GOLD CLOSED CLOSED DOWN $44.25 TO $5117.75

ACCESS MARKET

GOLD $5096,00 3:30 PM)

SILVER: 85.00 3;30 PM)

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MARCH 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 5,167.400000000 USD

INTENT DATE: 03/11/2026 DELIVERY DATE: 03/13/2026

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 7

363 H WELLS FARGO SECURITI 11

555 C BNP PARIBAS SEC CORP 13

624 H BOFA SECURITIES 35

657 H MORGAN STANLEY 131

661 C JP MORGAN SECURITIES 19

709 C BARCLAYS 56

737 C ADVANTAGE FUTURES 6

905 C ADM 5 1

TOTAL: 142 142

MONTH TO DATE: 7,642

JPMORGAN STOPPED 19/142

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2026: 142 CONTRACTs NOTICES FOR 14,200 OZ or 0.4416 TONNES

total notices so far: 7642 contracts for 764,200 OR 23.769 tonnes)

SILVER NOTICES: 364 NOTICE(S) FILED FOR 1.820 MILLION OZ /

total number of notices filed so far this month : 7064 CONTRACTS (NOTICES) for 35,320 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A STRONG QUEUE JUMP OF 24 CONTRACTS OR 120,000 OZ/NEW STANDING ADVANCES TO 39.065MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 31.370 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY TODAY’S 120,000 OZ QUEUE //NEW TOTAL STANDING ADVANCESTO 39.065 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES FOLLOWED BY TODAY’S STRONG 1.897 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 30.958 TONNES/

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES FOLLOWED BY TODAY’S 1.897 TONNES QUEUE JUMP//NEW STANDING ADVANCES TO 30.958TONNES OF GOLD./

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES FOLLOWED BY TODAY’S 1.897 TONNES QUEUE JUMP //NEW STANDING ADVANCES TO 30.958 TONNES/

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 103.30 TONNES//WILL BE VERY STRONG ISSUANCE THIS MONTH

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 331 CONTRACTS OI TO 115,789 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 112,794 CONTRACTS THIS MONTH( MARCH 4/2026)

EFP ISSUANCE 855 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 855 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 398 CONTRACTS AND ADD TO THE 585 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 1186 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $3.96

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 5.930 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $3.96

2.ASIAN AFFAIRS MARCH 12 /2025

SHANGHAI CLOSED DOWN 26.48 PTS OR 0.64%

HANG SENG CLOSED DOWN 182.00 PTS OR 0.70%

Nikkei CLOSED DOWN 998.37 PTS OR 1.81%

//Australia’s all ordinaries CLOSED DOWN 0.20%

//Chinese yuan (ONSHORE) CLOSED UDOWN6.8757

/ OFFSHORE CLOSED DOWN AT 6.8769 Oil UP TO 90.37 dollars per barrel for WTI and BRENT UP TO 97,77 Stocks in Europe OPENED ALL DEEPLY IN THE RED

ONSHORE USA/ YUAN TRADING 6.8759OFFSHORE YUAN TRADING DOWN TO 6.8769 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UDOWNAGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1726 CONTRACTS DOWN TO 415,682 OI , (AT A LEVEL FROM DECADES ALL TIME LOW OF 404,829), DESPITE OUR HUGE LOSS IN PRICE OF $70.55 WITH RESPECT TO WEDNESDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, DESPITE THAT HUGE PRICE LOSS FOR GOLD . AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1450).

WE HAD SOME T.A.S. LIQUIDATION DURING WEDNESDAY’S TRADING/RAID. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO MASSIVELY LONG THIS MONTH AFTER A BRIEF PERIOD OF GOING NET SHORT AT THE BEGINNING OF FEBRUARY.

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MARCH CONTRACT MONTH!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW MOVING AWAY FROM ITS ALL TIME LOW POINT IN OI OF 404,829 AND FROM THIS POINT, OI WILL RISE BUT IT WILL BE EXTREMELY DIFFICULT FOR THE CROOKS TO FLEECE OUR NEWBIE SPEC LONGS. THE ALL TIME LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 1 TO 2 %.(SILVER IS AT 7%). WITH AN OI OF 419,558 THERE IS LITTLE ROOM FOR THE CROOKS TO RAID OUR NEWBIE SPECULATORSWHO ARE VERY STICKY AT THIS POINT.

WE THUS HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 276 CONTRACTS (OR 0.855 TONNES) DESPITE THE HUGE LOSS IN PRICE, WEDNESDAY.

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. DURING THE MIDDLE OF THE MONTH. WE HAVE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE ARE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE THUS FAR FOR FEB NOW REMAINS AT SIX.(31.251 TONNES)

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MARCH:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUAY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: ZERO ISSUED SO FAR!

DETAILS ON OUR NEW MARCH COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 7,052 CONTRACTS DESPITE OUR HUGE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MARCH/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS ANOTHER HUMONGOUS SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 15,013 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND IT IS IN FULL FORCE WITH ANOTHERRAID TODAY.

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH NO EXCHANGE FOR RISK ISSUANCE SO FAR.. BUT DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE:

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT STRONG QUEUE JUMP OF 1.897 TONNES//NEW STANDING FOR GOLD ADVANCES TO: 30.958 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING MARCH,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $70.55 )

WE HAD SOME T.A.S. SPREADER LIQUIDATION WEDNESDAY (AND HUGE TODAY) // COMEX SESSION// DESPITE OUR LOSS IN PRICE BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD FOR FEBRUARY’S ACTIVE DELIVERY MONTH (157 TONNES) AND ALSO MARCH’S STANDING OF 18+ TONNES.

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO MARCH:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT STRONG QUEUE JUMP 1.897 TONNES// GOLD STANDING ADVANCES TO: 30.958 TONNES/

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $70.55

WE HAD A HUGE 7328 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE

NET LOSS ON THE TWO EXCHANGES : 276 CONTRACTS OR 27600 OZ OR 0.855TONNES

INITIAL GOLD COMEX

MARCH 12

MARCH DELIVERY MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES i) Out of Brinks; 64,302.000 oz (2000 kilobars) total tonnes removed: 2 tonnes. |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 142 CONTRACTS OR 14,200 OZ 0.4416 TONNES OF GOLD |

| No of oz to be served (notices) | 2313 contracts 231300 OZ 7.194 TONNES |

| Total monthly oz gold served (contracts) so far this month | 7642 notices 764,200 oz 23.769 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

DEPOSITS/CUSTOMER

0 ENTRY

0 entry

customer withdrawals:

1 ENTRIES

i) Out of Brinks; 64,302.000 oz (2000 kilobars)

total tonnes removed: 2 tonnes.

comex is draining of gold/.

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 1

dealer to customer account: BRINKS

i) 27,936.523 OZ

0.868 TONNES REMOVED FROM DEALER TO CUSTOMER ACCT.

COMEX IS DRAINING GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

chaos inside the comex

AMOUNT OF GOLD STANDING FOR MARCH

THE FRONT MONTH OF MARCH STANDS AT 2455 CONTRACTS FOR A LOSS OF 1265 CONTRACTS. WE HAD

1875 CONTRACTS SERVED ON WEDNESDAY, SO WE GAINED A HUGE 610 CONTRACTS OR AN ADDITIONAL 61,000 OZ WILL STAND FOR DELIVERY AT THE COMEX. THE TONNAGE EQUATES TO 1.892 TONNES . THIS IS A MASSIVE AMOUNT OF GOLD WILLING TO STAND AS CENTRAL BANKERS CLAMOUR FOR OUR ANCIENT METAL OF KINGS ON THIS SIDE OF THE PLANET

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 12,853 CONTRACTS DOWN TO 212,539 CONTRACTS. APRIL IS NOW THE NEW FRONT MONTH FOR DELIVERY OF GOLD. APRIL IS GENERALLY A VERY STRONG DELIVERY MONTH

MAY GAINED 12 CONTRACTS UP TO AN OI OF 863.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI ROSE BY A STRONG 14,633 CONTRACTS UP TO AN OI OF 132,898

We had 142 contracts filed for today representing 14,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 142 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 142 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAR. /2026. contract month, we take the total number of notices filed so far for the month (7642) to which we add the difference between the open interest for the front month of MAR (2455 CONTRACTS) minus the number of notices served upon today 142 x 100 oz per contract) equals 995,500 OZ OR (30.958 Tonnes of gold)

thus the INITIAL standings for gold for the MAR contract month: No of notices filed so far (7642 x 100 oz +we add the difference for front month of MAR (2455 OI} minus the number of notices served upon today (142 x 100 oz) which equals 995,500 OZ OR 30.958 TONNES//

new total of gold standing in MAR is 30.958 TONNES//

TOTAL COMEX GOLD STANDING FOR MARCH 30.958 TONNES TONNES WHICH IS NOW MEGA HUGE FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF MARCH.

confirmed volume WEDNESDAY confirmed 194,460 poor

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,717,146.01 oz 53.410 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,717,146.010 tonnes oz 52.58 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 32,656,406.591 oz

TOTAL REGISTERED GOLD 16,697,449.281 or 519.360 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 15,958,957.310 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 14,980,303 oz ((REG GOLD- PLEDGED GOLD)=

465.950 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER COMEX

MARCH DELIVERY MONTH

MARCH 12 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries i) Out of HSBC 16,006.370 oz ii) Out of Manfra 1058,679.682 total withdrawal: 1,074,686.052 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Stonex: 253,735.850 oz total dealer deposit; 253,735.850 oz xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT ENTRIES: 1 i) Into CNT 598,969.330 oz total deposit: 598,969.330 oz |

| No of oz served today (contracts) | 364 CONTRACT(S) ( 1.820 MILLION OZ |

| No of oz to be served (notices) | 749 Contracts (3.745 MILLION oz) |

| Total monthly oz silver served (contracts) | 7064 contracts 35.320 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRIES: 1

ENTRIES: 1

i) Into CNT 598,969.330 oz

total deposit: 598,969.330 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

deposits into dealer account: 1

1 ENTRY

i) Into Stonex: 253,735.850 oz

total dealer deposit; 253,735.850 oz

withdrawals: customer side/eligible

2 entries

i) Out of HSBC 16,006.370 oz

ii) Out of Manfra 1058,679.682

total withdrawal: 1,074,686.052 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 1// customer acct to dealer Manfra

a) Manfra 4667.506 oz

total removal from the registered silver to eligible silver: 1,524,812.662 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 78.610 MILLION OZ//.TOTAL REG + ELIGIBLE. 344.324 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH /2026 OI: 1113 OPEN INTEREST CONTRACTS FOR A GAIN OF 4 CONTRACTS.

WE HAD 20 NOTICES FILED ON WEDNESDAY SO WE GAINED A TINY 24 CONTRACTS OR AN ADDITIONAL 120,000 OZ OF SILVER WILL TRY FOR DELIVERY OVER HERE AS A BANKER ASSISTED QUEUE JUMP.

APRIL, THE NEW FRONT MONTH SAW A GAIN OF 486 CONTRACTS UP TO 1942 CONTRACTS

MAY SAW A 614 CONTRACT LOSS DOWN TO 77,860 CONTRACTS.

JUNE SAY A GAIN OF 92 CONTRACTS UP TO 365 OI CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 364 or 1.820 MILLION oz

CONFIRMED volume; ON WEDNESDAY 51,677 fair+++//

AND NOW MARCH. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 7064 X5,000 oz = 35.320 MILLION oz

to which we add the difference between the open interest for the front month of MARCH (1113) AND the number of notices served upon today (364)x (5000 oz)

Thus the standings for silver for the MARCH 2026 contract month: (7064)Notices served so far) x 5000 oz + OI for the front month of MARCH(1113) minus number of notices served upon today (364 )x 5000 oz equals silver standing for the FEB..contract month equating to 39.065 MILLION OZ.

NEW STANDING: 39.065MILLION OZ WHICH IS STILL LOWISH FOR A GENERALLY HUGE DELIVERY MONTH OF MARCH.

New total standing: 39.065 million oz.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are ONLY 78.610 million oz of registered silver

JPMorgan as a percentage of total silver: 152.021/344.324.million: 44.12%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

MAR 9/2026/WITH GOLD DOWN $53.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.573 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1073.321 TONNES

MAR 6/2026/WITH GOLD UP $77.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 5.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1075.894 TONNES

MAR 5/2026/WITH GOLD DOWN $49.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 18.032 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1081.038 TONNES

MAR 4/2026/WITH GOLD UP $9.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.545 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1099.07 TONNES

MAR 3/2026/WITH GOLD DOWN $188.75 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.35 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101.36 TONNES

MAR 2/2026/WITH GOLD UP $71.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101,13 TONNES

FEB 27/2026/WITH GOLD UP $52.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.90 TONNES

FEB 26/2026/WITH GOLD DOWN $30.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 11.45 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.62 TONNES

FEB 25/2026/WITH GOLD UP $48.40 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL WITHDRAWAL OF 0.300 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1086.17 TONNES

FEB 24/2026/WITH GOLD DOWN $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE PAPER DEPOSIT OF 7.72 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1086.47 TONNES

FEB 23/2026/WITH GOLD UP $148.25 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 20/2026/WITH GOLD UP $79.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 19/2026/WITH GOLD DOWN $9.00 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 18/2026/WITH GOLD UP $102.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 17/2026/WITH GOLD DOWN $136.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ /// ///INVENTORY RESTS AT 1077..04 TONNES

FEB 13/2026/WITH GOLD UP $94.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.140 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.18 TONNES

FEB 12/2026/WITH GOLD DOWN $143.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.000 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.32 TONNES

FEB 11/2026/WITH GOLD UP $63.65 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.34 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.32 TONNES

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

GLD INVENTORY: 1077.28 TONNES, TONIGHTS TOTALGOLD INVENTORY

SILVER

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

MAR 6 WITH SILVER UP $2.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 5.526 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508,287 MILLION OZ

MAR 5 WITH SILVER DOWN $0.98 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.097 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 512.726 MILLION OZ

MAR 4 WITH SILVER DOWN $0.21 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.545 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 513.813 MILLION OZ

MAR 3 WITH SILVER DOWN $5.27 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2/899 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 511.268 MILLION OZ

MAR 2 WITH SILVER DOWN $3.87 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.352 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 514.167 MILLION OZ

FEB 27 WITH SILVER UP $5.54 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 0.544 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 517.519 MILLION OZ

FEB 26 WITH SILVER DOWN $4.05 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 0.906 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 516.975 MILLION OZ

FEB 25 WITH SILVER UP $3.43 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 8.923 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 517.881 MILLION OZ

FEB 24 WITH SILVER UP $0.55 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 10.056 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 508.958 MILLION OZ

FEB 23 WITH SILVER UP $4.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT WITHDRAWAL OF 0.951 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 498.902 MILLION OZ

FEB 20 WITH SILVER UP $4.85 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.035 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.853 MILLION OZ

FEB 19 WITH SILVER DOWN $0.23 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 5.798 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 502.888 MILLION OZ

FEB 18 WITH SILVER UP $4.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 11.325 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508.686 MILLION OZ

FEB 17 WITH SILVER DOWN $4.39 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 4.253 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 515.753 MILLION OZ

FEB 13 WITH SILVER UP $2.35 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.994 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 520.011 MILLION OZ

FEB 12 WITH SILVER DOWN $8.78 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 635,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 522.005 MILLION OZ

FEB 11 WITH SILVER UP $3.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 815,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 521.370 MILLION OZ

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

CLOSING INVENTORY 499.592 MILLION OZ OF SILVER..

.2. MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

JESSE COLUMBO

3.CHRIS POWELL AND HIS GATA DISPATCHES:

4. ANDREW MAGUIRE AND LIVE FROM THE VAULT PODCASTS

KINESIS: PODCAST NO 262/ANDREW WITH BILL HOLTER

5. COMMODITY REPORT//COAL

ASIAN AFFAIRS MARCH 12/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 26.48 PTS OR 0.64%

HANG SENG CLOSED DOWN 182.00 PTS OR 0.70%

Nikkei CLOSED DOWN 998.37 PTS OR 1.81%

//Australia’s all ordinaries CLOSED DOWN 0.20%

//Chinese yuan (ONSHORE) CLOSED UDOWN6.8757

/ OFFSHORE CLOSED DOWN AT 6.8769 Oil UP TO 90.37 dollars per barrel for WTI and BRENT UP TO 97,77 Stocks in Europe OPENED ALL DEEPLY IN THE RED

ONSHORE USA/ YUAN TRADING 6.8759OFFSHORE YUAN TRADING DOWN TO 6.8769 ONSHORE YUAN TRADING ABOVE OFF SHORE AND DOWN ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING UDOWNAGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.8759

OFFSHORE YUAN: UP TO 6.8769

1.HANG SANG DOWN 182.00 POINTS OR 0.70%

2. Nikkei closed DOWN 998.39 PTS OR 1.81%

WEST TEXAS INTERMEDIATE OIL UP 91.93

BRENT; 97.77

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 99.42 /// EURO RISES TO 1.1549UP 6 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.184 UP 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.35… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.476UP 3 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: 6.87059(DOWN) AND OFFSHORE: DOWN AT 6.8769

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.9420 Italian 10 Yr bond yield UP to 3.706 SPAIN 10 YR BOND YIELD UP TO 3.426

3i Greek 10 year bond yield UP TO 3.681

3j Gold at $5180.50 Silver at: 86.94 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 4/100 roubles/79.18

3m oil (WTI) into the 91 dollar handle for WTI and 97 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.86 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.184% UP 2BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.476 UP 3 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7825 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9037 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.236UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.884 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.659 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 44.12 UP 4 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.7310 UP 8 PTS

30 YR UK BOND YIELD: 5.394 UP 6 BASIS PTS

10 YR CANADA BOND YIELD: 3.487 UP 8 BASIS PTS

5 YR CANADA BOND YIELD: 3.034UP 8 BASIS PTS.

1a New York Opening report

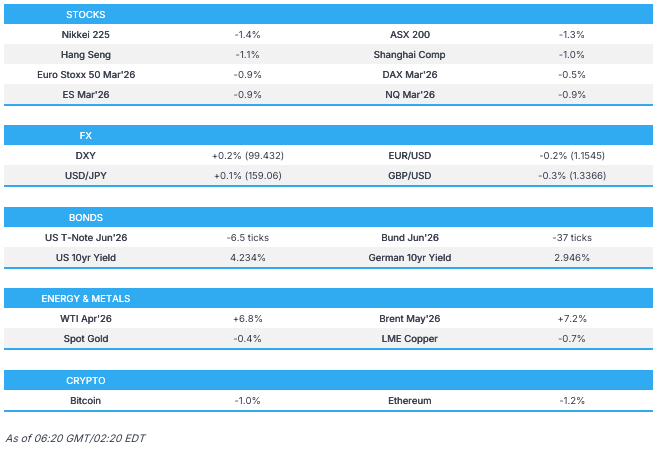

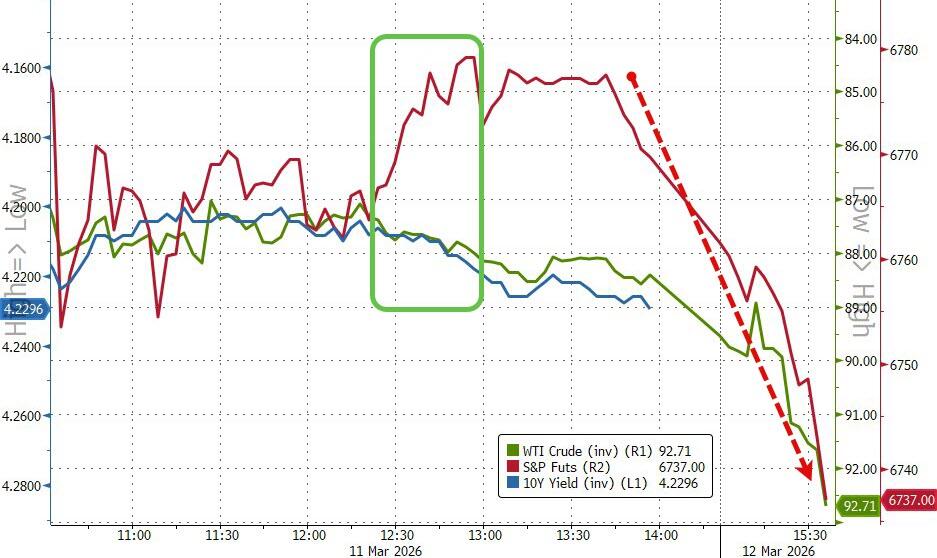

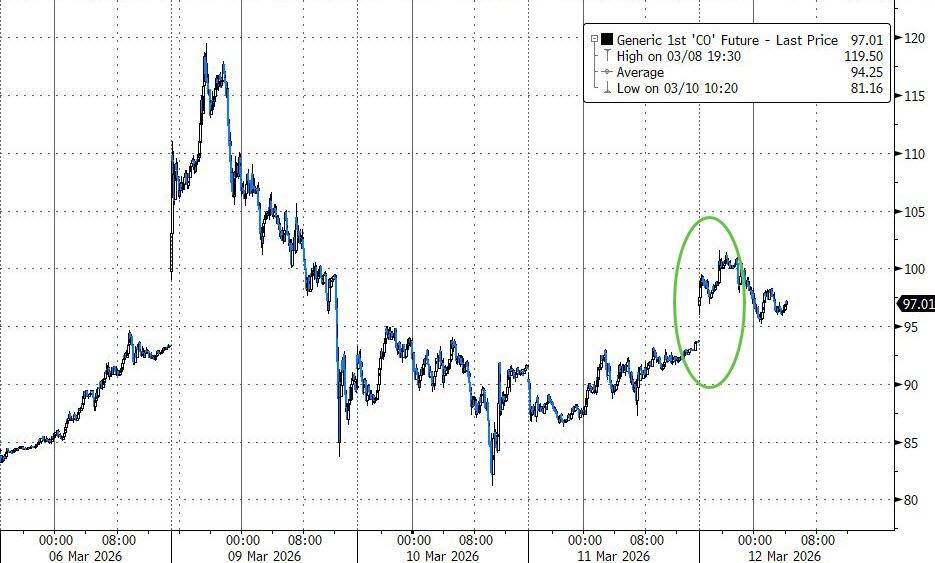

Futures Tumble As Oil Jumps Above $100 On Iran War Chaos

Thursday, Mar 12, 2026 – 08:33 AM

US futures are sharply lower, as oil briefly surges back over $100 while markets start to accept the view that the Iran war will not end this week, and possibly any time soon. As of 8:15am ET, S&P and Nasdaq futures are down 0.7% and R2K futures slide more than 1%. Futures dropped more than 1% overnight as Iraq suspended oil terminal activity following an attack on two tankers; they recovered some losses after the resumption of normal operations at Oman’s Mina Al Fahal oil terminal. Global market moves overnight were relatively benign: KOSPI down 48bps the most muted day in weeks, China flattish, Europe mixed with Germany flat and France down 50bps. In premarket trading, Mag 7 names are all weaker, energy names are stronger, and defensives outperform cyclicals on the move lower. Iran offered an off-ramp (guarantee of no future attacks from US and Israel) but unclear if that will be accepted. Private credit fears continue to surface as Morgan Stanley and Cliffwater gated withdrawals from their private credit funds, pressuring both Equities and Credit. Bond yields are flat, the USD is bid, and commodities are seeing strength across all 3 complexes, led by Energy. Today’s macro data focus is on jobless claims and housing starts. The Fed remains in blackout into next week’s (Mar 18) meeting. The market wants to see if Powell echoed Trump’s view that prices increases from the conflict are transitory when other central banks are seeing expectations flip from cuts to hikes.

In premarket trading, Mag 7 stocks are all lower (Alphabet -0.7%, Meta -0.7%, Amazon -0.6%, Microsoft -0.4%, Nvidia -0.4%, Tesla and Apple little changed)

- Fertilizer, energy and chemical stocks climb as the war in Iran and disruptions to the Strait of Hormuz tighten supply, raising prices, while airlines and cruise stocks are down as higher crude prices lift costs.

- Blue Owl Capital Inc. (OWL) falls 3% after the asset manager defended its recent sale of $1.4 billion of loans from three of its funds, arguing the transaction contained no backstops or hidden incentives.

- Bumble (BMBL) rises 24% after the online dating company forecast Ebitda for the first quarter that beat expectations. Analysts noted that focus now shifts to upcoming product overhaul planned for later in the year.

- Hims & Hers Health (HIMS) rises 5% after rallying 10% on Wednesday. The stock is set to extend its advance for a fourth straight session.

- Lightwave Logic (LWLG) climbs 16% after the company announced a development agreement with Tower Semiconductor.

- Petco (WOOF) rises 10% as the pet health and wellness company’s adjusted Ebitda forecast for the first quarter beat the average analyst estimate. Jefferies upgrades its rating, noting that investors underappreciate the progress made thus far.

- UiPath (PATH) falls 6% after the software company reported fourth-quarter results. Bloomberg Intelligence writes that growth concerns persist despite a strong quarter.

In corporate news, Atlassian is the latest software firm to announce AI-linked job cuts. Abivax shares are surging after French media reported that the biotech had granted AstraZeneca exclusive access to confidential information until March 23 with a view to formalizing an offer. And the widening war has upended global travel, sending fares soaring and leaving travelers facing record prices ahead of the Easter rush.

Iran escalated attacks on parts of Dubai and shipping assets, pushing oil briefly back above $100 a barrel and intensifying concern about the length of the Middle East war and the effective closure of the Strait of Hormuz. Multiple oil tankers were attacked in Iraqi waters and Oman evacuated ships from a key terminal. The Iran war has disrupted 7.5% of global crude supply, with flows through the Strait down by more than 90%, the IEA said. It’s telling that after yet another Whitehouse jawbone and the IEA’s record reserve release announcement, oil still failed to drop. Overnight Reuters reported, “Iran has laid about a dozen mines in Strait of Hormuz, sources say”.

Hostilities are fast-approaching a third week, with no sign of de-escalation. Iran escalated attacks on parts of Dubai and shipping assets, driving oil prices higher and increasing concern among traders about how much longer the conflict in the Middle East will go on for. The surge in oil prices reflects concern that the conflict could throw energy markets into turmoil for a prolonged period, with efforts to cushion the impact offering little relief. Crude is driving moves across asset classes as traders fear that higher fuel costs will rekindle inflation and hit economic growth.

“What you’re are seeing is the market pricing a long-lasting scenario of high oil prices,” said Karen Georges, an equity fund manager at Ecofi in Paris. “The security of shipping in the region is a big concern while the release of emergency oil reserves can only provide temporary relief.”

The International Energy Agency said in a monthly report that the Iran war is causing unprecedented turmoil in oil markets. Global oil supply will be slashed by 8 million barrels a day this month, or almost 250 million barrels in total, the IEA estimated. The report comes after the agency’s members agreed to release 400 million barrels from emergency reserves on Wednesday.

“While Trump’s claim that we could soon see a resolution to the conflict does provide hesitancy for the bulls, the reality of the situation will undoubtedly call for higher prices as the days roll on,” said Joshua Mahony, chief market analyst at Scope Markets.

For Francois Rimeu, senior strategist at Credit Mutuel Asset Management in Paris, the reaction in equity markets has been rather sanguine given how broad and impactful a worst-case scenario for the conflict could be. “The draw-down could really turn much lower should the conflict last longer, and the longer it lasts, the longer a return to business as usual will be,” Rimeu said. “If you ask me when is the right time to buy back, I would tend to say when one actually sees ships crossing the Strait of Hormuz again.”

In the latest hit to private credit, Morgan Stanley and Cliffwater gated withdrawals from their multibillion-dollar private credit funds after investors sought to redeem vastly more than the vehicles allow. Partners Group warned that private credit default rates could double in the next few years. Tariffs are also back in the spotlight as the US begins a probe into trade investigations that set the stage for new levies.

Back on oil, China tightened fuel export curbs, while the average retail cost for one gallon of gasoline in the US has risen to the highest level since May 2024, piling pressure onto the administration to find an off-ramp for the conflict. Trump has said that the war could end soon, but the latest rhetoric from Iran dimmed prospects for a quick resolution.

Elsewhere, JPMorgan said hedge funds are experiencing the biggest drawdown since April’s tariff turmoil, as unwinds in crowded trades punish the fast-money cohort. In a brutal trading week, Citadel’s Global Fixed Income Fund and Taula Capital Management are among the hedge funds worst hit, while D.E. Shaw’s two main vehicles were a rare bright spot in the industry.

European stocks are lower across the board but off session troughs after the resumption of normal operations at Oman’s Mina Al Fahal oil terminal provided some reprieve. Banks are the biggest underperformer, while chemicals outperform most. Here are the biggest movers Thursday:

- Accelleron Industries shares rise as much as 17%, a record jump that briefly sent the stock to an all-time high, after the maker of turbochargers posted full-year earnings that topped expectations, with a solid outlook and its first buybacks

- Abivax shares rise as much as 17% after La Lettre reported the biotech company had granted AstraZeneca exclusive access to confidential information until March 23 with a view to formalizing an offer

- K+S gains as much as 8.8%, the most since last April, after the German fertilizer group reported solid earnings, which analysts said boded well for 2026. They noted that higher sulfur prices due to tumult in the Middle East could prove a tailwind

- Zalando gains as much as 9.2%, the most since November, after the German online seller of fashion announced a new share buyback program of up to €300 million, which RBC said should soothe concerns over capital allocation

- Leonardo shares gain as much as 8.7% to a new record high after the defense technology firm outlined its targets through 2030, which Mediobanca described as “bullish.” Analysts highlight, in particular, order intake expectations

- Bachem shares jump as much as 9.7%, the most since July, after the pharmaceutical ingredients producer reported slightly better results than expected

- PolyPeptide advances as much as 11% after confirming its 2025 numbers and providing outlook commentary which Jefferies says demonstrates the biotechnology company’s strong execution

- Trainline shares slide as much as 6.7% after its annual results, with JPMorgan warning the rail ticketing platform is lacking visibility and faces a “more challenging chapter ahead” in FY27

- Bodycote drops as much as 5.5% after being downgraded at RBC Capital Markets, with analysts citing more limited upside. The cut comes a day after the provider of heat treatment and specialist thermal processing services beat expectation

- Savills shares fall as much as 8.4% to the lowest in six months, as the property services group’s in-line results are overshadowed by the war in the Middle East

- On the Beach shares drop as much as 15% to the lowest level since November 2024. The online seller of package holidays suspended its full-year guidance of £39m to £43m adjusted profit before tax due to a “significant slowdown”

Earlier in the session, Asian stocks fell on Thursday, snapping a two-day rising streak after a string of disruptions in the Iran war renewed fears of a longer-term energy supply strain in the Middle East and briefly pushed Brent crude back above $100 a barrel. The MSCI Asia Pacific Index fell as much as 2%, led by chipmakers TSMC, Samsung and SK Hynix. The jump in oil prices came as Iran suspended oil terminal activity following an assault on two tankers, and Oman temporarily evacuated its main export hub. The regional benchmark had climbed for two previous sessions when oil prices softened, underscoring investors’ focus on volatile energy markets. Bonds in the euro area trimmed early declines.

In FX, the Bloomberg Dollar Spot Index gains 0.3%, before paring the advance; the greenback is on course for a fresh 2026 high, options markets show. USD/JPY is little changed at 158.90; it rose earlier to a two-month high at 159.24 as options traders and strategists see a high threshold for intervention from Japan to defend the yen

In rates, US rates have clambered off session lows but remain weak with global bonds erasing 2026 gains. US yields are down around 1bps across the curve. US long-end yields are little changed with front-end tenors richer by 1bp-2bp, steepening 5s30s spread by around 1bp. 10-year near 4.21% is lower by about 1bp with UK counterpart up about 4bp. In IG issuance, Salesforce led eight issuers that sold a combined $41.7 billion Wednesday, taking weekly volume past $107b, the third largest on record achieved in only two sessions. Issuers paid an elevated 21bp in new issue concessions on deals that were 1.9 times covered. At least one issuer stood down Wednesday, while a couple are considering Thursday.

A Bloomberg index that tracks total returns from investment-grade government and corporate bonds is now flat for 2026. The gauge had been up as much as 2.1% this year through Feb. 27, just before the US and Israel attacked Iran.

In commodities, Brent crude futures rise 4.6% to $98 but off session highs; Iranian attacks on shipping assets and areas of Dubai alongside China tightening fuel export curbs briefly lifted prices above the $100 a barrel mark.Spot gold and silver are higher by 1.5% and 0.1% respectively. Bitcoin is down 0.4%.

US economic data slate includes January trade balance and housing starts and weekly jobless claims (8:30am) and 4Q household change in net worth (12pm)

Market Snapshot

- S&P 500 mini -0.6%

- Nasdaq 100 mini -0.6%

- Russell 2000 mini -1.3%

- Stoxx Europe 600 -0.6%

- DAX -0.5%

- CAC 40 -0.7%

- 10-year Treasury yield little changed at 4.23%

- VIX +1.3 points at 25.53

- Bloomberg Dollar Index +0.2% at 1204.95

- euro -0.1% at $1.1551

- WTI crude +6.2% at $92.66/barrel

Top Overnight News

- Iran escalated attacks on parts of Dubai and shipping assets, pushing oil briefly back above $100 a barrel and intensifying concern about the length of the Middle East war and the effective closure of the Strait of Hormuz. Two oil tankers were attacked in Iraqi waters and Oman evacuated ships from a key terminal. The Iran war has disrupted 7.5% of global crude supply, with flows through the Strait down by more than 90%, the IEA said. BBG

- President Trump—faced with rising oil prices and pushback from his MAGA base—is signaling that he wants to wind down the war he launched against Iran less than two weeks ago. Stopping the fighting carries risks. Leaving in place Iran’s theocratic regime—angry, defiant and in possession of its nuclear stockpile and what remains of its arsenal of missiles and drones—would essentially grant Tehran control over the world’s energy markets. WSJ

- India plans to unveil a more than $10.8 billion fund aimed at bolstering domestic chipmaking, people familiar said. BBG

- German bond yields rose to their highest since October 2023 as the Iran war stoked inflation concerns. BBG

- Oracle has stepped up preparations to cut jobs over the coming months as it credits AI with driving efficiencies in its team and conserves cash to fund its costly push into data centers. FT

- President Trump—faced with rising oil prices and pushback from his MAGA base—is signaling that he wants to wind down the war he launched against Iran less than two weeks ago. Stopping the fighting carries risks. Leaving in place Iran’s theocratic regime—angry, defiant and in possession of its nuclear stockpile and what remains of its arsenal of missiles and drones—would essentially grant Tehran control over the world’s energy markets. WSJ

- U.S. officials say relentless American and Israeli aerial attacks have crippled Iran’s air defenses, navy and missile arsenal. But the regime in Tehran has so far held on to power, and it effectively shut down a crucial choke point for the world’s oil supplies. CNBC

- The White House believes it has until the end of March before rising gas prices become an “unsustainable” political five-alarm fire, one of the officials said. CNBC

- Morgan Stanley and private credit lender Cliffwater have restricted withdrawals from private credit funds, in the latest sign of investor unease about the sector. Separately, a US distressed debt investment fund told its investors that private credit lenders such as Blue Owl are obscuring weaknesses in their portfolios and a sharp correction in debt markets is approaching soon. FT

- Investors demanded significant concessions in Salesforce’s $25bn bond deal on Wed, highlighting rising worries on Wall Street about how AI technology could disrupt software companies. FT

- Trump is to signs orders on housing in the coming days, according to Punchbowl citing a White House spokesperson.

- BofA Card Spending (w/e March 7th): +4.6% Y/Y, vs 3.2% in February. Y/Y spending appears to be robust in the early part of March.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined as rising oil prices dampened sentiment and stoked inflationary concerns, while the announcement of a record joint emergency reserves release failed to drag energy prices lower, due to likely slow deliveries and with further disruptions in the Middle East from the ongoing hostilities. ASX 200 was dragged lower by losses in nearly all sectors aside from energy, and with further calls by large banks for the RBA to deliver a back-to-back rate hike next week. Nikkei 225 briefly slumped below the 54,000 level as the higher oil prices lifted yields and weighed on manufacturer and exporter sentiment. Hang Seng and Shanghai Comp conformed to the broad downbeat mood in the region, with risk appetite also not helped by the announcement that the US is initiating a Section 301 investigation into 16 trading partners, including China, the EU, Mexico, Vietnam, India and Japan.

Top Asian News

- Japanese PM Takaichi said won’t rule out using FY25 reserve funds for fuel and the existing fund has JPY 280bln remaining, adds no additional budget for fuel subsidies now and will use existing fund for fuel price measures.

European bourses (STOXX 600 -0.4%) have started the cash session on the backfoot, with higher oil prices continuing to weigh on growth prospects. Weakness in banks continues to affect the IBEX 35 (-0.9%), given its exposure. The DAX 40 (U/C) is modestly lower, but losses are limited due to gains in Zalando (+12.2%), Rheinmetall (+2.9%) and Hannover Re (+3.2%). European sectors are broadly in the red, with Banks (-2.1%) continuing to underperform. Automobiles (-0.9%) also sit near the bottom of the pile after BMW (-1.1%) missed Q4 sales estimates and forecast higher tariffs acting as a headwind on EBIT margin. Basic Resources (+0.7%) are benefiting from the rise in metals prices, while Chemicals (+0.8%) gain after K+S (+8.0%) beat Adj. EBITDA estimates.

Top European News

- Germany’s IFW institute sees 2026 inflation at 2.5% (prev. 1.8%), GDP at 0.8% (prev. 1.0%), 2027 GDP at 1.4% (prev. 1.3%).

Trade/Tariffs

- USTR Greer said US is initiating Section 301 investigation into 16 trading partners, including China, EU, Mexico, Vietnam, India and Japan, adds the investigation could lead to responsive actions, including tariffs. Said the EU has done approximately 0% of what was agreed in the bilateral trade deal.

- South Korea parliament passes US investment bill, as expected.

FX

- DXY is slightly firmer this morning and trades within a 99.31-99.52 range, and now heading back to the YTD high at 99.69 (March 9th). Upside on Wednesday was facilitated by higher yields as the energy prices continue to trudge higher as the geopolitical situation in Iran is showing little signs of abating any time soon, as an overnight attack on Omani export terminals led Brent back above USD 100/bbl. The recent IEA 400mln barrel reserve release has ultimately had little impact on prices, given the lengthy timeline for the barrels to enter the market and ING rightly points out, it still works out to be “far short of the supply losses we are seeing from the Persian Gulf”. Domestically, weekly jobless claims, trade data and Fed speak via Bowman – though she will not touch on monetary policy.

- G10s are broadly flat to lower against the USD. The JPY and CAD hold afloat, though the former remains within the touted intervention zone beyond 158.00. As mentioned in previous FX pieces, intervention seems unlikely given, a) intervention would prove to be ineffective given the current geopolitical environment, b) low volume short positions on the JPY, c) the move is fundamentally driven by higher energy prices d) the recent lack of verbal intervention suggests potentially higher bar for USD/JPY to rise. Nonetheless, markets will be cognizant of any jawboning heading into the BoJ meeting and wage negations next week.

- AUD underperforms vs USD this morning, scaling back some of this week’s gains. RBA hike bets continue to be taken by sell-side banks, with ANZ the latest see a 25bps increase at next week’s meeting; money markets now assign a circa 80% chance of such a move.

Central Banks

- Bank of Japan Governor Ueda said foreign exchange is an important factor affecting the economy and prices, during parliamentary testimony. Need to be mindful that Forex has larger impacts on prices than in the past and could affect inflation expectations. Will conduct appropriate monetary policy while assessing how Forex affects the likelihood of our forecasts.

- ANZ Bank and Goldman Sachs now see the RBA hiking the Cash Rate at next week’s meeting.

- NBP’s Janczyk said the current base rate is at an appropriate level for the coming quarters.

- BoK member Hwang said need to make rate decision with greater caution.

Fixed Income

- Another bearish session for fixed as, despite the IEA stockpile announcement, energy benchmarks are on the front foot once again with Brent eclipsing USD 100/bbl in APAC trade and Dutch TTF as high as EUR 53.80/MWh. In brief, energy strength comes as the market digests the time it will take for the IEA flows to hit the market, the Middle East conflict showing no immediate signs of stopping, and the associated ongoing Strait of Hormuz block.

- Given this, USTs are lower by a handful of ticks and holding just off a 111-21 base. If the move continues, we look to support at 111-19+, 111-10 and 111-08+ from earlier in the year. The US docket is headlined by Fed speak and then a 30yr auction to round off the week, after a poor 3yr and a 10yr that was an improvement from the last outing, but softer than the average tap.

- Gilts lower by around 40 ticks at most, hitting a 89.36 trough, which, while notable is still some way clear of the 88.80 MTD low and the 88.52 contract base. Pressure a function of the referenced energy moves and a return towards some of the hawkish BoE pricing seen at the start of the week, with around a 20% chance of a hike by end-2026 currently implied.

- Finally, Bunds followed suit at first and hit a 125.91 base, taking the German 10yr yield to another multi-year high. Amidst this, market pricing got to around an 80% chance of two 25bps hikes by the ECB in 2026; reminder, at most we have seen two hikes fully priced in recent sessions. However, this pared across the mid-morning with the benchmark briefly, but only marginally, moving into the green. No clear or overt fundamental behind the gradual turnaround, but the action is potentially a function of energy benchmarks easing from overnight peaks.

Commodities

- WTI and Brent futures trade firmer but off best levels after Brent futures briefly rose above USD 100/bbl in APAC hours, with the former currently in a USD 88.61-95.97/bbl range and the latter in a USD 96.69-101.59/bbl parameter. The gains come amid a war that seems to be escalating rather than abating (full Newsquawk Analysis available on the headline feed).

- European natgas prices are firmer but off their best levels after rising almost 8% in sympathy with crude prices. The EU’s Dombrovskis warned that inflation could exceed 3% this year if the Middle East war keeps Brent around USD 100/bbl and gas prices elevated for a prolonged period; under that scenario, 2026 growth would be up to 0.4ppts below the 1.4% pace forecast late last year.

- Spot gold is mildly firmer this morning and largely moves in tandem with the USD, which in turn tracks oil prices. Gold retreated overnight following US CPI data, which reduced expectations for any near-term Fed rate cuts, and as the Middle East conflict lifted crude prices. XAU/USD resides in a USD 5,125.64-5,189.86/oz range within Tuesday’s USD 5,117.35-5,238.75/oz.

- 3M LME copper ekes mild gains on either side of USD 13,000/t as the red metal largely tracks the USD and oil for any impact on the growth narrative, with further upside likely capped by the US initiating a Section 301 investigation into 16 trading partners, including China, the EU. 3M LME copper currently resides in a narrow USD 12,920.60-13,055.88/t range at the time of writing.

- IEA OMR: cuts 2026 global oil supply growth forecast to 1.1mln BPD (prev. 2.4mln BPD), total 2026 supply forecast 107.2mln BPD (prev. 108.6mln BPD). Middle East conflict is the largest oil supply disruption ever. Demand Forecasts. 2026, total: 104.8mln BPD. 2026, growth: 640k BPD (prev. 850k BPD). OPEC+ production decreased by 210k BPD in February.

- US is to release 172mln barrels of crude from strategic petroleum reserve, according to Energy Department. The release will begin next week, with delivery expected to take around 120 days based on planned discharge rates, while the US will replace reserves by 20% more than what will be withdrawn. SPR release is part of the broader coordinated crude oil release from IEA member countries in response to the Iran war.

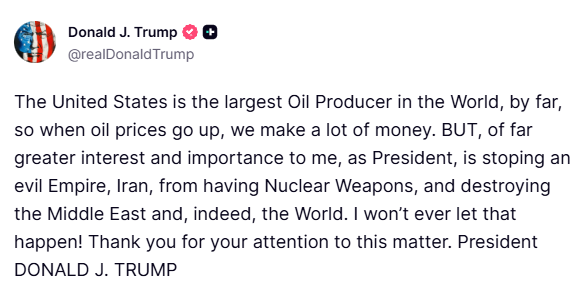

- US President Trump said IEA decision to release oil from reserves will substantially reduce oil prices.

- Oman’s Mina Al Fahal crude export terminal has resumed normal operations after a temporary halt earlier Thursday, with loading activities now proceeding as usual, according to reported.

- Iraqi official said oil ports have completely stopped operations, while commercial ports continue to operate following attack on two fuel tankers.

- India is in discussions with Iran to secure passage for 20 tankers through the Strait of Hormuz, Bloomberg reported citing sources.

- US Energy Secretary Wright said hope to see ships through the Strait of Hormuz in a few weeks.

- China reportedly expands BHP’s (BHP AT) iron ore ban to new products, asking domestic steel mills not to take delivery from BHP’s Portside Newman fines from next week.

Geopolitics

- A senior US administration official, on the Middle East conflict and President Trump’s view, said “The Iranians fcking around with the Strait makes him more dug in”. An advisor said that Trump is bullish on the success of the operation thus far and believes the American people will believe it was the right approach once it is over. Advisor adds that Trump, and others in the administration, genuinely believe that gas prices will substantially fall when the Middle East conflict concludes, and long enough before the midterms to not be a problem.

- US President Trump was reportedly “ambiguous and noncommittal” during the G7 leaders call, Axios reported; with some participants thinking POTUS wants to end the war, while other attendees left with the opposite view.

- US President Trump said we knocked out Iran’s navy and mine layers, adds oil prices will come down, but we won’t leave early. said the job on Iran must be finished and don’t want to return every two years.

- US President Trump said we know where Iranian sleeper cells are and have eyes on all of them, adds we are going to look very closely at the Straits.

- Reports of a drone attack on a US military base in Kuwait, Tasnim reported.

- According to Lebanese newspaper citing diplomatic sources, Iran clarified that they defend itself against American and Israeli aggression and that it will not agree to a ceasefire that is not accompanied by clear guarantees, via N12 News reporter Lipkin.

- Officials from four nations are attempting to persuade Iran to begin talks with the US, Jerusalem Post reported citing sources; however, thus far, Iran has refused to engage and is maintaining a hardline position.

- Reports suggests that Iran says it struck a US oil tanker in the Strait of Hormuz.

- Iran said it gives permission for Indian oil tankers to pass through the Strait of Hormuz. This was later denied by an Iranian source.

- “The campaign against Hezbollah will not be short and will not adhere to a specific timetable”, according to Sky News Arabia citing Israeli officials.

- Iranian explosive-laden boats hit two fuel tankers in Iraqi waters.

- Iran military-affiliated outlet Defa press cites informed sources that note Yemeni resistance and some other resistance groups are fully prepared to join the battle in the coming days. According to predictions, with the entry of these groups, there is a risk of closing the strategic Bab-al-Mandab Strait which would disrupt transit in the Suez Canal.

- UKMTO received a report of an incident 35 nautical miles north of Jebel Ali in United Arab Emirates, in which a container ship was struck by an unknown projectile causing a small fire, while all crew are safe.

- Saudi Ministry of Defence said they are intercepting a drone heading to the Shaybah oil field, Sky News Arabia reported; reported suggest the interception was successful.

- Qatar residents reportedly receive mobile alert for missile threat.

US Event Calendar

- 8:30 am: United States Jan Trade Balance, est. -66b, prior -70.3b

- 8:30 am: United States Mar 7 Initial Jobless Claims, est. 215k, prior 213k

- 8:30 am: United States Feb 28 Continuing Claims, est. 1849k, prior 1868k

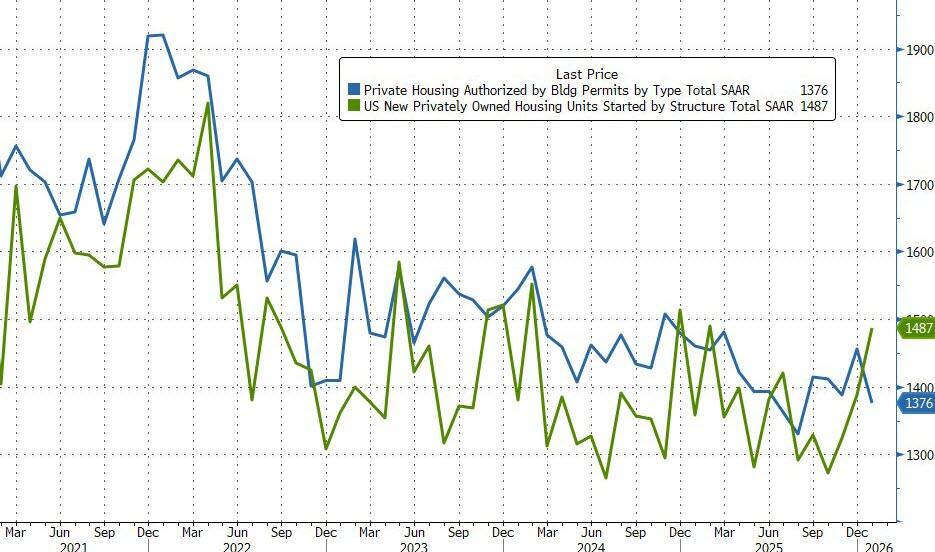

- 8:30 am: United States Jan Housing Starts, est. 1340.5k, prior 1404k

- 8:30 am: United States Jan P Building Permits, est. 1410k, prior 1455k

- 11:00 am: United States Fed’s Bowman Speaks on Basel III

DB’s Jim Reid concludes the overnight wrap

As we go to press this morning, the market volatility has shown no sign of easing, with Brent crude surging back +8.95% overnight to $100.21/bbl. The main catalyst for that has been further attacks on shipping, with two tankers and a container vessel struck in the Gulf this morning. Moreover, Bloomberg have also reported overnight that Oman has evacuated ships from the export terminal of Mina Al Fahal, which exports around 1mn barrels per day. So that’s driven a fresh surge in oil prices, and there’s been a clear risk-off move as a result. Indeed, futures on the S&P 500 (-0.86%) and the German DAX (-1.06%) have seen further declines this morning, and the major indices in Asia have all lost ground as well.

From a market perspective, the problem is that investors are increasingly pricing in a more protracted conflict that causes extensive economic damage. After all, with no concrete signs of de-escalation yet, that’s keeping oil prices elevated, and raising the risk of a broader stagflationary shock. Indeed, we know that investors are pricing in the longer scenarios, because the 6-month Brent future is also up +3.06% this morning to $82.97/bbl, and with each passing day it gets harder to argue that the disruption to shipping and energy infrastructure will only prove temporary.