MARCH 20/OUR SPECULATOR SHORTS WILL ASK FOR DIVINE INTERVENTION ONCE THEY RECEIVE NOTICE TO DELIVER UPON THEIR SHORTS; GOLD CLOSED DOWN $39.55 TO $4591.30 WITH SILVER DOWN $1.92 TO $69.33 //PLATINUM CLSOED UP $11.85 TO $1970.65 WITH PALLADIUM DOWN $1441.00//GOLD PODCAST OF ANDREW MAGUIRE TALKING TO DR DANIEL LACALLE//GOLD COMMENTARY TONIGHT COURTESY OF ALASDAIR MACLEOD//HIGHIGHTS FROM EUROPE: THE UK AND ON HJUNGRY//UPDATES FROM THE MIDDLE EAST: ISRAEL TBN THE LAST 24 HRS AND ALL THE HIGHLIGHTS ON THE BOMBING OF ENERGY FACILITIES ON THEM ALL//EXCELLENT USA ECONOMIC SCENE COURTESY OF TOM NASH//SWAMP STORIES FOR YOU TONIGHT///

099 H DEUTSCHE BANK AG 179 118 C MACQUARIE FUTURES US 10 190 H BMO CAPITAL MARKETS 34 363 H WELLS FARGO SECURITI 37 555 C BNP PARIBAS SEC CORP 7 624 H BOFA SECURITIES 494 22 661 C JP MORGAN SECURITIES 77 709 C BARCLAYS 231 905 C ADM 11 2

TOTAL: 552 552 MONTH TO DATE: 11,783

JPMORGAN STOPPED 77/552

MARCH

GOLD: NUMBER OF NOTICES FILED FOR MARCH/2026: 552 CONTRACTs NOTICES FOR 55,200 OZ or 1.716 TONNES

total notices so far: 11,783contracts for 1,178,300 OR 36.650tonnes)

FOR MARCH

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 138 NOTICE(S) FILED FOR 0.690 MILLION OZ /

total number of notices filed so far this month : 8681 CONTRACTS (NOTICES) for 43.405 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $39.55 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

HUGE CHANGES IN GOLD INVENTORY AT THE GLD:: A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/.

INVENTORY RESTS AT 1062.135 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $1.92 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 2.49 MILLION OZ INTO THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 488.271 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1464 CONTRACTS TO 112,034 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $6.22+ LOSS IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S // TRADING. WE ARE NOW AT OUR RECORD LOW OI OF 112,034 SURPASSING OUR PREVIOUS LOW OF 112,874 SET EARLIER IN THIS MONTH.

NOW ON A NET BASIS OUR SPECULATORS HAVE REVERTED BACK TO GOING SHORT. THE FRBNY ON A NET BASIS IS PROVIDING THE NECESSARY PAPER TO OUR LONGS AND THEN HUGE NUMBERS OF LONGS ,OUR BANKERS TOOK THE LONG SIDE ANDTENDER EDFOR PHYSICAL AT 4 PM EACH NIGHT. BECAUSE OF THE HUGE SHORTFALL IN PHYSICAL SILVER IN LONDON THERE IS A LOTTERY TO SEE WHO GETS ANY OF THE PHYSICAL SILVER AVAILABLE THAT WHICH THEY ARE OBLIGATED TO DELIVER. THEY WAIT PATIENTLY FOR THEIR PHYSICAL METAL AND IF NOBODY GETS ANY THEY THEN COME BACK THE NEXT DAY AND SO ON. THIS IS IN LONDON, THE HOME OF PHYSICAL SILVER!!

IT WAS SOME OF OUR SILVER SPECULATORS THAT WERE BRUTALLY BEATEN UP AT THE SILVER COMEX THIS PAST MONTH AS THEY GOT RINSED OUT BADLY AT LAST MONTH’S RAID ON FIRST DAY NOTICE FOR THE MAR CONTRACT/.HOWEVER, WE FINALLY ARE NOW MOVING TO A MUCH HIGHER BASE IN SILVER PRICING SURPASSING THE $70.00 SILVER PRICE BARRIER TO A HIGH DEGREE, AND NOW READY TO ATTACK AGAIN, OUR LAST MAJOR HURDLE OF $100.00 SILVER.

WE HAVE A STRONG SIZED LOSS OF 906TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A STRONG SIZED 558 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO THURSDAY TRADING//RAID/WITH OUR HUGE LOSS IN PRICE ALONG WITH A HUGE 2195 CONTRACT T.A.S. ISSUANCE!! / THEY DESPERATELY AGAIN TODAY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON WEDNESDAY WITH SILVER’S MASSIVELOSS IN PRICE

THE PRICE FINISHED STILL MASSIVELY ABOVE THE MAGIC NUMBER OF $70.00 SILVER SPOT PRICE BUT BELOW THE $100.00 MARK CLOSING AT $71.25 DOWN 6$.22 WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS AT A HUGE SIZED 2195 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING ABOVE THE 100.00 DOLLAR MARK!!.MAMMOTH SIZE T.A.S ISSUANCES ARE BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A STRONG SIZED 558 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 2195 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TODAY’S TRADING//AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HAD A STRONG LOSS OF 906 CONTRACTS ON OUR TWO EXCHANGES IDESPITE OUR MAMMOTH LOSS IN PRICE OF $6.22+. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE STICKY SPECULATOR LONGS STILL REMAIN STOIC EVEN ON OUR HUGE PRICE FALLS. THE NON STICKY SPECULATORS WERE WIPED OUT WITH OUR HUGE FEB 24TH RAID!! THE RAID ON 3 CONSECUTIVE DAYS WAS A MASSACRE TO THE PAPER PRICE OF SILVER BUT NOBODY SOLD AN OUNCE OF PHYSICAL SILVER WITH THE ABOVE MENTIONED RAID !

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, THROUGHOUT MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT//FRIDAY MORNING: A HUGE SIZED 2196 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS AS ONE UNIT, BUT SELL THE SHORT SIDE FIRST AND THEN LIQUIDATE THE LONG SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A SMALL QUEUE JUMP OF 17 CONTRACTS OR 0.085 MILLION OZ/NEW STANDING ADVANCES TO 43.980 MILLION OZ

WE HAD:

/ HUGE COMEX OI LOSS+// STRONG SIZED 558 EFP ISSUANCE CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 2195 CONTRACTS

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 81 SILVER CONTRACT//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB.. ACCUMULATION

TOTAL CONTRACTS for 15 DAY(S), total 9065contracts: OR 45.325 MILLION OZ (604 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 45.325MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 45.325 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1464 CONTRACTS DESPITE OUR MASSIVE LOSS IN PRICE OF $6.22 IN SILVER PRICING AT THE COMEX// THURSDAY,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED CONTRACT EFP ISSUANCE 558 CONTRACTS ISSUED FOR MAY, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. INITIAL STANDING 31.176 MILLION OZ FOLLOWED BY TODAY’S 0.0.085MILLION OZ QUEUE JUMP //STANDING ADVANCES TO 43.980 MILLION OZ. DESPITE HUGE SILVER DELIVERIES DURING THE PAST SEVERAL MONTHS, THIS PAST WEEK, WE HAVE REACHED OUR ABSOLUTE LOW POINT IN SILVER COMEX OI. (112,115). TODAY IT HIT OUR LOW POINT IN OI OF 112,034. RAIDS ACCOMPLISH NOTHING FOR OUR CROOKS AS LONGS WILL BE QUITE STICKYWITH THIS LOW COMEX OI!! HOWEVER WE HAD A HUGE INCREASE IN SPEC SHORTS AND THESE GUYS WILL HAVE TO DELIVER TO OUR LONGS .

LAST 11 MONTHS OF SILVER DELIVERIES

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY TODAY’S 0.0.085 MILLION OZ QUEUE //NEW TOTAL STANDING ADVANCESTO 43.980MILLION OZ

THE NEW TAS ISSUANCE THURSDAY NIGHT (2195 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!

WE HAD 138 NOTICE(S) FILED TODAY FOR 0.690 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT. THE SILVER COMEX IS NOW ON A MASSIVE SIEGE LOOKING FOR PHYSICAL SILVER!!

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6616 OI CONTRACTS DOWNTO 405,419 OI AND FURTHER DROM THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE ARE STILL CLOSE TO OUR ALL TIME NADIR OI IN COMEX BUT WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 3683 CRIMINAL CONTRACTS //.

WE HAD A STRONG SIZED LOSS IN COMEX OI (6616 ONTRACTS) . THIS LOSS OCCURRED DESPITE OUR MASSIVE LOSS IN PRICE OF $270.85 THURSDAY///.

LAST 10 MONTHS OF GOLD DELIVERIES: (MAY THROUGH TO /FEB)

MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES FOLLOWED BY TODAY’S STRONG 3.918 TONNES QUEUE JUMP AND THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 6.22 TONNES //NEW STANDING ADVANCES TO 45.5512TONNES/

E.F.P. ISSUANCE/FOR OPENING MARCH. GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2875 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 405,419AND WE NOW WITNESSING A LOWER COMEX OI BUT WITH AN EXTREMELY HIGH PRICE OF GOLD.//NOW ALMOST IMPOSSIBLE TO FLEECE. THIS LEVEL ADVANCES FROM ITS DECADES LOW OI AT 404,829.

SILVER ALSO HAS AN ULTRA SMALL SIZED AND RECORD LOW COMEX OI OF 112,034CONTRACTS// LOWERING A BIT FROM OUR PREVIOUS ALL TIME LOW SET MARCH 5 OF 112,878 CONTRACTS.

IN ESSENCE WE HAVE A FAIR LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3741 CONTRACTS WITH 6616 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 2875 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3741 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED BUT CRIMINAL 2318 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON LIKE TUESDAY THROUGH TO THURSDAY

GOLD PRICE ON THURSDAY FELL BY $279.85

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT(2318) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI OF 6616 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 3741 CONTRACTS..

WE HAVE 1) NOW REVERTED TO OUR ABNORMAL FORMAT OF BANKER (FRBNY) GOING ON THE LONG SIDE AND NEWBIE SPECULATORS GOING TO THE SHORT SIDE// . ,2.) STRONG FINAL STANDING FOR GOLD FOR FEBRUARY AND VERY STRONG FOR MARCH:

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.012 TONNES TO ALL OTHER QUEUE JUMPS//NEW QUEUE JUMP TOTALS INCREASES: 41.233 TONNES// /// TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK FOR 31.251 TONNES//NEW STANDING FINISHED AT 157.878 TONNES

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES FOLLOWED BY TODAY’S 3.968TONNES QUEUE JUMP FOLLOWED BY OUR FIRST EXCHANGE FOR RISK: 6.220///NEW STANDING ADVANCES TO 45.980TONNES OF GOLD./

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES FOLLOWED BY TODAY’S 3.968TONNES QUEUE JUMP +6.20 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 45.55127TONNES/

3) HUGE T.A.S. LIQUIDATION AND SOME GOVT LIQUIDATION // WITH A HUGE LOSSOF EQUITY SHARES/MARCH 18 HAVING 1)A $279.85 COMEX PRICE LOSS AND YET WE HAD 2) NEWBIE SPEC SHORTS GETTING CLOBBERED ON A NET BASIS, + EASTERN CENTRAL BANKERS WERE PILING INTO THE LONG SIDE AS WE HAD A SMALL SIZED LOSS OF 58 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A STRONG AMOUNT OF GOLD WILL STAND FOR DELIVERY IN MARCH. (45.5512TONNES). //, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED THURSDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4)A FAIR SIZED COMEX OI LOSS 5) V) STRONG SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD (2195) AND A STRONG T.A.S. ISSUANCE (2318) FOR RAID PURPOSES

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

TOTAL EFP CONTRACTS ISSUED: 50,579 CONTRACTS OR 5,057,900OZ OR 17.32 TONNES IN 15TRADING DAY(S) AND THUS AVERAGING: 3258 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN15 TRADING DAY(S) IN TONNES: 157.32TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2025, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 157.32TONNES DIVIDED BY 3550 x 100% TONNES = 4.43% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 157.32 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1464 CONTRACTS OI TO 112,034 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 112,034 CONTRACTS TODAY MARCH 20.2026

EFP ISSUANCE 558 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 558 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1464 CONTRACTS AND ADD TO THE 558 E.FP. ISSUED

WE OBTAIN A STRONG SIZED LOSS OF 906 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR MAMMOTH LOSS OF $6.22+

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.153MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $6.22+

2.ASIAN AFFAIRS MARCH 20 /2025

HANGHAI CLOSED DOWN 49.50 PTS OR 1.24 %

HANG SENG CLOSED DOWN 223.25 PTS OR 0.88%

Nikkei CLOSED DOWN 1687.50PTS OR 3.15%

//Australia’s all ordinaries CLOSED UDOWN0.49%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.8864

/ OFFSHORE CLOSED DOWN AT 6.8880 1Oil UP TO 96.20ollars per barrel for WTI and BRENT UP TO 109.95 Stocks in Europe OPENED ALL DEEPLY IN THE GREEN

ONSHORE USA/ YUAN TRADING 6.8864/ OFFSHORE YUAN TRADING DOWN TO 6.8880ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAK/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6616 CONTRACTS DOWN TO 405,419 OI , (CLOSE TO DECADES LOW OI OF 404,000. THE ALL TIME LOW IN OI IS 390,00 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00)

WE HAD HUGE T.A.S. LIQUIDATION DURING THURSDAY’S TRADING//RAID. IT SEEMS THAT THE SPECULATORS STARTED AGAIN TO GO MASSIVELY SHORT WITH THE BANKERS TAKING THE LONG SIDE, THUS THE REASON FOR A TNY LOSS IN CONTRACTS ON BOTH OF OUR EXCHANGES.

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MARCH CONTRACT MONTH!!

YOU WILL NOTICE THAT THE COMEX OI IS NOW MOVING SLIGHTLY AWAY FROM ITS DECADES ALL TIME LOW POINT IN OI OF 404,829 AND FROM THIS POINT, OI WILL RISE BUT IT WILL BE EXTREMELY DIFFICULT FOR THE CROOKS TO FLEECE OUR NEWBIE SPEC LONGS. THE ALL TIME EVER LOW OF COMEX OI IS 390,000 CONTRACTS WHICH OCCURRED IN 2001 WITH GOLD AROUND $260. FROM CHINA WE LEARN THAT TODAY, THE GOLD LEASE RATE IS NOW AROUND 1 TO 2 %.(SILVER IS AT 8%). WITH AN OI OF 409,102THERE IS LITTLE ROOM FOR THE CROOKS TO RAID OUR LONG SPECULATORSWHO ARE VERY STICKY AT THIS POINT. HOWEVER IT WAS THE SHORT SPECS THAT WILL BE MASSACRED TODAY AS THEY TENDERED FOR PHYSICAL DELIVERY.

WE THUS HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 3741 CONTRACTS (OR 11.63 TONNES) DESPITE THE HUGE LOSS IN PRICE, THURSDAY. SEEMS ON A NET BASIS NOBODY LEFT THE ARENA! ALSO WITH THAT HUGE RAID NOBODY SOLD ANY PHYSICAL GOLD.

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD 0 CONTRACTS FOR 0 OZ OR 0.00TONNES OF GOLD. DURING THE MIDDLE OF THEFEB. MONTH. WE HAVE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE ARE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB NOW REMAINED AT SIX.(31.251 TONNES).

AND NOW MARCH WAS GIVEN YESTERDAY ITS INITIAL 200 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. TODAY 0 ISSUANCE OF EXCHANGE FOR RISK.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MARCH:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUAY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD WHICH WILL BE ADDED TO OUR DELIVERY TOTALS. THUS, SO FAR ONE ISSUANCE

DETAILS ON OUR NEW MARCH COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 3741 CONTRACTS DESPITE OUR MASSIVE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MARCH/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 2318 T.A.S CONTRACTS (ENDING OUR 5 STRAIGHT DAY OF MEGA ISSUANCES LAST FRIDAY. . THESE WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING THIS WEEK WITH OUR CONTINUOUS 3 DAY RAID!

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S ONE ISSUANCE FOR 6.22 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH 1 EXCHANGE FOR RISK ISSUANCE SO FAR FOR 20000 CONTRACTS OR 200,000 OZ/6.220 TONNES.. BUT DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE:

FOR EXAMPLE:

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 11 MONTHS:

FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT STRONG QUEUE JUMP OF 3.968TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 6.220 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 45.5512TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING MARCH,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $279.85)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION THURSDAY // COMEX SESSION// WITH OUR LOSS IN PRICE BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD FOR FEBRUARY’S ACTIVE DELIVERY MONTH (157 TONNES) AND ALSO MARCH’S STANDING OF 43+ TONNES.

THURSDAY NIGHT//FRIDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING/FRIDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO MARCH:

ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT STRONG QUEUE JUMP 3.968 TO WHICH WE ADDD OUR FIRST EXCHANGE FOR RISK FOR 6.220 TONNES// GOLD STANDING ADVANCES TO: 45.5512 TONNES/

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $111.90

WE HAD A SMALL 34 CONTRACTS ADDED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE (YOU ADD CONTRACTS?)

NET LOSS ON THE TWO EXCHANGES : 3741 CONTRACTS OR 374100OZ OR 11/636TONNES

Total monthly oz gold served (contracts) so far this month

11,783 notices 1,178,300 oz 36.650 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0

DEPOSITS/CUSTOMER

0 ENTRY

0 entry

customer withdrawals:

comex is draining of gold/.

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs

ADJUSTMENTS 2

adjustments: / /

a) dealer to customer: Brinks: 144,583.047 oz

b) customer to dealer: 20,404.189. JPMorgan

net dealer gold removal: 124,175.855 oz

COMEX IS DRAINING GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

chaos inside the comex

THE FRONT MONTH OF MARCH OI STANDS AT 1414 CONTRACTS FOR A LOSS OF 224 CONTRACTS. WE HAD 1500 CONTRACTS SERVED ON THURSDAY, SO WE GAINED A STRONG 1276 CONTRACTS OR AN ADDITIONAL 127,600OZ WILL STAND FOR DELIVERY AT THE COMEX. THE TONNAGE EQUATES TO 3.9680TONNES . WE HAVE A MASSIVE AMOUNT OF GOLD WILLING TO STAND AS CENTRAL BANKERS CLAMOUR FOR OUR ANCIENT METAL OF KINGS ON THIS SIDE OF THE PLANET AND YET THIS HAPPENED WITH OUR HUGE RAID. IT PROVES NOBODY SOLD ANY PHYSICAL GOLD WITH THA HUGE DOWNFALL IN PRICE!

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 15,769 CONTRACTS DOWN TO 160,469 CONTRACTS. APRIL IS NOW THE NEW FRONT MONTH FOR DELIVERY OF GOLD. APRIL IS GENERALLY A VERY STRONG DELIVERY MONTH

MAY LOST 32 BCONTRACTS TO AN OI OF 932

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI ROSE BY A HUGE 8048 CONTRACTS DOWN TO AN OI OF 166,466

We had 552 contracts filed for today representing 55200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 552 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 77 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAR. /2026. contract month, we take the total number of notices filed so far for the month (11,753) to which we add the difference between the open interest for the front month of MAR (1414 CONTRACTS) minus the number of notices served upon today 552 x 100 oz per contract) equals 1,264,500OZ OR (39.3312Tonnes of gold) to which we add our first exchange for physical of 6.22 tonnes//standing advances to 45.5512 tonnes

thus the INITIAL standings for gold for the MAR contract month: No of notices filed so far (11,753 x 100 oz +we add the difference for front month of MAR (1414OI} minus the number of notices served upon today (552)x 100 oz) which equals 1,264,500OZ OR 39.3312 ONNES// to which we add our first exchange for risk of 6.22 tonnes//new standing advances to 45.5512

new total of gold standing in MAR is 45.5512 TONNES//

TOTAL COMEX GOLD STANDING FOR MARCH 45.5512 TONNES TONNES WHICH IS NOW MEGA HUGE FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF MARCH.

confirmed volume THURSDAY confirmed 399,979 ok

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,767,323.662 oz 54.97 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,767.323.662 tonnes oz 54.97 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 32,054,275.291 oz

TOTAL REGISTERED GOLD 16,518,712.066 or 513.803 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 15,535,563.225 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 14,751,389 oz ((REG GOLD- PLEDGED GOLD)=

458.830 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

SILVER COMEX

MARCH DELIVERY MONTH

MARCH 20 2026

INITIAL/

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

3 ENTRIES

i) Brinks: 616,162.834 oz ii) Delaware 969.90 oz iii) Manfra 1,413,2211.936 oz

total withdrawal: 2,030,354.670 oz

the comex is being drained of silver

Deposits to the Dealer Inventory

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Deposits to the Customer Inventory

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into CNT 40,890.850 oz

total deposit 40,890.850 oz

No of oz served today (contracts)

138. CONTRACT(S) ( 0.689 MILLION OZ

No of oz to be served (notices)

115 Contracts (0.575 MILLION oz)

Total monthly oz silver served (contracts)

8651 contracts 43.405 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRIES

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

ENTRIES: 0

1 ENTRIES

i) Into CNT 40,890.850 oz

total deposit 40,890.850 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

3 entries

i) Brinks: 616,162.834 oz

ii) Delaware 969.90 oz

iii) Manfra 1,413,2211.936 oz

total withdrawal: 2,030,354.670 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 4//dealer to customer acct:

a)) Asahi; 102,298.700 oz

b)CNT 40,932.900 oz

c) HSBC 63,950.200 oz

d) Stonex: 4991.430 oz

net removal from dealer silver: 212,172.830

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 79.149 MILLION OZ//.TOTAL REG + ELIGIBLE. 332.693 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH /2026 OI: 253 OPEN INTEREST CONTRACTS FOR A LOSS OF 224CONTRACTS.

WE HAD 241 NOTICES FILED ON THURSDAY SO WE GAINED A MALL17 CONTRACTS OR AN ADDITIONAL 0.085MILLION OZ OF SILVER WILL TRY FOR DELIVERY OVER HERE AS A BANKER ASSISTED QUEUE JUMP.

APRIL, THE NEW FRONT MONTH SAW A LOSS OF 111 CONTRACTS DOWN TO 1946 CONTRACTS

MAY SAW A LOSS CONTRACT LOSS OF 1095DOWN TO 73,318 CONTRACTS.

JUNE SAW A GAIN OF 5 CONTRACTS UP TO 411 OI CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 138 or 0.690 MILLION oz

CONFIRMED volume; ON THURSDAY 96,971 strong

AND NOW MARCH. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 8681 X5,000 oz = 43.405 MILLION oz

to which we add the difference between the open interest for the front month of MARCH (253) AND the number of notices served upon today (138)x (5000 oz)

Thus the standings for silver for the MARCH 2026 contract month: (8681)Notices served so far) x 5000 oz + OI for the front month of MARCH (253) minus number of notices served upon today (138 )x 5000 oz equals silver standing for the MAR..contract month equating to 43.980 MILLION OZ.

NEW STANDING: 43.980 MILLION OZ WHICH IS STILL LOWISH FOR A GENERALLY HUGE DELIVERY MONTH OF MARCH.

New total standing: 43.980 million oz.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 79.149 million oz of registered silver

JPMorgan as a percentage of total silver: 147.514/332.693million: 44.31%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

MAR 16/2026/WITH GOLD DOWN $60.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4/327 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1071/.565 TONNES

MAR 13/2026/WITH GOLD DOWN $61.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.428 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1075.852 TONNES

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

MAR 9/2026/WITH GOLD DOWN $53.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.573 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1073.321 TONNES

MAR 6/2026/WITH GOLD UP $77.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 5.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1075.894 TONNES

MAR 5/2026/WITH GOLD DOWN $49.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 18.032 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1081.038 TONNES

MAR 4/2026/WITH GOLD UP $9.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.545 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1099.07 TONNES

MAR 3/2026/WITH GOLD DOWN $188.75 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.35 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101.36 TONNES

MAR 2/2026/WITH GOLD UP $71.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101,13 TONNES

FEB 27/2026/WITH GOLD UP $52.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.90 TONNES

FEB 26/2026/WITH GOLD DOWN $30.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 11.45 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.62 TONNES

FEB 25/2026/WITH GOLD UP $48.40 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL WITHDRAWAL OF 0.300 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1086.17 TONNES

FEB 24/2026/WITH GOLD DOWN $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE PAPER DEPOSIT OF 7.72 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1086.47 TONNES

FEB 23/2026/WITH GOLD UP $148.25 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 20/2026/WITH GOLD UP $79.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.14 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1078.75 TONNES

FEB 19/2026/WITH GOLD DOWN $9.00 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 18/2026/WITH GOLD UP $102.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.43 TONNES OF GOLD OUT OF THE GLD/ /// ///INVENTORY RESTS AT 1075.61 TONNES

FEB 17/2026/WITH GOLD DOWN $136.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ /// ///INVENTORY RESTS AT 1077..04 TONNES

FEB 13/2026/WITH GOLD UP $94.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.140 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1076.18 TONNES

FEB 12/2026/WITH GOLD DOWN $143.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.000 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1081.32 TONNES

FEB 11/2026/WITH GOLD UP $63.65 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.34 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.32 TONNES

FEB 10/2026/WITH GOLD DOWN $46.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.43 TONNES OF GOLD FROM THE GLD/ /// ///INVENTORY RESTS AT 1079.66 TONNES

MAR 120 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

MAR 16 WITH SILVER DOWN $0.57: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.536 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 497.056 MILLION OZ.

MAR 13 WITH SILVER DOWN $3.83: NO CHANGES IN SILVER INVENTORY AT THE SLV// . ./ :INVENTORY RESTS AT 499.592

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

MAR 6 WITH SILVER UP $2.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 5.526 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508,287 MILLION OZ

MAR 5 WITH SILVER DOWN $0.98 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.097 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 512.726 MILLION OZ

MAR 4 WITH SILVER DOWN $0.21 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.545 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 513.813 MILLION OZ

MAR 3 WITH SILVER DOWN $5.27 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2/899 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 511.268 MILLION OZ

MAR 2 WITH SILVER DOWN $3.87 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.352 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 514.167 MILLION OZ

FEB 27 WITH SILVER UP $5.54 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 0.544 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 517.519 MILLION OZ

FEB 26 WITH SILVER DOWN $4.05 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 0.906 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 516.975 MILLION OZ

FEB 25 WITH SILVER UP $3.43 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 8.923 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 517.881 MILLION OZ

FEB 24 WITH SILVER UP $0.55 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 10.056 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 508.958 MILLION OZ

FEB 23 WITH SILVER UP $4.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT WITHDRAWAL OF 0.951 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 498.902 MILLION OZ

FEB 20 WITH SILVER UP $4.85 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.035 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.853 MILLION OZ

FEB 19 WITH SILVER DOWN $0.23 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 5.798 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 502.888 MILLION OZ

FEB 18 WITH SILVER UP $4.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT WITHDRAWAL OF 11.325 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508.686 MILLION OZ

FEB 17 WITH SILVER DOWN $4.39 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 4.253 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 515.753 MILLION OZ

FEB 13 WITH SILVER UP $2.35 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.994 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 520.011 MILLION OZ

FEB 12 WITH SILVER DOWN $8.78 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 635,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 522.005 MILLION OZ

FEB 11 WITH SILVER UP $3.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 815,000 OZ INTO THE SLV. ./ :INVENTORY RESTS AT 521.370 MILLION OZ

FEB 10 WITH SILVER DOWN $2.21 NO CHANGES IN SILVER INVENTORY AT THE SLV//. ./ :INVENTORY RESTS AT 520.555 MILLION OZ

Paper gold and silver have sold down in light trade. The bullion establishment is scrambling to close its shorts and go long as the outlook for gold gets increasingly bullish.

The chart below shows that gold could be described as consolidating nicely giving it a firm platform for its next leg up against the dollar. Meanwhile, the war in Iran is destabilising the world’s exporter of investment capital — Japan. The consequences are bound to speed up the collapse of bond and equity prices, and therefore the life of all fiat currencies. Despite its current volatility, physical gold remains the true safe haven.

This week, gold and silver were marked down heavily in financial markets awakening to the reality of a prolonged conflict against Iran. Yesterday (Thursday) was particularly challenging though there has been some recovery from the lows. At the time of writing, gold this morning is $4,670 down $345 over the week, and silver at $71.90 is down $8.60. On the sharp selloff, gold’s volume on Comex has picked up sharply indicating a possible bottom, while silver’s less so.

For investment managers the playbook replicates that of the 2008-2009 financial crisis, when gold fell from $1,000 to $680 while equities crashed and the dollar’s trade weighted rose from 72 to 88. The highly liquid dollar is perceived as safety at times of extreme crisis and this time is no different, with the dollar’s rally taking it back up from 96.30 to test the 100 level:

Following the 2008-2009 30% decline in the gold price, the consequences of the financial crisis led to gold tripling to $1,920, and the dollar’s TWI declining from 88 to 75. This is the pattern being followed today — so far.

Whether bullion bank traders and market makers understand this is not an issue. They take each day as it comes, using every opportunity to level their books while trading profitably. When they perceive speculators are long and their buying pauses, they will mark down prices to take out long stops. And vice-versa for the shorts. However, the difference today is that speculators have minimal long positions to shake out. This is particularly noticeable in silver, where on this morning’s preliminary estimate Comex open interest is the lowest it has been for over 20 years:

Clearly, the current markdown in silver is paper vapour, meaningless in terms of its physical value. The same can be said of gold despite its increased marketability compared with silver. While bullion banks in the West play their paper games, such is the demand for physical gold in China that their banks are rationing customers, with daily allocations reportedly sold out within minutes. This is sucking gold out of other centres.

Chinese and Asian savers have a better grasp of the implications of the war on Iran than their Western counterparts, since they are more reliant on energy from the Persian Gulf. Nowhere is this more economically destructive than for Japan which depends on the Gulf for 70% of her oil and 90% from the whole region. This explains why the Nikkie index has been the worst casualty of the war so far. But this is only the start of Japan’s problems, and therefore of all credit markets.

Lau Vegys of Doug Casey’s Crisis Investing (dougcasey@substack.com) points out that as a consequence of the 1973 oil crisis, Japan’s inflation rate rose 20% and panic buying emptied store shelves. He goes on to point out that the problem today is compounded by the dire state of Japan’s finances with debt to GDP of 255%.

Clearly, inflation of prices will be a major problem for Japan in the coming months. Not only will the Bank of Japan be forced to raise interest rates sharply if it is to prevent the yen collapsing. Equities will crash and bond yields soar. As the chart below illustrates, these bond yields are already the highest they have been for decades:

Current JGB yields are nowhere near discounting an inflation surge and they should be on their way to 10% or even more. Not only would that collapse the entire Japanese financial system and its currency, but Japan’s institutions are the world’s largest exporters of investment capital, and the yen is the basis of the carry trade into dollar debt — both of which are bound to cease and reverse.

Today, this is the obvious source of future global credit instability. And along with Japan, other G7 nations seeing their 10-year bond yields challenging new high ground are the UK, Germany, and France. We are entering falling-dominoes territory, where the only safety is to get out of all forms of credit including currencies and equity markets.

In conclusion, a global financial credit crises in being brought forward in time. Today’s markdowns in gold and silver are simply sucker plays designed to deceive amateur investors who will come to regret being hoodwinked into selling by professional traders.

3.CHRIS POWELL AND HIS GATA DISPATCHES:

4. ANDREW MAGUIRE AND LIVE FROM THE VAULT PODCASTS NO 264/263

5. COMMODITY REPORT//

ASIAN AFFAIRS MARCH 20/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 49.50 PTS OR 1.24 %

HANG SENG CLOSED DOWN 223.25 PTS OR 0.88%

Nikkei CLOSED DOWN 1687.50PTS OR 3.15%

//Australia’s all ordinaries CLOSED UDOWN0.49%

//Chinese yuan (ONSHORE) CLOSED DOWN 6.8864

/ OFFSHORE CLOSED DOWN AT 6.8880 1Oil UP TO 96.20ollars per barrel for WTI and BRENT UP TO 109.95 Stocks in Europe OPENED ALL DEEPLY IN THE GREEN

ONSHORE USA/ YUAN TRADING 6.8864/ OFFSHORE YUAN TRADING DOWN TO 6.8880ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAK/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.8864

OFFSHORE YUAN: DOWN TO 6.8880

1.HANG SANG DOWN 223.35 POINTS OR 0.88%

2. Nikkei closed DOWN 1687.80PTS OR 3.15%

WEST TEXAS INTERMEDIATE OIL UP TO 96.20

BRENT; 109.95

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 99.33/// EURO FALLS TO 1.1565 DOWN 13 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.264 UP 4FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.91… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.526 UP 4 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: 6.8864(DOWN AND OFFSHORE: DOWNAT 6.8880

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UPTO +2.9783Italian 10 Yr bond yield UP to 3.818 BSPAIN 10 YR BOND YIELD UP TO 3.491

3i Greek 10 year bond yield UP TO 3.797

3j Gold at $4990.59 Silver at: 72.95 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 2AND 18 100 roubles/84.08

3m oil (WTI) into the 96 dollar handle for WTI and 109handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.97 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.264% UP 2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.526 UP 2 PTS..: USA/SF this 0.7881 as the Swiss Franc . Euro vs SF: 0.9195

USA 10 YR BOND YIELD: 4.293 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.864 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.886 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 44.24 UP 0 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.48980 UP 6 PTS

30 YR UK BOND YIELD: 5.490 UP 5 BASIS PTS

10 YR CANADA BOND YIELD: 3.438 DOWN 2BASIS PTS

5 YR CANADA BOND YIELD: 3.045 UP 3 BASIS PTS.

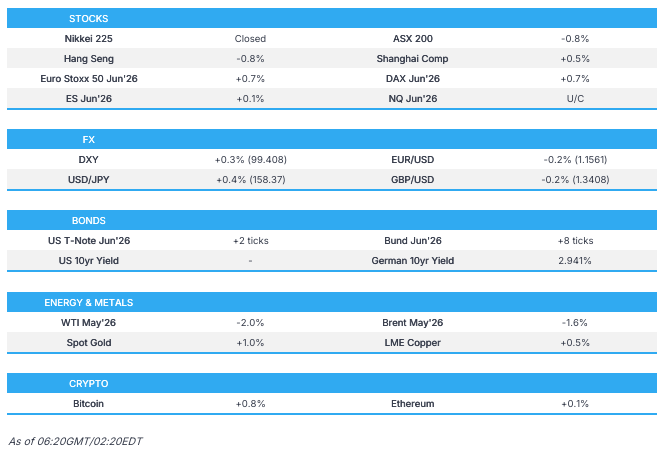

1a New York Opening report

Futures Slide Ahead Of Massive $5.7 Trillion OpEx As Iran War Shows No Signs Of Easing

Friday, Mar 20, 2026 – 08:37 AM

Futures are weaker heading into the weekend after US equities finished lower yesterday despite Netanyahu headlines leading to a late day bounceback into EOD. Geopolitical headlines remain the focus overnight with Brent rising as much as 90bps before reversing, as Iran pressed ahead with hitting energy assets & headlines that the US is considering plans to occupy Iran’s Kharg Island to press for the reopening of the Strait of Hormuz. As of 8:15am, S&P 500 futures fell 0.4% after finishing on Thursday under its 200-day moving average which could trigger even more forced selling; Nasdaq 100 futures declined 0.6%. US stocks are on course for a fourth week of losses, the longest losing streak in a year. Brent crude oil prices reversed earlier gains to decline 0.7% to around $108. The VIX rose to around 25. Elsewhere, it was a relatively quiet overnight with upward pressure on yields still the focus (USGG10YR +4bps @ 4.29%) amid concerns about hawkish central bank reaction functions. Metals are mostly lower: Aluminum -4.4%, Silver -1.0%. The US Dollar is up 0.2% as markets price in less than 5bp of Fed rate cuts this year, down from 60bp last month. There is no macro on today’s calendar.

In premarket trading, Mag 7 stocks are all lower (Alphabet -0.7%, Amazon -0.6%, Tesla -0.4%, Nvidia -0.5%, Meta -0.4%, Microsoft -0.5%, Apple -0.4%)

FedEx (FDX) climbs 7% after raising its full-year profit forecast, signaling that the courier’s plan to restructure its delivery network is gaining traction despite geopolitical conflict and economic volatility.

Figs Inc. (FIGS) rises 6% after Oppenheimer upgraded the seller of medical scrubs to outperform, saying a sustained recovery is underway.

Firefly Aerospace (FLY) gains 7% after the spacecraft maker reported revenue for the fourth quarter that beat the average analyst estimate

Planet Labs (PL) gains 14% after the satellite imaging firm reported revenue for the fourth quarter that beat the average analyst estimate.

Rhythm Pharmaceuticals (RYTM) rises 6% after the drugmaker said it received expanded indication approval from the FDA for its drug Imcivree (setmelanotide) to treat patients four years and older with acquired hypothalamic obesity.

Super Micro Computer Inc. (SMCI) tumbles 26% after the US charged a co-founder with illegally diverting billions of dollars in Nvidia Corp.-powered servers to China.

York Space Systems (YSS) rises 9% after the space and defense company gave revenue guidance in its first report as a public company that JPMorgan called “solid.” The firm also saw revenue grow and its losses narrow in the fourth quarter.

In other corporate news, at least a dozen large drugmakers are set to roll out copies of Novo Nordisk’s blockbuster weight-loss drugs in India, crashing prices as soon as the patent expires Friday. JPMorgan started a monitoring program to guard against overwork by its junior investment bankers, according to the Financial Times. Alibaba and Tencent lost $66 billion of market value in 24 hours after failing to lay out clear visions for how to profit off AI. Meanwhile, investors overwhelmed by Iran news are turning to AI tools – mining history for insights and context to assist work-flows and time management.

“Investors are stuck in geopolitical pinball right now,” said Max Gokhman, deputy CIO at Franklin Templeton Investment Solutions, as “literally and figuratively explosive developments are bouncing global market sentiment.” Confidence is being tested, and different schools of thought on the length of conflict are emerging.

An ugly, rollercoaster week is set to end with the Iran war – about to enter its third week – showing no signs of easing as Tehran keeps up attacks on Arab states in the Persian Gulf even after Israel signaled it would spare the country’s energy infrastructure. Axios reported the US is considering plans to take over Iran’s key oil-export site Kharg Island to add pressure on Tehran to reopen the Strait of Hormuz. Iran’s Revolutionary Guard insists it’s still building missiles and vowed the war will continue. Oil is headed for another weekly surge.

“I think that the market is right now coming to grips with the reality that higher energy prices are going to persist longer than expected,” said Mark Malek, chief investment officer at Siebert Financial. “It is clear that the Iran regime turned to the last page in its playbook: MAD, mutually assured destruction.”

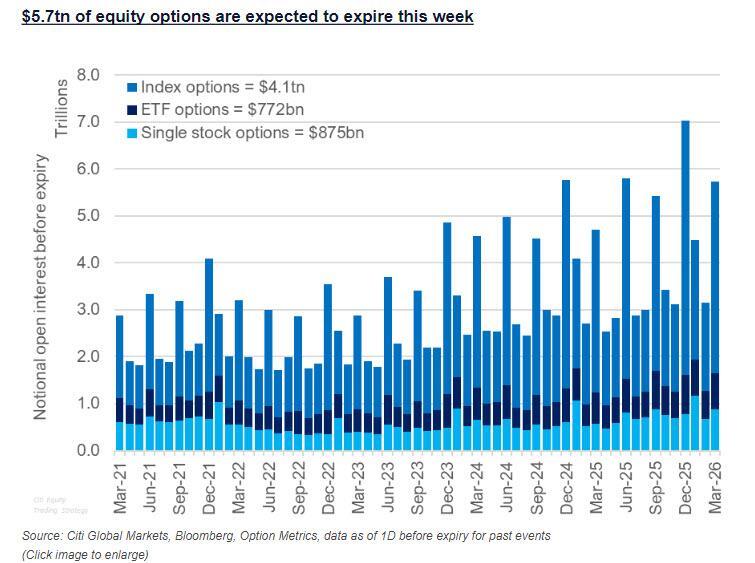

Meanwhile, traders braced for a historic amount of March options expiry. Roughly $5.7 trillion in notional options tied to individual US stocks, indexes and exchange-traded funds are set to expire on Friday in the quarterly event that traders have dubbed the “triple-witching”, the largest March expiry in 30 years and one the 4th largest ever. That includes $4.1 trillion in index contracts, $772 billion in exchange-traded funds and $875 billion in single-stock options. The event has a reputation for triggering abrupt price swings as large pools of derivatives exposure suddenly vanish. It also tends to reset dealer gamma sharply lower, unleashing an “unclenching” that lead to higher volatility in subsequent days. The scale of this week’s expiration is also notable relative to the broader market. At 8.4% of Russell 3000 Index market capitalization, it’s well above historical norms, amplifying the potential for positioning-driven flows.

Trading activity in options markets has surged in recent weeks, particularly in index and ETF contracts, both of which hit record notional volumes in March, about 9% above their year-to-date averages, according to Citi’s Vishal Vivek. In contrast, single-stock options volumes are roughly 3% below the level, a move partly attributed to waning retail participation and worries around geopolitical risks.

Stocks including Regeneron Pharmaceuticals Inc., PDD Holdings Inc. and T. Rowe Price Group Inc. are among those seen as vulnerable to outsized moves during the session as they have large open interest in options that expire near the current prices, according to Citi.

“Given recent volatility, today could almost be described as unchanged but clearly the bias has been lower,” said Sameer Samana, head of global equities and real assets at Wells Fargo Investment Institute. “I think the true test of today will be what investors decide to do at the close, before the weekend.”

Crude oil prices continued to be traders’ main concern as it affects inflation and consumer sentiment. The latest oil future curves showed “markets are beginning to price a more persistent ‘higher for longer’ oil backdrop,” Barclays strategists including Emmanuel Cau said in a note. “This dynamic is reinforcing stagflation concerns.”

On Wednesday, Jerome Powell said the Fed will not lower interest rates until inflation cools, as it was too early to determine the impact of rising oil prices on the US economy. The central bank left rates steady for a second straight meeting.

“We think the Fed staying on hold remains the most appropriate positioning,” said Deborah Cunningham, chief investment officer for global liquidity markets at Federated Hermes. “The current conflict with Iran is nowhere near the magnitude of the disruptions seen during COVID, nor the 2008 global financial crisis, so there is no justification for cutting rates by hundreds of basis points.”