GOLD CLOSED CLOSED UP $52.50 TO $5229.75

ACCESS MARKET

GOLD $5261.25 3:30 PM)

SILVER: 93.65 3;30 PM)

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 5,176.500000000 USD

INTENT DATE: 02/26/2026 DELIVERY DATE: 03/02/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 29

099 H DEUTSCHE BANK AG 31

104 C MIZUHO SECURITIES US 14

118 C MACQUARIE FUTURES US 53

132 C SG AMERICAS 38

167 C MAREX 4

323 H HSBC 875

363 H WELLS FARGO SECURITI 578

435 H SCOTIA CAPITAL (USA) 500

555 C BNP PARIBAS SEC CORP 290

624 H BOFA SECURITIES 548

661 C JP MORGAN SECURITIES 1495

685 C RJ OBRIEN 20

686 C STONEX FINANCIAL INC 4

737 C ADVANTAGE FUTURES 8

880 H CITIGROUP 48

905 C ADM 19

TOTAL: 2,277 2,277

MONTH TO DATE: 2,277

JPMORGAN STOPPED 0/2277

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2026: 2277 CONTRACTs NOTICES FOR 227,700 OZ or 7.082 TONNES

total notices so far: 2227 contracts for 227,700 OR 7.082 tonnes)

SILVER NOTICES: 4540 NOTICE(S) FILED FOR 22,700 MILLION OZ /

total number of notices filed so far this month : 4540 CONTRACTS (NOTICES) for 22.700 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SUSRPRISINGLY LOW 31.076 MILLION OZ/

NEW TOTALS FOR SILVER OZ STANDING IS AS FOLLOWS

NORMAL STANDING 31.076 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF ISLVER STANDING IS 31.076 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES.

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

\

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 2209 CONTRACTS OI TO 117,865 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 630 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 630 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2209 CONTRACTS AND ADD TO THE 630 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF 1579 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WTH OUR LOSS OF $4.05

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 78955 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $4.05

2.ASIAN AFFAIRS FEB 27/2025

SHANGHAI CLOSED UP 16.25 PTS OR 0.39%

HANG SENG CLOSED UP 249,52 PTS OR 0.95%

Nikkei CLOSED UP 213.61 PTS OR 0.36%

//Australia’s all ordinaries CLOSED UP 0.26%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.8582

/ OFFSHORE CLOSED DOWN AT 6.8589 Oil UP TO 66.49 dollars per barrel for WTI and BRENT UP TO 72.00 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8582 OFFSHORE YUAN TRADING DOWN TO 6.8589 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1036 CONTRACTS DOWN TO 407,015 OI WITH OUR LOSS IN PRICE OF $30.25 WITH RESPECT TO THURSDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST SOME NET LONGS, WITH THAT PRICE LOSS FOR GOLD . AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1975).

WE HAD SOME T.A.S. LIQUIDATION DURING THURSDAY’S TRADING. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO MASSIVELY LONG THIS WEEK AFTER A BRIEF PERIOD OF GOING NET SHORT LAST WEEK. HOWEVER SOME OF THOSE LONG SPECULATORS WERE ANNHILATED DURING LAST TUESDAY RAID (FEB 17)AND OTHERS WAITED UNTIL THE CONCLUSION OF TRADING EACH AND EVERY DAY AND TENDERED FOR BADLY NEEDED PHYSICAL

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS FEBRUARY CONTRACT MONTH!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW MOVING TO ITS LOW POINT IN OI TO NOW 414,078 AND NOW AMPLE ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE EXTREMELY DIFFICULT FOR THE CROOKS TO FLEECE OUR NEWBIE SPEC LONGS. THE ALL TIME LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 5 %. RECENT LOWS FOR COMEX OI IS AROUND 409,000

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 839 CONTRACTS (OR 2.609TONNES) DESPITE THE LOSS IN PRICE, THURSDAY.

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. DURING THE MIDDLE OF THE MONTH. WE HAVE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE ARE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE THUS FAR FOR FEB NOW REMAINS AT SIX.(31.251 TONNES)

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MARCH:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUAY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: ZERO ISSUED SO FAR!

DETAILS ON OUR NEW MARCH COMEX CONTRACT MONTH//

IN TOTAL WE HAD A SMALL SIZED GAIN ON OUR TWO EXCHANGES OF 839 CONTRACTS DESPITE OUR LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MARCH/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS (1439 CONTRACTS).THE CME NOTIFIES US THAT THEY HAVE ISSUED 1256 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND NOW FINALLY IN USE TODAY WITH OTC/LONDON OPTIONS EXPIRY.

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0,000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

11.FEB; 0. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD EXCHANGE OUR NEXT 0.0248 TONNESS .1555 TONNES QUEUE JUMP AND THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 TONNNES//NEW TOTAL QUEUE JUMP: 41.233/ STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO TO 157.879 TONNES!!

12. MARCH: INITIAL GOLD STANDING FOR THIS NON ACTIVE DELIVERY MONTH IS 8.099 TONNES!!

THE FED IS THE OTHER MAJOR SHORT IN GOLD OF AROUND 106+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED ALL BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THE 106 TONNES IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD TO KEEP THE GOLD SUPPRESSION GAME ALIVE!! .. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. A MUCH HIGHER GOLD PRICE BLOWS UP THE DERIVATIVE APPARATUS OF THE BULLION BANKS.

BUT IT WAS IMPOSSIBLE/ THAT THE FED WAS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER,(LATEST BIS DATA SHOWS AN INCREASE IN GOLD BORROWING BY THE FRBNY// AND IT WAS NOT THE BUYER IN JANUARY OF 22.315 TONNES TOTAL IN JANUARY/6 EXCHANGE FOR RISK ISSUANCES AS WE NOW HAVE THE BIS DATA FOR GOLD SWAPS FOR JANUARY 2025 AND HERE WE FIND THAT THE FED ACTUALLY INCREASED THEIR GOLD SWAP LOANS WITH THE BIS TO THE 106 TONNES WHICH I NOW RECORD FOR YOU.!!THEN MUCH TO OUR ANGER WE RECEIVED NOTICE ON TODAY OF OUR 6TH EXCHANGE FOR RISK OF 1.505 TONNES//TOTAL EXCHANGE FOR RISK FEB OF 6 ISSUANCES EQUATES TO 31.251 TONNES OF GOLD WHICH WE ADD TO OUR NORMAL DELIVERY TOTALS.

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY.

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THIS WEEK SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/MARCH.//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1975 CONTRACTS.

THAT IS A FAIR SIZED 1975 EFP CONTRACT WAS ISSUED: : /APRIL 1975 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1975 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 106+ TONNES

WE HAD :

- SOME LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + BUT DID HAVE SOME GOVERNMENT LIQUIDATION

- MONTH END SPREADERS LIQUIDATION IS STILL IN FULL FORCE TODAY AS COMEX OPTIONS EXPIRY ENDED ON TUESDAY. LONDON OPTIONS EXPIRY CONCLUDES TODAY. THESE MONTH END SPREADERS HAVE DISTORTED OUR OI NUMBERS FOR GOLD COMEX GREATLY.

T.A.S.SPREADER ISSUANCE//FEBRUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT/FRIDAY MORNING WAS A FAIR SIZED 1256 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP THURSDAY’S HUGE LOSS IN PRICE IN GOLD YET WITH A CORRESPONDING STRONG GAIN OF OI ON OUR TWO EXCHANGES..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- JANUARY’S 6 ISSUANCE FOR 22.215 TONNES

- AND NOW FEB’S SIX ISSUANCES FOR A MONSTER 31.251 TONNES WHICH I BELIEVE IS THE HIGHEST EVER RECORDED AT THE COMEX.

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 30 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 106+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAIDS TO BE!GENERALLY HAPPENS ONCE EVERY TWO MONTHS

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OPTIONS EXPIRY MONTH INCLUDING JANUARY’S OTC/LBMA DRIVE BY SHOOTING! ALONG WITH RAIDS IN EARLY FEBRUARY LIKE WE EXPERIENCED FEB 10 AND NOW THE RAID// TUESDAY FEB 26..AND ATTEMPTED RAIDS THROUGHOUT OTC//LONDON OPTIONS EXPIRY ENDING TODAY!

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES!

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING MARCH,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $30.25 )

WE HAD SOME T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// WITH OUR LOSS IN PRICE AND CONSIDERABLE MONTH END SPREADER LIQUIDATION WHICH ACCOUNTS FOR THE LOSS IN PRICE… BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL THURSDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR FEBRUARY. THE COMEX IS ONE BIG MESS!!

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO MARCH:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $30.25

WE HAD A HUGE 3416 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .

INITIAL GOLD COMEX

FEB 27

MARCH DELIVERY MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 3 ENTRIES i) Out of Brinks 28,260.729 oz ii) Out of JPMorgan: 97,442.448 oz iii) Out of Manfra: 60,961.126 oz total withdrawal: 166,554.341 oz or 5.180 tonnes comex is draining of gold/. |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 entry xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 2277 CONTRACTS OR 227,700 OZ 7.082 TONNES OF GOLD |

| No of oz to be served (notices) | 327 contracts 32700 OZ 1.017 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2277 notices 227700 oz 7.082 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 1

1 ENTRY

1 ENTRY

i) Into Brinks: 13,092.095 oz

total deposit: 13,092.095 oz

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entry

customer withdrawals:

customer withdrawals:

3 ENTRIES

i) Out of Brinks 28,260.729 oz

ii) Out of JPMorgan: 97,442.448 oz

iii) Out of Manfra: 60,961.126 oz

total withdrawal: 166,554.341 oz

or 5.180 tonnes

comex is draining gold/.

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 2

customer to dealer (out of customer to the dealer account)//to replenish supplies

Brinks 2000.200 oz

Delaware 672.043 oz

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF MARCH STANDS AT 2604 CONTRACTS FOR A HUGE LOSS OF 333 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX IS AS FOLLOWS:

2604 NOTICES X 100 OZ PER NOTICE

EQUALS

260400 OZ OR 8.099 TONNES

WE LOST A LOT OF FRONT MONTH OI THESE PAST FEW DAYS

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 244 CONTRACTS DOWN TO 275,174 CONTRACTS

MAY GAINED 99 CONTRACTS UP TO AN OI OF 519.

We had 3984 contracts filed for today representing 398400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 1485 notices issued from their client or customer account. The total of all issuance by all participants equate to 2277 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAR. /2026. contract month, we take the total number of notices filed so far for the month (2277) to which we add the difference between the open interest for the front month of MAR (2604 CONTRACTS) minus the number of notices served upon today (2277 x 100 oz per contract) equals 260,400 OZ OR (8.099 Tonnes of gold)

thus the INITIAL standings for gold for the MAR contract month: No of notices filed so far (2277 x 100 oz +we add the difference for front month of MAR (2604 OI} minus the number of notices served upon today (2277 x 100 oz) which equals 260,400 OR 8.099 TONNES//

new total of gold standing in MAR is 8.099 TONNES//

TOTAL COMEX GOLD STANDING FOR MARCH 8.099 TONNES TONNES WHICH IS AVERAGE FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF MARCH.

confirmed volume THURSDAY confirmed 148,344 extremely poor/????

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,745,557.024 oz 54.29 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 33,321,135.041 oz (draining huge of gold)

TOTAL REGISTERED GOLD 17,101,111.68. or 531.916 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,220,023.355 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 15,355,554 oz ((REG GOLD- PLEDGED GOLD)=

477.62 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER/COMEX

FEB 27 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of Delaware 3158.787 oz ii) Out of HSBC 623,546.3000 oz iii) Out of JPMORGAN 24,905.770 oz iv) Out of Manfra 619,757.709 oz total withdrawal 1,270,767.526 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 0 ENTRY 1 entries i) Into Stonex: 13,092.095 oz total deposit: 13,092.095 oz xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT ENTRIES: 1 i) Into Delaware: 26,231.510 oz total deposit: 26,231.510 oz |

| No of oz served today (contracts) | 4540 CONTRACT(S) ( 22.700 MILLION OZ |

| No of oz to be served (notices) | 77 Contracts (0.385 MILLION oz) |

| Total monthly oz silver served (contracts) | 4540 contracts 22.700 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 ENTRIES

i) Into Stonex: 13,092.095 oz

total deposit: 13,092.095 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRIES: 1

ENTRIES: 1

i) Into Delaware: 26,231.510 oz

total deposit: 26,231.510 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

deposits into dealer account: 2

i) Into Stonex: 307,500.101 oz

ii) Into Brinks 824,168.850 oz

total dealer deposit: 1,131,669.030 oz

withdrawals: customer side/eligible

5 entries

i) Out of CNT 485,175.710 oz

ii) Out of Delaware 999.801 oz

iii) Out of JPMorgan 647,661.500 oz

iv) Out of Malca: 128,731.000 oz

v) Out of Manfra: 192,764.302 oz

total withdrawal 1,464,332.322 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 3

all customer account into the dealer: to replenish silver supplies

i) Brinks: 111,428,054 oz

ii)Delaware 85,768.116 oz

iii) Loomis: 964,465.510 oz

total customer to dealer; 1.161 million oz

total removal from the registered silver to eligible silver

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 88,423 MILLION OZ//.TOTAL REG + ELIGIBLE. 360.332 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH /2026 OI: 6214 OPEN INTEREST CONTRACTS FOR A HUGE LOSS OF 4302 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER WILLING TO STAND AT THE COMEX IS AS FOLLOWS:

6214 CONTRACTS X 5000 OZ PER CONTRACT

EQUALS

31,076 MILLION OZ.

WHICH IS SURPRISINGLY LOW COMPARED TO THE NON ACTIVE MONTHS OF FEB AND JANUARY

WE WE HAVE WITNESSED STRONG DELIVERIES.

APRIL LOST 146 CONTRACTS TO AN OI 1013 CONTRACTS.

MAY SAW A GAIN OF 2057 CONTRACTS UP TO AN OI OF 77,822, THE NEXT BIG ACTIVE DELIVERY MONTH.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4540 or 22.700 oz

CONFIRMED volume; ON THURSDAY 73,064 strong+++//

AND NOW MARCH. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 4540 X5,000 oz = 22.700 MILLION oz

to which we add the difference between the open interest for the front month of MARCH (6214) AND the number of notices served upon today (4540)x (5000 oz)

Thus the standings for silver for the MARCH 2026 contract month: (4540)Notices served so far) x 5000 oz + OI for the front month of MARCH(6214) minus number of notices served upon today (4540 )x 5000 oz equals silver standing for the FEB..contract month equating to 31.076 MILLION OZ.

NEW STANDING: 31.076 MILLION OZ WHICH IS SMALL FOR A GENERALLY HUGE DELIVERY MONTH OF MARCH.

New total standing: 31.076 million oz.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 88.423 million oz of registered silver

JPMorgan as a percentage of total silver: 153.844/360.332.million: 42.68%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

FEB 27/2026/WITH GOLD UP $52.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.90 TONNES

FEB 26/2026/WITH GOLD DOWN $30.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 11.45 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.62 TONNES

FEB 25/2026/WITH GOLD UP $48.40 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL WITHDRAWAL OF 0.300 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1086.17 TONNES

FEB 24/2026/WITH GOLD DOWN $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE PAPER DEPOSIT OF 7.72 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1086.47 TONNES

FEB 23/2026/WITH GOLD UP $148.25 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 20/2026/WITH GOLD UP $79.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 19/2026/WITH GOLD DOWN $9.00 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 18/2026/WITH GOLD UP $102.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 17/2026/WITH GOLD DOWN $136.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ /// ///INVENTORY RESTS AT 1077..04 TONNES

FEB 13/2026/WITH GOLD UP $94.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.140 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.18 TONNES

FEB 12/2026/WITH GOLD DOWN $143.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.000 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.32 TONNES

FEB 11/2026/WITH GOLD UP $63.65 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.34 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.32 TONNES

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

GLD INVENTORY: 1097.90 TONNES, TONIGHTS TOTAL

SILVER

FEB 27 WITH SILVER UP $5.54 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 0.544 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 517.519 MILLION OZ

FEB 26 WITH SILVER DOWN $4.05 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 0.906 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 516.975 MILLION OZ

FEB 25 WITH SILVER UP $3.43 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 8.923 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 517.881 MILLION OZ

FEB 24 WITH SILVER UP $0.55 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 10.056 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 508.958 MILLION OZ

FEB 23 WITH SILVER UP $4.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT WITHDRAWAL OF 0.951 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 498.902 MILLION OZ

FEB 20 WITH SILVER UP $4.85 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.035 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.853 MILLION OZ

FEB 19 WITH SILVER DOWN $0.23 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 5.798 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 502.888 MILLION OZ

FEB 18 WITH SILVER UP $4.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 11.325 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508.686 MILLION OZ

FEB 17 WITH SILVER DOWN $4.39 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 4.253 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 515.753 MILLION OZ

FEB 13 WITH SILVER UP $2.35 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.994 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 520.011 MILLION OZ

FEB 12 WITH SILVER DOWN $8.78 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 635,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 522.005 MILLION OZ

FEB 11 WITH SILVER UP $3.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 815,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 521.370 MILLION OZ

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 517.519 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

SHANGHAI/CITIC

FROM ROBERT LAMBOURNE:

| Robert Lambourne | 3:29 AM (1 hour ago) | ||

| to me, Chris | |||

I’ve double checked this with another AI and it confirms that there has been no update either from CITIC or SHFE on what has happened. It also confirms that there is no evidence from the market that it has been covered.

The new market rule introduced today has been put into effect, so in theory something should have happened. See the AI section below titled Delivery Surge which is in bold text.

I’m confused by the statement in the very last sentence of the Conclusion section about the position being rolled as I had read the new rule as prohibiting that.

I’ll check on the situation again later.

AI content

Based on the latest market data and reports available as of **February 27, 2026**, here is the updated status of CITIC Futures’ silver position:

### **Current Status: Position Still Open but Under Extreme Regulatory Pressure**

As of today, **CITIC Futures has not fully covered** its massive short position in silver on the Shanghai Futures Exchange (SHFE), but it is facing a critical deadline due to new exchange rules effective **today, February 27, 2026**.

* **Remaining Exposure:** Recent data from mid-February indicated CITIC held a net short position of over **12,000 to 14,800 contracts** (approximately 180–222 metric tons), making it the largest single short entity on the SHFE [[11]], [[12]], [[45]].

* **The “February 27” Catalyst:** Today marks the effective date of a major rule change by the SHFE specifically targeting near-term silver futures, which effectively forces the closure or physical settlement of speculative short positions in the delivery month [[32]], [[33]], [[87]].

* **No Full Cover Confirmed:** There is no public confirmation that CITIC has bought back all contracts in the open market; instead, the position is being addressed through the mandatory mechanisms imposed by the exchange’s new hedging limits [[87]].

### **New Mechanism: The SHFE “Rule Change” of Feb 27**

Rather than a voluntary market cover, the position is being “dealt with” via a regulatory强制 (mandatory) mechanism:

* **Zero Hedging Limit Rule:** Effective February 27, 2026, the SHFE has set hedging position limits for the delivery month and the preceding month to **zero contracts** for non-production entities, directly targeting paper silver shorts like CITIC [[87]].

* **Forced Deleveraging:** This rule essentially declares “war on paper silver,” requiring holders of large short positions in the front-month contract to either roll their positions (if eligible under strict new criteria), take physical delivery, or close out immediately before the First Notice Day [[32]], [[90]].

* **Delivery Surge:** Coinciding with this rule, delivery demand for silver futures has reportedly surged to **98%**, shattering the historical norm of 3–5%, which puts immense pressure on shorts like CITIC to resolve their obligations physically or face default [[92]].

### **Market Context & Implications**

* **Physical Inventory Crunch:** SHFE silver inventories have already declined sharply (from ~449 tons to ~423 tons in early February), exacerbating the difficulty for shorts to source metal for delivery [[19]], [[63]].

* **Price Volatility:** Silver prices have been highly volatile, surging past $90/oz on COMEX and reaching record premiums in Shanghai, driven by this squeeze dynamic [[3]], [[74]].

* **Strategic Shift:** While CITIC Securities maintains a bullish long-term outlook for precious metals, the immediate pressure on its futures arm suggests a forced restructuring of its book rather than a strategic exit [[7]], [[102]].

### **Conclusion**

The CITIC short position has **not been voluntarily covered** in the traditional sense. Instead, it is being **forced out or converted** by the SHFE’s new **February 27 rule** which eliminates hedging allowances for the delivery month, effectively squeezing the position out of the paper market and demanding physical resolution [[87]], [[33]]. Investors should watch today’s closing data and delivery notices for confirmation of how much of this volume was rolled versus settled physically.

end

then this later in the morning

Silver Calms Following Turbulent Volatility; China Faces Tightening Supply Crunch – Forex News by FX Leaders

Inbox

| Robert Lambourne | 9:07 AM (42 minutes ago) | ||

| to Chris, me | |||

This was published today and is quoted extensively by the AI update I’ve just received. This update is in full below the link

AI content – I’ve highlighted the conclusion that CITIC has not covered.

I’ll search for the latest updates on the CITIC silver short position and any SHFE inventory or exchange announcements from today, February 27, 2026.

I now have critical new information from today, February 27, 2026. Let me provide you with the updated factual summary, with specific focus on the CITIC short position and SHFE inventory updates.

CRITICAL UPDATE – February 27, 2026 (Today)

1. TODAY IS THE BREAKING POINT – DUAL EXCHANGE DEADLINE

Event Date Status

SHFE new hedging limits February 27, 2026 (Today) Effective now – near-month hedging automatically set to ZERO for non-approved participants

COMEX March silver First Notice Day February 27, 2026 (Today) Delivery intentions due – 400M oz contracts vs 98M oz registered

This is a synchronized liquidity event – both major exchanges implementing restrictive measures on the same day.

—-

2. SHFE SILVER INVENTORY – CRITICAL UPDATE (FEB 26 DATA)

Metric Data Change Implication

SHFE silver inventory (Feb 26) 346.369 tonnes ↓ 9.461 tonnes from Feb 25 (355.830t) Continued drawdown

SHFE low (Feb 9) 318.546 tonnes Lowest since 2015 All-time low territory

vs. historical peak 3,091.112 tonnes (Jan 2021) -88.8% Structural depletion

Key quote: “Silver inventories on the Commodity Exchange, Inc. (COMEX) and the Shanghai Futures Exchange (SHFE) have declined sharply, reflecting sustained drawdowns across key global trading hubs” .

—-

3. COMEX INVENTORY – FEB 26 UPDATE

Metric Data Change Status

COMEX total silver 360.64 million oz ↓ 1.21 moz (-0.33%) 32% below Oct 2025 (532 moz)

COMEX registered 86.13 million oz ↓ 0.18% Below 90 moz threshold

COMEX eligible 274.51 million oz ↓ 1.05 moz (-0.38%) Not available for delivery

Coverage ratio 86.13 moz registered / ~400 moz open interest 21.5% Cannot perform if >25% demand delivery

—-

4. CITIC/ZHONGCAI SHORT POSITION – NO UPDATE YET

Metric Current Status Evidence

Last verified position ~12,000+ contracts (~181.5 tonnes) – “over 12,000” InProved Feb 24

Peak position 28,000-30,000 contracts (450 tonnes) Reduced but still massive

Restriction status Cannot add/roll since Feb 5 Position limit ban active

Today’s status (Feb 27) NO OFFICIAL UPDATE Awaiting SHFE position report

Critical: The SHFE Volume & OI data was last updated at the end of Feb 26, 2026 , but specific silver contract position data (including CITIC) has not been published yet today. The exchange typically releases detailed position reports with a 1-2 day lag.

However, market structure indicates no covering has occurred:

Indicator Observation Implication

SHFE silver price ~$90.52 +3.44% today – rising, not falling

Shanghai premium $8.71 over international Widening, not compressing

Backwardation Record premiums for timely delivery Shorts paying to avoid delivery

Inventory trend ↓ 9.5 tonnes (Feb 26) No metal returned from covering

If CITIC had covered, we would see: rising inventory, falling price, compressing backwardation. None of these are present.

—-

5. MARKET COMMENTARY – TODAY (FEB 27)

From FX Leaders (published today):

“Short sellers on the Shanghai Gold Exchange who wagered that silver prices would decline have been paying deferral fees to long-holders to avoid having to make deliveries, underscoring the lack of metal to close positions.”

“The market’s overwhelming preference for timely delivery of the metal is evident in the front-month contract on the Shanghai Futures Exchange, which has reached a record premium.”

“The depletion of deliverable material and an inventory crisis are the main causes of this significant backwardation, according to Zhang Ting, senior analyst at Sichuan Tianfu Bank Co.”

From FX Leaders (also today):

“Silver is officially in ‘beast mode.’ As of today, February 27, 2026, the silver spot price has exploded into the $89–$91 per ounce range… COMEX registered inventories are at multi-year lows, and with a major delivery month ahead, a historic physical squeeze could be developing.”

—-

6. COMEX DELIVERY NOTICES – FEB 27 FIRST NOTICE DAY

Metric Data Source

February silver deliveries (month to date) Substantial but down from January CME delivery reports

March open interest ~400 million oz equivalent Market estimates

First Notice Day Today (Feb 27) Delivery intentions due

Delivery capacity 86.13 moz registered vs 400 moz open interest 21.5% coverage

Key risk: If 25-50% of March contract holders demand delivery, COMEX cannot perform and may face force majeure or cash settlement .

—-

7. BOTTOM LINE FOR FEBRUARY 27, 2026 (TODAY)

Factor Status Implication

CITIC short position ~12,000+ contracts (181.5t) – NO UPDATE Awaiting SHFE data; no evidence of covering

SHFE inventory 346.37t (↓9.5t Feb 26) Continued depletion

COMEX inventory 86.13 moz registered Below critical threshold

Today is First Notice Day COMEX March silver Delivery squeeze risk

SHFE rule change Near-month hedging ZEROED CITIC cannot roll

Price action Silver $90.52 (+3.44%) Squeeze pressure building

Market structure Deep backwardation Physical scarcity confirmed

The trap is sprung. The CITIC short has not covered (no inventory inflow, no price drop, no backwardation compression). Today is the breaking point – with SHFE hedging limits zeroed and COMEX First Notice Day, the market will discover whether physical delivery is possible or if a nickel-style squeeze unfolds.

Watch for: SHFE position report (likely tomorrow or Monday), COMEX delivery notices (today/tomorrow), and any exchange announcements regarding force majeure or position limits.

END

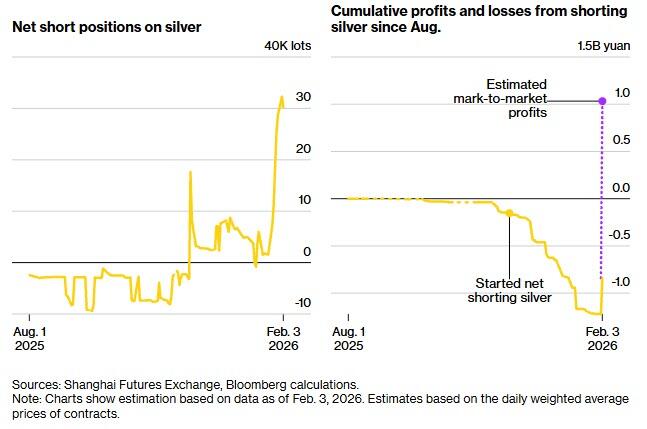

AND HERE HE IS: CITIC: BIAN

Beijing’s Big Short: Meet The Chinese “Anti Hunt Brother” Billionaire Betting Against Silver Bulls

2026 – 07:42 PM

Born in 1963 in Zhuji, Zhejiang Province, right in the middle of some pretty chaotic times in China’s history, reclusive billionaire Bian Ximing grew up to become a commodity titan after making some huge bets in the metals markets over the past few years.

In 2003, he bought Zhongcai Futures Co., which would become the centerpiece of his trading empire.

Bian spends much of his time in Gibraltar, and previously made nearly $3 billion from bullish bets on Shanghai Futures Exchange gold contracts since early 2022.

It is unknown if he has closed any of that position out.

In May 2025, the billionaire went all-in on copper, believing the metal is vital for China’s tech-heavy future and the global green energy push. Even with market volatility and political tensions, sources confirmed Bian’s massive copper position – nearly 90,000 tons – on the Shanghai Futures Exchange, confident that copper prices will climb.

It is unknown if he has closed any of that position out.

And now, Bloomberg reports that he has now built the bourse’s largest net short position in silver, according to Bloomberg analysis of exchange data and people with knowledge of his investments. They asked not to be named as the information is not public.

Bian’s big short comes with significant risk, and he has been forced to liquidate some positions at a loss in a volatile silver market.

From August last year, he built a long position in silver that generated more than 1.3 billion yuan in profit, according to calculations based on exchange data.

In November, however, he began shifting his position, attempting to call the top of the rally with tentative moves that occasionally left him on the losing side of trades.

From last week, however, Bian held his short position with conviction, spreading his exposure across longer-dated contracts and holding it through upward price swings.

Bian, through his brokerage Zhongcai Futures, began ramping up silver shorts in the final week of January, according to exchange data.

Exchange data showed Zhongcai’s silver short position surged to about 18,000 lots on Jan. 28.

It climbed further to about 28,000 lots on Jan. 30, when the metal in Shanghai reached an all-time high.

But he now holds a short that stands at about 450 tons of silver, or 30,000 contracts – so the metal’s sharp drop since last week has resulted in a paper gain of about 2 billion yuan ($288 million).

Including previous losses, Bian stands to make a net profit of around 1 billion yuan, based on his position and prices at the end of Tuesday.

Silver is again sliding in Thursday trade and has tumbled more than 40% from record highs a week ago – almost certainly significantly increasing Bian’s proceeds.

Bian’s “Big Short” is the antithesis of the billionaire Hunt Brothers’ bullish cornering of the silver market in the last 1970s (that didn’t end well for them).

Will ‘the herd’ go full ‘Gamestop’ on this newly exposed massive short position, which unlike so many of the myths about JPMorgan being short the precious metals, Bian is actually short… in size… for now.

END

1/PETER SCHIFF

JOHN RUBINO

2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Blue skies ahead for silver

Gold was steady but silver volatile as Comex March contracts matured. Suspension due to “technical failures” saw high volatility in silver which has since recovered.

| Alasdair MacleodFeb 27∙Paid |

At 13.00 Eastern Time yesterday, Comex suspended trading in metals and national gas contracts and options, citing technical issues. The suspension lasted about 40 minutes and all-day orders and GTD orders (good ‘till day) were cancelled. It came at a delicate time for the March silver contract, with the earlier prospect of deliveries demanded exceeding silver registered for delivery. Instead, they appear to have been cashed out.

Was this Comex’s way of defusing a silver crisis? We will probably never know…

In a difficult week for traders due to Comex contract expiries, gold and silver both firmed on balance. In European morning trade, gold was $5170, up $63 from last Friday’s close, and silver at $89.70 was up $4.20 Comex turnover was very subdued in both contracts.

Gold futures expiry, not being an active month caused few difficulties for traders who appear to be generally uninterested in the contract. Open interest is unusually low, which suggests that there is significant room for speculative buying before the contract is deemed overbought. The relationship between price and open interest is shown below:

This is an immensely bullish setup, unusual in character. Hedge funds and trend-chasers could buy up to 200,000 contracts before gold becomes overbought. Under those conditions, buying would not be restricted to Comex. Add in Chinese savers’ demand and we can justify a call for significantly higher gold prices.

Silver is much more interesting. Comex open interest has collapsed, which is explained by the short interest side effectively refusing to deal, other than to close existing positions. This is the next chart:

Meanwhile, Shanghai reopened on Tuesday following New Year celebrations and premiums for silver up to 12% over London spot have returned with a vengeance. These persistently high premiums are draining Comex and London’s liquidity.

On Comex, silver registered for delivery has declined to the equivalent of only 17,226 contracts, which explains yesterday’s controversy over Comex suspensions. There are still 6,214 March contracts outstanding this morning, suggesting that the grip around the shorts is still tight.

At least the shorts have succeeded in deterring buyers. The next chart shows that at 12,121 contracts the managed money category comprised mainly of hedge funds had the lowest long exposure for the last 20 years:

This was the position on 17th February, the date of the last Commitment of Traders figures, when open interest was 13,496 more than this morning’s preliminary number. We shall have an update for last Tuesday’s position after markets close tonight.

It is all very curious. Technical analysts are saying the silver price is going far higher, but trend-chasing hedge funds and investment managers are sitting firmly on their hands. It suggests that if silver resumes its march higher, disbelieving investors and speculators will change their minds but find there is no stock available at anything near current prices. And as commented above, gold is in a similar position but with more liquidity, likely to underwrite and possibly turbocharge the silver bull.

There is one important insight to share on silver. Last September, when China announced severe limitations on exports of rare earth metals, she unexpectedly withdrew from supplying silver. It was this which caused the crisis in London a fortnight later on 9th October, when lease rates spiked to 40% in a scramble for physical silver.

The reason China created this crisis is simple. The US had just put silver on its critical minerals list, signalling that the US government was about to buy large quantities for strategic purposes. China wasn’t going to supply silver that would end up in the USG’s stockpile.

It leaves the US with a problem. This week, fringe speculation suggested that President Trump was looking at Mexico’s silver as a solution, and if his form over Greenland was anything to go by, seek to incorporate Mexico into the US. That is unlikely to be a viable short-term fix, and individual supply deals with the mines are more likely, taking up to 200 million ounces of supply off the market. This would worsen the supply deficit for the current year, already estimated at 300 million ounces. But it’s difficult to see where else the US can go.

END

3.CHRIS POWELL AND HIS GATA DISPATCHES:

INDIA’S REGULATOR NOW ALLOWS GOLD TO BE PARKED INTO FUNDS

(Bloomberg/GATA)

India expands rules for $385 billion stock funds to add gold

Submitted by admin on Thu, 2026-02-26 22:08 Section: Daily Dispatches

By Ashutosh Joshi

Bloomberg News

Thursday, February 26, 2026

India’s market regulator has allowed the country’s $385 billion actively managed equity funds to park more of their money in gold and silver, giving them greater flexibility at a time when global demand for hard assets is rising.

Under revised rules by the Securities and Exchange Board of India, stock funds can invest the remainder of their portfolios — up to 35% of their assets — in gold and silver instruments, as well as in units of infrastructure investment trusts.

By widening the list of permitted assets, the regulator has given equity funds a broader toolkit that already includes money market and other liquid securities. The change could also create a new source of demand for gold and silver, which have attracted robust investor interest amid a blistering rally. …

… For the remainder of the report:

end

ECB sells some U.S. dollar assets, cuts weight of dollar in reserves

Submitted by admin on Thu, 2026-02-26 22:14 Section: Daily Dispatches

By Balazs Koranyi

Reuters

Thursday, February 26, 2026

FRANKFURT, Germany — The European Central Bank sold some of its dollar assets early last year and reduced the weight of the dollar in its foreign exchange reserves in what it said was a standard rebalancing of its portfolio.

The bank played down the significance of the move, which came before the market turbulence generated by U.S. President Donald Trump’s tariff announcement last April.

The ECB generated a gain of 909 million euros ($1.07 billion) from this first quarter transaction and invested all proceeds into Japanese yen assets, it said in its financial accounts today. …

… For the remainder of the report:

end

wow!! this is interesting!!

India tells mutual funds to stop using LBMA gold and silver prices

Submitted by admin on Thu, 2026-02-26 22:04 Section: Daily Dispatches

India’s Markets Regulator Changes Gold, Silver Valuation for Mutual Funds

From Reuters

Thursday, February 26, 2026

India’s markets regulator today directed mutual funds to use domestic stock exchange spot prices to value their physical gold and silver holdings from April 1, 2026.

The Securities and Exchange Board of India said mutual funds may now use polled spot prices from recognized stock exchanges that settle physically delivered gold and silver derivatives contracts, ensuring that valuations reflect domestic market conditions.

The change moves away from the currently used London Bullion Market Association prices to arrive at the valuation of gold and silver held by exchange traded funds.

end

Gold rigging researcher Stuart Englert interviewed by TF Metals Report

Submitted by admin on Wed, 2026-02-25 19:12 Section: Daily Dispatches

7:10p ET Wednesday, February 25, 2026

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke today interviewed Stuart Englert, author of the book “Rigged,” which documents gold price suppression policy, and now author of “Patient Millionaire — A Financial Memoir,” recounting his personal approach to the weaknesses of the world’s debt-based financial system.

Englert now is also writing frequent commentary at Substack here:

The interview is 24 minutes long and can be heard at the TF Metals Report here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4.LIVE FROM THE VAULT YOU TUBE: 261 and 260

5. COMMODITY REPORT/

2.ASIAN AFFAIRS FEB 27/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 16.25 PTS OR 0.39%

HANG SENG CLOSED UP 249,52 PTS OR 0.95%

Nikkei CLOSED UP 213.61 PTS OR 0.36%

//Australia’s all ordinaries CLOSED UP 0.26%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.8582

/ OFFSHORE CLOSED DOWN AT 6.8589 Oil UP TO 66.49 dollars per barrel for WTI and BRENT UP TO 72.00 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8582 OFFSHORE YUAN TRADING DOWN TO 6.8589 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.8582

OFFSHORE YUAN: DOWN TO 6.8589

HANG SENG CLOSED UP 249.52 PTS OR 0.95%

2. Nikkei closed UP 213.61 PTS OR 0.36%

WEST TEXAS INTERMEDIATE OIL UP 66.49

BRENT; 72.00

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 97.70 /// EURO FALLS TO 1.1798 DOWN 5 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.113/ DOWN 4 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.99… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.345 DOWN 3 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: 6.8582 AND THUS UP OFFSHORE: DOWN AT 6.8589

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6862 Italian 10 Yr bond yield DOWN to 3.307 SPAIN 10 YR BOND YIELD DOWN TO 3.099

3i Greek 10 year bond yield DOWN TO 3.305

3j Gold at $5174.80 Silver at: 89.56 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 84/100 roubles/

3m oil (WTI) into the 66 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.99 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.113% UP 3 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.345 DOWN 3 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7723 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9114 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.988 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.650 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.406 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.96 UP 6 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.2630 DOWN 6 PTS

30 YR UK BOND YIELD: 5.060 DOWN 6 BASIS PTS

10 YR CANADA BOND YIELD: 3.1717 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.717 DOWN 3 BASIS PTS.

1a New York Opening report

Futures Slide As Renewed AI Disruption And Private Credit Fears Spark Selling

Friday, Feb 27, 2026 – 08:30 AM