GOLD $4706.00. 3:30 PM)

EXCHANGE: COMEX

CONTRACT: APRIL 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,656.800000000 USD

INTENT DATE: 04/06/2026 DELIVERY DATE: 04/08/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 4

092 C DEUTSCHE BANK 48

118 C MACQUARIE FUTURES US 15

118 H MACQUARIE FUTURES US 34

323 H HSBC 49

332 H STANDARD CHARTERED B 97

357 C WEDBUSH SECURITIES 1

363 H WELLS FARGO SECURITI 5

365 C MAREX CAPITAL MARKET 3

435 H SCOTIA CAPITAL (USA) 1

555 C BNP PARIBAS SEC CORP 357

624 C BOFA SECURITIES 5

624 H BOFA SECURITIES 20

657 C MORGAN STANLEY 348 18

661 C JP MORGAN SECURITIES 70

686 C STONEX FINANCIAL INC 10 14

709 C BARCLAYS 154

730 C PTG DIVISION OF SGAS 538

732 C RBC CAP MARKETS 25 38

905 C ADM 6

TOTAL: 930 930

MONTH TO DATE: 16,263

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2026: 930 CONTRACTs NOTICES FOR 93,000 OZ or 2.8926TONNES

total notices so far: 16,263 contracts for 1,626,300 OR 50.584 tonnes)

SILVER NOTICES: 133 NOTICE(S) FILED FOR 690,000 OZ /

total number of notices filed so far this month : 1435 CONTRACTS (NOTICES) for 7.175 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A STRONG QUEUE JUMP OF 42 CONTRACTS OR 0.210 MILLION OZ/NEW STANDING REDUCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 0 CONTRACT QUEUE JUMP WHERE 0 ADDITIONAL OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS IS REMAINS AT 7.315 MILLION OZ

NOW OUR APRIL 2026 CONTRACT MONTH:

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 8.4100 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING REMAINS AT 7.370 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR STRONG 345 CONTRACT QUEUE JUMP FOR 345,000 OZ//NEW STANDING ADVANCES TO 53.710 TONNES

MARCH:: SMALL INITIAL STANDING FOR GOLD FOR MARCH AT 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 46 CONTRACT QUEUE JUMP OF 4400 OZ OR 0.2320 TONNESAND THEN WE ADD BY OUR THREE EXCHANGE FOR RISK: 22.3818///NEW STANDING ADVANCES TO 67.6648 TONNES OF GOLD./

APRIL: INITIAL STANDING FOR GOLD; 52.600 TONNES FOLLOWED BY TODAY’S 500 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON //NEW STANDING REDUCES TO 53.600 TONNES.

STANDING FOR THE LAST 4 MONTHS JANUARY TO APRIL:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES MINUS 500 OZ QUEUE JUMP (0.015 TONNES): NEW STANDING REDUCESS TO 53.600 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 16.668 TONNES

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONG

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL SIZED 117 CONTRACTS OI TO 114,379 AND FURTHER FROMTHE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 111,576 CONTRACTS MARCH 20.2026

EFP ISSUANCE 2 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 117 CONTRACTS AND ADD TO THE 2 E.FP. ISSUED

WE OBTAIN A SMALL SIZED LOSS OF 115 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $0.41

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 0.575 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.41

2.ASIAN AFFAIRS APRIL 7 /2025

SHANGHAI CLOSED UP 10.07 PTS OR 0.26%

HANG SENG CLOSED DOWN 177.50 PTS OR 0.70%

Nikkei CLOSED UP 112.82 PTS OR 0.21%

//Australia’s all ordinaries CLOSED UP 2.16%

//Chinese yuan (ONSHORE) CLOSED UP 6.8563

/ OFFSHORE CLOSED UP AT 6.8579 Oil UP TO 112.77 ollars per barrel for WTI and BRENT UP TO 109.30 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8563 (UP) OFFSHORE YUAN TRADING UP TO 6.8579 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR 929 CONTRACTS UP TO AN OI OF 355,510 CONTRACT OI , HAVING SURPASSSED OUR NEW RECORD LOW OI SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 354,581 SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 354,581 WITH GOLD AT AN EXTREMELY HIGH $4,676.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD STRONG T.A.S. LIQUIDATION DURING MONDAY’S TRADING. IT SEEMS THAT THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE SHORT SIDE WITH THE BANKERS TAKING THE LONG SIDE, AS WELL AS COVERING THEIR SHORTFALL, WITH OUR TAS SPREADER LIQUIDATIONS ACCOUNTING FOR THE LOSS IN OI!!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE MASSIVE AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MARCH CONTRACT MONTH!!

THE FAIR SIZED GAIN ON OUR TWO EXCHANGES OCCURRED WITH OUR SMALL GAIN IN PRICE IN GOLD. THE SPECS HAVE NOW GONE MASSIVELY ON THE SHORT SIDE WITH THE BANKERS BUYING UP ALL THEY COULD AND COVERING THEIR SHORTFALL IN GOLD. THE SHORT SPECS WILL BE MURDERLIZED AFTER THURSDAY’S MASSIVE RAID.

WE THUS HAD A FAIR GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 1081 CONTRACTS (OR 5.822 TONNES) WITH OUR SMALL GAIN IN PRICE, AS WE WERE INFORMED OF A SMALL 152 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE..

THEN WE WERE NOTIFIED TODAY OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0.0 TONNES OF GOLD.

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 0 EXCHANGE FOR RISK FOR FAR.

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO APRIL:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 0 EXCHANGE FOR RISK SO FAR.

DETAILS ON OUR NEW APRIL COMEX CONTRACT MONTH//

IN TOTAL WE HAD A FAIR SIZED GAIN ON OUR TWO EXCHANGES OF 1081 CONTRACTS WITH OUR GAIN IN PRICE ($5.30). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH APRIL/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A SMALL SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 535 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING THIS WEEK WITH MUCH FAILURE DURING LONDON LBMA/OTC OPTION EXPIRY WEEK!! (APRIL FIRST DAY NOTICE)

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD.

FOR MARCH WE HAVE 3 EXCHANGE FOR RISK ISSUANCES SO FAR FOR 7196 CONTRACTS OR 719,600 OZ/22.3818 TONNES.. AS DELIVERIES OF GOLD THESE PAST SEVERAL MONTHS HAVE BEEN HUGE!!

APRIL: 0 SO FAR HAVE BEEN ISSUED

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

AND NOW APRIL 2026: INITIAL STANDING FOR GOLD: 52.600 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ (0.0155 TONNES) EXCHANGE FOR PHYSICAL TRANSFER TO LONDON. THUS STANDING FOR GOLD AT THE COMEX REDUCES TO 53.6000 TONNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING APRIL,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $5.30

WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION // COMEX SESSION// DESPITE OUR SMALL GAIN IN PRICE , OUR LONG SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX STARTING TO BUILD ON ITS OI //(OTHER SPECULATORS WENT CONTINUALLY ON THE SHORT SIDE AND THEY WILL BE TORCHERED). OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD FOR FEBRUARY’S ACTIVE DELIVERY MONTH (157 TONNES) , MARCH’S STANDING OF 53+ TONNES+ TODAY’S HUGE APRIL’S DELIVERY TOTALS A VERY STRONG 53 + TONNES. HOWEVER HIGH FREQUENCY TRADERS LED OUR SHORT SPECULATORS BY THE NOSE ACCOUNTING FOR THE LOSS IN OI. THIS WAS SET UP FOR THURSDAY’S MASSIVE RAID STARTING RIGHT AFTER TRUMP’S SPEECH TO THE NATION.,(WEDNESDAY NIGHT)

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 7 MONTHS:

STANDING FOR GOLD OCT THROUGH TO APRIL:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR LATEST QUEUE JUMP OF 0.0298 TONNES TO WHICH THIS IS ADDED TO ALL OTHER QUEUE JUMPS OF 41.2082 / NEW QUEUE JUMP ADVANCES TO: 41.233 TONNES//STANDING ADVANCES TO: 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES/NEW STANDING ADVANCES TO 157.879 TONNES

MARCH: INITIAL STANDING: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TO WHICH WE THEN ADD OUR THREE EXCHANGE FOR RISK FOR 22.3818 TONNES// GOLD STANDING ADVANCES TO: 67.6648 TONNES/

APRIL: INITIAL STANDING: A VERY STRONG 52.600 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON (0.0155 TONNES). THUS STANDING FOR GOLD AT THE COMEX REDUCES TO 53.600 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $5.30

WE HAD A FAIR 791 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES : 1081 CONTRACTS OR 183,200 OZ OR 3.362 TONNES

INITIAL GOLD COMEX

APRIL DELIVERY MONTH

APRIL 7 2026

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES i) Out of Brinks 147,330.054 oz total withdrawal 147,330.054 oz or 4.525 tonnes |

| Deposit to the Dealer Inventory in oz | 0 ENTRY |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRY I) into Manfra: 11,119.699 oz total deposit 11,119.699 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 930 CONTRACTS OR 93,000 OZ 2.8926 TONNES OF GOLD |

| No of oz to be served (notices) | 970 Contracts 97000 OZ 3.017 TONNES |

| Total monthly oz gold served (contracts) so far this month | 16,263 notices 1,626,300 oz 50.584 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

DEPOSITS/CUSTOMER

0 ENTRY

1 entry

customer withdrawals:

comex is draining of gold/.

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs

ADJUSTMENTS dealer to customer

adjustments: / / 1

ADJUSTMENTS 1//DEALER TO CUSTOMER

a) Loomis

total loss of gold from dealer: 8198.805 oz (0.25 TONNES)

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF APRIL OI STANDS AT 1900 CONTRACTS HAVING A LOSS OF 831 CONTRACTS.

WE HAD 826 CONTRACTS SERVED UPON MONDAY SO WE LOST 5 CONTRACTS THROUGH AN EXCHANGE FOR PHYSICAL TRANSFER TO LONDON (0.0155 TONNES) THUS STANDING FOR GOLD AT THE COMEX DECREASES TO 53.600 TONNES OF GOLD.

MAY LOST 546 CONTRACTS TO AN OI OF 4567

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI ROSE BY A HUGE 2121 CONTRACTS DOWN TO AN OI OF 265,946

We had 930 contracts filed for today representing 93,000oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 930 contract(s) of which 70 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for APRIL. /2026. contract month, we take the total number of notices filed so far for the month (16,263) to which we add the difference between the open interest for the front month of APRIL (XXX CONTRACTS) minus the number of notices served upon today 930 x 100 oz per contract) equals 1,723,300. OZ OR (53.6000Tonnes of gold)

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (16,263 x 100 oz +we add the difference for front month of APRIL (1900 OI} minus the number of notices served upon today (930 )x 100 oz) which equals 1,723,300 OZ OR 53.600 TONNES//

new total of gold standing in APRIL is 53.600 TONNES//

TOTAL COMEX GOLD STANDING FOR APRIL 53.600 TONNES TONNES WHICH IS NOW HUGE FOR THIS NORMALLY VERY ACTIVE ACTIVE DELIVERY MONTH OF APRIL.

confirmed volume MODAY confirmed 97,092 poor

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,878,352.072 oz 58.42 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,878,352.072 tonnes oz 58.42 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 30,825,897.376 oz

TOTAL REGISTERED GOLD 16,248,709.281 or 505.658 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 14,577,168.095 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 14,370,357 oz ((REG GOLD- PLEDGED GOLD)=

446.978 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

APRIL DELIVERY MONTH

APRIL7

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries i) Out of CNT 1200,050.098 oz ii) Out of Loomis: 632,268.390 oz total withdrawal 1,8323,183.30 oz |

| Deposits to the Dealer Inventory | 0 entries xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx |

| Deposits to the Customer Inventory | DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 ENTRIES i) Into Manfra: 881,514.939 oz total deposit 881,514.939 oz |

| No of oz served today (contracts) | 138 CONTRACT(S) ( 690,000 OZ |

| No of oz to be served (notices) | 177 Contracts (0.885 MILLION oz) |

| Total monthly oz silver served (contracts) | 1435 contracts 7.175 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 entries

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

DEPOSITS one entry

1 ENTRIES

i) Into Manfra: 881,514.939 oz

total deposit 881,514.939 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

2 entries

i) Out of CNT 1200,050.098 oz

ii) Out of Loomis: 632,268.390 oz

total withdrawal 1,8323,183.30 oz

the comex is being drained of silver

the comex is being drained of silver

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 77. MILLION OZ//.TOTAL REG + ELIGIBLE. 326.239 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2026 OI: 177 OPEN INTEREST CONTRACTS FOR A LOSS OF 42 CONTRACTS. WE HAD 42 CONTRACTS SERVED ON MONDAY, SO WE GAINED 0 CONTRACTS OR 0 OZ UNDERWENT A QUEUE JUMP. STANDING THUS REMAINS AT 7.370 MILLION OZ WHICH IS PRETTY GOOD FOR THIS NORMALLY SMALL NON ACTIVE DELIVERY MONTH OF APRIL

MAY SAW A LOSS OF 663 CONTRACTS DOWN TO 70,391 CONTRACTS.

JUNE SAW A GAIN OF 38 CONTRACTS UP TO 449 OI CONTRACTS

ZZ.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 138 or 690,000 oz

CONFIRMED volume; ON MONDAY; 24,611 poor

AND NOW APRIL. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1438 X5,000 oz = 7.175 MILLION oz

to which we add the difference between the open interest for the front month of APRIL (177) AND the number of notices served upon today (138)x (5000 oz)

Thus the standings for silver for the APRIL 2026 contract month: (1435 )Notices served so far) x 5000 oz + OI for the front month of APRIL (177) minus number of notices served upon today (138 )x 5000 oz equals silver standing for the APRIL..contract month equating to 7.370 MILLION OZ.

NEW STANDING: 7.370 MILLION OZ WHICH IS STRONG FOR A GENERALLY LOUSY DELIVERY MONTH OF APRIL.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 77.129 million oz of registered silver

JPMorgan as a percentage of total silver: 145.541/326.239million: 44.44%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054/419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

APRIL 1/2026/WITH GOLD UP $134.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 1.143 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1047.276 TONNES

MAR 31/2026/WITH GOLD UP $119.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE WITHDRAWAL OF 3.429 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1046.133 TONNES

MAR 30/2026/WITH GOLD UP $33.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.143 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1049.562

MAR 27/2026/WITH GOLD UP $103.55 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.285 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.705

MAR 26/2026/WITH GOLD DOWN $213.05 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.580 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1052.42

MAR 25/2026/WITH GOLD UP $155.30 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.300 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1053.000

MAR 24/2026/WITH GOLD DOWN $7.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.286 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1052.705

MAR 23/2026/WITH GOLD DOWN $165.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 5.149 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1056.991

MAR 20/2026/WITH GOLD DOWN $39,55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4.855 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1062.135

MAR 19/2026/WITH GOLD DOWN $XXX TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 2.57 TONNES OF GOLD OUT OF THE GLD/INVENTORY RESTS AT 1066.99

MAR 18/2026/WITH GOLD DOWN $111.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1069.564 TONNES

MAR 17/2026/WITH GOLD UP $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 0.857 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.708 TONNES

MAR 16/2026/WITH GOLD DOWN $60.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 4/327 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1071/.565 TONNES

MAR 13/2026/WITH GOLD DOWN $61.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE WITHDRAWAL OF 1.428 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1075.852 TONNES

MAR 12/2026/WITH GOLD DOWN $49.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.715 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1077.28 TONNES

MAR 11/2026/WITH GOLD DOWN $70.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 2.858 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1073.565 TONNES

MAR 10/2026/WITH GOLD UP $137.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.614 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1070.707 TONNES

MAR 9/2026/WITH GOLD DOWN $53.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 2.573 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1073.321 TONNES

MAR 6/2026/WITH GOLD UP $77.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:ANOTHER MONSTER WITHDRAWAL OF 5.144 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1075.894 TONNES

MAR 5/2026/WITH GOLD DOWN $49.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 18.032 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1081.038 TONNES

MAR 4/2026/WITH GOLD UP $9.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.545 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1099.07 TONNES

MAR 3/2026/WITH GOLD DOWN $188.75 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.35 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101.36 TONNES

MAR 2/2026/WITH GOLD UP $71.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A HUGE DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1101,13 TONNES

FEB 27/2026/WITH GOLD UP $52.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL DEPOSIT OF 0.28 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.90 TONNES

FEB 26/2026/WITH GOLD DOWN $30.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE DEPOSIT OF 11.45 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1097.62 TONNES

FEB 25/2026/WITH GOLD UP $48.40 TODAY/SMALL CHANGES IN GOLD AT THE GLD:A SMALL WITHDRAWAL OF 0.300 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1086.17 TONNES

FEB 24/2026/WITH GOLD DOWN $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A MASSIVE PAPER DEPOSIT OF 7.72 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1086.47 TONNES

GLD INVENTORY: 1054.419 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

APRIL 1 WITH SILVER UP $1.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND WITHDRAWAL OF 0.453 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 491.079 MILLION OZ

MAR 31 WITH SILVER UP $4.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE AND FRAUDULENT WITHDRAWAL OF 3.893 MILLION OZ FROM THE SLV // :INVENTORY RESTS AT 491.532 MILLION OZ

MAR 30 WITH SILVER UP $0.74: NO CHANGES IN SILVER INVENTORY AT THE SLV: // :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 27 WITH SILVER UP $1.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV// :INVENTORY RESTS AT 495.425 MILLION OZ

MAR 26 WITH SILVER DOWN $4.75: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 25 WITH SILVER UP $3.25: NO CHANGES IN SILVER INVENTORY AT THE SLV// :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 24 WITH SILVER DOWN $0.15: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MASSIVE AND FRAUDULENT DEPOSIT OF 10.505 MILLION OZ INTO THE SLV :INVENTORY RESTS AT 498.776 MILLION OZ

MAR 23 WITH SILVER UP $0.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// NO CHANGE IN INVENTORY/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 20 WITH SILVER DOWN $1.92: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.490 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 488.271 MILLION OZ

MAR 19 WITH SILVER DOWN $6.22: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.9444 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 490.761 MILLION OZ

MAR 18 WITH SILVER DOWN $2.36: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 1.087 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 494.792 MILLION OZ.

MAR 17 WITH SILVER DOWN $0.89: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.351 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 493.705 MILLION OZ.

MAR 16 WITH SILVER DOWN $0.57: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2.536 MILLION OZ FROM THE SLV/.. ./ :INVENTORY RESTS AT 497.056 MILLION OZ.

MAR 13 WITH SILVER DOWN $3.83: NO CHANGES IN SILVER INVENTORY AT THE SLV// . ./ :INVENTORY RESTS AT 499.592

MAR 12 WITH SILVER DOWN $0.51 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 3.713 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 499.592 MILLION OZ

MAR 11 WITH SILVER DOWN $3.96 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// ANOTHER MONSTER WITHDRAWAL OF 1.812 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 503.305 MILLION OZ

MAR 10 WITH SILVER UP $5. HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.63 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 505.117 MILLION OZ

MAR 9 WITH SILVER DOWN $0.30 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 1.54 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 506.747 MILLION OZ

MAR 6 WITH SILVER UP $2.02 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A MONSTER WITHDRAWAL OF 5.526 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 508,287 MILLION OZ

MAR 5 WITH SILVER DOWN $0.98 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.097 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 512.726 MILLION OZ

MAR 4 WITH SILVER DOWN $0.21 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.545 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 513.813 MILLION OZ

MAR 3 WITH SILVER DOWN $5.27 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 2/899 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 511.268 MILLION OZ

MAR 2 WITH SILVER DOWN $3.87 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.352 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 514.167 MILLION OZ

FEB 27 WITH SILVER UP $5.54 SMALL CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 0.544 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 517.519 MILLION OZ

FEB 26 WITH SILVER DOWN $4.05 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 0.906 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 516.975 MILLION OZ

FEB 25 WITH SILVER UP $3.43 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 8.923 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 517.881 MILLION OZ

FEB 24 WITH SILVER UP $0.55 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT PAPER DEPOSIT OF 10.056 MILLION OZ INTO THE SLV. ./ :INVENTORY RESTS AT 508.958 MILLION OZ

FEB 23 WITH SILVER UP $4.89 HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A FRAUDULENT WITHDRAWAL OF 0.951 MILLION OZ OUT OF THE SLV. ./ :INVENTORY RESTS AT 498.902 MILLION OZ

CLOSING INVENTORY 490.764 MILLION OZ OF SILVER..

1.PETER SCHIFF

2. MATHEW PIEPENBERG/EGON VON GREYERZ

MATHEW PIEPENBURG…

XXX

JOHN RUBINO

Recession Watch: Everything All At Once

| John RubinoApr 7 |

Tech layoffs have become front-page news…

And the picture for this year’s class of graduating coders is apocalyptic. From Tech Layoff Tracker:

Computer science professor at a major state university just finished the worst faculty meeting in 32 years of academia

Department head dropped the placement statistics like a bomb at 2:47 PM on a Wednesday

2023: 89% placement rate within 6 months of graduation

2024: 67% placement rate

2025: 34% placement rate

2026 projections: 12% placement rate

312 CS majors graduating this spring. Industry contacts saying maybe 40 will find work.

The dean wants to know why enrollment is still climbing while job prospects crater

Faculty sitting there like deer in headlights because what the fuck do you tell 19-year-olds taking out $40k per year in loans

Half the curriculum is already obsolete. Teaching data structures while companies replace entire engineering teams with Claude and Cursor.

One professor suggested pivoting to “AI collaboration skills” and got laughed out of the room

Another said we should warn students. Department head said that would “damage program reputation and university revenue”

So they keep taking tuition money from kids who will graduate into a wasteland

Career services still posts those bullshit salary averages from 2022 when new grads were getting $140k offers

Now the same companies are hiring 2 senior engineers with AI tools instead of 12 junior developers

Every CS professor knows their students are walking into a meat grinder

But the university needs those enrollment numbers to hit budget targetsThey’re literally selling degrees that lead to DoorDash drivingTech Layoffs,

Private credit is looking like this decade’s subprime mortgage bubble, except a lot bigger and more widespread:

Oil has gone parabolic, with multiple countries running out of crude, gasoline, and/or diesel:

And — no surprise — the bond markets are rebelling, with US 10-year Treasuries back to levels that imply 7% mortgages and 10% car loans:

It’s all coming to a head as this is written:

Trump warns Iran’s ‘whole civilization will die tonight’ unless deal struck

President Donald Trump on Tuesday sharply ramped up his threats against Iran, warning “a whole civilization will die tonight” unless the country’s leadership strikes a deal that involves reopening the Strait of Hormuz.

The threat came after U.S. forces overnight struck military targets on Kharg Island, Iran’s main oil export terminal, a White House official confirmed to CNBC.

“A whole civilization will die tonight, never to be brought back again. I don’t want that to happen, but it probably will,” Trump wrote Tuesday morning on Truth Social.

“However, now that we have Complete and Total Regime Change, where different, smarter, and less radicalized minds prevail, maybe something revolutionarily wonderful can happen, WHO KNOWS?” he wrote.

“We will find out tonight, one of the most important moments in the long and complex history of the World.”

Lots of Reasons Not to Spend Money

Pretty much everyone who’s paying attention will find a reason in the above to limit their discretionary spending. The result? A world where government deficits are soaring and private sector growth is minimal.

You’re currently a free subscriber to John Rubino’s Substack. For the full experience, upgrade your subscription.

JESSE COLUMBO

ALASDAIR MACLEOD

3.CHRIS POWELL AND HIS GATA DISPATCHES:

4. ANDREW MAGUIRE AND LIVE FROM THE VAULT PODCASTS NO 266/265

ANDREW SCHECTMAN//THIS WEEK

end.

5. COMMODITY REPORT//HELIUM..

Wyoming’s Helium Empire Ascends As Qatar Gas Goes Flat

Monday, Apr 06, 2026 – 04:40 PM

Readers have already been well briefed, see here and here, that roughly one-third of global helium supply has been disrupted, setting the perfect storm of chaos to spread across high-tech industries, particularly semiconductors. The shock is being driven by shipping restrictions through the Gulf and the shutdown of output from top producer Qatar, where damage to the Ras Laffan complex could keep supplies constrained for years.

As the U.S.-Iran conflict enters its second month, one of the clearest second-order effects of the widening Gulf energy shock is the rewiring of global energy flows.

Buyers are already being forced to reassess the risks of concentrated energy exposure to the Gulf region, whether in crude and refined products or in LNG and helium, as war damage to major LNG export facilities in Qatar and Hormuz-related shipping constraints suggest energy flows could remain impaired for a prolonged period. Some of the countries most exposed to Gulf disruptions are in Asia, Africa, and Europe, as well as California in the U.S.

The good news for global buyers seeking more reliable alternatives to Gulf energy products is a theme we pointed out last month: American LNG exporters in the Gulf of America stand to be major beneficiaries of the disruption.

Adding to that theme, UBS analysts led by Manav Gupta said ExxonMobil stands out as a major beneficiary of the helium shock.

“Qatar was expected to increase its share of global capacity to 34% over the next five years; however, damage to the Ras Laffan facility could delay this expansion,” Gupta noted. But as it has turned out, the head-to-head race with the U.S. in LNG export capacity has paused for now, as the U.S. pulls ahead.

2025 Helium production by country

Gupta continued, noting that XOM is set to dominate the global helium market through its facilities in Wyoming:

XOM’s LaBarge facility in Wyoming, provides 20% of the world’s supply, which has not been impacted by recent events in the Middle East. With an estimated eight decades worth of helium left to produce there, LaBarge is poised to play a significant role through the end of this century.

This facility, is capable of producing ~1.4 billion cubic feet per year of Grade A helium. With over 30% of global capacity disrupted, this location will play a key role in meeting global needs for Helium which is a critical element for many advanced technologies, like MRIs for healthcare, rockets for space exploration, and microchips for advanced computing.

Extracting helium was not part of LaBarge’s original design when the facility began producing natural gas in the mid-1980s. After large quantities of helium were discovered underground, it soon became central to the facility’s operation.

The two wars now stretching across Eurasia – the Russia-Ukraine conflict and, now, the U.S.-Iran conflict – are accelerating a rewiring of global energy flows toward suppliers seen as more stable and secure, above all the U.S.

Professional subscribers can read the full note on why UBS says XOM is a “net beneficiary of the current helium market tightness” at our new Marketdesk.ai portal.

END

PETROCHEMICALS//ASIA

Petrochemical Supply Shock Begins Idling Asian Factories

Tuesday, Apr 07, 2026 – 02:20 PM

For weeks, we mapped out for readers how the Gulf energy shock dominoes would fall, spreading outward from the Middle East and striking Asia first through tightened energy-product flows that risk destabilizing the global economy. That transmission of tightening energy flows is now becoming alarmingly visible on factory floors across Asia.

Goldman analysts, led by Georgina Fraser, warned clients on Monday that the petrochemical shock is worsening across Asia, with textile and packaging plants emerging as the first major downstream casualties.

“The supply shock is transmitting faster and at a greater magnitude than we had anticipated,” Fraser emphasized in the note.

She said the supply shock is moving beyond higher energy prices into production cuts, margin compression, and early demand destruction, adding that “signals are materializing fastest, with textiles and packaging among the first downstream sectors affected.”

Impact chain on the Chemicals sector from the Middle East conflict

Last week, supply chain disruptions in critical plastic feedstocks began to emerge, with several producers of monoethylene glycol (MEG) and purified terephthalic acid (PTA) declaring force majeure, while tanker flows through the Strait of Hormuz remained heavily disrupted. These feedstocks are essential in the production of plastics, the very material that is core to the modern economy.

Fraser noted that China’s PTA supply chain accounts for roughly three-quarters of global PTA capacity. She said spot PTA prices have jumped by more than 30% since the U.S.-Iran conflict began.

At the same time, about 15% of China’s PTA capacity and 11% of global capacity have been taken offline due to shutdowns and curtailments.

For context, MEG and PTA are the two primary feedstocks used to produce polyethylene terephthalate (PET) and polyester fibers. These petrochemicals are essential to the production of everyday consumer goods that make life in the developed world convenient, including plastic bottles, food packaging, clothing, home furnishings, and a wide range of consumer and industrial goods.

The analyst then shifted focus to India, where she said the first signs of a petrochemical supply shock are already emerging: In Surat, the country’s main synthetic textile hub, producers have reduced operations to a single 12-hour shift, halving output as soaring plastics costs collide with weak demand.

She noted that for apparel and textiles, where petrochemical-linked inputs account for 50% to 65% of the cost of goods sold, the latest moves in raw material spot prices imply a 17% COGS shock, enough to idle less efficient plants.

Packaging is also at risk. While demand is lower for discretionary goods than for clothing, elevated price pressures in PTA and related petrochemicals threaten to spill over into food, beverage, and consumer goods packaging, increasing the odds of inflationary pass-through.

Circling back to JPMorgan’s commodity expert on how the energy shock dominoes fall: Asia first (happening now), then Africa and Europe, before settling on the US – primarily California.

“Even an imminent end to the conflict would not fully unwind the supply chain disruption already in motion,” the analyst warned.

Professional subscribers can read the full “Petrochemical supply shock hits textiles and packaging faster and harder than anticipated” note here at our new Marketdesk.ai portal. Fraser

ASIAN AFFAIRS APRIL 7/2026

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 10.07 PTS OR 0.26%

HANG SENG CLOSED DOWN 177.50 PTS OR 0.70%

Nikkei CLOSED UP 112.82 PTS OR 0.21%

//Australia’s all ordinaries CLOSED UP 2.16%

//Chinese yuan (ONSHORE) CLOSED UP 6.8563

/ OFFSHORE CLOSED UP AT 6.8579 Oil UP TO 112.77 ollars per barrel for WTI and BRENT UP TO 109.30 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING 6.8563 (UP) OFFSHORE YUAN TRADING UP TO 6.8579 ONSHORE YUAN TRADING ABOVE OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.8563

OFFSHORE YUAN: UP TO 6.8579

1.HANG SANG CLOSED DOWN 177.50 PTS OR 0.70%

2. Nikkei closed UP 112.82 PTS OR 0.21%

WEST TEXAS INTERMEDIATE OIL UP TO 112.77

BRENT; 109.30

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 99.61/// EURO RISES TO 1.1574 UP 33 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +2.390 DOWN 3 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.48… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.7570 UP 8 FULL BASIS PTS

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: 6.8563( UP AND OFFSHORE: UP AT 6.8579

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and BRENT UP this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +3.0054 Italian 10 Yr bond yield UP to 3.865// SPAIN 10 YR BOND YIELD UP TO 3.484%

3i Greek 10 year bond yield UP TO 3.818%

3j Gold at $4688.20 //Silver at: 72.93 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 36 100 roubles/78.66

3m oil (WTI) into the 112 dollar handle for WTI and 108 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.56 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.390% DOWN 3 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.737 DOWN 2 PTS..: USA/SF this 0.7979 as the Swiss Franc . Euro vs SF: 0.9277

USA 10 YR BOND YIELD: 4.327 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.892 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.848 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 44.61 UP 2 BASIS PTS/LIRA GETTING KILLED//IDIOTS FOR SELLING GOLD

10 YR UK BOND YIELD: 4.8460 UP 0 PTS

30 YR UK BOND YIELD: 5.4530 DOWN 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.469 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 3.097 UP 1 BASIS PTS.

1a New York Opening report

Futures Slide, Oil Jumps After US Attacks Kharg Island Ahead Of Trump’s 8pm Iran Deadline

Tuesday, Apr 07, 2026 – 08:30 AM

US futures reversed earlier gains and oil advanced following reports that Iran’s Kharg island was targeted earlier on Tuesday, while the market was largely paralyzed ahead of Trump’s 8pm ET deadline for Iran to agree to a ceasefire or face escalation. As of 8:00am ET, S&P futures are down 0.4%, and Nasdaq futures slide 0.6%. In premarket trading, all Mag7 names are lower even as AVGO (+3% pre-mkt) is bid after a TPU supply pact with GOOGL (+55bps) while ASML (-80bps) is weaker following a proposed US law that would further curb semiconductor exports to China (targeting ASML’s deep ultraviolet lithography machine ). Managed care is well bid after the final Medicare Advantage rate of +2.48% (vs ~1% bogey) was released last night (HUM +9%, CVS +7%, UNH +6%, ALHC +11%). Bond yields rise 1bp, 10Y TSY yield at 4.34%, the USD is also higher while commodities are mixed with oil reversing earlier losses and rising over 2%. Today’s macro data focus is weekly ADP, Durable / Cap Goods, and NY Fed 1-year Inflation Expectations. Ultimately, expect weaker volumes today with some market swings on unconfirmed ceasefire / deal chatter.

In premarket trading, Mag 7 stocks are all lower (Alphabet -0.06%, Amazon -0.4%, Meta -0.6%, Microsoft -0.4%, Tesla -1.3%, Nvidia -1.2%, Apple -1%)

- Managed care companies including Humana gain after the Centers for Medicare & Medicaid Services finalized a 2.48% rate hike for health insurers in 2027. Investors see the pay boost as a meaningful improvement over the initial rates the agency proposed in January. Humana (HUM) rises 9% and CVS Health gains 6%.

- Broadcom (AVGO) rises 3% after the chipmaker announced a long-term agreement with Google to develop and supply Tensor Processing Units. The companies also confirmed plans to work with Anthropic to power the AI startup’s burgeoning operations.

- Estée Lauder (EL) slips 1% after Spanish newspaper Expansion reported that the the company and Puig owning families are set to hold talks this week in New York over their potential merger.

- Organogenesis Holdings Inc. (ORGO) rises 19% after the company said a randomized controlled trial of 170 patients in a diabetic foot ulcer trial achieved its primary endpoint.

- Wingstop (WING) rises 1.9% as Citi upgrades the fried chicken restaurant operator to buy, saying the valuation offers an attractive entry point.

- Pershing Square proposed a combination with Universal Music Group that would move the listing into a US-based acquisition vehicle. It’s a deal that Bill Ackman’s fund said values the world’s biggest music label at a 78% premium to its last closing price.

In other news, Samsung reported preliminary operating profit that soared 755% to a record, with memory’s contribution estimated to be close to 90% of total operating profit. Rivals OpenAI, Anthropic, and Alphabet’s Google have begun working together to try to clamp down on Chinese competitors extracting results from cutting-edge US AI models. And Anthropic said its revenue run rate has now topped $30 billion, with more than 1,000 businesses spending over $1 million annually, a rate that has doubled since February. BlackRock is setting its sights on a corner of the $13.7 trillion US ETF industry long controlled by Invesco — tracking the Nasdaq 100 Index. Some Tiger Cub funds incurred losses in March. Maverick Capital’s Long Enhanced Fund and its main hedge fund tumbled 8.1% and 5%, respectively, while Viking Global Investors’ flagship fund lost 4.1%, according to people familiar with the matter.

Trump has threatened “all Hell” will rain down on Iran if it doesn’t agree to a ceasefire that reopens the Strait of Hormuz by 8 p.m. Eastern time. The Pentagon canceled the morning press briefing due to be led by Pete Hegseth, giving no reason. WSJ reported last night that hope is fading for a final deal by the deadline and RTRS reported this morning that a Senior Iranian Source said Tehran has rejected any temporary ceasefire with the U.S. and the IRGC warned neighboring countries “restraint is over” and threatened to disrupt regional oil and gas supplies for years to come. Strikes continued overnight.

“It seems clear that it is extraordinarily difficult to invest on expectations for binary outcomes,” notes Jeffrey Palma at Cohen & Steers. On the other hand, David Kruk at La Financiere de l’Echiquier, set out the dilemma confronting traders, observing that the “market is now set up in such a way that the real pain trade is upwards.”

Investors are watching for any sign of a breakthrough amid a flurry of diplomacy before the 8 p.m. Eastern Time deadline. Trump insists any deal must ensure uninterrupted transit through the Strait of Hormuz — a key artery for Middle East oil flows. He’s threatened to destroy Iran’s bridges and power plants if no accord is reached. “The market remains volatile,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin. “It continues to swing between de-escalation hopes and Trump following through on his threats.”

Oil remains in focus, with WTI crude rising to the highest since June 2022. Meanwhile, Bloomberg Intelligence analysts expressed caution over the wide gap between the Brent spot price, which reflects expectations of a resolution, and Dated Brent, which represents actual cargoes assigned specific loading dates. At above $140, the latter signals acute spot scarcity.

Trump’s deadline marks the latest pivotal moment in the war, which has killed thousands of people and triggered the largest-ever disruption to the global oil market. Israel told Iranians to refrain from using their country’s railway network until 9 p.m. local time, the first warning about such infrastructure that usually precedes an attack. Iran launched seven ballistic missiles and several more drones at Saudi Arabia overnight into Tuesday, while the Israel Defense Forces reported two missile volleys from Iran since midnight.

Meanwhile, the technology sector is looking increasingly attractive for investors as valuations fall below those of the wider stock market, according to Goldman strategists. Any lasting shock to the global economy from the war in Iran is also likely to benefit the sector as tech cash flows are less sensitive to economic growth, the strategists said.

The recent economic numbers aren’t boosting the case for the Federal Reserve to resume cutting rates anytime soon. March CPI on Friday is predicted to show the largest month-over-month increase in headline inflation since June 2022, largely driven by a spike in gasoline prices tied to the Iran conflict.

Europe’s Stoxx 600 is up by 0.6%, with the media subindex leading the way on a jump for Universal Music on a €56 billion takeover proposal. UMG is the biggest gainer after Pershing Square offered to buy the entertainment company, while tech underperforms, weighed down by ASML as US lawmakers propose tighter curbs on chip equipment exports to China. Here are the biggest movers:

- Universal Music Group shares rise as much as 24% in Amsterdam, but trade well below the value of an offer from Pershing Square Capital Management amid doubt over whether the deal will happen

- JCDecaux rises as much as 5.8% as TD Cowen upgrades the outdoor advertising company to buy from hold, seeing a clear inflection point as China returns to growth

- Volati gains as much as 7.2%, the most since November, as Nordea reiterates its buy rating and raises its price target on the Swedish industrial group, saying the company is well-positioned to benefit from a cyclical rebound

- ASML shares fall as much as 4.7% on Tuesday after US lawmakers unveiled legislation aimed at tightening restrictions on chip tool exports to China. The goal is to subject Dutch and Japanese firms to the same curbs that American companies face

- Leonardo shares fall as much as 5.5% on the possibility of a management change at the Italian defense group; Bloomberg News reported that CEO Roberto Cingolani could be replaced as soon as this week

- AddTech falls as much as 5.9% after DNB Carnegie downgraded the stock to hold from buy, saying the Swedish industrial equipment maker could face weakening earnings growth momentum in 4Q

- Ninety One tumbles as much as 14% as BofA Global Research downgrades its rating on the investment management firm to neutral from buy and cuts its target price to 260p from 280p because of lower expected market returns

- Colruyt drops as much as 4.3%, biggest decliner in Belgium’s BEL Mid Index, after UBS downgraded the stock to neutral from buy, saying it looks “fairly valued for modest growth”

Asian stocks advanced for a third-straight session even as the approach of President Donald Trump’s deadline for a peace deal with Iran kept traders on edge. The MSCI Asia Pacific Index rose 1%, with technology shares including TSMC and SK Hynix among the biggest boosts. Stocks climbed in Taiwan and Australia. Hong Kong’s market remained shut for holidays. Stocks also gained in India, while equities traded mixed in Japan, China and much of Southeast Asia. South Korea’s Kospi climbed after better-than-expected results from Samsung Electronics.

“While oil prices remain elevated for now, there is a strong view that the conflict will come to an end within the next one to two weeks, with crude prices returning to prior levels,” said Hideyuki Ishiguro, chief strategist at Nomura Asset Management. “Geopolitical risks themselves have not been resolved, but VIX in Japan, US, and Europe have peaked, suggesting that markets may have largely priced in these risks,” he added.

In FX, the Bloomberg Dollar Spot Index rises by 0.1%, with Aussie dollar and sterling the outperformers and Swedish krona lagging after a surprise cooling in inflation.

In rates, treasury futures hold small losses after erasing gains amid rising oil prices, with yields across tenors slightly higher on the day. US 10-year yield is less than 1bp higher near 4.34%, and curve spreads are within a basis point of Monday’s closing levels. With European bond markets open for first time since Thursday, German and UK yields are 2bp-5bp cheaper across flatter curves. The US session includes the first of this week’s three Treasury coupon auctions, a 3-year note sale at 1pm. Treasury’s $58 billion 3-year new-issue auction, to be followed by $39 billion 10-year and $22 billion 30-year reopenings Wednesday and Thursday, has WI yield near 3.895%, about 32bp cheaper than last month’s, which tailed by 1.1bp, a notably poor result.

In commodities, WTI crude oil futures are up about 2% from Monday’s multiyear high close, which followed Trump’s threat to obliterate key Iranian infrastructure if an agreement to end the war isn’t reached by 8pm Tuesday. Gold prices up, though paring back from highs near $4,700/oz.

US event calendar, includes ADP weekly employment change (8:15am), February durable goods orders (8:30am), March New York Fed 1-year inflation expectations (11am) and February consumer credit (3pm). Fed speaker slate includes Williams (8:30am), Goolsbee (12:35pm, 1:45pm) and Jefferson (5:50pm)

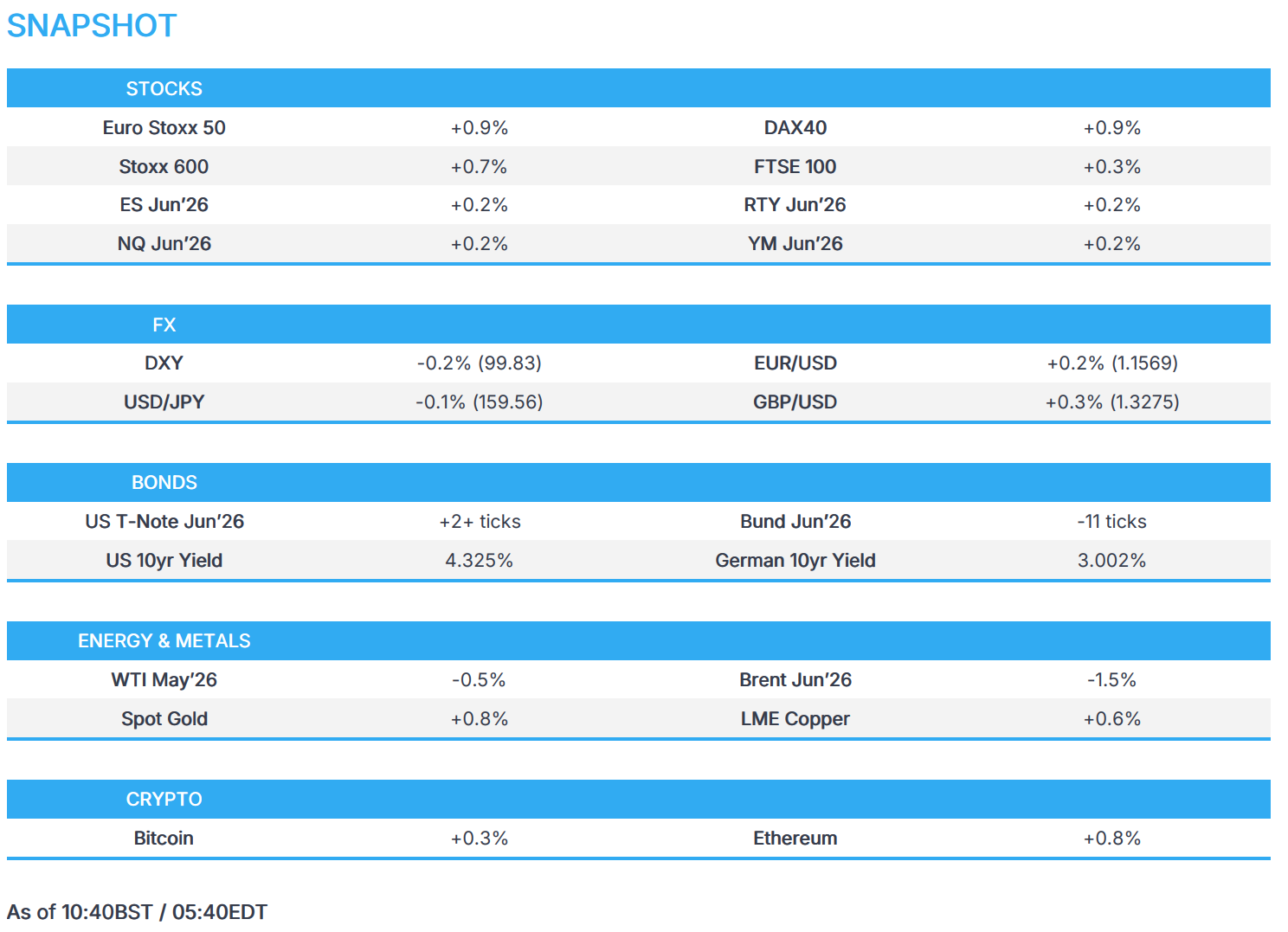

Market Snapshot

- S&P 500 mini -0.6%,

- Nasdaq 100 mini -0.7%,

- Russell 2000 mini -0.2%

- Stoxx Europe 600 +0.3%

- DAX +0.5%

- CAC 40 +1.0%

- 10-year Treasury yield +1 basis point at 4.34%

- VIX +0.3 points at 24.48

- Bloomberg Dollar Index -0.2% at 1211.85

- euro +0.3% at $1.1571

- WTI crude -0.4% at $111.97/barrel

Top Overnight News

- Negotiators are pessimistic Iran will bend to meet President Trump’s demand to reopen the Strait of Hormuz before his Tuesday-night deadline, paving the way for the U.S. to target Iranian bridges and power plants in a fresh escalation of the war. Twice in his second term, Trump set a deadline for a deal with Iran, said he would bomb the country if its leaders didn’t comply, then followed through with military operations. WSJ

- Airstrikes pounded Tehran on Tuesday, and Iranian officials urged young people to form human chains to protect power plants, hours before the expiration of U.S. President Donald Trump’s latest deadline for the Islamic Republic to reopen the crucial Strait of Hormuz or face punishing strikes on its infrastructure. AP

- Iran on Monday delivered a 10 point proposal to end the war with the US and Israel. The plan was conveyed by Pakistan, which has been acting as a primary intermediary, but appeared unlikely to resolve major questions ahead of Trump’s Tuesday evening deadline for new attacks on Iran. NYT

- A cross-party group of U.S. politicians have proposed a law to impose further restrictions on exports of computer chipmaking equipment to China, affecting companies such as ASML and China’s top chipmakers. RTRS

- Japan’s households reduced spending for a third straight month even after real wages turned positive. Outlays by households adjusted for inflation fell 1.8% in February from a year earlier, a faster decline compared with January’s 1% retreat. Real consumption remains weak, with economists citing growing consumer fatigue and inflation pressure as key challenges to domestic demand. BBG

- Taiwan’s opposition leader is set to arrive in China on Tuesday on what she has called a “historic journey for peace” as she hopes for a face-to-face meeting with Chinese leader Xi Jinping, the first such contact in a decade. FT

- Anthropic’s revenue run rate has topped $30 billion and the company confirmed partnerships with Broadcom and Google. BBG

- Cleveland Federal Reserve President Beth Hammack and Chicago Fed President Austan Goolsbee both see inflation as a far bigger problem than employment, underscoring their support for tighter rather than looser monetary policy as the Iran war puts upward pressure on energy prices and the job market remains stuck in low gear. RTRS

- Bill Ackman’s Pershing Square offered to buy Universal Music Group in a cash-and-stock deal at a 78% premium to Thursday’s closing price. Ackman cited UMG’s stock underperformance as a trigger for the bid. BBG

- Republicans are reportedly weighing how broadly to structure a party-line bill to fund President Trump’s immigration enforcement, with some senators seeking multi-year DHS funding and others favoring a narrower ICE and CBP measure: Semafor

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded cautiously following the positive lead from the US and with all focus remaining on geopolitics heading into US President Trump’s Tuesday evening deadline for Iran to open up the Strait of Hormuz or face the US destroying its power plants and bridges, although President Trump had also previously stated that he thinks talks are going well with Iran and they would like to be able to make a deal. ASX 200 rallied with tech and miners leading the upside and with almost all sectors in the green aside from industrials and consumer staples. Nikkei 225 failed to sustain its initial advances with the index pressured amid headwinds from higher oil prices and following disappointing Household Spending data. KOSPI surged at the open with strong gains in Samsung Electronics after its preliminary results topped forecasts and showed around an eight-fold jump in Q1 operating profit, although most of the advances were then pared as shares in the index heavyweight also pulled back. Shanghai Comp lacked conviction on return from the long weekend, with upside limited after another meek PBoC liquidity operation and with the Stock Connect still closed as Hong Kong markets remained shut.

Top Asian News

- Japanese Finance Minister Katayama said won’t comment on JGB yield levels and will refrain from commenting on levels in the markets, adds impact of Middle East and oil prices on the market is high.

- Chinese President Xi called for new energy system as war on Iran rocks global economy and said China needs to accelerate planning and construction of a new energy system to ensure the country’s energy security.

- South Korean FX Chief said are to deploy bold measures in the FX market, if needed.