EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,647.600000000 USD

INTENT DATE: 03/31/2026 DELIVERY DATE: 04/02/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 25 46

092 C DEUTSCHE BANK 235

099 H DEUTSCHE BANK AG 1721

104 C MIZUHO SECURITIES US 3

118 C MACQUARIE FUTURES US 23

118 H MACQUARIE FUTURES US 170

323 H HSBC 242

332 H STANDARD CHARTERED B 481

363 H WELLS FARGO SECURITI 215

365 C MAREX CAPITAL MARKET 16

435 H SCOTIA CAPITAL (USA) 1

555 C BNP PARIBAS SEC CORP 389

624 H BOFA SECURITIES 77

657 C MORGAN STANLEY 105

661 C JP MORGAN SECURITIES 1590 418

686 C STONEX FINANCIAL INC 4

686 H STONEX FINANCIAL INC 1

709 C BARCLAYS 12 759

732 C RBC CAP MARKETS 187

737 C ADVANTAGE FUTURES 4

905 C ADM 6

DLV615-T CME CLEARING

BUSINESS DATE: 03/31/2026 DAILY DELIVERY NOTICES RUN DATE: 03/31/2026

PRODUCT GROUP: METALS RUN TIME: 20:37:25

TOTAL: 3,365 3,365

MONTH TO DATE: 13,503

JPMORGAN STOPPED 1078/10,138

MARCH 31

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2026: 3,365 CONTRACTs NOTICES FOR 336,500 OZ or 10.466TONNES

total notices so far: 13,503 contracts for 1,350,300 OR 42.0000 tonnes)

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000 OZ /

total number of notices filed so far this month : 1184 CONTRACTS (NOTICES) for 5.920 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A STRONG QUEUE JUMP OF 42 CONTRACTS OR 0.210 MILLION OZ/NEW STANDING REDUCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 17 CONTRACT EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE 85,000 OZ WILL TAKE DELIVERY OVER ON THAT SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS IS REDUCED TO 7.035 MILLION OZ

NOW OUR APRIL 2026 CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 4.475 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 85,00 OZ EXCHANGE FOR PHYSICAL TRANSFER//NEW STANDING REDUCES TO 7.035 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR STRONG 53,000 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON//NEW STANDING IS THUS REDUCED TO 51.175 TONNES/

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 46 CONTRACT QUEUE JUMP OF 4400 OZ OR 0.2320 TONNESAND THEN WE ADD BY OUR THREE EXCHANGE FOR RISK: 22.3818///NEW STANDING ADVANCES TO 67.6648 TONNES OF GOLD./

APRIL: INITIAL STANDING FOR GOLD; 52.600 TONNES FOLLOWED BY TODAY’S 53,000 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON//NEW STANDING REDUCES TO 51.035 TONNES.

STANDING FOR THE LAST 4 MONTHS JANUARY TO APRIL:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES MINUS OUR 1.678 TONNES OF EXCHANGE FOR PHYSICAL TRANSFER: NEW STANDING REDUCES TO 51.175 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 9.228 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONG

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1242 CONTRACTS OI TO 115,169 AND CLOSER THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 111,576 CONTRACTS MARCH 20.2026

EFP ISSUANCE 895 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 895 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1242 CONTRACTS AND ADD TO THE 895 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 2137 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $4.22

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 10.685 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $4.22

2.ASIAN AFFAIRS APRIL 1 /2025

SHANGHAI CLOSED UP 56.69 PTS OR 1.46%

HANG SENG CLOSED UP 574.00 PTS OR 2.25%

Nikkei CLOSED UP 2709.28 PTS OR 5.31%

//Australia’s all ordinaries CLOSED UP 1.20%

//Chinese yuan (ONSHORE) CLOSED UP 6.8740

/ OFFSHORE CLOSED UP AT 6.8961 Oil DOWN TO 97.47 ollars per barrel for WTI and BRENT DOWN TO 99.84 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8740 (UP) OFFSHORE YUAN TRADING UP TO 6.8767 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG 5901 CONTRACTS DOWN TO 361,409 CONTRACT OI , HAVING NOW REACHED A NEW RECORD LOW OI SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 367,310 SET MARCH 31/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 361,409 WITH GOLD AT AN EXTREMELY HIGH $4,696.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD STRONG T.A.S. LIQUIDATION DURING TUESDAY’S TRADING ALONG WITH FINALIZATION OF MONTHLY SPREADER LIQUIDATION. IT SEEMS THAT THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY LONG WITH THE BANKERS TAKING THE SHORT SIDE, WITH OUR TWO SPREADER LIQUIDATIONS ACCOUNTING FOR THE LOSS IN OI!!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MARCH CONTRACT MONTH!!

THE FAIR SIZED LOSS ON OUR TWO EXCHANGES OCCURRED DESPITE OUR HUGE GAIN IN PRICE IN GOLD. THE SPECS HAVE NOW GONE MASSIVELY ON THE LONG SIDE WITH THE BANKERS BUYING UP ALL THEY COULD AND COVERING THEIR SHORTFALL IN GOLD. THE SHORT SPECS WERE MURDERLIZED LAST WEEK.

WE THUS HAD A FAIR LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 2934 CONTRACTS (OR 26.77 TONNES) DESPITE OUR HUGE GAIN IN PRICE, AS WE WERE INFORMED OF A STRONG 2967 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE..

THEN WE WERE NOTIFIED TODAY OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD.

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 0 EXCHANGE FOR RISK FOR FAR.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO APRIL:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUAY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 0 EXCHANGE FOR RISK SO FAR.

DETAILS ON OUR NEW APRIL COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 2934 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE ($119.65). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH APRIL/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1694 T.A.S CONTRACTS. THESE AND NOW ACCOMPANIED WITH OUR FINALIZATION OF MONTHLY SPREADER LIQUIDATION AS THEY ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING THIS WEEK WITH MUCH FAILURE DURING LONDON LBMA/OTC OPTION EXPIRY WEEK!!

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH WE HAVE 3 EXCHANGE FOR RISK ISSUANCES SO FAR FOR 7196 CONTRACTS OR 719,600 OZ/22.3818 TONNES.. AS DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE!!

APRIL: 0 SO FAR HAVE BEEN ISSUED

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

AND NOW APRIL 2026: INITIAL STANDING FOR GOLD: 52.600 TONNES FOLLOWED BY TODAY’S HUGE 53,000 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON. THUS STANDING FOR GOLD AT THE COMEX IS REDUCED TO 51.175 TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING APRIL,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $119.65

WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION TUESDAY ALONG WITH FINALIZATION OF MONTHLY SPREADER LIQUIDATION // COMEX SESSION// DESPITE OUR HUGE GAIN IN PRICE BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI // BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD FOR FEBRUARY’S ACTIVE DELIVERY MONTH (157 TONNES) , MARCH’S STANDING OF 67+ TONNES+ TODAY’S HUGE APRIL’S DELIVERY TOTALS A VERY STRONG 51 + TONNES

TUESDAY NIGHT//WEDNESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO APRIL:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK FOR 22.3818 TONNES// GOLD STANDING ADVANCES TO: 67.6648 TONNES/

APRIL: INITIAL STANDING: A VERY STRONG 52.600 TONNES FOLLOWED BY TODAY’S HUGE 53,000 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON (1.648 TONNES). THUS STANDING FOR GOLD AT THE COMEX IS NOW REDUCED TO 51.175 TONNES OF GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $119.65

WE HAD A FAIR 1686 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES : 2934 CONTRACTS OR 293,400 OZ OR 26.77 TONNES

INITIAL GOLD COMEX

APRIL DELIVERY MONTH

APRIL 1 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRY xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 3,365 CONTRACTS OR 336,500 OZ 10.466 TONNES OF GOLD |

| No of oz to be served (notices) | 2950 Contracts 295,000 OZ 9.175 TONNES |

| Total monthly oz gold served (contracts) so far this month | 13,503 notices 1,350,300 oz 42.0000 ONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

DEPOSITS/CUSTOMER

0 ENTRY

0 entry

customer withdrawals:

0 ENTRIES

comex is draining of gold/.

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs

ADJUSTMENTS dealer to customer

i) Asahi 19,814.042 oz

ii) Brinks 15,641,106 oz

iii) Manfra: 3,101.153. oz

total removed from dealer (reg) to eligible 38,556.301 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF APRIL OI STANDS AT 6315 CONTRACTS HAVING A HUGE LOSS OF 10,668 CONTRACTS.

WE HAD 10,138 CONTRACTS YESTERDAY SO WE LOST 530 CONTRACTS OR 53000 OZ (1.648 TONNES) AS THEY UNDERWENT A STRONG EXCHANGE FOR PHYSICAL TRANSFER TO LONDON SO AS TO TAKE DELIVERY OVER IN LONDON ON A FAST T PLUS ONE BASIS. THEY NEEDED GOLD IN A HURRY.

MAY GAINED 76 CONTRACTS TO AN OI OF 5441

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI ROSE BY A HUGE 3558 CONTRACTS UP TO AN OI OF 268,353

We had 3365 contracts filed for today representing 336,500oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 1590 notices issued from their client or customer account. The total of all issuance by all participants equate to 13,503 contract(s) of which 418 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (13,503) to which we add the difference between the open interest for the front month of APRIL (6315 CONTRACTS) minus the number of notices served upon today 3365 x 100 oz per contract) equals 1,645,300 OZ OR (51.175Tonnes of gold)

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (13,503 x 100 oz +we add the difference for front month of APRIL (6315 OI} minus the number of notices served upon today (3,365 )x 100 oz) which equals 1,645,300 OZ OR 51.175 TONNES//

new total of gold standing in APRIL is 51.175 TONNES//

TOTAL COMEX GOLD STANDING FOR APRIL 51.175 TONNES TONNES WHICH IS NOW MEGA HUGE FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF MARCH.

confirmed volume TUESDAY confirmed 197,318 poor

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,822.966.773 oz 56.70 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,822,966.773 tonnes oz 56.70 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 31,533,900.538 oz

TOTAL REGISTERED GOLD 16,524,687.166 or 513.98 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 14,917,970,657.171 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 14,701,721 oz ((REG GOLD- PLEDGED GOLD)=

457.28 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

APRIL DELIVERY MONTH

APRIL1

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries i) JPMorgan 160,715.000 oz total withdrawal: 106,715.000 oz |

| Deposits to the Dealer Inventory | 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 2 ENTRIES i) Into Delaware: 15,219.685 oz ii) Into HSBC 218,028.390 oz total deposit: 231,241.005 pz |

| No of oz served today (contracts) | 3 CONTRACT(S) ( 15,000 OZ |

| No of oz to be served (notices) | 223 Contracts (1.115 MILLION oz) |

| Total monthly oz silver served (contracts) | 1184 contracts 5.920 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

1 entries

1 entries

i) JPMorgan 160,715.000 oz

total withdrawal: 106,715.000 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 2

ADJUSTMENTS 2

first one: dealer to customer Manfra: 14,636.800 oz

next : Customer to dealer account

b) Stonex: 5194.73 oz

net loss dealer 9442 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 76.420 MILLION OZ//.TOTAL REG + ELIGIBLE. 327.659 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2026 OI: 226 OPEN INTEREST CONTRACTS FOR A LOSS OF 1198 CONTRACTS. WE HAD 1181 CONTRACTS SERVED YESTERDAY, SO WE LOST 17 CONTRACTS OR 85,000 OZ UNDERWENT AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON. THIS IS THE FIRST TIME WE WITNESS THAT BOTH GOLD AND SILVER HAD AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON. I GUESS NO CONFIDENCE IN THE COMEX

MAY SAW A GAIN OF 1828 CONTRACTS UP TO 73,622 CONTRACTS.

JUNE SAW A LOSS OF 76 CONTRACTS UP TO 407 OI CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 or 15,000 oz

CONFIRMED volume; ON TUESDAY 53,067 awful

AND NOW APRIL. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1184 X5,000 oz = 5.920 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (226) AND the number of notices served upon today (3)x (5000 oz)

Thus the standings for silver for the APRIL 2026 contract month: (1184 )Notices served so far) x 5000 oz + OI for the front month of APRIL (226) minus number of notices served upon today (3 )x 5000 oz equals silver standing for the APRIL..contract month equating to 7.035 MILLION OZ.

NEW STANDING: 7.035 MILLION OZ WHICH IS STRONG FOR A GENERALLY LOUSY DELIVERY MONTH OF APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 76.420 million oz of registered silver

JPMorgan as a percentage of total silver: 145.341/659million: 44.44%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

MAR 16/2026/WITH GOLD DOWN $60.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4/327 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1071/.565 TONNES

MAR 13/2026/WITH GOLD DOWN $61.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.428 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1075.852 TONNES

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

MAR 9/2026/WITH GOLD DOWN $53.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.573 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1073.321 TONNES

MAR 6/2026/WITH GOLD UP $77.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 5.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1075.894 TONNES

MAR 5/2026/WITH GOLD DOWN $49.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 18.032 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1081.038 TONNES

MAR 4/2026/WITH GOLD UP $9.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.545 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1099.07 TONNES

MAR 3/2026/WITH GOLD DOWN $188.75 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.35 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101.36 TONNES

MAR 2/2026/WITH GOLD UP $71.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101,13 TONNES

FEB 27/2026/WITH GOLD UP $52.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.90 TONNES

FEB 26/2026/WITH GOLD DOWN $30.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 11.45 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.62 TONNES

FEB 25/2026/WITH GOLD UP $48.40 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL WITHDRAWAL OF 0.300 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1086.17 TONNES

FEB 24/2026/WITH GOLD DOWN $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE PAPER DEPOSIT OF 7.72 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1086.47 TONNES

GLD INVENTORY: 1047.276 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

MAR 16 WITH SILVER DOWN $0.57: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.536 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 497.056 MILLION OZ.

MAR 13 WITH SILVER DOWN $3.83: NO CHANGES IN SILVER INVENTORY AT THE SLV// . ./ :INVENTORY RESTS AT 499.592

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

MAR 6 WITH SILVER UP $2.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 5.526 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508,287 MILLION OZ

MAR 5 WITH SILVER DOWN $0.98 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.097 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 512.726 MILLION OZ

MAR 4 WITH SILVER DOWN $0.21 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.545 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 513.813 MILLION OZ

MAR 3 WITH SILVER DOWN $5.27 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2/899 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 511.268 MILLION OZ

MAR 2 WITH SILVER DOWN $3.87 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.352 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 514.167 MILLION OZ

FEB 27 WITH SILVER UP $5.54 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 0.544 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 517.519 MILLION OZ

FEB 26 WITH SILVER DOWN $4.05 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 0.906 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 516.975 MILLION OZ

FEB 25 WITH SILVER UP $3.43 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 8.923 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 517.881 MILLION OZ

FEB 24 WITH SILVER UP $0.55 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 10.056 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 508.958 MILLION OZ

FEB 23 WITH SILVER UP $4.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT WITHDRAWAL OF 0.951 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 498.902 MILLION OZ

CLOSING INVENTORY 491.079 MILLION OZ OF SILVER..

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

MATHEW PIEPENBURG…

JOHN RUBINO

JESSE COLUMBO

ALASDAIR MACLEOD.

3.CHRIS POWELL AND HIS GATA DISPATCHES:

4. ANDREW MAGUIRE AND LIVE FROM THE VAULT PODCASTS NO 265

end.

5. COMMODITY REPORT//ALUMINUM

Aluminum Supply Shock: Top Gulf Producer Halts Operations After Iran Strike, Price To Spike

Wednesday, Apr 01, 2026 – 11:52 AM

Over the weekend, both Emirates Global Aluminum (EGA) – the largest aluminum producers in the Gulf – and Aluminium Bahrain (ALBA) reported drone attacks damaging smelting facilities after hits on Iranian steel infrastructure last week.

Neither company (at the time) confirmed whether supply will be impacted, but this morning the worst case appears to be confirmed with Reuters reporting that according to a Wednesday note by consultancy Wood Mackenzie “EGA’s Al Taweelah facility in the United Arab Emirates halted operations after an Iranian missile and drone attack on Saturday damaged a power plant.” A subsequent report from Bloomberg confirmed the report, writing that “Emirates Global Aluminium, the Middle East’s top producer of the metal, halted operations at its Al Taweelah smelter after the site was struck by Iranian missiles and drones over the weekend, according to a person familiar with the matter.“

At the same time, the smelter belonging to Aluminium Bahrain – Alba – which was also targeted on Saturday, “sustained significant damages and is expected to operate at an estimated utilisation of 30 percent”, Wood Mackenzie said.

“The ongoing Middle East conflict is triggering a critical supply crisis in the global aluminium market, with disruptions potentially removing 3 to 3.5 million tonnes of output in 2026,” Wood Mackenzie said. For context, the world produced just under 74 million tonnes of primary aluminum last year.

Wood Mackenzie’s press office said its information was sourced from the consultancy’s contacts in the Middle East, but declined to provide further details.

As a reminder, the aluminum smelter in Al Taweelah, in the emirate of Abu Dhabi, has a capacity of roughly 1.5 million metric tonnes per year, and an alumina refinery. Alba’s capacity of 1.6 million tonnes per year in Bahrain makes it the world’s biggest single-site aluminium smelter. The Middle East as a whole produces about 9% of global supply, with EGA and others playing a key role in supplying manufacturers across Europe, Asia and the US. Even before the industry was directly targeted, the effective closure of the Strait of Hormuz had already left the region’s major producers short of critical inputs, with the sector anticipating a cascading wave of production cuts unless the strait reopens soon.

As Goldman commodity specialist James McGeoch writes, it’s “hard to think of a bigger metal supply shock: High degree of expectation this was where it was heading, but the initial reaction was to fade the uncertainty yesterday, that should be replaced by fresh length if history is a guide.”

This is how the Goldman trader does the math on lost output:

Lost ALBA 1mm + EGA 1.6mm + Qatalam 0.3mm + Mozal 0.6mm = 3.5m on a 74mt mkt = 4.7% impact to supply, and 7.7% of ex china supply

Balance this with Oil price demand destruction ~1mm, assume China overproduce and ship 500k – need to price demand destruction to balance ~2mt (inventory we see at ~1.5mt but majority of that is China link).

McGeoch says that in light of the shut downs, some traders have been eyeballing a significant surge in the aluminum price to $4500 (15% premium to LME for China is a clear starting point).

- The Goldman trader also writes that if the report is accurate, the market will first draw LME stocks, which is hard as not everyone can take Russian units, both regionally and financially.

- Second, market needs to solve for the China export tax.

- Third, it will be important to see China ramp supply, which means you have to convince them its a good use of power allocations.

Aluminum futures on the London Metal Exchange have surged since the strikes, with LME Aluminum trading up 50% from a year ago, and if production remains shuttered, it will likely move notably higher.

ASIAN AFFAIRS APRIL 1/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 31.43 PTS OR 0.80%

HANG SENG CLOSED UP 20.21 PTS OR 0.08%

Nikkei CLOSED DOWN 658.85 PTS OR 1.27%

//Australia’s all ordinaries CLOSED UP 0.43%

//Chinese yuan (ONSHORE) CLOSED UP 6.9063

/ OFFSHORE CLOSED UP AT 6.9124 Oil UP TO 102.70 ollars per barrel for WTI and BRENT UP TO 106.81 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.9063 (UP) OFFSHORE YUAN TRADING UP TO 6.9124 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.8740

OFFSHORE YUAN: UP TO 6.8767

1.HANG SANG UP 574.00 POINTS OR 2.25%

2. Nikkei closed UP 2709.28 PTS OR 5.31%

WEST TEXAS INTERMEDIATE OIL DOWN TO 97.47

BRENT; 99.84

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.35/// EURO RISES TO 1.15912 UP 18 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.304 DOWN 4 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.38… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.618 DOWN 10 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: 6.8740( UP AND OFFSHORE: UP AT 6.8767

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields LOWER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.9322 Italian 10 Yr bond yield DOWN to 3.781// SPAIN 10 YR BOND YIELD DOWN TO 3.405%

3i Greek 10 year bond yield DOWN TO 3.779%

3j Gold at $4711.00 //Silver at: 74.04 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 80 100 roubles/80.49

3m oil (WTI) into the 97 dollar handle for WTI and 99 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.25 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.305% DOWN 4 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.618 DOWN 10 PTS..: USA/SF this 0.7935 as the Swiss Franc . Euro vs SF: 0.9200

USA 10 YR BOND YIELD: 4.263 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.860 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.744 DOWN 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 44.47 DOWN 1 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 4.7950 DOWN 12 PTS

30 YR UK BOND YIELD: 5.426 DOWN 10 BASIS PTS

10 YR CANADA BOND YIELD: 3.474 DOWN 4 BASIS PTS

5 YR CANADA BOND YIELD: 3.092 DOWN 5 BASIS PTS.

1a New York Opening report

Futures, Bonds Surge On Optimism War May End, Oil Tumbles Below $100

26 – 08:30 AM

Futures and bonds jump and oil fell, sending Brent briefly below $100 a barrel, as the de-escalation/technical/macro led relief rally continues on hopes of the Middle East conflict reaching an end soon after Donald Trump said he expects the war in Iran to end in two to three weeks, and indicated that it was possible that Iran could still reach a deal with the US during that timeframe. Trump has a national address tonight at 9pm ET to discuss Iran, but the content is unclear, with the market is expressing the view that this will be details on a wind-down rather than an escalation. As of 8:15am ET, S&P Futures were 0.7% higher, after the cash index posted a near 3% advance on Tuesday, the best end to a quarter since September 2008. Nasdaq futures jumped 1.1% with all Mag 7 names higher premarket. European stocks jumped 2.6%, alongside a 4.9% surge in Asian shares. Final Mfg PMIs from the Europe were mixed (EU, Germany, Italy small beats/UK, France small missed) while Japan/Korea Manf PMIs were slightly better. Trump is set to address the nation tonight at 9pm EST and said he expects the war to end in two to three weeks/US would withdraw once Tehran can no longer obtain nuclear weapons. Otherwise, the US is sending a third aircraft carrier to the region, Iran said the US “isn’t serious about diplomacy”, the WSJ reported that the UAE wants to force the Strait of Hormuz open and is willing to join the fight, and attacks continued on both sides with Qatar saying Iran struck an oil tanker. Brent fell 5.4% before paring the move as the Strait of Hormuz remained largely closed and attacks continued across the Gulf. Traders trimmed bets on tighter monetary policy, sending two-year Treasury yields three basis points lower to 3.76%. Comparable UK gilt yields dropped 10 basis points to 4.30%. Looking at today’s US economic calendar, we get March ADP employment change (8:15am), February retail sales (8:30am), March final S&P Global US manufacturing PMI (9:45am), March ISM manufacturing and January business inventories (10am). Fed speaker slate includes Musalem (9:05am) and Barr (9:10am)

In premarket trading, Mag 7 stocks are all higher (Tesla +2.1%, Microsoft +1.5%, Amazon +0.9%, Nvidia +1.4%, Meta +0.6%, Alphabet +0.9%, Apple +0.5%)

- Li Auto ADRs (LI) rise 4% after the Chinese EV firm reported March vehicle deliveries that surpassed its own guidance and analyst estimates.

- MSC Industrial (MSM) falls 6% after the distributor of metalworking products reported adjusted earnings per share for the second quarter that missed the average analyst estimate.

- NCino (NCNO) jumps 24% after the cloud-banking software company’s subscription revenue forecast for 2027 beat the average analyst estimate.

- Nike (NKE) falls 10% after the retailer gave a surprisingly gloomy outlook for the year ahead, complicating Chief Executive Officer Elliott Hill’s efforts to turn around the business.

- RH (RH) plunges 17% after the home furnishing company forecast revenue for the first quarter that missed the average analyst estimate.

- Oric Pharmaceuticals (ORIC) slides 21% after the clinical-stage oncology company gave safety and efficacy data from an early-stage trial of its drug-candidate for prostate cancer that underwhelmed Wall Street.

- Target Hospitality (TH) rises 24% after the provider of modular housing announced secured a multi-year contract worth more than $550 million. The company will construct and provide hospitality services for a hyperscaler’s data center development in North Texas.

In other corporate news, Unilever said talks to sell most of its food business to McCormick are advanced and a final deal could be announced later on Tuesday. Boeing will team up with Rheinmetall to offer drones known as the Ghost Bat to Germany’s military.

Signs of an increased desire for de-escalation from Trump may reduce anxiety over his threats to attack Iranian energy infrastructure. On the other hand, Tehran would be left in control of the key oil shipment chokepoint. Meanwhile, Iran hit a fully laden Kuwaiti oil tanker off Dubai in a drone attack. Without a ceasefire or tangible progress in negotiations, the market will keep “fading the administration’s ‘everything is going well’ happy talk,” Vital Knowledge’s Adam Crisafulli wrote in a note. Carmignac Gestion’s Kevin Thozet observed that “Trump can’t simply turn an on/off switch on the crisis.” Other observers argue that rhetoric alone about a potential end to the conflict cannot create certainty for the market.

Equities are, nonetheless, primed to rip higher on positive news about the war following large-scale unwinding of risk by hedge funds and CTAs. The concern is that, post an initial bounce, worries about the economy and the path for interest rates will trigger further volatility episodes, setting up stocks for months of roller-coaster conditions.

In any case, traders said it would take time for oil flows to return to normal even if the war ends within Trump’s timeframe, especially given the damage to some energy facilities. Trump’s team has also suggested that reopening the Hormuz strait, which carries 20% of global crude, may not be necessary to end the hostilities.

“The correlation between Brent oil prices and global equity markets has been exceptionally strong since the conflict started,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin. “This goes to show that a return to previous equity market highs would need the Strait of Hormuz to reopen and oil prices to drop significantly. It is probably too early for an all-clear yet.”

Trump, who will give an address at 9 p.m. Eastern Time to provide an “important update” on Iran, said the Islamic Republic could still reach a deal with the US. He added, however, that an agreement with Tehran isn’t a prerequisite to conclude the war. “We are seeing a relief rally, and with more information we may see a reversal, so we just need to be careful here,” Remi Olu-Pitan, multi-asset growth and income head at Schroders, told Bloomberg TV. “There’s still a lot of volatility, the market is still fragile.”

Oil remains in focus for traders, policy makers and consumers. WTI futures are trading above $100 a barrel, while there’s been more commentary around the risks of spikes to $200. Crucially, retail unleaded pump prices climbed above $4 a gallon, the highest since August 2022. With higher gas prices adding near-term pressure on household budgets, Tuesday’s consumer confidence print will be closely watched. Oil, and the uncertainty around the magnitude and duration of supply disruption, was cited by strategists at Morgan Stanley as they downgraded global equities to equal-weight.

The Middle East conflict has caught high-flying chip stocks in its tentacles. Citigroup’s Jim McCormick describes a market wake-up call, noting “we’re looking at a world of sustained higher yields and sustained higher energy costs and that doesn’t help the AI sector.”

Traders at Goldman Sachs Group Inc. and JPMorgan Chase & Co. suggested Tuesday’s sharp rebound in US stocks was more about the unwinding of negative positioning by market participants than a shift in sentiment over the war. “Investors have been counting on a swift off-ramp to war essentially since it began, but I think from a market or global economy perspective it’s important to define what the true clearing event to revisit risk and take down recession odds really is,” wrote JPMorgan industrials sector specialist sales Paige Hanson.

Space is also making the headlines this week, with Virgin Galactic soaring in late trading after it resumed some sales of commercial space flights. NASA is making final preparations for the Artemis II missions, while what a history-making SpaceX IPO could mean for the space economy is discussed in the Big Take podcast.

European stocks are rallying, with the Stoxx 600 up 2% as markets look toward a potential resolution to the Iran conflict. Banks as well as travel and leisure shares are leading gains, while the energy sector is the biggest laggard. Stoxx 600 rises 2.2% to 595.73 with 65 members down, 532 up, and 3 little changed. Here are the biggest movers Wednesday:

- Athens Stock Exchange Index rises as much as 4.3% at Wednesday open, following index provider MSCI’s decision to upgrade the Greek market to developed status

- Thule rises as much as 5.7% after SEB Equities upgrades to hold, removing the only sell rating on the maker of roof and bike racks, to reflect “more reasonable expectations” now baked into the stock

- Sandoz shares rise as much as 5.1%, the most in five weeks, after Goldman Sachs initiated coverage on the stock with a buy recommendation

- Inficon gains as much as 8.1%, the most since Jan. 15, as JPMorgan starts coverage at overweight, saying the vacuum instrument maker should be a beneficiary of the multiyear upcycle in wafer fabrication equipment

- Arcadis shares rise as much as 6.6%, the most in six months, after Bank Degroof Petercam upgraded the engineering services firm on expectation that the new management team will be able to drive a recovery

- Jungheinrich shares rise as much as 9.8%, their steepest ascent in around a year, as Bernstein boosts its price target on the German machinery company, citing enticing long-term prospects

- Nordex falls as much as 3.8% after Bank of America downgraded the German wind turbine manufacturer to neutral from buy following a 56% year-to-date rally that the bank says has priced in most of the bull case

- Berkeley Group shares plunge as much as 19% to hit a nine-year low, after the housebuilder’s profit goal for the FY27 to FY30 period significantly undershot expectations

- SoftwareONE shares drop as much as 8.9%, hitting a seven-month low, after an investor offloaded shares at a discount to yesterday’s closing price. Shares have fallen below the offer price this morning

- Cirsa Enterprises drops as much as 5% after one of its investors offloaded shares at a discount to Tuesday’s closing price. The stock is holding above the offer price on Wednesday

UK Prime Minister Keir Starmer said his government will coordinate a diplomatic push for the strait’s reopening, affirming Britain’s desire not to be dragged into the military conflict. “I would expect further volatility in the days to come and the market to oscillate between losses and gains for a few more sessions until we get clarity on how the crisis unfolds,” said Alexandre Baradez, chief market analyst at IG Markets. “This is likely more a temporary respite than a final game changer.”

Earlier in the session, Asian stocks jumped the most in nearly a year, tracking Wall Street’s rally on optimism that the war in Iran may end in the near future. The MSCI Asia Pacific Index gained as much as 5.2%, the most since April 10, with shares in South Korea, Taiwan and Japan leading the gains. Technology giants Taiwan Semiconductor Manufacturing Co., Samsung Electronics Co. and SK Hynix Inc. provided the biggest boost to the gauge’s advance. Asian markets would stand to gain more than others if the US manages to defuse the war with Iran, as investors unwind an energy‑driven risk premium that has hit the region harder than most. The conflict has pushed oil prices sharply higher, driving equity sell‑offs and currency volatility across Asia’s oil‑importing economies. Still, the regional gauge remains down about 9% from a peak in February, with investors questioning how quickly oil can fall and how credible Trump’s assurances are. Market focus will now shift to an “important update” on Iran that Trump is scheduled to deliver at 9 p.m. Washington time.

In FX, the Bloomberg Dollar Spot Index fell as much as 0.4%, while Treasury yields dropped four basis across the curve. Swaps imply 11 basis points of Federal Reserve rate reductions by year-end, compared to 5bps on Tuesday. EUR/USD up as much as 0.5% to 1.1611, while GBP/USD up as much as 0.6% to 1.3301. USD/CHF drops 0.8% to 0.7928, EUR/CHF down 0.5% to 0.9190; leveraged desks seen unwinding franc shorts, a Europe-based trader says

In rates, fixed income markets have rallied but lost a bit of steam in recent trade. US yields are around 3bps lower across the curve as markets assign a 40% chance of a Fed rate cut by year-end versus a 64% chance of a hike last week. Treasury futures are off session highs in early US session, although yields remain 2bp-4bp lower across a steeper curve. US 10-year is about 3bp richer on the day near 4.29%, while 5s30s spread is steeper by ~1bp. Gilts outperform, with UK front-end yields richer by 8bp as oil broadly holds losses. Investors face the prospect that US President Trump, slated to speak at 9 p.m. in Washington, will soon declare an end to the war in Iran.

In commodities, despite the optimism in stocks, crude prices have faded declines in the European session. Brent is now back above $100 per barrel having earlier dropped below the key level. WTI crude oil contract has pared a 4.8% slump to about 2.5%, and was last trading just around $99. Precious metals are diverging, with spot gold up 1.4% and silver down 0.5%. Bitcoin has added 0.5%.

Looking at today’s US economic calendar, we get March ADP employment change (8:15am), February retail sales (8:30am), March final S&P Global US manufacturing PMI (9:45am), March ISM manufacturing and January business inventories (10am). Fed speaker slate includes Musalem (9:05am) and Barr (9:10am)

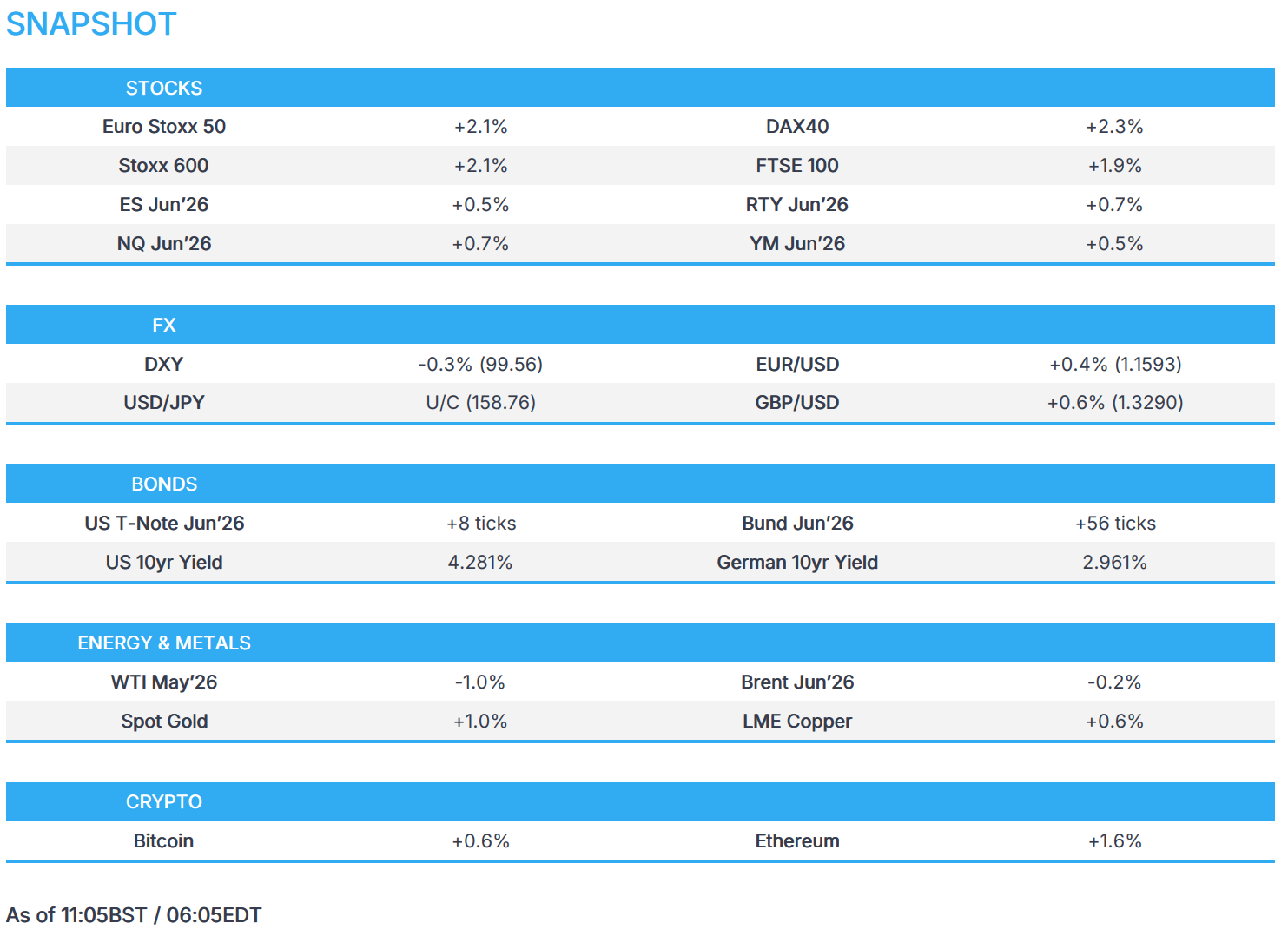

Market Snapshot

- S&P 500 mini +0.9%

- Nasdaq 100 mini +0.8%

- Russell 2000 mini +1.4%

- Stoxx Europe 600 +0.7%

- DAX +0.7%

- CAC 40 +0.5%

- 10-year Treasury yield -3 basis points at 4.32%

- VIX -1.7 points at 28.87

- Bloomberg Dollar Index little changed at 1221.56

- euro little changed at $1.147

- WTI crude -0.9% at $101.92/barrel

Top Overnight News

- Trump will deliver a speech on Wednesday at 9 p.m. Washington time to give an update about the war in Iran: BBG

- Oil fell, sending Brent briefly below $100 a barrel, after Donald Trump said he expects the war in Iran to end in two to three weeks. The US would withdraw once Tehran can no longer obtain nuclear weapons, he said. Attacks continued across the Middle East. Qatar said a cruise missile from Iran struck an oil tanker. BBG

- The United Arab Emirates is preparing to help the U.S. and other allies open the Strait of Hormuz by force, Arab officials said, a move that would make it the first Persian Gulf country to become a combatant, after being hit by Iranian attacks. WSJ

- Trump said he’s strongly considering pulling the US out of NATO after it didn’t join the war on Iran. He told the Telegraph that leaving the block was now “beyond reconsideration.” BBG

- California is confronting sky-high petrol prices and the threat of jet fuel shortages because of disruption caused by the Iran war, exposing US energy insecurity as the Strait of Hormuz remains closed. The most populous US state is vulnerable to the turmoil in world energy markets because it relies on imports of refined products such as petrol and jet fuel from Asia after introducing ambitious plans to phase out fossil fuels and significantly reduce refining capacity in favor of renewables. Californians pay the most for petrol in the country, with a gallon averaging $5.88 — the highest level since the pandemic — compared to $4.01 in the rest of the US, according to the American Automobile Association. FT

- Russia exported more liquefied natural gas in the first quarter of 2026 than it did a year earlier, with shipments to Europe increasing despite Moscow’s push to redirect supply away from the region. RTRS

- China’s factory activity slowed in March for export-oriented firms as their costs surged, according to RatingDog’s PMI. That contrasts with an official gauge that showed manufacturing improving despite the Iran war. BBG

- Chinese government bonds have sidestepped a global debt sell-off since the start of the Iran war, as the world’s second-biggest economy emerges as a haven from soaring energy prices and rising global inflation. Investors are betting that whereas major central banks in the US and Europe will be forced to keep interest rates at higher levels than previously expected to counter inflation triggered by rising oil and gas prices, China will be relatively insulated thanks to its energy mix and very low inflation before the conflict. FT

- Japan may face stagflation risks from the Iran war that would be challenging to deal with using monetary policy, new Bank of Japan board member Toichiro Asada said on Wednesday. RTRS

- Trump signs executive order related to mail-in voting, said working on proof of citizenship and that voter ID and citizenship proof are subjects for another time.

- OpenAI raised $122 billion at an $852 billion valuation in its largest funding round yet. BBG

- Since the start of the Iran war, market pricing for the fed funds rate has swung sharply, and it now implies a roughly 45% chance that the FOMC will hike in 2026. While some of this reflects changing demand for insurance against the tail risk of more hikes, the market-implied probability that the FOMC delivers 1-2 cuts—the modal case before the war—has declined from 35-40% to about 18%. Expectations for other central banks have moved even more, and market pricing now implies about 70bp of hikes from the ECB in 2026, compared to 8bp of cuts before the war

- Trump asks CPA for lists of insurers who were good to clients, and list who were bad in response to California fires.

A more detailed look at global markets courtesy of Newsquawk

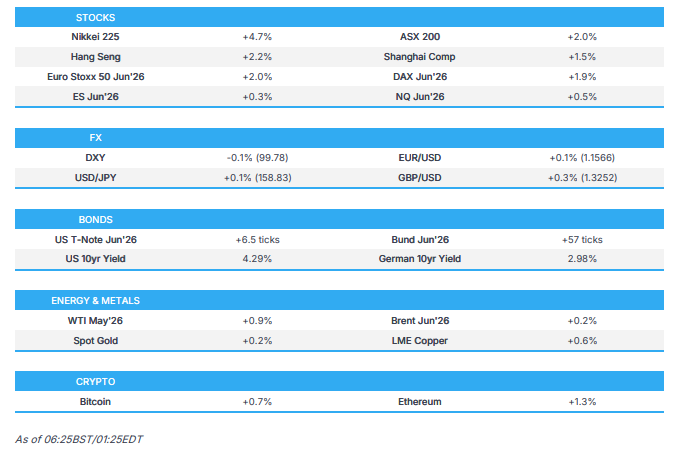

APAC stocks mostly rallied with global risk sentiment buoyed by hopes for an end to the Iran conflict following encouraging comments from the US and Iran, while President Trump also suggested that the war could end in 2 or 3 weeks, and he will deliver a nationwide address on Wednesday evening to give an important update regarding Iran. ASX 200 gained at the open and was led by outperformance in mining, materials, resources and tech, with nearly all sectors in the green aside from some defensives, while the index also shrugged off weak PMIs. Nikkei 225 surged back above the 53,000 level amid hopes of a nearing end to the conflict and after the latest BoJ Tankan survey mostly topped forecasts, with the headline large manufacturing index at its highest in more than five years. Hang Seng and Shanghai Comp conformed to the broad upbeat mood across the region with notable strength seen in mining, tech and biopharmaceuticals, while a miss on Chinese RatingDog Manufacturing PMI and the smallest PBoC injection in more than a decade failed to derail the momentum.

Top Asian News

- Chinese RatingDog Manufacturing PMI (Mar) 50.8 vs. Exp. 51.6 (Prev. 52.1, Low. 50.5, High. 53).

- Japanese Tankan Large Manufacturers Index (Q1) 17 vs. Exp. 16 (Prev. 15, Low. 8, High. 18).

- Japanese Tankan Large Non-Manufacturing Index (Q1) 36 vs. Exp. 33 (Prev. 34, Low. 28, High. 36)

- Japanese Tankan Small Manufacturers Index (Q1) 7 vs. Exp. 7 (Prev. 6, Low. -1, High. 9)

- Japanese Tankan Large Manufacturing Outlook (Q1) 14 vs. Exp. 13 (Prev. 15, Low. 5, High. 15)

- Japanese Tankan Large Non-Manufacturing Outlook (Q1) 29 vs. Exp. 28 (Prev. 28, Low. 24, High. 34)

- Japanese Tankan Large All Industry Capex (Q1) 3.3% vs. Exp. 13% (Prev. 12.6%)

European bourses (STOXX 600 +2.1%) continue to rebound, printing a third straight day of gains thus far. The positive was helped following reports that Iranian officials are leaning towards dialogue, while President Trump said that the war is coming to an end. European sectors are entirely in the green, ex. Energy. Banks and Travel and Leisure top the sector pile. Oil prices have been the main driver for airlines, with the drop in energy prices making jet fuel cheaper. Banks have been hit throughout the Iran war, so the prospects of it coming to an end have boosted the sector. To add, HSBC was added to Goldman Sachs’ European conviction list.

Top European News

- Germany’s VDMA said German Engineering Orders -8% in Dec-Feb Y/Y (Domestic Orders -6%, Foreign Orders -8%).

- German Economic Institutes confirm cutting 2026 and 2027 GDP growth forecasts.

- UK government said new measures to ease cost of living pressure to come into force on April 1st. Increasing national living wage to £12.71. Energy bills are to be cut by average £117 a year for millions across the UK and locked in until end of June.

FX

- DXY is on the backfoot this morning with markets pricing in a “de-escalation” trade, after US President Trump said to NBC News regarding the Iran war that “it is coming to an end”, with a White House official suggesting Trump is confident an agreement will be reached soon. Interestingly, from the Iranian side, President Pezeshkian noted that Iran seeks to end the war with guarantees against further attacks. DXY currently holds at the lower end of a 99.41-99.88 range. It is worth highlighting that the index saw some strength after the Iranian Deputy Speaker of Parliament said that the “Strait of Hormuz will never be opened, there has been no negotiation and there will be no negotiation”.

- G10s are entirely stronger against the USD, albeit to varying degrees. The CHF outperforms, benefiting from lower energy prices – the likes of GBP and EUR also benefit. For the GBP specifically, the UK government confirmed new measures to ease the cost of living pressure are to come into force today, including an increase in the national living wage to GBP 12.71 and with energy bills to be cut by an average GBP 117 a year for millions across the UK, which will be locked in until end of June.

- JPY also gains vs USD, albeit to a lesser degree vs peers. The seemingly easing Iran tensions has benefited the JPY, which builds on the strength seen in recent sessions, facilitated by jawboning and a hawkish-leaning BoJ SOO earlier this week. As for today, Japan’s Tankan survey was mostly stronger-than-expected, which supports the case for an April BoJ rate hike. USD/JPY currently trades within a narrow 158.27-159.01 range.

Central Banks

- BoJ new Board Member Asada does not comment on any specific stance. Rising oil prices put upward pressure on inflation while weighing on growth, creating a stagflationary trend.

- ECB’s Stournaras said if oil prices rise over USD 150/bbl Europe could face a recession.

- ECB’s Dolenc said ECB’s adverse scenario is more likely to be the next baseline and current baseline is more like the best-case scenario.

Fixed Income

- An overall positive start in the fixed income benchmarks, with energy prices falling and higher hopes of a potential end to the Iran conflict. President Trump stated that the war is coming to an end, while a White House official said that the President is confident that an agreement will be reached soon.