GOLD CLOSED CLOSED DOWN $70.55 TO $5162.90

ACCESS MARKET

XXX

GOLD $5176.95 3:30 PM)

SILVER: 85.05 3;30 PM)

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 5,229.700000000 USD

INTENT DATE: 03/10/2026 DELIVERY DATE: 03/12/2026

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL MARKETS 37

363 H WELLS FARGO SECURITI 200

555 C BNP PARIBAS SEC CORP 211

624 C BOFA SECURITIES 2

624 H BOFA SECURITIES 135 602

657 C MORGAN STANLEY 1738

661 C JP MORGAN SECURITIES 298

709 C BARCLAYS 502

737 C ADVANTAGE FUTURES 6

905 C ADM 19

TOTAL: 1,875 1,875

MONTH TO DATE: 7,500

JPMORGAN STOPPED 294/1875

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2026: 1875 CONTRACTs NOTICES FOR 187,500 OZ or 5.832 TONNES

total notices so far: 7500 contracts for 750,000 OR 23.328 tonnes)

SILVER NOTICES: 20 NOTICE(S) FILED FOR 0.100 MILLION OZ /

total number of notices filed so far this month : 6700 CONTRACTS (NOTICES) for 33.500 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A SMALL EXCHANGE FOR PHYSICAL TRANSFER TO LONDON JUMP OF 5 CONTRACTS OR 25,000 OZ/NEW STANDING REDUCES TO 38.945 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 27.095 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY TODAY’S 25,000 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON //NEW TOTAL STANDING REDUCES TO 38.945 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES FOLLOWED BY TODAY’S RECORD SETTING 11.026 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 29.129 TONNES/

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES FOLLOWED BY TODAY’S RECORD SETTING 11.026 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 29.129 TONNES OF GOLD./

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES FOLLOWED BY TODAY’S 11/076 TONNES QUEUE JUMP //NEW STANDING ADVANCES TO 29.129 TONNES/

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 98.79 TONNES//WILL BE VERY STRONG ISSUANCE THIS MONTH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE SIZED 1358 CONTRACTS OI TO 115,458 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 112,794 CONTRACTS THIS MONTH( MARCH 4/2026)

EFP ISSUANCE 562 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 562 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1358 CONTRACTS AND ADD TO THE 562 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1920 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $5,36

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 9.60 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $5.36

2.ASIAN AFFAIRS MARCH 10/2025

SHANGHAI CLOSED UP 10.30 PTS OR 0.25%

HANG SENG CLOSED DOWN 61.14 PTS OR 0.24%

Nikkei CLOSED UP 817.61 PTS OR 1.51%

//Australia’s all ordinaries CLOSED DOWN 0.65%

//Chinese yuan (ONSHORE) CLOSED UP 6.8701

/ OFFSHORE CLOSED UP AT 6.8711 Oil UP TO 86.69 dollars per barrel for WTI and BRENT UP TO 89.96 Stocks in Europe OPENED ALL DEEPLY IN THE RED

ONSHORE USA/ YUAN TRADING 6.8701 OFFSHORE YUAN TRADING UP TO 6.8711 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 9127 CONTRACTS UP TO 413,956 OI , RISING FROM DECADES ALL TIME LOW OF 404,829, WITH OUR HUGE GAIN IN PRICE OF $137..75 WITH RESPECT TO WEDNESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT HUGE PRICE GAIN FOR GOLD . AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2879).

WE HAD NO T.A.S. LIQUIDATION DURING TUESDAY’S TRADING. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO MASSIVELY LONG THIS MONTH AFTER A BRIEF PERIOD OF GOING NET SHORT AT THE BEGINNING OF FEBRUARY.

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MARCH CONTRACT MONTH!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW MOVING AWAY FROM ITS ALL TIME LOW POINT IN OI OF 404,829 AND FROM THIS POINT, OI WILL RISE BUT IT WILL BE EXTREMELY DIFFICULT FOR THE CROOKS TO FLEECE OUR NEWBIE SPEC LONGS. THE ALL TIME LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 1 TO 2 %.(SILVER IS AT 7%). WITH AN OI OF 413,956 THERE IS SOME ROOM FOR THE CROOKS TO RAID OUR NEWBIE SPECULATORS!

WE THUS HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 12,006 CONTRACTS (OR 37.34 TONNES) WITH THE HUGE GAIN IN PRICE, WEDNESDAY.

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. DURING THE MIDDLE OF THE MONTH. WE HAVE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE ARE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE THUS FAR FOR FEB NOW REMAINS AT SIX.(31.251 TONNES)

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MARCH:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUAY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: ZERO ISSUED SO FAR!

DETAILS ON OUR NEW MARCH COMEX CONTRACT MONTH//

IN TOTAL WE HAD A HUGE SIZED GAIN ON OUR TWO EXCHANGES OF 17,768 CONTRACTS WITH OUR HUGE GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MARCH/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS ANOTHER HUMONGOUS SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 16,212 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND IT IS IN FULL FORCE WITH TODAY’S RAID!

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH NO EXCHANGE FOR RISK ISSUANCE SO FAR.. BUT DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE:

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT MEGA MEGA HUGE RECORD SETTING QUEUE JUMP OF 11.076 TONNES//NEW STANDING FOR GOLD ADVANCES TO: 29.129 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING MARCH,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $137.75 )

WE HAD NO T.A.S. SPREADER LIQUIDATION TUESDAY // COMEX SESSION// WITH OUR GAIN IN PRICE .. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD FOR FEBRUARY’S ACTIVE DELIVERY MONTH (157 TONNES) AND ALSO MARCH’S STANDING OF 18+ TONNES.

TUESDAY NIGHT//WEDNESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO MARCH:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT MEGA MEGA HUGE QUEUE JUMP 11.026 TONNES// GOLD STANDING ADVANCES TO: 29.129 TONNES/

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $137.75

WE HAD A HUGE XXXX CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE

NET GAIN ON THE TWO EXCHANGES : 12,006 CONTRACTS OR 1,200,600 OZ OR 33.34 TONNES

INITIAL GOLD COMEX

MARCH 11

MARCH DELIVERY MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1875 CONTRACTS OR 187,500 OZ 5.832 TONNES OF GOLD |

| No of oz to be served (notices) | 1865 contracts 186,500 OZ 5.800 TONNES |

| Total monthly oz gold served (contracts) so far this month | 7500 notices 750,000 oz 23.328 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

DEPOSITS/CUSTOMER

0 ENTRY

0 entry

customer withdrawals:

0 ENTRIES

comex is draining of gold/.

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1

dealer to customer account: BRINKS

i) 113,139.369 OZ

3.519 TONNES REMOVED FROM DEALER TO CUSTOMER ACCT.

COMEX IS DRAINING GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

chaos inside the comex

AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH STANDS AT 3740 CONTRACTS FOR A GAIN OF 3098 CONTRACTS. WE HAD

447 CONTRACTS SERVED ON TUESDAY, SO WE GAINED A MEGA HUGE 3545 CONTRACTS OR AN ADDITIONAL 354,500 OZ WILL STAND FOR DELIVERY AT THE COMEX. THE TONNAGE EQUATES TO 11.026 TONNES AND THIS BECOMES THE NEW ALL TIME RECORD QUEUE JUMP. THIS IS A MASSIVE AMOUNT OF GOLD WILLING TO STAND AS CENTRAL BANKERS CLAMOUR FOR OUR ANCIENT METAL OF KINGS ON THIS SIDE OF THE PLANET

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 10,240 CONTRACTS DOWN TO 225,392 CONTRACTS. APRIL IS NOW THE NEW FRONT MONTH FOR DELIVERY OF GOLD. APRIL IS GENERALLY A VERY STRONG DELIVERY MONTH

MAY GAINED 82 CONTRACTS UP TO AN OI OF 851.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI ROSE BY A STRONG 15,3111 CONTRACTS UP TO AN OI OF 114,938

We had 1875 contracts filed for today representing 187,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1875 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 298 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAR. /2026. contract month, we take the total number of notices filed so far for the month (7500) to which we add the difference between the open interest for the front month of MAR (3740 CONTRACTS) minus the number of notices served upon today 1875 x 100 oz per contract) equals 936,500 OZ OR (29.129 Tonnes of gold)

thus the INITIAL standings for gold for the MAR contract month: No of notices filed so far (7500 x 100 oz +we add the difference for front month of MAR (3740 OI} minus the number of notices served upon today (1875 x 100 oz) which equals 936,500 OZ OR 29.129 TONNES//

new total of gold standing in MAR is 29.129 TONNES//

TOTAL COMEX GOLD STANDING FOR MARCH 29.129 TONNES TONNES WHICH IS NOW MEGA HUGE FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF MARCH.

confirmed volume TUESDAY confirmed 237,025 fair

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,717,146.01 oz 53.410 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,717,146.010 tonnes oz 52.58 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 32,720,708.541 oz

TOTAL REGISTERED GOLD 16,725,380.804 or 520.229 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 15,995,327.787 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 15,008,234 oz ((REG GOLD- PLEDGED GOLD)=

466.819 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER COMEX

MARCH DELIVERY MONTH

MARCH 11 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) out of cnt 603,147.620 OZ ii) Out of Delaware 5999.850 oz iii) Out of JPMorgan: 159,483.220 oz total withdrawal: 768,640.670 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Stonex: 20,186.220 oz total dealer deposit; 02,186.220 oz xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT ENTRIES: 0 oz |

| No of oz served today (contracts) | 20 CONTRACT(S) ( 0.100 MILLION OZ |

| No of oz to be served (notices) | 1089 Contracts (5.445 MILLION oz) |

| Total monthly oz silver served (contracts) | 6690 contracts 33.500 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRIES: 0

xxxxxxxxxxxxxxxxxxxxxxxxx

deposits into dealer account: 1

1 ENTRY

i) Into Stonex: 20,186.220 oz

total dealer deposit; 20,186.220 oz

withdrawals: customer side/eligible

3 entries

i) out of cnt 603,147.620 OZ

ii) Out of Delaware 5999.850 oz

iii) Out of JPMorgan: 159,483.220 oz

total withdrawal: 768,640.670 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 1//all dealer to customer acct

a) Brinks: 136,505.132 oz

total removal from the registered silver to eligible silver: 1,524,812.662 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 78.347 MILLION OZ//.TOTAL REG + ELIGIBLE. 344.541 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH /2026 OI: 1109 OPEN INTEREST CONTRACTS FOR A LOSS OF 70 CONTRACTS.

WE HAD 65 NOTICES FILED ON TUESDAY SO WE LOST A TINY 5 CONTRACTS THROUGH AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON OR AN ADDITIONAL 25,000 OZ OF SILVER WILL NOT TRY FOR DELIVERY OVER HERE AS THEY TRY THEIR LUCK ON THE OTHER SIDE OF THE POND. THIS REDUCES THE AMOUNT OF SILVER WILLING TO STAND AT THE COMEX (NEW YORK)

APRIL, THE NEW FRONT MONTH SAW A GAIN OF 29 CONTRACTS UP TO 1456 CONTRACTS

MAY SAW A 1004 CONTRACT GAIN UP TO 78,474 CONTRACTS.

JUNE SAY A GAIN OF 23 CONTRACTS UP TO 273 OI CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 20 or 0.110 MILLION oz

CONFIRMED volume; ON TUESDAY 52,299 fair+++//

AND NOW MARCH. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 6700 X5,000 oz = 33.500 MILLION oz

to which we add the difference between the open interest for the front month of MARCH (1109) AND the number of notices served upon today (20)x (5000 oz)

Thus the standings for silver for the MARCH 2026 contract month: (6700)Notices served so far) x 5000 oz + OI for the front month of MARCH(1109) minus number of notices served upon today (20 )x 5000 oz equals silver standing for the FEB..contract month equating to 38.945 MILLION OZ.

NEW STANDING: 38.945 MILLION OZ WHICH IS STILL LOWISH FOR A GENERALLY HUGE DELIVERY MONTH OF MARCH.

New total standing: 38.945 million oz.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are ONLY 78.347 million oz of registered silver

JPMorgan as a percentage of total silver: 152.021/344.541.million: 44.12%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

MAR 9/2026/WITH GOLD DOWN $53.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.573 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1073.321 TONNES

MAR 6/2026/WITH GOLD UP $77.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 5.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1075.894 TONNES

MAR 5/2026/WITH GOLD DOWN $49.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 18.032 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1081.038 TONNES

MAR 4/2026/WITH GOLD UP $9.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.545 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1099.07 TONNES

MAR 3/2026/WITH GOLD DOWN $188.75 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.35 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101.36 TONNES

MAR 2/2026/WITH GOLD UP $71.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101,13 TONNES

FEB 27/2026/WITH GOLD UP $52.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.90 TONNES

FEB 26/2026/WITH GOLD DOWN $30.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 11.45 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.62 TONNES

FEB 25/2026/WITH GOLD UP $48.40 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL WITHDRAWAL OF 0.300 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1086.17 TONNES

FEB 24/2026/WITH GOLD DOWN $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE PAPER DEPOSIT OF 7.72 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1086.47 TONNES

FEB 23/2026/WITH GOLD UP $148.25 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 20/2026/WITH GOLD UP $79.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 19/2026/WITH GOLD DOWN $9.00 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 18/2026/WITH GOLD UP $102.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 17/2026/WITH GOLD DOWN $136.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ /// ///INVENTORY RESTS AT 1077..04 TONNES

FEB 13/2026/WITH GOLD UP $94.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.140 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.18 TONNES

FEB 12/2026/WITH GOLD DOWN $143.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.000 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.32 TONNES

FEB 11/2026/WITH GOLD UP $63.65 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.34 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.32 TONNES

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

GLD INVENTORY: 1073/565 TONNES, TONIGHTS TOTAL

SILVER

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

MAR 6 WITH SILVER UP $2.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 5.526 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508,287 MILLION OZ

MAR 5 WITH SILVER DOWN $0.98 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.097 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 512.726 MILLION OZ

MAR 4 WITH SILVER DOWN $0.21 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.545 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 513.813 MILLION OZ

MAR 3 WITH SILVER DOWN $5.27 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2/899 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 511.268 MILLION OZ

MAR 2 WITH SILVER DOWN $3.87 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.352 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 514.167 MILLION OZ

FEB 27 WITH SILVER UP $5.54 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 0.544 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 517.519 MILLION OZ

FEB 26 WITH SILVER DOWN $4.05 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 0.906 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 516.975 MILLION OZ

FEB 25 WITH SILVER UP $3.43 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 8.923 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 517.881 MILLION OZ

FEB 24 WITH SILVER UP $0.55 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 10.056 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 508.958 MILLION OZ

FEB 23 WITH SILVER UP $4.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT WITHDRAWAL OF 0.951 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 498.902 MILLION OZ

FEB 20 WITH SILVER UP $4.85 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.035 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.853 MILLION OZ

FEB 19 WITH SILVER DOWN $0.23 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 5.798 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 502.888 MILLION OZ

FEB 18 WITH SILVER UP $4.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 11.325 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508.686 MILLION OZ

FEB 17 WITH SILVER DOWN $4.39 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 4.253 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 515.753 MILLION OZ

FEB 13 WITH SILVER UP $2.35 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.994 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 520.011 MILLION OZ

FEB 12 WITH SILVER DOWN $8.78 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 635,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 522.005 MILLION OZ

FEB 11 WITH SILVER UP $3.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 815,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 521.370 MILLION OZ

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

CLOSING INVENTORY 503.305 MILLION OZ OF SILVER..

.2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

JESSE COLUMBO

This is a post from Jesse Colombo’s The Bubble Bubble Report—a bestselling newsletter focusing on precious metals investing and global economic risks. We specialize in detailed reports and analyses.

Why It’s Still Early for Silver

Despite silver’s powerful gains over the past couple of years, it is still only about 20% of the way through its bull market based on historical cycles, and I believe this one will be the biggest yet.

| Jesse ColomboMar 10∙Paid |

A major focus of this newsletter is identifying where the bull market in precious metals and mining stocks currently stands in the cycle. Based on extensive data, my view is that this bull market remains in its early stages and still has considerable room to run in both time and price.

A few days ago I published a report applying this framework to gold, which was well received. In today’s report, I apply the same methodology to silver, though I recommend reading the original gold report as well for additional context.

Practically everyone is aware that silver has been on a major run over the past year, surging as much as 320% at its most recent peak in late January and still up 206% despite the sharp pullback. This bull market in silver is exactly what I anticipated two years ago, when the metal was still unpopular and trading at just $28 an ounce.

Now that silver has had a powerful run, many analysts and investors, most of whom never foresaw the bull market in the first place, are quick to stick a fork in it, claiming it was a bubble that has now burst and that it is all downhill from here.

My response, however, is simple: they have it all wrong. A powerful secular bull market began only two years ago, and based on history it should last at least a decade. That is what I intend to demonstrate in this report.

My thesis is based on the principle that it is more meaningful to compare gains in precious metals to other assets rather than viewing them solely in nominal price terms, since nominal prices fail to account for the substantial inflation that erodes the dollar’s value over long periods of time.

For example, by comparing the price of silver to benchmarks such as the Consumer Price Index (CPI), the money supply, the national debt, or the stock market, you can gain a much clearer sense of whether it is truly overvalued or undervalued. Looking at the nominal price alone cannot provide that insight. Silver at $30 could be overvalued, while $100 silver could be extremely cheap, depending on how it stands relative to other assets.

One of the most important benchmarks is the U.S. stock market because stocks and precious metals have a long-established relationship in which capital rotates between the two over extended periods, typically lasting at least a decade. This relationship is the focus of today’s report.

To illustrate this phenomenon, I created the logarithmic chart below of the silver-to-Dow ratio going back to the late 1920s. I use the Dow because it has the longest history of any major U.S. stock index.

When the ratio is increasing (periods when there are silver-colored trendlines), silver is gaining in price relative to stocks. When the ratio is decreasing (periods when there are green-colored trendlines), stocks are gaining relative to silver. A new cycle begins when a major generational trendline, either silver or green, is broken, triggering a reversal of the conditions that defined the previous cycle.

When stocks are gaining relative to silver, also known as a secular bull market in stocks, capital flows en masse into equities and out of silver. In this environment, stocks are the place to be while silver becomes a laggard investment with a high opportunity cost because it keeps investors out of higher-performing stocks. During such secular bull markets, pullbacks and corrections prove to be temporary and present good buying opportunities, at least until a generational trendline is eventually broken.

Once a green trendline is eventually broken to the upside, however, that signifies the start of a new secular bull market in silver and a secular bear market in stocks as capital flows out of stocks and into both silver and gold. During such precious metals bull markets, pullbacks and corrections prove temporary and present good buying opportunities, at least until a generational trendline is eventually broken, starting the cycle all over again.

As the chart below shows, secular bull markets in silver occurred from the early 1970s to the early 1980s and again from the early 2000s to the early 2010s. The most recent cycle began in April 2024, when the silver-to-Dow ratio broke above the green trendline that began in 2011.

That breakout signals that capital is now flowing out of stocks and into both silver and gold. This secular bull market is barely two years old and it should continue at least as long as the prior ones did, which means a decade or longer.

The chart below compares the performance of silver and the Dow over the past four years. It shows that the two tracked each other closely until early 2024, when silver began to significantly outperform the U.S. stock market as its latest secular bull market emerged following eleven years of stagnation:

I previously mentioned the past two secular bull markets in silver, which occurred from the early 1970s to the early 1980s and again from the early 2000s to the early 2010s, and I noted that a third one began only two years ago in April 2024.

I now want to explore that topic in greater detail, specifically by measuring the prior two bull markets in terms of their length and magnitude of gains and then comparing the current secular bull market to see where it stands relative to those earlier cycles and what that tells us about how mature it is.

Based on the silver-to-Dow ratio breakout methodology I previously explained, the first modern secular bull market in silver began in May 1973 and ended in June 1981, lasting a total of 97 months, or a little over 8 years. During that time, the silver-to-Dow ratio surged 2,043% from its trendline breakout to its peak. While that period delivered stellar performance for precious metals, the stock market experienced one of its worst stretches of stagnation in decades.

The second modern secular bull market in silver began in September 2001 and ended in April 2013, lasting a total of 139 months, or roughly 11.5 years. During that time, the silver-to-Dow ratio surged 775% from its trendline breakout to its peak. In an echo of the 1970s, precious metals boomed during that period while stocks languished as capital flowed out of equities and into precious metals following the dot-com bust.

Finally, we arrive at the third modern secular bull market in silver, which began in April 2024 and is therefore only 23 months old, a mere baby compared to the first secular bull market that lasted 97 months and the second that lasted 139 months. If you average the last two secular bull markets in silver, they lasted 118 months, or just under 10 years. In contrast, the current bull market has lasted only about 19% of that average, which means it is still in its infancy.

For further confirmation that the current bull market is still quite young, the silver-to-Dow ratio has gained only 255% so far, which pales in comparison to the 2,043% surge of the first secular bull market and the 775% increase of the second. If you average the silver-to-Dow ratio’s performance during the last two secular bull markets, it increased 1,409%. By that measure, the current secular silver bull market is only 18% of the way there!

Knowing just how young the current silver bull market is, even without considering other important factors such as the runaway global debt situation and the unsustainability of fiat/paper money, is one of the reasons why I have so confidently brushed off fears surrounding every pullback in precious metals over the past two years. I know they have much further to go, and I believe that will remain true even several years from now. I fully expect this bull market to last more than a decade, ultimately taking silver to $500+ an ounce and gold to $20,000+ an ounce.

Although I compared silver’s current secular bull market with previous ones and showed that it has much further to run if it merely matches their average length and magnitude, I believe this bull market will actual exceed the prior two.

There are several reasons for this, including the fact that the U.S. stock market is in the largest bubble in its history, which represents a massive pool of additional capital that will eventually rotate into precious metals and drive them far higher than in previous cycles. For a fuller explanation of this argument, I recommend reading my gold report from a few days ago.

One reliable indication that the U.S. stock market is in a bubble is the total U.S. stock market capitalization-to-GDP ratio shown in the chart below, which billionaire investor Warren Buffett once called his “favorite indicator.” He warned that when this ratio rises above 200, investors are “playing with fire.”

Alarmingly, in recent months the ratio has exceeded 200 and is indicating that the current stock market bubble is even larger than the late-1990s dot-com bubble. I expect this bubble to end in a severe bear market, which will prove highly beneficial for precious metals.

Another reason I have been so bullish on silver is the enormous five-decade-old cup and handle pattern that finally broke out in November. The breakout indicates that this bull market is only getting started and that silver should rise to hundreds of dollars per ounce based on the sheer magnitude of the pattern.

This recent breakout, and its extremely bullish implications, is one of the many reasons I am not concerned about the recent volatility in silver.

Once you are aware of how young silver’s secular bull market is, as I showed earlier in this report, and how large the U.S. stock market bubble is, it is not far-fetched to believe that silver will soar to hundreds of dollars an ounce now that it has broken out of its cup and handle pattern. All of the stars have aligned for that outcome.

To summarize, although many conventionally minded analysts have been quick to declare silver’s bull market over after only two years, a look at past cycles shows that it is only about one fifth complete if it merely follows its historical pattern. That means the bull market is still extremely young.

On top of that, I believe this cycle will prove far more powerful and extensive than any seen in the past, which is why I have no interest in selling my silver anytime soon. In addition, short-term volatility does not faze me because I know where silver is ultimately headed, and that is much higher from here.

To learn more about why the precious metals bull market is only getting started, I recommend reading my other recent reports:

- Here’s When I’ll Sell My Gold & Silver

- The Next Fuel for Gold’s Bull Market

- Proof That Precious Metals Are Just Getting Started

Disclaimer: the information provided in The Bubble Bubble Report and related content is for informational and educational purposes only and should not be construed as investment, financial, or trading advice. Nothing in this publication constitutes a recommendation, solicitation, or offer to buy or sell any securities, commodities, or financial instruments.

All investments carry risk, and past performance is not indicative of future results. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions. The author and publisher disclaim any liability for financial losses or damages incurred as a result of reliance on the information provided.

3.CHRIS POWELL AND HIS GATA DISPATCHES:

4. ANDREW MAGUIRE AND LIVE FROM THE VAULT PODCASTS

KINESIS: PODCAST NO 262/ANDREW WITH BILL HOLTER

5. COMMODITY REPORT//COAL

ASIAN AFFAIRS MARCH 11/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 10.30 PTS OR 0.25%

HANG SENG CLOSED DOWN 61.14 PTS OR 0.24%

Nikkei CLOSED UP 817.61 PTS OR 1.51%

//Australia’s all ordinaries CLOSED DOWN 0.65%

//Chinese yuan (ONSHORE) CLOSED UP 6.8701

/ OFFSHORE CLOSED UP AT 6.8711 Oil UP TO 86.69 dollars per barrel for WTI and BRENT UP TO 89.96 Stocks in Europe OPENED ALL DEEPLY IN THE RED

ONSHORE USA/ YUAN TRADING 6.8701 OFFSHORE YUAN TRADING UP TO 6.8711 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.8701

OFFSHORE YUAN: UP TO 6.8711

1.HANG SANG DOWN 61.14 POINTS OR 0.24%

2. Nikkei closed UP 817.61 PTS OR 1.51%

WEST TEXAS INTERMEDIATE OIL UP 86.69

BRENT; 89.96

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 98.91 /// EURO RISES TO 1.1612 UP 6 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +2.164/ DOWN 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.35… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.445 UP 2 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: 6.8701 (UP) AND OFFSHORE: UP AT 6.8711

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.8709 Italian 10 Yr bond yield UP to 3.600 SPAIN 10 YR BOND YIELD UP TO 3.333

3i Greek 10 year bond yield UP TO 3.547

3j Gold at $5183.50 Silver at: 86.69 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 4/100 roubles/79.01

3m oil (WTI) into the 86 dollar handle for WTI and 89 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.82 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.165% DOWN 1 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.445 UP 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7785 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9041 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.164 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.801 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.592 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 44.08 UP 3 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.6190 UP 6 PTS

30 YR UK BOND YIELD: 5.293 UP 6 BASIS PTS

10 YR CANADA BOND YIELD: 3.410 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.953 UP 3 BASIS PTS.

1a New York Opening report

l b European opening report

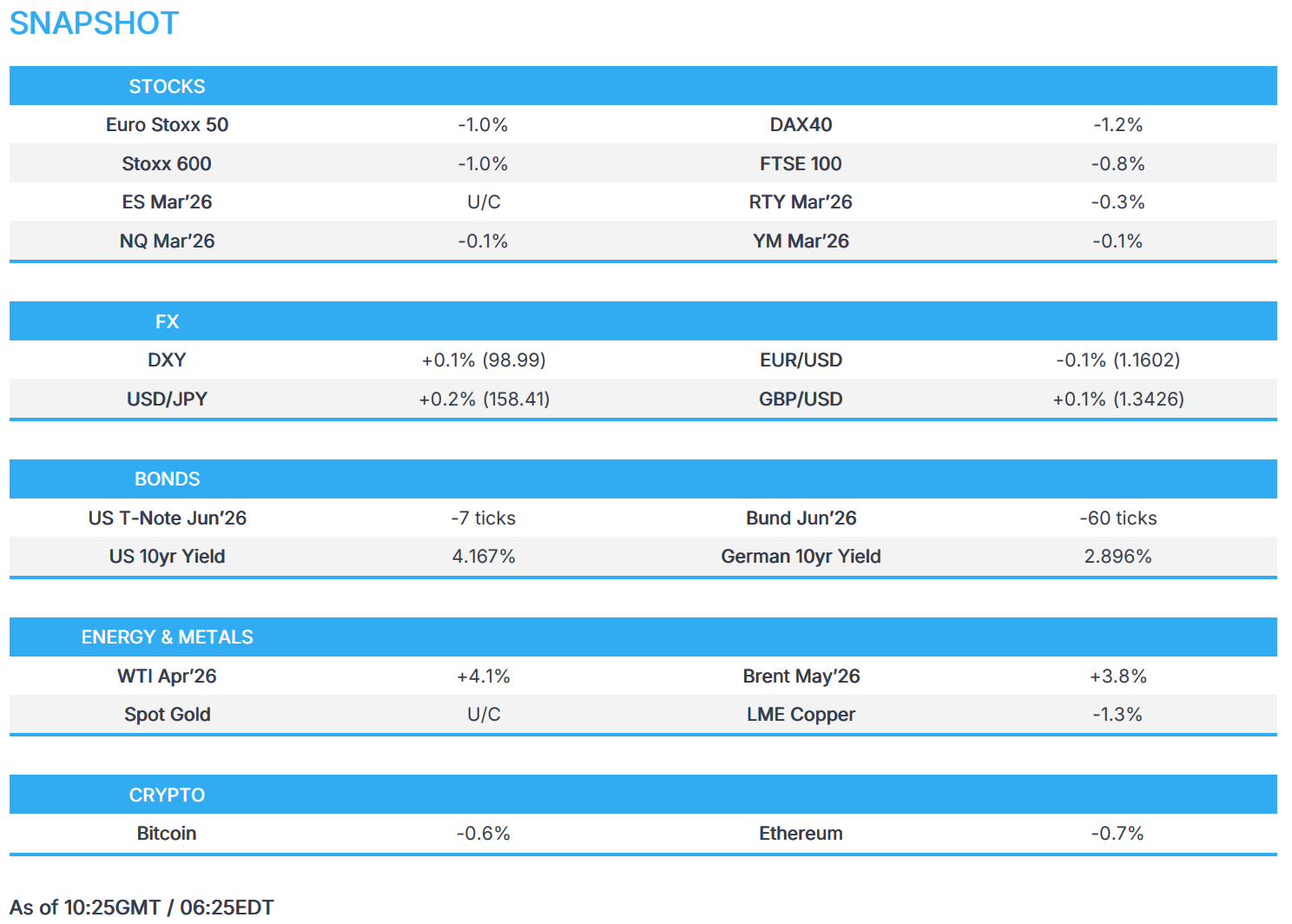

IEA set to announce oil reserve recommendation; DXY flat heading into CPI – Newsquawk US Market Open

Wednesday, Mar 11, 2026 – 06:45 AM

- The IEA has proposed the largest ever release of oil from its strategic reserves, with Bloomberg reporting around 300-400mln barrels to be released.

- Separate reporting stated that the volume in the first month of the release of oil reserves would exceed 100mln barrels.

- Crude rises as geopolitics show no real signs of abating; copper falls as sentiment deteriorates.

- European equities entirely in the red, Rheinmetall disappoints despite increased need for defence; US equity futures continue to consolidate.

- DXY flat heading into CPI, AUD outperforms as more banks forecast a hike next week.

- Hawkish ECB speak drives EGBs lower; packed UK agenda ahead.

- Looking ahead, highlights include US CPI (Feb), OPEC MOMR, IEA recommendation, G7 call. Speakers include ECB’s Schnabel & Fed’s Bowman, Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -1.0%) are entirely in the red, as the Iran conflict intensifies. Losses in the IBEX 35 (-0.4%) have been limited after positive Inditex (+0.8%) earnings, which beat Q4 EBIT estimates and boosted capex following a strong start to 2026. The DAX 40 (-1.2%) underperforms after Rheinmetall (-6.2%) missed FY net income and guided softer 2026 revenue than analysts expected.

- European sectors are broadly weaker across the board, as Energy (+0.3%) continues to gain. Real Estate (-1.3%) and Financial Services (-1.3%), alongside Industrial Goods and Services (-1.8%), sit at the bottom of the pile, with higher yields and risk tone weighing on the sectors.

- US equity futures (ES U/C, NQ -0.1%, RTY -0.3%) are posting modest losses. In pre-market trade, Oracle (+10.5%) gains after-hours. The Co. reported earnings and revenue above expectations, and raised its FY revenue guidance as cloud revenue surged.

- Rheinmetall (RHM GY) – FY 2025 (EUR): Net Income 696mln (exp. 1.15bln), Revenue 9.9bln (prev. 9.75bln Y/Y), Backlog 63.8bln (prev. 49.9bln Y/Y). Raises dividend to EUR 11.50/shr (prev. EUR 8.10/shr).Guides initial FY26 Revenue 14-14.5bln (exp. 15bln), Op. Margin 19% (exp. 19.1%).

- Oracle (ORCL) – Q3 2026 (USD): Adj. EPS 1.79 (exp. 1.70), Revenue 17.2bln (exp. 16.92bln). Raises FY27 revenue view to USD 90bln (exp. 86.37bln) and said it expects to comfortably meet and likely exceed its FY27 revenue growth forecast.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is choppy this morning; currently trading around the unchanged mark, within a narrow 96.69-99.07 range. Little fresh from a European perspective, as focus remains on newsflow out of Iran. As it stands, the current conflict is showing few signs of ending, with reports now suggesting that Iran is taking steps to lay mines in the Strait of Hormuz. On the energy front, the IEA Governing Board is meeting today, whilst a separate G7 discussion on energy coordination is also scheduled for 14:00 GMT today. It was recently reported that the IEA proposed a 300-400mln barrel release of stockpiles – sources suggest that, should there be no objections, it could be announced as soon as today. Focus later will also be on US CPI, though it may lack signalling capacity given the current geopolitical situation.

- The Aussie extends on recent outperformance, as more banks now expect the RBA to hike rates at next week’s meeting. NAB and Westpac are the latest banks seen supporting a hike, joining the likes of Goldman Sachs and Bank of America. Delving into Westpac briefly, the bank previously forecast a hike in May, but the analysts now believe that the RBA will be “compelled to react” to the recent strength in oil prices. AUD/USD currently trades towards the upper end of a 0.71154 to 0.7185 range.

- Other G10s are trading modestly on either side of the unchanged mark vs the USD. The Loonie posts mild gains, given today’s strength in oil prices, whilst the JPY is the slight laggard, joined by the EUR. USD/JPY is venturing back into the touted “intervention zone”, beyond the 158.00 mark – though desks question the efficacy of intervening as the Iran war continues. GBP is essentially flat, awaiting cues from the Treasury Committee, which will question the Chancellor Reeves on the Spring Statement. BoE’s Breeden is also set to speak.

- For the EUR, currently trades just above the 1.1600 mark, within a 1.15904-1.1645 range. Today, there was a slew of ECB speakers, with particular focus on Kazimir who suggested that a rate hike on Iran may be closer than thought. This spurred some very modest upside in the EUR at the time, but was ultimately short-lived, given that he stated there is no reason to move rates at the next meeting.

FIXED INCOME

- APAC trade for fixed income was for the most part rangebound, with USTs and Bunds holding a handful of ticks in the red. JGBs also opened under pressure, with downside of 20 ticks at most. However, the move proved short lived as strong demand at the 5yr JGB tap underpinned the benchmark and lifted it to a 131.98 high, just shy of yesterday’s 132.01 best.

- While relatively contained at first, EGBs came under renewed pressure early doors following ECB speak and a further uptick in energy benchmarks. Sending Bunds to a 126.55 trough over the course of the morning. On the former, Kazimir said an Iran-related rate hike could be closer than thought, though clarified that there is no reason to act in March. Near term market pricing has seen a very slight hawkish move this morning, but more pertinently end-2026 pricing implies around 25bps of tightening.

- In geopols, the UKMTO update seemingly spurred another leg higher in the crude space, with additional impetus potentially coming from the ongoing reporting around but lack of action on a reserve release.

- Moving to Gilts, the benchmark opened lower by over 50 ticks and has since slipped another 30 or so to a 90.27 base. Currently lagging, posting downside of 78 ticks vs 63 for Bunds. Action is very much occurring in tandem with the EGB move. Additionally, the UK has a packed agenda with Chancellor Reeves discussing her Spring Statement with the TSC, the release of Mandelson-related files by the government (around 12:30GMT) and then an appearance from BoE’s Breeden, however this is scheduled to be on stablecoins.

- Vnet (VNET) , China’s largest data centre operator, is considering a dollar bond sale to fund expansion, Bloomberg reported citing sources.

- Amazon (AMZN) opens books on eight-part EUR denominated bond offering.

- Japan sold JPY 1.9tln 5yr JGBs; b/c 3.69x (prev. 3.10x), average yield 1.633% (prev. 1.640%).

- Australia sold AUD 1bln 4.25% October 2036 bonds, b/c 3.87, avg. yield 4.9002%.

COMMODITIES

- WTI and Brent front-month futures have been grinding higher since early European hours following a choppy APAC session and the declines seen during the prior session. Yesterday, there was a bout of selling pressure after US Energy Secretary Wright mistakenly posted that the US Navy escorted an oil tanker through the Strait of Hormuz, although oil then pared some of the losses as the post was deleted shortly after, and the White House confirmed that this was false.

- Note, the IEA Governing Board is meeting today, whilst a separate G7 discussion on energy coordination is also scheduled for 14:00 GMT today. It was recently reported that the IEA proposed a 300-400mln barrel release of stockpiles – sources suggest that, should there be no objections, it could be announced as soon as later today.

- Spot gold holds an upward bias on either side of the USD 5,200/oz level, with the precious metal kept afloat alongside the recent easing in oil price pressures, although DXY has clambered off worst levels as eyes remain on flows in the Strait of Hormuz. A deterioration in sentiment in early European hours cushions downside for the yellow metal for now, which resides in a narrow USD 5,175.35-5,223.38/oz at the time of writing.

- Copper futures traded rangebound overnight but then slipped in early European hours amid a broader deterioration of sentiment as the Iranian war shows no signs of ending despite recent commentary from US President Trump. 3M LME copper is back under USD 13,000/t and resides towards the bottom end of a USD 12,993.00-13,151.53/t at the time of writing.

- G7 statement said the group is vigilantly monitoring the energy market, and G7 supports in principle the use of strategic oil reserve.

- IEA to recommend the release of strategic reserves, according to sources; volume in the first month would reportedly exceed 100mln barrels.

- IEA reportedly proposed oil stockpile release of around 300-400mln barrels, according to Bloomberg; decision is possible later on Wednesday, said a source.

- IEA has proposed the largest ever release of oil from strategic reserves to bring down the price of crude, according to WSJ. “Countries would decide Wednesday whether to release oil stocks in an attempt to tame crude prices”. “The release would exceed the 182 million barrels of oil that IEA member countries put onto the market in two releases in 2022 when Russia launched its full-scale invasion of Ukraine”.

- As part of a potential 400mln barrel IEA crude release, Germany would release around 19.5mln barrels, Handelsblatt reports citing sources; equating to around 20% of Germany’s reserves

- Black Sea CPC blend oil exports were reportedly revised down to around 1.4-1.5mln BPD for March (prev. 1.7mln BPD)

- White House reportedly believes it can “withstand a brief spike in oil prices — for as many as four weeks… before the political hit does lasting damage”, according to Politico citing sources.

- Iraq’s oil ministry has sent a letter to the Kurdistan regional government for the export of at least 100k BPD via the Kurdistan pipeline to Turkey’s Ceyhan, according to oil officials.

- EU Commission President von der Leyen said Europe’s dependency on fossil fuels have cost it EUR 3bln in extra costs in the first 10 days of the Iran war, returning to Russian fossil fuels in the current crisis would be a strategic blunder. EU is preparing options to lower energy prices, which include better use of purchase power agreements and CFDs, state aid measures, gas price subsidies or caps.

- Maersk (MAERSKB DC) CEO tells the WSJ that 10 ships are trapped in the Persian Gulf and would need at least 10 days to resume normal operations if a ceasefire was to occur.

- Glencore (GLEN LN) workers reportedly set to conduct a strike at Australian copper refinery, according to Bloomberg.

TRADE/TARIFFS

- Ireland Prime Minister is planning to talk about EUR 6.1bln in investment into the US during the visit on March 17th, WSJ reported.

NOTABLE EUROPEAN HEADLINES

- European Commission draft Citizens’ Energy Package recommends concrete measures to lower household energy prices, Handelsblatt reported; aim is to lower electricity taxes to a minimum.

NOTABLE EUROPEAN DATA RECAP

- German Inflation Rate YoY Final (Feb) Y/Y 1.9% vs. Exp. 1.9% (Prev. 2.1%, Low. 1.9%, High. 1.9%).

- German Inflation Rate MoM Final (Feb) M/M 0.2% vs. Exp. 0.2% (Prev. 0.1%).

- Spanish Retail Sales MoM (Jan) M/M 0.1% (Prev. -0.8%).

- Spanish Retail Sales YoY (Jan) Y/Y 4.0% (Prev. 2.9%).

CENTRAL BANKS

- ECB’s de Guindos said risks are tilted to the downside, macroeconomic projections will be much more complicated now.

- ECB’s Kazaks said the ECB could act if war raises inflation expectations.

- ECB’s Kazimir said a rate hike on Iran may be closer than thought; no reason to act at next week’s meeting.

- ECB’s Villeroy said he does not expect a rate hike at next week’s ECB meeting, said energy costs are a minor part of consumer spending, said banks should stay calm amid the Iran crisis.

- ECB’s Nagel said the ECB will act decisively if an energy spike feeds into durably higher inflation; the risk of higher inflation has risen, economic outlook has deteriorated; the latest US statements on Iran war offer cause for hope.

- Westpac and National Australia Bank now expect the RBA to hike rates in March and May.

NOTABLE US HEADLINES

- Senators Warner (D) and Rounds (R) are to introduce new legislation focused on AI and the workforce, Axios reported citing an announcement.

GEOPOLITICS

MIDDLE EAST

- Iran’s Joint Command Spox said US and Israeli banks will be hit after an attack on an Iranian bank, via IRNA.

- Iran’s IRGC said it carried out its heaviest and most intense attacks since the start of the war, targeting US and Israeli assets across the region, according to WSJ.

- IRGC said it launched missiles carrying 2-ton warheads in a new wave of heavy, multi-warhead strikes targeting US bases in Iraq and Bahrain as well as Israel.

- Iran’s police chief said anyone taking to the streets at the enemy’s request will be confronted as an enemy and not a protester, adds security forces are prepared to respond and have their fingers on the trigger.

- Iran launches new wave of missiles on occupied territories.

- Iranian armed forces spokesperson vows retaliation for Israeli and US strikes on residential areas.

- US officials said Iran has laid less than 10 mines in the Strait of Hormuz and it is unclear if it intends to lay more in the near term, according to WSJ.

- Drone reportedly hits a US diplomatic facility in Iraq, according to Washington Post.

- US Central Command said US forces eliminated multiple Iranian naval vessels on March 10th, including 16 mine layers near the Strait of Hormuz.

- Air defenses shoot down a drone targeting a US military base near Erbil Airport in Iraqi Kurdistan.

- Israeli army announces massive wave of raids on Tehran, targeting Iranian regime infrastructure.

- UAE Defence Ministry reported air defences are currently intercepting missiles and drones from Iran.

- Israel rejects Lebanon’s request for a halt in fighting to allow for talks, according to FT.

- UKMTO said it has received a report of an incident 50NM north-west of Dubai, with a bulk carrier hit by an unknown projectile.

RUSSIA-UKRAINE

- Russia’s Kremlin said Istanbul is an possible location for talks next week but there is no specific clarity yet.

OTHERS

- North Korea conducted strategic cruise missile tests on Tuesday for a naval destroyer, while Leader Kim said destroyers must be equipped with supersonic weapons, according to KCNA.

CRYPTO

- Bitcoin returns below USD 70k while Ethereum continues to trade above USD 2k.

APAC TRADE

- APAC stocks traded higher as the recent easing of oil prices helped the region shrug off the lacklustre lead from Wall Street and reports of Iran beginning to lay mines in the Strait of Hormuz.

- ASX 200 gained with strength in mining, resources, materials and financials, front-running the advances, but with upside capped amid increased bets for the RBA to hike rates at next week’s meeting following recent central bank rhetoric and calls by some of Australia’s largest banks for consecutive rate increases in March and May.

- Nikkei 225 rallied following the recent easing of oil price pressures and as softer-than-expected PPI data, which showed a surprise monthly deflation, supports the case for a delay in BoJ policy normalisation.

- Hang Seng and Shanghai Comp lagged amid quiet catalysts and with Chinese officials said to be frustrated by what they see as insufficient US preparation for the Trump-Xi summit later this month, while China also moved to curb the use of OpenClaw AI by banks and state agencies.

NOTABLE ASIA-PAC HEADLINES

- Japan’s government is considering measures amid Middle East tensions and will announce gas and utility price measures at an appropriate time, according to Nikkei.

NOTABLE APAC DATA RECAP

- Japanese PPI MoM (Feb) M/M -0.1% vs. Exp. 0.1% (Prev. 0.2%, Low. -0.2%, High. 0.4%).

- Japanese PPI YoY (Feb) Y/Y 2.0% vs. Exp. 2.1% (Prev. 2.3%, Low. 1.9%, High. 2.5%).

1 c) Asian opening report

Crude choppy on Hormuz updates; Potential IEA decision and US CPI awaits – Newsquawk EU Market Open

Wednesday, Mar 11, 2026 – 02:50 AM

- APAC stocks traded higher as the recent easing of oil prices helped the region shrug off the lacklustre lead from Wall Street and reports of Iran beginning to lay mines in the Strait of Hormuz.

- US intelligence began to see indications that Iran is taking steps to deploy mines in the Strait of Hormuz shipping lane, according to CBS.

- US Energy Secretary Wright posted that the US Navy had escorted an oil tanker through the Strait of Hormuz, although this post was later deleted, and a White House official clarified that this wasn’t true.

- UKMTO received a report that a cargo vessel was hit by an unknown projectile in the Strait of Hormuz, which has resulted in a fire on board, while the crew are evacuating the vessel.

- The IEA meeting on Tuesday ended with no decision on a crude stockpile release; WSJ reported that the IEA proposed the largest ever release of oil from strategic reserves (no figures mentioned), with countries to decide today on whether to release oil stocks.

- Looking ahead, highlights include German HICP Final (Feb), US CPI (Feb), OPEC MOMR. Speakers include ECB’s de Guindos & Schnabel, BoE’s Breeden & Fed’s Bowman, Supply from Germany & the US.

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

IRAN CONFLICT

- US intelligence began to see indications that Iran is taking steps to deploy mines in the Strait of Hormuz shipping lane, according to CBS reports. Furthermore, CNN reported that Iran had begun laying mines in the Strait of Hormuz.

- US President Trump posted “If Iran has put out any mines in the Hormuz Strait, and we have no reports of them doing so, we want them removed, IMMEDIATELY! If for any reason mines were placed, and they are not removed forthwith, the Military consequences to Iran will be at a level never seen before. If, on the other hand, they remove what may have been placed, it will be a giant step in the right direction.” Trump posted shortly after that the US “has hit, and completely destroyed, 10 inactive mine-laying boats and/or ships, with more to follow”.

- US officials said Iran has laid fewer than 10 mines in the Strait of Hormuz and that it is unclear if it intends to lay more in the near term, according to WSJ.

- US Central Command said US forces eliminated multiple Iranian naval vessels on March 10th, including 16 mine-layers near the Strait of Hormuz. CENTCOM also stated that the Air Force continued to deliver devastating strikes against the Iranian regime during Operation Epic Fury.