GOLD CLOSED CLOSED UP $77.25 TO $5149.50

ACCESS MARKET

GOLD $5157.50 3:30 PM)

SILVER: 83.95 3;30 PM)

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 5,065.300000000 USD

INTENT DATE: 03/05/2026 DELIVERY DATE: 03/09/2026

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 5

363 H WELLS FARGO SECURITI 516

555 C BNP PARIBAS SEC CORP 24

624 H BOFA SECURITIES 543

661 C JP MORGAN SECURITIES 94

709 C BARCLAYS 150

TOTAL: 666 666

MONTH TO DATE: 4,791

JPMORGAN STOPPED 94/666

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2026: 666 CONTRACTs NOTICES FOR 66,600 OZ or 2.0715 TONNES

total notices so far: 4791 contracts for 479,100 OR 14.902 tonnes)

SILVER NOTICES: 511 NOTICE(S) FILED FOR 2.555 MILLION OZ /

total number of notices filed so far this month : 6466 CONTRACTS (NOTICES) for 32.330 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A HUGE QUEUE JUMP OF 423 CONTRACTS OR A HUGE 2.115 MILLION OZ/NEW STANDING ADVANCES TO 38.010 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 20.535 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF ISLVER STANDING IS 31.076 MILLION OZ FOLLOWED BY TODAY’S 2/115 MILLION OZ QUEUE JUMP//NEW TOTAL STANDING ADVANCES TO 38.010 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES FOLLOWED BY TODAY’S 3.017 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 16.5007 TONNES/

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES FOLLOWED BY TODAY’S 3.017 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 16.5007 TONNES OF GOLD./

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES FOLLOWED BY TODAY’S 3.017 TONNES QUEUE JUMP //NEW STANDING ADVANCES TO 16.5007 TONNES/

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 80.93 TONNES//WILL BE VERY STRONG ISSUANCE THIS MONTH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A STRONG SIZED 532 CONTRACTS OI TO 112,794 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 112,794 CONTRACTS MARCH 4/2026

EFP ISSUANCE 320 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 320 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 452 CONTRACTS AND ADD TO THE 320 E.FP. ISSUED

WE OBTAIN ASMALL SIZED LOSS OF 212 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $0.98

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 1.06 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $0.98

2.ASIAN AFFAIRS MARCH 6/2025

SHANGHAI CLOSED UP 15.63 PTS OR 0.38%

HANG SENG CLOSED UP 435.95 PTS OR 0.72%

Nikkei CLOSED UP 346.94 PTS OR 0.63%

//Australia’s all ordinaries CLOSED UP 0.06%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.9047

/ OFFSHORE CLOSED DOWN AT 6.9153 Oil UP TO 82.73 dollars per barrel for WTI and BRENT UP TO 86.93 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING 6.9047 OFFSHORE YUAN TRADING UP TO 6.9133 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A TINY SIZED 203 CONTRACTS UP TO 413,937 OI DESPITE OUR HUGE LOSS IN PRICE OF $49.00 WITH RESPECT TO THURSDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT HUGE PRICE LOSS FOR GOLD . AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2813).

WE HAD NO T.A.S. LIQUIDATION DURING THURSDAY’S RAID. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO MASSIVELY LONG THIS MONTH AFTER A BRIEF PERIOD OF GOING NET SHORT AT THE BEGINNING OF FEBRUARY.

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MARCH CONTRACT MONTH!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW MOVING SLIGHTLY AWAY FROM ITS LOW POINT IN OI TO NOW 413,937 AND NOW ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE EXTREMELY DIFFICULT FOR THE CROOKS TO FLEECE OUR NEWBIE SPEC LONGS. THE ALL TIME LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 1 TO 2 %.(SILVER IS AT 7%) RECENT ALL TIME LOWS FOR COMEX OI IS AROUND 409,000

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3,016 CONTRACTS (OR 9.3810 TONNES) DESPITE THE LOSS IN PRICE, TUESDAY.

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. DURING THE MIDDLE OF THE MONTH. WE HAVE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE ARE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE THUS FAR FOR FEB NOW REMAINS AT SIX.(31.251 TONNES)

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MARCH:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUAY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: ZERO ISSUED SO FAR!

DETAILS ON OUR NEW MARCH COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 3016 CONTRACTS DESPITE OUR HUGE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MARCH/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 4962 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH NO EXCHANGE FOR RISK ISSUANCE SO FAR.. BUT DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE:

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 3.017//NEW STANDING FOR GOLD ADVANCES TO: 16.5007 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING MARCH,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $49.00 )

WE HAD ZERO T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// DESPITE OUR LOSS IN PRICE .. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD FOR FEBRUARY’S ACTIVE DELIVERY MONTH (157 TONNES) AND ALSO MARCH’S STANDING OF 13+ TONNES.

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO MARCH:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP 3.017 TONNES//N GOLD STANDING ADVANCES TO: 16.5007 TONNES/

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $9.55

WE HAD A HUGE zero CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .first time ever!!

NET GAIN ON THE TWO EXCHANGES : 3,016 CONTRACTS OR 301,600 OZ OR 9.3810 TONNES

INITIAL GOLD COMEX

MARCH 6

MARCH DELIVERY MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES i) Brinks 20,415.249 oz 0.635 tonnes comex is draining of gold/. |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRY one entry BRINKS 2000.01 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 666 CONTRACTS OR 66,600 OZ 2.0715 TONNES OF GOLD |

| No of oz to be served (notices) | 514 contracts 51400 OZ 1.598 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4791 notices 479,100 oz 14.902 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

DEPOSITS/CUSTOMER

1 ENTRY

one entry BRINKS

2000.01 oz

0 entry

customer withdrawals:

i) Brinks

20,415.249 oz

0.635 tonnes

comex is draining of gold/.

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1

dealer to customer account: Brinks

i) 103,590.522 oz or 3.22 tonnes leaves registered comex gold acct

COMEX IS DRAINING GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

chaos inside the comex

AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH STANDS AT 1180 CONTRACTS FOR A GAIN OF 473 CONTRACTS. WE HAD

497 CONTRACTS SERVED ON THURSDAY, SO WE GAINED A HUGE 970 CONTRACTS OR AN ADDITIONAL 97,000 OZ WILL STAND FOR DELIVERY AT THE COMEX. THE TONNAGE EQUATES TO 3,017 TONNES, A RATHER HUGE QUEUE JUMP.

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 8747 CONTRACTS DOWN TO 262,481 CONTRACTS. APRIL IS NOW THE NEW FRONT MONTH FOR DELIVERY OF GOLD. APRIL IS GENERALLY A VERY LARGE MONTH AND AN ACTIVE MONTH FOR GOLD.

MAY GAINED 68 CONTRACTS DOWN TO AN OI OF 678.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI ROSE BY A STRONG 7662 CONTRACTS UP TO AN OI OF 82,443

We had 666 contracts filed for today representing 66,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 666 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 94 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAR. /2026. contract month, we take the total number of notices filed so far for the month (4791) to which we add the difference between the open interest for the front month of MAR (1180 CONTRACTS) minus the number of notices served upon today (666 x 100 oz per contract) equals 530,500 OZ OR (16..5007 Tonnes of gold)

thus the INITIAL standings for gold for the MAR contract month: No of notices filed so far (4791 x 100 oz +we add the difference for front month of MAR (1180 OI} minus the number of notices served upon today (666 x 100 oz) which equals 530,500 OZ OR 16.5007 TONNES//

new total of gold standing in MAR is 16.5007 TONNES//

TOTAL COMEX GOLD STANDING FOR MARCH 16.5007 TONNES TONNES WHICH IS NOW HUGE FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF MARCH.

confirmed volume WEDNESDAY confirmed 182,546 weak

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,690,628.288 oz 52.58 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,690,628.288 tonnes oz 52.58 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 33,081,878.480 oz

TOTAL REGISTERED GOLD 16,899,869.562 or 525.656 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,182,008.868 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 15,209,241 oz ((REG GOLD- PLEDGED GOLD)=

473.07 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER COMEX

MARCH DELIVERY MONTH

MARCH 6 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) out of Brinks 305,127.770 oz ii) Out of CNT 611,508.09oz iii) Out of Delaware 1000.0000 oz iv) Out of Manfra 1,278,394.461 oz total withdrawals 2,196,030,321 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 0 ENTRY xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT ENTRIES: 0 |

| No of oz served today (contracts) | 511 CONTRACT(S) ( 2.555 MILLION OZ |

| No of oz to be served (notices) | 1136 Contracts (5.680 MILLION oz) |

| Total monthly oz silver served (contracts) | 6466 contracts 32.330 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRIES: 0

total deposit: nil oz

xxxxxxxxxxxxxxxxxxxxxxxxx

deposits into dealer account: 0

0 ENTRY

withdrawals: customer side/eligible

4 entries

i) out of Brinks 305,127.770 oz

ii) Out of CNT 611,508.09oz

iii) Out of Delaware 1000.0000 oz

iv) Out of Manfra 1,278,394.461 oz

total withdrawals 2,196,030,321 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 1

customer acct to dealer; (eligible to registered)

Loomis

i) 498,427.321 oz

total removal from the registered silver to eligible silver

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 81.733 MILLION OZ//.TOTAL REG + ELIGIBLE. 349.145 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH /2026 OI: 1687 OPEN INTEREST CONTRACTS FOR A GAIN OF 162 CONTRACTS.

WE HAD 261 NOTICES FILED ON THURSDAY SO WE GAINED A HUGE STRONG 423 CONTRACTS OR AN ADDITIONAL 2.115 MILLION OZ OF SILVER WILL TRY THEIR LUCK AND STAND FOR DELIVERY AT THE COMEX. THIS IS A HUGE QUEUE JUMP

APRIL, THE NEW FRONT MONTH SAW A GAIN OF 105 CONTRACTS UP TO 1271 CONTRACTS

MAY SAW A 301 CONTRACT GAIN UP TO 77,302 CONTRACTS.

JUNE SAY A GAIN OF 2 CONTRACTS DOWN TO 258 OI CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 511 or 2.555 MILLION oz

CONFIRMED volume; ON THURSDAY 59,140 strong+++//

AND NOW MARCH. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 6466 X5,000 oz = 32.330 MILLION oz

to which we add the difference between the open interest for the front month of MARCH (1647) AND the number of notices served upon today (511)x (5000 oz)

Thus the standings for silver for the MARCH 2026 contract month: (6466)Notices served so far) x 5000 oz + OI for the front month of MARCH(1647) minus number of notices served upon today (511 )x 5000 oz equals silver standing for the FEB..contract month equating to 38.010 MILLION OZ.

NEW STANDING: 38.010 MILLION OZ WHICH IS STILL LOWISH FOR A GENERALLY HUGE DELIVERY MONTH OF MARCH.

New total standing: 38.010 million oz.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are ONLY 81.733 million oz of registered silver

JPMorgan as a percentage of total silver: 152.794/349.145.million: 43.74%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAR 6/2026/WITH GOLD UP $77.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 5.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1075.894 TONNES

MAR 5/2026/WITH GOLD DOWN $49.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 18.032 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1081.038 TONNES

MAR 4/2026/WITH GOLD UP $9.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.545 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1099.07 TONNES

MAR 3/2026/WITH GOLD DOWN $188.75 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.35 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101.36 TONNES

MAR 2/2026/WITH GOLD UP $71.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101,13 TONNES

FEB 27/2026/WITH GOLD UP $52.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.90 TONNES

FEB 26/2026/WITH GOLD DOWN $30.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 11.45 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.62 TONNES

FEB 25/2026/WITH GOLD UP $48.40 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL WITHDRAWAL OF 0.300 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1086.17 TONNES

FEB 24/2026/WITH GOLD DOWN $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE PAPER DEPOSIT OF 7.72 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1086.47 TONNES

FEB 23/2026/WITH GOLD UP $148.25 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 20/2026/WITH GOLD UP $79.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 19/2026/WITH GOLD DOWN $9.00 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 18/2026/WITH GOLD UP $102.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 17/2026/WITH GOLD DOWN $136.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ /// ///INVENTORY RESTS AT 1077..04 TONNES

FEB 13/2026/WITH GOLD UP $94.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.140 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.18 TONNES

FEB 12/2026/WITH GOLD DOWN $143.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.000 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.32 TONNES

FEB 11/2026/WITH GOLD UP $63.65 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.34 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.32 TONNES

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

GLD INVENTORY: 1075.894 TONNES, TONIGHTS TOTAL

SILVER

MAR 6 WITH SILVER UP $2.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 5.526 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508,287 MILLION OZ

MAR 5 WITH SILVER DOWN $0.98 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.097 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 512.726 MILLION OZ

MAR 4 WITH SILVER DOWN $0.21 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.545 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 513.813 MILLION OZ

MAR 3 WITH SILVER DOWN $5.27 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2/899 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 511.268 MILLION OZ

MAR 2 WITH SILVER DOWN $3.87 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.352 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 514.167 MILLION OZ

FEB 27 WITH SILVER UP $5.54 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 0.544 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 517.519 MILLION OZ

FEB 26 WITH SILVER DOWN $4.05 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 0.906 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 516.975 MILLION OZ

FEB 25 WITH SILVER UP $3.43 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 8.923 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 517.881 MILLION OZ

FEB 24 WITH SILVER UP $0.55 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 10.056 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 508.958 MILLION OZ

FEB 23 WITH SILVER UP $4.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT WITHDRAWAL OF 0.951 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 498.902 MILLION OZ

FEB 20 WITH SILVER UP $4.85 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.035 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.853 MILLION OZ

FEB 19 WITH SILVER DOWN $0.23 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 5.798 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 502.888 MILLION OZ

FEB 18 WITH SILVER UP $4.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 11.325 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508.686 MILLION OZ

FEB 17 WITH SILVER DOWN $4.39 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 4.253 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 515.753 MILLION OZ

FEB 13 WITH SILVER UP $2.35 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.994 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 520.011 MILLION OZ

FEB 12 WITH SILVER DOWN $8.78 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 635,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 522.005 MILLION OZ

FEB 11 WITH SILVER UP $3.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 815,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 521.370 MILLION OZ

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

CLOSING INVENTORY 508.287 MILLION OZ OF SILVER..

.2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

Gold shortages in China

ICBC and Agricultural Bank of China have run out of investment gold bars. And silver premiums over London spot are 13%. Comex silver contract is sinking into irrelevance.

| Alasdair MacleodMar 6∙Paid |

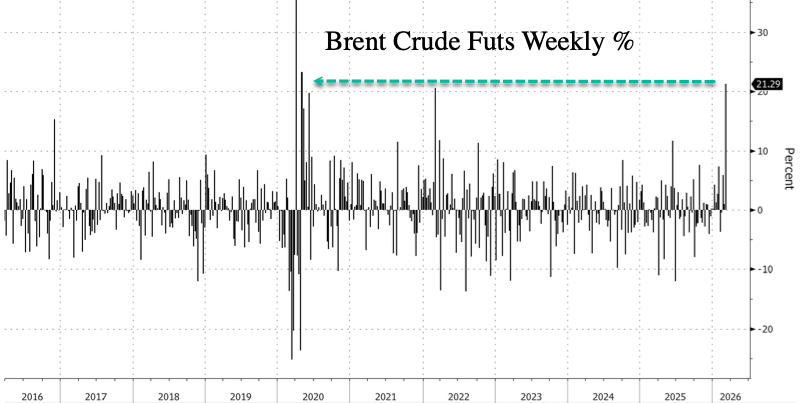

Last weekend, the US and Israel attacked Iran and the week’s news was dominated by another Middle East war. Markets’ gut reaction was to mark down investment assets and mark up dollars. Consequently, in the confusion gold and silver declined on the week as the dollar rallied. In European trade this morning gold was $5,090, down $230 from last Friday’s close, and silver at $82.70 was down $11 over the same timescale. Turnover on Comex in both contracts remained very low.

Meanwhile, premiums for silver in Shanghai held in the 12%-14% band. Given that silver imported into China bears 13% VAT and the cost of delivering from London or New York adds an extra 2%, this price difference is not enough to trigger an arbitrage. Nonetheless, silver is still being drained from all vaults, China’s included.

The delivery situation on Comex is dire, with the equivalent of only 16,250 silver contracts registered for delivery. Compare this with the 6,466 contracts delivered in the March contract to date. The March contract is still being bought with the obvious intention of standing for delivery, as is the April contract, which can be delivered from the last week in March onwards.

Comex silver is the most oversold it has been in over 20 years, with open interest on Wednesday at 112,794 contracts. This means that speculative activity is the lowest it’s ever been, discouraged by shorts not willing to sell any more contracts by widening their spreads. This is reflected in the next chart:

With over nine times paper liabilities compared with deliverable silver, which is also rapidly declining, this Comex contract is heading for trouble. Registered for delivery silver is being withdrawn along with eligible. Since the silver crisis in London on 9th October last, 175 million ounces have gone from Comex vaults, presumably to London where lease rates have remained elevated.

To summarise the position, paper silver in all markets is being encashed for physical, despite the fall in prices since 29th January when silver peaked at over $120. And with China being more of a physical delivery market, Comex and London paper contracts are declining into irrelevance.

Meanwhile, gold marches on with demand ranging from central banks to retail buyers and remaining strong despite the volatility. Yesterday, it transpired that two of China’s largest banks, ICBC and the Agricultural Bank, have run out of investment bars. Additionally, we can assume that there is strong demand for gold accumulation accounts at all Chinese retail banks with household savings running at an additional annual $5-$6 trillion equivalent and mirroring public demand for investment bars.

As with silver, there is minimal speculative interest in gold, with Comex’s open interest at the lowest levels since the covid pandemic:

It is remarkable that despite gold being in a strong bull market, speculative interest is so low, particularly when most of the major banks expect higher prices by the year-end. For now, hedge funds’ pair trading would sell paper gold short to buy dollars, which will lead to a short squeeze later.

The logarithmic chart demonstrates the underlying strength of gold’s uptrend despite short-term dollar demand:

As noted above, the market’s gut reaction to a new war on Iran is to presume that safety is to be found in cash dollars. Accordingly, the US$ trade weighted index has been marked higher against other currencies, shown next:

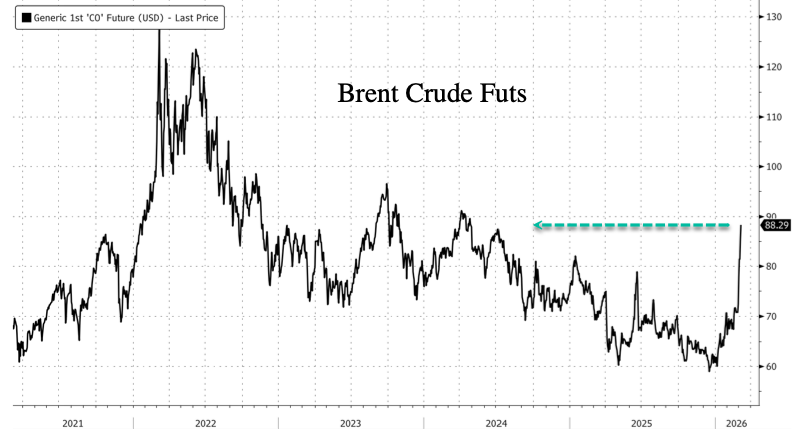

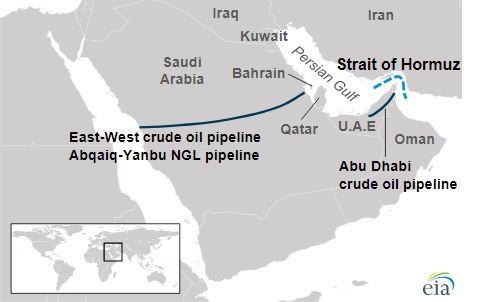

Most important of all, the blockade of Hormuz is driving energy prices skywards, as the oil chart shows:

Far from Iran rapidly admitting defeat, it is becoming obvious that this conflict will last some time. That being the case, we can expect yet higher oil and LNG prices and investor attention turning to the unexpected consequences for inflation later this year. Hopes of lower interest rates are vanishing and beginning to destabilise bond and equity markets, leading to a dash for cash.

It is worth recalling the move to higher interest rates and bond yields that followed Russia’s invasion of Ukraine and sanctions against Russian oil and gas. This is almost certain to happen again with even greater consequences, in which case bond yields will soar again and financial bubbles will be bursting everywhere.

In that event, any attempt to mark down gold and silver will be manna from heaven for stackers. Both metals are already in high demand, particularly in China, which cannot be satisfied.

A word to the wise: If gold and silver are marked down, stack, stack, and stack again!

END

3.CHRIS POWELL AND HIS GATA DISPATCHES:

4. ANDREW MAGUIRE AND LIVE FROM THE VAULT PODCASTS

KINESIS: PODCAST NO 262/ANDREW WITH BILL HOLTER

5. COMMODITY REPORT//GOLD //SILVER//CRAIG HEMKE

Gold to $6,100: Resistance Risk Is Real — Silver Short-Term Warning

by Sprott Money

Thursday, Mar 05, 2026 – 15:36

In this March 2026 episode, Craig Hemke for Sprott Money is joined by technical analyst Chris Vermeulen of The Technical Traders to analyze the latest volatility in gold, silver, and global markets. As geopolitical tensions shake commodities and equities, investors are watching whether the stock market could face a deeper correction while capital rotates into precious metals. Chris breaks down the recent spike in crude oil, key technical levels in the S&P 500 and Nasdaq, and why markets may be approaching a critical turning point. The discussion also explores the outlook for the gold price and silver price, including whether gold could be preparing for another breakout while silver remains volatile in the short term.

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.3,8655

END

ROBERT LAMBOURNE: FRBNY GOLD SWAP LOANS FROM THE BIS:

BIS – February gold swaps estimate

Chris, Harvey

It is essentially unchanged at 104 tonnes. This is down 2 tonnes versus the January estimate.

We now enter the quiet period where no monthly statement of accounts are published until late May or even June. This is the time when the BIS accounting personnel will be finalising the preparation of the published accounts for the year to 31 March 2026. This will include an external audit and so the delay is perfectly normal.

There is no new information on the status of Colin so it is reasonable to assume that he is stable.

I’ll leave it to you to decide what to write. I am happy to comment if you wish. Personally I would definitely leave in a reference to the drop in the swap volumes calculated at the time JP Morgan became a joint custodian. As we’ve discussed I’m reasonably sure that further double claims exist on ETF gold over and above the 104 tonne

end

this is terrific:

From G>G> to us:

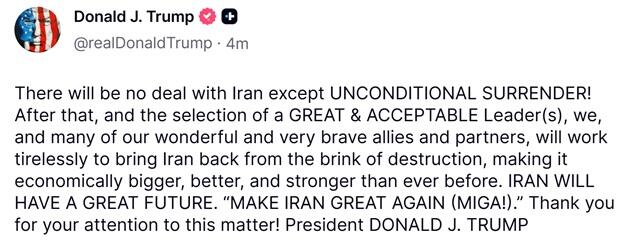

Gold should have exploded when the Iran war started. It did not. Understanding why it did not is more important than the price itself.

Inbox

| gijsbert groenewegen | 3:35 PM (3 minutes ago) | ||

| to gijsbert | |||

Read. Gijs

Gold should have exploded when the Iran war started. It did not. Understanding why it did not is more important than the price itself. On February 28, when US-Israeli strikes killed Khamenei, closed Hormuz, and destroyed twenty Iranian warships in forty-eight hours, gold spiked to an intraday high of $5,390.

By March 4, six days into the largest Middle East military campaign since the Gulf War, gold had dropped approximately 4 percent in a single session. It sits at $5,093 today. Net gain since escalation began: 2.3 percent. Brent crude surged 13 percent. Jet fuel gained 140 percent. Gold gained 2.3 percent.

The question every institutional investor is asking is why. The answer is the dollar.

When oil spikes 13 percent, the mechanism it activates first is not the safe-haven gold bid. It is the inflation expectation channel, which strengthens the dollar, which tightens real yields, which is the one macro environment where gold historically underperforms. The Fed faces its impossible trinity: oil-driven inflation demands rate hikes, growth shock demands rate cuts, war financing demands monetization. Markets read the inflation signal first and bought dollars. The dollar roared. Gold waited. This is not gold failing. This is gold being temporarily outbid by the dollar in the first phase of an inflation shock.

These two phases have played out in sequence in every major energy-driven geopolitical crisis: phase one, dollar strengthens on inflation expectations; phase two, when the sustained economic damage becomes visible and recession probability rises, the dollar weakens and gold surges because the market shifts from pricing inflation to pricing monetary debasement. In 1973 the second phase took roughly six months and produced gold gains of 73 percent.

In 2022 Russia-Ukraine it was compressed because the war was geographically contained and the Fed moved fast. In 2026 the relevant question is whether the war duration extends into the second phase window. Goldman Sachs has already moved. Their end-2026 gold target is $6,300, conditioned on prolonged Hormuz disruption. The probability architecture built from eight days of evidence suggests a 50 percent probability of a one-to-three month conflict. If Goldman’s scenario is correct, the current $5,093 level represents a $1,207 gap between today’s price and year-end target that the market has not yet priced. That gap exists because the market is still betting on a short war. The evidence is betting on a long one. The $5,000 support level is the number every technical trader is watching. The market is currently defending it. If it holds through the Fed’s March 18 meeting and the UN Security Council session on March 10, the base for the second phase move is intact. Gold reached $5,062 on February 20, before this war. Thesis Seven predicted $5,000 by Q2. It arrived four months early.

The war that arrived February 28 did not create this gold move. It inherited a gold price already priced for civilizational insurance and added a geopolitical premium that is still settling into its correct value. At $5,093 with Goldman at $6,300, with the Fed paralyzed, with Hormuz closed, with the Israeli Finance Ministry absorbing 9.4 billion shekels per week, and with the dollar’s inflation-driven strength carrying a self-limiting fuse, the gap between what gold is priced at today and what the evidence says it should be priced at is the temporal arbitrage that resolves when the market finishes pricing a short war and starts pricing the one actually being fought.

END

2.ASIAN AFFAIRS MARCH 6/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 15.63 PTS OR 0.38%

HANG SENG CLOSED UP 435.95 PTS OR 0.72%

Nikkei CLOSED UP 346.94 PTS OR 0.63%

//Australia’s all ordinaries CLOSED UP 0.06%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.9047

/ OFFSHORE CLOSED DOWN AT 6.9153 Oil UP TO 82.73 dollars per barrel for WTI and BRENT UP TO 86.93 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING 6.9047 OFFSHORE YUAN TRADING UP TO 6.9133 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9047

OFFSHORE YUAN: DOWN TO 6.9133

HANG SENG CLOSED UP 435.95 PTS OR 1.72%

2. Nikkei closed UP 346.94 PTS OR 0.63%

WEST TEXAS INTERMEDIATE OIL UP 82.73

BRENT; =86.88

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 99.20 /// EURO FALLS TO 1.1579 DOWN 28 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.166/ UP 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.82… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.394 UP 1 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: 6.9047 (DOWN) AND OFFSHORE: DOWN AT 6.9133

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8578 Italian 10 Yr bond yield UP to 3.582 SPAIN 10 YR BOND YIELD UP TO 3.323

3i Greek 10 year bond yield UP TO 3.552

3j Gold at $5080.95 Silver at: 82.73 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 55/100 roubles/79.22

3m oil (WTI) into the 82 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.82 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.166% UP 2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.394 UP 1 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7865 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9048 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.168 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.776 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.616 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 44.08 UP 8 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.6190 UP 8 PTS

30 YR UK BOND YIELD: 5.296 UP 6 BASIS PTS

10 YR CANADA BOND YIELD: 3.359 UP 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.902 UP 8 BASIS PTS.

1a New York Opening report

Futures, Global Markets Tumble As Oil Soars Amid Fears Of Lenghty Energy Crisis

Friday, Mar 06, 2026 – 08:28 AM

Seven days into the war on Iran and markets are getting increasingly shaky. US equity futures tumbled ahead of the February jobs report, and are on pace to close the worst week for global markets since 2020 deep in the red as the selloff in global bonds deepened after another jump in oil prices fanned fears that the war in the Middle East is fueling inflation. As of 8:00am ET, S&P 500 futures were 0.7% lower while contracts on the Nasdaq 100 fell 0.9% with all Mag7 names lower in premarket trading (NVDA -0.9%, GOOGL -0.6%). The yield on 10-year Treasuries climbed four basis points to 4.18%, on course for its biggest weekly advance since April as global government bonds tumble amid upside risks to inflation from higher energy prices. The dollar gained 0.2% while gold approached $5,100 an ounce. Commodities are mostly higher: Oil added another 6% with WTI now at $86.25; Oil prices are set for their strongest week since 2022, with the war in the Middle East effectively closing the Strait of Hormuz to shipping. Precious metals are mixed (gold down, silver +0.8%); base metals are lower. Overnight, the biggest catalysts was another escalation in Middle East with some articles pointing to potential shutdown in energy exports from Gulf states. Today’s US economic data slate includes February jobs report, January retail sales (8:30am), December business inventories (10am) and January consumer credit (3pm). Fed speaker slate includes Waller (7:30am), Daly (8:30am, 10:15am), Goolsbee (9:50am), Paulson (10:15am), Miran (11:30am), Collins (1:20pm) and Hammack (1:30pm, 3:10pm).

In premarket trading, Magnificent Seven are lowe (Microsoft -0.3%, Meta -0.5%, Tesla -0.6%, Alphabet -0.9%, Apple -0.7%, Amazon -1%, Nvidia -1.3%)

- Energy stocks are rising and airline stocks are declining as oil prices hit their highest level since 2024 and gas prices gained as the Iran conflict disrupted shipping through the Strait of Hormuz, limiting oil supply.

- Gap Inc. (GAP) falls 8% after reporting fourth-quarter sales and profit that came in slightly below expectations, as two of its apparel chains underperformed. Old Navy, the company’s biggest brand, and Athleta, its smallest, missed comparable-sales estimates.

- Guidewire Software (GWRE) rises 3% after the company reported second-quarter results that were much stronger than expected. It also raised its full-year forecast.

- Marvell Technology (MRVL) rallies 11% after the chipmaker said its year-over-year revenue growth rate will accelerate each quarter throughout fiscal 2027, a bullish target that shows soaring demand from data center-related applications.

- Nutex Health Inc. (NUTX) plunges 28% after the health-focused application software firm reported revenue for the fourth quarter that missed the average analyst estimate.

- Samsara (IOT) climbs 11% after the technology firm reported fourth-quarter adjusted earnings per share that topped the average analyst estimate.

- Trade Desk (TTD) slips 1% after Wedbush downgraded the advertising technology company to underperform — a sell equivalent — from neutral, saying the impact of an OpenAI partnership is “overestimated.”

In corporate news, Anthropic vowed to legally contest a Pentagon decision to declare it a threat to the US supply chain under an authority normally reserved for foreign adversaries, escalating a showdown with the Trump administration over AI safeguards.

The Iran war has entered its seventh day, with Iran firing a barrage of missiles and drones across the Persian Gulf and Israel renewing its airstrikes. Qatar’s energy minister sparked a powerful spike in energy price after he warned that war in the region could “bring down the economies of the world” and predicted that all Gulf energy exporters would shutter production within weeks, in an interview with the Financial Times. This is precisely what we warned about yesterday in “JPMorgan’s New Hormuz Closure Math: Just 3 Days Until Commodity Chaos.”

In the latest developments in the Middle East, Iran fired a barrage of missiles and drones targeting countries across the Persian Gulf overnight, while Israel renewed airstrikes on the Islamic Republic in a war that’s entered a seventh day with no end in sight. Saudi Arabia, Kuwait and Bahrain were among those came under renewed attack from the Islamic Republic, while Israeli airstrikes hit Tehran and Beirut.

Trump told NBC News that he wants Iran’s leadership structure fully removed, and that he has some names in mind for a “good leader.” The financial and logistical troubles the Iran war is causing for the global aviation industry are compounding by the day, with the number of canceled flights to Middle East hubs surpassing 27,000 since fighting began even as carriers look to resume some operations.

Still, US stocks are set to outperform global peers in a week that saw Middle East conflict drive fears of energy-driven price pressures, as traders awaited US jobs and retail sales data for insight into the Federal Reserve’s appetite for rate cuts.

That’s the good news for Trump, the bad news is that retail gasoline hit $3.32 a gallon on Thursday as the Iran conflict disrupts energy supplies from the Middle East. At the same time, the selloff in global bonds deepened on concern the shock to energy markets could broaden and drive inflation higher.

Friday’s market moves are capping a week of sharp swings in which investors repeatedly recalibrated their outlook on the impact of the US-Israeli war against Iran. Fears that a near-complete halt in traffic through the Strait of Hormuz could trigger a new inflation spike have led investors to scale back bets on Federal Reserve interest-rate cuts.

“This is an anxiety not only about how long the conflict goes on, but what kind of effect it’s going to have on the mix between growth and inflation,” Peter Oppenheimer, chief global equity strategist at Goldman Sachs Group Inc., told Bloomberg TV. “The issue really is 20% of world supplies are going through that channel, it’s obviously very, very significant.”

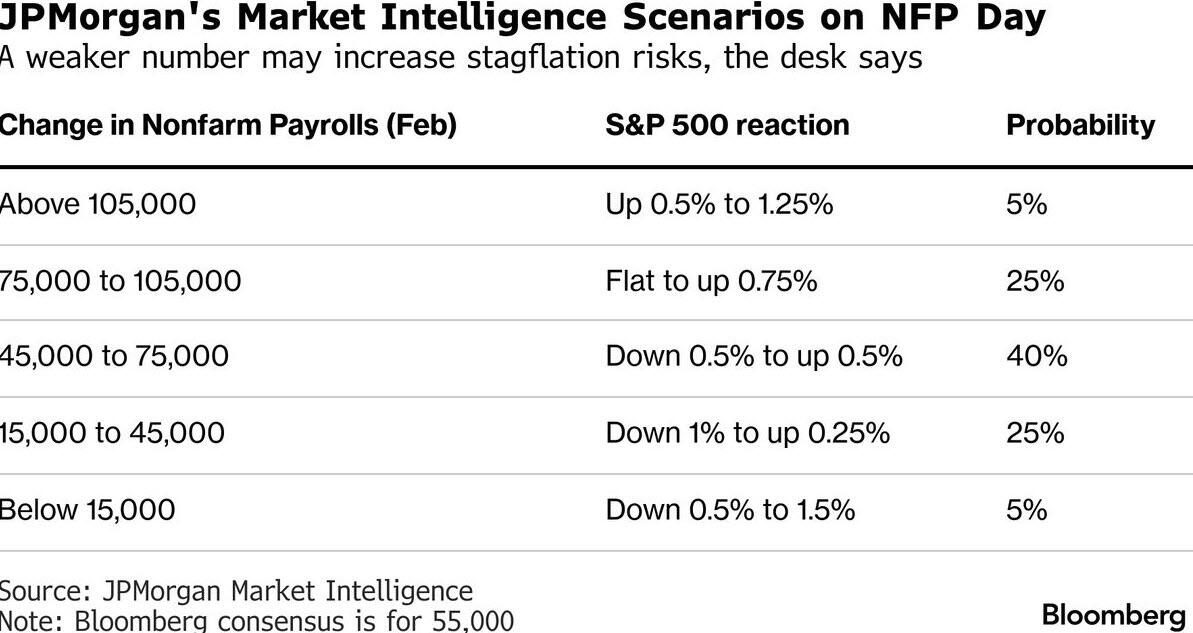

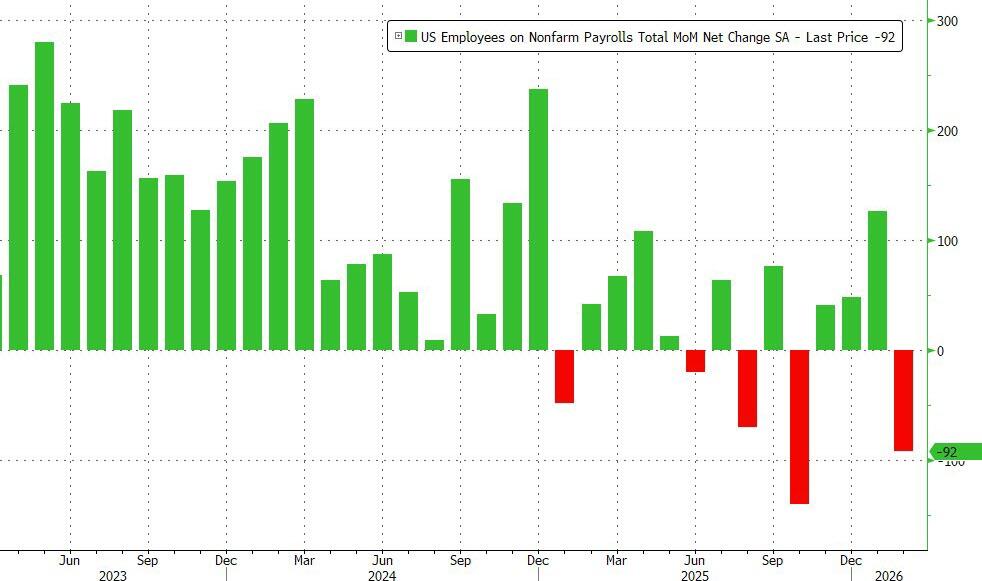

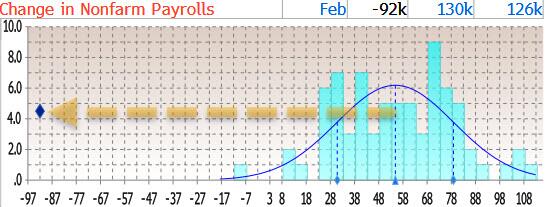

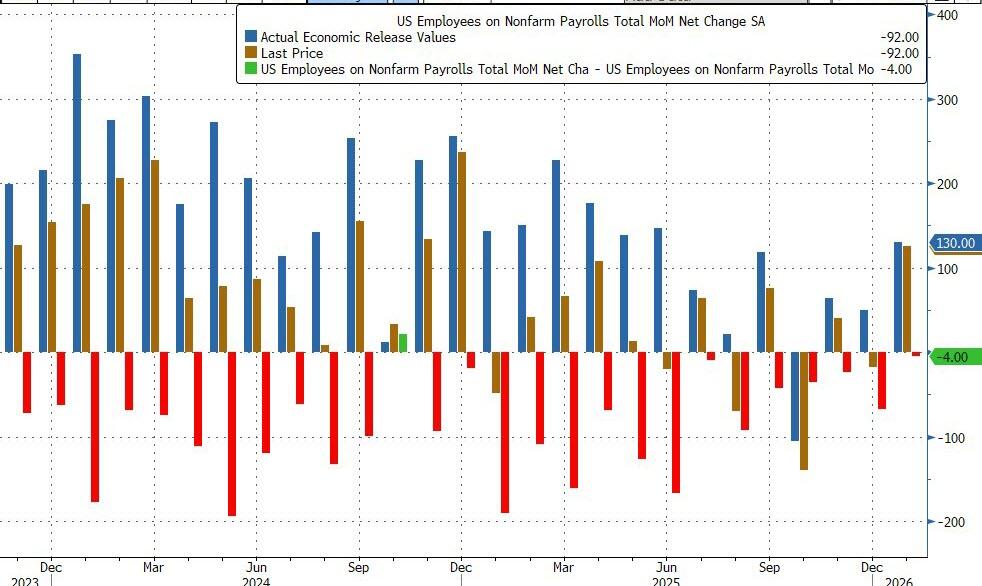

Today’s jobs report may offer more insight on the Fed’s rate path. Headline NFP print estimate is currently 55k, down from 130k last month with unemployment rate expected unchanged at 4.3%. Bloomberg whisper number for headline print is currently 55k (our full preview is here).

“The market would likely interpret robust job creation as evidence that the US economy remains on solid footing,” said Florian Ielpo, head of macro research at Lombard Odier Investment Managers. “This would accelerate the current rapid return to US equities and further fuel the reverse rotation we’ve observed over the past two weeks.”

Anna Wong, Chief US Economist at Bloomberg Economics, expects a tepid job report, largely reflecting temporary disruptions.

She forecasts the US economy to have added just 13,000 jobs in February, down from 130,000 in January. The consensus among analysts is for 55,000, and the “whisper” is for 65,000.

“For this print, the stronger the better given the increase in inflation expectations due to energy prices,” the JPMorgan Market Intelligence desk led by Andrew Tyler says. “A weaker number will increase rate cut expectations, but the risk is stagflation in the near-term given the expected increase in inflation.”

Bond yields are ticking higher heading into the print, and the dollar is muted, with markets pricing in less than 40 basis points of rate cuts for the rest of this year. In another sign of risk aversion, gold remains on track for its first weekly decline in over a month, pressured by a stronger dollar and inflationary risks tied to the Middle East conflict.

Traders slashed bets on Bank of England rate cuts for 2026, pricing just about a 50% chance of a quarter-point move. The yield on two-year gilts surged 13 basis points to 3.93%. Money markets are also fully pricing in that the European Central Bank will raise borrowing costs this year, a turnaround from a week ago when a cut was viewed more likely.

European stocks are now in the red after opening higher. Energy is up, while media, construction and technology sectors fall. Here are some of the biggest movers on Friday:

- Lufthansa shares climb as much as 4% after Europe’s largest carrier reported strong results and said it sees “significant” improvement in earnings in 2026.

- SFS rises as much as 6.1%, recovering some of this week’s losses, after the maker of components for the construction and automotive industries delivered better-than-expected results, according to analysts.

- ITV shares climb as much as 8.1% after Kepler Cheuvreux analyst Conor O’Shea raised his recommendation on the stock to buy from hold as he sees the weakness in advertising demand dissipating.

- Engineer IMI shares rise as much as 4.6% after the company delivered results ahead of expectations and announced a new £500 million buyback, supported by solid cash conversion.

- Zealand Pharma shares sink as much as 33%, the most on record, after mid-stage trial results for its experimental obesity shot being developed with Roche fell short of expectations.

- BE Semiconductor Industries shares fall as much as 12% as traders point to an article in Korean media on high-bandwidth memory.

- Infineon shares fall as much as 4% after UBS cut the recommendation on the chipmaker to neutral from buy, seeing limited upside to the firm’s margins and 2027 AI outlook, and growing inventory risk from a slowdown in China.

- Comet shares drop as much as 13% after the supplier of radio-frequency tools reported Ebitda for the full year that missed the average analyst estimate.

- Spie shares slide as much as 5.5% after the technical services provider delivered softer fourth-quarter organic growth across the majority of divisions, while consensus had already anticipated the improved mid-term margin goal, according to analysts at Jefferies.

- UCB drops as much as 2.9% after Morgan Stanley downgrades the stock to equal-weight from overweight, citing increasing concerns around the Belgian biopharmaceutical company’s growth story

In FX, the greenback advances with the Bloomberg Dollar Spot Index rising 0.2%.

In rates, treasury futures continue to be pressured, sitting on session lows into the early US session as WTI futures extend their climb through $86 barrel, higher by another 6% on the day. US yields cheaper by 2bp to 5bp across the curve in a bear flattening move with 5s30s spread down around 2bp on the day. US 10-year yields trade close to highs of the day around 4.17%, with gilts leading the selloff in bonds with UK two-year yields up 11 bps as traders pare bets on easing by the BOE this year. In Europe, bonds underperform further with front-end gilts cheaper by 12bp on the day. US session focus includes February nonfarm payrolls at 8:30am New York. Fed cut premium continues to fade out of front-end swaps, which now price in around 32bp of rate cuts for the year and the first full 25bp move priced out to the October meeting. In Europe, a full rate hike is now priced by the end of the year. Treasury auctions resume next week with 3-, 10- and 30-year sales for a combined $119 billion.

This week’s spike in Treasury yields is a sharp reversal from last month when they notched their sharpest drop in a year. Swaps now price between one and two Fed cuts for 2026 compared to as many as three a week ago. The dollar, meanwhile, has reclaimed its status as the ultimate haven as it headed for its best week in more than three years.

“Unless there can be some real political breakthrough that leads to a ceasefire, the dollar won’t be ready to resume a decline anytime soon,” ING Bank strategist Chris Turner wrote in a note. “The story will remain one of governments trying to handle the fallout of high energy prices, a negative for bond markets around the world.”

In commodities, Brent crude futures climb to a fresh high this week above $88 a barrel while European natural gas futures also rise after Qatar’s energy minister told the Financial Times the Middle East conflict will likely force Persian Gulf countries to halt energy exports.

Today’s US economic data slate includes February jobs report, January retail sales (8:30am), December business inventories (10am) and January consumer credit (3pm). Fed speaker slate includes Waller (7:30am), Daly (8:30am, 10:15am), Goolsbee (9:50am), Paulson (10:15am), Miran (11:30am), Collins (1:20pm) and Hammack (1:30pm, 3:10pm).

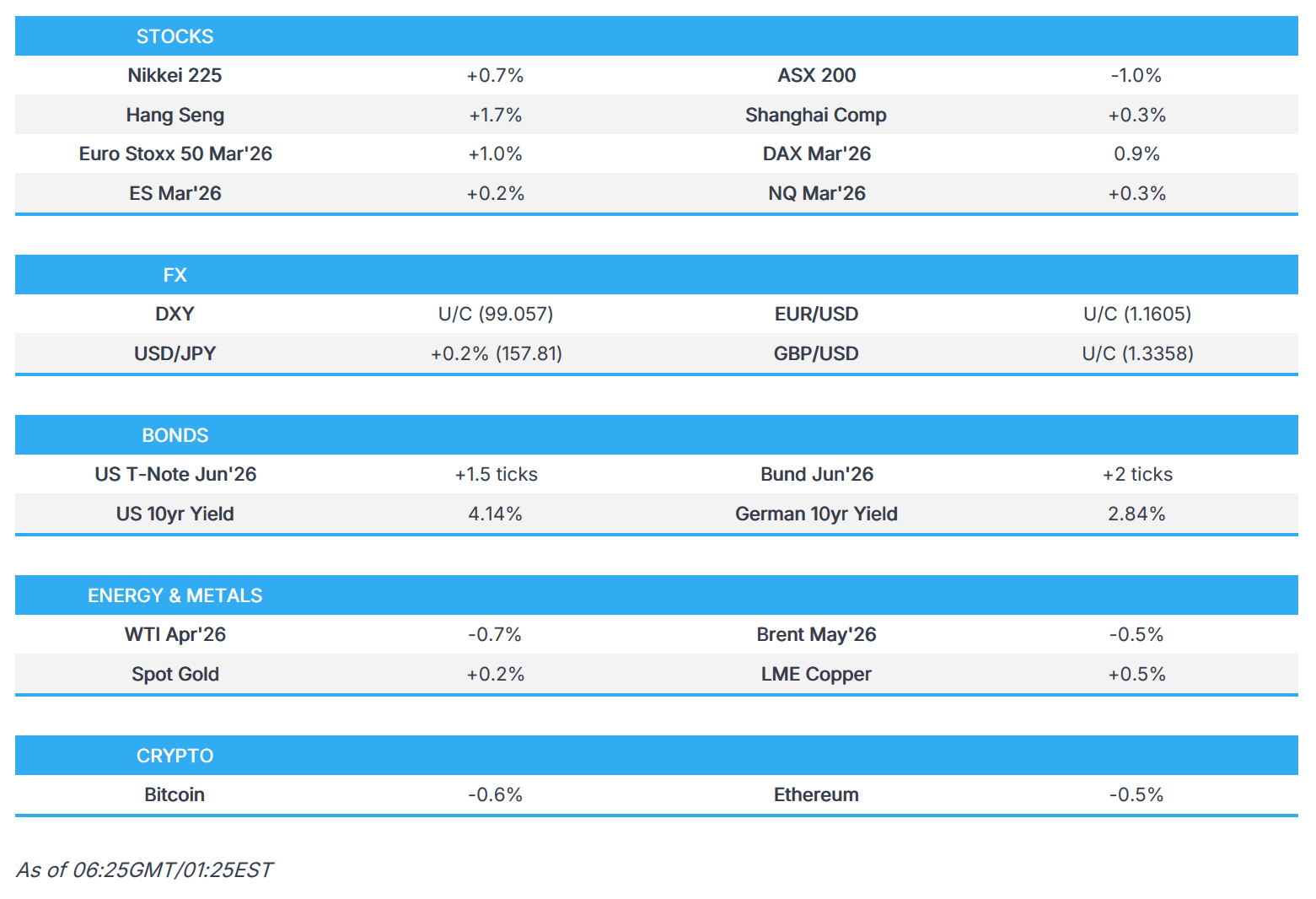

Market Snapshot

- S&P 500 mini -0.6%

- Nasdaq 100 mini -0.8%

- Russell 2000 mini -0.5%

- Stoxx Europe 600 -0.4%

- DAX -0.2%

- CAC 40 -0.3%

- 10-year Treasury yield +3 basis points at 4.17%

- VIX +0.4 points at 24.19

- Bloomberg Dollar Index +0.1% at 1205.77

- euro -0.2% at $1.158

- WTI crude +3.9% at $84.13/barrel

Top Overnight News

- U.A.E. Explores Freezing Iranian Assets to Punish Tehran for Attacks: WSJ

- Oil Soars as Iran War Threatens Long Energy Outage; WTI Crude Tops $85 a Barrel as War Paralyzes Hormuz Traffic: BBG

- Israeli Military Moving to ‘Next Phase’ of Iran Campaign: WSJ

- Iran barrage sweeps Mideast as Trump weighs in on succession: BBG

- Iran says countries have begun mediation efforts: WSJ

- Iran’s Attacks on the UAE Are Costing It Access to Vital Imports: BBG

- Tehran Is Fighting With Jets That Date Back to the Vietnam War: WSJ

- Trump on rising gas prices during Iran operation – ‘If they rise, they rise’: RTRS

- SoftBank Seeks Record Loan of Up to $40 Billion for OpenAI Stake: BBG

- Drone strike drives calls to end British military presence on Cyprus: RTRS

- Trump Faces Criticism From UAE Business Community Over Iran War: BBG

- Israel targets bunker beneath Khamenei’s compound in new wave of attacks: RTRS

- Israel’s Hezbollah attacks are likely to continue beyond Iran war: RTRS

- Turkey asks Britain’s MI6 to step up protection of Syria’s Sharaa: RTRS

- Wealthy Moscow cuts investment, revealing Russia’s deeper budget problems: RTRS

- Axel Springer Strikes $770 Million Deal for U.K.’s Daily Telegraph: WSJ

- Texas Republican Ends Re-Election Bid After Affair: AP

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded somewhat mixed following the risk-averse mood in the US as geopolitics continued to dominate headlines, and with participants also cautious heading into key US jobs data. ASX 200 was dragged lower as the heavy losses in miners, materials and resources sectors offset the gains in tech and telecoms, while recent higher energy prices stoke inflationary concerns and narrow the policy space for the RBA. Nikkei 225 traded indecisively and swung between gains and losses with very little fresh macro catalysts for Japan. Hang Seng and Shanghai Comp trade higher, albeit to varying degrees, with the mainland rangebound, while Hong Kong outperforms amid tech strength and as participants reflected on recent earnings from the likes of JD.com and Bilibili.

Top Asian News

- Japan’s Finance Minister Katayama said Japan is ready to take timely steps against the economic impact from the Iran conflict, adds Japan is not fully out of deflation. Japan is ready to act on market volatility while consulting international authorities. Bank of Japan’s monetary policy is focused on inflation and not on currency intervention. Wage gains are not BoJ’s direct target but is key to price stability.

- PBoC adviser Huang Yiping said China’s push to shift its economy towards consumer spending will take a long time, according to Bloomberg. Investors should dampen expectations for “aggressive” stimulus as the government doesn’t view it as a “crisis time”.

European bourses (STOXX 600 -0.1%) initially traded mixed, but now hold a strong negative bias as the risk tone soured. Little driving the latest downturn, but with focus remaining on the geopolitical situation. European sectors were initially mixed, but now hold a negative bias. Energy takes the top spot, buoyed by strength in underlying energy prices, whilst Industrials is lifted by Defence names. To the downside, Media lags, hampered by post-earning losses in UMG (-5.5%).

Top European News

- EU GDP Growth Rate YoY 3rd Est (Q4) Y/Y 1.2% vs. Exp. 1.3% (Prev. 1.4%, Low. 1.3%, High. 1.3%)

- EU Employment Change QoQ Final (Q4) Q/Q 0.2% vs. Exp. 0.2% (Prev. 0.2%)

- UK Halifax House Price Index YoY (Feb) Y/Y 1.3% vs. Exp. 0.9% (Prev. 1.1%, Rev. From 1%, Low. 0.5%, High. 0.9%).

- UK Halifax House Price Index MoM (Feb) M/M 0.3% vs. Exp. 0.3% (Prev. 0.8%, Rev. From 0.7%).

- Norwegian Manufacturing Production MoM (Jan) M/M -0.3% (Prev. -0.1%).

FX

- DXY is relatively flat with a mild upward bias after a session of gains on Thursday. Thursday’s action was spurred by a haven bid, and as yields climbed on firmer oil prices, in addition to well-received data ahead of NFP.

- EUR/USD returned below the 1.1600 handle after initially reclaiming the level in APAC trade, with downside exacerbated by the ongoing geopolitical and energy-related concerns, alongside the firming USD as traders flock to the haven. Little reaction to the rhetoric from ECB officials. Meanwhile, traders fully price in a 25bps ECB hike this year, Bloomberg reported. EUR/USD trades in a 1.1583-1.1621 range, within Thursday’s 1.1559-1.1647.

- GBP/USD is subdued amid the recent USD strength but remains tucked within yesterday’s 1.3297-1.3387 range. News flow for the UK remains light, but recent headlines centre around UK PM Starmer’s shift from initially refusing to assist US military operations against Iran to later granting access to British military bases for “limited” and “defensive” purposes.

- USD/JPY is firmer with the JPY the underperforming G10 amid a rise in US yields and given Japan’s exposure to energy imports. The pair traded sideways for most of the APAC session, given the indecisive mood in Japan; although, it gradually edged higher as domestic sentiment stabilised.

- Antipodeans are mixed, the AUD mildly outperforms amid gains in copper and gold prices and as recent inflationary concerns spurred some outside bets for a rate hike by the RBA this month. AUD/USD trimmed gains after hitting an intraday peak of 0.7047 (vs low 0.7015). NZD/USD hit a current low of 0.5881 (vs high 0.5916), with the 200 DMA (0.5876).

Central Banks

- BoJ Deputy Governor Himino said Japan is seeing inflation in terms of rising consumer prices, adds BoJ is keeping monetary conditions accommodative and gradually adjusting degree of monetary accommodation. Will continue to scrutinise market moves and their impact on the economy and prices. Rising import costs from a weak yen may affect inflation trends. BoJ policy is not aimed at FX rates, yet FX shifts impact inflation and the economy.

- ECB’s Escriva said it is highly unlikely the ECB touches rates at its next meeting.

- ECB’s Sleijpen said the ECB policy is still in a good place and data dependent.

- PBoC Governor said the central bank will flexibly use various monetary policy tools including interest rates and RRR cuts; PBoC said China has no intention to, not necessary to use FX rate to gain trade competitiveness.

Fixed Income

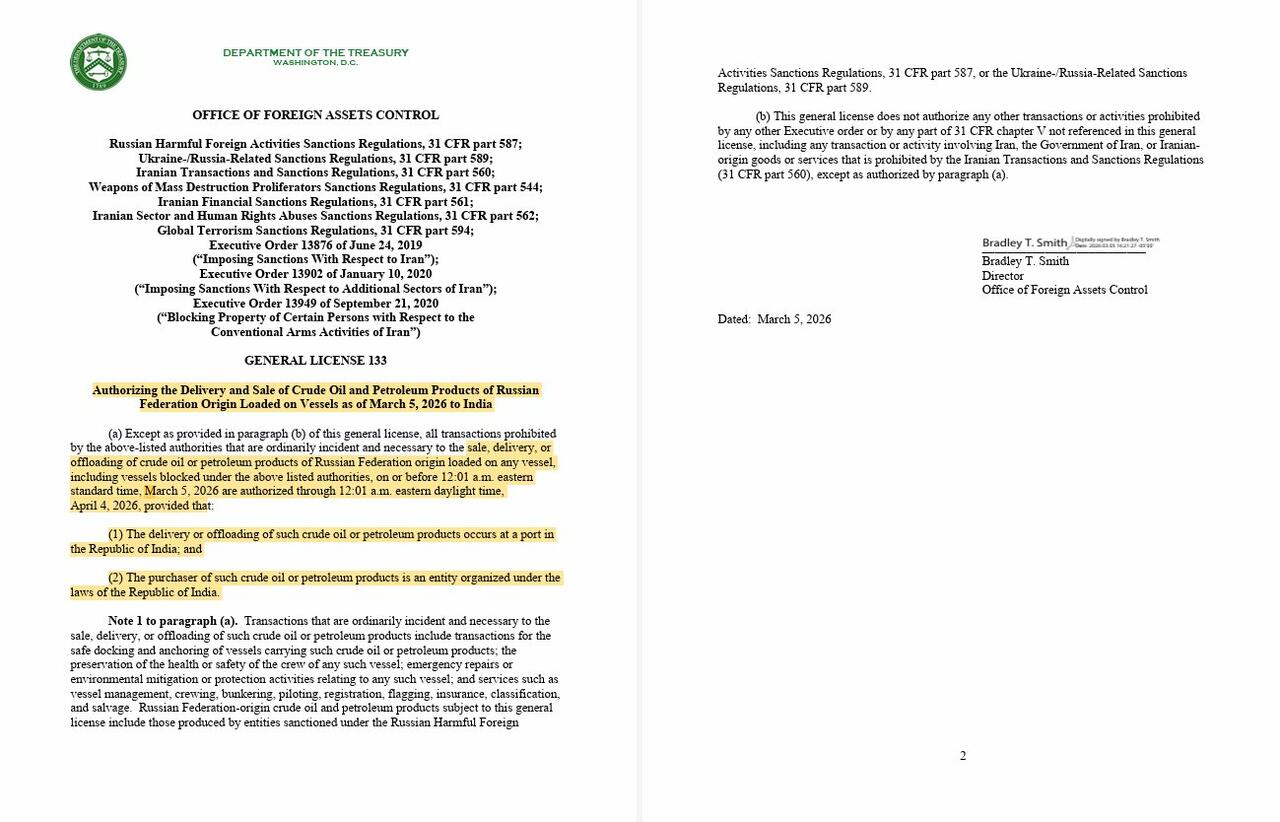

- USTs are lower. US paper spent much of the overnight session trading sideways, alongside weakness across the crude complex. However, as energy prices turned positive – the benchmark also dipped off best levels in the European morning. The geopolitical situation remains unchanged, with missiles being launched from both sides – but updates related to the Strait of Hormuz helped to improve sentiment, including; a) China is in talks with Iran to allow safe oil and gas passage through Hormuz, b) US allowed India to purchase Russian oil for 30-days. USTs now trade at the lower end of a 112-03 to 112-14+ range.

- Bunds follow peers, for the same reasons as above, and currently towards the bottom end of a 126.96 to 127.32 range. European newsflow has seen a few ECB speakers take to the wires, to generally touch on the Iran situation, whilst Escriva said it is “highly unlikely” that the ECB touches rates at it next meeting. From a yield perspective, the 10yr yield now trades at 2.868% (vs YTD high at 2.909%). Thereafter, 2.938%, a peak spurred by the mini-banking crisis surrounding the collapse of First Brands.

- Gilts underperform, lower by around 75 ticks and trades at the bottom end of a 90.43 to 91.25 range. Underperformance which can be explained by, a) net-importer of energy, b) BoE rate cut expectations entirely priced out for the year; pre-war pricing indicated a cut in either March or April. A lot of focus has been on the front-end Gilt situation, with the 2yr yield now surging beyond 3.90%, to now approach the 4% mark from mid-October 2025 – back where traders were increasingly sceptical of Chancellor Reeves and her Autumn Budget.

Commodities

- Crude benchmarks remain firmer, though are off their best levels seen yesterday, which saw Brent firmer by 4.9%, marking the highest close since the conflict between the US, Israel, and Iran began. As the conflict reaches its seventh day, there’s been little sign of a reprieve following comments by the Iranian Foreign Minister via NBC News that Iran is ready for a US ground invasion of the country, with further comments this morning via Al Arabiya where the FM said that Iran has no choice but to continue fighting. WTI and Brent are trading in the upper end of USD 78.24-82.93/bbl and 83.16-86.35/bbl, ranges respectively.