing Middle East tensions, early this month China advised domestic investment institutions and banks holding US treasuries to reduce their exposure. This is the most public attack on US finances so far, a message sure to be noticed by other holders of US debt when as much as $10 trillion of it is due to be refinanced in 2026 in addition to funding the current budget deficit.

We shall see how it plays out. But for now, it should be noted that the dollar’s purchasing power is declining at an alarming rate, which is the message from the gold price rising sharply in recent months. And where gold goes, so do commodities in general, indicated by the chart of the CRB Index which is clearly heading higher:

This index comprises 19 commodities, including base metals, agriproducts and energy. It has tripled since 2020 and indicates commodity-driven inflation will continue to be a problem in 2026—2027.

This gives the Fed a headache when the US economy appears to be stalling and therefore requiring lower interest rates to lessen a recession. Domestic issues are bound to take precedence over preserving the purchasing power of the dollar, driving the dollar lower still, and therefore gold and commodity prices higher.

end

GOLD

COURTESY ROBERT H

| Robert |  10:18 AM (0 minutes ago) 10:18 AM (0 minutes ago) | ||

| to | |||

Trust is high in Gold

Cheers

Robert

One attachment • Scanned by Gmail

end

4.LIVE FROM THE VAULT YOU TUBE: 260 and 259

7

5. COMMODITY REPORT/URANIUM

2.ASIAN AFFAIRS FEB 20/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED

HANG SENG CLOSED

Nikkei CLOSED DOWN 292.59 PTS OR 1.10%

//Australia’s all ordinaries CLOSED UP 0.28%

//Chinese yuan (ONSHORE) CLOSED XXXX

/ OFFSHORE CLOSED DOWN AT 6.9023 Oil UP TO 66.62 dollars per barrel for WTI and BRENT UP TO 71.28 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING XXXX OFFSHORE YUAN TRADING DOWN TO 6.9023 ONSHORE YUAN TRADING BELOW OFF SHORE AND XXX ON THE DOLLAR// / AND THUS XXXXX//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED XXXX

OFFSHORE YUAN: DOWN TO 6.9023

HANG SENG CLOSED

2. Nikkei closed DOWN 292.59 PTS OR 1.10%

WEST TEXAS INTERMEDIATE OIL UP 66.42

BRENT; 71.28

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 97.84 /// EURO FALLS TO 1.1765 DOWN 6 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +2.112/ DOWN 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.40… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.338 DOWN 1 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: XXX OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.7368 Italian 10 Yr bond yield DOWN to 3.348 SPAIN 10 YR BOND YIELD DOWN TO 3.153

3i Greek 10 year bond yield DOWN TO 3.353

3j Gold at $5028.60 Silver at: 80.37 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 46/100 roubles/dollar; ROUBLE AT 77.20

3m oil (WTI) into the 66 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.40 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.112% DOWN 2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.308 DOWN 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7762 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9129 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.073 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.700 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.472 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.84 UP 6 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.351 DOWN 2 PTS

30 YR UK BOND YIELD: 5.151 DOWN 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.239 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.752 DOWN 1 BASIS PTS.

1a New York Opening report

Futures Drop As Iran Tensions Rise, Data Deluge Looms

Friday, Feb 20, 2026 – 08:29 AM

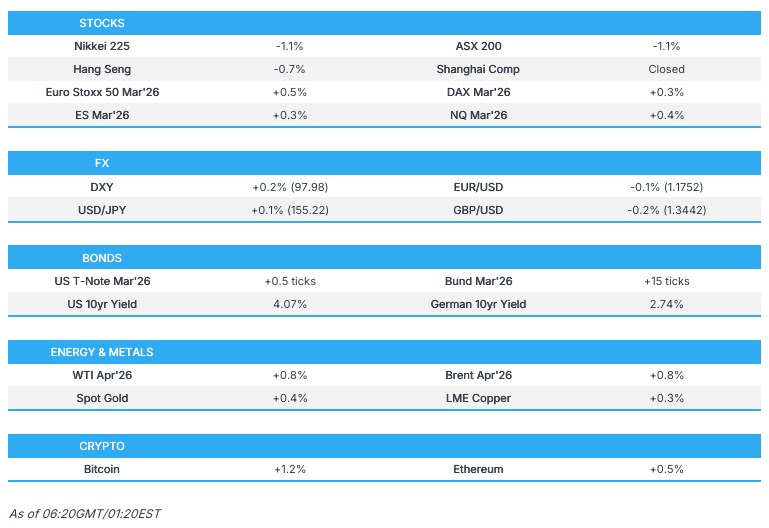

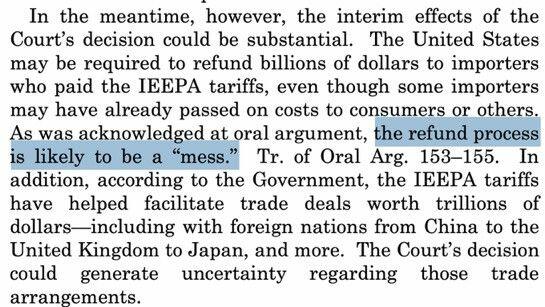

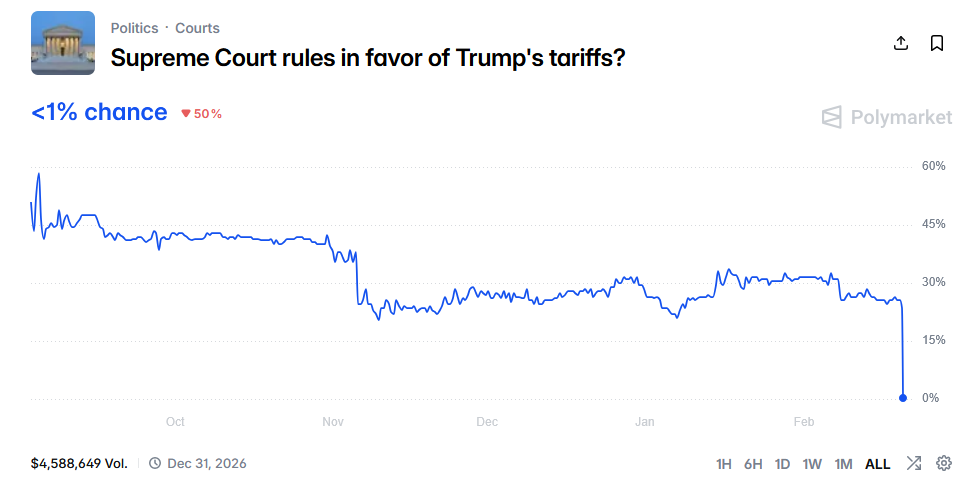

US equity futures are lower, sliding from session highs around the European open to session low just before 8am E as traders assessed the potential market impact of war with Iran, and awaited a firehose of US economic data including GDP and core PCE. As of 8:15am ET, S&P and Nasdaq futures are down 0.1% having traded in the green for much of the overnight session. Pre-market, Mag 7 are mostly red with GOOGL bucking the trend and rising +1.2%. Blue Owl Capital’s shares were set to fall a further 3.5% after its decision to limit withdrawals from a private credit fund. Bond yields have also reversed and are now lower on the session while the USD is flat. Commodities are mixed: base metals are lower while precious metals are rallying, sending gold above $5000 again; Brent crude fell toward $71 a barrel, paring gains since Monday to about 5%. Overnight, a WSJ article rehashed the now familiar story that Trump considers an initial limited strike to force negotiation. Today, key macro focus will be PCE, Flash PMIs and SCOTUS opinion day (markets are waiting for possible decision on IEEPA tariffs).

In premarket trading, magnificent Seven stocks are mixed early Friday (Alphabet (GOOGL) +1.2%, Nvidia (NVDA) -0.3%, Tesla (TSLA) -0.1%, Amazon (AMZN) +0.02%, Meta (META) -0.3%, Microsoft (MSFT) -0.1%, Apple (AAPL) -0.3%)

- Akamai Technologies (AKAM) falls 11% after the software company gave an outlook for adjusted earnings that is weaker than expected for both the first quarter and the full year.

- Ardelyx (ARDX) drops 6% after the drugmaker gave sales forecast for its Ibsrela drug in the first quarter that Jefferies views as softer than expected

- Copart (CPRT) falls 8% after the online vehicle salvage auction company reported operating income for the second quarter that missed the average analyst estimate.

- Floor & Decor (FND) climbs 4% after the flooring and tile retailer reported adjusted earnings per share for the fourth quarter that exceeded the average analyst estimate.

- Grail (GRAL) tumbles 47% after the early cancer detection test maker said Galleri, its multi-cancer screener, failed to meet its primary endpoint of statistically significant reduction in combined Stage III and IV cancer.

- Harmonic (HLIT) rises 9% after the communications equipment’s book-to-bill is seen as strong and reinforcing its growth potential.

- Hudbay Minerals (HBM) declines almost 5% after the miner reported fourth-quarter adjusted earnings per share that missed the average analyst estimate as production fell year-over-year.

- Newmont (NEM) drops 4% after the world’s biggest gold miner said it expects to produce less bullion this year, due to planned upgrades at some of its managed mines and lower output at two joint ventures with Barrick Mining.

- Opendoor Technologies (OPEN) climbs 19% as the online marketplace for residential real estate reported revenue for the fourth quarter that beat the average analyst estimate.

- RingCentral (RNG) rises 10% after the software company’s fourth-quarter results beat expectations on key metrics and it gave a positive forecast for both the first quarter and the full year.

- Texas Roadhouse (TXRH) rises 4% after the restaurant chain said it expects positive comparable restaurant sales growth for the year as it plans to implement a menu price increase in early April.

- Workiva Inc. (WK) gains 12% after the software company reported fourth-quarter results that beat expectations and gave revenue forecasts for both the first quarter and the full year that are seen as positive.

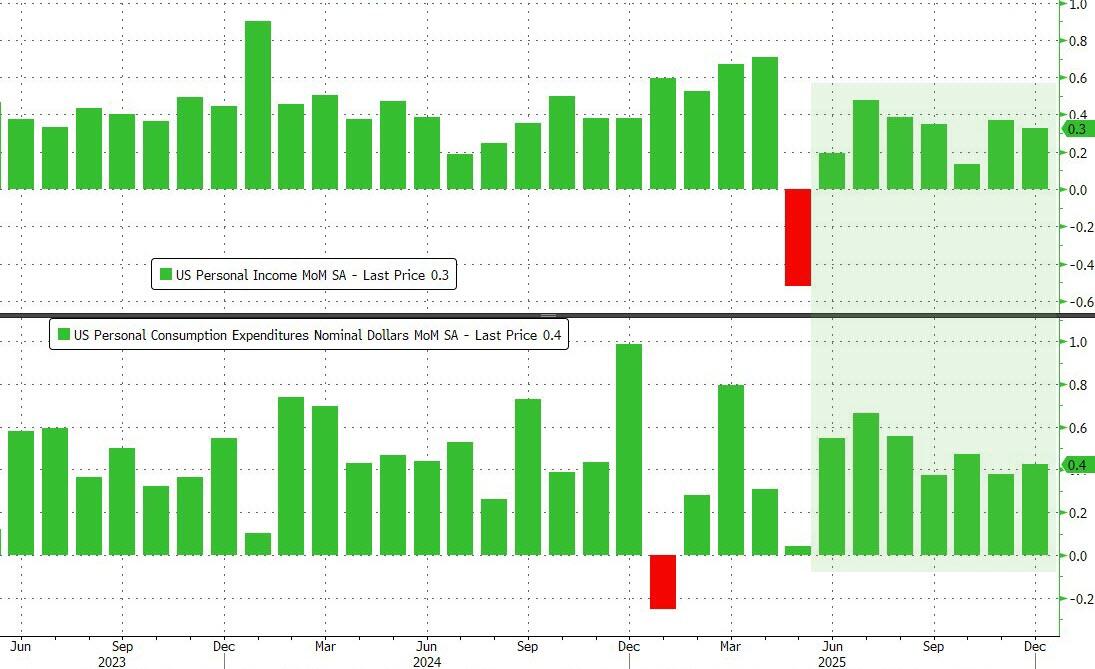

Friday morning brings long-delayed readings of core personal consumption expenditure — a measure of price changes in consumer goods and services that excludes volatile food and energy costs. The data may prove important not only in deciphering the next move in interest rates, but also the outlook for the great rotation trade out of tech names into materials, energy and other cyclicals linked to a stronger economy. Bloomberg Economics expects core inflation to have accelerated into the year end. Prices of services including recreation, accommodation and video streaming are likely to have contributed to a month-on-month increase of 0.32% in the core PCE deflator for December and a tick-up in the annual rate to 2.9% from 2.8%.

Wider inflation is set to be stoked by oil near a six-month high as Trump oversees the biggest US military buildup in the Middle East since 2003 and warns Iran that it has 10 to 15 days at most to strike a deal over its nuclear program — or else.

Speaking of “or else”, the US military is deploying a vast array of forces in the Middle East as President Donald Trump ramps up pressure on Tehran to strike a deal over its nuclear program. While the move in oil seeped into risk assets, traders note that recent geopolitical flare-ups have had only a limited impact on markets.

“Geopolitical stories are really notoriously difficult to price,” Marija Veitmane, head of equity research at State Street Global Markets, told Bloomberg TV. “Right now it’s almost impossible to assign probabilities to any outcome, given how quickly those narratives change.”

Elsewhere, as Trump looks to soothe concerns among rich and poor alike ahead of the midterms, he declared victory in the fight over cost-of-living concerns. It signals a new approach from the president that denies problems with his economic agenda while touting stock market gains to insist that his tariff plans have been a success. The White House is ratcheting up pressure on Congress to enact Trump’s proposed ban on investors buying homes, laying out for the first time what sort of investment firms he plans to target, The Wall Street Journal reports.

Turning to earnings, Of the 425 S&P 500 companies to have reported so far this earnings season, more than 74% have beaten analysts’ estimates, while nearly 21% have missed. No major companies are due to report today, but the earnings season picks up pace again next week, with companies representing a further 13% of the S&P’s market value on deck.

European stocks rebound after a halt to their rally in the prior session. Stoxx 600 up by 0.5%, with consumer, construction and chemicals outperforming. Moncler leads luxury stocks to outperform, while the energy and utilities sectors lag. Here are some of the biggest movers on Friday:

- Moncler shares gain as much as 13%, the most since September 2024, after the maker of high-end puffer jackets reported results that Barclays said were significantly ahead of estimates.

- Air Liquide shares rise as much as 3.9%, trading at a three-month high, after the French industrial-gas producer posted second-half earnings that beat expectations and raised its dividend more than anticipated, according to a Jefferies analyst.

- Kingspan shares climb as much as 9.4%, touching their highest level since 2024, after the construction firm generated record revenue and said the part of its business that builds infrastructure for data centers has an “extraordinary pipeline.”

- Unipol shares rise as much as 6.6%, their biggest gain in over 10 months, after the Italian insurer topped expectations in the latest quarter, with Barclays noting a higher dividend, stronger capital returns and better margins.

- Dis-Chem shares rally as much as 4.6% in Johannesburg, touching its highest intraday level in over a year, after the pharmacy stores chain reported a loyalty program-driven increase in revenue.

- ALK-Abello shares rise as much as 4.7%, hitting their highest level in over a month, after the pharmaceutical company with a focus on allergies said it will pay its first dividend since 2017 and topped expectations in the final quarter, according to analysts at Jefferies.

- Siegfried shares fall as much as 6.7%, the most since August, after weaker-than-expected 2026 guidance from the the Swiss pharma firm.

- Umicore shares decline as much as 7.1% in Brussels, hitting its lowest intraday level since December after the specialty chemicals company reported net income for 2H 2026 that missed the average analyst estimate.

- Danone shares drop 2.1% after a like-for-like sales beat was offset by a miss in volumes and misses in certain units in China and the US, according to Jefferies.

- Aston Martin shares slip as much as 4.4% after the British carmaker posted another profit warning.

- Chemring shares slide as much as 5.5% after the defense firm said it has made a slower start to the year than anticipated.